After working for the IRS for 27 years, we would all prepare for the three seasons; tax season, notice season and education season. Audits happen all year long and most of IRS education takes place, when there is a budget, throughout the year. As for us the tax professional, most education begins in June and is in full swing throughout the rest of the year. Both live seminars, webinars and self-study are options we can all manage within our schedules.

This summer, Basics and Beyond is offering numerous Qualified Business Income (QBI) deduction webinars and other tax issues which may impact your client base. See our listing at the end of the newsletter and sign up for those which spark your interest.

As we enter Notice Season several IRS issues will be addressed. Most non-profits returns are due in May, all refunds will attempt to be issued before June 1 to avoid paying interest and the remaining balance due returns will begin processing. In addition, your client could receive a notice of balance due for returns filed just before the deadline and were paid at that time. This often causes a panic among the client population. Just advise them to verify the check has been cashed, or the debit has been made to their account and if so, ignore the notice, for now. If they receive a second notice 6-8 weeks later, they should give IRS a call.

For those who have yet not received their refund, have them check the Where’s My Refund? Application on IRS.gov. Since we are entering Notice Season, our newsletter this month will discuss some of the common notices your clients could receive as well as some new guidance that will impact 2019 returns. In addition, if you do not have a security plan in place now is the time to get this accomplished.

Finally, we continue to monitor the proposed extender legislation, which is in committee, and the new IRS reorganization bills introduced, the Taxpayer First Act of 2019, which has passed the House unanimously on April 9th. The legislation would establish an independent office of appeals within the IRS and require the IRS to submit to Congress plans to redesign the structure of the agency to improve efficiency, modernize technology systems, enhance cybersecurity and better meet taxpayer needs.

The extender legislation package, if passed could impact the 2018 returns as some key provisions such as mortgage insurance premiums, mortgage debt forgiveness and tuition and fees deductions are part of that bill.

In addition, the IRS has hinted that they are still contemplating additional guidance on the Qualified Business Income Deduction (QBI).

Issue 1: Security Message from IRS

Increasingly, there has been a lot of discussion and messaging around the importance of data and information security. It’s because tax professionals are the prime targets for identity thieves and data breaches continue to affect tax professionals at an alarming rate. Cybercriminals use sophisticated and ever evolving techniques to gain access to your systems. These criminals steal sensitive taxpayer data, file fraudulent tax returns and create financial havoc for you and your clients. Data security is a necessity for every tax professional; protecting taxpayer data is your legal responsibility.

While there are many steps you can take to reduce the risk of becoming a victim of cybercriminals, creating and maintaining a data security plan tops the list. The Federal Trade Commission requires all financial institutions (yes, tax return preparers are included in the definition of financial institutions) to have a data security plan. Your plan should be designed to protect all the sensitive taxpayer data entrusted to you as a tax professional. A data security plan is an essential step in protecting your business against data loss and tax related identity theft. A security plan does not guarantee that your business will not be targeted, but it will help you identify what aspects of your business may be vulnerable and how to improve your security posture related to that weakness.

Getting started on a security plan is a challenge for some. Many tax professionals seek the help of a cybersecurity professional to customize a data security plan for their business. Because every business is unique, cybersecurity pros can address your individual business needs and craft a security plan that safeguards both your business and your clients’ data. There is a big market for cybersecurity professionals, but before hiring a cyber pro:

• Ask for recommendations – talk to other tax professionals and business owners for references.

• Be selective – hire a professional that you feel comfortable with and trust discussing the safety and security of your business and your clients.

• Do interviews – ask about their level of experience in data and systems protection, available options for backing up data, experience developing security plans for similar sized businesses, and the scope of monitoring for current and emerging security threats.

• Make it official – secure an agreement or engagement letter that details the terms of each service provided.

The Internal Revenue Service and its Security Summit partners in state government and industry announced new results that show major progress in the fight against tax-related identity theft and added protection for thousands of taxpayers and billions of dollars. Key improvements between 2015 and 2018 include:

• The number of taxpayers reporting they were identity theft victims fell 71 %.

• The number of confirmed identity theft returns stopped by the IRS declined by 54 %.

• The IRS protected a combined $24 billion in fraudulent refunds by stopping the confirmed identity theft returns.

• Financial industry partners recovered an additional $1.4 billion in fraudulent refunds.

Issue 2: Notices in General

The IRS sends notices and letters for the following reasons:

o Balance due.

o Larger or smaller refund.

o Questions about the tax return.

o Verification of identity.

o Additional information is needed.

o A change in the return has occurred.

o Notification of a delay in processing, this can affect the carryforward of a refund to apply to the first estimated tax payment.

Each notice or letter contains information related to the tax return and an issue which may have impacted the processing, a reminder of a balance due or a notification that additional information is needed to finish the processing. In most cases, it will be necessary to respond and provide the information requested. There are good reasons to respond timely as this may, in some cases, minimize additional interest and penalty charges and preserve appeal rights if the client does not agree.

Stress annually, that when a notice or letter is received to notify you immediately.

It’s also important to keep a copy of all notices or letters with the tax records. They may be needed later. This is especially true when IRS failed to apply your election to apply a refund to the first future year estimate. Notice CP 45 will be sent explaining the return has been delayed in processing and they cannot apply the carryforward to the future year. When the client receives the check, void and write IRS asking that they apply to first estimated tax payment.

Location of the Notice or Letter Number

You can find the notice (CP) or letter (LTR) number on either the top or the bottom right-hand corner of the correspondence.

