As a tax professional, you probably work with a wide range of clients. It doesn’t matter whether you’re an accountant specializing in taxes, an enrolled agent, a certified tax preparer, a tax attorney, or any other professional covered under circular 230. Regardless, your clients probably come in all shapes and sizes.

When working with various clients, there are a number of questions you might ask yourself. Particularly when it comes to working with businesses, you might wonder: how large is my client’s company? What’s the best form of business entity for my client: a sole proprietorship, partnership, C-corp, or S-corp? Is my client’s S-corp adhering to the rules surrounding reasonable compensation? Is there more my client could be doing throughout the year to make things easier come tax time? The list goes on.

However, there are a couple of questions that you rarely find yourself asking with respect to a client’s business: is the business my client’s company engages in even legal? And if so, what are the tax implications?

Years ago, the idea of preparing tax returns and offering tax advice to a seemingly “illegal” company would have seemed absurd to the majority of tax professionals. In recent years, though, it’s become an increasingly common issue.

We’re talking, of course, about marijuana and taxes.

To put it plainly, here’s the conundrum. On the one hand, marijuana is still illegal at the federal level. This holds true despite the fact that eight states (plus the District of Columbia) have now legalized marijuana for recreational use. At the same time, though, the IRS has made it clear that businesses producing marijuana are still obligated to pay federal income tax. As the IRS says in a memo from 2014, “Though a medical marijuana business is illegal under federal law, it remains obligated to pay federal income tax on its taxable income because §61(a) does not differentiate between income derived from legal sources and income derived from illegal sources.” That language is pretty clear.

With this in mind, though, filing taxes as a business that grows and sells marijuana — even in a state where recreational use is completely legal — is far from simple. You can’t simply prepare your federal return the same way that any other business would and expect the IRS to approve it without any issues.

Given the complexity of this topic, we highly recommend that any and all tax professionals planning to work with marijuana-related businesses sign up for a dedicated marijuana tax webinar. It’s important to have a complete understanding of both the state and federal tax implications of growing and selling marijuana before working with individual clients.

While it’s not possible to go into that level of depth in this introductory blog post, we will take a look at some of the big picture issues at play when it comes to marijuana and taxes. By the end of this guide, you should have a better understanding of some of the issues that tend to arise for companies attempting to file taxes for revenue generated from marijuana sales.

Below, we’ll look at a number of individual topics as they relate to the tax implications of marijuana. Topics include:

- A brief history of marijuana legalization and legislation

- Tax laws for the sale of recreational marijuana by state

- Federal tax implications for the sale of marijuana

Let’s get started.

A Brief History of Marijuana Legislation and Taxation

Part of the question regarding the sale of marijuana and its associated tax implications comes down to what exactly this income ought to be considered. Is it business income? Is it personal income? Since marijuana is an illegal substance according to the federal government, the answer isn’t immediately self-evident.

As it turns out, the U.S. Supreme Court has determined more than once that the sale of marijuana is to be counted as gross income, regardless of whether the act of selling it is actually legal or not. This raises an important question, though: can you actually deduct business expenses from this gross income? For example, is the purchase of equipment used to cultivate marijuana a legitimate business expense? Can you deduct the cost of paying your employees’ salaries, when that money is being spent in order to engage in an enterprise that (at the federal level) is deemed illegal?

Back in 1982, Congress passed a law which answers this question. According to U.S. tax code § 280E:

“No deduction or credit shall be allowed for any amount paid or incurred during the taxable year in carrying on any trade or business if such trade or business (or the activities which comprise such trade or business) consists of trafficking in controlled substances (within the meaning of schedule I and II of the Controlled Substances Act) which is prohibited by Federal law.”

