The Definitive Guide to Crowdfunding for Accountants and Tax Professionals

The Definitive Guide to Crowdfunding for Accountants and Tax Professionals

When starting a business, there are all sorts of options for funding. You might form an LLC and back it yourself with your own private funds. You could attempt to raise venture capital from accredited investors and form a C-Corporation. Or, you could distribute shares of an S-Corp to a limited number of initial investors. All of these options have their advantages and disadvantages, and the choice of which one makes the most sense for any particular business owner largely depends upon the particular circumstances surrounding the formation of that business. As an accountant or tax professional, you’re likely quite familiar with these forms of startup funding. However, there’s another approach to funding a startup that’s considerably newer and less familiar for many CPAs: crowdfunding. What is crowdfunding? What are some key terms relating to it? What kinds of crowdfunding models are the most common, and how do they work? What are the tax implications of raising money through crowdfunding for a new business? If you’re looking to learn more about crowdfunding, you’ve come to the right place. This guide will give you a broad overview of some of the most important elements of crowdfunding. We’ll answer the questions above, and you’ll gain a sense of how to treat crowdfunding from an accounting perspective when working with a new client. That said, if you’d like to learn all the ins and outs of crowdfunding, we highly recommend taking one of our crowdfunding webinars as part of your annual CPA or CPE requirements.

Ready to learn more about crowdfunding? Let’s get started.

What Is Crowdfunding?