Letter 4888C/5071C

These letters notify the client they have received the federal income tax return, but IRS needs more information to verify the client’s identity in order to process the tax return. This can be for an individual return or for a business. The letter may ask a series of questions to verify the client is the legitimate taxpayer or may ask that the client send them a copy of certain pages from the tax return. A fax number is provided to fax the documents requested. Fax is generally the fastest way to respond and it is important to respond timely, as IRS will delay processing awaiting a response.

CP501/CP502/CP503

Three of the most common notices sent out, a CP501 or CP 502 and sometimes CP 503 alerts the client that they have a past due tax obligation. The notice will provide the balance due, the year, interest that has accrued and the due date for payment.

CP504

The CP504 notice is the last alert to the tax debt before it is turned over to collection. Clients should regard this letter as a warning that the IRS is preparing to garnish income or seize future tax refunds. The levy could impact future state or federal refund until the debt is paid off in full. The Past Due Notice of Intention to Levy CP 504 Notice is intended to get the clients attention when the other notices failed to do so. Once this notice time frame has past the account generally goes into collection status so it is important to get the client on a payment agreement if they cannot pay in full.

CP71C

A CP71C notification reminds the client of a tax debt that may have been overlooked for several years. If the client has not made any payments or contacted the agency to work out an arrangement, they may receive this notice in the mail. At times it is a surprise, and some people assume that since they haven’t received a letter in awhile the debt is forgiven.

CP521

If the client fails to or cannot keep up with their payment agreement, they will receive a CP521 notice in the mail. This notice tells them officially that they have defaulted on the installment agreement, as well as the balance remaining, interest that has accrued and the date that they must remit payment in full. A quick review may be needed to determine

CP 523

This notification comes after the failure to maintain the installment agreement and the IRS plans to garnish wages or seize assets. The client needs to act and contact the IRS to attempt to reinstate the installment agreement.

Reminder: If your client has a current installment agreement for prior years and then owes once again for 2018, they have not met the terms of the installment agreement. IRS will default the agreement and begin to issue the notices mentioned.

Letter 1058 or Letter 11C

Letter 1058 is the final notice of the IRS’ intent to levy. The IRS sends Letter 1058 or LT11 to notify the client of their right to a hearing on the matter and as the final notice of intent to levy property, potentially including paychecks, bank accounts, state income tax refunds and more. It also reminds the client that the agency has the right to search for other assets like bank accounts that it can seize to pay the obligation.

CP90/CP297

This letter also alerts the client to impending levies and garnishments. It may demand payment in full within a 30-day time period. It should also tell the client how to file a Form 12153 and request an appeal hearing.

Letter 3172

Letter 3172 lets the client know that the IRS is moving ahead with seizing assets and property. It stipulates that the agency has the right to sell those assets and use the money to satisfy the debt.

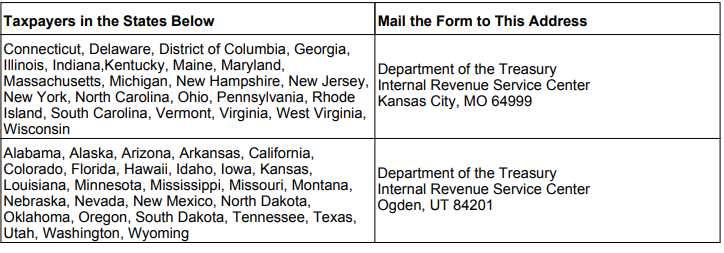

Issue 3: Address Changes for Some Forms – New Mailing Addresses

Addresses for mailing certain forms have changed since the forms were last published. The new mailing addresses are shown below. Mailing address for Forms 706-A, 706-GS(D), 706-GS(T), 706-NA, 706-QDT, 8612, 8725, 8831, 8842, 8892, 8924, 8928:

Department of the Treasury Internal Revenue Service Center Kansas City, MO 64999

Mailing address for Forms 2678, 8716, 8822-B, 8832, 8855:

This update supplements these forms’ instructions. Filers should rely on this update for the changes described, which will be incorporated into the next revision of the forms’ instructions.

Issue 4: Rev. Proc. 2019-15

For individual who must leave a foreign country because of war, civil unrest, or similar adverse conditions in that country, Rev. Proc. 2019-15 adds the Democratic Republic of the Congo, Cuba, Iraq, and Nicaragua to the list of waiver countries for tax year 2018 for which the minimum time requirements are waived. The procedure provides a waiver for the time requirements for individuals electing to exclude their foreign earned income who must leave a foreign country because of war, civil unrest, or similar adverse conditions in that country.

Issue 5: IRS Clarifies Tax Treatment of State and Local Tax Refunds for 2019 and Beyond

The Internal Revenue Service has clarified the tax treatment of state and local tax refunds arising from any year in which the new limit on the state and local tax (SALT) deduction is in effect.

Revenue Ruling 2019-11 provides four examples illustrating how the long-standing tax benefit rule interacts with the new SALT limit to determine the portion of any state or local tax refund that must be included on the taxpayer’s federal income tax return. This does not affect state tax refunds received in 2018 for tax returns currently being filed.

The Tax Cuts and Jobs Act (TCJA), enacted in December 2017, limited the itemized deduction for state and local taxes to $5,000 for a married person filing a separate return and $10,000 for all other tax filers. The limit applies to tax years 2018 to 2025.

