Happy Holidays!

As we approach the end of the year, Basic and Beyond, our staff and instructors thank you all, for your support of our programs this year. We wish you all a wonderful holiday season and we look forward to serving you in 2020.

Our December Newsletter is filled with up to date information as well as some Tax Planning Ideas. Along with that, we have the recently released inflationary adjustment figures for 2020. This and other news can be utilized in forming your own end of year tax-planning newsletter. We serve a vast variety of practitioners who have an even greater number of varied clients. You, better than anyone, know your clients and the information they may need to plan for filing the 2019 return as well as planning the 2020 tax year. Take advantage of any information we have supplied from our February – December newsletters. Our newsletters this year have covered procedures, state information, IRS release of guidance, new tax law and so many other topics that will assist you and your client.

Due to providing the inflationary adjustments and other tax planning, the newsletter is especially long this month.

January 2020 – Mark Your Calendars for the 2020 Form W-4 class on January 14, 2020, and the Getting Ready for Filing Season update on January 15, 2020. More on this in the January Newsletter.

December 2019 Issue Headlines:

- Virtual Currency Becoming a Hot Issue with IRS

- IRS Issues Appeals Memo with Guidance on BBA Partnership Procedures

- Annual Enrollment Renewal Application Period for Enrolled Agents

- IOWA Filing Deadline for W-2s and 1099s is February 15, 2020.

- Pennsylvania Department of Revenue Sales and Use Tax Bulletin

- Some Year End Tax Planning that Is Still Available to Clients – Plan to Plan

- More Tax Planning as IRS Provided the Tax Inflation Adjustments for Tax Year 2020 on November 6, 2019, Tax Rates – for 2020

- Changes in Form 1065 for 2019

- IRS Issues Draft Instructions for 2019 Form 1041- Changes for 2019

- Deductions Allowable under § 67(e)

- New Addresses for Applications for Recognition of Tax Exempt Status

- Sanctioning from E-File – Good Time to Review this Process

- Are Your Stockpiling?

- TCJA Provisions for Eligible Terminated S Corporations

- Guidance to be Released by Year-End/January 2020

- How Do I Reach a Live Person on the 800-829-1040 IRS Assistance Number? PERSONAL Income Tax Refund

- Special IRS Efforts to Focus on Tax Compliance, Education

- Rul. 2019-26 – Applicable Federal Rates for December 2019

Issue 1: Virtual Currency Becoming a Hot Issue with IRS

The Office of Chief Counsel has issued Notice CC-2020-003 to identify procedures IRS attorneys are to follow when working and coordinating issues involving virtual currency, including digital assets, digital currency, crypto-assets, and cryptocurrency. These cases may involve information received from various third-party sources, such as information returns, and information received from a summons of a virtual currency exchange. They may involve a request for advice from the Service on Title 26 or Title 31 (Bank Secrecy Act) audits or cases in litigation.

In Notice 2014-21, the IRS concluded that, for Federal income tax purposes, virtual currency is treated as property. In that Notice, the IRS used the term “virtual currency” as a general term to mean a digital representation of value that functions as a medium of exchange, a unit of account, or a store of value. The IRS uses the term virtual currency broadly to include all digital representations of value not issued by a government that function as a medium of exchange, a unit of account, or a store of value. A unit of virtual currency may have an equivalent value in U.S. dollars or a foreign currency or may only be exchanged for other property or services. In light of the evolving technology and terminology concerning virtual currency, this Notice applies to all virtual currency existing now or created in the future, including digital assets, digital currency, crypto-assets, and cryptocurrency.

New Revenue Ruling 2019-24 and Notice 2014-21 are the only IRS guidance on virtual currency. If you have a client involved with this medium, a review of this information would be prudent. The October 2019 newsletter reviewed Rev. Rul. 2019-24.

Issue 2: IRS Issues Appeals Memo with Guidance on BBA Partnership Procedures – Control No. AP-08-1019-0013. Expiration Date: 10/18/2021. Affected IRM: 8.19 – In revision – memo serves as guidance until IRM revised.

Bipartisan Budget Act of 20151 – Appeals Procedures

The memorandum provides guidance on the Bipartisan Budget Act of 2015, on new case procedures for different phases of the BBA centralized partnership audit regime, including the following:

- Early Election into BBA.

- Administrative Adjustment Request (AAR).

- Notice of Proposed Partnership Adjustment (NOPPA).

- Modification Disputes; and,

- Notice of Final Partnership Adjustment (FPA).

- 1101 of the Bipartisan Budget Act of 2015 repealed TEFRA partnership procedures and electing large partnership provisions and replaced them with an entirely new centralized partnership audit regime.

Previously, tax, penalty, and interest adjustments were passed through to the partners. Now, the new partnership audit regime generally provides for determination of adjustments, assessment, and collection of tax attributable to such adjustments at the partnership level. This Interim Guidance supplements previously issued BBA guidance, AP-08-0319-0005.

Procedural Change:

- For tax years beginning after November 2, 2015, and before January 1, 2018, eligible partnerships may elect into BBA within 30 days of the date the IRS first notifies the partnership in writing that the return has been selected for examination. Either the Tax Matters Partner (TMP) or an individual authorized to sign the partnership return for the taxable year under examination is authorized to make the election by completing the Form 7036, Election under § 1101(g)(4) of the Bipartisan Budget Act of 2015. IRS examiner will issue Letter 5893, Notice of Administrative Proceeding, to the Partnership at least 30 days after a valid election is received by the IRS.

- After January 1, 2018, this election may also be made when filing an Administrative Adjustment Request (AAR) under § 6227 as amended by BBA for tax periods beginning after November 2, 2015 and before January 1, 2018.

- If an early election into BBA was requested or the entity is covered under BBA for tax years beginning on or after January 1, 2018, BBA cases will have Appeals rights.

- If there is a dispute on any BBA case, the examiner will issue a 30-day BBA letter (Letter 5891) with a summary report for the taxpayer to request an Appeals hearing. The dispute may cover the substantive audit issues, penalties and/or imputed underpayment adjustment groupings and subgroupings disputes.

- At the end of the Appeals process and issuance of the Notice of Proposed Partnership Adjustment (NOPPA) for all disputed tax issues (resolved and unresolved), Appeals will send the BBA case to Ogden BBA Unit for processing.

- In response to the NOPPA, the partnership may request modification. If there is a dispute regarding modification, the taxpayer will have an opportunity to appeal this dispute. Appeals will not reconsider an unagreed previous disputed tax issue if the entire case is later returned to Appeals for modification hearing.

- LB&I will issue the Notice of Final Partnership Adjustment (FPA) notice. The FPA allows the partnership to either request a push out the adjustments for its partners to take into account, petition for judicial review of the adjustments, or both. Under normal circumstances Appeals will not issue the FPA.

Affected IRMs: 8.19.14, 8.20.5, 8.20.6, and 8.20.7

This guidance will be incorporated into IRM 8.19 within two years from the date of this memorandum.

Issue 3: Annual Enrollment Renewal Application Period for Enrolled Agents

The 2020 Enrollment Renewal Application Period is open from November 1, 2019 through January 31, 2020. Per U.S. Treasury Department Circular 230, an Enrolled Agent is required to renew their EA status during this time frame if the SSN ends in 4, 5, or 6. Without renewal the current enrollment will expire on March 31, 2020.

Submit the enrollment renewal application and payment directly online through Pay.gov. To renew you must:

- Have an active preparer tax identification number (PTIN).

- Complete a minimum of 72 hours per enrollment cycle (every three years). Additionally, you must also obtain a minimum of 16 hours of CE (including 2 hours of ethics or professional conduct) each enrollment year. EXCEPTION: If this is your first renewal, you must complete 2 hours of CE for each month of your enrollment, including 2 hours of ethics, or professional conduct each year.

