Tax Season Cheer! The March Tax Newsletter is Here!

We are all knee deep in the 2020 Tax Season so this month we would like to review some items that may be causing difficulties and a reminder of law that is expiring at the end of 2020 which may impact your clients.

Our firm will celebrate HUMP DAY, the half way point through the filing season with a pot luck. Something to consider for your firm. With all the stress of tax season, its nice to spend one hour with each other to relax and enjoy the day.

Basics and Beyond has posted the webinar series for 2020 and extended the Unlimited hours at $199 – a 75% Savings and our Best Value.

We will be introducing on May 13, 2020 our Quarterly Tax Update. We will update you quarterly on tax news and other tax issues and IRS procedures we all need to be aware of. The plus is you can get CPE for this information and at the same time be up to date on the current news. A plus is the fact that three of our instructors will be providing the information and each will discuss issues that may affect your practice. See notice near the end of the newsletter.

March 2020 Issue Headlines:

- Qualified Business Income Deduction – Farmers and Cooperative Reports and Other Issues

- Expiring Provisions at the End of 2020

- The Secure Act – Select Issues

- IRS Increases Visits to High-Income Taxpayers Who Have Not Filed Tax Returns

- Letter 4858, You May Not Have Met Your Due Diligence Requirements

- Treasury, IRS Issues Guidance to Farmers on Uniform Capitalization Rules

- Tips for Working with the Taxpayer Advocate Service

- IRS Adding Seasonal Phone Line Tax Collection Employees

- 7508A(c) and the Application of § 6611(b)(3) and (e), Which Limits Overpayment Interest

- The President’s Budget Proposes to Extend TCJA Estate Tax and Individual Income Tax Cuts

- Business Interest Expense and the §163(j) Limitation

- State Refund Issues

- Secure Act and Disaster

- Rul. 2020-06 – Applicable Federal Rates for March 2020

Issue 1: Qualified Business Income Deduction – Farmers and Cooperative Reports

Not all practitioners have farming clients, but for those who do, confusion still reigns concerning the §199A(g) and the old DPAD under §199.

How do Cooperatives Qualify for the Qualified Business Income Deduction?

Cooperatives do not qualify for the QBI deduction under § 199A(a) but may be eligible to take the § 199A(g) deduction. § 199A(g) provides a deduction for Specified Agricultural or Horticultural Cooperatives (Specified Cooperatives) and their patrons similar to the deduction under former section 199, which was known as the domestic production activities deduction. The IRS issued additional guidance for cooperatives and their patrons on June 18, 2019. Note the §199A(g) is not §199(a) the old DPAD. A farmer can have a qualified trade or business that generates a QBI deduction and could be passed through a § 199A(g) deduction from the Specified Cooperative of which the farmer is a patron. Regardless of whether the § 199A(g) deduction was passed through, the farmer would have to determine whether their QBI deduction is subject to the patron reduction under § 199A(b)(7). The farmer may take any § 199A(g) deduction passed through to the extent of their taxable income determined after their QBI deduction.

What is the § 199A(g) deduction?

§ 199A(g) provides a deduction for Specified Cooperatives and their patrons similar to the deduction under former §199, which was known as the domestic production activities deduction. §199A(g) allows a deduction for income attributable to domestic production activities of Specified Cooperatives. The deduction allowed is equal to 9 % of the lesser of;

- the qualified production activities income (QPAI) or

- the taxable income of the Specified Cooperative for the taxable year. The deduction is further limited to 50 % of the W-2 wages of the Specified Cooperative for the taxable year that are properly allocable.

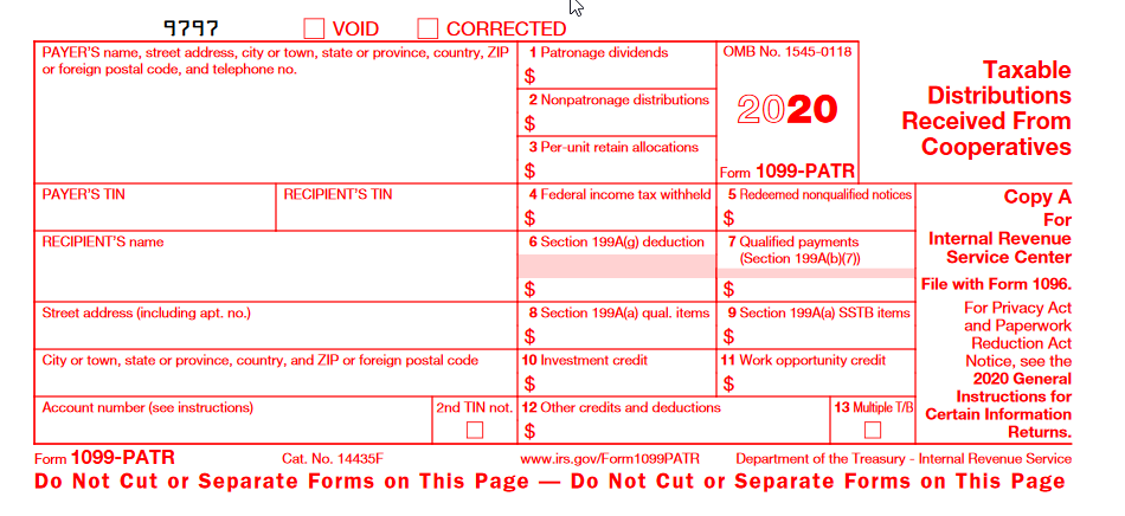

Review your patrons’ statement to check if a §199A(g) amount has passed through. The amount is not detailed on the 2019 PATR but can be identified in an attached statement. Note below, the 2020 PATR does provide specific information for the §199A(g).

Old DPAD §199

The new U.S. tax law (Pub. L. No. 115-97) repealed the DPAD under §199 for tax years beginning after December 31, 2017. As noted in the LB&I directive, claims for the DPAD for 2018 or later years are not to be made unless one of the following situations applies:

- The tax year began before January 1, 2018.