As in the past, state and local tax refunds are not subject to tax if a taxpayer chose the standard deduction for the year in which the tax was paid. But if a taxpayer itemized deductions for that year on Schedule A, Itemized Deductions, part or all the refund may be subject to tax, to the extent the taxpayer received a tax benefit from the deduction.

Taxpayers who are impacted by the SALT limit—those taxpayers who itemize deductions and who paid state and local taxes in excess of the SALT limit—may not be required to include the entire state or local tax refund in income in the following years 2019-2025. A key part of that calculation is determining the amount the taxpayer would have deducted had the taxpayer only paid the actual state and local tax liability—that is, no refund and no balance due.

Situation 1: Matthew a single taxpayer paid local real property taxes of $4,000 and state income taxes of $5,000 in 2018. His state and local tax deduction was not limited by § 164(b)(6) because it was below $10,000. Including other allowable itemized deductions, he claimed a total of $14,000 in itemized deductions on his 2018 federal income tax return. In 2019, Matthew received a $1,500 state income tax refund due to an overpayment of state income taxes in 2018. Matthew received a tax benefit from the overpayment of $1,500 in state income tax in 2018. Thus, he is required to include the entire $1,500 state income tax refund in his gross income in 2019. Had Matthew taken the standard deduction; no tax benefit would have incurred?

Situation 2: Bonnie paid local real property taxes of $5,000 and state income taxes of $7,000 in 2018. § 164(b)(6) limited her state and local tax deduction on her 2018 federal income tax return to $10,000, so Bonnie could not deduct $2,000 of the $12,000 state and local taxes paid. Including other allowable itemized deductions, Bonnie claimed a total of $15,000 in itemized deductions on her 2018 federal income tax return. In 2019, she received a $750 state income tax refund due to her overpayment of state income taxes in 2018. In this situation the state income tax refund not includable. In 2019, Bonnie received a $750 refund of state income taxes paid in 2018. Had she paid only the proper amount of state income tax in 2018, her state and local tax deduction would have remained the same ($10,000) and her itemized deductions would have remained the same ($15,000). Bonnie received no tax benefit from the overpayment of $750 in state income tax in 2018. Thus, she is not required to include the $750 state income tax refund in her gross income in 2019.

Situation 3: Charles paid local real property taxes of $5,000 and state income taxes of $6,000 in 2018. § 164(b)(6) limited his state and local tax deduction on the 2018 federal income tax return to $10,000, so he could not deduct $1,000 of the $11,000 state and local taxes paid. Including other allowable itemized deductions, Charles claimed a total of $15,000 in itemized deductions on his 2018 federal income tax return. In 2019, he received a $1,500 state income tax refund due to the overpayment of state income taxes in 2018. In this situation, the state income tax refund partially includable. In 2019, he received a $1,500 refund of state income taxes paid in 2018. Had he paid only the proper amount of state income tax in 2018, his state and local tax deduction would have been reduced from $10,000 to $9,500 and as a result, Charles’s itemized deductions would have been reduced from $15,000 to $14,500, a difference of $500. He received a tax benefit from $500 of the overpayment of state income tax in 2018. Thus, Charles is required to include $500 of his state income tax refund in his gross income in 2019.

Situation 4: Dani paid local real property taxes of $4,250 and state income taxes of $6,000 in 2018. § 164(b)(6) limited her state and local tax deduction on the 2018 federal income tax return to $10,000, so she could not deduct $250 of the $10,250 state and local taxes paid. Including other allowable itemized deductions, Dani claimed a total of $12,500 in itemized deductions on her 2018 federal income tax return. In 2019, Dani received a $1,000 state income tax refund due to her overpayment of state income taxes in 2018. Had she paid only the proper amount of state income tax in 2018, Dani’s state and local tax deduction would have been reduced from $10,000 to $9,250, and, as a result, her itemized deductions would have been reduced from $12,500 to $11,750, which is less than the standard deduction of $12,000 that she would have taken in 2018. The difference between Dani’s claimed itemized deductions ($12,500) and the standard deduction she could have taken ($12,000) is $500. She received a tax benefit from $500 of the overpayment of state income tax in 2018. Thus, Dani is required to include $500 of the state income tax refund in her gross income in 2019.

The ruling has no impact on state or local tax refunds received in 2018 and reportable on 2018 returns taxpayers are filing this season.

Issue 6: Revised 2019 Form 656 Booklet, Offer in Compromise, Online March 25

The 2019 revision of the Form 656 Booklet, Offer in Compromise (OIC) is now available for download on IRS.gov. The booklet contains current forms and instructions for submitting an OIC. Using previous versions of the booklet may result in delayed processing of OIC applications. Use the OIC Pre-Qualifier Tool to confirm that the client is eligible for an OIC and to calculate a preliminary offer amount.

Issue 7: New W-4 Draft to Be Released in Early June 19

Another draft version of a new W-4 will be released in early June 2019. After the complex “first draft “which was eventually “trashed” due to the complexity, IRS will attempt another revision based on comments received from the public as well as the tax professional community. What IRS doesn’t seem to understand is that most people never understood the current form and basically relied on what the employer advised or what others suggested. A few fine points we would all do well to remember and pass on to our employer clients:

• An employer should never help an individual fill out the W-4.

• It is the employee’s responsibility to fill out and file with the employer.

• Individuals do not fully understand what the “exempt” box entails.

• An employer has 30 days to place a new W-4 into operation.

