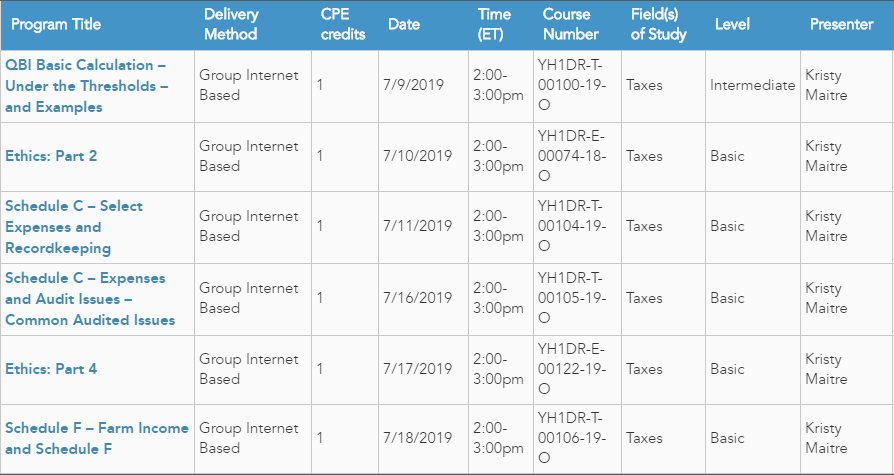

July 2019 Issues

Issue 1: Tax Court Approves IRS Denial of Installment Plan Request

IRS has made great strides in the installment agreements arena with both individuals and business entities. The criteria has been modified, numerous times, and is much less strict then several years ago, but in entering an installment agreement the client must meet their current tax obligations. This is demonstrated fully in a new case, Coastal Luxury Management, TC Memo 2019-43, 4/29/19, where the Tax Court upheld the IRS’ refusal to approve an installment agreement for unpaid payroll taxes.

Under the “trust fund penalty,” IRS can impose tax liability for the full amount of back taxes on a responsible person. Trust fund taxes are also not to be used as working capital as they are funds entrusted to the employer to pay to IRS to cover the employee tax liability. However, in a change of policy years ago the tax debtor may arrange an affordable payment plan with the IRS if five requirements are met:

- The client has filed all outstanding employment tax returns.

- The client is current with all tax deposits.

- The client must complete a Form 433-B, Collection Information Statement for Businesses and gather specific documents to support the entries.

- Financial information must be provided to the IRS and a request for an installment agreement must be in writing. The agreement request must state the amount per month the client intends to pay, the date the payments will begin, and the tax periods the installment agreement covers.

- Finally, the client complies with any deadlines set by the IRS to provide additional documents or information.

Coastal Luxury Management is a hospitality management company that operates food and wine festivals in California. IRS issued a notice of intent to levy for unpaid payroll taxes totaling over $1.4 million. The firm did not dispute the liabilities and asked for other relief. The firm stated they were behind on their tax obligations because an employee had embezzled funds. The Revenue Officer assigned to the case realized that the company was not in compliance with their current federal employment tax deposit obligations, a requirement for the requested relief.

The court held that the company failed to be in compliance with the IRS policy for relief and upheld the determination that the full amount was due.

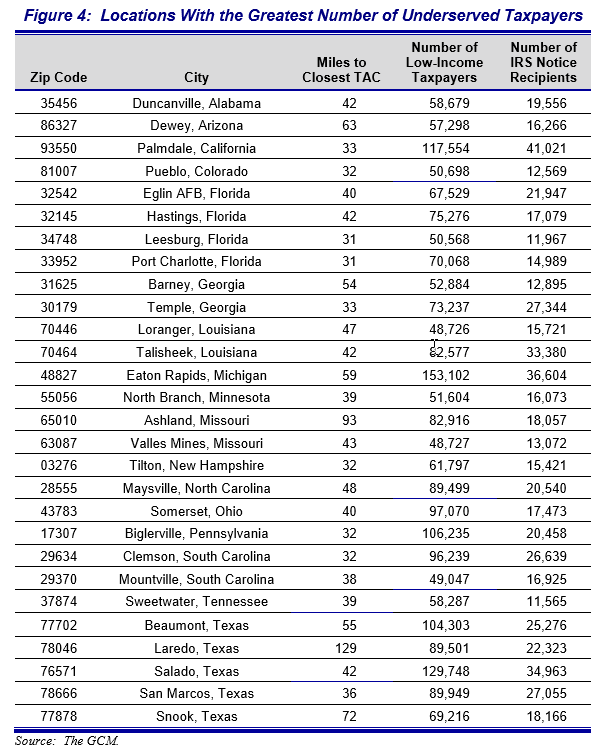

Issue 2: Internal Revenue Service Did Not Follow Congressional Directives Before Closing Taxpayer Assistance Centers

The IRS provides taxpayers with face-to-face tax assistance throughout the Nation at 359 Taxpayer Assistance Centers, 38 Virtual Service Delivery sites, and five Social Security Administration offices, as of December 31, 2018. Assistance includes taxpayers whose issues cannot be resolved through other methods or who prefer face-to-face assistance to meet their tax obligations. The IRS established a face-to-face assistance appointment system in Fiscal Year 2017. Since November 2016, taxpayers have been required to call the IRS appointment line to schedule an appointment for services. If they are unable to call, or they arrive at a TAC with an emergency or immediate issue, they can receive assistance the same day if employees are available.