- The DPAD results from being a shareholder or partner in an S corporation or partnership with a tax year that began before January 1, 2018.

- The DPAD results from being a beneficiary of an estate or trust with a tax year that began before January 1, 2018.

- The DPAD results from being a patron of an agricultural or horticultural cooperative with a tax year that began before January 1, 2018.

How do Specified Cooperatives and Their Patrons Handle the §199A(g) Deduction?

Only a Specified Cooperative may calculate the §199A(g) deduction. A Specified Cooperative may pass all, some, or none of the §199A(g) deduction to patrons that are eligible to take the deduction (this does not include a patron that is C corporation, unless that patron is a Specified Cooperative). The Specified Cooperative will reduce its deduction under §1382 by the amount of the §199A(g) deduction that was passed through.

If the Specified Cooperative passes through any of the §199A(g) deduction to a patron that is eligible, that patron is allowed to deduct the amount so long as the deduction does not exceed the patron’s taxable income (after taking into account any QBI deduction allowed to the patron).

How Does a Specified Cooperative Pass Through a §199A(g) Deduction to its Patrons?

Specified Cooperatives may pass through all, some, or none of their allowable §199A(g) deduction to patrons who are eligible taxpayers as defined in §199A(g)(2)(D), that is:

- a patron, that is not a C corporation, or

- a patron that is a Specified Cooperative.

A Specified Cooperative must notify each of its patrons of the amount of §199A(g) deduction being passed to them in a written notice mailed to the patron during the payment period described in §1382(d) and also include any amount passed through in such written notice on the Form 1099-PATR issued to its patrons. The amount of the §199A(g) deduction that a Specified Cooperative can pass through to an eligible taxpayer is limited to the portion of the §199A(g) deduction that is allowed with respect to the QPAI to which the qualified payments made to the patron are attributable.

Individual patrons that receive a written notice from a Specified Cooperative allocating a §199A(g) deduction may take the deduction to the extent of their taxable income determined after their QBI deduction. A §199A(g) deduction that can’t be used in the year it is received is lost.

Other QBI Issues

Do I Need to File Information Returns, Such as Form 1099-MISC, if I Take a QBI Deduction from Income Generated by My Rental Property?

As provided in §6041, persons engaged in a trade or business and making payment in the course of such trade or business to another person of $600 or more in any taxable year may be required to file an information return reflecting the details of such transactions. Application of §199A and its rules do not change any existing requirement for information reporting as provided under §6041.

Do I Have to Materially Participate in the Business to Qualify for the Deduction?

No. Material participation under § 469 is not required for the QBI deduction. Eligible taxpayers with income from a trade or business may be entitled to the QBI deduction(if they otherwise satisfy the requirements of §199A regardless of their involvement in the trade or business.

I Am a Statutory Employee and Report My Income on Schedule C. Does it Qualify for the Qualified Business Income Deduction?

Payments made to statutory employees, as defined in §3121(d)(3), are excluded from the definition of wages and considered income from the trade or business of performing services as an employee under §1.199A-5(d)(1). Items of income, gain, deduction, and loss from performance of services as a statutory employee are considered QBI and are eligible for the QBI deduction to the extent the requirements of §199A are satisfied.

What About Fiscal-Year Pass-Through Entities?

The QBI deduction itself is available only to taxpayers whose tax years begin after December 31, 2017. However, any QBI reported to a taxpayer from a related passthrough entity with a taxable year beginning in 2017 and ending in 2018 is treated as having been incurred in the owner’s taxable year in which the passthrough entity’s taxable year ends.

For example, a calendar year partner in a partnership with a fiscal year end of March 31, 2018, will be able to include the partnership’s QBI for the entire fiscal year in determining the partner’s 2018 QBI deduction. The partner may also use the partnership’s W-2 wages and UBIA of qualified property in computing the deduction, if applicable. Note that the pass-through entity’s 2017 Schedule K-1 does not have the detail relating to the new QBI deduction. The entity should still provide the necessary detail to the owners as an attachment to the Schedule K-1.

The 2020 PATR Taxable Distribution Received from Cooperatives

Issue 2: Expiring Provisions at the End of 2020

Several provisions will expire but few will impact many of our clients. Of course, Congress may extend some provisions but with it being an election year, generally the outlook is bleak for any significant legislation which extenders are often attached to. The following provisions expire at the end of 2020.

I have highlighted some provisions that commonly may impact clients.

- Credit for certain nonbusiness energy property (§25C(g))

- Credit for qualified fuel cell motor vehicles (§30B(k)(1))

- Credit for alternative fuel vehicle refueling property (§30C(g))

- Credit for two-wheeled plug-in electric vehicles (§30D(g)(3)(E)(ii))

- Credit for health insurance costs of eligible individuals (§35(b)(1)(B))

- Second generation biofuel producer credit (§ 40(b)(6)(J))

- Beginning-of-construction date for renewable power facilities eligible to claim the electricity production credit or investment credit in lieu of the production credit (§§45(d) and 48(a)(5))

- Credit for production of Indian coal (§45(e)(10)(A))

- Indian employment credit (§45A(f))

- New markets tax credit (§45D(f)(1))

- Credit for construction of new energy efficient homes (§45L(g))

- Mine rescue team training credit (§45N(e))

- Employer credit for paid family and medical leave (§45S(i))

- Work opportunity credit (§51(c)(4))

- Exclusion from gross income of discharge of indebtedness on principal residence (§108(a)(1)(E))

- Benefits provided to volunteer firefighters and emergency medical responders (§139B(d))

- Treatment of premiums for certain qualified mortgage insurance as qualified residence interest (§163(h)(3)(E)(iv))

- Three-year recovery period for race horses two years old or younger (§168(e)(3)(A))

- Seven-year recovery period for motorsports entertainment complexes (§§168(e)(3)(C)(ii) and (i)(15)(D))

- Accelerated depreciation for business property on an Indian reservation (§168(j)(9))

- Special depreciation allowance for second generation biofuel plant property (§168(l)(2)(D))

- Energy efficient commercial buildings deduction (§179D(h))

- Special expensing rules for certain film, television, and live theatrical productions (§181(g))

- Medical expense deduction: adjusted gross income (AGI) floor 7.5 percent (§213(f))

- Deduction for qualified tuition and related expenses (§222(e))

- Special rule for sales or dispositions by a qualified electric utility to implement Federal Energy Regulatory Commission (“FERC”) or State electric restructuring policy (§451(k)(3))

- Look-through treatment of payments between related controlled foreign corporations under the foreign personal holding company rules (§954(c)(6)(C))

- Empowerment zone tax incentives:

- Designation of an empowerment zone and of additional empowerment zones (§§1391(d)(1)(A)(i) and (h)(2)).