- Pay the $67 non-refundable renewal fee. This fee applies regardless of the enrollment status. Use these tips to ensure the application is processed as quickly as possible:

- Do not submit the application prior to November 1, 2019.

- Fill in the CE table in Part 1 completely.

- Sign, and date the form in Part 3.

Please allow 90 days for processing before calling 855-472-5540 to check on the status of the application.

Terminate/Inactivate EAs Who Haven’t Renewed

The Internal Revenue Service sent letters to EAs whose enrollment status was terminated or inactivated because of failure to renew. Termination letters went out in late July, while inactive letters went out mid-August 2019.

The IRS has also reissued Forms:

Form 23, Application for Enrollment to Practice Before the Internal Revenue Service (rev. 11/2019)

These are two forms that must be submitted by tax professionals who want to practice before the IRS as enrolled agents (EAs).

Form 23 is filed by first-time applicants who are eligible to be enrolled as EAs and who have not previously practiced before the IRS. The form notes that prior to submitting the form, applicants must pass the Special Enrollment Examination (SEE) and obtain a Preparer Tax Identification Number (PTIN).

It adds that for former IRS employees, the eligibility to practice may be limited by the applicant’s work experience.

Form 8554 is used to renew status as an EA with either “active” status or “inactive retirement” status. All agents who wish to renew their enrollment must have an active PTIN, and complete 72 hours of continuing education credit (less if the agent is renewing for the first time).

Both forms have a $67 application fee. Both forms and applicable payments may be submitted electronically at www.pay.gov.

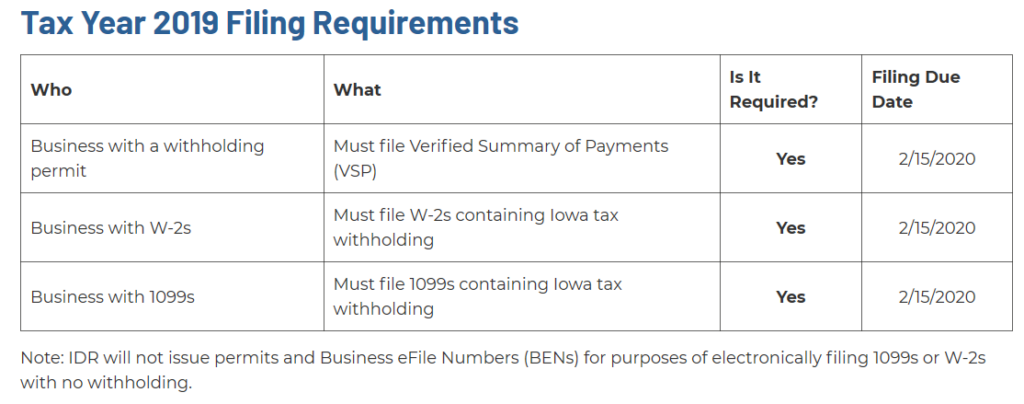

Issue 4: IOWA Filing Deadline for W-2s and 1099s is February 15, 2020.

Businesses that issued W-2s or 1099s that contain Iowa withholding must electronically file those documents with the Iowa Department of Revenue. This data is an essential tool the Department uses to increase the accuracy of tax refunds and detect tax refund fraud during the current income tax filing season.

New this year: W-2 Key & Send

Business owners now have the option to manually enter their W-2 information in eFile & Pay.

https://tax.iowa.gov/w-2-1099-software-vendor-list

Issue 5: Pennsylvania Department of Revenue Sales and Use Tax Bulletin – SALES AND USE TAX BULLETIN 2019-01 Issued: January 8, 2019 Revised: January 11, 2019. Effective July 1, 2019 – Maintaining a Place of Business in the Commonwealth

The Department of Revenue issued this bulletin to clarify when marketplace and remote sellers, marketplace facilitators, and all other vendors maintain a place of business in the Commonwealth, after the June 21, 2018, Supreme Court of the United States opinion in South Dakota v. Wayfair, Inc. The decision upheld South Dakota’s economic nexus statute and overturned its previous decision in Quill Corp. v. North Dakota, 504 U.S. 298 (1992), which required a business to have a physical presence in a state in order for it to be required to collect that state’s sales tax. The decision in Wayfair, read in conjunction with the Tax Reform Code, creates an economic nexus for certain sellers of products in the Commonwealth, where previously, nexus existed only for those with a physical presence.

South Dakota’s statute, enacted in 2016, required out-of-state vendors who sold more than $100,000 worth of property to South Dakota’s residents in the past year, or in more than 200 separate transactions, to begin to collect South Dakota’s sales tax on future sales into the state. The statute applied prospectively only, and South Dakota previously had adopted the Streamlined Sales and Use Tax Agreement. The Agreement system standardizes taxes, including a single, state level tax, uniform definitions, simplified tax rates, and the availability of free tax administration software. Users of the state supplied software are immune from select audit liability.

In its decision, the Supreme Court concluded that its earlier decision in Quill was incorrect; a physical presence nexus rule is not required by the Constitution’s Commerce Clause. As long as a vendor has a substantial nexus with a taxing state and the tax does not create an undue burden to that vendor, a virtual presence is sufficient to require the vendor to collect sales tax.

Although choosing not to resolve the undue burden issue in its decision, the Court did address those specific portions of South Dakota’s Act that it found to satisfactorily prevent discrimination. These included the safe harbor for those vendors who have limited business within South Dakota (less than $100,000 of sales or 200 transactions per year); no retroactive application; and the uniform rules and administration of the tax afforded by the Streamlined Agreement and corresponding software

The Tax Reform Code requires every person maintaining a place of business in the Commonwealth to sell tangible personal property, or perform taxable services, to be licensed to, and collect, sales tax from its customers. The Code defines “maintaining a place of business in this Commonwealth” to include “having any contact within this Commonwealth which would allow the Commonwealth to require a person to collect and remit tax under the Constitution of the United States.”

Upon careful review of the Supreme Court’s decision in Wayfair that a physical presence was not required by the United States Constitution, and that an economic nexus, such as that prescribed by the South Dakota Act, is sufficient, the Department provides this guidance that a substantial economic nexus satisfies the Tax Reform Code’s definition of maintaining a place of business, requiring a person to collect and remit Pennsylvania’s sales tax.

Pennsylvania currently has only one state sales tax rate that applies across the Commonwealth.

To prevent any discrimination or undue burden on taxpayers whose virtual presence with the Commonwealth is limited:

- Pennsylvania’s economic nexus applies only to those persons who, in the previous twelve months, made more than $100,000 of gross sales into the Commonwealth.

- A marketplace facilitator with no physical presence in Pennsylvania should use both facilitated and direct sales to determine whether it has exceeded the economic nexus threshold.

- A marketplace seller with no physical presence in Pennsylvania should use only its direct sales and those sales made through a marketplace facilitator that does not collect sales tax on its behalf, to determine whether it has exceeded the economic nexus threshold.

- The Department will certify service providers that will offer software and perform services that when relied upon by a vendor to determine whether or not the sale of a particular product or provision of a particular service is subject to sales tax, will relieve the vendor of liability upon audit.

- The certified service provider also will aid in the registration, collection, reporting, and remittance of sales tax.

The economic nexus rules do not replace or provide an alternative to the provisions of Act 43. The provisions of Act 43 remain valid law applicable to those vendors who have neither a physical presence nexus nor an economic nexus in Pennsylvania. However, for those marketplace facilitators and remote sellers who were required by Act 43 to elect to either collect and remit sales tax or give notice to customers and report to the Department, but now have an economic nexus in Pennsylvania, the Act 43 election no longer is available. Marketplace facilitators and sellers who made over $100,000 in Pennsylvania sales now will be required to register for a license and collect, report, and remit sales tax on sales into the Commonwealth. Additionally, if a marketplace facilitator has economic nexus in Pennsylvania, it now will be required to collect the sales tax on all sales into the Commonwealth, even if the sale is on behalf of a marketplace seller that does not individually have any nexus.