Depending on the complexity of the new W-4, it may come to pass that we as tax professionals should consider performing a W-4 checkup based on the NEW FORM. An additional service, that will save the taxpayer owing and us trying to explain why they owe. With the Qualified Business Income Deduction we are all struggling with this year, for which many of us raised our prices, a quick W-4 Checkup along with the preparation of the 2019 tax return is a bit extra to help with rising costs and complexities we have to deal with annually, and gives a freebie making the customer feel he received more for his dollar.

Myth: Getting a refund this year means there’s no need to adjust withholding for 2019.

Annual tax planning is for everyone. To help avoid an unexpected tax outcome next year, the client should make changes now to prepare for the filing of the 2019 tax return. This can mean adjusting tax withholding with their employer or increasing estimated or additional tax payments.

Checking withholding is important every year, and the IRS encourages people to do a Paycheck Checkup. This is especially important for anyone who got an unexpected result from filing their tax return this year because they had too much or too little withheld from their paycheck in 2018.

Once the form is released, watch the newsletter for an update on what has changed.

Issue 8: Chief Counsel Advice 201912001 – “Self-employed” Health Insurance Deduction for Employee Family Members of 2% Shareholders – This advice may not be used or cited as precedent.

Whether an individual who is a 2 % shareholder of an S corporation pursuant to the attribution of ownership rules under § 318 is entitled to the deduction under § 162(l) for amounts that are paid by the S corporation under a group health plan for all employees and included in the individual’s gross income, if the individual otherwise meets the requirements of § 162(l).

An individual who is a 2 % shareholder of an S corporation pursuant to the attribution of ownership rules under § 318 is entitled to the deduction under § 162(l) for amounts that are paid by the S corporation under a group health plan for all employees and included in the individual’s gross income, if the individual otherwise meets the requirements of § 162(l).

Facts of the Question

An individual owns 100% of an S corporation, which employs the individual’s family member. The family member is considered to be a 2 % shareholder pursuant to the attribution of ownership rules under § 318. The S corporation provides a group health plan for all employees, and the amounts paid by the S corporation under such group health plan are included in the family member’s gross income.

Issue 9: Curious Question of the Month – If the client mails the estimates in a big envelope it takes longer to cash the check. Why is that?

Big envelopes cannot be opened by the sanding machines, yes, they open normal envelopes with high blasted sand. Anyway, the big envelopes have to go to special processing and be opened by hand. If they went through the sand machines, the electric eye lets IRS know if there is a check inside due to the type of ink on the check and the envelope is popped out for fast processing. When hand processed, no scanning. This is not something to recommend to client’s – that they send in big envelopes. The best way to pay is electronically, less chance of check getting lost, credited to the wrong taxpayer or worse credited to the wrong year of tax period.

Issue 10: Correction to 2018 Instructions for Form 1065, U.S. Return of Partnership Income

Several updates and corrections to the 2018 Instructions for Form 1065 are being made, as follows.

(1) On page 6, the late filing penalty should be $200 (not $210) per month for each month or part of a month the failure to file continues.

(2) On page 27, the paragraph headed “Taxpayer identification numbers (TINs) of partnership representatives and designated individuals” is not valid. Instead, on Form 1065, under Designation of Partnership Representative, taxpayers may enter all 0s (examples: 00-0000000 or 000-00-0000) for the TIN of the partnership representative (PR) or designated individual (DI). A preparer tax identification number (PTIN) or centralized authorization file (CAF) number may not be used as a TIN to designate a PR or DI.

(3) On page 30, under Item L. Partner’s Capital Account Analysis, the partnership is instructed that if it reports other than tax basis capital accounts to its partners on Schedule K-1 in Item L, and tax basis capital, if reported on any partner’s Schedule K-1 at the beginning or end of the tax year would be negative, the partnership must report on line 20 of Schedule K-1, using code AH, each partner’s beginning and ending shares of tax basis capital, and this is in addition to the required reported in Item L of Schedule K-1. See Notice 2019-20.

Issue 11: IRS Issues Guidance Providing Safe Harbor for Trades of Player and Staff-member Contracts and Draft Picks

The Internal Revenue Service issued guidance that provides a safe harbor allowing professional sports teams to treat certain player and staff-member contracts and draft picks as having a zero value for determining gain or loss to be recognized on the trade of a player or staff-member contract or a draft pick.

Historically it has been difficult for professional sports teams to assign a monetary value to contracts or draft picks due to the fluctuating nature of the performance of players and staff members, and market conditions. This guidance allows professional sports teams to avoid having to value their player contracts, staff-member contracts, and draft picks to determine the amount of any gain or loss to be recognized. A team using the safe harbor recognizes gain only if cash is received in the trade. Revenue Procedure 2019-18.

Issue 12: Information Letter 2018-033, Office of Chief Counsel, September 28, 2018, IRS Lists Situations in Which Employer May Recoup an HSA Contribution

This letter responds to a request for information concerning mistaken contributions to a Health Savings Account (HSA). § 223(d)(1)(E) of the Internal Revenue Code provides that the interest of an individual in the balance in an HSA is nonforfeitable.

Questions and Answers 23, 24, and 25 of IRS Notice 2008-59, clarified certain limited circumstances under which an employer may recoup contributions to an employee’s HSA.

Question and Answer 23 states that if an employee was never an eligible individual under § 223(c), then an HSA never existed, and the employer may correct the error. In particular, at the employer’s option, the employer may request that the financial institution return to the employer the amounts mistakenly contributed to the employee’s HSA.

