2022 Tax Season Begins on January 24th 2022, and Announces Deadline Information

In This Issue

- List of Provisions Expiring in 2021 – Tax Planning Issues

- The 2022 Form W-4 Employee’s Withholding Certificate

- IRS Corrects the American Opportunity Tax Credit Identification Requirement in the FAQ’s

- IRS Announced Delays in Processing Employer Credit Advanced Payments

- FS-2022-02 Announcement Updates Information Concerning the Recovery Rebate Credit, FAQ’s

- Advance Payment of Child Tax Credit—2021 Recovery Rebates to Individuals — Economic Impact Payments — Information Letters

- New PPP Loan Information Required on 1040, 1102, 1120-S and Form 1065 – Applies to All Entities that Received a PPP Loan – Not All Instructions Final

- Identity Verification Issues Letters 5071C, 5747C, 6331C or 5447C as Well as 4883C or a 6330C – What’s the Difference and How to Respond

- Summary of My Recommendations for IRS Improvement – Provided to a National Tax Professional Organization Upon Request – It Cannot Hurt to Ask

- Update on Medicare Income Thresholds and Costs 2022

- Taxpayer Advocate Preface of their Annual Report _ Interesting to Say the Least – No Holds Barred – An Honest Evaluation – Full Report: 2021 Annual Report to Congress – Taxpayer Advocate Service (irs.gov)

- Issue 13: FQA on Over-the-Counter COVID Tests

- Q and A from January 2021 Filing Season Webinars

- Recovery Rebate FAQ’s

- Applicable Federal Rates for February 2022, Rev. Rul. 2022-3

Issue 1: 2022 Tax Season Begins on January 24, 2022, and Announces Deadline Information

The Internal Revenue Service announced that the nation’s tax season will start on Monday, Jan. 24, 2022, when the tax agency will begin accepting and processing 2021 tax year returns.

Like last year, there will be individuals filing tax returns who, even though they are not required to file, need to file a 2021 return to claim a Recovery Rebate Credit to receive the tax credit from the 2021 stimulus payments or reconcile advance payments of the Child Tax Credit. People who don’t normally file also could receive other credits.

IRS Free File will open January 14 when participating providers will accept completed returns and hold them until they can be filed electronically with the IRS. Many commercial tax preparation software companies and tax professionals will also be accepting and preparing tax returns before January 24 to submit the returns when the IRS systems open.

April 18 Tax Filing Deadline for Most – Certain States Get a Few Extra Days to File

The filing deadline to submit 2021 tax returns or an extension to file and pay tax owed is Monday, April 18, 2022, for most taxpayers.

By law, Washington, D.C., holidays impact tax deadlines for everyone in the same way federal holidays do. The due date is April 18, instead of April 15, because of the Emancipation Day holiday in the District of Columbia for everyone except taxpayers who live in Maine or Massachusetts.

Taxpayers in Maine or Massachusetts has until April 19, 2022, to file their returns due to the Patriots’ Day holiday in those states. Taxpayers requesting an extension will have until Monday, Oct. 17, 2022, to file.

Watch for IRS Letters About Advance Child Tax Credit Payments and Third Economic Impact Payments

The IRS started sending Letter 6419, 2021 advance Child Tax Credit, in late December 2021 and continues to do so into January. The letter contains important information that can help ensure the return is accurate. People who received the advance CTC payments can also check the amount of the payments they received by using the CTC Update Portal available on IRS.gov.

Eligible taxpayers who received advanced Child Tax Credit payments should file a 2021 tax return to receive the second half of the credit. Eligible taxpayers who did not receive advanced Child Tax Credit payments can claim the full credit by filing a tax return.

The IRS will begin issuing Letter 6475, Your Third Economic Impact Payment, to individuals who received a third payment in 2021 in late January.

Key Filing Season Dates

- January 14: IRS Free File opens. Taxpayers can begin filing returns through IRS Free File partners; tax returns will be transmitted to the IRS starting January 24. Tax software companies also are accepting tax filings in advance.

- January 18: Due date for tax year 2021 fourth quarter estimated tax payment.

- January 24:IRS begins 2022 tax season. Individual 2021 tax returns begin being accepted and processing begins.

- April 18:Due date to file 2021 tax return or request extension and pay tax owed due to Emancipation Day holiday in Washington, D.C., even for those who live outside the area.

- April 19:Due date to file 2021 tax return or request extension and pay tax owed for those who live in MA or ME due to Patriots’ Day holiday.

- October 17:Due date to file for those requesting an extension on their 2021 tax returns.

