Due to the additional guidance provided regarding the PPP Loans and the Paycheck Protection Program Flexibility Act, we have created an additional newsletter for June.

For those of you who attended the PPP Loan Forgiveness webinar, we have summarized the questions we received.

In This Issue

- New Employer Tax Credits: Publication 5419

- PPP Questions and Answers

- Economic Impact Payments Information

- Glitch in the Transcript Delivery System

- Publication 3891 Lockbox Addresses

- OIC Procedures Due to Pandemic Issues

- FAQs on COVID-19 Retirement Plan Distribution and Loan Rule Changes

- DOL Announces Publication of Final E-Disclosure Rule

- Later this Summer we can E-file Forms 1040X

Issue 1: New Employer Tax Credits: Publication 5419 (Just Released) https://www.irs.gov/pub/irs-pdf/p5419.pdf

Issue 2: Questions and Answers on COVID Part 6 and the PPP Loans Webinar (purchase the recorded session here)

PPP Loan Forgiveness Q&A Summary

The Paycheck Protection Program (PPP) launched in early April with $349 billion in funding that was exhausted in less than two weeks. Congress provided an additional $310 billion in funding on April 21, 2020.

The program was established to provide relief to small businesses during the coronavirus pandemic as part of the $2 trillion Coronavirus Aid, Relief, and Economic Security (CARES) Act. PPP funds are available to small businesses that were in operation on Feb. 15 with 500 or fewer employees, including tax-exempt not-for-profits, veterans’ organizations, Tribal concerns, self-employed individuals, sole proprietorships, and independent contractors. Businesses with more than 500 employees also can apply for loans in certain situations.

On May 26, 2020, H.R.7010 – Paycheck Protection Program Flexibility Act of 2020 was introduced in the House and passed on May 28, 2020. The Senate passed the bill on June 3 and the President signed it into law on June 5, 2020.

The Act made significant changes to the original Paycheck Protection Program as detailed below.

- Current PPP borrowers can choose to extend the eight-week period to 24 weeks, or they can keep the original eight-week period.

- New PPP borrowers will have a 24-week covered period, but the covered period cannot extend beyond Dec. 31, 2020. This flexibility is designed to make it easier for more borrowers to reach full, or almost full, forgiveness.

- Under the language in the House bill, the payroll expenditure requirement drops to 60% from 75% but is now a cliff, meaning that borrowers must spend at least 60% on payroll or none of the loan will be forgiven. Currently, a borrower is required to reduce the amount eligible for forgiveness if less than 75% of eligible funds are used for payroll costs, but forgiveness isn’t eliminated if the 75% threshold isn’t met.

- Borrowers can use the 24-week period to restore their workforce levels and wages to the pre-pandemic levels required for full forgiveness. This must be done by Dec. 31, a change from the previous deadline of June 30.

- The legislation includes two new exceptions allowing borrowers to achieve full PPP loan forgiveness even if they do not fully restore their workforce. Previous guidance already allowed borrowers to exclude from those calculations employees who turned down good faith offers to be rehired at the same hours and wages as before the pandemic. The new bill allows borrowers to adjust because they could not find qualified employees or were unable to restore business operations to Feb. 15, 2020, levels due to COVID-19 related operating restrictions.

- New borrowers now have five years to repay the loan instead of two. Existing PPP loans can be extended up to 5 years if the lender and borrower agree. The interest rate remains at 1%.

- The bill allows businesses that took a PPP loan to also delay payment of their payroll taxes, which was prohibited under the CARES Act.

In light of the changes we await guidance on these issues and many others. We have addressed your questions to the best of our ability based on the guidance issued. The SBA has issued 14 Interim Final Rule documents, but many questions remain unanswered.

- What about costs for Workers Compensation insurance?

–Presently workers compensation insurance is not considered payroll, for purposes of the PPP Loan.

- Client received funding on the 12th of May. Payroll for the period ending May 11 was paid on May 15. Does that May 15 payment included on the forgiveness calculations?

–The Administrator of the Small Business Administration (Administrator), in consultation with the Secretary of the Treasury (Secretary), recognizes that the eight-week covered period will not always align with a borrower’s payroll cycle. For administrative convenience of the borrower, a borrower with a bi-weekly (or more frequent) payroll cycle may elect to use an alternative payroll covered period that begins on the first day of the first payroll cycle in the covered period and continues for the following eight weeks. If payroll costs are incurred during this eight-week alternative payroll covered period, but paid after the end of the alternative payroll covered period, such payroll costs will be eligible for forgiveness if they are paid no later than the first regular payroll date thereafter. The Administrator, in consultation with the Secretary, determined that this alternative computational method for payroll costs is justified by considerations of administrative feasibility for borrowers, as it will reduce burdens on borrowers and their payroll agents while achieving the paycheck protection purposes manifest throughout the CARES Act, including § 1102. Because this alternative computational method is limited to payroll cycles that are bi-weekly or more frequent, this computational method will yield a calculation that the Administrator does not expect to materially differ from the actual covered period, while avoiding unnecessary administrative burdens and enhancing auditability.

Note the 8-week period has now extended to 24 weeks.

- Are you going to cover what constitutes payroll for Sch C Sole Proprietors?

–Pursuant to the Interim Final Rule dated May 20 from the SBA with respect to the Schedule C sole proprietors: “Schedule C filers are capped by the amount of their owner compensation. This would include gross receipts less qualified business expenses resulting in Net Profit. If the sole proprietor has no employees, the PPP Loan amount would be based on Net profit divided by 12months. to get a monthly amount and then taken by 2.5 months get the loan amount.

At this time, we will await guidance on the new PPP Loan to see how this calculation may change or remain the same.

- Some bankers have suggested have the Sole Proprietors pay Owner Draws to themselves to show “payroll” for them?

-See the proper calculation in Question 3. Owners draws are not mentioned in any guidance.