The provisions of this Bulletin shall apply to transactions that occur on or after July 1, 2019 and do not affect marketplace sellers for whom marketplace facilitators collect and remit on their behalf.

Issue 6: Some Year End Tax Planning that Is Still Available to Clients – Plan to Plan

As we approach the new year, there is still one month to take advantage of some tax options to reduce tax.

- Max out on that retirement plan, when possible.

- If the client has stock losses that have occurred or a carryover of a capital loss, it is time to look at the portfolio. Was there something the client has been considering selling but the large capital gain is concerning? Use those stock losses to offset capital gains.

- Or defer those capital gains by investing in an opportunity zone fund.

- Fund a 529 education savings plan. (State Savings Only)

- Give to a favorite charity or make a Qualified Charitable Distribution if the client is 70 1/2.

- Does the client have enough withholding to cover the tax bill? Time to review and make sure they made those estimated payments recommended or maybe those payments need to be adjusted.

- The client should consider large purchases before many state taxes on internet purchases are effective. In addition, evaluate the issue of a Business decision vs. a Tax decision – is the purchase really needed or is it purchased to generate a tax benefit. Sometime a tax benefit will occur but if the assets is bought just for that purpose – it may not be a good business decision.

- Do not forget about potential state tax credits which could benefit the client or the client’s business.

- Has the client taken their required minimum distributions?

- Check the flexible spending accounts is there dollars to be spent?

- Does a Health Savings Account work for the client?

- Does the client have a will and an estate plan in place?

- Does business succession planning need to be a topic of discussion?

- These and more may save your client tax dollars, just by discussing the issues.