Issue 2: List of Provisions Expiring in 2021 – Tax Planning Issues

| Provision and Code Section | Expiring Date |

| Refundability and enhancement of child and dependent care tax credit (§ 21(g)) | 12/31/21 |

| Child tax credit: Increased credit amount (subject to lower phaseout thresholds), credit for 17-year-olds, fully refundable credit with no earned income phase-in, and safe harbor for excess advance payments (§ 24(i) and (j)) | 12/31/21 |

| Credit for certain nonbusiness energy property (§ 25C(g) | 12/31/21 |

| Credit for qualified fuel cell motor vehicles (§ 30B(k)(1) | 12/31/21 |

| Credit for alternative fuel vehicle refueling property (§ 30C(g)) | 12/31/21 |

| Credit for two-wheeled plug-in electric vehicles (§ 30D(g)(3)(E)(ii)) | 12/31/21 |

| Earned income tax credit: Special rules for individuals without qualifying children (§ 32(n)) | 12/31/21 |

| Credit for health insurance costs of eligible individuals (§ 35(b)(1)(B))

|

12/31/21 |

| Premium assistance credit special rule for individuals who receive unemployment compensation (§ 36B(g)) | 12/31/21 |

| Second generation biofuel producer credit (§40(b)(6)(J))

|

12/31/21 |

| Increase in State low-income housing tax credit ceiling (§ 42(h)(3)(I))

|

12/31/21 |

| Beginning-of-construction date for renewable power facilities eligible to claim the renewable electricity production credit or investment credit in lieu of the production credit (§§ 45(d) and 48(a)(5)) | 12/31/21 |

| Credit for production of Indian coal (§ 45(e)(10)(A)) | 12/31/21 |

| Indian employment credit (§ 45A(f)) | 12/31/21 |

| Credit for construction of new energy efficient homes (§ 45L(g)) | 12/31/21 |

| Mine rescue team training credit (§ 45N(e)) | 12/31/21 |

| Increase in exclusion for employer provided dependent care assistance (§ 129(a)(2)(D)) | 12/31/21 |

| Treatment of premiums for certain qualified mortgage insurance as qualified residence interest (§ 163(h)(3)(E)(iv)) | 12/31/21 |

| Computation of adjusted taxable income without regard to any deduction allowable for depreciation, amortization, or depletion for purposes of the limitation on business interest (§ 163(j)(8)(A)(v)) | 12/31/21 |

| Three-year recovery period for racehorses two years old or younger (§ 168(e)(3)(A)) | 12/31/21 |

| Accelerated depreciation for business property on an Indian reservation (§ 168(j)(9)) | 12/31/21 |

| Charitable contributions deductible by nonitemizers (§ 170(p)) | 12/31/21 |

| Payroll tax credit for paid sick leave (§ 3131(h)) | 9/30/21 |

| Payroll tax credit for paid family leave (§ 3132(h)) | 9/30/21 |

| Employee retention and rehiring tax credit (§ 3134(n)) | 9/30/21 |

| Black Lung Disability Trust Fund: Increase in excise tax on coal (§ 4121(e)(2)) | 12/31/21 |

| Incentives for alternative fuel and alternative fuel mixtures:

Excise tax credits and outlay payments for alternative fuel (§§ 6426(d)(5) and 6427(e)(6)(C)) Excise tax credits for alternative fuel mixtures (§ 6426(e)(3)) |

12/31/21 |

| 2021 recovery rebates to individuals (§ 6428B) | 12/31/21 |

| Advance payment of child tax credit (§ 7527A(f)) | 12/31/21 |

| Temporary increase in limit on cover over of rum excise tax revenues (from $10.50 to $13.25 per proof gallon) to Puerto Rico and the Virgin Islands (§ 7652(f)) | 12/31/21 |

| American Samoa economic development credit (§ 119 of Public Law 109-432, as amended) | 12/31/21 |

| Modification of limitation on charitable contributions

(§ 2205 of Public Law 116-136, as amended) |

12/31/21 |

| Prevention of partial plan termination (§ 209 of Division EE of Public Law 116-260)6 | 12/31/21 |

| Special rule for health and dependent care flexible spending arrangements (§ 214 of Division EE of Public Law 116-260) | 12/31/21 |

| Premium assistance for COBRA continuation coverage

(§ 9501 of Public Law 117-2) |

09/30/21

|

| Earned income credit special rule for determining earned income (§ 9626 of Public Law 117-2) | 12/31/21 |

| Credit for sick leave for certain self-employed individuals (§ 9642 of Public Law 117-2) | 9/30/21 |

| Credit for family leave for certain self-employed individuals (§ 9643 of Public Law 117-2) | 9/30/21 |

| Temporary extension of the funding improvement and rehabilitation periods for multiemployer pension plans in critical and endangered status for 2020 or 2021 (§ 9702 of Public Law 117-2) | 12/31/21 |

| Adjustments to funding standard account rules (§ 9703 of Public Law 117-2) | 12/31/21 |

Issue 3: The 2022 Form W-4 Employee’s Withholding Certificate

With the 2022 version of Form W-4, Employee’s Withholding Certificate, currently available, now is an opportune time for taxpayers to review their withholding information. Though the form remains unchanged since it was overhauled for 2020, individuals and families may want to adjust their withheld amounts to reflect life changes that occurred in the past year.