- Does the $100k payroll limit include benefits?

–No, benefits are separate

- Cash compensation-is that gross? Someone makes 52K gross then it’s 8K for the 8 weeks?

–Cash compensation is gross compensation

- When doe the application for forgiveness need to be submitted?

-There is significant time to submit the application. Based on the new law we will await guidance as to when the PPP Loan Forgiveness application needs to be submitted. New law has changed from 8 weeks to 24 weeks, but the business can still use the 8-week time frame. Based on my questions to the local bank, they are awaiting SBA guidance and have yet to get any training on the issue.

- I assume that if 75% or more of the PPP is used for payroll, then we don’t have to do anything with the nonpayroll costs, correct?

-That is correct but the percentages have been relaxed a bit to 60%

- Do SEP contributions for 2019 as well as 2020 if paid in the 8-week or 24-week period, count as payroll cost?

-Section III (f) of Interim Guidance issued April 15, states: Payroll costs consist of compensation to employees (whose principal place of residence is the United States) in the form of salary, wages, commissions, or similar compensation; cash tips or the equivalent (based on employer records of past tips or, in the absence of such records, a reasonable, good-faith employer estimate of such tips); payment for vacation, parental, family, medical, or sick leave; allowance for separation or dismissal; payment for the provision of employee benefits consisting of group health care coverage, including insurance premiums, and retirement; payment of state and local taxes assessed on compensation of employees; and for an independent contractor or sole proprietor, wages, commissions, income, or net earnings from self-employment, or similar compensation.

This is the only guidance we have at this point.

10. When you use PPP for self-employed payroll are you supposed to write yourself a check your share of the earnings?

-For the self-employed business owner with no employees, the amount is generally deposited in the individuals bank account – the business owner will then apply for forgiveness based on the rules outlined in question 3.

11. Can I get the link for the Forbes article?

12. Can the employer give an employee a raise to increase payroll costs?

–Yes, cannot reduce, however, nowhere does it state we cannot increase. The raise must be reasonable in light of the position. For example, a raise of $1.00 an hour was promised to a journeyman electrician once they received their initial certification.

13. Client pre-paid rent for 2020 in January 2020. Can they use the 2 months covered by during PPP period as part of non-payroll forgiveness?

–We need more guidance from the SBA on prepayments.

14. What if someone got a PPP loan and then could not open their business and still haven’t gotten the ok to open. What happens with the 8 weeks coming up?

-We now have 24 weeks so this should solve that issue.

- Why can’t accounting costs to process loan be considered non-payroll PPP expense?

–Accounting costs are not considered non- payroll costs. Congress did not see fit to include theses costs.

16. If the payroll expense is not deductible, do you still have to issue a W-2 to the employee?

–Yes, a W-2 is still required. The wages represent taxable income to the employee.

17. If shareholder with W-2 from his s corporation is treated as an owner-employee and forgiveness will be limited to the amount of 8 weeks from 52 weeks from 2019 W-2?

–Review the formula stated in question 3. As of this date and the passage of new law we do not have any information if this calculation will change.

18. Is it okay to pay payroll a day ahead of usually to get it into the 8 weeks? My client’s 8 weeks will end and the next day they will have payroll. I want to move it to the day before.

-Borrowers may seek forgiveness for payroll costs for the eight weeks beginning on either 1) the date of disbursement of the PPP loan proceeds or 2) the first day of the first payroll cycle covered period (the alternative payroll period).

Please note we now have 24 weeks.

19. Should a separate bank account be opened and use this account for all of the expenses be paid through this account?

–Nothing in the guidance requires holding the PPP loan proceeds in a separate account, however, some banks suggest or require.

20. Can you submit pension contributions for a Cash Balance Plan that is 100% employer sponsored and just take 1/12 of the annual expenses for 2 months, in effect covering the 8-week period?

–No direct guidance yet on this question; however, your math seems logical. One practical issue may be getting an actuary to develop what the 2020 cash balance plan contribution amount during the year in question.

21. For bonuses you are still capped at $ 1,923 for weekly employees over $100 k including.

–Total compensation would be limited to $15,385 for the 8-week period. For owner-owner employees and self-employed individuals’ compensation is further limited to 8/52 of 2019 compensation.

Please note the cap has changed now that we have 24 weeks. We await guidance.

22. What about employers who want to accelerate a payroll period to get one more in?

–Prepayment is not allowed.

23. Does interest on floor plan loan collateralized by inventory qualify for forgiveness?

–It appears the floor plan could qualify. More clarification to come from the SBA.

24. Discretionary employer contribution to pension plan for entire year paid during 8-week period, fully forgivable?

–We are hoping that we receive better guidance. Law states it has to be incurred, Paid and incurred during 8-week period It appears accrued costs paid during 8-week period will count toward forgiveness, I would also share AJ Reynolds comment here. We are hoping that we’ll further guidance in retirement plan provisions under the CARES Act.

Remember this time frame has changed to 24 weeks and we await more guidance on the retirement plan issue.

25. Not sure if you can cover but starting to worry my approval was not right. I work for the US arm of a large international company, but we are independent filing our own return in the US with all our employees located in the US. In my mind we have a definite need for the loan as cuts/payroll reductions have been discussed but can you dive into affiliation rules? The loan was strictly payroll in the amount of $400k but I am now worried this may not be allowed.

-We do not have enough guidance to address this issue. I suggest you review the affiliation rules in interim guidance issued on April 3, 2020 on the SBA website.

26. What is the salary amount considered for forgiveness per employee? Is it $8,333.33 per month or a GRAND total of $16,666.67? I want to see if bonus have to be issued each pay period (first 4 weeks) or just wait for the last pay period.

–Total compensation would be limited to $15,385 for the 8-week period. For owner-owner employees and self-employed individuals’ compensation is further limited to 8/52 of 2019 compensation.