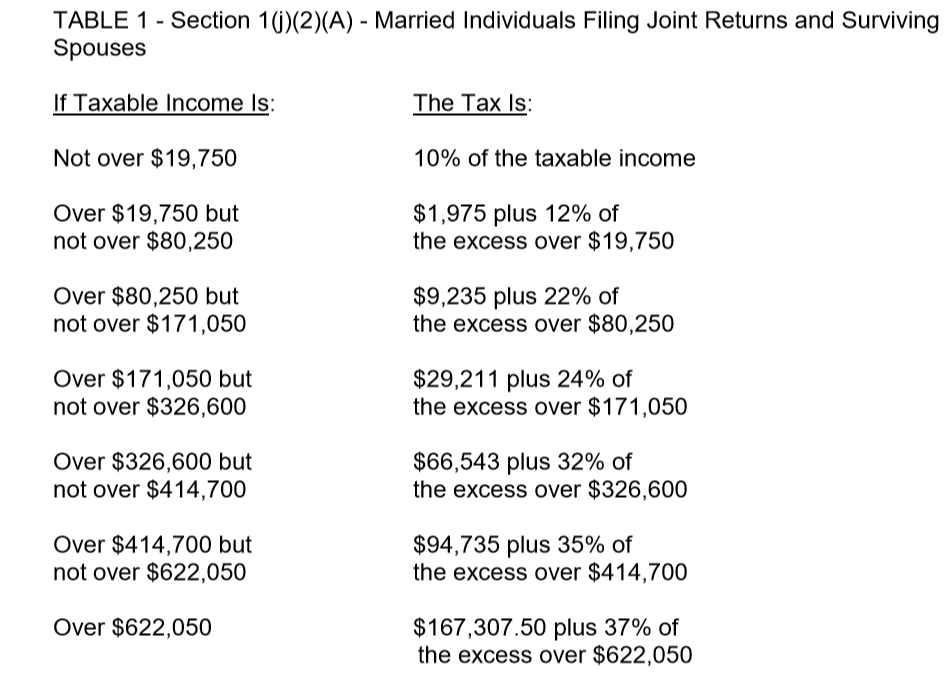

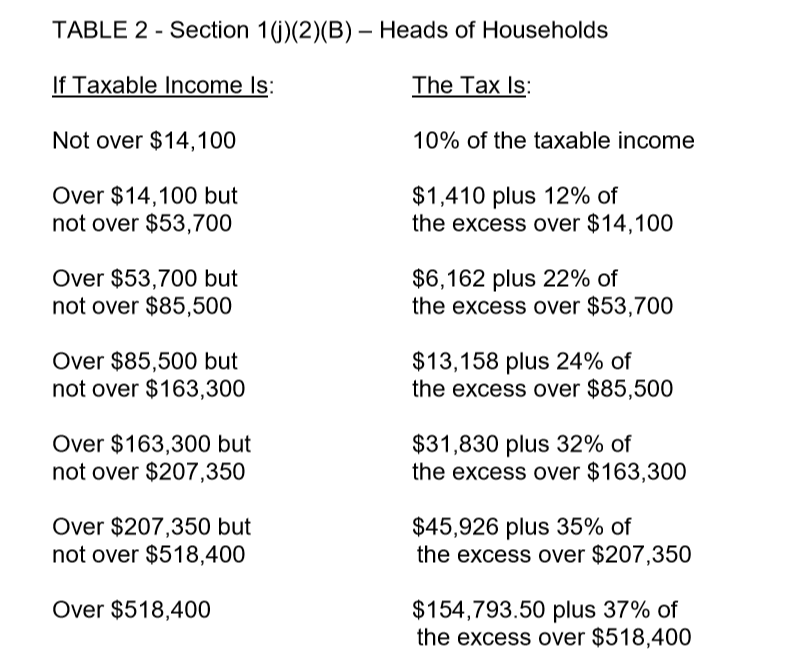

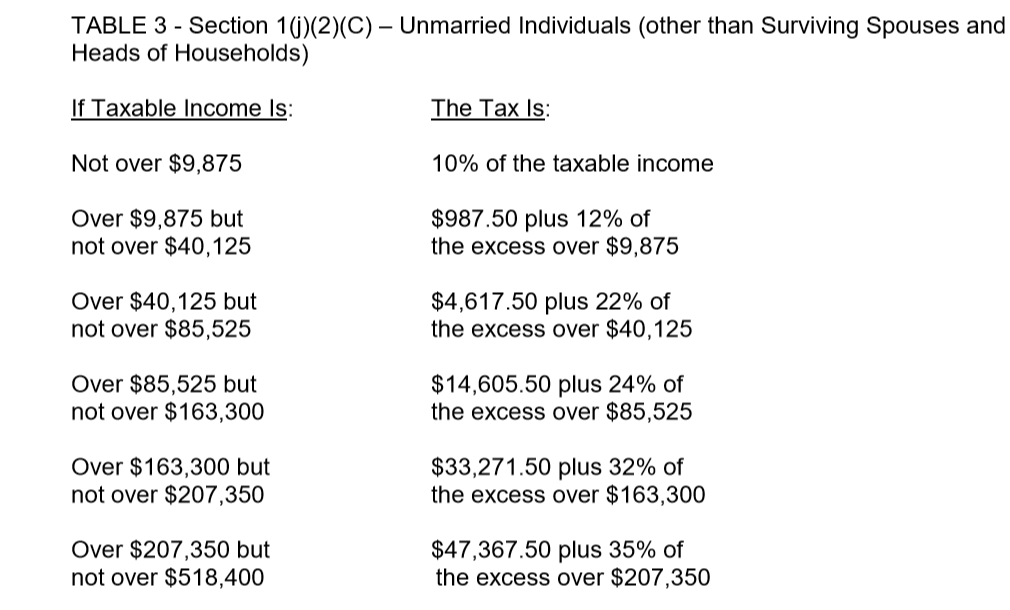

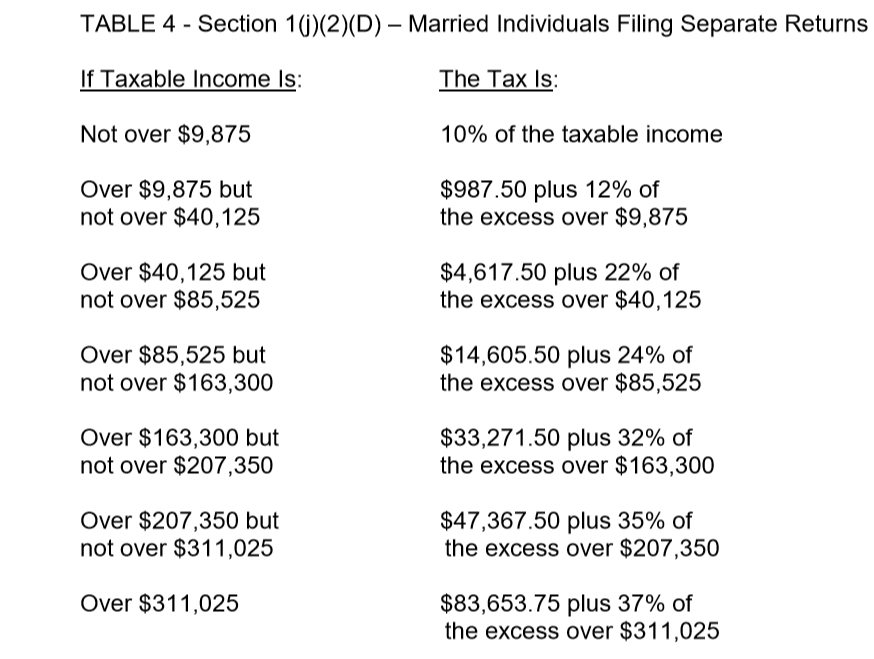

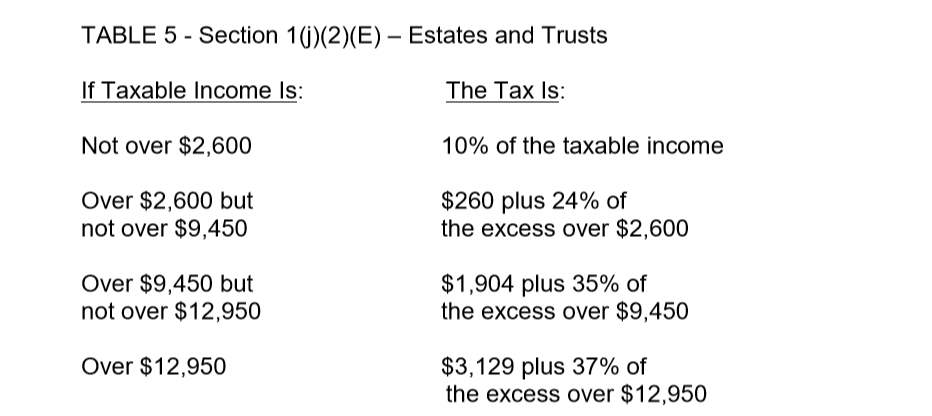

Issue 7: More Tax Planning as IRS Provided the Tax Inflation Adjustments for Tax Year 2020 on November 6, 2019

Tax Rates – for 2020

Unearned Income of Minor Children (the “Kiddie Tax”) for 2020

Unearned Income of Minor Children (the “Kiddie Tax”) for 2020

For taxable years beginning in 2020, the amount in § 1(g)(4)(A)(ii)(I), which is used to reduce the net unearned income reported on the child’s return that is subject to the “kiddie tax,” is $1,100. This $1,100 amount is the same as the amount provided in § 63(c)(5)(A), as adjusted for inflation. The same $1,100 amount is used for purposes of § 1(g)(7) (that is, to determine whether a parent may elect to include a child’s gross income in the parent’s gross income and to calculate the “kiddie tax”).

Maximum Capital Gains Rate for 2020

For taxable years beginning in 2020, the Maximum Zero Rate Amount under § 1(h)(1)(B)(i) is:

- $80,000 in the case of a joint return or surviving spouse

- $40,000 in the case of a married individual filing a separate return,

- $53,600 in the case of an individual who is a head of household (§ 2(b)),

- $40,000 in the case of any other individual (other than an estate or trust), and

- $2,650 in the case of an estate or trust.

The Maximum 15-percent Rate Amount under § 1(h)(1)(C)(ii)(l) is:

- $496,600 in the case of a joint return or surviving spouse,

- $248,300 in the case of a married individual filing a separate return,

- $469,050 in the case of an individual who is the head of a household (§ 2(b)),

- $441,450 in the case of any other individual (other than an estate or trust), and

- $13,150 in the case of an estate or trust.

Adoption Credit for 2020

For taxable years beginning in 2020, under § 23(a)(3) the credit allowed for an adoption of a child with special needs is $14,300. For taxable years beginning in 2020, under § 23(b)(1) the maximum credit allowed for other adoptions is the amount of qualified adoption expenses up to $14,300. The available adoption credit begins to phase out under § 23(b)(2)(A) for taxpayers with modified adjusted gross income in excess of $214,520 and is completely phased out for taxpayers with modified adjusted gross income of $254,520 or more.

Adoptions Assistance Programs 2020

The amount that can be excluded from an employee’s gross income for the adoption of a child with special needs is $14,300 and the maximum amount that can be excluded from an employee’s gross income for the amounts paid or expenses incurred by an employer for qualified adoption expenses furnished pursuant to an adoption assistance program for other adoptions by the employee is $14,300.

Child Tax Credit

For taxable years beginning in 2020, the value used in § 24(d)(1)(A) to determine the amount of credit under § 24 that may be refundable is $1,400.

Lifetime Learning Credit

For taxable years beginning in 2020, a taxpayer’s modified adjusted gross income in excess of $59,000 ($118,000 for a joint return) is used to determine the reduction under § 25A(d)(2) in the amount of the Lifetime Learning Credit otherwise allowable under § 25A(a)(2).

Earned Income Credit for 2020

Number of Children

| Item | One | Two | Three or More | None |

| Earned Income Amount | $10,540 | $14,800 | $14,800 | $7,030 |

| Maximum Amount of Credit | $3,584 | $5,920 | $6,660 | $538 |

| Threshold Phaseout Amount (Single, Surviving Spouse, or Head of Household) | $19,330 | $19,330 | $19,330 | $8,790 |

| Completed Phaseout Amount (Single, Surviving Spouse, or Head of Household) | $41,756 | $47,440 | $50,954 | $15,820 |

| Threshold Phaseout Amount (Married Filing Jointly) | $25,220 | $25,220 | $25,220 | $14,680 |

| Completed Phaseout Amount (Married Filing Jointly) | $47,646 | $53,330 | $56,844 | $21,710 |

Excessive Investment Income for 2020

- The earned income tax credit is not allowed under § 32(i) if the aggregate amount of certain investment income exceeds $3,650.

Employee Health Insurance Expense of Small Employers in 2020

- The dollar amount in effect under § 45R(d)(3)(B) is $27,600.