Issue 4: IRS Corrects the American Opportunity Tax Credit Identification Requirement in the FAQ’s

The IRS has revised its Education Credits FAQs to correctly represent who needs a taxpayer identification number in order to claim the American opportunity credit (AOTC).

The revised FAQ now notes that “You can’t claim the AOTC on either an original or an amended return if the student (you, your spouse or your dependent student claimed on the return) didn’t have a taxpayer identification number by the due date of your return (including extensions), even if the student later gets one of those numbers.”

Previously, the note read, “You can’t claim the American opportunity credit on either an original or an amended return if either you or the student didn’t have a taxpayer identification number by the due date of your return (including extensions), even if you or the student later gets one of those numbers.”

Issue 5: IRS Announced Delays in Processing Employer Credit Advanced Payments

Expect payment delays until late January for Form 7200, Advance Payment of Employer Credits Due to COVID-19. Taxpayers may continue to file Forms 7200 by fax until Jan. 31, and their applicable employment tax returns by the required due date.

Issue 6: FS-2022-02 Announcement Updates Information Concerning the Recovery Rebate Credit, FAQ’s

Topic F: Finding the First and Second Economic Impact Payment Amounts to Calculate the 2020 Recovery Rebate Credit

Clients can access their online account through a secure login at IRS.gov/account. They can also find the online account application by going to the IRS.gov homepage and clicking on “Sign into Your Account.”

Where do I find my first and second Economic Impact Payment amounts in my online account?

- When the client accesses their online account, go to the Tax Records tab/page to find the Economic Impact Payment amounts needed need for calculating the 2020 Recovery Rebate Credit. Once on the page, they will see the amounts of the first and second Economic Impact Payments under the section “2020 Economic Impact Payment Information.”

If the client and their spouse received joint payments, each of them will need to sign into their own account to retrieve their separate amounts.

- Both the first and second payment amounts should be used to calculate the Recovery Rebate Credit, such as by entering them on the applicable lines in the Recovery Rebate Credit Worksheet found in the 2020 Form 1040 and Form 1040-SR instructions.

If the client filed a joint 2020 tax return with the same spouse, combine their first and second payment amounts to calculate the Recovery Rebate Credit.

Issue 7: Advance Payment of Child Tax Credit—2021 Recovery Rebates to Individuals — Economic Impact Payments — Information Letters

IRS announced that it will send Letter 6419 to advance CTC recipients, which will include total amount of advance CTC payments recipients received in 2021 and number of qualifying children used to calculate advance payments, to help recipients reconcile and receive all CTCs that they are entitled to receive.

In addition, IRS announced that it will begin issuing Letter 6475 to recipients of 3d round of EIPs to help recipients determine if they are entitled to and should claim recovery rebate credit on their 2021 returns that they file in 2022.

Issue 8: New PPP Loan Information Required on 1040, 1102, 1120-S and Form 1065 – Applies to All Entities that Received a PPP Loan – Not All Instructions Final _ More to Come

Protection Program (PPP) Loans The forgiveness of a PPP Loan creates tax-exempt income, so although you don’t need to report the income from the forgiveness of your PPP Loan on Form 1040 or 1040-SR, you do need to report certain information related to your PPP Loan.

Rev. Proc. 2021-48, 2021-49 I.R.B. 835, permits taxpayers to treat tax-exempt income resulting from the forgiveness of a PPP Loan as received or accrued: (1) as, and to the extent that, eligible expenses are paid or incurred; (2) when you apply for forgiveness of the PPP Loan; or (3) when forgiveness of the PPP Loan is granted.

If you have tax-exempt income resulting from the forgiveness of a PPP Loan, attach a statement to your return reporting each taxable year for which you are applying Rev. Proc. 2021-48, and which section of Rev. Proc. 2021-48 you are applying—either section 3.01(1), (2), or (3).

Any statement should include the following information for each PPP Loan:

- Your name, address, and ITIN or SSN; 2.