In Fiscal Year (FY)3 2018, more than 220,000 (8 %) of the 2,783,665 taxpayers who sought assistance from a TAC were given a same-day appointment. Taxpayers without an appointment can still drop off a current year tax return, pick up a tax form or publication, and make a payment.

The IRS closed 12 TACs in Calendar Year 2018, including four that were closed subsequent to the March 23, 2018, enactment date of the Consolidated Appropriations Act of 2018. The review identified that the IRS did not comply with congressional directives accompanying this Act which require the IRS to:

- Report to the committees on appropriations of the Senate and House of Representatives within 120 days of enactment of the Act on the steps being taken to prevent any TAC closures and the status of any proposed alternatives to fully staffed TACs.

- Conduct a study on the impact of closing a TAC and the adverse effects it has on taxpayers’ ability to interact with the IRS.

The TIGTA study identified the locations where the greatest number of Unserved Taxpayers

Issue 3: Pilot Program to Audit Schedule F Expenses

February 27, 2017, Control Number: SBSE-04-0217-0014 MEMORANDUM FOR DIRECTOR, EXAMINATION – CAMPUS

There has been limited coverage of Schedule F in recent years in Correspondence Exam. IRS believes there may be compliance issues such as deducting expenses on the wrong form, deducting expenses actually belonging to another taxpayer, or related to Internal Revenue Code (IRC) § 183. IRS will use the same filtering process as is currently used for Schedule C examinations.

Taxpayers will be asked to provide documentation to show they qualify for the questioned expenses. Occasionally, the items being verified appear to be legitimate and verifiable deductions, but they should not be on a Schedule F and could be related to the taxpayer’s employment as an employee a Schedule A expense or related to a corporation return. These cases may also have start-up costs or a hobby loss where enjoyment is the main focus of the activity.

Leads will be generated from a series of compliance Data Environment (CDE) filters run through Campus Workload Delivery (CWD) elimination filters. The filter is designed to identify those taxpayers who have W-2s with large income who file a Schedule F and may not have the time to run a farm. The program has been completed and the information gathered could impact current audit and the selection process.

Issue 4: California – New Use Tax Collection Requirements for Remote Sellers and New District Use Tax Collection Requirements for All Retailers—Operative April 1, 2019

The California Legislature recently passed Assembly Bill No. (AB) 147 (Stats. 2019, ch. 5). AB 147 requires:

- Retailers located outside of California (remote sellers) to register with the California Department of Tax and Fee Administration (CDTFA) and collect California use tax if, in the preceding or current calendar year, the total combined sales of tangible personal property for delivery in California by the retailer and all persons related to the retailer1 exceed $500,000; and

- All retailers required to be registered with the CDTFA, whether located inside or outside of California, to collect and pay to the CDTFA district use tax on all sales made for delivery in any district that imposes a district tax if, in the preceding or current calendar year, the total combined sales of tangible personal property in this state or for delivery in this state by the retailer and all persons related to the retailer exceed $500,000.

The new collection requirements are operative April 1, 2019, and supersede our previous direction regarding:

1) the use tax collection requirements for out-of-state retailers (see Special Notice L-5652), and

2) the district use tax collection requirements for all retailers, including retailers located inside or outside of California (see Special Notice L-5913).

Additional registration and fee collection requirements for sales of certain items

Please note: If your client sells:

1) new tires or vehicles and equipment that include new tires,

2) covered electronic devices,

3) lead-acid batteries, or

4) lumber or engineered wood products, they may have additional registration and fee collection requirements. For information, see view online guide, Use Tax Collection Requirements Based on Sales into California Due to the Wayfair Decision on the website at www.cdtfa.ca.gov/industry/wayfair.htm.