Exemption Amounts for Alternative Minimum Tax in 2020

The exemption amounts under § 55(d)(1) are:

Joint Returns or Surviving Spouses |

$113,400 |

Unmarried Individuals (other than Surviving Spouses) |

$72,900 |

Married Individuals Filing Separate Returns |

$56,700 |

Estates and Trusts |

$25,400 |

For taxable years beginning in 2020, under § 55(b)(1), the excess taxable income above which the 28 % tax rate applies is:

Married Individuals Filing Separate Returns |

$98,950 |

Joint Returns, Unmarried Individuals (other than surviving spouses), and Estates and Trusts |

$197,900 |

For taxable years beginning in 2020, the amounts used under § 55(d)(2) to determine the phaseout of the exemption amounts are:

Joint Returns or Surviving Spouses |

$1,036,800 |

Unmarried Individuals (other than Surviving Spouses) |

$518,400 |

Married Individuals Filing Separate Returns |

$518,400 |

Estates and Trusts |

$84,800 |

Alternative Minimum Tax Exemption for a Child Subject to the “Kiddie Tax for 2020

- For a child to whom the § 1(g) “kiddie tax” applies, the exemption amount under §§ 55(d) and 59(j) for purposes of the alternative minimum tax under § 55 may not exceed the sum of (1) the child’s earned income for the taxable year, plus (2) $7,900.

Certain Expenses of Elementary and Secondary School Teachers for 2020

- The amount for an educator remains at $250.

Standard Deduction for 2020

Filing Status |

Standard Deduction |

Married Individuals Filing Joint Returns and Surviving Spouses (§ 1(j)(2)(A)) |

$24,800 |

Heads of Households (§ 1(j)(2)(B)) |

$18,650 |

Unmarried Individuals (other than Surviving Spouses and Heads of Households) (§ 1(j)(2)(C)) |

$12,400 |

Married Individuals Filing Separate Returns (§ 1(j)(2)(D)) |

$12,400 |

Dependent Standard Deduction for 2020

The standard deduction amount for an individual who may be claimed as a dependent by another taxpayer cannot exceed the greater of (1) $1,100, or (2) the sum of $350 and the individual’s earned income.

Aged or Blind Additional Standard Deduction for 2020

The additional standard deduction amount for the aged or the blind is $1,300. The additional standard deduction amount is increased to $1,650 if the individual is also unmarried and not a surviving spouse.

Cafeteria Plans for 2020

- The dollar limitation on voluntary employee salary reductions for contributions to health flexible spending arrangements is $2,750.

Qualified Transportation Fringe Benefit for 2020

- The monthly limitation regarding the aggregate fringe benefit exclusion amount for transportation in a commuter highway vehicle and any transit pass is $270. The monthly limitation regarding the fringe benefit exclusion amount for qualified parking is $270.

Income from United States Savings Bonds for Taxpayers Who Pay Qualified Higher Education Expenses for 2020

- The exclusion regarding income from United States savings bonds for taxpayers who pay qualified higher education expenses, begins to phase out for modified adjusted gross income above $123,550 for joint returns and $82,350 for all other returns. The exclusion is completely phased out for modified adjusted gross income of $153,550 or more for joint returns and $97,350 or more for all other returns.

Gross Income Limitation for a Qualifying Relative for 2020

- The exemption amount is $4,300.

Election to Expense Certain Depreciable Assets in 2020

- The aggregate cost of any § 179 property that a taxpayer elects to treat as an expense cannot exceed $1,040,000 and, the cost of any sport utility vehicle that may be taken into account under § 179 cannot exceed $25,900. The $2,590,000 limitation is reduced (but not below zero) by the amount the cost of § 179 property placed in service during the 2020 taxable year exceeds $2,590,000.

Qualified Business Income Thresholds for 2020

- $326,600 for married filing joint returns.

- $163,300 for married filing separate returns, and

- $163,300 for all other returns.

Eligible Long-Term Care Premiums for 2020

The limitations regarding eligible long-term care premiums included in the term “medical care,” are as follows:

Attained Age Before the Close of the Taxable Year |

Limitation on Premiums |

40 or less |

$430 |

More than 40 but not more than 50 |

$810 |

More than 50 but not more than 60 |

$1,630 |

More than 60 but not more than 70 |

$4,350 |

More than 70 |

$5,430 |

Medical Savings Accounts

(1) Self-only coverage

For taxable years beginning in 2020, the term “high deductible health plan” as defined in § 220(c)(2)(A) means, for self-only coverage, a health plan that has an annual deductible that is not less than $2,350 and not more than $3,550, and under which the annual out-of-pocket expenses required to be paid (other than for premiums) for covered benefits do not exceed $4,750.

(2) Family coverage

For taxable years beginning in 2020, the term “high deductible health plan” means, for family coverage, a health plan that has an annual deductible that is not less than $4,750 and not more than $7,100, and under which the annual out-of-pocket expenses required to be paid (other than for premiums) for covered benefits do not exceed $8,650.

Interest on Education Loans

For taxable years beginning in 2020, the $2,500 maximum deduction for interest paid on qualified education loans under § 221 begins to phase out under § 221(b)(2)(B) for taxpayers with modified adjusted gross income in excess of $70,000 ($140,000 for joint returns), and is completely phased out for taxpayers with modified adjusted gross income of $85,000 or more ($170,000 or more for joint returns).

Limitation on Use of Cash Method of Accounting

For taxable years beginning in 2020, a corporation or partnership meets the gross receipts test of § 448(c) for any taxable year if the average annual gross receipts of such entity for the 3-taxable-year period ending with the taxable year which precedes such taxable year does not exceed $26,000,000.

Threshold for Excess Business Loss

For taxable years beginning in 2020, in determining a taxpayer’s excess business loss, the amount under § 461(l)(3)(A)(ii)(II) is $259,000 ($518,000 for joint returns).

Foreign Earned Income Exclusion

For taxable years beginning in 2020, the foreign earned income exclusion amount under § 911(b)(2)(D)(i) is $107,600.

Valuation of Qualified Real Property in Decedent’s Gross Estate

For an estate of a decedent dying in calendar year 2020, if the executor elects to use the special use valuation method under § 2032A for qualified real property, the aggregate decrease in the value of qualified real property resulting from electing to use § 2032A for purposes of the estate tax cannot exceed $1,180,000.

Annual Exclusion for Gifts

(1) For calendar year 2020, the first $15,000 of gifts to any person (other than gifts of future interests in property) are not included in the total amount of taxable gifts under § 2503 made during that year.

(2) For calendar year 2020, the first $157,000 of gifts to a spouse who is not a citizen of the United States (other than gifts of future interests in property) are not included in the total amount of taxable gifts under §§ 2503 and 2523(i)(2) made during that year.

Notice of Large Gifts Received from Foreign Persons

For taxable years beginning in 2020, § 6039F authorizes the Treasury Department and the Internal Revenue Service to require recipients of gifts from certain foreign persons to report these gifts if the aggregate value of gifts received in the taxable year exceeds $16,649.

Persons Against Whom a Federal Tax Lien Is Not Valid

For calendar year 2020, a federal tax lien is not valid against (1) certain purchasers under § 6323(b)(4) who purchased personal property in a casual sale for less than $1,620, or (2) a mechanic’s lien or under § 6323(b)(7) who repaired or improved certain residential property if the contract price with the owner is not more than $8,100.

Property Exempt from Levy

For calendar year 2020, the value of property exempt from levy under § 6334(a)(2) (fuel, provisions, furniture, and other household personal effects, as well as arms for personal use, livestock, and poultry) cannot exceed $9,690. The value of property exempt from levy under § 6334(a)(3) (books and tools necessary for the trade, business, or profession of the taxpayer) cannot exceed $4,850.

Exempt Amount of Wages, Salary, or Other Income

For taxable years beginning in 2020, the dollar amount used to calculate the amount determined under § 6334(d)(4)(B) is $4,300.

Interest on a Certain Portion of the Estate Tax Payable in Installments

For an estate of a decedent dying in calendar year 2020, the dollar amount used to determine the “2-percent portion” (for purposes of calculating interest under § 6601(j)) of the estate tax extended as provided in § 6166 is $1,570,000.