- A statement that you are applying or applied section 3.01(1), (2), or (3) of Rev. Proc. 2021-48, and for what taxable year (2020 or 2021) as applicable

- The amount of tax-exempt income from forgiveness of the PPP Loan that you are treating as received or accrued and for what taxable year (2020 or 2021); and

- Whether forgiveness of the PPP Loan has been granted as of the date you file your return. Write “RP2021-48” at the top of your attached statement.

Section 3.01, 02 and 03 are below:

01 Overview. Subject to section 3.03 of this revenue procedure, a taxpayer that

received a PPP Loan may treat tax-exempt income resulting from the partial or

complete forgiveness of such PPP Loan as received or accrued:

(1) As, and to the extent that, the taxpayer pays or incurs eligible expenses as described in section 2.01(2). Under this section 3.01(1), a taxpayer that has elected to use the safe harbor provided under Revenue Procedure 2021-20 will be treated as paying or incurring the eligible expenses during the taxpayer’s immediately subsequent taxable year following the taxpayer’s 2020 taxable year in which the expenses were actually paid or incurred, as described in Revenue Procedure 2021-20.

(2) When the taxpayer files an application for forgiveness of the PPP Loan; or

(3) When the PPP Loan forgiveness is granted.

02 Amended returns

Taxpayers may report tax-exempt income pursuant to section 3.01 on a timely filed original or amended Federal income tax return, information return or administrative adjustment request (AAR) under § 6227 of the Code. See also Revenue Procedure 2021-50, 2021-49 I.R.B. ___, released November 18, 2021, allowing an eligible partnership to file an amended Form 1065, U.S. Return of Partnership Income, as an alternative to filing an AAR, and furnish a corresponding amended Schedule K-1 (Form 1065), Partner’s Share of Income, Deductions, Credits, etc., to each of its partners. Partners and shareholders that receive amended Forms K1 as provided in this section 3.02 must file amended Federal income tax returns, information returns or AARs, as applicable, consistent with the Forms K-1 received.

03 When PPP Loan is not fully forgiven

Unless otherwise provided in the 2021 filing year form instructions, if the taxpayer receives forgiveness for an amount of the PPP Loan that is less than the amount that the taxpayer previously treated as tax exempt income, the taxpayer must make appropriate adjustments on an amended Federal income tax return, information return or AAR, as applicable, for the taxable year(s) in which the taxpayer treated tax-exempt income from the forgiveness of such PPP Loan as received or accrued. Partners and shareholders that receive amended Forms K-1 as provided in this section 3.03 must file amended Federal income tax returns, information returns or AARs, as applicable, consistent with the Forms K-1 received.

Issue 9: Identity Verification Issues Letters 5071C, 5747C, 6331C or 5447C as Well as 4883C or a 6330C – What’s the Difference and How to Respond

IRS has a secure Identity Verification Service to verify the client’s identity available 24 hours a day.

Letters 5071C and 6331C Instructions – Using the Online System Only

- The client must register to the website through ID.me (create before verifying your identity). Be sure to check the website and prepare all the documents needed to complete the registration.

- The client needs to have a copy of the 5071C or 6331C letter they received and a copy of the tax return for the tax year shown in the letter.

- If the person did not file an income tax return, they can indicate that on the website.

If the client prefers to talk to an IRS representative, they can call the toll-free IRS Identity Verification telephone number in the 5071C or 6331C letter.

Although the letters request a response within 30 days, the IRS will continue to work with the client regardless of the amount of days that have passed.

Have ALL of the following available when you call:

- The 5071C or 6331C letter.

- The tax return referenced in the letter (the Form 1040 series return). Note: A Form W-2, Form 1099 is not a tax return.

- A prior year’s income tax return, other than the year in the letter, if you filed one. Note: A Form W-2, Form 1099 is not a tax return; and

- Supporting documents that you filed with each year’s tax return. (Form W-2, Form 1099, Schedule C or F, etc.).

Note: Authorized third parties may assist taxpayers, but the taxpayer must call us together and must participate on the call.

The toll-free number IRS Identity Verification number is for identity verification only. No other tax-related information, including refund status, is available.

If the client is incarcerated, they will need to coordinate with a Prison Official.

Until IRS hears from the client, they will not be able to process the tax return, issue refunds, or credit any overpayments to the client’s account.

If the client cannot verify their identity online or over the phone, IRS will ask them to schedule an appointment and bring the documents listed above to a local IRS office to verify in person. The schedule an appointment call: 844-545-5640

If the client can successfully verify their identity, IRS will process the tax return. It will take up to 9 weeks to receive any refund or credit any overpayment to the client’s account. However, IRS finds other problems, IRS will contact the client again by letter. This will delay your refund more.

Letter 5747 C – What to Do?

