Stay informed with the August 2024 Tax Newsletter: Special Edition – Energy Credits

Energy Credits have been around for a long time – but changes at the whim of Congress. The newsletter will discuss a bit of history so we understand how we arrive at the current energy policy and then will delve into the current law.

2024 virtual seminar registration discount deadline approaching August 19th.

$329 for Both Seminars: SAVE $139

History

The Energy Policy Act (EPACT) of 2005 first established the energy efficiency tax credits that were effective in 2006 & 2007. The majority of these tax credits were for 10% of the cost, up to $500.

- The tax credit was raised from 10% to 30%.

- The maximum credit was raised from $500 to $1,500 total for the two-year period (2009-2010). However, some improvements such as geothermal heat pumps, solar water heaters, and solar panels are not subject to the $1,500 maximum.

- The tax credits that were previously effective for 2009, were extended to 2010 as well.

- Efficiency levels for the following products were changed for: central air conditioners, air source heat pumps, windows, and gas, propane, or oil water heaters.

On December 17, 2010, the “Tax Relief, Unemployment Insurance Reauthorization, and Job Creation Act ” was signed extending the tax credits, but at lower levels, basically rolling back to the 2006-2007 levels. Highlights:

- The tax credit was extended for 2011.

- New Lifetime limit set at $500.

- 10% up to $500 for insulation, roofs, and doors.

- Windows capped at $200, but qualification now ENERGY STAR.

- Furnace and boilers capped at $150, and all furnaces and boilers must meet 95 AFUE.

- $50 for advanced main air circulating fan.

- $300 for air conditioners, water heaters, and biomass stoves.

On February 9, 2018, the “Bipartisan Budget Act of 2018 (BBA)” was signed, reinstating the non-business energy property credit for 2017, and the residential energy efficient property credit for qualified small wind energy property costs, qualified geothermal heat pump property costs, and qualified fuel cell property costs to the end of 2021.

On December 20, 2019, H.R.1865, the “Further Consolidated Appropriations Act, 2020” was signed into law retroactively extending the tax credits for alternative fuel vehicle refueling property, non-business energy property, new energy-efficient homes, and new energy-efficient commercial buildings. The extension is from 12/31/2017 through 12/31/2020.

On December 21, 2020, the “Continuing Appropriations Act, 2021 and Other Extensions Act” was signed into law extending the “Non-Business Energy Property” tax credit through the end of 2021.

On August 16, 2022, President Biden signed into law the Inflation Reduction Act of 2022. This landmark bill extended and modified many of the tax credits that were previously offered under the Energy Policy Act of 2005. The Inflation Reduction Act of 2022 features tax credits for consumers and businesses that save money on energy bills, create jobs, make homes and buildings more energy efficient, utilize clean energy sources and lower greenhouse gas emissions that contribute to climate change and global warming.

- R.5376 – Inflation Reduction Act of 2022

- Energy Efficiency Home Improvement Credit – 26 USC 25C

- Residential Clean Energy Credit – 26 USC 25D

Homeowners

If the client has made energy improvements to their home, tax credits are available for a portion of qualifying expenses. The credit amounts and types of qualifying expenses were expanded by the Inflation Reduction Act of 2022.

Who can claim the credits

A client can claim either the Energy Efficient Home Improvement Credit or the Residential Energy Clean Property Credit for the year when they make qualifying improvements.

- Homeowners who improve their “primary residence” will find the most opportunities to claim a credit for qualifying expenses.

- Renters may also be able to claim credits, as well as owners of second homes used as residences.

The credits are never available for improvements made to homes that the client does not use as a residence.

Primary Residence

What type of residence qualifies for these credits? For example, are the credits available for improvements made to a second home or to a home rented by the taxpayer?

The credits are available only for certain improvements made to second homes, and the credits are never available when the improvements are made to homes not used as a residence by the taxpayer.

For example, landlords can never use these credits for improvements made to any homes they rent out but do not use as a residence themselves.

However, if a taxpayer is renting a home as their principal residence and makes eligible improvements, a tax credit may be available to such tenant.

Can a taxpayer claim the credits for expenditures incurred for an existing home? What about a newly constructed home?