We now have a 24-week period and the amount has increased per employee. We await further guidance on how.

27. How do you handle the advance on the EIDL for the PPP loan forgiveness?

-We await guidance on this issue.

28. Can you include in payroll costs the pension contribution paid in the 8 weeks for the safe harbor and profit sharing for the 2019 tax year?

–It appears accrued costs paid during the 8 weeks period will count toward forgiveness (we are hoping for additional guidance will be forthcoming)

That 8-week period is now extended to 24 weeks.

29. To confirm that if a client has 7 FTE as of Feb 2020 but has been closed and has had no payroll, as long as they bring back all their FTE’s by June 30th then there are no issues with the FTE reduction limitation?

-Under the new Act the period has changed to 24 weeks, so bring them back within that timeframe. The percentages have also changed to at least 60% payroll and 40% for the other designated costs.

30. Owner employee of S Corp, usually bonus/commission paid in June, will that be allowed if over 8/52 of 2019 compensation?

-We are awaiting additional guidance under the new Act. Raises are allowed but bonuses are not mentioned. Also review the formula in Question 3.

31. How does EIDL play with this? I know you cannot use same expenses but there is a question about the EIDL on the forgiveness app.

-The forgiveness application must be revamped and did not address all issues. I would await the new application for forgiveness and guidance to be issued. Feedback on the application has been provided to SBA and we expect changes.

32. If the expenditures paid by the PPP loan not deductible, then the loan itself becomes taxable, right?

–The loan is not taxable, but rather may have to be paid back if you fail to have qualifying expenditures (i.e., payroll, overhead, interest on building, rent, etc.)

IRS has stated that the expenditures are not deductible, but Congress has stated that was not the laws intent and introduced the HEROS Act which has passed the House to correct and allow the expenses to be deductible. BUT, the HEROS Act is “dead on arrival” in the Senate and we await to see what parts of the bill the Senate will approve. We need to wait and see.

33. Are employees of an ESOP considered Owner-Employees for PPP loan purposes?

-We need more guidance on ESOP’s however they do not appear to be owner-employees.

34. We are trying to understand if equipment leases would be considered as an eligible non-payroll expense.

-Pursuant to the Interim Final guidance interest payments on any business mortgage obligation on real or personal property incurred before Feb 15,2020 qualifies, excluding any prepayments of interest. We anticipate more guidance on this issue.

Many of you expressed an interest in a Form 941 webinar on how to prepare the 2nd quarter Form 941 if a client qualifies for Family Medical leave/Sick Pay or the Employee Retention Credit. Below are the three potential credits a client with payroll MAY qualify for. In reviewing the three credits, this will address some of the questions you proposed.

Emergency Paid Sick Leave Act (EPSLA)

The EPSLA requires employers with less than 500 employees to provide paid sick leave to employees unable to work or telework after March 31, 2020, and before January 1, 2021, because the employee:

- Is subject to a federal, state, or local quarantine or isolation order related to COVID-19.

- Has been advised by a health care provider to self-quarantine due to concerns related to COVID-19.

- Is experiencing symptoms of COVID-19 and seeking a medical diagnosis.

- Is caring for an individual subject to an order described in (1) or who has been advised as described in (2).

- Is caring for a child if the school or place of care has been closed, or the childcare provider is unavailable, due to COVID-19 precautions.

- Is experiencing any other substantially similar condition specified by the U.S. Department of Health and Human Services.

The employee must meet one of the above and pay sick leave or family leave to get the credit.

The NEW Employee Retention Credit

The Employee Retention Credit is a fully refundable tax credit for employers equal to 50% of qualified wages (including allocable qualified health plan expenses) that Eligible Employers pay their employees. This Employee Retention Credit applies to qualified wages paid after March 12, 2020, and before January 1, 2021. The maximum amount of qualified wages taken into account with respect to each employee for all calendar quarters is $10,000, so that the maximum credit for an Eligible Employer for qualified wages paid to any employee is $5,000.

Eligible Employers for the purposes of the Employee Retention Credit are employers that carry on a trade or business during calendar year 2020, including tax-exempt organizations, that either:

- Fully or partially suspend operation during any calendar quarter in 2020 due to orders from an appropriate governmental authority limiting commerce, travel, or group meetings (for commercial, social, religious, or other purposes) due to COVID-19; or

- Experience a significant decline in gross receipts during the calendar quarter.

Each of the credits have designated limits, that were discussed in the COVID Legislation Part 1.

We will see what can be done to expand the information. This issue is highly technical and math extensive. We need to determine the best way to present the material – by class or through the newsletter.

Issue 3: Economic Impact Payments Being Sent by Prepaid Debit Cards, Arrive in a Plain White Envelope FAQ’s

As Economic Impact Payments continue to be successfully delivered, the Internal Revenue Service today reminds taxpayers that some payments are being sent by prepaid debit card. The debit cards arrive in a plain envelope from “Money Network Cardholder Services.”

Nearly 4 million people are being sent their Economic Impact Payment by prepaid debit card, instead of paper check. The determination of which taxpayers received a debit card was made by the Bureau of the Fiscal Service, a part of the Treasury Department that works with the IRS to handle distribution of the payments.

Those who receive their Economic Impact Payment by prepaid debit card can do the following without any fees.

- Make purchases online and at any retail location where Visa is accepted.

- Get cash from in-network ATMs.

- Transfer funds to their personal bank account.

- Check their card balance online, by mobile app or by phone.

This free, prepaid card also provides consumer protections available to traditional bank account owners, including protection against fraud, loss and other errors.

IRS FAQ’s

Can I have my economic impact payment sent to my prepaid debit card?