- Empowerment zone tax-exempt bonds (§§1394 and 1391(d)(1)(A)(i)).

- Empowerment zone employment credit (§§1396 and 1391(d)(1)(A)(i)).

- Increased expensing under sec. 179 (§§1397A and 1391(d)(1)(A)(i)).

- Nonrecognition of gain on rollover of empowerment zone investments (§§1397B and 1391(d)(1)(A)(i)).

- Black Lung Disability Trust Fund: increase in amount of excise tax on coal (§4121(e)(2))

- Oil Spill Liability Trust Fund financing rate (§4611(f)(2))

- Provisions modifying the rates of taxation of beer, wine, and distilled spirits, and certain other rules (§§263A(f)(4), 5001, 5041, 5051, 5212, and 5414)

- Incentives for alternative fuel and alternative fuel mixtures:

- Excise tax credits and outlay payments for alternative fuel (§§ 6426(d)(5) and 6427(e)(6)(C)).

- Excise tax credits for alternative fuel mixtures (§6426(e)(3)).

- American Samoa economic development credit (§119 of Pub. L. No. 109-432, as amended)

Issue 3: The Secure Act – Select Issues

On Dec. 20, President Donald J. Trump signed into law the Setting Every Community Up for Retirement Enhancement Act of 2019 (SECURE), the most sweeping legislation affecting retirement savings since the Pension Protection Act passed in 2006. This Act was added as Division O to the Further Consolidated Appropriations Act, 2020 (H.R. 1865). We will cover the Secure Act in our fall and year end seminars and a few webinars this summer. There are a few things you need to be aware of now to better assist your clients for tax planning in 2020 and beyond.

Repeal of Maximum Age for Traditional IRA Contributions. Repeals the prohibition on contributions to a traditional IRA by an individual who has attained age 70½. This provision puts traditional IRAs on par with Roth IRAs, which do not have an age limitation.

Increase in Age for Required Beginning Date for Mandatory Distributions. Increases the required minimum distribution age from 70 ½ to 72 for those who are not 70 ½ by the end of 2019. Conforming amendments were made in the case of a spouse as beneficiary and for owners. This rule also will apply to IRAs and governmental 457(b)plans.

Modifications to Required Minimum Distribution Rules with respect to defined contribution plan and IRA balances upon the death of the account owner – Under current law, if a participant dies before receiving the full distribution from a defined contribution plan, a plan may pay a designated beneficiary the amount over the designated beneficiary’s life. Under the SECURE Act, payment would need to be made within 10 years of the employee’s death, except for payment to a spouse, a minor child (until reaching majority), or an individual that is chronically ill, disabled, or who is not more than 10 years younger than the employee.

Certain Taxable Non-Tuition Fellowship and Stipend Payments Treated as Compensation for IRA Purposes – Under current law, stipend and non-tuition fellowship payments received by graduate and postdoctoral students do not count as eligible compensation to contribute to an Individual Retirement Account (IRA). This provision eliminates this hurdle by allowing these amounts to be treated as eligible compensation to make an IRA contribution.

Penalty-free Withdrawals from retirement plans for Individuals in Case of Birth of Child or Adoption – Under current law, there is an additional 10 % tax penalty on distributions that do not meet certain requirements. The SECURE Act provides that this penalty would not apply to distributions for a qualified birth or adoption, if that distribution does not exceed $5,000 for each birth or adoption. A qualified birth or adoption distribution is any distribution from a plan to an individual within one year of the date of the birth or date of the legal adoption. An eligible adoptee is defined as an individual (other than the child of the taxpayer’s spouse) who is not yet 18 years old or is physically or mentally incapable of self-support. The SECURE Act also would allow an individual to repay any qualified birth or adoption distribution. The details would need to be worked out in the regulations.

Treating Excluded Difficulty of Care Payments as Compensation for Determining Retirement Contribution Limitations – Some home health care workers receive difficulty of care payments to care for certain foster children in their homes. These payments are not includible as income. Home healthcare workers receiving only these payments cannot participate in tax-qualified retirement plans or IRAs because “difficulty of care” payments are not considered compensation or earnings upon which contributions to such plans or IRAs may be made. The SECURE Act amended the Code to consider such payments compensation for purposes of a qualified plan and an IRA.

Expansion of §529 Plans – The Act expands § 529 qualified tuition program accounts to cover costs associated with registered apprenticeship programs including expenses for fees, books, supplies, and equipment required for participation. The Act also provides that principal and interest payments of up to $10,000 over a lifetime, reduced by the amount of distributions so treated for all prior taxable years, will be eligible as qualified higher education expenses.

Increase in Penalty for Failure to File to the lesser of $400 or 100 % of the amount of the tax due.

Issue 4: IRS Increases Visits to High-Income Taxpayers Who Have Not Filed Tax Returns

As part of a larger effort to ensure compliance and fairness, the Internal Revenue Service will step up efforts to visit high-income taxpayers who in prior years have failed to timely file one or more of their tax returns.

Following the recent and ongoing hiring of additional enforcement personnel, IRS revenue officers across the country will increase face-to-face visits with high-income taxpayers who haven’t filed tax returns in 2018 or previous years. These visits are primarily aimed at informing these taxpayers of their tax filing and paying obligations and bringing these taxpayers into compliance.