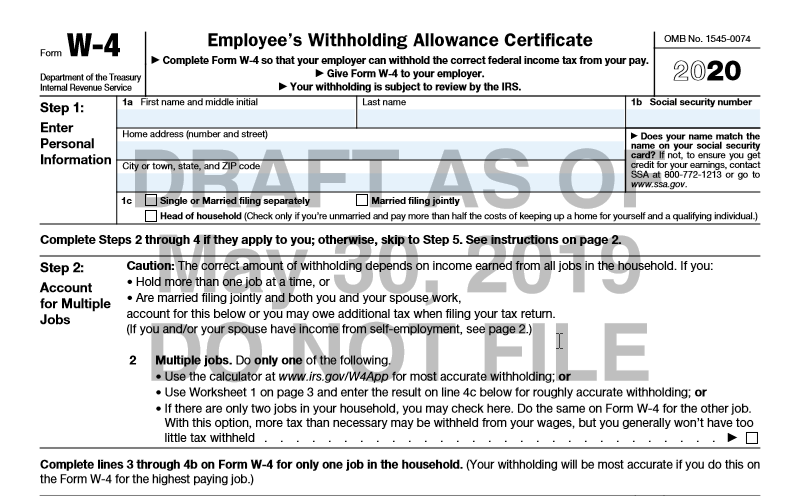

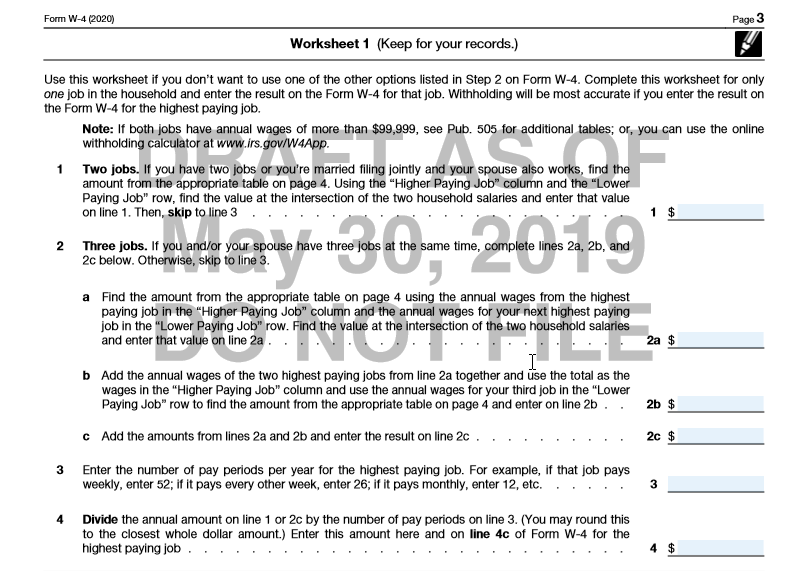

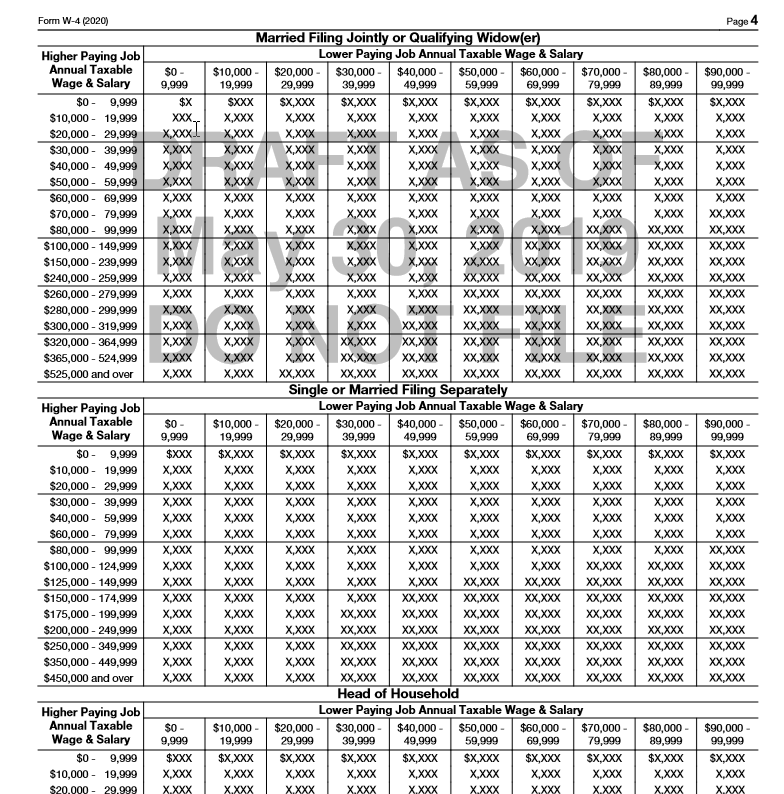

Issue 5: IRS, Treasury unveil proposed W-4 design for 2020

Complete Form W-4 so that the employer can withhold the correct federal income tax from pay. Complete a new Form W-4 when personal or financial situation changes.

Step 1, line 1c. Check the anticipated filing status. This will determine the standard deduction and tax rates used to compute withholding. Step 2. Use this line if the client has more than one job at the same time or are married filing jointly and both spouses work.

If the client meets meet both requirements on line 4d, they may skip lines 2–4c and complete line 4d. If the client claims an exemption from withholding, they will need to submit a new Form W-4 by February 16, 2021.

Remember, it is the employee/client’s responsibility to fill out and submit the W-4.