Online

- If the client received the option to verify their identity online, use the IRS secure Identity Verification Service, available 24 hours a day, by creating an online account through ID.me.

- Have a copy of the 5747C letter received and a copy of the tax return for the tax year shown in the letter.

- The client can use this option if they did or didn’t file a tax return.

If the client did not file

- Call the IRS Identity Verification number on the letter to tell IRS they did not file a tax return.

If the client did file, schedule an in-person appointment

Call the Taxpayer Assistance Center toll-free at the number on the letter.

Please note:

- Authorized third parties may assist taxpayers, but the client must be present in-person.

- Although the letters request a response within 30 days, the IRS will continue to work with the client regardless of the amount of days that have passed.

Bring the following to the appointment

- The 5747C letter.

- The income tax return referenced in the letter (the Form 1040 series return).

- A previous year’s income tax return, other than the year in the letter, if the client filed one.

Note: A Form W-2 or Form 1099 is not a tax return. - Supporting documents that the client filed for each year’s income tax return (Form W-2, Form 1099, Schedule C or F, etc.).

Bring the following Identity Verification Documents to the appointment

- A valid U.S. federal or state government-issued picture identification, such as a driver’s license, state ID, or passport.

At least ONE of the following forms of identification:

- Current U.S. federal or state government-issued identification that is different from the first document provided.

- U.S. Social Security card; mortgage statement with current address.

- Lease agreement for a house or apartment with current address.

- Car title.

- Voter registration card (not the voter registration application).

- Utility bill with current address.

- Birth certificate (the IRS no longer accepts Puerto Rican birth certificates issued before July 1, 2010); or

- Current school records.

If IRS does not hear from the client

IRS may not be able to process the return, issue refunds, or apply overpayments to next year’s estimated tax.

The letter applies to identity verification only. No other tax-related information, including refund status, is available at the IRS Identity Verification telephone number provided on your letter.

Letter 5447 C – What to Do?

If the client did not file:

Contact IRS immediately to confirm if they may be a victim of tax-related identity theft, or write to IRS within 15 days, include copies of the requested information and mail it to the address on the letter.

If the client did file, call or write to verify their identity

- Call the IRS Identity Verification number on the letter. Have the following available when calling:

- The 5447C letter.

- The income tax return referenced in the letter (the Form 1040 series return).

Note: A Form W-2 or Form 1099 is not a tax return. - A previous year’s tax return, other than the year in the letter, if you filed one.

Note: A Form W-2 or Form 1099 is not a tax return. - Supporting documents that you filed with each year’s income tax return (Form W-2, Form 1099, Schedule C or F, etc.).

- If the client prefers to write, write to IRS within 15 days of receiving the letter and include copies of the requested information. Mail the information to the address on the letter.

Note: Although the letters request a response within 30 days, the IRS will continue to work with the case regardless of the amount of days that have passed.

If IRS does not hear from the client

IRS may not be able to process the return, issue refunds, or apply overpayments to next year’s estimated tax.

The toll-free and non-toll-free numbers are for identity verification only. No other tax-related information, including refund status, is available.

Letter 4883C and 6330C – What to Do?

Call IRS so they can verify identity and process the federal income tax return. Use the phone number in the letter with the information listed below. When calling, IRS will ask questions to verify identity.

Note: Although the letters request a response within 30 days, the IRS will continue to work the case regardless of the amount of days that have passed.

Have ALL of the following available when you call:

- The 4883C or 6330C letter.

- The income tax return referenced in the letter (the Form 1040 series return).

- Note: A Form W-2 or Form 1099 is not a tax return.

- A prior year income tax return, other than the year in the letter, if the client filed a return.

- Note: A Form W-2 or Form 1099 is not a tax return; and

- Supporting documents that were filed with each year’s income tax return (Form W-2 or Form 1099, Schedules C or F, etc.).

NOTE: Authorized third parties may assist taxpayers, but the client must call us together and must participate on the call.

The toll-free IRS Identity Verification number is for identity verification only. No other tax-related information, including refund status, is available.

Issue 10: Summary of My Recommendations for IRS Improvement – Provided to a National Tax Professional Organization Upon Request – It Cannot Hurt to Ask

Recently, I was asked to provide a list of issues facing clients for a tax professional organization. I provided the following:

- IRS wants taxpayers to sign up for an IRS account. Many people have issues verifying their ID as it is difficult for some. Can IRS provide another option to verify identity if the taxpayer is unable to do so through ID.me? Other than through a computer, which people do not have or a smart phone that they do not have or have no idea how to operate. There is the option to contact a “Trusted Referee” to assist and help from ID.me, but by that time most are so frustrated they just give up. An IRS video they can easily find, and watch may help. Perhaps a video step by step registration process to guide them through the verification, or entirely different option.