For the new visits taking place, high-income non-filers taxpayers are those who generally received income in excess of $100,000 during a tax year and did not file a tax return with the IRS. Taxpayers who exercise their best efforts in filing their tax returns and paying or entering into agreements to pay their taxes deserve to know that the IRS is aggressively pursuing others who have failed to satisfy their filing and payment obligations. During the visits, IRS revenue officers will share information and work with the taxpayer to hopefully resolve the tax issue.

Issue 5: Letter 4858, You May Not Have Met Your Due Diligence Requirements

IRS is sending Letter 4858, You May Not Have Met Your Diligence Requirements, to some tax preparers who completed 2019 returns claiming the:

- Head of Household filing status (HoH)

- Earned Income Tax Credit (EITC)

- American Opportunity Tax Credit (AOTC)

- Child Tax Credit/Additional Child Tax Credit (CTC/ACTC)

- Credit for Other Dependents (ODC)

The IRS sends Letter 4858 to remind tax preparers about the importance of meeting due diligence requirements to ensure returns are complete and correct. Disregarding the requirements could result in penalties and other consequences for them and their clients. The penalty is $530 per failure for tax returns filed in 2020.

Issue 6: Treasury, IRS Issues Guidance to Farmers on Uniform Capitalization Rules

Treasury and the Internal Revenue Service issued Revenue Procedure 2020-13 providing procedures for farmers who have elected out of certain capitalization rules and want to apply the small business taxpayer exemption in the same taxable year.

The Tax Cuts and Jobs Act (TCJA) added a provision exempting small business taxpayers from the capitalization rules under § 263A. A taxpayer, other than a tax shelter, qualifies as a small business taxpayer by satisfying the gross receipts test for the taxable year. To satisfy the gross receipts test, a farming business must have gross receipts of $25 million or less for taxable years beginning in 2018, and $26 million or less for taxable years beginning in 2019. Unlike the §263A(d)(3) election, the small business taxpayer exemption does not require the special rules for the use of the Alternative Depreciation System (ADS) or characterization of certain property as §1245 property.

The guidance provides procedures for farmers to revoke their election under §263A(d)(3) and apply the small business taxpayer exemption under §263A(i) in the same taxable year. It also provides procedures for eligible farmers that want to make an election under § 263A(d)(3) in the same taxable year that they no longer qualify as small business taxpayers.

Issue 7: Tips for Working with the Taxpayer Advocate Service

The Taxpayer Advocate Service works in two main ways:

- helping with individual taxpayer problems, and

- recommending “big picture” or systemic changes at the IRS or in the tax laws.

In most instances, federal tax account issues can be resolved by working directly with the IRS. Issues involving State taxes must be worked through the respective State agencies.

Clients’ cases are generally eligible for our help if an IRS problem is causing financial difficulty or if attempts to resolve issues with the IRS fail.

What to Expect When Working with Us

If the case qualifies:

- a case advocate will be assigned for the duration of the case.

- contact will be made within seven days (or less) from the date you contacted us or the date your inquiry was referred to us.

- An estimated completion date will be provided based on the time it takes the IRS to resolve similar issues. Be aware, this is only an estimate and can change depending on IRS actions needed and timely responses to requests for information.

Requests for documentation

- We may require documentation or additional information to resolve the inquiry. If so, we will request it when we call. Your prompt reply will ensure we can continue to advocate for you and your client. If we are continuously unable to reach you by phone or by letter, our office may be required to contact the taxpayer directly or possibly close the case.

Case status updates

- Case advocates are responsible for keeping you informed of their progress throughout the case. However, be aware that we cannot leave tax information on a representative’s answering machine or voicemail, even if requested to do so. You will also be provided with a clear, complete, and correct explanation of what actions were taken to resolve the problem when we are done.

Please understand that in many instances, the Taxpayer Advocate Service must rely on the IRS to take the action needed to resolve the issue. Our role is to ensure that actions are completed accurately and expeditiously and that the taxpayer’s rights have been protected.

How to Contact Us

You can find local office information on our website at https://taxpayeradvocate.irs.gov/contact-us or call us at 1-877-777-4778.

- Please note although we usually work cases by geographic locations, your case may be worked by a TAS office in another state. This will not delay contact or resolution. We are simply ensuring the inventory is spread as evenly as possible across TAS offices to be able to timely work the case.

Issue 8: IRS Adding Seasonal Phone Line Tax Collection Employees

The IRS is adding up to 1,000 seasonal employees at 18 collection call sites to help staff phone lines. These employees will work with taxpayers who are behind on their tax payments and have received a balance due notice. The contact representative positions, which are at the government’s GS-5 level in the IRS Small Business/Self-Employed division, are open now for a brief period. These phone lines can’t be used to answer general filing questions during the 2020 tax season.

Issue 9: § 7508A(c) and the Application of § 6611(b)(3) and (e), Which Limits Overpayment Interest, to Taxpayers Who Qualify for Relief under § 7508A Because of a Presidentially Declared Disaster or Terroristic or Military Actions

Does §7508A(c) provide an exception from the late return rule of §6611(b)(3) and the 45-day rule of §6611(e), which limit the payment of interest on any overpayment, when a taxpayer qualifies for relief under §7508A because of a Presidentially declared disaster or terroristic or military actions?

Yes. Because §7508A(c) incorporates the special rule for overpayments in § 7508(b), neither the late return rule of §6611(b)(3) nor the 45-day rule of §6611(e) applies when a taxpayer qualifies for relief under §7508A.

Example: An individual lives in a county affected by a Presidentially declared natural disaster that began on April 1, 2018. Pursuant to §7508A(a), the Secretary announces that one year will be disregarded for purposes of determining, among other things, whether a return was timely filed for tax year 2017. Specifically, individual taxpayers who reside in the county are granted additional time to file an individual tax return for tax year 2017 until April 15, 2019. An individual taxpayer who was affected by the disaster files its 2017 return on April 15, 2019, one year after the original deadline. The taxpayer made payments through withholding during 2017, which were deemed paid on April 15, 2018, and resulted in an overpayment for tax year 2017 as of that date. The Service pays a refund on May 15, 2019, 30 days after the return was filed.