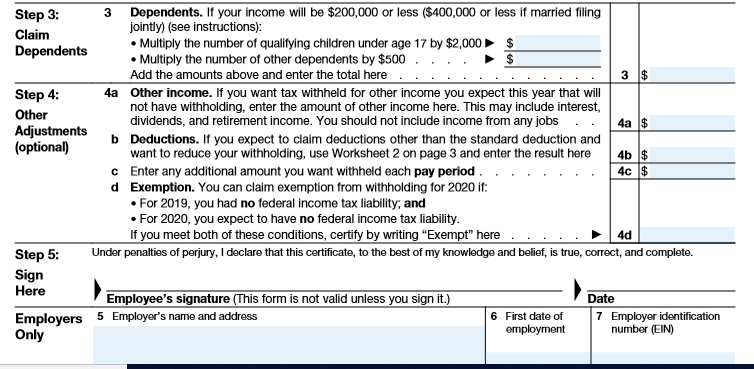

Self-employment. Generally, a client will owe both income and self-employment taxes on any self-employment income received separate from the wages receive as an employee. The new W-4 draft still requires the employee to have knowledge of dependents, other income issues and multi-employer special calculations. They also must estimate their itemized deductions and have knowledge of the “taxes” limitation in the calculations. To successfully submit a correct W-4 will require some understanding of tax law as we know it.

This new draft places a lesser burden on the employer in the calculation of proper withholding that the original form issued last year but could still be a problematic issue for employees. The near-final draft is expected to be released mid-to-late July. The summer release will give employers and payroll processors what they need to make system updates before the final form is released in November. The W-4 Instructions for employees are a part of this release and a separate set of instructions for employers will be available soon.

The new W-4 form will better incorporate the changes ushered in by Tax Cuts and Jobs Act. The goals of the new design are to provide simplicity, accuracy and privacy for employees while minimizing burden for employers and payroll processors.

Issue 6: IRS Now Billing Those Who Filed for 2018 but Didn’t Pay

The Internal Revenue Service advised those now receiving tax bills because they filed on time but didn’t pay in full that there are many easy options for paying what they owe. Taxpayers can pay online, by phone or using their mobile device. Taxpayer who can’t pay in full may consider payment plans and compromise options.

If a tax return was filed but the amount owed are unpaid, the taxpayer will receive a letter or notice in the mail from the IRS. These notices, including CP14 and CP501, which notify taxpayers that they have a balance due, are frequently mailed during June and July.

Making a payment

Taxes can be paid anytime throughout the year. When paying, taxpayers should keep in mind:

- Electronic payment options are the quickest way to make a tax payment.

- IRS Direct Pay (bank account) is a free way to pay online directly from a checking or savings account.

- Taxpayers can choose to pay with a debit or credit card. Although the payment processor will charge a processing fee, no fees go to the IRS.

- The IRS2Go app provides mobile-friendly payment options. Taxpayers can use Direct Pay or card payments on mobile devices.

- Taxpayers can pay using their tax software when they e-file. For those using a tax preparer, they can ask the preparer to make the tax payment electronically.

- Taxpayers may also enroll in the Electronic Federal Tax Payment System and have a choice of using the internet or phone and using the EFTPS Voice Response System.

Those who can’t pay in full have several options. They can:

Set up a payment plan

- With the Online Payment Agreement, taxpayers can usually set up a payment plan (including an installment agreement) in a matter of minutes. Individuals who owe $50,000 or less in combined income tax, penalties and interest likely qualify for an Online Payment Agreement. Online applications to establish tax payment plans are available Monday – Friday, 6 a.m. to 12:30 a.m.; Saturday, 6 a.m. to 10 p.m.; Sunday, 6 p.m. to midnight. All times are Eastern time.

- Another option is getting a loan. In many cases, loan costs may be lower than the combination of interest and penalties the IRS must charge under federal law.

- Automating payments makes it easy to avoid default. Using direct debit from a bank account or a payroll deduction means taxpayers don’t have to remember to send in a payment and saves postage costs. User fees may apply, except to low-income taxpayers, but are lower than fees for manual payment plans.

- Pausing collection – If the IRS determines a taxpayer is unable to pay, it may delay collection until their financial condition improves.

Issue 7: Congress Has a Lot on Its Plate – Summary

Back from the Memorial Day holiday Congress is back in session but has much work to do to keep the nation on track.

$19 billion in Disaster Aid – numerous disasters have spread across the nation that will be addressed in the disaster bill.

The Retirement Enhancement Act (SECURE Act, H.R. 1994) was passed by the House but now faces a challenge in the Senate due to the dropping of a provision to extend § 529 plans to homeschooling.

A task force was established to look at extenders that failed to be extended as well as other technical corrections needed. We will be monitoring these actions, especially the Secure Act which if passed and signed into law will be part of our Year-End Seminar.