Question and Answer 24 states that if an employer contributes amounts to an employee’s HSA that exceed the maximum annual contribution allowed in § 223(b) due to an error, the employer may correct the error. In that case, at the employer’s option, the employer may request that the financial institution return the excess amounts to the employer. However, Question and Answer 24 further provides that if the amounts contributed are less than or equal to the maximum annual contribution allowed in § 223(b), the employer may not recoup any amount from the employee’s HSA even though the employer claims certain contributions were made in error.

Question and Answer 25 clarifies that notwithstanding the ability to recoup contributions if the employee was never an eligible individual or if the amount exceeds the maximum contribution allowed under § 223(b), if an employer contributes to the HSA of an employee who ceases to be an eligible individual during a year, the employer may not recoup any amounts that the employer contributed after the employee ceased to be an eligible individual.

Notice 2008-59 does not specifically address other situations in which contributions to an employee’s HSA are the result of the employer’s or trustee’s administrative or process errors, but the notice also was not intended to provide an exclusive set of circumstances in which an employer may request the return of contributed amounts. Rather if there is clear documentary evidence demonstrating that there was an administrative or process error, an employer may request that the financial institution return the amounts to the employer, with any correction putting the parties in the same position that they would have been in had the error not occurred. Employers should maintain documentation to support their assertion that a mistaken contribution occurred.

Outside of the specific situations described in Notice 2008-59, some examples of the type of errors which may be corrected under the standard described above include:

• An amount withheld and deposited in an employee’s HSA for a pay period that is greater than the amount shown on the employee’s HSA salary reduction election.

• An amount that an employee receives as an employer contribution that the employer did not intend to contribute but was transmitted because an incorrect spreadsheet is accessed or because employees with similar names are confused with each other.

• An amount that an employee receives as an HSA contribution because it is incorrectly entered by a payroll administrator (whether in-house or third-party) causing the incorrect amount to be withheld and contributed.

• An amount that an employee receives as a second HSA contribution because duplicate payroll files are transmitted.

• An amount that an employee receives as an HSA contribution because a change in employee payroll elections is not processed timely so that amounts withheld and contributed are greater than (or less than) the employee elected.

• An amount that an employee receives because an HSA contribution amount is calculated incorrectly, such as a case in which an employee elects a total amount for the year that is allocated by the system over an incorrect number of pay periods. •An amount that an employee receives as an HSA contribution because the decimal position is set incorrectly resulting in a contribution greater than intended.

Issue 13: Revenue Procedure 2019-19 – IRS Updates Retirement Plan Correction Programs

The IRS has expanded the use of the Self-Correction Program (SCP) to permit correction of certain Plan Document Failures and certain plan loan failures, including the ability to correct defaulted plan loans, the failure to obtain spousal consent on a plan loan, and permitting plan loans that exceed the number of plan loans permitted under the terms of the plan.

Issue 14: The SECURE Act – Setting Every Community Up for Retirement Enhancement Act of 2019

On April 2nd the 116th Congress’ most powerful committee in the US House of Representatives, the House Ways & Means Committee, advanced a powerful pice of retirement reform legislation (unanimously).

What’s in the SECURE Act?

From a number of bipartisan bills that were introduced last Contress, but never enacted, the estimated $16 billion SECURE Act, among other things, would:

• increase the auto enrollment safe harbor cap;

• simplify safe harbor 401(k) rules;

• increase the tax credit for small employer plan start-up costs;

• provide portability of lifetime income options;

• allow long-term part-time workers to participate in 401(k) plans;

• allow plans adopting by the filing due date to be treated as in effect as of close of year;

• provide a fiduciary safe harbor for selection of lifetime income provider;

• modify the treatment of custodial accounts on termination of section 403(b) plans;

• require disclosures regarding lifetime income; and

• modify the nondiscrimination rules to protect longer service participants.

For a deeper dive in the details of the bill, we provide the following –

TITLE I: Expanding and Preserving Retirement Savings

Section 101. Expand Retirement Savings by Increasing the Auto Enrollment Safe Harbor Cap

The legislation increases the cap from 10% to 15% of employee pay that required automatic escalation of employee deferrals go no higher than under an automatic enrollment safe harbor plan.

Section 102. Simplification of Safe Harbor 401(k) Rules

The legislation changes the nonelective contribution 401(k) safe harbor to provide greater flexibility, improve employee protection and facilitate plan adoption. The legislation eliminates the safe harbor notice requirement, but maintains the requirement to allow employees to make or change an election at least once per year. The bill also permits amendments to nonelective status at any time before the 30th day before the close of the plan year. Amendments after that time would be allowed if the amendment provides (1) a nonelective contribution of at least 4% of compensation (rather than at least 3%) for all eligible employees for that plan year, and (2) the plan is amended no later than the last day for distributing excess contributions for the plan year, that is, by the close of following plan year.

Sec. 103. Increase Credit Limitation for Small Employer Pension Plan Start-Up Costs

Increasing the credit for plan start-up costs will make it more affordable for small businesses to set up retirement plans. The legislation increases the credit by changing the calculation of the flat dollar amount limit on the credit to the greater of (1) $500 or (2) the lesser of (a) $250 multiplied by the number of non-highly compensated employees of the eligible employer who are eligible to participate in the plan or (b) $5,000. The credit applies for up to three years.