Conclusion: The Service will pay interest on the overpayment. The 45-day rule of §6611(e) does not bar the payment of interest even though the refund was paid in 30 days. Also, the late return rule of §6611(b)(3) does not limit the time period for which overpayment interest will be calculated even though the return was filed after the original due date and without extension. Interest will be calculated from the date of overpayment (April 15, 2018) until the refund date on May 15, 2019. This includes the one-year period that was disregarded for purposes of determining whether the return was timely filed.

Issue 10: The President’s Budget Proposes to Extend TCJA Estate Tax and Individual Income Tax Cuts

Trump’s – A Budget for America’s Future – Fiscal Year 2021

The budget proposes to extended some of the TCJA provisions through 2035. These include the wealth transfer tax (i.e., estate, gift, etc.) cuts and individual income tax cuts. The TCJA contained provisions that cut tax rates and made other changes to individual income tax rules; these provisions are scheduled to expire for tax years beginning before Jan. 1, 2026. The TCJA also increased the estate/gift tax exclusion to $11 million plus annual cost of living increases for estates of decedents dying and gifts made before Jan. 1, 2026.

Other tax provisions propose:

- $12.0 billion in fiscal year 2021 funding for IRS, providing $300 million to continue IRS efforts to modernize its information technology.

- Funding to digitize more IRS communications to taxpayers so they can respond quickly and accurately to IRS questions.

- Create a call-back function for certain IRS telephone lines so taxpayers do not need to wait on hold to speak with an IRS representative

- Make it easier for taxpayers to make and schedule payments online.

- Improving oversight of paid tax preparers.

- Giving IRS the authority to correct more errors on tax returns before refunds are issued.

- Requiring a valid Social Security Number for work in order to claim certain tax credits

- Increasing wage and information reporting.

We will be monitoring as to what makes it to the final budget approved by Congress. The Joint Committee on Taxation will be preparing a costs and benefits analysis which Congress will use in determining what should be included and excluded in the final approved budget.

Issue 11: Business Interest Expense and the §163(j) Limitation

TCJA significantly changed the § 163(j) limitation. It was generally thought that most tax practitioners would not have to worry much about this, as the requirements seemed that they would not apply to most of their clients. We have found that this issue can raise it head for some of our taxpayers.

Generally, taxpayers can deduct interest expense paid or accrued in the taxable year. However, if § 163(j) applies, the amount of deductible business interest expense in a taxable year cannot exceed the sum of:

- the taxpayer’s business interest income for the year;

- 30% of the taxpayer’s adjusted taxable income (ATI) for the year; and

- the taxpayer’s floor plan financing interest expense for the year.

For tax years beginning after 2017, the limitation applies to all taxpayers who have business interest expense, other than certain small businesses that meet the gross receipts test in §448(c) (“exempt small business”). The limitation does not apply to certain excepted trades or businesses, see below. A business generally meets the gross receipts test of § 448(c) when it is not a tax shelter (as defined in §448(a)(3)) and has average annual gross receipts of $25 million or less in the previous three years. For tax year 2019 and subsequent years, the $25 million amount will be adjusted for inflation. For 2019 the amount has increased to $26 million.

Gross receipts for tax years 2016-2018 will need to be in the software to calculate if the limitation applies. If you have picked up a new client you will need to obtain the information for the limitation to be calculated correctly.

The following are excepted trades or businesses:

- The trade or business of providing services as an employee;

- Certain real property trades or businesses that elect to be excepted;

- Certain farming businesses that elect to be excepted; and

- Certain regulated utility trades or businesses.

An eligible real property trade or business or farming business may elect to be an excepted trade or business by following the procedures outlined in §1.163(j)-9 of the proposed regulations, including the requirement to attach a statement to a timely filed federal income tax return (including any extensions) for the year of election. Review Revenue Procedure 2018-59. An exempt small business is not permitted to make an election to be an excepted trade or business because that taxpayer is already not subject to the §163(j) limitation. Once made, the election is generally irrevocable and binding on the trade or business for all succeeding years. Review §1.163(j)-9 of the proposed regulations for certain circumstances where the election may no longer apply. The statement must include the following information:

- The taxpayer’s name, address, and social security number or employer identification number;

- A description of the electing trade or business, including the principal business activity code; and

- A statement that the taxpayer is making an election as a real property trade or business (under §163(j)(7)(B) or as a farming business (under §163(j)(7)(C)), as applicable.

Business interest expense is any interest expense that is properly allocable to a trade or business. Floor plan financing interest expense is also business interest expense. The interest expense that is properly allocable to an excepted trade or business is not subject to the §163(j) limitation. Similarly, the amount of the items of income, gain, deduction, or loss, including interest income that is properly allocable to an excepted trade or business, is excluded in determining the §163(j) limitation. Therefore, allocate tax items between excepted and non-excepted trades or businesses in order to determine the §163(j) limitation.

- 1.163(j)-10 of the proposed regulations provides special rules for allocating various tax items. You must generally compare the basis in the assets used in the excepted trades or businesses and the basis in the assets used in the non-excepted trades or businesses to determine what portion of interest expense and interest income to allocate to the excepted trades or businesses. In limited cases, tracing of interest expense paid on certain nonrecourse debt may be available.

Are there any consequences I should be aware of in making an election to be an excepted trade or business?

Yes. If you make an election to be an excepted real property trade or business, the following assets that you hold in the electing real property trade or business must be depreciated using the alternative depreciation system (ADS), and are not eligible for a bonus depreciation deduction under §168(k):

- Nonresidential real property;

- Residential rental property; and

- Qualified improvement property.