Issue 8: Income Averaging Calculations for Farmers and Fishermen Should Take into Account the Qualified Business Income Deduction

Farmers and fishermen who elect to use Schedule J (Form 1040) to calculate their income tax by averaging all or part of their taxable income from their trades or businesses of farming or fishing should figure the amount that may be entered on Line 2a of Schedule J by taking into account amounts on Form 1040, line 9, Qualified Business Income Deduction, but only to the extent that deduction is attributable to any farming or fishing business. This item is in addition to the many items already listed in the instructions for Line 2a showing where to find income, gains, losses, and deductions from farming or fishing.

Issue 9: IRS Takes Additional Steps to Protect Taxpayer Data; Plans to End Faxing and Third-Party Mailings of Certain Tax Transcripts

As part of its ongoing efforts to protect taxpayers from identity thieves, the Internal Revenue Service announced it will stop its tax transcript faxing service in June and will amend the Form 4506 series to end third-party mailing of tax returns and transcripts in July. Tax transcripts are summaries of tax return information. Transcripts have become increasingly vulnerable as criminals impersonate taxpayers or authorized third parties. Identity thieves use tax transcripts to file fraudulent returns for refunds that are difficult to detect because they mirror a legitimate tax return.

The halt to the faxing and third-party service this summer are two more steps the IRS is taking to protect taxpayer data. In September 2018, the IRS began to mask personally identifiable information for every individual and entity listed on the transcript. We discussed the New Tax Transcript and Customer File Number in last month’s newsletter, check our blog for the June 2019 issue.

Starting June 28, 2019, the IRS will stop faxing tax transcripts to both taxpayers and third parties, including tax professionals. This action affects individual and business transcripts.

Individual taxpayers have several options to obtain a tax transcript. They may:

- Use IRS.gov or the IRS2Go app to access Get Transcript Online; after verifying their identities, taxpayers may immediately download or print their transcript, or

- Use IRS.gov or the IRS2Go app to access Get Transcript by Mail; transcript will be delivered within 10 days to the address of record, or

- Call 800-908-9946 for an automated Get Transcript by Mail feature, or

- Submit Form 4506-T or 4506T-EZ to have a transcript mailed to the address of record.

Tax professionals also have several options to obtain tax transcripts necessary for tax preparation or representation as follows:

- Request that the IRS mail a transcript to the taxpayer’s address of record, or

- Use e-Services’ Transcript Delivery System online to obtain masked individual transcripts and business transcripts, or

- Obtain a masked individual transcript or a business transcript by calling the IRS, faxing authorization to the IRS assistor and the IRS assistor will place the document in the tax practitioner’s e-Services secure mailbox.

When needed for tax preparation purposes, tax practitioners may:

- Obtain an unmasked wage and income transcript by calling the IRS, faxing authorization to the IRS assistor and the IRS assistor will place the document in the tax practitioner’s e-Services secure mailbox, or

- Obtain an unmasked wage and income transcript if authorization is already on file by using e-Service’s Transcript Delivery System.

Effective July 1, 2019, the IRS will no longer provide transcripts requested on Form 4506, Form 4506-T and Form 4506T-EZ to third parties, and the forms will be amended to remove the option for mailing to a third-party. These forms are often used by lenders and others to verify income for non-tax purposes. Among the largest users are colleges and universities verifying income for financial aid purposes. Tax professionals also are large volume users.

Taxpayers may continue to use these forms to obtain a copy of their tax return or obtain a copy of their tax transcripts. This change will NOT affect use of the IRS Data Retrieval Tool through the Free Application for Federal Student Aid (FAFSA) process.

Third parties who use these forms for income verification have other alternatives. The IRS offers an Income Verification Express Service (IVES) which has several hundred participants, who, with proper authorization, order transcripts. Lenders or higher education institutions can either contract with existing IVES participants or become IVES participants themselves. The tax transcript is an official IRS record. Taxpayers may choose to provide transcripts to requestors instead of authorizing the third party to request these transcripts from the IRS on their behalf.

Tax professionals who are attorneys, Certified Public Accountants or Enrolled Agents (i.e., Circular 230 practitioners) and do not have an e-Services account may create one and, with proper authorization from clients, can access the e-Services’ Transcript Delivery System. Unenrolled tax practitioners must have an e-File application on file and be listed as delegated users to access TDS.

Customer File Number helps match transcripts

Because the taxpayer’s name and Social Security number are now partially masked, the IRS also created a Customer File Number space that can be used to help third parties match transcripts to taxpayers. Third parties can assign a Customer File Number, such as a loan application number or a student identification number. The number will populate on the transcript and help match it to the client/student.

Issue 10: Interest Rates Decrease for the Third Quarter of 2019

- 5% for over payments [4% in the case of a corporation];

- 5% for the portion of a corporate over payment exceeding $10,000;

- 5% for underpayments; and

- 7% for large corporate underpayments.

For taxpayers other than corporations, the over payment and underpayment rate is the federal short-term rate plus 3 percentage points.