- Reinstate “holds” called a STAUP on a taxpayer’s account when phone calls are made requesting additional time to respond or correspondence is received and IRS needs time to work the correspondence. This would prevent thousands of Notices from going out and causing untold concern as to why they are getting the notice again and again. IRS use to do this and then stopped. Or the program was disabled.

- Additional staffing on the 1-800-829-1040 number would be wonderful – but we know that is somewhat out of your control.

- Explore a way to get the POA thru e-services – 6 + weeks to get POA installed in IRS module (fax), the other method thru the client is froth with issues as client does not understand system.

- Expand e-services to business issues. Correct me on this one.

- Try to provide more information on processing throughout the year, as a guideline to let tax preparers know delays – problems. I know we have e-news use that to provide some updates through the tax season as to IRS processing issues, etc. This enables the tax professional to provide up to date information on IRS processing problems and may many phone calls that IRS cannot handle and frustrated taxpayers.

- Campaign to get tax professionals to sign up for subscriptions like e-news and other subscriptions. Many do not even know this exists.

- Continue to press Congress for no tax changes/new law after September 30, 20XX. This causes misunderstand concerning new law which causes mistakes and can deprive some taxpayers with credits and deduction due to lack of guidance and results in amended returns and causes IRS to scramble with limited staff to turn on a dime.

Update:

The IRS conceded that insufficient funding, staffing, and return processing times have necessitated taxpayer relief and “meaningful assistance” during yet another tax filing season underscored by the COVID-19 pandemic. The American Institute of Certified Public Accountants (AICPA), however, is skeptical that the IRS’s efforts do enough to shift the burden from taxpayers and practitioners.

The IRS released a statement January 27 announcing that it has suspended automatic notices in situations when the IRS has “credited taxpayers for payments” but has “no record of the tax return being filed.”

These notices are often sent regarding unprocessed returns but are “statutorily required to be issued within a timeframe to be legally valid. The IRS argues that for many types of notices to not be sent automatically, Congress needs to act.

The AICPA said that suspending some notices is a “positive first step,” but that should not be the only relief the IRS commits to.

On January 26, nearly 200 members of Congress wrote to Treasury Secretary Janet Yellen echoing the coalition’s sentiments and call for action. Specifically, the letter requests that the IRS:

- “Halt automated collections from now until at least 90 days after April 18, 2022.

- Delay the collection process for filers until any active and pending penalty abatement requests have been processed.

- Streamline the reasonable cause penalty abatement process for taxpayers impacted by the COVID-19 pandemic without the need for written correspondence.

- Provide targeted tax penalty relief for taxpayers who paid at least 70 percent of the tax due for the 2020 and 2021 tax year; and

- Expedite processing of amended returns and provide TAS and congressional caseworkers with timely responses.

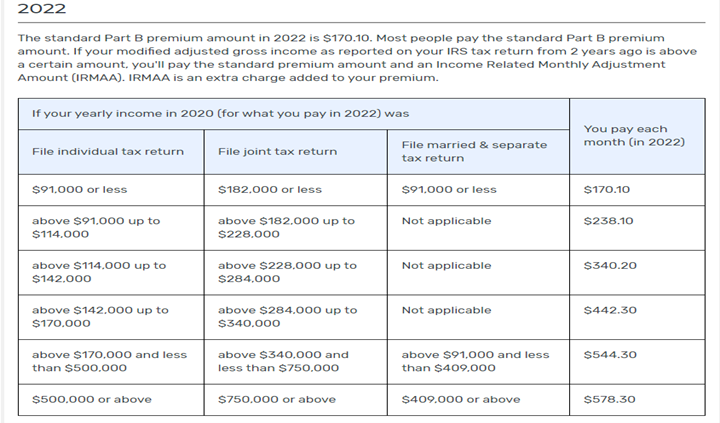

Issue 11: Update on Medicare Income Thresholds and Costs 2022

Issue 12: Taxpayer Advocate Preface of their Annual Report _ Interesting to Say the Least – No Holds Barred – An Honest Evaluation – Full Report: 2021 Annual Report to Congress – Taxpayer Advocate Service (irs.gov)

The IRS Deserves Credit for Playing the Hand It Was Dealt

One irony of the past year is that, despite its challenges, the IRS performed well under the circumstances. The imbalance between the IRS’s workload and its resources has never been greater.

On the workload side, the number of individual taxpayers the IRS serves has increased by about 19% since 2010, as the number of Form 1040 series returns rose from about 142 million in that year to about 169 million in 2021. While there is no perfect measure of the IRS’s workload, return filings are a good approximation because most IRS work – including fraud screening, telephone calls, audits, collection actions, TAS cases, Appeals cases, Tax Court cases, and other downstream consequences – keys off the number of taxpayers filing returns.

