Congratulations to AJ Reynolds for being selected to speak at the National Association of Tax Professionals in Chicago last month!

August 2019 Issues

Issue 1: Tax Security 2.0 “Taxes. Security. Together.” Checklist

Leaders from the IRS, state tax agencies and the tax industry today called on tax professionals nationwide to take time this summer to review their current security practices, enhance safeguards where necessary and take steps to protect their businesses from global cyber criminal syndicates prowling the Internet. To further combat identity theft, the Security Summit partners created a new “Taxes. Security. Together.” Checklist to serve as a starting point for tax professionals.

Beginning the week of July 15, the IRS and Summit partners will issue a series of five Tax Security 2.0 news releases highlighting “Taxes. Security. Together.” Checklist action items.

The number of taxpayers who reported to the IRS that they were victims of identity theft has fallen by 71%. In 2018, the IRS received 199,000 identity theft affidavits from taxpayers compared to 677,000 in 2015. This was the third consecutive year this number declined. The number of confirmed identity theft returns stopped by the IRS declined by 54 %, falling from 1.4 million in 2015 to 649,000 in 2018.

As the Summit has increased the tax community’s defenses against identity theft and refund fraud, cyber criminals continue to evolve. Increasingly, they look to data theft at tax professionals’ offices to obtain large amounts of sensitive taxpayer data. Thieves then use stolen data from tax professionals to create fraudulent returns that are harder to detect.

The “Taxes. Security. Together.” Checklist

The Summit partners urge the tax community to review these basic security steps this summer. Some tax pros may routinely overlook these checklist items and others need to regularly revisit them. The steps are not only important for tax practitioners, but for taxpayers as well. Everyone has a responsibility to protect sensitive data.

- Deploy the “Security Six” measures:

- Activate anti-virus software.

- Use a firewall.

- Opt for two-factor authentication when it’s offered.

- Use backup software/services.

- Use Drive encryption.

- Create and secure Virtual Private Networks.

Create a data security plan:

Federal law requires all “professional tax preparers” to create and maintain an information security plan for client data. The security plan requirement is flexible enough to fit any size of tax preparation firm, from small to large.

Tax professionals are asked to focus on key risk areas such as employee management and training; information systems; and detecting and managing system failures.

Educate yourself and be alert to key email scams, a frequent risk area involving:

- Learn about spear phishing emails.

- Beware ransomware.

- Recognize the signs of client data theft:

- Clients receive IRS letters about suspicious tax returns in their name.

- More tax returns filed with a practitioner’s Electronic Filing Identification Number than submitted.

- Clients receive tax transcripts they did not request.

Create a data theft recovery plan including:

- Contact the local IRS Stakeholder Liaison immediately.

- Assist the IRS in protecting clients’ accounts.

- Contract with a cyber security expert to help prevent and stop thefts.

Resources available for tax professionals

Tax professionals also can get help with security recommendations by reviewing IRS Publication 4557, Safeguarding Taxpayer Data, and Small Business Information Security: The Fundamentals by the National Institute of Standards and Technology.

Publication 5293, Data Security Resource Guide for Tax Professionals provides a compilation of data theft information available on IRS.gov. Also, tax professionals should stay connected to the IRS through subscriptions to e-News for Tax Professionals and social media.

Issue 2: Filing Student Financial Aid Applications

The IRS Data Retrieval Tool is available to use with the 2019‒2020 FAFSA Form. This tool is the fastest, most accurate way to input tax return information into the FAFSA form. Students and parents who are eligible to use the IRS Data Retrieval Tool can access it from within the Free Application for Federal Student Aid.

Applicants filing a 2019-20 FAFSA must use data from their 2017 tax returns. Clients should always keep a copy of their tax return. Whether they keep it electronically or on paper, they should keep it in a secure place. Here are some options for the client who did not keep a copy of their tax return.

- Access the tax software product used to prepare and file their 2017 return.

- Contact the tax preparer or provider who filed their 2017 return.

- Download their tax transcript at Get Transcript Online. The IRS will mail a transcript to the address on their return within five to 10 days.

- Call the IRS’s automated line at 800-908-9946 to order a transcript by mail.

- Taxpayers who filed an amended tax return, Form 1040-X, should use the adjusted gross income and earned income listed on their revised tax return.

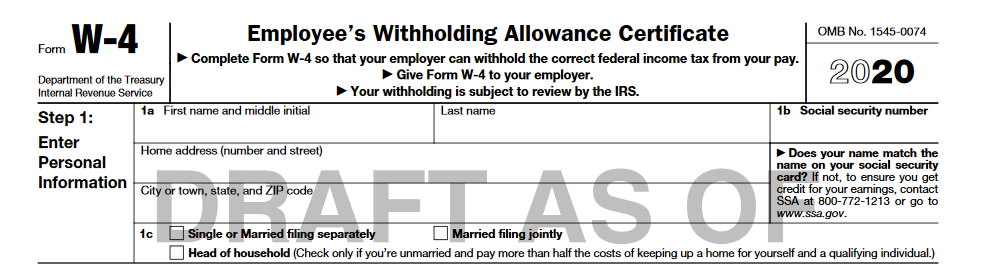

Issue 3: IRS, Treasury unveil proposed W-4 design for 2020

The July newsletter unveiled the proposed New Form W-4 along with step-by-step instructions for completion.