Section 104. Small Employer Automatic Enrollment Credit

Automatic enrollment is shown to increase employee participation and higher retirement savings. The legislation creates a new tax credit of up to $500 per year to employers to defray startup costs for new §401(k) plans and SIMPLE IRA plans that include automatic enrollment. The credit is in addition to the plan start-up credit allowed under present law and would be available for three years. The credit would also be available to employers that convert an existing plan to an automatic enrollment design.

Section 105. Treat Certain Taxable Non-Tuition Fellowship and Stipend Payments as Compensation for IRA Purposes

Stipends and non-tuition fellowship payments received by graduate and postdoctoral students are not treated as compensation and cannot be used as the basis for IRA contributions. The legislation removes this obstacle to retirement savings by taking such amounts that are includible in income into account for IRA contribution purposes. The change will enable these students to begin saving for retirement and accumulate tax-favored retirement savings.

Section 106. Repeal of Maximum Age for Traditional IRA Contributions

The legislation repeals the prohibition on contributions to a traditional IRA by an individual who has attained age 70½. As Americans live longer, an increasing number continue employment beyond traditional retirement age.

Section 107. Qualified Employer Plans Prohibited from Making Loans through Credit Cards and Other Similar Arrangements

The legislation prohibits the distribution of plan loans through credit cards or similar arrangements. The change will ensure that plan loans are not used for routine or small purchases, thereby preserving retirement savings.

Section 108. Portability of Lifetime Income Options

The legislation permits qualified defined contribution plans, §403(b) plans, or governmental §457(b) plans to make a direct trustee-to-trustee transfer to another employer-sponsored retirement plan or IRA of lifetime income investments or distributions of a lifetime income investment in the form of a qualified plan distribution annuity, if a lifetime income investment is no longer authorized to be held as an investment option under the plan. The change will permit participants to preserve their lifetime income investments and avoid surrender charges and fees.

Section 109. Treatment of Custodial Accounts on Termination of §403(b) Plans

Under the provision, not later than six months after the date of enactment, Treasury will issue guidance under which if an employer terminates a §403(b) custodial account, the distribution needed to effectuate the plan termination may be the distribution of an individual custodial account in kind to a participant or beneficiary. The individual custodial account will be maintained on a tax-deferred basis as a §403(b) custodial account until paid out, subject to the §403(b) rules in effect at the time that the individual custodial account is distributed. The Treasury guidance shall be retroactively effective for taxable years beginning after December 31, 2008.

Section 110. Clarification of Retirement Income Account Rules Relating to Church-Controlled

Organizations

The legislation clarifies individuals that may be covered by plans maintained by church controlled organizations. Covered individuals include duly ordained, commissioned, or licensed ministers, regardless of the source of compensation; employees of a tax-exempt organization, controlled by or associated with a church or a convention or association of churches; and certain employees after separation from service with a church, a convention or association of churches, or an organization described above.

Section 111. Allowing Long-term Part-time Workers to Participate in 401(k) Plans

Under current law, employers generally may exclude part-time employees (employees who work less than 1,000 hours per year) when providing a defined contribution plan to their employees. As women are more likely than men to work part-time, these rules can be quite harmful for women in preparing for retirement. Except in the case of collectively bargained plans, the bill will require employers maintaining a 401(k) plan to have a dual eligibility requirement under which an employee must complete either a one year of service requirement (with the 1,000-hour rule) or three consecutive years of service where the employee completes at least 500 hours of service. In the case of employees who are eligible solely by reason of the latter new rule, the employer may elect to exclude such employees from testing under the nondiscrimination and coverage rules, and from the application of the top-heavy rules.

Section 112. Penalty-free Withdrawals from Retirement Plans for Individuals in Case of Birth or Adoption

The legislation provides for penalty-free withdrawals from retirement plans for any “qualified birth or adoption distributions.”

Section 113. Increase in Age for Required Beginning Date for Mandatory Distributions

Under current law, participants are generally required to begin taking distributions from their retirement plan at age 70½. The policy behind this rule is to ensure that individuals spend their retirement savings during their lifetime and not use their retirement plans for estate planning purposes to transfer wealth to beneficiaries. However, the age 70½ was first applied in the retirement plan context in the early 1960s and has never been adjusted to take into account increases in life expectancy. The bill increases the required minimum distribution age from 70½ to 72.

Section 114. Community Newspapers Pension Funding Relief

Community newspapers are generally family-owned, non-publicly traded, independent newspapers. This provision provides pension funding relief for community newspaper plan sponsors by increasing the interest rate to calculate those funding obligations to 8%. Additionally, this bill provides for a longer amortization period of 30 years from 7 years. These two changes would reduce the annual amount struggling community newspaper employers would be required to contribute to their pension plan.

Section 115. Treating Excluded Difficulty of Care Payments as Compensation for Determining

Retirement Contribution Limitations

Many home healthcare workers do not have a taxable income because their only compensation comes from “difficulty of care” payments exempt from taxation under §131. Because such workers do not have taxable income, they cannot save for retirement in a defined contribution plan or IRA. This provision would allow home healthcare workers to contribute to a plan or IRA by amending §§415(c) and 408(o) to provide that tax exempt difficulty of care payments are treated as compensation for purposes of calculating the contribution limits to defined contribution plans and IRAs.

TITLE II: Administrative Improvements

Section 201. Plans Adopted by Filing Due Date for Year May Be Treated as in Effect as of Close of Year

The legislation permits businesses to treat qualified retirement plans adopted before the due date (including extensions) of the tax return for the taxable year to treat the plan as having been adopted as of the last day of the taxable year. The additional time to establish a plan provides flexibility for employers that are considering adopting a plan and the opportunity for employees to receive contributions for that earlier year and begin to accumulate retirement savings.