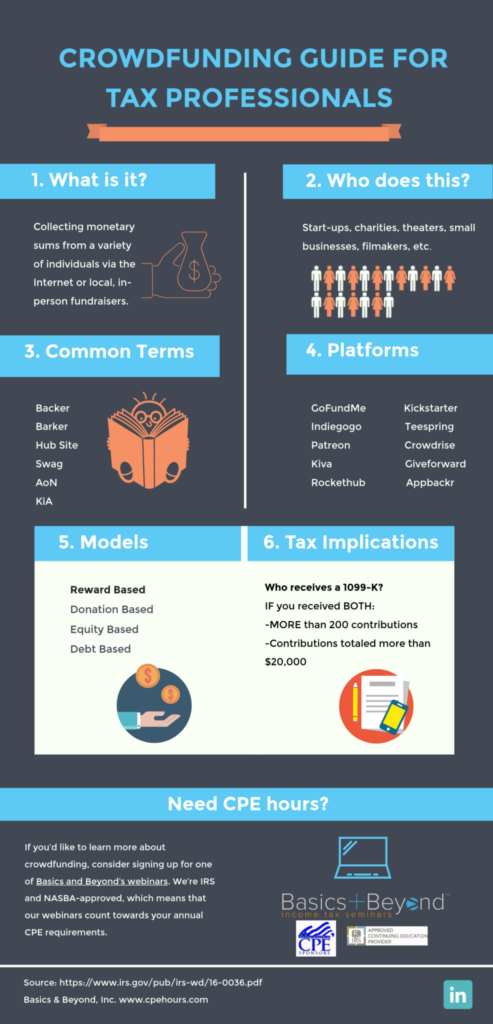

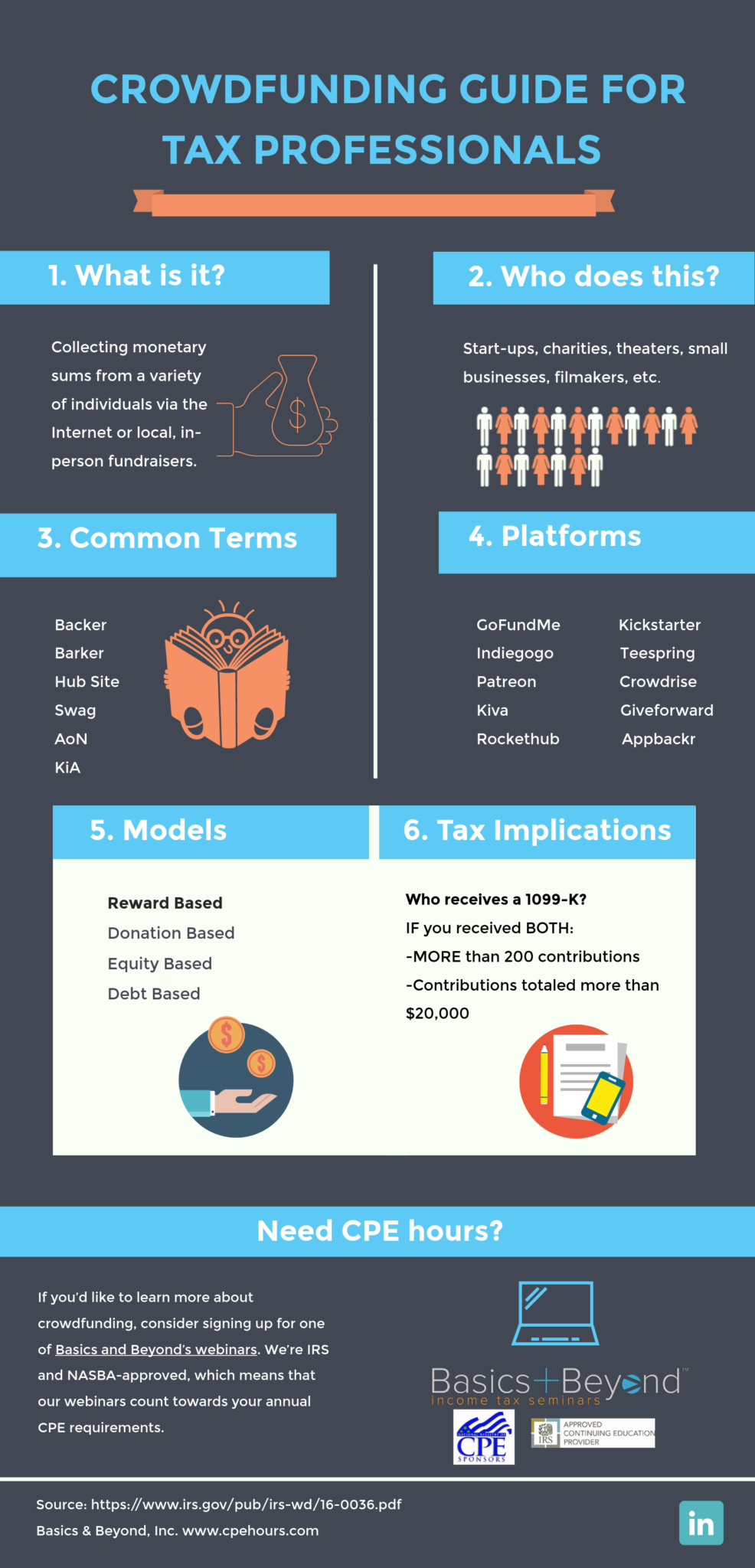

What exactly do we mean when we use the term “crowdfunding?” To put it simply, crowdfunding is the act of funding a new startup or project by collecting monetary sums from a variety of individuals (commonly referred to as “backers”) via the Internet or local, in-person fundraisers. Internet crowdfunding has exploded in popularity in recent years, and the majority of people tend to think of this model when they hear the term “crowdfunding.”

Crowdfunding continues to grow in popularity as a means of generating the necessary capital to fund all sorts of projects and businesses. This can include everything from local community development to launching a small business, or even paying off sudden personal expenses. This fundraising model gives the individual or entity that’s doing the fundraising the ability to bypass the standard means of raising money for a new venture, such as bank loans or venture capital. Crowdfunding can be a one-off event, or it can go on for an extended period of time.

Crowdfunding Lingo

With every funding approach, there are all sorts of technical terms involved that are specific to that method of fundraising. Crowdfunding is no different. And, even if we’re talking about crowdfunding, we’ll often need to refer to technical terms related to other fundraising formats of the sake of illustrating both similarities and differences. With that in mind, we’ve put together this brief list of common crowdfunding and fundraising terms. Remember, this list is far from exhaustive: it’s just meant to give you an overview of some key terms related to fundraising. If you’re looking for more in depth information, consider fulfilling your annual CPE requirements by signing up for one of our webinars.