According to the IRS, the new design reduces the form’s complexity and increases the transparency and accuracy of the withholding system. While it uses the same underlying information as the old design, it replaces complicated worksheets with more straightforward questions that make accurate withholding easier for employees.

Step 1: Personal Information – Entity Section

The information remains basically the same in the entity section, with five significant changes, first, the Head of Household status has been added. This will cause much confusion as many assume, they qualify for Head of Household status. The result of selecting this filing status will reduce withholding and may cause a balance due.

Example: A client walks into your firm and provides information for return preparation. They have already determined their Head of Household status based on how they filled out their W-4 or based on “discussions” with others, that they qualify. Once you interview them, you deliver the news they do not qualify as they did not pay for more than half the cost of keeping up a home and have no qualifying child. Change in the W-4 withholding would be recommended, as needed.

With the “heighten” due diligence requirements of the Head of Household status the interview will be even more important in determining the appropriate filing status.

TIP: Taxpayers should never determine their filing status. We as tax professionals will make that determination based on the interview and materials presented for the return preparation. If you begin with the wrong filing status, the whole return is wrong from the very beginning.

The second change in the entity section is the removal of the Married, but withhold at a higher single rate. If the client requires additional withholding this choice was beneficial. Currently, there is no items in the new W-4 instructions that state the client can claim a single status for withholding if they are married.

Change number three removes the term “allowances” from the form. Clients often confuse “allowances” with exemptions. Personal exemptions have been “suspended” for tax years 2018-2025.

And fourth and fifth is the change in placement of the “Exempt” status, which has been moved to Step 4, as well as the “additional withholding”.

Note: Employees who have submitted Form W-4 in any year before 2020 are not required to submit a new form merely because of the redesign. Employers will continue to compute withholding based on the information from the employee’s most recently submitted Form W-4.

New employees who fail to submit a Form W-4 after 2019 will be treated as a single filer with no other adjustments. This means that a single filer’s standard deduction with no other entries will be taken into account in determining withholding. The IRS and Treasury anticipate issuing guidance consistent with this approach. Beginning in 2020, all new employees must use the redesigned form. Similarly, any employees hired prior to 2020 who wish to adjust their withholding must use the redesigned form.

Reminder your employer client, that it is the employee’s responsibility to fill out and submit the W-4. They should not assist.

More on the other sections of the new W-4 in the September Newsletter

Issue 4: Tax Professional in Illinois – Update

Key Points:

Legalize marijuana in Illinois begins January 1, 2020. The law allows the licensed growth, sales, possession and consumption of cannabis for adults 21 and over. The plant remains illegal under federal law, and the state previously decriminalized possession of small amounts. (House Bill 1438)

A tax amnesty program is set to begin Oct. 1 and run through Nov. 15. During that time, people who owe back taxes to the state can pay off those debts and avoid having to pay interest and penalties.

SB 687, which includes new income tax rates, was signed by the governor. Voters will either approve or deny the constitutional amendment establishing a new tax system in November 2020. If approved, the new rates would be applied and could be part of the Fiscal Year 2021 budget.

Beginning July 1, 2019, the state’s gas tax will double to 38 cents and the diesel fuel tax will get bumped 5 cents to 45.5 cents total.

Wages for Illinoisans will rise to $15 hourly by 2025, going up incrementally each year.