Maybe. It depends on the prepaid card and whether the payment has already been scheduled. Many reloadable prepaid cards have account and routing numbers that can be provided to the IRS through the Get My Payment application or Non-Filers: Enter Payment Info Here tool. The client will need to check with the financial institution to ensure the card can be re-used and to obtain the routing number and account number, which may be different from the card number. If they obtained the prepaid debit card through the filing of a federal tax return, they must contact the financial institution that issued the prepaid debit card to get the correct routing number and account number. Do not use the routing number and account number shown on the client’s copy of the tax return filed. When providing this information to the IRS, the client should indicate that the account and routing number provided are for a checking account unless the financial institution indicates otherwise.

Will IRS be sending prepaid debit cards?

Some payments may be sent on a prepaid debit card known as The Economic Impact Payment Card The Economic Impact Payment Card is sponsored by the Treasury Department’s Bureau of the Fiscal Service, managed by Money Network Financial, LLC and issued by Treasury’s financial agent, MetaBank®, N.A.

If the client received an Economic Impact Payment Card, it will arrive in a plain envelope from “Money Network Cardholder Services.” The Visa name will appear on the front of the Card; the back of the Card has the name of the issuing bank, MetaBank®, N.A. Information included with the Card will explain that the card is your Economic Impact Payment Card.

Can a Client specifically ask the IRS to send the Economic Impact Payment to me as a debit card?

Not at this time. For those who don’t receive their Economic Impact Payment by direct deposit, they will receive their payment by paper check, and, in a few cases, by debit card. The determination of which taxpayers receive a debit card will be made by the Bureau of the Fiscal Service (BFS), another part of the Treasury Department that works with the IRS to handle distribution of the payments. At this time, taxpayers cannot make a selection to receive a debit card.

Watch out for scams related to Economic Impact Payments

The IRS urges taxpayers to be on the lookout for scams related to the Economic Impact Payments. To use the new app or get information, taxpayers should visit IRS.gov. People should watch out for scams using email, phone calls or texts related to the payments. Be careful and cautious: The IRS will not send unsolicited electronic communications asking people to open attachments, visit a website or share personal or financial information. Remember, go directly and solely to IRS.gov for official information.

More information can be found at: EIPcard.com

Our clients have not had much success in reaching Customer Service at: 1.800.240.8100

Issue 4: IRS Working on a Glitch That Prevents Some Practitioners from using the Transcript System

IRS has stated that it is aware that some practitioners have lost access to IRS’s Transcript Delivery Service (TDS) and they are working to restore that access. If professionals need immediate assistance, they should contact the IRS e-help Desk at 866-255-0654.

Issue 5: Publication 3891 – Current Lock Boxes

Publication 3891 issued in January of 2020 has the most current mailing information for most returns. Watch annually for this publication in early January as IRS will update the lockboxes for both individual and businesses.

Issue 6: Temporary Relief for Taxpayers – Suspension of Offer Activities During the COVID-19 Pandemic Procedures COIC and FOIC Procedures

The following guidance addresses questions raised about the impact of OIC investigations, deadlines, and payment terms in relation to COVID-19 and the deferral on tax payments.

The guidance detailed is effective immediately and continues until July 15, 2020 (referred to as the restricted period), unless extended.

If the Tax Increase and Prevention Reconciliation Act (TIPRA) of 2005 (TIPRA) statute reaches 22 months, employees must take the additional required actions outlined below.

Acceptances

IRS employees may process acceptances if the taxpayer is able to meet the payment terms. The timeframe for payment terms (lump sum or periodic) for an offer in compromise is set by the Form 656 contract and employees cannot extend it.

- Note: The taxpayer will not get credit for missed payments, and the terms of an offer cannot exceed 24 months. If the taxpayer does not meet the terms and does not pay within 24 months due to the restricted period, an addendum must be secured. The addendum will address the extended time frame.

Notices of Federal Tax Lien (NFTL)

IRS employees will review their case to determine if any of the following situations exist which would require the filing or refiling of a NFTL.

- A jeopardy situation exists, or the taxpayer is liquidating assets and there is no NFTL filed, (with managerial approval).

- Recommending offer acceptance and the terms provide for payment in more than five months and the liability is over $50,000.

- The underlying statutory lien will expire because tax period(s) on an existing Notice of Federal Tax Lien are within the refile period.

For all other cases, IRS employees should not file a NFTL against any taxpayer, without senior managerial approval. Employees must make a lien determination when the restricted period ends. In addition, IRS employees need to ensure they have discussed CAP rights before filing a NFTL.

Return of Offers Due Dates for Information

The IRM allows for flexibility when setting deadlines. IRS employees may establish deadlines based on the facts of the case. For all due dates, employees will consider reasonable extensions of time when requested by the taxpayer. The IRS will not return any offers prior to July 15, 2020 for failure to provide information.

Estimated Payments and Federal Tax Deposits Payments

IRS encourages the client to make the payment(s) based on the established due dates, if possible. IRS employees are instructed to not return the offer for payment noncompliance during the restricted period. IRS employees need to be aware that inactivity may reduce the estimated payments and payroll tax requirements. The offer will remain under consideration during the tax payment deferment time period. Once the pandemic time frame expires on July 15, 2020, if the client has not contacted IRS to make satisfactory arrangements regarding the required tax payments, IRS will return the offer, and close the case with no further notice.

Tax Returns

The deadline to file Form 1040 for 2019 is July 15, 2020. The IRS will not return any offers prior to July 15, 2020 for failure to file delinquent tax returns.

Returns for Reasons Other than Failure to Provide Requested Information/Payments

The restricted period applies only to closures for failure to provide requested items such as payment, returns, or information. If the case qualifies for a return due to lack of jurisdiction (e.g. if the taxpayer files bankruptcy, Department of Justice tax periods, or the liability does not qualify for compromise), the offer will be returned.