If you make an election to be an electing farming business, any property with a recovery period of 10 years or more that you hold in the electing farming business must be depreciated using ADS, and such property is not eligible for a bonus depreciation deduction under §168(k).

Treatment of disallowed business interest expense carryforwards

Disallowed business interest expense is the amount of business interest expense for a tax year in excess of the amount allowed as a deduction for that tax year under the §163(j) limit (Prop. Regs. §1.163(j)-1(b)(8)). Disallowed disqualified interest is interest expense, including carryforwards, for which a deduction was disallowed under former §163(j) (which was repealed) in the taxpayer’s last tax year beginning before 2018.

Current-year business interest expense is deducted before any disallowed business interest expense carryforwards are deducted in that year. Disallowed business interest expense carryforwards are then deducted in the order of the tax year in which they occurred.

The §163(j) limit applies before the application of the §465 at-risk, §469 passive activity, and §461(l) excess loss provisions. If a disallowed amount is carried forward to a tax year in which the small business exemption applies to the taxpayer, the limit on business interest expense does not apply to the carryforward amount in that tax year.

Issue 12: State Refund Issues

With the limitation of $10,000 on the Schedule A Taxes we need to be careful when calculating any amount of state tax refund which would be income on Form 1040. If state income taxes are deducted on Schedule A, and then a state issues a refund of some or all of those taxes, the refund may have to be reported as income in the following year. If the total taxes exceed $10,000 not all of the state refund may be taxable. Make sure the software is calculating this issue correctly.

Issue 13: Applicability of Revenue Procedure 84-35 to Partnerships with Taxable Years beginning on or after January 1, 2018 – Program Manager Technical Advice 2020-001

Issues: Whether the relief granted to small partnerships by Revenue Procedure 84-35, relating to the penalty under §6698(a)for failure to file a partnership return, is obsolete. If the revenue procedure is not obsolete, whether Revenue Procedure 84-35 allows the IRS to implement procedures to ensure that partnerships claiming relief under Revenue Procedure 84-35 are in fact entitled to such relief.

Conclusion: Revenue Procedure 84-35 is not obsolete and continues to apply. The reference to § 6231(a)(1)(B) contained in the revenue procedure is a means by which to define small partnerships for the purpose of the relief provided by the revenue procedure. The repeal of the small partnership exception in §6231(a)(1)(B) does not affect the scope of the penalty under §6698for failure to file a partnership return. Revenue Procedure 84-35 allows the IRS to implement procedures requiring partnerships claiming relief under Revenue Procedure 84-35 to demonstrate that they are entitled to this relief.

Issue 14: Secure Act and Disaster

A disaster relief provision, which was not originally part of SECURE, was added as Division Q under the 2020 budget bill. It will apply with respect to major disasters, as declared by the President under federal law, during the period beginning January 1, 2018, and ending 60 days after the date of enactment.

Under this provision, “qualified disaster distributions” of up to $100,000 are exempt from the premature distribution penalty tax under §72(t); they may be rolled back into a qualified plan or IRA for up to 3 years after the distribution; and they may be included in income ratably over the 3-year period beginning in the year of the distribution.

A “qualified disaster distribution” is a distribution made to an individual who suffered an economic loss and whose principal residence is located in a qualified disaster zone during the period of the disaster (as specified by the Federal Emergency Management Agency (FEMA)).

In addition, the participant loan limit is increased for these individuals from $50,000 to $100,000 for the 180-day period beginning on the date of enactment. To the extent a California wildfire disaster qualified under earlier relief provided by the Bipartisan Budget Act of 2018, the bill specifically denies a double benefit under both laws.

Issue 15: REG-100814-19. Meals and Entertainment Expenses Under §274

This document contains proposed regulations that provide guidance under §274 of the Internal Revenue Code (Code) regarding certain statutory amendments made to §274 by 2017 legislation. Specifically, the proposed regulations address the elimination of the deduction under §274 for expenditures related to entertainment, amusement, or recreation activities, and provide guidance to determine whether an activity is of a type generally considered to be entertainment.

The proposed regulations also address the limitation on the deduction of food and beverage expenses under §274(k) and (n), including the applicability of the exceptions under §274(e)(2), (3), (4), (7), (8), and (9). These proposed regulations affect taxpayers who pay or incur expenses for meals or entertainment in taxable years beginning after December 31, 2017. This document also provides notice of a public hearing on these proposed regulations.

- 1.274-11 Disallowance of deductions for certain entertainment, amusement, or recreation expenditures paid or incurred after December 31, 2017.

In general. Except as provided in this section, no deduction otherwise allowable under chapter 1 of the Internal Revenue Code (Code) is allowed for any expenditure with respect to an activity that is of a type generally considered to be:

- Entertainment, or

- With respect to a facility used in connection with an entertainment activity.

For purposes of this paragraph (a), dues or fees to any social, athletic, or sporting club or organization are treated as items with respect to facilities and, thus, are not deductible. In addition, no deduction otherwise allowable is allowed for amounts paid or incurred for membership in any club organized for business, pleasure, recreation, or other social purpose.

Entertainment— In general. For § 274 purposes, the term entertainment means any activity which is of a type generally considered to constitute entertainment, amusement, or recreation, such as entertaining at bars, theaters, country clubs, golf and athletic clubs, sporting events, and on hunting, fishing, vacation and similar trips, including such activity relating solely to the taxpayer or the taxpayer’s family. These activities are treated as entertainment under this section, subject to the objective test, regardless of whether the expenditure for the activity is related to or associated with the active conduct of the taxpayer’s trade or business.

The term entertainment may include an activity, the cost of which otherwise is a business expense of the taxpayer, which satisfies the personal, living, or family needs of any individual, such as a hotel suite or an automobile to a business customer or the customer’s family. The term entertainment does not include activities which, although satisfying personal, living, or family needs of an individual, are clearly not regarded as constituting entertainment, such as a hotel room maintained by an employer for lodging of employees while in business travel status or an automobile used in the active conduct of trade or business even though used for routine personal purposes such as commuting to and from work. On the other hand, the providing of a hotel room or an automobile by an employer to an employee who is on vacation would constitute entertainment of the employee.