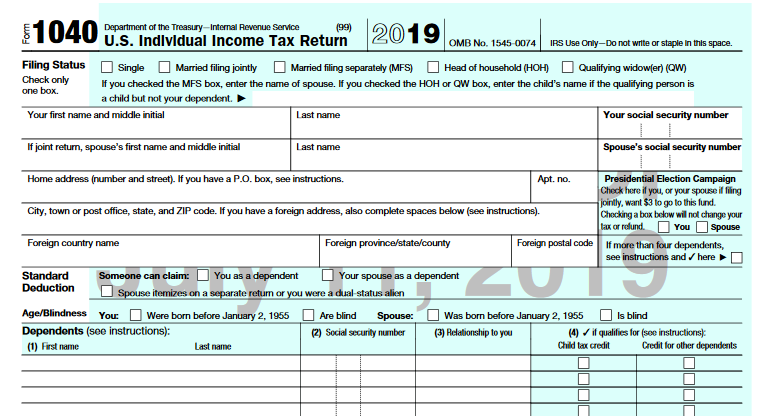

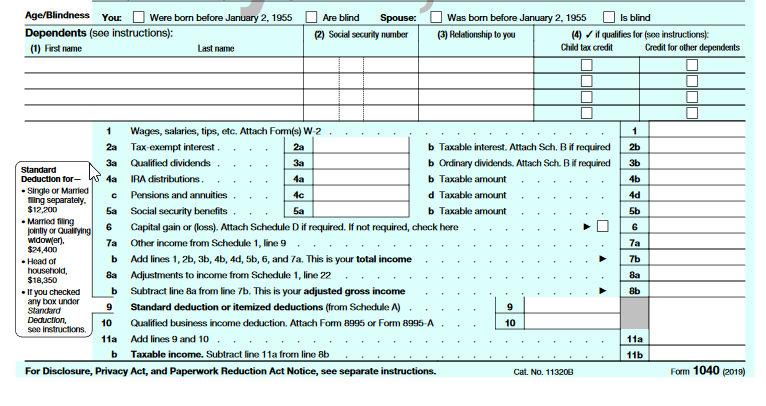

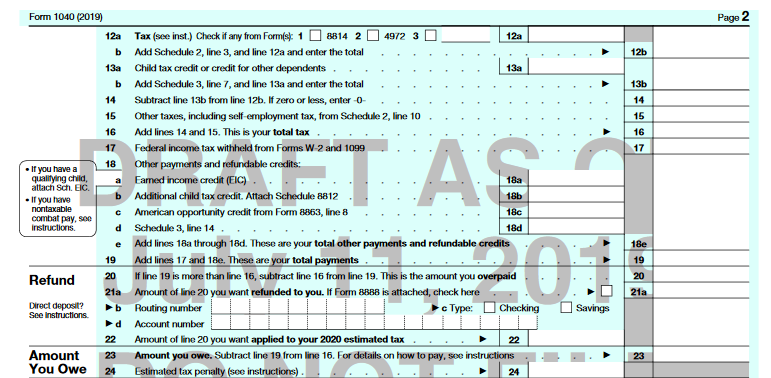

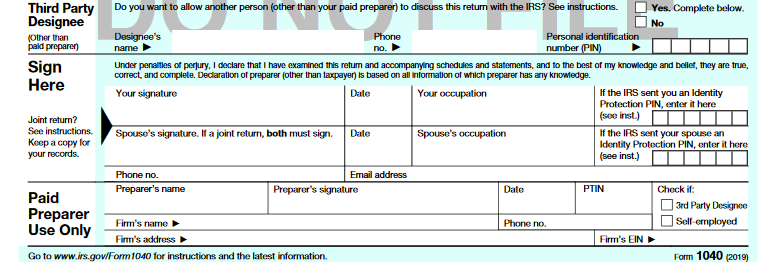

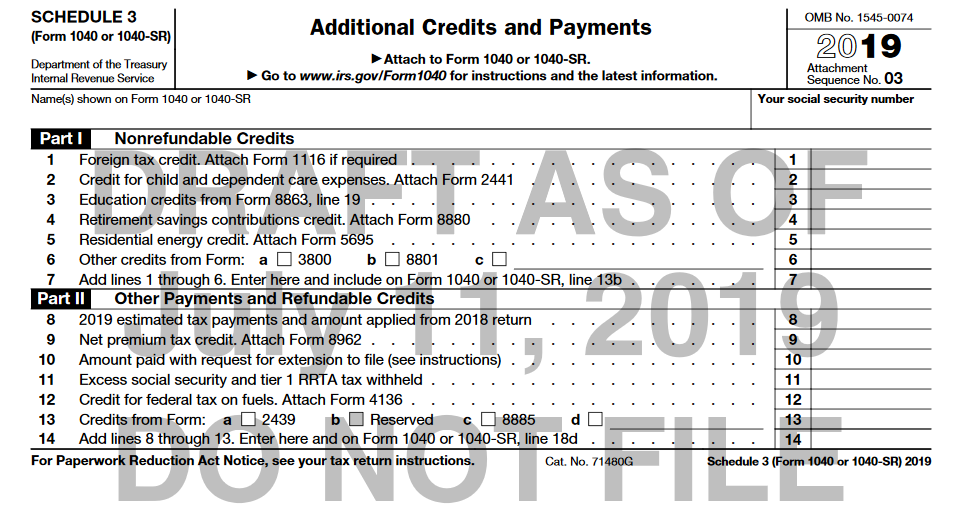

Issue 5: IRS Issues 2019 1040 Draft and Schedules

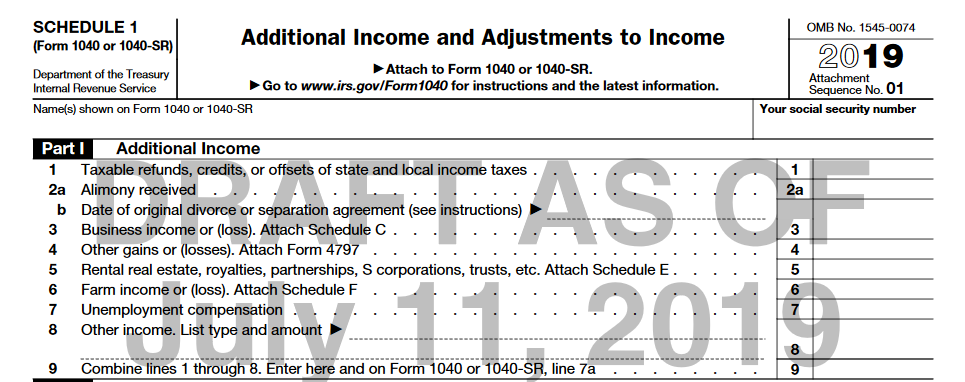

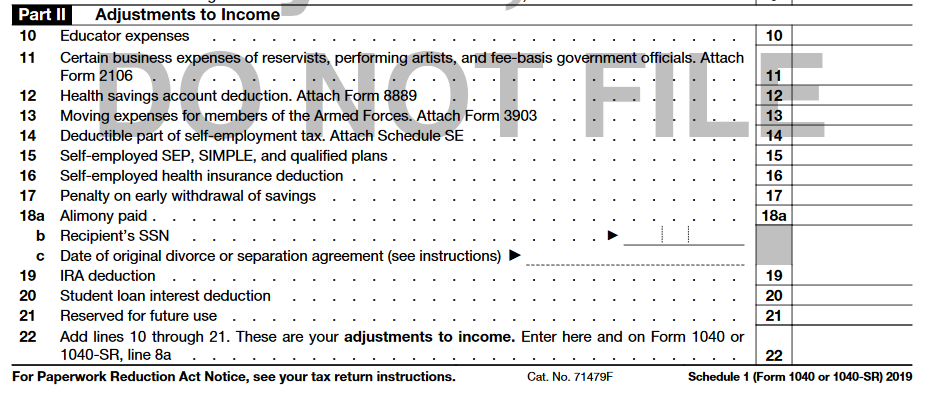

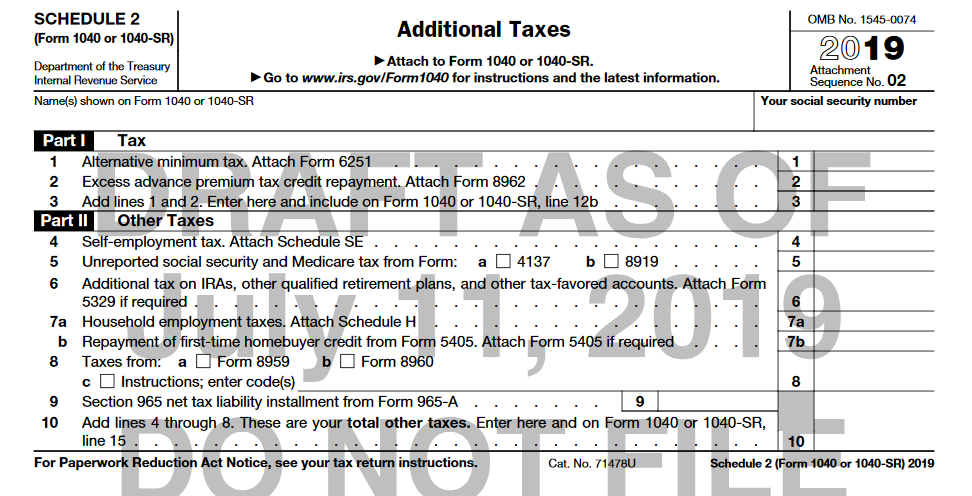

Prepare yourselves for more changes in the Form 1040 for 2019. The Form 1040 is back to two pages, similar to the 2018 form. The signature has returned to page 2. Schedules 4, 5 and 6 have been incorporated into the two-page form and are obsolete. The main Form 1040 and additional schedules: Schedule 1, Additional Income and Adjustments to Income, Schedule 2, Additional Taxes and Schedule 3, Additional Credits and Payments, make up the complete form.

The filing status line at the top of Form 1040 asks for additional information for taxpayers whose filing status is Married, filing separately (the name of the spouse) and Head of household and Qualifying widow(er) (name of child who isn’t a dependent).

The detailed listing of types of gross income, which had been on schedules last year, is now on page 1 of Form 1040. For example, the line for capital gains or losses, that was on the 2018 Schedule 1 is now on Form 1040, Line 6.

The checkbox for health care coverage has been removed; health care coverage is not required in 2019 in order to avoid a tax penalty.

Several of the most-used credits, the earned income credit and the additional child tax credit, have been moved from schedules to page 2 of Form 1040.

Lines to identify any foreign address and to name a third party with which IRS had permission to discuss the return, which had been on Schedule 6, has been moved to page 2 of the main form.

Schedule 1, Additional Income and Adjustments to Income, adds new lines upon which alimony recipients and payors must include the date of the original divorce or separation agreement; this is necessary because only alimony based on pre-2019 agreements is included in income/is deductible.

Form 1040 SR

Forms 1040A and 1040 EZ are still obsolete. But IRS introduced the new Form 1040 SR for Seniors.

Taxpayers can reach their 65th birthday at any time during the tax year—even Dec. 31—to qualify for using the 1040-SR. But the tax form imposes a few other qualifying restrictions in addition to the age rule.