Mandatory Withdrawals TIPRA Payments

If the taxpayer misses any or all of the required payments during the restricted period, the employees will not deem the offer a mandatory withdrawal. When the restricted period ends, the taxpayer will resume making payments and will not need to remit missed payments from the restricted period.

Appeal Timeframe

If the rejection letter is issued, the client has 30 days to provide a written appeal. The client may use USPS (postmark date) or fax to remit the appeal by the 30th day. Special rules apply to third party mailing services. If the client uses a non-designated delivery service (e.g. ground service by a third-party service), the IRS must physically receive the appeal in the IRS office by the 30th day. Additionally, taxpayers should use USPS registered or certified mail if they want to verify the IRS received their appeal, in the event the appeal gets misplaced.

Offer Evaluations

If the taxpayer indicates they can no longer meet the proposed terms of the offer under consideration, The IRS will the re-evaluate the information to determine if the reasonable collection potential (RCP) calculation may warrant acceptance. They must look at the following:

- When calculating future income, determine the anticipated reduction.

- Did the client lose all business or just a portion and for what length of time?

- Is the client only temporarily unemployed due to the current situation?

If the IRS cannot recommend acceptance, they are to advise the client that they may withdraw the offer and resubmit after the situation has stabilized or appeal the rejection.

Reconsideration

If a taxpayer requests reconsideration of an offer because they were impacted by COVID-19, the procedures in IRM 5.8.7.3.3 will apply. A returned offer may be reloaded under return reconsideration procedures if the TP/POA contacts OIC and criteria is met in IRM 5.8.7.3.1.

Processability

There has been no change to processability. Once an employee processes an offer, the procedures above apply to requests for shortfall. Deadlines may be set for payment, but employees may not return offers due to lack of payment during the restricted period.

Issue 7: IRS Adds FAQs on COVID-19 Retirement Plan Distribution and Loan Rule Changes

What are the special rules for retirement plans and IRAs in § 2202 of the CARES Act?

In general, §2202 of the CARES Act provides for expanded distribution options and favorable tax treatment for up to $100,000 of coronavirus-related distributions from eligible retirement plans (certain employer retirement plans, such as §§ 401(k) and 403(b) plans, and IRAs) to qualified individuals, as well as special rollover rules with respect to such distributions. It also increases the limit on the amount a qualified individual may borrow from an eligible retirement plan (not including an IRA) and permits a plan sponsor to provide qualified individuals up to an additional year to repay their plan loans.

Does the IRS intend to issue guidance on §2202 of the CARES Act?

Treasury and the IRS are formulating guidance on §2202 of the CARES Act and anticipate releasing that guidance in the near future. IRS Notice 2005-92 (PDF), issued on November 30, 2005, provided guidance on the tax-favored treatment of distributions and plan loans under §§101 and 103 of the Katrina Emergency Tax Relief Act of 2005 (KETRA) as those provisions applied to victims of Hurricane Katrina. The Treasury Department and the IRS anticipate that the guidance on the CARES Act will apply the principles of Notice 2005-92 to the extent the provisions of §§2202 of the CARES Act are substantially similar to the provisions of KETRA that are addressed in that notice.

Am I a qualified individual for purposes of §2202 of the CARES Act?

You are a qualified individual if –

- You are diagnosed with the virus SARS-CoV-2 or with coronavirus disease 2019 (COVID-19) by a test approved by the Centers for Disease Control and Prevention.

- Your spouse or dependent is diagnosed with SARS-CoV-2 or with COVID-19 by a test approved by the Centers for Disease Control and Prevention.

- You experience adverse financial consequences as a result of being quarantined, being furloughed, or laid off, or having work hours reduced due to SARS-CoV-2 or COVID-19.

- You experience adverse financial consequences as a result of being unable to work due to lack of childcare due to SARS-CoV-2 or COVID-19 or

- You experience adverse financial consequences as a result of closing or reducing hours of a business that you own or operate due to SARS-CoV-2 or COVID-19.

Under §2202 of the CARES Act, Treasury and the IRS may issue guidance that expands the list of factors considered to determine whether an individual is a qualified individual as a result of experiencing adverse financial consequences. Treasury and the IRS have received and are reviewing comments from the public requesting that the list of factors be expanded.

What is a coronavirus-related distribution?

A coronavirus-related distribution is a distribution that is made from an eligible retirement plan to a qualified individual from January 1, 2020, to December 30, 2020, up to an aggregate limit of $100,000 from all plans and IRAs.

Do I have to pay the 10% additional tax on a coronavirus-related distribution from my retirement plan or IRA?

No, the 10% additional tax on early distributions does not apply to any coronavirus-related distribution.

When do I have to pay taxes on coronavirus-related distributions?

The distributions generally are included in income ratably over a three-year period, starting with the year in which the client receives the distribution. For example, if the client received a $9,000 coronavirus-related distribution in 2020, they would report $3,000 in income on their federal income tax return for each of 2020, 2021, and 2022. However, the client has the option of including the entire distribution in their income for the year of the distribution.

May I repay a coronavirus-related distribution?

In general, yes, the client may repay all or part of the amount of a coronavirus-related distribution to an eligible retirement plan, provided that they complete the repayment within three years after the date that the distribution was received. If they repay a coronavirus-related distribution, the distribution will be treated as though it were repaid in a direct trustee-to-trustee transfer so that they do not owe federal income tax on the distribution.

If, for example, the client received a coronavirus-related distribution in 2020, and they chose to include the distribution amount in income over a 3-year period (2020, 2021, and 2022), and they choose to repay the full amount to an eligible retirement plan in 2022, they may file amended federal income tax returns for 2020 and 2021 to claim a refund of the tax attributable to the amount of the distribution that they included in income for those years, and they will not be required to include any amount in income in 2022.

What plan loan relief is provided under section 2202 of the CARES Act?

- 2202 of the CARES Act permits an additional year for repayment of loans from eligible retirement plans (not including IRAs) and relaxes limits on loans.