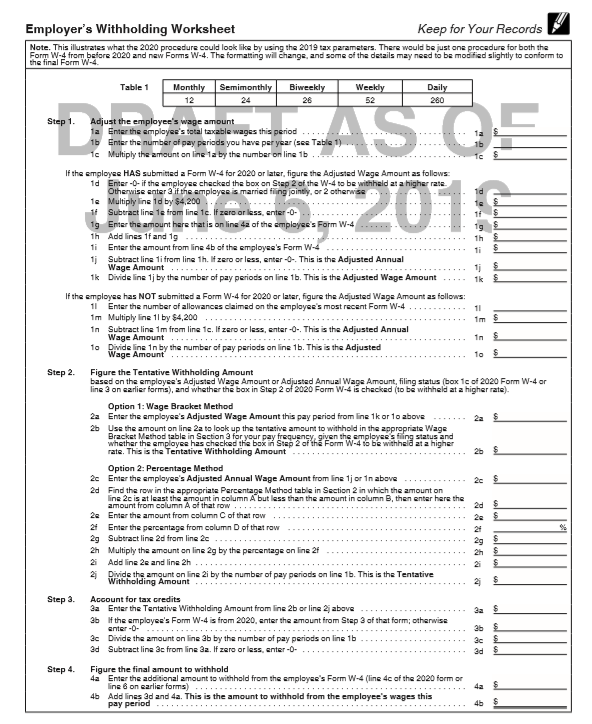

Issue 11: New Publication 15-T Issued in Conjunction with Draft of W-4

The way employers will figure federal income tax withholding for 2020 Form W-4, Employee’s Withholding Allowance

Certificate, is changing to match the changes to the new form. This special draft release of new Pub. 15-T contains a first look at the new employer steps to figure federal income tax withholding. The calculation of withholding for Form W-4 submitted prior to 2020 is unchanged from prior years, but this publication describes how to compute withholding for 2020 and earlier Forms W-4 as one procedure.

The 2020 Form W-4 has been redesigned to reduce the form’s complexity and to increase transparency and accuracy in the withholding system. Beginning with the 2020 Form W-4, employees will no longer be able to request adjustments to their withholding using withholding allowances. Instead, using the new Form W-4, employees will provide employers with amounts to increase or reduce taxes and amounts to increase or decrease the amount of wage income subject to income tax withholding. The computation described in the Employer’s Withholding Worksheet will allow employers to figure withholding regardless of whether the employee provided a Form W-4 in an earlier year or will provide a new Form W-4 in 2020.

The 2020 Form W-4 is broken up into steps. Every 2020 Form W-4 employers receive from an employee should show a completed Step 1 (name, address, social security number, and filing status) and a dated signature on Step 5. Employees will complete Steps 2, 3, and/or 4 only if relevant to their personal situation. Steps 2, 3, and 4 show adjustments that will affect withholding calculations. For employees who do not complete any steps other than Step 1 and Step 5, employers will withhold the amount using the appropriate method based on the filing status and wage amounts. We will break this down in a future newsletter.

There is an Employer’s Withholding Worksheet:

Issue 12: H.R. 3151, Taxpayer First Act (As posted on the House Rules Committee website on June 7, 2019)

H.R. 3151 would change many of the rules that govern the Internal Revenue Service (IRS). The aim would be improving customer service and the process for assisting taxpayers with appeals and to combat identity theft and fraud. Provisions of the bill would restrict certain IRS enforcement activities, modify the agency’s organization, change the operations of the U.S. tax court, create an automated system to verify taxpayer information for authorized users, modernize information technology systems in the IRS, and expand the use of electronic information systems within the agency.

One of the issues that may be of concern is the increase in the penalty for tax returns filed more than 60 days after the due date. This portion of the bill is the “revenue raiser” and would change as follows:

- 3201 of Taxpayer’s First Act – Increase in Penalty for Failure to File

The second sentence of subsection (a) of § 6651 is amended by striking “$205” and inserting “$330”. In addition, an inflation adjustment would be attached. The effective date would apply to returns required to be filed after December 31, 2019.

Other portions of the bill include:

- Establishment of Internal Revenue Service Independent Office of Appeals.

- Comprehensive customer service strategy.

- Clarification of equitable relief from joint liability.

- Reform of notice of contact of third parties.

- Public-private partnership to address identity theft refund fraud.

- Identity protection personal identification numbers.

- Single point of contact for tax-related identity theft victims.

- Notification of suspected identity theft.

- Guidelines for stolen identity refund fraud cases.

- Internet platform for Form 1099 filings.

- Uniform standards for the use of electronic signatures for disclosure authorizations to, and other authorizations of, practitioners.

- Prohibition on rehiring any employee of the Internal Revenue Service who was involuntarily separated from service for misconduct.

- Mandatory e-filing by exempt organizations.

- Notice required before revocation of tax-exempt status for failure to file return.

We are monitoring and will provide updates as needed.

Issue 13: IRS Issues Final Regulations on Contributions in Exchange for State or Local Tax Credits

The final regulations require taxpayers to reduce their charitable contribution deductions by the amount of any state or local tax credits they receive or expect to receive on the return.