- Backer: A backer is someone who has made a monetary contributed to a crowdfunding project. Backers often receive something in exchange for their contribution.

- Barker: This term refers to someone who uses various digital promotional techniques — especially including (but not limited to) social media — to help spread the word about a crowdfunding project.

- Fan: A fan is someone who is interested in a crowdfunding project, but who may not have yet made any sort of contribution to it. Fans are often “barkers” rather than “backers”: they may work to promote a project and help create a buzz for it rather than contributing to it themselves.

- Honor roll: This refers to the list of backers who have contributed to a project.

- Hub site: Hub sites are websites designed specifically for hosting crowdfunding projects. See the “common crowdfunding platforms” section below.

- Landing page: This is a web page designed specifically for the crowdfunding project. This page is where a user who wants to contribute the project first “lands” after clicking a link to learn more about the project itself. Landing pages are generally designed with conversion in mind: they present visitors with an overview of the project, some information on why it matters, an explanation of what the creator’s funding needs are, and a call to action urging visitors to contribute.

- Patron: Also known as a donor or sponsor, these are people who have made a monetary contribution to a particular project.

- Perk: Perks are benefits given to patrons/donors who contribute to a crowdfunding campaign. These perks are meant to reward donors for their contribution, and often vary based on the size of the donation.

- Progress meter: The vast majority of crowdfunding campaigns will feature a progress meter on their landing page. This shows visitors (including both prior donors as well as potential backers and fans) where the campaign is in its progress, and how close it is to meeting its goal.

- Swag: Swag is often used interchangeably with “perk” to describe gifts given to donors. Swag is usually promotional in nature and is often heavily branded.

- Third party settlement organization: This is the “merchant acquiring entity” which receives credit card transactions on behalf of the crowdfunding campaign’s creator. This organization must then pay out the final sum of collected donations to the creator. A 1099-K form is often issued in connection with this payout, as we’ll discuss in greater detail below.

- All or Nothing (AoN) vs. Keep it All (KiA): These terms refer to the type of funding method associated with a campaign. With the All or Nothing method, funds collected from contributors are only released to the project creator if a predetermined fundraising threshold is met or exceeded. If the fundraising goal isn’t met, contributors’ accounts will not actually be debited (or, if they were already debited, the debited funds will be returned). With the Keep it All methods, funds are distributed to the project creator regardless of whether or not the predetermined fundraising goal was met. The initiator of the campaign can then determine on their own whether they want to refund contributions or go ahead with the project.

Common Crowdfunding Platforms

While it’s possible to set up your own website and third-party merchant acquiring entity in order to process transactions and run a crowdfunding campaign, it’s much more common for crowdfunding to take place via an established online platform. While new crowdfunding platforms are springing up every day, a handful of them are the ones you’re most likely to run into. Some are targeted more at small businesses, others are non-profits, and still others are tech startups and app developers.

Common crowdfunding platforms include:

- GoFundMe

- Kickstarter

- Indiegogo

- Teespring

- Patreon

- com

- Crowdrise

- org

- Kiva

- Giveforward

- Rockethub

- Appbackr

Crowdfunding Models

Depending on the needs of your particular project, there are multiple approaches one can take to crowdfunding. Each individual model has its own advantages and disadvantages, and the decision of which one to use is largely based on the type of project you’re attempting to launch. Let’s take a look at the four most common models for crowdfunding: reward-based, donation-based, equity-based, and debt-based.

- Reward-based crowdfunding: This involves selling specific items before the launch of a new project, product, or business. The items involved in the pre-sale can only be completed if the funding goal of the campaign is met or exceeded. This generally means that reward-based crowdfunding projects are All or Nothing (AoN). A reward-based campaign isn’t generally targeted at investors who are looking to profit from their investment. Instead, these kinds of crowdfunding projects generally attract people who are excited about a particular product or project, and who want to be the first to own a new product before anyone else has access to it. As a result, the vast majority of reward-based crowdfunding projects need initial investors before they can get started.