- Certain loan repayments may be delayed for one year: If a loan is outstanding on or after March 27, 2020, and any repayment on the loan is due from March 27, 2020, to December 31, 2020, that due date may be delayed under the plan for up to one year. Any payments after the suspension period will be adjusted to reflect the delay and any interest accruing during the delay.

- Loan limit may be increased: The CARES Act also permits employers to increase the maximum loan amount available to qualified individuals. For plan loans made to a qualified individual from March 27, 2020, to September 22, 2020, the limit may be increased up to the lesser of:

- (1) $100,000 (minus outstanding plan loans of the individual), or

- (2) the individual’s vested benefit under the plan.

Is it optional for employers to adopt the distribution and loan rules of §2202 of the CARES Act?

It is optional for employers to adopt the distribution and loan rules of §2202 of the CARES Act. An employer is permitted to choose whether, and to what extent, to amend its plan to provide for coronavirus-related distributions and/or loans that satisfy the provisions of §2202 of the CARES Act. Thus, for example, an employer may choose to provide for coronavirus-related distributions but choose not to change its plan loan provisions or loan repayment schedules. Even if an employer does not treat a distribution as coronavirus-related, a qualified individual may treat a distribution that meets the requirements to be a coronavirus-related distribution as coronavirus-related on the individual’s federal income tax return.

Does §2202 of the CARES Act provide additional distribution rights to participants or otherwise change the rules applicable to plan distributions?

Under §2202 of the CARES Act, a coronavirus-related distribution is treated as meeting the distribution restrictions for a §401(k) plan, §403(b) plan, or governmental §457(b) plan. For example, under §2202 of the CARES Act, a §401(k) plan may permit a coronavirus-related distribution, even if it would occur before an otherwise permitted distributable event (such as severance from employment, disability, or attainment of age 59½). However, the CARES Act does not otherwise change the limits on when plan distributions are permitted to be made from employer-sponsored retirement plans. For example, a pension plan (such as a money purchase pension plan) is not permitted to make a distribution before an otherwise permitted distributable event merely because the distribution, if made, would qualify as a coronavirus-related distribution. Further, a pension plan is not permitted to make a distribution under a distribution form that is not a qualified joint and survivor annuity without spousal consent merely because the distribution, if made, could be treated as a coronavirus-related distribution.

May an administrator rely on an individual’s certification that the individual is eligible to receive a coronavirus-related distribution?

The administrator of an eligible retirement plan may rely on an individual’s certification that the individual satisfies the conditions to be a qualified individual in determining whether a distribution is a coronavirus-related distribution, unless the administrator has actual knowledge to the contrary.

Although an administrator may rely on an individual’s certification in making and reporting a distribution, the individual is entitled to treat the distribution as a coronavirus-related distribution for purposes of the individual’s federal income tax return only if the individual actually meets the eligibility requirements.

Is an eligible retirement plan required to accept repayment of a participant’s coronavirus-related distribution?

In general, it is anticipated that eligible retirement plans will accept repayments of coronavirus-related distributions, which are to be treated as rollover contributions. However, eligible retirement plans generally are not required to accept rollover contributions. For example, if a plan does not accept any rollover contributions, the plan is not required to change its terms or procedures to accept repayments.

How do qualified individuals report coronavirus-related distributions?

If the client is a qualified individual, they may designate any eligible distribution as a coronavirus-related distribution as long as the total amount that they designate as coronavirus-related distributions is not more than $100,000. As noted earlier, a qualified individual may treat a distribution that meets the requirements to be a coronavirus-related distribution as such a distribution, regardless of whether the eligible retirement plan treats the distribution as a coronavirus-related distribution. A coronavirus-related distribution should be reported on the individual federal income tax return for 2020. They must include the taxable portion of the distribution in income ratably over the 3-year period – 2020, 2021, and 2022 – unless they elect to include the entire amount in income in 2020. Whether or not they are required to file a federal income tax return, they would use Form 8915-E (which is expected to be available before the end of 2020) to report any repayment of a coronavirus-related distribution and to determine the amount of any coronavirus-related distribution includible in income for a year.

How do plans and IRAs report coronavirus-related distributions?

The payment of a coronavirus-related distribution to a qualified individual must be reported by the eligible retirement plan on Form 1099-R, Distributions from Pensions, Annuities, Retirement or Profit-Sharing Plans, IRAs, Insurance Contracts, etc. This reporting is required even if the qualified individual repays the coronavirus-related distribution in the same year. The IRS expects to provide more information on how to report these distributions later this year.

Issue 8: DOL Announces Publication of Final E-Disclosure Rule

On May 21, 2020, the Department of Labor (DOL) announced its final rule on electronic disclosures, which is scheduled to was published on May 27th. The final rule allows employers to deliver participant disclosures primarily electronically. The DOL anticipates this will reduce plan costs by an estimated $3.2 billion over the next decade, while making disclosures more readily accessible and useful to plan participants. The final rule also preserves the right of participants to receive disclosures in paper form, if they choose.

Issue 9: 1040X Will Soon Be Ready to E-file

The Internal Revenue Service announced that later this summer taxpayers will for the first time be able to file their Form 1040-X, Amended U.S Individual Income Tax Return, electronically using available tax software products.

Making the 1040-X an electronically filed form has been a goal of the IRS for a number of years. It’s also been an ongoing request from the nation’s tax professional community and has been a continuing recommendation from the Internal Revenue Service Advisory Council (IRSAC) and Electronic Tax Administration Advisory Committee (ETAAC).

Currently, taxpayers must mail a completed Form 1040-X to the IRS for processing. The new electronic option allows the IRS to receive amended returns faster while minimizing errors normally associated with manually completing the form.

About 3 million Forms 1040-X are filed by taxpayers each year.