The tax form for seniors also disallows itemized deductions. Seniors must claim the standard deduction for their filing status if they choose Form 1040-SR. In most case with the doubled standard deductions many seniors will opt not to itemized. And seniors age 65 or older are also entitled to an extra standard deduction depending on filing status.

Filers do not have to be retired yet to qualify.

Issue 6: Clarification of Line 28, Column (e) of Schedule E, Form 1040

A client who owns an interest in an S corporation and reports a loss, receives a distribution, disposes of stock, or receives a loan repayment from the S corporation must check a corresponding box under line 28, column (e), and attach a computation detailing their S corporation basis. The discussion about basis rules for S corporations in the Instructions for Schedule E (Form 1040) for Parts II and III does not limit or modify this requirement. Note: This applies only to an S Corporation basis.

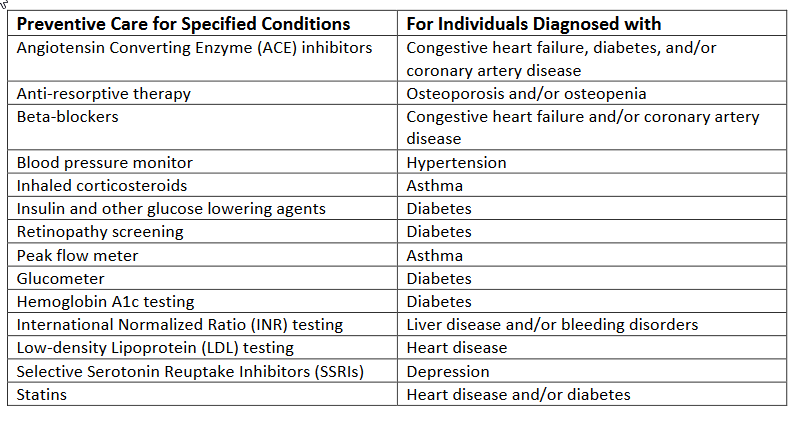

Issue 7: Notice 2019-45 Expands the list of Preventive Care Benefits Permitted to be Provided by a High Deductible Health Plan (HDHP)

- 223 of the Code permits eligible individuals to establish Health Savings Accounts (HSAs). Among the requirements to qualify as an eligible individual under § 223(c)(1) is that the individual be covered under an HDHP and have no disqualifying health coverage. Only eligible individuals under § 223(c)(1) are allowed to make contributions to an HSA or to receive contributions from an employer to their HSA. An HDHP is a health plan that satisfies certain requirements with respect to minimum deductibles and maximum out-of-pocket expenses.

Treasury and the IRS have been directed to consider ways to expand the use and flexibility of HSAs and HDHPs consistent with the provisions of § 223 and the appropriate standard for preventive care under § 223(c)(2)(C).

Specifically, on June 24, 2019, President Trump issued Executive Order 13877,3“Improving Price and Quality Transparency in American Healthcare to Put Patients First,” including, among other things, an order that the Secretary of Treasury, to the extent consistent with law, issue guidance to expand the ability of patients to select HDHPs that can be used alongside an HSA, and that cover low-cost preventive care, before the deductible, that helps maintain health status for individuals with chronic conditions. In response to Executive Order 13877, Treasury and the IRS are issuing this notice.

Treasury and the IRS consider benefits for services and items set forth in the chart below as preventive care for purposes of § 223(c)(2)(C). These specified services and items are treated as preventive care only when prescribed to treat an individual diagnosed with the associated chronic condition specified in the chart, and only when prescribed for the purpose of preventing the exacerbation of the chronic condition or the development of a secondary condition. If an individual is diagnosed with more than one chronic condition, all listed services and items applicable to the two or more conditions are preventive care. However, services and items not listed in the chart that are for secondary conditions or complications that occur notwithstanding the preventive care are not treated as preventive care for purposes of § 223(c)(2)(C).

Issue 8: Iowa Attorney General Issues Clarification on Hemp and CBD Laws

Various state agencies have been fielding hundreds of questions about the legality of products containing cannabidiol (CBD). CBD is a specific type of cannabinoid that occurs naturally in cannabis plants, predominately in its flowering tops and to a lesser extent in its resin and leaves.

Confusion about the legality of CBD products has increased in light of the federal Agriculture Improvement Act of 2018 (2018 Farm Bill, § 10113) and the passage of SF599, the Iowa Hemp Act, at the state level.

Attorney General Tom Miller issued a memo to clarify the legal status of CBD products under state law, provide information to people who are interested in buying or selling CBD products, and will explain enforcement authority.

Currently, Iowa law defines marijuana as “all parts of the plants of the genus Cannabis, whether growing or not; the seeds thereof; the resin extracted from any part of the plant; and every compound, manufacture, salt, derivative, mixture, or preparation of the plant, its seeds or resin, including tetrahydrocannabinols.” Iowa Code § 124.101(20).