Failure to File Tax Return

In the case of any return required to be filed in 2021, the amount of the addition to tax under § 6651(a) for failure to file a tax return within 60 days of the due date of such return (determined with regard to any extensions of time for filing) shall not be less than the lesser of $330 or 100 percent of the amount required to be shown as tax on such returns

Failure to File Partnership Return

In the case of any return required to be filed in 2021, the dollar amount used to determine the amount of the penalty under § 6698(b)(1) is $210. .56 Failure to File S Corporation Return. In the case of any return required to be filed in 2021, the dollar amount used to determine the amount of the penalty under § 6699(b)(1) is $210.

Revocation or Denial of Passport in Case of Certain Tax Delinquencies

For calendar year 2020, the amount of a serious delinquent tax debt under § 7345 is $53,000.

Attorney Fee Awards

For fees incurred in calendar year 2020, the attorney fee award limitation under § 7430(c)(1)(B)(iii) is $210 per hour.

Periodic Payments Received Under Qualified Long-Term Care Insurance Contracts or Under Certain Life Insurance Contracts

For calendar year 2020, the stated dollar amount of the per diem limitation under § 7702B(d)(4), regarding periodic payments received under a qualified long-term care insurance contract or periodic payments received under a life insurance contract that are treated as paid by reason of the death of a chronically ill individual, is $380.

Qualified Small Employer Health Reimbursement Arrangement

For taxable years beginning in 2020, to qualify as a qualified small employer health reimbursement arrangement under § 9831(d), the arrangement must provide that the total amount of payments and reimbursements for any year cannot exceed $5,250 ($10,600 for family coverage).

Refundable Credit for Coverage Under a Qualified Health Plan

For taxable years beginning in 2020, the limitation on tax imposed under § 36B(f)(2)(B) for excess advance credit payments is determined using the following table:

If the household income – expressed as a percent of the poverty line – is- |

The limitation amount for unmarried individuals – other than a surviving spouse or head of household – is: |

The limitation amount for all other taxpayers is: |

Less than 200% |

$325 |

$650 |

At least 200% but less than 300% |

$800 |

$1,600 |

At least 300% but less than 400% |

$1,350 |

$2,700 |

The contribution limit for employees who participate in 401(k), 403(b), most 457 plans, and the federal government’s Thrift Savings Plan is increased from $19,000 to $19,500.

The catch-up contribution limit for employees aged 50 and over who participate in these plans is increased from $6,000 to $6,500.

The limitation regarding SIMPLE retirement accounts for 2020 is increased to $13,500, up from $13,000 for 2019.

The income ranges for determining eligibility to make deductible contributions to traditional Individual Retirement Arrangements (IRAs), to contribute to Roth IRAs and to claim the Saver’s Credit all increased for 2020.

Taxpayers can deduct contributions to a traditional IRA if they meet certain conditions. If during the year either the taxpayer or his or her spouse was covered by a retirement plan at work, the deduction may be reduced, or phased out, until it is eliminated, depending on filing status and income. (If neither the taxpayer nor his or her spouse is covered by a retirement plan at work, the phase-outs of the deduction do not apply.) Here are the phase-out ranges for 2020:

- For single taxpayers covered by a workplace retirement plan, the phase-out range is $65,000 to $75,000, up from $64,000 to $74,000.

- For married couples filing jointly, where the spouse making the IRA contribution is covered by a workplace retirement plan, the phase-out range is $104,000 to $124,000, up from $103,000 to $123,000.

- For an IRA contributor who is not covered by a workplace retirement plan and is married to someone who is covered, the deduction is phased out if the couple’s income is between $196,000 and $206,000, up from $193,000 and $203,000.

- For a married individual filing a separate return who is covered by a workplace retirement plan, the phase-out range is not subject to an annual cost-of-living adjustment and remains $0 to $10,000.

The income phase-out range for taxpayers making contributions to a Roth IRA is $124,000 to $139,000 for singles and heads of household, up from $122,000 to $137,000. For married couples filing jointly, the income phase-out range is $196,000 to $206,000, up from $193,000 to $203,000. The phase-out range for a married individual filing a separate return who makes contributions to a Roth IRA is not subject to an annual cost-of-living adjustment and remains $0 to $10,000.

The income limit for the Saver’s Credit (also known as the Retirement Savings Contributions Credit) for low- and moderate-income workers is $65,000 for married couples filing jointly, up from $64,000; $48,750 for heads of household, up from $48,000; and $32,500 for singles and married individuals filing separately, up from $32,000.

Key limit remains unchanged

The limit on annual contributions to an IRA remains unchanged at $6,000. The additional catch-up contribution limit for individuals aged 50 and over is not subject to an annual cost-of-living adjustment and remains $1,000.

Issue 8: Changes in Form 1065 for 2019

New Question 27 has been added to Schedule B to enter the number of foreign partners that transferred all or part of their interests or received a distribution subject to § 864(c)(8).

New Question 28 regarding disclosures for disguised sales has been added to Schedule B.

Schedule K and Schedule K-1, line 4, Guaranteed payments, now has three lines:

- Guaranteed payments for services,

- Guaranteed payments for capital, and

- Total.

Schedule K, lines 16(d) and (k), are reserved for future use because § 951A categories are no longer reported on Schedules K and K-1.

Schedule K-1

- Item E—A parenthetical has been added to caution against using the TIN of a disregarded entity.

- Item H—Has been revised to request the name and TIN of a disregarded entity, if applicable.

- Item J – A new checkbox has been added to indicate the sale of a partnership interest.

- Item K – A new checkbox has been added to indicate whether liabilities shown in Item K include liabilities from lower-tier partnerships.

- Item L – Partner’s capital accounts are now reported only on the tax basis method and checkboxes to indicate other methods have been removed.

- Item N – A new item has been added for partners share of unrecognized § 704(c) gain or (loss) at the beginning and the end of the year.

- Box 11 – Code F will no longer be used for §951A income. Instead, it will now be used for any net positive income from §743(b) adjustments.

- Box 13 – New code V has been added for any negative income effect from § 743(b) adjustments.

- Box 20—Codes Z through AD that were previously used to report § 199A information have been changed. Only code Z will be used to report § 199A information.

Box 20—Code AA is used for the net income/loss effect for all section 704(c) adjustments.

Box 20—Code AB is used for § 751 gain or loss from the sale of a partnership interest.

Box 20—Code AC is used for any deemed gain or loss from §1(h)(5) collectibles from the sale of a partnership interest.

Box 20—Code AD is used for any deemed gain under § 1250 from the sale of a partnership interest.

Box 20—Code AH, Other, includes net § 743(b) adjustment for partners with basis adjustments.

Lines 21 and 22—These new lines have checkboxes to indicate that there are attachments to the Schedule K-1 related to the partnership having more than one activity for § 465 at-risk purposes, or more than one activity for § 469 passive activity purposes, or both.

The draft instructions point out that at the time the instructions went to print, several credits and deductions available to partnerships expired prior to 2019.

Issue: 9: IRS Issues Draft Instructions for 2019 Form 1041- Changes for 2019

- Line 20—Qualified Business Income Deduction. A line has been added to the draft Form 1041 to be used when reporting the deduction attributable to the entity’s share of qualified items. The Schedules K and K-1, Box 14, code I, related to the qualified business income deduction, has been changed. New pass-through entity reporting statements have been included in the instructions to assist the trust or estate in reporting the proper qualified business income items and other information to its beneficiaries. These statements, or substantially similar statements, must be attached to each beneficiary’s Schedule K-1 reporting their pro rata share of each item and other information as applicable.

- Schedule G (Tax Computation). This schedule now has two parts: Part I—Tax Computation, and Part II—Payments.

- Other Information. The Other Information questions on Form 1041 have been updated to include new questions 11 through 14. Questions 11 and 12 relate to estates and trusts that hold S corporation stock. Questions 13 and 14 relate to electing small business trusts (ESBTs).