During the last 18 months, Congress charged the IRS with administering several COVID-19 pandemic financial relief programs, including three rounds of stimulus payments (also known as Economic Impact Payments), monthly payments of the Advance Child Tax Credit (AdvCTC), reduction of the taxability of unemployment compensation in the middle of the 2021 filing season, and other provisions directly impacting tax administration.

Each financial relief program consumed considerable IRS resources to administer, including overall planning, information technology (IT) programming, implementation, public communications, and responding to taxpayers’ questions and account issues. To address these needs, the IRS had to reallocate resources from its core tax administration responsibilities.

Over the last decade, examination coverage has decreased, enforcement efforts have been negatively impacted, and the Level of Service has continued to drop as the IRS’s workforce and budget have declined.

On the resources side, the IRS’s baseline budget has been reduced by about 20% on an inflation-adjusted basis since fiscal year (FY) 2010, and its workforce has shrunk by about 17%.

Although Congress provided supplemental funding to help the IRS implement pandemic-relief programs, it is not feasible for an agency the size of the IRS to staff up and train new employees quickly. The IRS also is limited in its ability to hire new employees when funding is provided on a one-time basis because there is no assurance it will have sufficient funding in future years to retain those employees. In addition, the social distancing required during the pandemic forced the agency to close or limit staffing in processing centers where employees work in close quarters, further restricting its production capacity.

Despite its limitations, the IRS processed most e-filed tax returns timely, it issued 130 million refunds totaling $365 billion, it issued 478 million stimulus payments totaling $812 billion, and it sent AdvCTC payments to over 36 million families that totaled over $93 billion.

The IRS’s leadership and workforce deserve considerable credit for their accomplishments.

Issue 13: FQA on Over-the-Counter COVID Tests

On January 10, 2022, the Biden Administration issued highly anticipated guidance in the form of Frequently Asked Questions (FAQs) aimed at clarifying a requirement announced late last year that insurance companies and group health plans cover the cost of over-the-counter (OTC) at-home COVID-19 tests throughout the duration of the public health emergency (PHE), beginning on January 15, 2022. Among the FAQs are those aimed at clarifying the circumstances under which OTC tests must be covered, along with various limits and safe harbors for plans and issuers. This includes clarifying that plans and issuers:

- Must provide coverage without cost-sharing requirements, prior authorization, or other medical management requirements with respect to OTC COVID-19 tests available without an order or individualized clinical assessment by a health care provider purchased on or after January 15, 2022, and during the PHE. Coverage may, but is not required to, be provided for OTC COVID-19 tests purchased before January 15, 2022.

- May not limit coverage to tests that are provided through preferred pharmacies or other retailers unless a plan or issuer arranges for direct coverage through both its pharmacy network and a direct-to-consumer shipping program if various access and costs stipulations are met. In that case, they may limit reimbursement from non-preferred pharmacies or other retailers to no less than the actual price, or $12 per test (whichever is lower).

- May set limits on the number or frequency of OTC COVID-19 tests covered without cost sharing to no less than 8 tests per 30-day period (or per calendar month) per participant, beneficiary, or enrollee, for those tests administered without a provider’s involvement or prescription.

- Are permitted and may act to prevent, detect, and address fraud and abuse.

- May provide education and information resources to support consumers seeking OTC COVID-19 testing, as long as such resources make clear that the plan or issuer provides coverage and reimbursement of all eligible OTC COVID-19 tests, and such information is consistent with the test’s emergency use authorization (EUA).

Issue 14: Q and A from January 2021 Filing Season Webinars

| If a fiscal return has been filed for a C corporation for 2020 and no statement was attached, should the return be amended to include the attachment? Or can this be sent in separately. | THIS applies to the 2021 return which has not been filed? If you have filed the 2021, you can do a superseded return for the corporation. Both the 2020 and 2021 PPP Loan information must be on the 2021 return. There is not a separate filing for the attachment that I have seen. Place the required statement in the 2021 filing.

|

| Do any of you have clients who draw a W-2 and participate in profit sharing plans vs 401k plans? I have a new client, who makes $800K on a W-2 and is participating in a profit-sharing plan, setting aside 25% of his income.

Gross income is around $900K; salary is $720K.

|

A profit-sharing plan is a type of plan that gives employers flexibility in designing key features. It allows the employer to choose how much to contribute to the plan (out of profits or otherwise) each year, including making no contribution for a year.