The new electronic filing option will provide the IRS with more complete and accurate data in an easily readable format to enable customer service representatives to answer taxpayers’ questions. Taxpayers can still use the “Where’s My Amended Return?” online tool to check the status of their electronically filed 1040-X.

When the electronic filing option becomes available, only tax year 2019 Forms 1040 and 1040-SR returns can be amended electronically. In general, taxpayers will still have the option to submit a paper version of the Form 1040-X and should follow the instructions for preparing and submitting the paper form. Additional enhancements are planned for the future.

Issue 10: IRS Extends Deadlines for Certain Taxes – Additional Time Granted – Notice 2020-35

Deadlines extended to June 30, 2020

With respect to the remedial amendment period and plan amendment rules for §403(b) plans, actions that were otherwise required to be performed on or before March 31, 2020, with respect to form defects or plan amendments are postponed to June 30, 2020.

Deadlines extended to July 15, 2020

The following tax deadlines have been extended to July 15, 2020:

Employers correcting employment tax reporting errors using the interest-free adjustment process.

- Employers correcting employment tax underpayments or overpayments.

- Exempt organizations filing Form 990-N, e-Postcard.

- Exempt organizations commencing a declaratory judgment suit.

- Single employer defined benefit plans applying for a funding waiver.

- Multi-employer defined benefit plans:

- Certifying funded status and giving notice to interested parties of that certification.

- Adopting, and notifying the bargaining parties of the schedules under, a funding improvement or rehabilitation plan and

- Providing the annual update of a funding improvement plan and its contribution schedules, or rehabilitation plan and its contribution schedules, and filing those updates with their annual return.

Cooperative and small employer charity (CSEC) plans:

- Making contributions required to be made for the plan year.

- Making required quarterly installments.

- Adopting a funding restoration plan and

- Certifying funded status.

Employee benefit plans filing Form 5330, Return of Excise Taxes Related to Employee Benefit Plans, and paying the associated excise tax.

In addition, the period beginning on March 30, 2020, and ending on July 15, 2020, will be disregarded in the calculation of any interest or penalty for failure to file the Form 5330 or to pay the excise tax postponed by the notice. Interest and penalties with respect to such postponed filing and payment obligations will begin to accrue on July 16, 2020.

Deadlines extended to July 31, 2020

Defined benefit plans have until July 31, 2020:

(1) to adopt a pre-approved defined benefit plan that was approved based on the 2012 Cumulative List.

(2) to submit a determination letter application under the second six-year remedial amendment cycle and

(3) to take actions that are otherwise required to be performed regarding disqualifying provisions in a plan during the remedial amendment period that would otherwise have ended on April 30, 2020.

Deadlines extended to August 31, 2020

The due date for filing and furnishing Form 5498, IRA Contribution Information, Form 5498-ESA, Coverdell ESA Contribution Information, and the Form 5498-SA, HSA, Archer MSA, or Medicare Advantage MSA Information, is postponed to August 31, 2020.

In addition, the period beginning on the original due date of those forms and ending on August 31, 2020, will be disregarded in the calculation of any penalty for failure to file those forms. Penalties with respect to such a postponed filing will begin to accrue on September 1, 2020.

Waiver of electronic filing requirement

The IRS has also provided a temporary waiver of the requirement that Certified Professional Employer Organizations (CPEOs) file certain employment tax returns, and their accompanying schedules, on magnetic media (including electronic filing).

This temporary waiver is extended to all CPEOs; individual requests for waiver do not need to be submitted.

This waiver applies only to Forms 941, Employer’s Quarterly Federal Tax Return, filed for the second, third, and fourth quarter of 2020 and only to Forms 943, Employer’s Annual Federal Tax Return for Agricultural Employees, filed for calendar year 2020, and their accompanying schedules.

Accordingly, CPEOs are permitted, but not required, to file a paper Form 941, and its accompanying schedules, in lieu of electronic submission for the second, third, and fourth quarters of calendar year 2020. In addition, CPEOs are permitted, but not required, to file a paper Form 943, and its accompanying schedules, in lieu of electronic submission for calendar year 2020.

Issue 11: TIGTA Report on Non-Filer – High Income Earners – Interesting to Say the Least

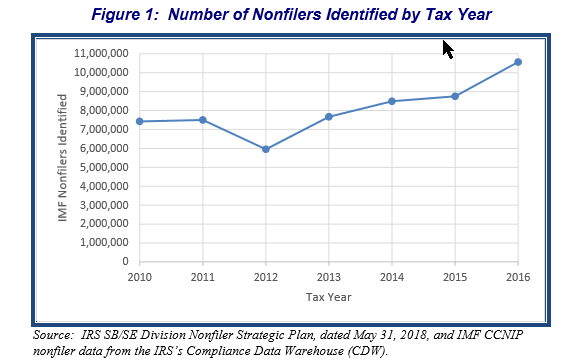

The gross Tax Gap is the estimated difference between the amount of tax that taxpayers should pay, and the amount paid voluntarily and on time. The average annual gross Tax Gap is estimated to be $441 billion for Tax Years 2011 through 2013, and approximately $39 billion (9 %) is due to non-filers, taxpayers who do not timely file a required tax return and timely pay the tax due for such delinquent returns.

According to the IRS, high-income non-filers, although fewer in number, contribute to the majority of the non-filer Tax Gap.

As mentioned previously, approximately $37 billion of the $441 billion average annual gross Tax Gap for TYs 2011 through 2013 is due to individual non-filers. According to the new non-filer strategy, high-income non-filers, although fewer in number, contribute to the majority of the non-filer Tax Gap.

IRS analyzed TYs 2014 through 2016 Individual Master File (IMF) inventory data to identify the number of high-income non-filers and matched the inventory against the IRS’s IMF database to determine the status of the high-income non-filers.