The definition of marijuana explicitly excludes “the mature stalks of the plant, fiber produced from the stalks, oil or cake made from the seeds of the plant, any other compound, manufacture, sale derivative, mixture, or preparation of such mature stalks (except the resin extracted therefrom), fiber, oil, or cake, or the sterilized seed of the plant which is incapable of germination.”

Because CBD is derived from parts of the cannabis plant that are included in definition of marijuana, CBD is considered marijuana under Iowa law. Iowa law places both marijuana and its psychoactive component, tetrahydrocannabinols (THC), in Schedule I of the Uniform Controlled Substances Act. Consequently, any product containing any amount of CBD or any amount of THC is classified as a Schedule I controlled substance under Iowa law.

The only exception in state law is, the Medical Cannabidiol Act, which permits the manufacturing and distribution of medical cannabidiol (mCBD). mCBD is any pharmaceutical grade cannabinoid found in a cannabis plant with a THC level of no more than 3% that is manufactured and distributed pursuant to the Iowa Department of Public Health’s mCBD program. Under this program, Iowa’s two licensed manufacturers can manufacture mCBD for distribution to individuals with state-issued mCBD registration cards at Iowa’s five licensed dispensaries.

Iowa Hemp Act

On May 13, 2019, Governor Reynolds signed SF599, known as the Iowa Hemp Act, which will allow for the production of hemp in Iowa in the future. Under the Act, hemp means the plant cannabis and any part of that plant with a THC concentration of not more than 0.3% on a dry weight basis. Before hemp production can commence in Iowa, the United States Department of Agriculture (USDA) must approve a state plan.

The USDA will not begin approving state plans until after it promulgates regulations. The USDA has indicated it intends to issue regulations in the fall of 2019 and is committed to completing its review of plans within 60 days once regulations are effective.

The only provision of the Iowa Hemp Act that can be currently implemented is Section 3, which requires the Iowa Department of Agriculture and Land Stewardship (IDALS) to prepare a state plan to be submitted to the USDA. Per § 18 of the Act, the other provisions of the newly adopted Chapter 204 cannot be implemented until after the USDA approves Iowa’s state plan. Therefore, at present time, no one can grow, manufacturer, or process hemp in Iowa, outside of the two mCBD manufacturers licensed by the Iowa Department of Public Health.

In addition, the coordinating amendments, many of which remove hemp and hemp products from the Uniform Controlled Substances Act, do not become effective until after the USDA approves Iowa’s state plan.

When the Iowa Hemp Act becomes fully effective, CBD products containing no more than 0.3% THC will no longer be controlled substances under Iowa law. But this does not mean that all such products will become legal. While items such as cloth, cordage, fiber, fuel, paint, paper, particle board, and plastic will be able to be legally produced, § 7 of the Act clarifies that hemp-derived CBD can only be added to products intended for human consumption to the extent consistent with applicable federal law. The U.S. Food and Drug Administration’s (FDA) current position is that products marketed with therapeutic benefit claims must be approved by the FDA as drugs prior to introducing them into interstate commerce.

Finally, two state agencies may have jurisdiction over an entity that sells CBD products. The Iowa Department of Inspections and Appeals (DIA) licenses and regulates entities that sell or serve food, unless an entity sells only pre-packaged and non-temperature-controlled foods. The DIA has issued a regulatory notice to licensees indicating that they are prohibited from selling CBD products for human consumption.

The Alcoholic Beverages Division (ABD) licenses and regulates those who sell and serve alcoholic beverages. The ABD has issued a regulatory bulletin to license and permit holders indicating that both CBD and THC are prohibited in alcoholic beverages sold in Iowa.

Issue 9: IRS Has Begun Sending Letters to Virtual Currency Owners Advising them to Pay Back Taxes, File Amended Returns

The Internal Revenue Service has begun sending letters to taxpayers with virtual currency transactions that potentially failed to report income and pay the resulting tax from virtual currency transactions or did not report their transactions properly. By the end of August, more than 10,000 taxpayers will receive these letters. The names of these taxpayers were obtained through various ongoing IRS compliance efforts.

For taxpayers receiving an educational letter, there are three variations: Letter 6173, Letter 6174 or Letter 6174-A, all three versions strive to help taxpayers understand their tax and filing obligations and how to correct past errors.

Last year the IRS announced a Virtual Currency Compliance campaign to address tax noncompliance related to the use of virtual currency through outreach and examinations of taxpayers. The IRS will remain actively engaged in addressing non-compliance related to virtual currency transactions through a variety of efforts, ranging from taxpayer education to audits to criminal investigations.

Virtual currency is an ongoing focus area for IRS Criminal Investigation. IRS Notice 2014-21 states that virtual currency is property for federal tax purposes and provides guidance on how general federal tax principles apply to virtual currency transactions. The IRS anticipates issuing additional legal guidance in this area in the near future.

