Last December, Congress passed the Tax Cuts and Jobs Act. A few days later, President Donald Trump signed it into law. The sweeping tax reform that’s come as a result will have a dramatic impact on federal tax filers across a wide spectrum of income levels, types of employment, and personal financial situations.

If you’re a certified public accountant (CPA), enrolled agent (EA), certified tax preparer, or attorney, it’s important to fully understand what this multi-hundred page document will entail for your clients. It doesn’t matter whether you’re working with an individual who files single and receives a W2, a married couple filing jointly who co-own a business, a large corporate client, a small business owner, or any other type of client. Regardless, there are likely significant changes in store come tax time 2019, and you’ll need to be able to explain these changes to your clients.

If you’re a certified public accountant (CPA), enrolled agent (EA), certified tax preparer, or attorney, it’s important to fully understand what this multi-hundred page document will entail for your clients. It doesn’t matter whether you’re working with an individual who files single and receives a W2, a married couple filing jointly who co-own a business, a large corporate client, a small business owner, or any other type of client. Regardless, there are likely significant changes in store come tax time 2019, and you’ll need to be able to explain these changes to your clients.

With this in mind, we highly recommend signing up for a tax reform webinar in order to come to grips with the nitty gritty details of the Tax Cuts and Jobs Act. The legislation clocks in at over 1,100 pages and attempting to educate yourself about it without the help of a knowledgeable professional will be incredibly difficult. That said, it can be helpful to get a sense of some of the most important aspects of the new law, along with how certain changes to the tax code may impact federal tax filers.

With this in mind, we’ve put together this blog post on tax reform for employers. While individual filers will see a number of changes in their tax return come 2019, employers in particular have quite a bit to grapple with. You should expect many of your small business and/or corporate clients to look to you in the coming months as a source of information. They may already be browsing the web on their own, attempting to get a sense of what’s going to change for them when they file their 2019 taxes. When they come in for their annual review, you’ll want to be prepared to assuage their concerns and resolve any confusion they might have.

It would be impossible to cover every aspect of the tax reform bill that impacts employers in a single blog post. Instead, we’ll focus on some of the most important changes.

Topics that we’ll cover include:

- Employer-sponsored health plans and the ACA

- Tax credits for paid family and medical leave

- Fringe benefits

- Employee achievement awards and performance-based compensation

- Income tax withholding

…and more.

Ready? Let’s get started.

Employer-Sponsored Health Plans and the Affordable Care Act

Up until the Tax Cuts and Jobs Act was passed, the Affordable Care Act (ACA) carried with it what was called an “individual mandate.” This mandate required all individuals to maintain some sort of health coverage for themselves. If an individual was enrolled in Medicaid, Medicare, a university health plan, an employer-provided health plan, or any sort of private health insurance plan, they were considered to be in compliance with the mandate — provided that the plan met the requirements for minimum coverage as specified in the Affordable Care Act.

If an individual failed to maintain qualifying health coverage, they were considered to be in violation of the individual mandate. Anyone in violation of the individual mandate would then be required to pay a fee of either $695 or 2.5% of their household income — whichever was greater.

As part of the new tax reform law, the individual mandate has been repealed. Beginning in 2019, individuals will no longer be required to pay any sort of fee or penalty if they fail to maintain health coverage for themselves.

In the meantime, however, the IRS has clearly stated that it will not under any circumstances accept a 2017 tax return without verification of individual mandate compliance. In other words, all tax returns filed in 2018 for tax year 2017 must include evidence of enrollment in a valid health plan or payment of the individual mandate penalty.

It’s hard to say for certain what sort of impact this major change will have on employers. On the one hand, some employers might experience a reduction in the number of employees enrolled in their group health plan. This would be due to the fact that individuals are no longer penalized for failing to enroll, and some employees might choose to forego enrollment rather than pay for their portion of a monthly health insurance premium.

At the same time, though, employers might experience the opposite effect. The repeal of the individual mandate could very well increase the average cost of private health insurance plan premiums in state exchange marketplaces, or even cause some insurers to stop participating in the exchange altogether. If this happens, employer-sponsored plans may suddenly become the more affordable and attractive option for individuals who had previously obtain insurance from the exchange.

Keep in mind, too, that individual states might opt to implement their own individual mandates. As of now, Massachusetts has already done so. Meanwhile, there’s discussion of an individual mandate in other states around the country, including California, the District of Columbia, and Maryland.

Remember: The Tax Cuts and Jobs Act has not made any changes to reporting requirements or the health care mandate for employers. It’s important to remain in compliance with these requirements in the years to come.