- ESBT Worksheet. An ESBT Tax Worksheet has been added to the instructions to calculate the ESBT tax.

- Qualified Opportunity Investment. A qualified investment in a qualified opportunity fund (QOF) must be reported on Form 1041 with Form 8997, Initial and Annual Statement of Qualified Opportunity Fund Investments, attached. See the Form 8997 instructions.

- Capital gains and qualified dividends. For tax year 2019, the 20% maximum capital gains rate applies to estates and trusts with income above $12,950.

-

- The 0% and 15% rates apply to certain threshold amounts.

- The 0% rate applies to amounts up to $2,650.

- The 15% rate applies to amounts over $2,650 and up to $12,950.

- Bankruptcy estate filing threshold. For tax year 2019, the requirement to file a return for a bankruptcy estate applies only if gross income is at least $12,200.

- Qualified disability trust. For tax year 2019, a qualified disability trust can claim an exemption of up to $4,200. This amount is not subject to phaseout.

Issue 10: Deductions Allowable under § 67(e)

This is is often missed since Miscellaneous Itemized Deductions have been suspended.

Miscellaneous itemized deductions subject to the 2% floor aren’t deductible for tax years 2018 through 2025. However, deductions under § 67(e)(1) continue to be deductible if they are costs that are incurred in connection with the administration of an estate or a non-grantor trust that would not have been incurred if the property were not held in such estate or trust. Review Notice 2018-61 for more information. Also see Regulations § 1.67-4 for costs that are commonly or customarily incurred by an individual.

Issue 11: New Addresses for Applications for Recognition of Tax Exempt Status

The addresses for applications requesting recognition of exempt status have changed.

The new addresses apply to Forms 1023, 1024, 1024-A, 1028, 8940, and 8718.

The new mailing address is as follows.

Internal Revenue Service

TE/GE Stop 31A Team 105

P.O. Box 12192

Covington, KY 41012-0192

For submissions sent by private delivery service, the new address is as follows.

Internal Revenue Service

7940 Kentucky Drive

TE/GE Stop 31A Team 105

Florence, KY 41042

Issue 12: Sanctioning from E-File – Good Time to Review this Process

Violations of IRS e-file requirements may result in warning or sanctioning Principals, Responsible Officials and the Provider. The IRS may sanction any Provider when the firm or any of its Principals or Responsible Officials fails to comply with any requirement or any provision. The IRS may also sanction for the same reasons that it denies an application to participate in IRS e-file. Before sanctioning, the IRS may issue a warning letter that describes specific corrective action the Provider must take. The IRS may also sanction without issuance of a warning letter.

Sanctioning may be a written reprimand, suspension or expulsion from participation from IRS e-file, or other sanctions, depending on the seriousness of the infraction. The IRS categorizes the seriousness of infractions as Level One, Level Two and Level Three. The firm, Principal or Responsible Official may appeal sanctions through the Administrative Review Process. Suspended Providers and individuals are usually ineligible to participate in IRS e-file for a period of either one or two years from the effective date of the sanction, but they may reapply after resolution of suitability issues. Individuals of firms expelled from participation may be eligible for reconsideration after a five-year waiting period.

In most circumstances, a sanction is effective 30 days after the date of the letter informing of the sanction or the date the reviewing offices or the Office of Appeals affirms the sanction, whichever is later. In certain circumstances, the IRS can immediately suspend or expel a Provider, Principal or Responsible Official without warning or notice. If a firm, Principal or Responsible Official is suspended or expelled from participation in IRS e-file, every related entity, including those that listed the suspended or expelled Principal or Responsible Official on its IRS e-file Application, may also be suspended or expelled.

Levels of Infraction

Level One Infractions – Level One Infractions are violations of IRS e-file rules and requirements that, in the opinion of the IRS, have little or no adverse impact on the quality of electronically filed returns or on IRS e-file. The IRS may issue a written reprimand for a Level One Infraction.

Level Two Infractions – Level Two Infractions are violations of IRS e-file rules and requirements that, in the opinion of the IRS, have an adverse impact upon the quality of electronically filed returns or on IRS e-file. Level Two Infractions include continued Level One Infractions after the IRS has brought the Level One Infraction to the attention of the Authorized IRS e-file Provider (Provider). Depending on the infractions, the IRS may either restrict participation in IRS e-file or suspend the Provider from participation in IRS e-file for a period of one year beginning with the effective date of suspension.

Level Three Infractions – Level Three Infractions are violations of IRS e-file rules and requirements that, in the opinion of the IRS, have a significant adverse impact on the quality of electronically filed returns or on IRS e-file. Level Three Infractions include continued Level Two Infractions after the IRS has brought the Level Two Infraction to the attention of the Provider. A Level Three Infraction may result in suspension from participation in IRS e-file for two years beginning with the effective date of the suspension year, or depending on the severity of the infraction, such as identity theft, fraud or criminal conduct, it may result in expulsion without the opportunity for future participation. The IRS reserves the right to suspend or expel a Provider prior to administrative review for Level Three Infractions.

Issue 13: Are Your Stockpiling?

An ERO must ensure that stockpiling of returns does not occur at its offices. Stockpiling is defined as one of the following two conditions:

(1) collecting returns from taxpayers or from another Authorized IRS e-file provider prior to official acceptance in the IRS e-file program (this is prior to your EFIN being approved by the IRS); or

(2) after official acceptance to participate in IRS e-file (EFIN has been approved by the IRS), stockpiling refers to waiting more than three calendar days to submit the return to the IRS once the ERO has all necessary information for origination (of the return).

Exception to the 3-day stockpiling rule

The IRS does not consider returns held prior to the date that it (IRS) accepts transmission of electronic returns as stockpiled. This includes when the IRS is not able to accept specific returns, forms, or schedules until a date later than the start-up of IRS e-file due to constraints such as late legislation (IRS) programming issues, etc. EROs must advise taxpayers that it cannot transmit returns to the IRS until the date the IRS accepts transmission of electronic returns. (Therefore the 3-day calendar period mentioned above does not start until January 30th for most forms.)

Issue 14: TCJA Provisions for Eligible Terminated S Corporations

Treasury and the IRS issued proposed regulation REG-131071-18, defining an eligible terminated S Corporation, and how cash distributions will be treated following the post-termination transition period. Once a corporation revokes its S status, generally the Post Termination Transition Period (“PTTP”) rules apply to give special treatment to cash distributions with respect to that corporation’s stock for a certain period.

After the PTTP ends, if the corporation qualifies as an ETSC, § 1371(f) applies. § 1371(f) also provides special treatment to cash distributions, which takes places in the form of a ratio of the corporation’s accumulated adjustment account and accumulated earnings and profits.

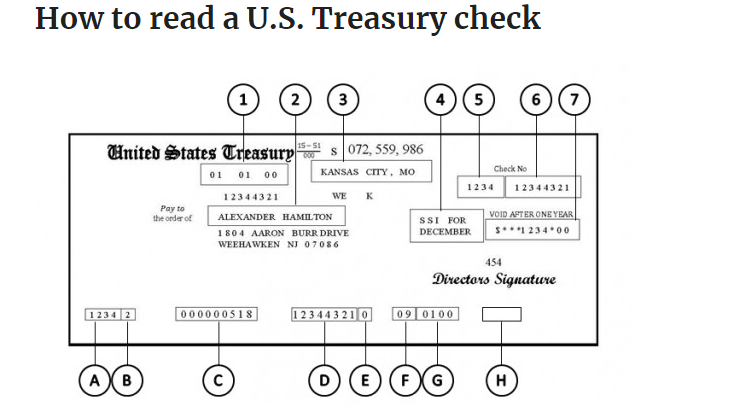

Issue 15: Why Did I Receive a U.S. Treasury Check? What is it All About?