A profit-sharing plan gives employees a share in their company’s profits based on its quarterly or annual earnings. It is up to the company to decide how much of its profits it wishes to share. Contributions to a profit-sharing plan are made by the company only; employees cannot make them, too.

Contribution Limits 100% of the participant’s compensation, or $57,000 for 2020 and $58,000 for 2021, the lesser of these two amounts. If you, the employer, make contributions to a profit-sharing plan, you can deduct up to 25%percent of the compensation paid during the taxable year to all participants. Are you sure it is not some other plan??????????? |

| When a client receives crypto is that considered buying it?

|

If you receive it as an inheritance, gift, something like that, then you’d put YES for the crypto question. But just buying it is a no.

|

| If you have a debit card, then is a person using virtual currency! Even though, it is not defined as such.

|

If you have a virtual currency debit card, then you’re exchanging property for goods or services, definitely a taxable transaction!

|

| Would employees who works for a Farm qualify under the Families First Coronavirus Response Act? There are no – related employees.

|

This is a complex issue with many rules. Your best information can be found at the following website.

There are many resources on the IRS website.

|

| Is IRS likely to audit an entity due to an informal loan document with owner?

If pulled for audit, is there still requirement for interest paid? Do you still recommend imputing interest even when it would be a wash, since deductible by the company?

|

Imputed interest is the law and will apply in all cases where interest is not a stated issue. |

| Realizing Form 7203 is submitted with Form 1040, where is 7203 actually prepared? With the 1120-S?

|

The Form is prepared and submitted with Form 1040.

|

Issue 15: Recovery Rebate FAQ’s

The Internal Revenue Service has issued frequently asked questions (FAQs) for the 2021 Recovery Rebate Credit. Individuals who did not qualify for, or did not receive, the full amount of the third Economic Impact Payment may be eligible to claim the 2021 Recovery Rebate Credit based on their 2021 tax year information. Individuals may have received their third Economic Impact Payment through initial and “plus-up” payments in 2021.

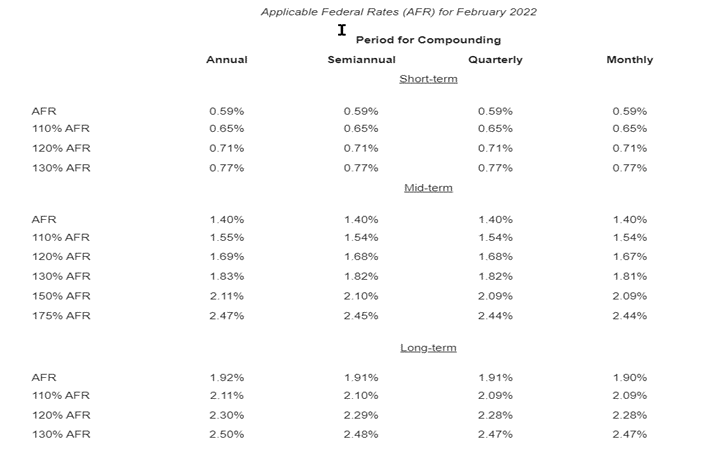

Issue 15: Applicable Federal Rates for February 2022, Rev. Rul. 2022-3

Rev. Rul. 2022-3 TABLE 2

Adjusted AFR for February 2022

| Period for Compounding | ||||

| Annual | Semiannual | Quarterly | Monthly | |

| Short-term adjusted AFR |

0.45% | 0.45% | 0.45% | 0.45% |

| Mid-term adjusted AFR |

1.06% | 1.06% | 1.06% | 1.06% |

| Long-term adjusted AFR |

1.46% | 1.45% | 1.45% | 1.45% |

Rev. Rul. 2022-3 TABLE 3

Rates Under § 382 for February 2022

| Adjusted federal long-term rate for the current month: 1.46% | 1.46% |

| Long-term tax-exempt rate for ownership changes during the current month (the highest of the adjusted federal

long-term rates for the current month and the prior two months.) 1.46% |

1.46% |

Rev. Rul. 2022-3 TABLE 4

Appropriate Percentages Under § 42(b)(1) for February 2022

| Note: Under § 42(b)(2), the applicable percentage for non-federally subsidized new buildings placed in

service after July 30, 2008, shall not be less than 9%. |

|

| Appropriate percentage for the 70% present value low-income housing credit: 7.38% | 7.38% |

| Appropriate percentage for the 30% present value low-income housing credit: 7.38% | 3.16% |

Rev. Rul. 2022-3 TABLE 5

Rate Under § 7520 for February 2022

| Applicable federal rate for determining the present value of an annuity, an interest in life or a term of years,

or a remainder or reversionary interest. 1.6% |

1.6% |