Issue 10: PTIN Required to Prepare Estate, Trust Returns

Tax professionals specializing in estate and trust returns must have a Preparer Tax Identification Number (PTIN) and renew it annually. A PTIN is required of paid professionals who prepare or assist in preparing certain federal tax returns, including Form 1041, U.S. Income Tax Return for Estates and Trusts. Failure to enter a valid PTIN can result in a $50 penalty per return and could cause processing delays for your clients.

The IRS urges the estate and trust community, especially financial institutions offering services to clients, to ensure that staff who prepare or assist in preparing Forms 1041 have PTINs. PTINs cannot be shared: Each paid professional must have his or her own.

Issue 11: TCJA: Section 965 Transition Tax and New Limits on Partners’ Shares of Partnership Losses

A new question and answer document is available to help you help your clients meet their filing and payment requirements for the § 965 transition tax. The Q&As address subsequent installment payments when the transition tax is paid over eight years, the filing of transfer and consent agreements, and more.

The IRS has also posted frequently asked questions to help partners properly determine their share of partnership losses. The FAQs, related to Section 704(d), address changes made by the Tax Cuts and Jobs Act that apply partners’ basis limitations to distributive shares of partnership charitable contributions and foreign taxes.

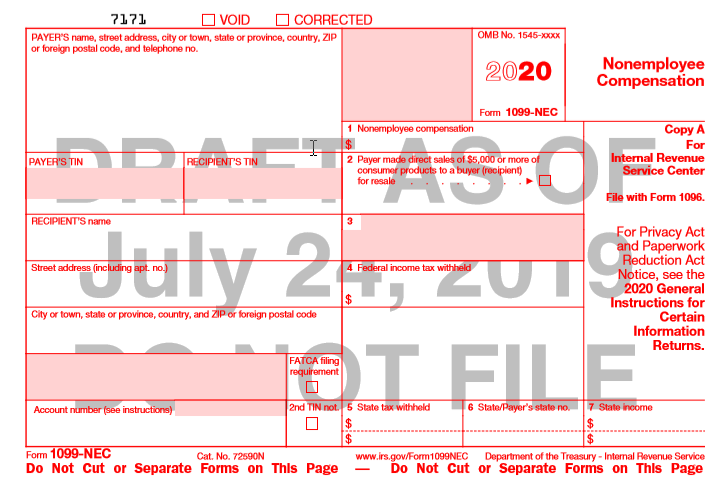

Issue 12: New Form 1099 NEC Looks to Replace the Form 1099 Misc for Non-Employee Compensation Issues in 2020

If the following four conditions are met, a payor must generally report a payment to the IRS as nonemployee compensation (NEC):

The payor made the payment to someone who is not the payor’s employee.

The payor made the payment for services in the course of the payor’s trade or business (including government agencies and nonprofit organizations).

The payor made the payment to an individual, partnership, estate, or, in some cases, a corporation.

The payor made payments to the payee of at least $600 during the year. (2019 Instructions to Form 1099-MISC)

Information that currently is required on the Form 1099 Misc. for Nonemployee Compensation will be mirrored on the new Form and it is assume Box 7 NEC requirements will be removed from Form 1099 Misc.

Issue 13: 2020 Applicable Percentage Tables to Determine Premium Tax Credit Eligibility

Rev. Proc. 2019-29 provides indexing adjustments required by statute for certain provisions under § 36B. Specifically, this revenue procedure updates the applicable percentage table used to calculate an individual’s premium tax credit for taxable years beginning in calendar year 2020 and updates the required contribution percentage for plan years beginning after calendar year 2019.

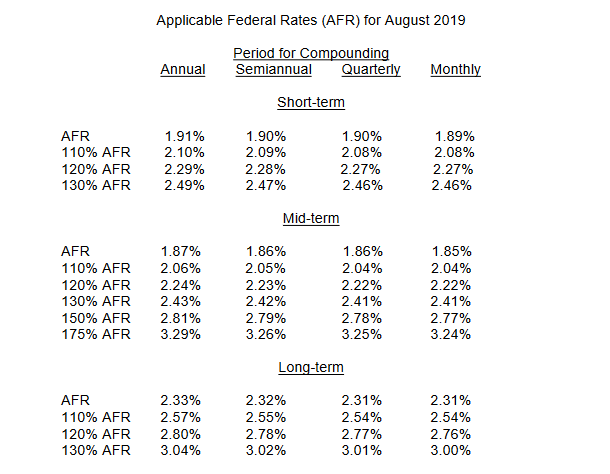

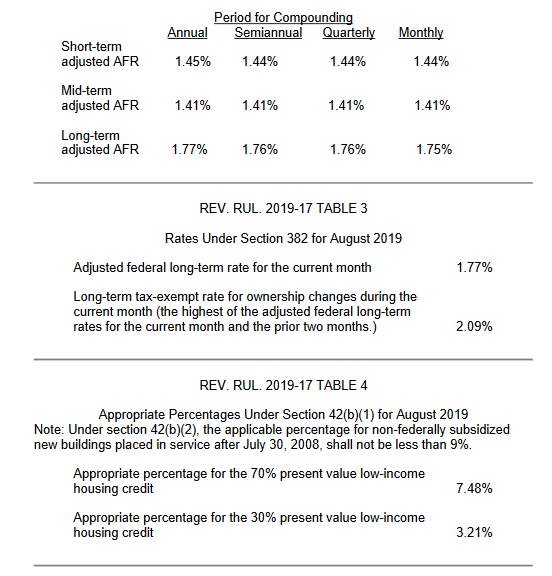

Issue 14: IRS has provided various applicable federal rate tables for August 2019.