Tax Credit for Paid Family and Medical Leave

If you provide paid family and medical leave to your employees, the tax reform law could be good news for you. Under the new law, employers who offer paid family and medical leave benefits to their employees may be eligible for a tax credit.

That said, there are certain eligibility requirements involved. In order to qualify for the credit, employers have to offer all of their full-time employees who qualify for leave to take at least two weeks of paid family and medical leave annually. Part-time employees must receive the same opportunity on a pro rata basis.

So, what does it mean for an employee to qualify for leave? Essentially, an employee must have worked for an employer for a minimum of one year, and their earnings from the prior tax year cannot be more than 60% of what’s considered the “highly compensated” threshold. This number is currently set at $120,000 per year for 2018. As a result, any employee making more than $72,000 in 2017 would not be considered “qualifying.” Thus, an employer would not be required to offer these employees a minimum of two weeks of paid family and medical leave in order to be eligible for the credit.

Keep in mind that certain other forms of leave cannot be counted towards this paid family leave requirement. For example, and employer who provides employees with personal leave, sick leave, vacation days, and so on cannot claim to be in compliance with the Family and Medical Leave Act as a result. Instead, an employer would have to offer paid family and medical leave (of at least two weeks for full-time employees earning less than 60% of the “highly compensated” threshold) in addition to this other leave. It isn’t entirely certain whether unspecified paid time off (that is, paid time off which is not classified according to a specific purpose, such as vacation leave) can be counted towards the requirement for the sake of filing for the credit.

Lastly, an employer must offer to pay a minimum of half of an employee’s standard wage during the time that they’re on leave. The tax credit itself is actually tied to the proportion of an employee’s standard compensation that’s offered to them while they’re on leave. Specifically, employers can deduct anywhere from 12.5 to 25% of the amount of leave paid out to employees.