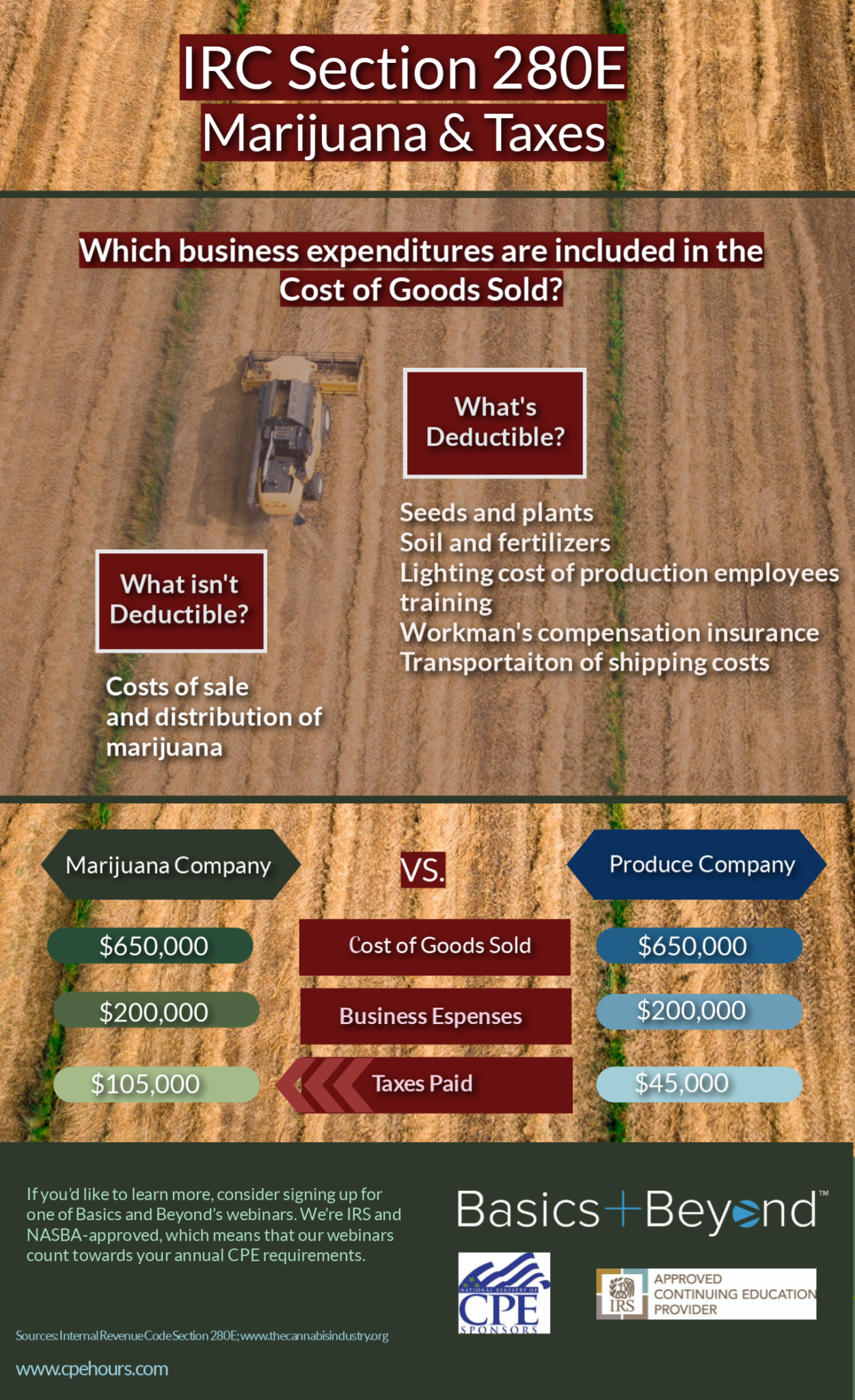

In other words, Congress decided more than 35 years ago that any business engaging in the sale of a schedule I or II substance cannot deduct any of the expenses associated with that business. According to the DEA’s website, marijuana is a schedule I substance — alongside heroin, LSD, and ecstasy. Therefore, as a result of U.S. tax code § 280E, there’s no way for marijuana-related businesses to deduct any of their expenses when filing their federal income taxes.

As you can imagine, the implications of this are huge. According to one marijuana producer grossing around $10 million per year in sales, the inability to deduct any expenses before paying their federal income taxes cuts into their profits by as much as $1.5 million per year. It’s unclear whether this law is set to change anytime in the near future.

State Marijuana Tax Laws

As of 2018, there are 29 states (as well as the District of Columbia) where marijuana is legal for medicinal use. In 8 states and the District of Columbia, marijuana is legal for recreational use.

Every state taxes the sale of recreational marijuana differently. Let’s take a look at each state’s requirements, one by one.

- In addition to standard state sales tax, the state of Washington charges a 37% sales tax on the sale of marijuana.

- The state of Oregon has no sales tax for general goods. However, Oregon charges a 17% sales tax on the sale of marijuana in addition to regular state taxes.

- Nevada enforces several marijuana taxes. First, producers must pay a tax of 15% of Fair Market Value when selling marijuana on to a distributor. In addition to this, consumers must absorb a further 10% sales tax on the retail side.