Section 202. Combined Annual Reports for Group of Plans

The legislation directs the IRS and DOL to effectuate the filing of a consolidated Form 5500 for similar plans. Plans eligible for consolidated filing must be defined contribution plans, with the same trustee, the same named fiduciary (or named fiduciaries) under ERISA, and the same administrator, using the same plan year, and providing the same investments or investment options to participants and beneficiaries. The change will reduce aggregate administrative costs, making it easier for small employers to sponsor a retirement plan and thus improving retirement savings.

Section 203. Disclosure Regarding Lifetime Income

The legislation requires benefit statements provided to defined contribution plan participants to include a lifetime income disclosure at least once during any 12-month period. The disclosure would illustrate the monthly payments the participant would receive if the total account balance were used to provide lifetime income streams, including a qualified joint and survivor annuity for the participant and the participant’s surviving spouse and a single life annuity. The Secretary of Labor is directed to develop a model disclosure. Disclosure in terms of monthly payments will provide useful information to plan participants in correlating the funds in their defined contribution plan to lifetime income. Plan fiduciaries, plan sponsors, or other persons will have no liability under ERISA solely by reason of the provision of lifetime income stream equivalents that are derived in accordance with the assumptions and

guidance under the provision and that include the explanations contained in the model disclosure.

Section 204. Fiduciary Safe Harbor for Selection of Lifetime Income Provider

The legislation provides certainty for plan sponsors in the selection of lifetime income providers, a fiduciary act under ERISA. Under the bill, fiduciaries are afforded an optional safe harbor to satisfy the prudence requirement with respect to the selection of insurers for a guaranteed retirement income contract and are protected from liability for any losses that may result to the participant or beneficiary due to an insurer’s inability in the future to satisfy its financial obligations under the terms of the contract. Removing ambiguity about the applicable fiduciary standard eliminates a roadblock to offering lifetime income benefit options under a defined contribution plan.

Section 205. Modification of Nondiscrimination Rules to Protect Older, Longer Service

Participation

The legislation modifies the nondiscrimination rules with respect to closed plans to permit existing participants to continue to accrue benefits. The modification will protect the benefits for older, longer service employees as they near retirement.

TITLE III: Other Benefits

Section 301. Benefits for Volunteer Firefighters and Emergency Medical Responders

The legislation reinstates for one year the exclusions for qualified State or local tax benefits and qualified reimbursement payments provided to members of qualified volunteer emergency response organizations and increases the exclusion for qualified reimbursement payments to $50 for each month during which a volunteer performs services.

Section 302. Expansion of Section 529 Plans

The legislation expands §529 education savings accounts to cover costs associated with registered apprenticeships; homeschooling; up to $10,000 of qualified student loan repayments (including those for siblings); and private elementary, secondary, or religious schools.

TITLE IV: Revenue Provisions

Section 401. Modifications to Required Minimum Distribution Rules

The legislation modifies the required minimum distribution rules with respect to defined contribution plan and IRA balances upon the death of the account owner. Under the legislation, distributions to individuals other than the surviving spouse of the employee (or IRA owner), disabled or chronically ill individuals, individuals who are not more than 10 years younger than the employee (or IRA owner), or child of the employee (or IRA owner) who has not reached the age of majority are generally required to be distributed by the end of the tenth calendar year following the year of the employee or IRA owner’s death.

Section 402. Increase in Penalty for Failure to File

The legislation increases the failure to file penalty to the lesser of $400 or 100 % of the amount of the tax due. Increasing the penalties will encourage the filing of timely and accurate returns which, in turn, will improve overall tax administration.

Section 403. Increased Penalties for Failure to File Retirement Plan Returns

The legislation modifies the failure to file penalties for retirement plan returns. The Form 5500 penalty would be modified to $105 per day, not to exceed $50,000. Failure to file a registration statement would incur a penalty of $2 per participant per day, not to exceed $10,000. Failure to file a required notification of change would result in a penalty of $2 per day, not to exceed $5,000 for any failure. Failure to provide a required withholding notice results in a penalty of $100 for each failure, not to exceed $50,000 for all failures during any calendar year. Increasing the penalties will encourage the filing of timely and accurate information returns and statements and the provision of required notices, which, in turn, will improve overall tax administration.

Section 404. Increase Information Sharing to Administer Excise Taxes

The legislation allows the IRS to share returns and return information with the U.S. Customs and Border Protection for purposes of administering and collecting the heavy vehicle use tax.

Issue 15: AICPA Letter to Department of Treasury and IRS on QBI Under IRS §199A (4/9/2019)

On April 9, 2019 the AICPA submitted a letter regarding the guidance relating to the QBI deduction under IRC §199A. In particular the letter addesses the “Safe Harbor for Rental Real Estate”. Issue 15 discussed some of the points addressed by the AICPA.

Overview: To minimize uncertainty related to rental real estate enterprises and IRC §199A, proposed Rev. Proc. under Notice 2019-07 provides a safe harbor for when a rental real estate enterprise is treated as a trade or business under §162 for purposes of §199A. The AICPA seeks additional clarity while also recommending options to reduce taxpayer burden in complying with the provisions.