Treasury Decision 9864 finalizes proposed regulations published Aug. 27, 2018, that were designed to clarify the relationship between state and local tax credits and the federal tax rules for charitable contribution deductions. Over 7,700 written comments were received during the comment period and 25 comments made at the November 2018 public hearing. About 70 % of the comments recommended adopting the proposed regulations without change.

The final regulations, which apply to contributions made after Aug. 27, 2018, and are effective on Aug. 12, 2019, largely adopt the rules in the proposed regulations. Under the final regulations, a taxpayer making payments to an entity eligible to receive tax-deductible contributions must reduce the federal charitable contribution deduction by the amount of any state or local tax credit that the taxpayer receives or expects to receive in return. The regulations also apply to payments made by trusts or decedents’ estates in determining the amount of their charitable contribution deductions.

For example, if a state grants a 70 % state tax credit pursuant to a state tax credit program, and an itemizing taxpayer contributes $1,000 pursuant to that program, the taxpayer receives a $700 state tax credit. A taxpayer who itemizes deductions must reduce the $1,000 federal charitable contribution deduction by the $700 state tax credit, leaving a federal charitable contribution deduction of $300.

The regulations provide exceptions for dollar-for-dollar state tax deductions and for tax credits of no more than 15 % of the amount transferred. Thus, a taxpayer who receives a state tax deduction of $1,000 for a contribution of $1,000 is not required to reduce the federal charitable contribution deduction to take into account the state tax deduction; and a taxpayer who makes a $1,000 contribution is not required to reduce the $1,000 federal charitable contribution deduction if the state or local tax credit received or expected to be received is no more than $150.

The IRS also posted a notice (Notice 2019-12) providing a safe harbor that allows an individual who itemizes deductions to treat, in certain circumstances, payments that are or will be disallowed as charitable contribution deductions under the final regulations as state or local taxes for federal income tax purposes. Eligible taxpayers can use the safe harbor to determine their state and local tax (SALT) deduction on their tax-year 2018 return. Those who have already filed may be able to claim a greater SALT deduction by filing an amended return, Form 1040X, if they have not already claimed the $10,000 maximum amount ($5,000 if married filing separately).

Issue 14: IRS Adds Identity Protection Step to Apply for, View or Change Online Payment Plans

The IRS recently updated its identity verification process to create or access online payment plan accounts to better protect tax information. Here’s what you need to know to apply for, view or change a payment plan. Creating an account has always been fast, secure, easy and free. Your client will need:

- Valid email address.

- Date of birth.

- Social Security number or individual tax identification number.

Information from most recent tax return:

- Name

- Address

- Filing status.

The IRS added one simple identity protection step. Now, your client will need to verify either of the following:

A financial account linked to their name.

A mobile phone number registered in their name.

If they do not have either of these additional items, they can request the IRS mail a verification code to them, which takes about 5 to 10 business days to arrive. If the client already has an account for an online payment plan, Get Transcript, or an Identity Protection PIN (IP PIN), they can login with the same user ID and password.

However, they will need to complete the new verification step, if they haven’t already. They must complete the new step even if they just need to review or change the existing plan. If they choose to verify a financial account, they can use any of the following types of accounts:

- Credit card (no American Express, debit or corporate cards).

- Student loan.

- Home mortgage.

- Home equity loan or line of credit.

- Auto loan.

The IRS only uses this information to verify identity. The card won’t be charged, and your client is not sharing balance or other financial information. If they choose to verify a phone number, the phone must be:

- A mobile phone in their name (family plans may not work).

- Able to receive texts and

- Based in the U.S.

If they have any issues creating or accessing their accounts, they can exit to see offline options.

Issue 15: REG-118425-18 § 199A Rules for Cooperatives and their Patrons

IRS has issued the long awaited regulations for Cooperatives, only 147 pages. Our August 8, 2019 webinar will fill you in on all the specifics.

These proposed regulations provide guidance to cooperatives to which §§ 1381 through 1388 and their patrons regarding the deduction for qualified business income (QBI) under § 199A(a) as well as guidance to specified agricultural or horticultural cooperatives (Specified Cooperatives) and their patrons regarding the deduction for domestic production activities under § 199A(g) of the Code. The proposed regulations also provide guidance on § 199A(b)(7), the rule requiring patrons of Specified Cooperatives to reduce their deduction for QBI under § 199A(a). In addition, these proposed regulations include a single definition of patronage and non patronage under § 1388 of the Code. Finally, these proposed regulations propose to remove the final regulations, and withdraw the proposed regulations that have not been finalized, under former § 199. These proposed regulations affect Cooperatives as well as patrons that are individuals, partnerships, S corporations, trusts, and estates engaged in domestic trades or businesses. Our discussion will center on the patrons who receive the patronage dividends.