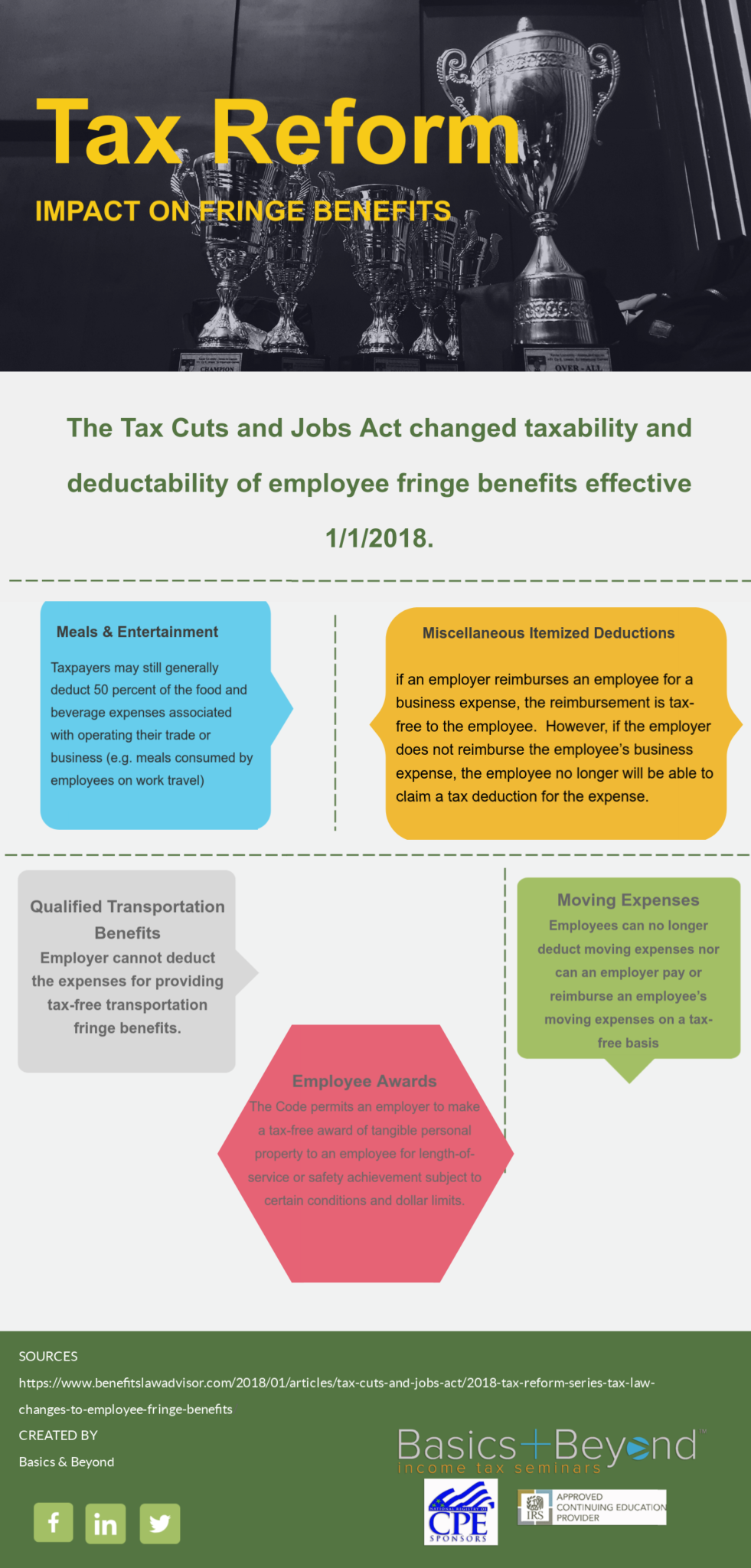

Employer Fringe Benefits

One area of the tax code where the Tax Cuts and Jobs Act makes significant and sweeping changes is fringe benefits offered by employers. Under the new tax reform law, transportation benefits, moving expenses, entertainment, and meals will all be treated differently.

Transportation Benefits

When it comes to transportation, the tax reform bill removes an employer’s ability to deduct so-called qualified transportation benefits. This includes things like parking, reimbursement for certain forms of commuting, and so on. The only way that these benefits can continue to be tax exempt is in the event that an employee pays for them with some sort of pre-tax reduction in their salary.

Moving Expenses

From 2018 until 2025, the tax reform law suspends two types of tax deductions for qualified moving expenses: those deductions taken by employees for non-reimbursable moving expenses related to work, and those related to employer-paid moving expenses. In other words, it will no longer be possible for any moving-related expenses to be deducted from one’s taxes, whether they were paid by the employer or the employee.

Entertainment

Beginning in 2018, employers will no longer be able to deduct entertainment-related activities from their taxes. This includes all sorts of activities which are currently deductible, such as fishing trips, rounds of golf, attending sporting events, and so on.

Meals

Under the new tax reform law, employers are no longer eligible to deduct any entertainment-related food or beverages from their tax liability. Additionally, on-site cafeterias for employees will be nondeductible as of 2026.

Employee Achievement Awards and Performance-Based Compensation

The Tax Cuts and Jobs Act will also change the way that employee achievement awards and other forms of performance-based compensation are treated from a tax perspective.

Up until the new tax law came into effect, an employer could offer various types of so-called “employee achievement awards” without said awards being subject to taxation. Under the new law, this tax exclusion will continue to apply to any sort of physical property awarded to the employee as a result of their achievement, be it a wallet, a jacket, or anything else. However, monetary awards and certain other items are no longer eligible. For example, awards such as cash, gift cards, vacations and trips, meals, stocks, or securities are now considered to be fully taxable income.

Federal Income Tax Withholding

Under prior tax law, employers were required to withhold federal taxes from their employees’ wages using methodology laid out according to the IRS. These requirements could be found in IRS Reg. §31.3402. The IRS updates Publication 15 each year with the applicable tax withholding tables for employers, along with instructions on how to determine withholding using specific percentages adjusted for annual inflation.

With the introduction of the new tax law, individual income tax rates have changed significantly. As a result, new withholding tables must be used for determining employee withholding amounts. Here are the changes for each tax bracket from 2017 (first amount) to 2018 (second amount):

- 10% remains at 10%

- 15% is lowered to 12%

- 25% is lowered to 22%

- 28% is lowered to 24$

- 33% is lowered to 32%

- 35% remains at 35%

- 6% is lowered to 37%

Prior to the implementation of the new tax law, supplemental withholding (that is, withholding of supplemental taxable wages) was allowed at a flat rate of 25% — provided that the amount of supplemental wages in a given tax year did not exceed $1,000,000. According to the new law, the percentage of withholding for supplemental wages must match the highest tax bracket (which is now 37%) is supplemental wages are in excess of $1,000,000. For wages up to $1,000,000, an employer may use a flat withholding rate of 22% (rather than 25%).

Tax Reform Webinar

The tax reform details laid out above are only intended to serve as an introduction to the incredibly complex and intricate changes that have accompanied the Tax Cuts and Jobs Act. If you’re a CPA or other tax professional, it’s essential that you bring yourself up to date with the tax reform law in order to provide your clients — especially those clients that are employers — with the highest level of service possible.

At Basics & Beyond™, we’re offering the most comprehensive, accurate, and frequently updated tax reform webinar available anywhere online. With more than 25 years of experience providing continuing professional education (CPE) training to accountants and tax professionals, Basics & Beyond your number one source for continuing education. Click here to sign up for a webinar today!