- While Maine legalized recreational marijuana in a ballot initiative in 2016 and legislation has been passed by both chambers of its state legislature, the law has not gone into effect. That said, two taxes will likely be enforced: an excise tax on producers (set to be $94 per pound of trim, $335 per pound of flowers, $0.30 per seed, or $1.50 per seedling) as well as a 10% sales tax.

- Colorado currently imposes two sets of taxes on marijuana as well: an excise tax for producers of 15%, and a sales tax of 15%.

- Massachusetts (which will begin retail sales later this year) currently has its tax rate set at 10.75%.

- California charges both excise and sales taxes on marijuana. The excise tax is currently $9.25 per ounce for flowers and $2.75 per ounce for leaves, while the sales tax rate is 15%.

- Alaska has no state sales tax and has not placed a sales tax on marijuana. However, producers must pay an excise tax of $50 per ounce of product sold to retailers.

- The District of Columbia has not yet established a retail market for marijuana, and thus has no excise or sales taxes in place.

Federal Tax Implications for Marijuana

As we saw above, U.S. tax code § 280E stipulates sharp limitations on a marijuana-related business’ ability to deduct expenses from their gross income before paying federal income taxes.

However, some deductions are still allowed. In 2007, one court case in particular resulted in a dramatic change to what can and can’t be deducted. In the case Californians Helping to Alleviate Medical Problems, Inc., v. Commissioner, 128 T.C. 173 (2007) (“CHAMP”), the government admitted that § 280E should not prevent a company from deducting the Cost of Goods Sold (COGS) from their gross income when determining what amount of income would be subject to federal income tax.

The rules surrounding what can and cannot be counted as Cost of Goods Sold for marijuana producers is quite complicated. According to the IRS, marijuana businesses must still adhere to both § 280E and § 471 (which governs rules for inventories when determining business income) when assessing Cost of Goods Sold.

How does this actually play out for marijuana producers and resellers?

For resellers, federal deduction options are still very limited. According to Chief Counsel Advice (CCA) 201504011, an IRS memo from 2014, § 280E still more or less holds true: any costs incurred in the resale of marijuana which are ineligible for deduction under § 280E are, in fact, still ineligible. Simply put, this means that resellers can only deduct the actual cost of purchasing marijuana (and transporting it for the purpose of resale) from their expenses. However, no other expenses can be deducted.

For marijuana producers, there are a significantly larger number of deduction opportunities available. Many of the standard expenses associated with any business — including the cost of employee wages, land and/or building rent, maintenance to equipment, utility payments, non-capitalized tools, and other expenses — are deductible from gross income. However, some expenses are still ineligible for deduction: for example, marketing expenses.

However, many marijuana businesses find themselves still subject to an incredibly high tax rate due to their inability to deduct the same expenses as other companies. Some producers and resellers have even reported paying an effective federal tax rate of up to 70%.

Cash Accounting Issues for Marijuana

In addition to the issues surrounding deductions and the ensuing effective federal tax rates, many marijuana businesses are faced with a simpler and more practical problem when it comes to paying their federal income taxes.

Due to the fact that marijuana is banned at the federal level, any federally insured (FDIC) bank is unable to open a checking account for a company which trades in marijuana. While such a bank could technically choose to work with a marijuana retailer, they could face a potential shutdown from the federal government. In practicing due diligence, the vast majority of banks aren’t interested in taking that risk.

As a result, all of the accounting for many marijuana businesses must be conducted in cash. This can result in literally millions of dollars in cash on hand at any given time. While this creates obvious accounting issues, things can get even more complicated come tax time.

That’s right: many marijuana businesses are forced to pay their federal income taxes in cash, rather than being able to use a checking account to transfer funds as the vast majority of businesses do. This is already an enormous problem for federal authorities attempting to count such large amounts of cash at local IRS offices. Even more problematic, though, is the projected future scenario: by 2021, the marijuana industry is expected to exceed $21 billion in revenue. That’s literally billions of dollars in income taxes that will likely be paid in cash.

Marijuana Tax Webinar

As you’ve probably gathered from this overview of marijuana and taxes, the topic is incredibly complex. While the introduction should give you a good sense of the general tax implications for marijuana businesses — both at the state and the federal level — it’s by no means intended to be comprehensive.

If you’re a tax professional who’s looking to provide tax services to clients with businesses in the marijuana industry, we highly recommend signing up for a tax webinar dedicated specifically to marijuana. At Basics & Beyond™, we offer tax webinars designed specifically for busy tax professionals. Our webinars bring you up to date on the tax code, and we keep things interesting and engaging every step of the way. Take a look at our affordable pricing. To sign up today, click here.