Food or beverages. Under this section, the term entertainment does not include food or beverages unless the food or beverages are provided during or at an entertainment activity. Food or beverages provided during or at an entertainment activity generally are treated as part of the entertainment activity. However, in the case of food or beverages provided during or at an entertainment activity, the food or beverages are not considered entertainment if the food or beverages are purchased separately from the entertainment, or the cost of the food or beverages is stated separately from the cost of the entertainment on one or more bills, invoices, or receipts. The amount charged for food or beverages on a bill, invoice, or receipt must reflect the venue’s usual selling cost for those items if they were to be purchased separately from the entertainment or must approximate the reasonable value of those items. Unless the food or beverages are purchased separately from the entertainment, or the cost of the food or beverages is stated separately from the cost of the entertainment on one or more bills, invoices, or receipts, no allocation can be made and the entire amount is a nondeductible entertainment expenditure.

Objective test. An objective test is used to determine whether an activity is of a type generally considered to be entertainment. Thus, if an activity is generally considered to be entertainment, it will be treated as entertainment for purposes of this section and §274(a) regardless of whether the expenditure can also be described otherwise, and even though the expenditure relates to the taxpayer alone.

This objective test precludes arguments that entertainment means only entertainment of others or that an expenditure for entertainment should be characterized as an expenditure for advertising or public relations. However, in applying this test the taxpayer’s trade or business is considered. Thus, although attending a theatrical performance generally would be considered entertainment, it would not be so considered in the case of a professional theater critic, attending in a professional capacity. Similarly, if a manufacturer of dresses conducts a fashion show to introduce its products to a group of store buyers, the show generally would not be considered entertainment. However, if an appliance distributor sponsors a fashion show, the fashion show generally would be considered to be entertainment.

Expenditure. The term expenditure as used in this section includes amounts paid or incurred for goods, services, facilities, and other items, including items such as losses and depreciation.

Expenditures for production of income. For purposes of this section, any reference to trade or business includes an activity described in §212.

Exceptions. Paragraph (a) of this section does not apply to any expenditure described in §274(e)(1), (2), (3), (4), (5), (6), (7), (8), or (9).

The following examples illustrate the application of paragraphs (a) and (b) of this section. In each example, neither the taxpayer nor the business associate is engaged in a trade or business that relates to the entertainment activity.

The Hot Dog Rule

Andrew invites, Ben, a business associate, to a baseball game to discuss a proposed business deal. Andrew purchases tickets for himself and Ben to attend the game. The baseball game is entertainment as defined in paragraph (b)(1) of this section and thus, the cost of the game tickets is an entertainment expenditure and is not deductible by Andrew.

Assume the same facts as in paragraph (d)(1) of this section, except that Andrew also buys hot dogs and drinks for both himself and Ben from a concession stand. The cost of the hot dogs and drinks, which are purchased separately from the game tickets, is not an entertainment expenditure and is not subject to the § 274(a)(1) disallowance. Therefore, Andrew may deduct 50 % of the expenses associated with the hot dogs and drinks purchased at the game if they meet the requirements of §§162 and §1.274-12.

Clyde invites Daniel, a business associate, to a basketball game. Clyde purchases tickets for himself and Daniel to attend the game in a suite, where they have access to food and beverages. The cost of the basketball game tickets, as stated on the invoice, includes the food or beverages. The basketball game is entertainment as defined in paragraph (b)(1) of this section and, thus, the cost of the game tickets is an entertainment expenditure and is not deductible by Clyde. The cost of the food and beverages, which are not purchased separately from the game tickets, is not stated separately on the invoice. Thus, the cost of the food and beverages is an entertainment expenditure that is subject to the §274(a)(1) disallowance. Therefore, Clyde may not deduct the cost of the tickets or the food and beverages associated with the basketball game. If the costs of food and beverage were separately stated, the cost would be deductible.

(4) Example 4. Assume the same facts as in paragraph (d)(3) of this section (Example 3), except that the invoice for the basketball game tickets separately states the cost of the food and beverages and reflects the venue’s usual selling price if purchased separately. As in paragraph (d)(3) (Example 3), the basketball game is entertainment as defined in paragraph (b)(1) of this section and, thus, the cost of the game tickets, other than the cost of the food and beverages, is an entertainment expenditure and is not deductible by C. However, the cost of the food and beverages, which is stated separately on the invoice for the game tickets, is not an entertainment expenditure and is not subject to the section 274(a)(1) disallowance. Therefore, C may deduct 50 percent of the expenses associated with the food and beverages provided at the game if they meet the requirements of section 162 and §1.274-12.

Issue 16: Social Security Modernizing its Disability Program

Social Security Commissioner Andrew Saul announced a new final rule today, modernizing an agency disability rule that was introduced in 1978 and has remained unchanged. The new regulation, “Removing the Inability to Communicate in English as an Education Category,” updates a disability rule that was more than 40 years old and did not reflect work in the modern economy. This final rule has been in the works for a number of years and updates an antiquated policy that makes the inability to communicate in English a factor in awarding disability benefits.

“It is important that we have an up-to-date disability program,” Commissioner Saul said. “The workforce and work opportunities have changed, and outdated regulations need to be revised to reflect today’s world.”

A successful disability system must evolve and support the right decision as early in the process as possible. Social Security’s disability rules must continue to reflect current medicine and the evolution of work.

Social Security is required to consider education to determine if someone’s medical condition prevents work, but research shows the inability to communicate in English is no longer a good measure of educational attainment or the ability to engage in work. This rule is another important step in the agency’s efforts to modernize its disability programs.

In 2015, Social Security’s Inspector General recommended that the agency evaluate the appropriateness of this policy. Social Security owes it to the American public to ensure that its disability programs continue to reflect the realities of the modern workplace. This rule also supports the Administration’s longstanding focus of recognizing that individuals with disabilities can remain in the workforce.