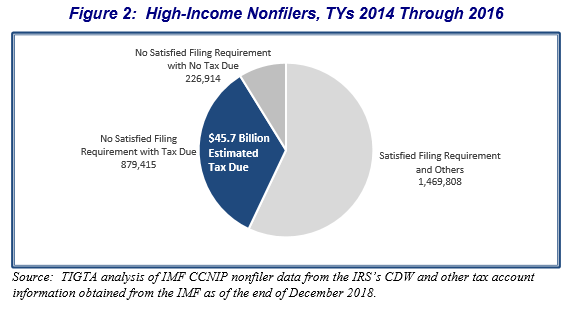

As of the end of December 2018, approximately 34 % (879,415/2,576,137) of the high-income non-filers did not have a satisfied filing requirement and had estimated tax due of $45.7 billion. Figure 2 summarizes the total number of high-income non-filers we identified during our analysis.

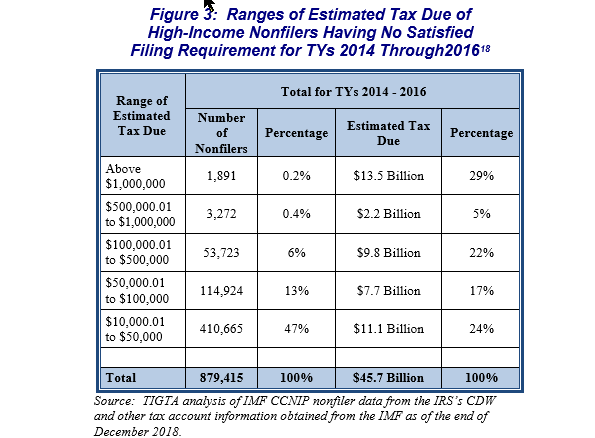

IRS found that a large portion of the estimated tax due involves a small portion of the high-income non-filers. Figure 3 above shows the 879,415 high-income non-filers that do not have a satisfied filing requirement in ranges based on the estimated tax due. Although the lowest two ranges account for approximately 80% of the total high-income non-filers, the estimated tax due for these ranges represents 27% of the $45.7 billion. In contrast, the highest two ranges account for less than 1 % of the total non-filers but represent approximately 34% of the total estimated tax due.

TIGTA Made Seven Recommendations

- Designating a senior management official with appropriate resources and specific non-filer duties to address non-filers.

- Not pausing the non-filer program.

- Working multiple tax year cases.

- Not removing high-income non-filer cases from the inventory without resolution.

The IRS disagreed with one of the recommendations, agreed with two recommendations, and partially agreed with four recommendations.

The IRS disagreed with placing the non-filer program under its own management structure.

The IRS agreed not to pause the Individual Master File Case Creation Non-filer Identification Process in the future, absent unusual circumstances.

Issue 12: Update on NOL Carrybacks for C Corporations from CARES Act

You may recall that one of the tax provisions in the CARES Act was to permit NOLs incurred in tax years 2018, 2019, and 2020 to be carried back five years to recover prior years’ taxes. For C Corporations, this created an unusual situation as it allowed carrying back an NOL from a tax regime in which there is no AMT (after TCJA) to a tax regime in which AMT existed (pre-TCJA). Under pre-TCJA there were two types of NOLs – regular NOLS and AMT NOLs. Thus, this change made by CARES presented a quandary – what would a C Corporation that generates an NOL in 2018, 2019, or 2020 do for AMT purposes in carrying back an NOL to prior years? Tax practitioners had raised this issue, but the IRS had not issued any guidance until yesterday (5/27/2020). The IRS issued on its website an FAQ that addressed this situation. Please see the attached PDF, and also this link to the webpage on the IRS website:

Here are a few comments from the IRS guidance provided on its website:

First, this is only for C Corporations, as individuals still have AMT in effect both before and after TJCA, thus, they will have regular NOLs and AMT NOLs in 2018, 2019, and 2020.

Next, the IRS indicated that the AMT NOL to use is -0- in the carryback of regular NOLs incurred in 2018, 2019, and 2020. Thus, if there is a regular NOL in say 2018, the AMT NOL in 2018 will be deemed to be -0-. When the Regular NOL is carried back five years, to the 2013 year, this may create an AMT in the 2013 year (or perhaps in the 2014, 2015, 2016, or 2017 years). This AMT triggered in 2013 (or other years) from the NOL carryback, then creates an AMT credit. This AMT credit is then allowed to be carried forward. Eventually the AMY credit will move into 2018 (post-TCJA), where AMT credits are allowed to be refunded.

Further, the CARES Act allowed AMT credits to be refunded in full, either in 2019 or electing to take in 2018 [new Section 53(e)(5) election]. I can help you with this election if you have any questions.

Thus, the NOL from post-2017 years can be carried back to the prior five years and then will likely create AMT credits that will be eventually be received in 2018, 2019, and 2020, but you need to navigate the filings on Form 1139.

The IRS has updated the filing procedures for these NOL carrybacks and AMT Credits, and these can, in some cases, be filed as part of the Form 1139 through the new NOL carryback procedures. Pleases review these 6 FAQs issued yesterday, and also the separate IRS guidance on sending in NOL carryback claims via Fax as explained in earlier e-mails. Here is the link to the IRS website for these revised filing procedures via Fax:

https://www.irs.gov/newsroom/temporary-procedures-to-fax-certain-forms-1139-and-1045-due-to-covid-19

Again, you should still consider filing these NOL carrybacks for C Corporations as they will likely lead to a permanent tax benefit with higher tax rates in prior years compared with the current 21%, but you will need to navigate these AMT credit hurdles. We should consider the extra costs in talking with our clients about working on these carryback returns. This extra time and fees are worth the additional tax benefit they are receiving and we should bill accordingly.

Stay tuned for additional COVID-19 webinars related to the Paycheck Protection Program Flexibility Act on our webinar schedule page.