REV. RUL. 2019-17 TABLE 1

REV. RUL. 2019-17 TABLE 2

Adjusted AFR for August 2019

2019 Tax Seminar Dates are Now Available

Can’t attend in person? Join the live stream webinar to earn CPE and get the updates:

Live Stream Fall Update Webinar: Cedar Rapids October 1

Live Stream Year-End Webinar: Cedar Rapids December 10

https://www.cpehours.com/dates-locations/

This Fall, we will be discussing the issues listed below at our seminars:

2019 Tax Legislation–Overview: Let us provide you with an overview of new law enacted in 2019 and IRS rulings and pronouncements. We will cover some key issues where guidance has been issued concerning prior enacted law, additional guidance on the SALT deduction, meals and entertainment and other updates as released.

Safe Harbor Election & Rentals: To Use or Not to Use, that is the Question? Notice 2019-07 – released concurrently with the Final Regs, provides notice of a proposed revenue procedure detailing a proposed safe harbor under which an RPE enterprise may be treated as a trade or business solely for purposes of IRC §199A. This is a key issue we are monitoring. Additional direction is expected on this issue and as this develops, this session will explain and provide examples that demonstrate the updated guidance. We will discuss related issues on deducting losses from Real Estate.

Centralized Partnership Audit Regime: This section will focus on the new series of forms issued concerning the Centralized Partnership Audit Regime. Form 8988 Election for Alternative to Payment of the Imputed Underpayment – IRC Section 6226, Form 8989, Request to Revoke the Election for Alternative to Payment of the Imputed Underpayment, Form 8980 Partnership Request for Modification of Imputed Underpayments Under IRC Section 6225(c) and more.

754 Election: Review the basics of a §754 Election to “step-up” the basis of the assets within a partnership when one of two events occur: distribution of partnership property or transfer of an interest by a partner. Basic class but will discuss how QBI is impacted.

Ethics and the Tax Client: During the past several years, news rules have been adopted or proposed that impact how we interact with our clients. This segment will provide a look at the latest IRS regulations and changes to professional standards. Security is all important and one segment of our discussion will center on the issue of protecting your client’s data. We will discuss how to ethically interact with the QBI deduction when you address the issue with your client. And finally, a review of the disciplinary proceedings you could face if your practice comes under scrutiny from the Office of Professional Responsibility.

IRS Procedures: We’ll present information on how to keep your EFIN current, navigating e-services and renewal of IP PTINs. Did you know IRS can “lock” you EFIN in the middle of filing season making you unable to e-file. It’s important to keep that information current, addresses, key officials, etc. E-services is the electronic way of doing business with the IRS. Get answers sooner, get transcripts when needed. What estimates have been paid? With a filed Power of Attorney, you can use e-services to get the above information and save a call to IRS and save time. Other online applications will also be reviewed as well as some common IRS procedures we all need to know.

Insolvency & Cancellation of Debt: A taxpayer is insolvent when the total liabilities exceed his or her total assets. The forgiven debt may be excluded as income under the “insolvency” exclusion. We will review the tax consequences for real estate property that is disposed of through foreclosure, short sale, deed in lieu of foreclosure, and abandonments. We will also delve into which business entity is more, or less, beneficial when it comes to cancellation of debt and insolvency. The segment will include examples and any law updates as the extension of the forgiveness of primary residents’ cancellation of debt (expired in 2017) is still being discuss as a potential retroactive law provision.

Penalty Abatement: We will demonstrate how to navigate a first-time Abatement Program, using Form 843, Rev Procedure 84-35 (Partnership Returns), Written & Oral Advice from the IRS, advice from a tax professional or attorney, ordinary business care, lost or destroyed records, code, regulations, Internal Revenue Manual, and case law to support your reasonable cause position.

Statute of Limitations: A review of the statute of limitations as they apply to federal tax law. If you do not understand your statute limits, a client’s refund could slip through your fingers. Or you could execute an Offer in Compromise for a year where the collection statute expires. With all the new changes a review of this area of the law will be a good refresher for all.

Marijuana & CBD Oil: The US Court of Appeals for the 9th Circuit in Hemp Industries Assn. et.al., vs. U.S. Drug Enforcement Admin., maintained the Drug Enforcement Administration’s (DEA) wide-ranging rule creating a separate classification for “Marijuana Extracts.” Though still illegal in the U.S., Marijuana legalization continues to pick up steam for legalization, due to many states who have adopted laws legalizing the use in various aspects from recreational to medicinal purposes. A review of where we stand tax wise concerning the Marijuana client will be provided.