The rule will be effective on April 27, 2020.

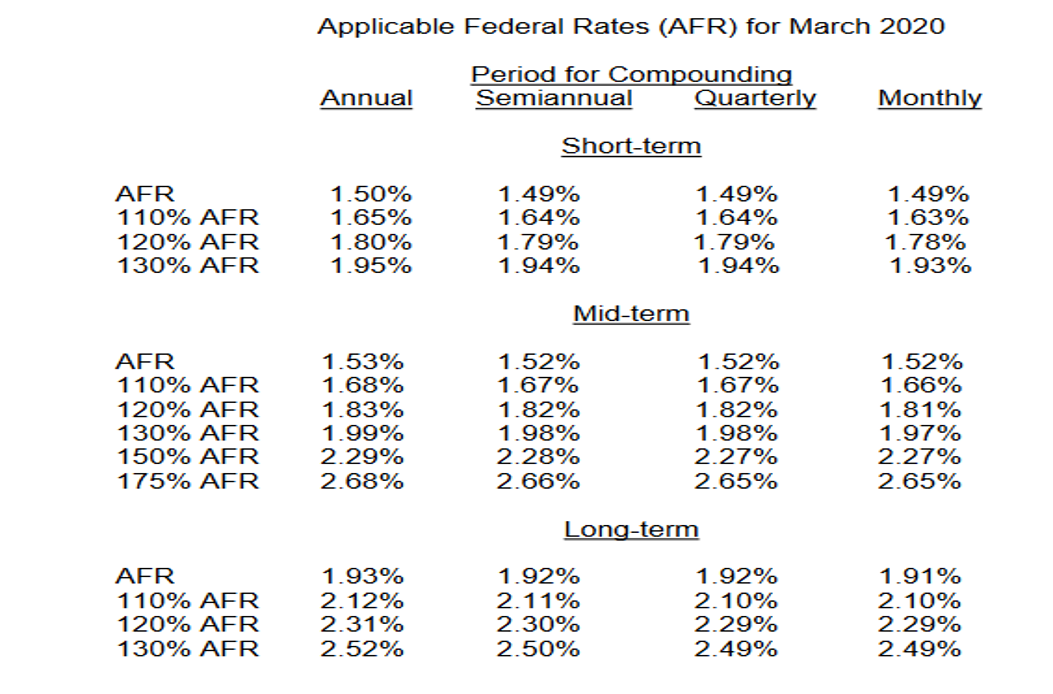

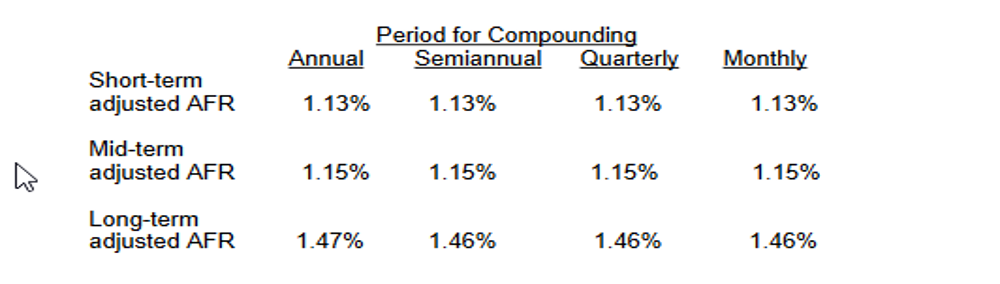

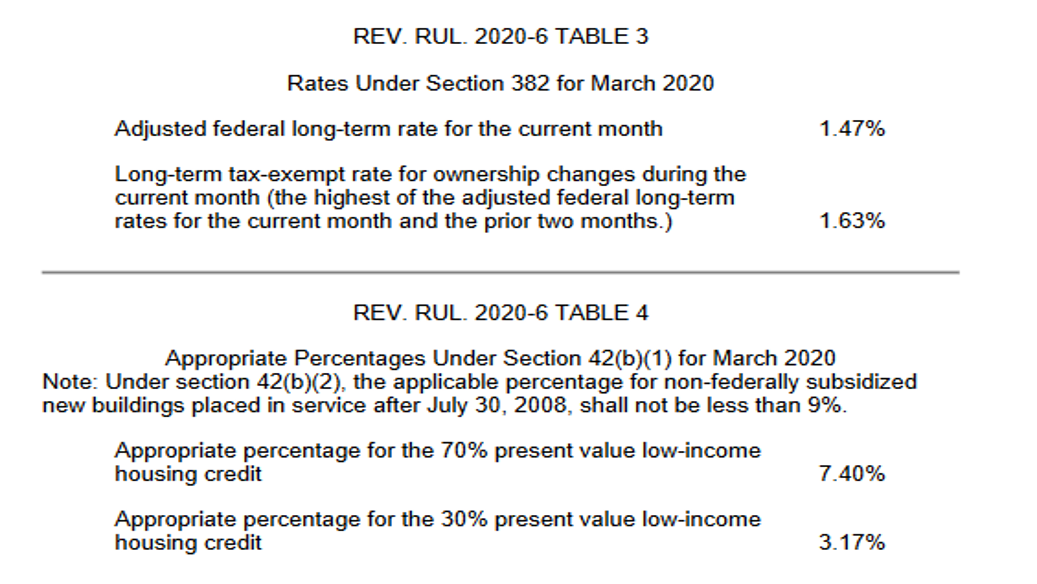

Issue: 17: Rev. Rul. 2020-06 – Applicable Federal Rates for March 2020

Table 1

REV. RUL. 2020-6 TABLE 2

Adjusted AFR for March 2020

REV. RUL. 2020-6 TABLE 5

Rate Under Section 7520 for March 2020

Applicable federal rate for determining the present value of an annuity, an interest for life or a term of years, or a remainder or reversionary interest 1.8%

Remember, our webinar series for 2020 is published and we are offering the Unlimited hours at $199 – a 75% Savings and our Best Value.