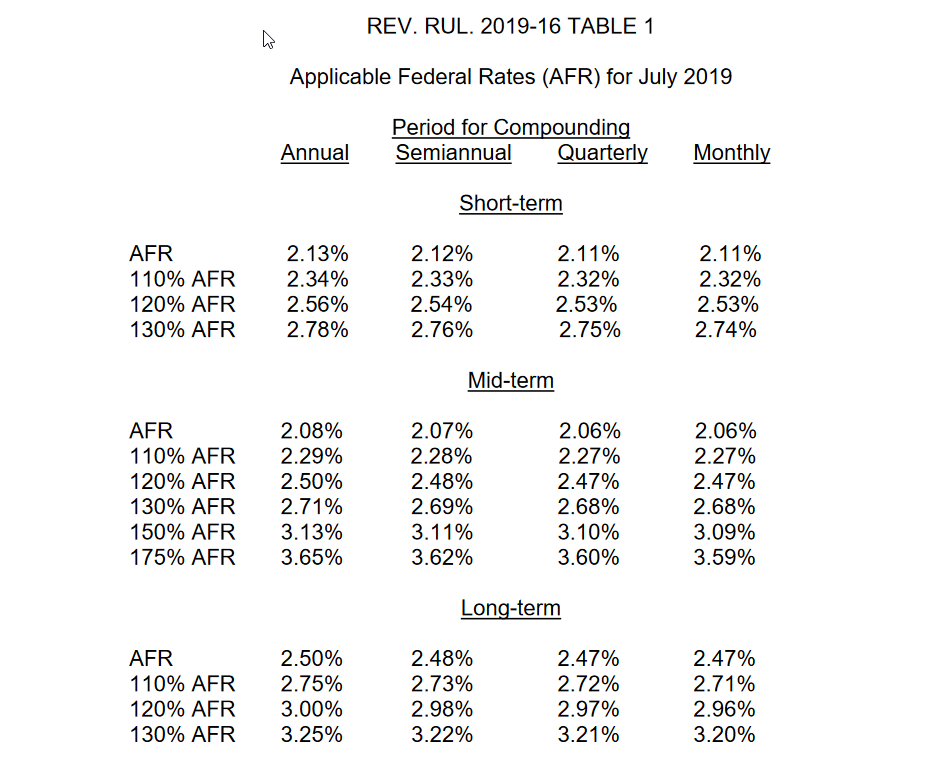

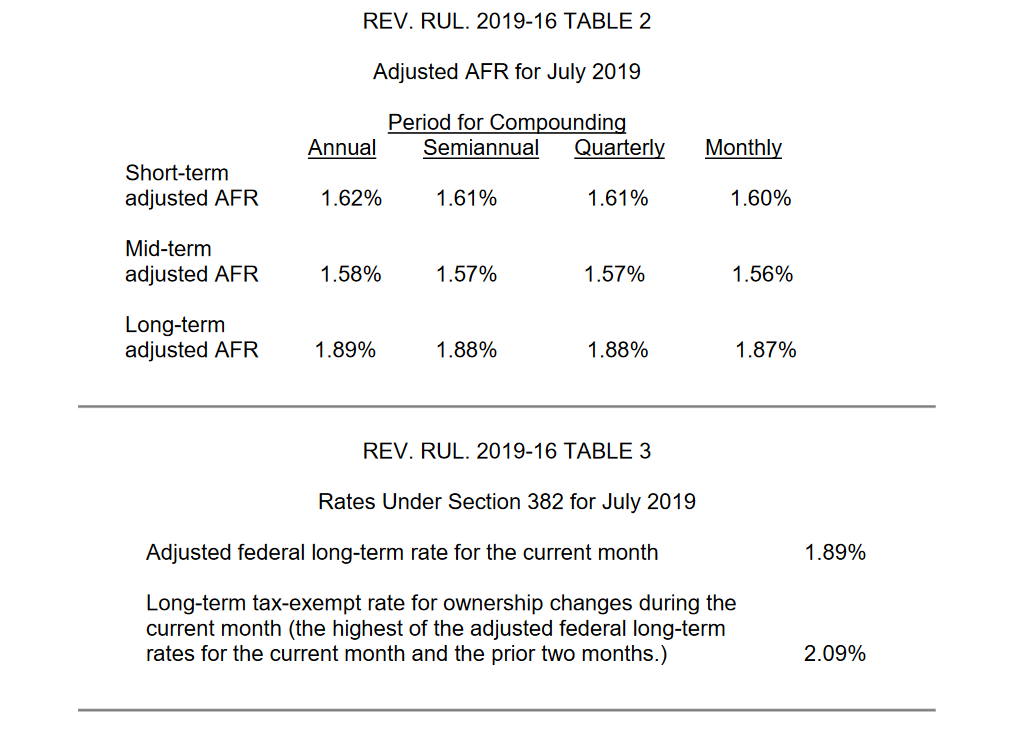

Issue 16: IRS has provided various applicable federal rate tables for July 2019.

July 2019 Webinars Unlimited Package Available: $199

2019 Tax Seminar Dates are Now Available https://www.cpehours.com/dates-locations/