Treasury’s Bureau of the Fiscal Service is there to assist when your client receives a government check and they are unsure what the payment is for.

The Kansas City Financial Center, one of two financial centers, processes all of Treasury-disbursed payments, both domestic and international, including printing and mailing responsibilities. Disbursement of paper checks is split between the Kansas City Center and its sister site, the Philadelphia Financial Center.

The Payment Management Call Center can answer questions about Treasury-sponsored programs and Treasury-disbursed payments.

- Call Center: 855-868-0151 or 816-414-2100

- E-mail: [email protected]

The image above will help you identify specific information printed on the Treasury check. Find the corresponding number or letter below.

Information contained on a U.S. Treasury check:

- 1 = Issue Date

- 2 = Payee Name

- 3 = Fiscal Service Financial Center

- 4 = Issue Type

- 5 = Check Symbol

- 6 = Check Serial Number

- 7 = Issue Amount

Information on the Magnetic Ink Character Recognition (MICR) line of a U.S. Treasury check:

- A = Check Symbol

- B = Check Digit

- C = Routing Number unique to U.S. Treasury checks

- D = Check Serial Number

- E = Check Digit

- F = Federal Agency Code

- G = Issue Date (MM/YY)

- H = Paid Amount, if the financial institution encodes the amount

Issue 16: Guidance to be Released by Year-End/January 2020

- Final rules under § 2010 regarding the increased basic exclusion amount for estate and gift taxes.

- The final regs on the Opportunity Zone program.

- Final and proposed regs on the § 163(j) interest expense deduction.

- Final and proposed regs under 267A addressing related-party amounts paid or accrued in hybrid transactions or by or to hybrid entities.

- Proposed regs under 863(b) on the new inventory sourcing rule.

- Proposed regs dealing with the cap on the state and local tax deduction.

- Proposed regs under 162(m) addressing the executive compensation deduction limitation.

- Proposed regs under 512 on computing unrelated business taxable income for exempt organizations’ separate trades or businesses.

- Proposed carried interest regs under 1061.

- Proposed regs on 3402 withholding.

Issue 17: How Do I Reach a Live Person on the 800-829-1040 IRS Assistance Number? PERSONAL Income Tax Refund

After listening to the many “telephone trees” associated with the IRS toll free number – I think I have found the right combo to answer a client’s questions about their refund. Many times, we need to “live person.”

You must listen to the full telephone tree options. Selecting an option before the announcements are completed will not work.

Select the following options as you move through the telephone tree. 2 then 1, then 1, then 3, then 2 where you will be placed in hold status with nice music to listen to – which you will become tired of very soon. I stress listen to all the options and then press the number.

Issue 18: Social Security Administration Issues Second Round of Notices to Notify More Employers Concerning Mismatch of W-2 Information

The Social Security Administration (SSA) has announced that it is sending a second round of notices to businesses and employers who submitted a Form W-2 (Wage and Tax Statement) for 2018 that contained name and Social Security Number (SSN) combinations that do not match SSA records.

Background. Generally, § 6051, requires employers to file information returns reporting employee wages and tax withholding to the SSA on Form W-2. The SSA uses Form W-2 to update an employee’s SSA records.

If the SSA cannot match the name and SSN reported on a Form W-2 with its records, it cannot reconcile employer wage reports and credit earnings to the record of a worker. When earnings are missing, the worker may not qualify for the Social Security benefits he or she is due, or the benefit amount may be incorrect.

When the SSA receives a Form W-2 that contain names and SSN combinations that don’t match its records, it sends the employer a notice referred to by the SSA as Educational Correspondence (EDCOR). According to the SSA, reported names and SSNs may not agree with SSA records because of typographical errors, unreported name changes, and inaccurate or incomplete employer records.

In March 2019, the SSA began mailing notifications to employers identified as having at least one name and Social Security Number (SSN) combination submitted on Forms W-2 that does not match SSA records. The purpose of the EDCOR is to advise employers that corrections are needed in order for the SSA to properly post employee earnings to the correct record.

As of April 26, 2019, the SSA mailed 577,349 EDCOR to employers regarding corrections needed so the SSA can properly post 2018 employee earnings.

New round of notices. In October and November 2019, the SSA is mailing out the remaining EDCOR generated from processing Forms W-2 that do not match the SSA records for tax year 2018.

Issue 19: Special IRS Efforts to Focus on Tax Compliance, Education

As part of a larger effort by the IRS to ensure fairness in the tax system, the IRS is taking steps to conduct special compliance efforts for individual and business taxpayers in various communities.

The goal of these visits is to help resolve tax compliance issues by meeting face-to-face with taxpayers with ongoing tax issues. The IRS will focus these efforts in areas where there have been a limited number of revenue officers available due to declining IRS resources.

Revenue officers are trained IRS civil enforcement employees who work to resolve compliance issues, such as missing returns or taxes owed. During these visits, the revenue officers interview taxpayers to gather financial information and provide them with the necessary steps to become and remain compliant with the law. When necessary, they will take the appropriate actions to collect the amount owed, following the law and respecting taxpayer rights.

The IRS routinely conducts these face-to-face visits. The primary factors of these visits are to make contact with taxpayers who have a previously known tax issue that wasn’t resolved through mail contact. The first face-to-face contact from a revenue officer is almost always unannounced.

The new effort involves focusing resources in a specific area during a specific time. Announcing general details about the efforts in specific areas are an important step to raise community awareness about IRS activity at a specified time to avoid confusion during a period where IRS scam artists and imposters remain active.

Visits shouldn’t be confused as a scam; what to look for

When an IRS revenue officer visits a taxpayer, they will always provide two forms of official credentials, both include a serial number and photo of the IRS employee. Taxpayers have the right to see each of these credentials.

A legitimate revenue officer is there to help taxpayers understand and meet their tax obligations, not to make threats or demand some unusual form of payment for a nonexistent liability. The officer will explain the liability to the taxpayer.

The IRS emphasizes these visits typically occur after numerous contacts by mail about an existing tax issue; taxpayers should be aware they have a tax issue when these visits occur.

If someone has an outstanding federal tax debt, the visiting officer will request payment but will provide a range of payment options, including paying by check that is payable to the U.S. Treasury.

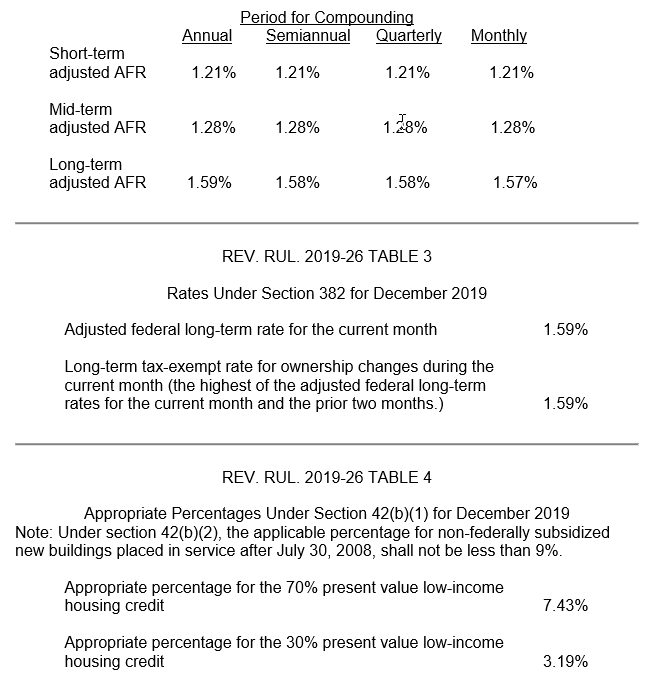

Issue: 20: Rev. Rul. 2019-26 – Applicable Federal Rates for December 2019

Table 1