- Donation-based crowdfunding: With donation-based crowdfunding, investors make “donations” to a project or company and receive a product of some kind in return. This is similar to reward-based crowdfunding, except that it may include products as rewards which already exist rather than a product that has yet to be developed. Additionally, some forms of donation-based crowdfunding don’t involve any sort of reward. Instead, donors opt to contribute because they want to further a particular cause.

- Equity-based crowdfunding: Unlike reward-based or donation-based crowdfunding, an equity-based approach is targeted at investors. An individual investor can make a contribute which then entitles them to a share of the soon-to-launch company. This is essential a form of shareholder investment: the donor becomes a shareholder in the new company once it has launched. This shareholder often has voting rights related to decisions that pertain to the new company. This investor can also sell their share at a later date (or a portion of their share) at whatever that share’s current market value might be. Equity-based crowdfunding involves the same risks as any other type of equity-based investment: there’s a chance that the company could fail, in which case the investor’s shares would be worthless.

- Debt-based crowdfunding: With a debt-based crowdfunding model, a backer can contribute to an organization which then makes a loan to a business that’s looking to crowdfund, with the intention of subsequently getting their money back with additional interest. This is also sometimes referred to as peer-to-peer lending (p2p lending).

How Does Crowdfunding Usually Work?

Now that you understand what crowdfunding is, what some of its key terms are, and what models are generally used, you might be wondering: how does it actually work?

These days, the vast majority of crowdfunding — particularly the kind that most people have in mind when they hear the term — happens online. As a result, credit cards are the go-to payment method for backers. Rather than receiving a contribution directly, most crowdfunding initiators will opt to work with a third-party settlement organization to process all of their contributors’ payments. As you might have guessed, though, these services aren’t free: crowdfunding platforms generally charge a percentage fee of the total amount raised, which can be as low as a few percent or as high as 15% depending on the platform.

All sorts of projects make their way into the crowdfunding sphere, including venture investments, mobile apps, personal expense funding needs, and new business startups.

Tax Implications and Form 1099-K

As an accounting professional, you may be thinking: alright, this is all well and good. But, what about tax liability? How do you account for these funds?

As it turns out, the answer to those questions can be a bit complicated. While many people think of crowdfunding as a simple, straightforward way to raise money for a new project, it can actually be more than a little complex once tax time rolls around. As an accounting professional, your clients who have launched crowdfunding-based ventures will look to you for advice. Remember, in addition to what you’ve learned here, you can further your education about crowdfunding by fulfilling part of your annual CPE requirements with a Basics & Beyond™ CPE webinar.

Will I Receive a Form 1099-K?

Not every crowdfunding creator will end up receiving a 1099-K form from the platform that they use to host the campaign. Rather, you’ll only receive a Form 1099-K if you received both more than 200 contributions, and if those contributions totaled more than $20,000. If either of those requirements isn’t met, you won’t be receiving a 1099-K and you’ll be expected to account for the contributions on your own.

Remember that if you receive a 1099-K, the IRS will receive a matching form and will be looking for income tax and possible self-employment tax as well. If the amount you’ve received isn’t income, you’ll need to prove it. As an accountant or tax professional, you’ll need to determine what the contributions actually count as. Are they gifts with no expectation of value in return? Are they business income? Could they be considered a charitable donation? Or, are they an equity contribution? Depending on the answer to these questions, you’ll need to classify the 1099-K income differently on your client’s tax returns. Remember, the amount on the 1099-K must still be reported somewhere on your client’s tax return, even if it’s exempt from federal income tax.

Learn More About Crowdfunding

In this guide, we’ve attempted to go into as much detail as possible about crowdfunding. When it comes to taxes, though, there’s enough information related to crowdfunding to fill up an entire CPE webinar. If you’d like to learn more about crowdfunding, consider signing up for one of Basics and Beyond’s webinars. We’re NASBA-approved, which means that our webinars count towards your annual CPE requirements in the vast majority of states. Click here to see our affordable prices.