Recommendations:

1. Allow for aggregation of commercial and residential rental real estate activities;

2. Allow taxpayers that enter into triple net lease arrangements to qualify under the revenue procedure, in situations where the activities of the taxpayer surrounding the triple net lease would otherwise satisfy the requirements outlined in the Rev Proc;

3. Provide clarity around the taxpayer’s use of real property as a residence in which the taxpayer rents a portion and resides in a portion of the real property;

4. Clarify that the time spent by a professional real estate management company would qualify toward the 250-hour requirement;

5. Reduce the 250-hour requirement;

6. Reduce the requirements of contemporaneous documentation as it relates to independent contractors and agents of the taxpayer; and

7. Provide additional clarity around reporting, specify what a taxpayer needs to include in the reporting statement, and remove the signatory requirement.

Stay tuned for more guidance on this matter. During the Federal Bar Association conference held in Washington DC on March 8th of this year, Frank Fisher (Branch 1 Attorney, IRS Office of Associate Chief Counsel (Passthroughs and Special Industries) told attendees, “We are open to additional guidance”. He also noted that there are internal conversions within the agency on whether to issue additional guidance on areas not addressed in [the final] regulations.

Issue 16: North Carolina Department of Revenue v. Kimberley Rice Kaestner 1992 Family Trust

During oral arguments held by the U.S. Supreme Court on April 16th, the justices expressed doubt over North Carolina’s tax scheme involving an in-state beneficiary of an out-of-state trust. Justice Stephen G. Breyer noted that there is something wrong with allowing North Carolina to tax income the beneficiariy may never receive. North Carolina Socicitor General Matthew Sawchak argued that trust beneficiaries are the true owners of trusts and that the beneficiary’s in-state residency provides the necessary minimum contact under the federal due process clause.

The North Carolina Department of Revenue has asked the high Court to reverse a state Supreme Court decision that in-state residency of the trust’s beneficiary did not provide the necessary minimum contacts under the federal due process clause for the state to tax the trust.

This case should be decided in June of this year. It also appears that the South Dakota v. Wayfair may be having an influcence in North Carolina’s continue pursuit of this matter with the Supreme Count.

Issue 17: IRS Explains Effect of Farmer / Fisherman Income Averaging on IRC §199A Deduction (4/23/2019)

On its website, the IRS has explained how farmers are to compute their §199A (QBI) deduction when they use the income averaging method under §1301. IRS states on its website that, “[i]n figuring the amount [of the]… QBI Deduction, income, gains, losses, and deductions from farming or fishing should be taken into account, but only to the extent that deduction is attributable to your farming or fishing business and included in elected farm income on line 2a of Schedule J (Form 1040).”

NOTE: The IRS announcement lacks clarity. That being said, it appears that is is requiring a farmer that elects to use income averaging, to use EFI (elected farm income) to calculate the QBI deduction. The farmer has a choice as to whether to elect income averaging, but once the farmers makes the election, the farmer has to be consistent and use EFI to calculate the QBI deduction as well. This position appears to consistent with §199A(c)(3)(A)(ii).

Issue 18: Predicted SSA Wages Base for 2020

In keeping with Social Security Administration news, the Office of the Chief Actuary (OCA) has projected that the Social Security wage base will increase from $132,900 to $136,800 in 2020. We will see how close they are this fall.

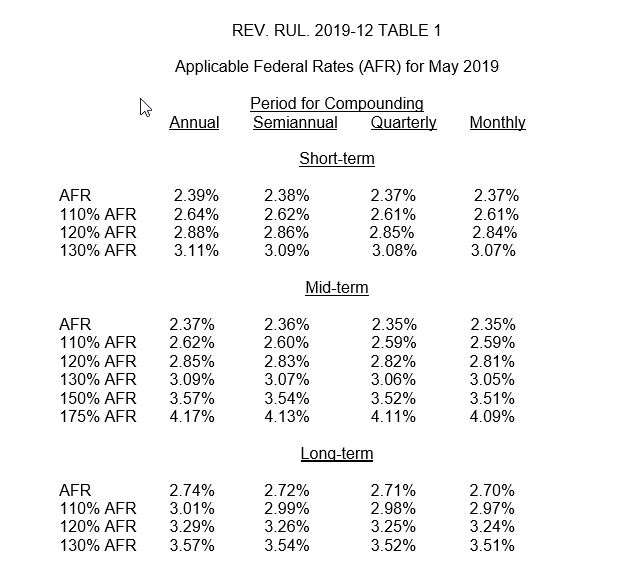

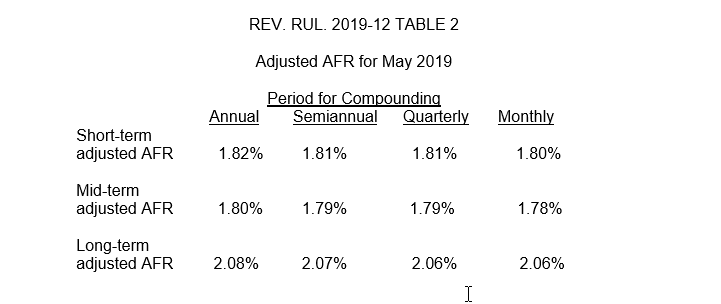

Issue 19: IRS has provided various applicable federal rate tables for May 2019.

2019 Tax Seminar Dates are Now Available

https://www.cpehours.com/dates-locations/

2019 Tax Webinar Schedule is Here!

https://www.cpehours.com/webinar-schedule/

Claudine Raschi, MS.

Program Director

Basics & Beyond

[email protected]

727-210-6600 ext. 103