The rules vary by credit.

- Under the Energy Efficient Home Improvement Credit: a taxpayer can claim the credit only for qualifying expenditures incurred for an existing home or for an addition to or renovation of an existing home, and not for a newly constructed home.

- Under the Residential Clean Energy Property Credit: a taxpayer can claim the credit for qualifying expenditures incurred for either an existing home or a newly constructed home.

May a taxpayer claim a credit if the qualified property is also used for business purposes, such as in a dwelling unit in which the taxpayer also conducts a business?

For both credits, if a taxpayer uses property solely for business purposes, the property will not qualify for the credit.

A taxpayer who qualifies for the credits and whose use of the qualified property for business purposes is not more than 20 % may claim the full credit.

For a taxpayer who otherwise qualifies for the credits, but whose use of the qualified property for business purposes exceeds 20 %, the taxpayer must calculate the amount of credit by including only that portion of the expenditures for the property that are properly allocable to use for nonbusiness purposes.

Note: The principal residence of a taxpayer is determined by taking into account all the facts and circumstances, such as their place of employment and mailing address for bills and correspondence, but ordinarily will be the property where the taxpayer spends the majority of their time. Treas. Reg. § 1.121-1(b).

We Have two Credits:

- Energy Efficient Home Improvement Credit

- Residential Clean Energy Credit

Unfortunately, the requirements are similar in nature BUT are different in other aspects, so it is important to understand the ins and outs of each to property obtain the credit.

Overview – Summary

General Overview of the Energy Efficient Home Improvement Credit

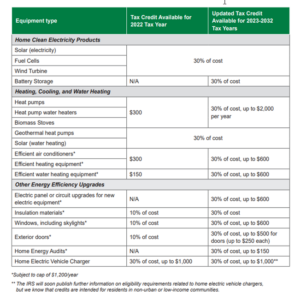

Through December 31, 2022, the energy efficient home improvement credit is a $500 lifetime credit.

As amended by the IRA, the energy efficient home improvement credit is increased for years after 2022, with an annual credit of generally up to $1,200. Beginning January 1, 2023, the amount of the credit is equal to 30% of the sum of amounts paid by the taxpayer for certain qualified expenditures, including:

- qualified energy efficiency improvements installed during the year,

- residential energy property expenditures during the year, and

- home energy audits during the year.

There are limits on the allowable annual credit and on the amount of credit for certain types of qualified expenditures. Credit is allowed for qualifying property placed in service on or after January 1, 2023, and before January 1, 2033.

Energy Efficient Home Improvement Credit

Building envelope components

To qualify, building envelope components must have an expected lifespan of at least 5 years. Qualified components include new:

Building envelope components satisfying the energy efficiency requirements under the Energy Efficiency Requirements section:

- Exterior doors (30% of costs up to $250 per door, up to a total of $500)

- Exterior windows and skylights (30% of costs up to $600) and

- Insulation materials or systems and air sealing materials or systems (30% of costs).

Note: Materials or systems installed in 2025 must meet the IECC standard in effect on Jan. 1, 2023. These items do not have a specific credit limit, other than the maximum credit limit of $1,200.

Remember these items must have an expected lifespan of five years.

Finally, the above expenses do not include labor.

Home energy audits (30% of costs up to $150)

Residential energy property (30% of costs, including labor, up to $600 for each item) satisfying the energy efficiency requirements

- Central air conditioners

- Natural gas, propane, or oil water heaters

- Natural gas, propane, or oil furnaces and hot water boilers and

- Improvements to or replacements of panelboards, sub-panelboards, branch circuits, or feeders that are installed along with building envelope components or other energy property that enable its installation and use. (Limit $600.00 per item)

Heat pumps and biomass stoves and biomass boilers (30% of costs, including labor).

- Electric or natural gas heat pump water heaters

- Electric or natural gas heat pumps and

- Biomass stoves and biomass boilers

How Do We Determine if a Purchase Qualifies for Credit?

Energy Efficient Products | ENERGY STAR

The energy Star.Gov website has a search application which will be helpful to verify if a purchase/product qualifies for the energy credit.

How to Claim the Credit

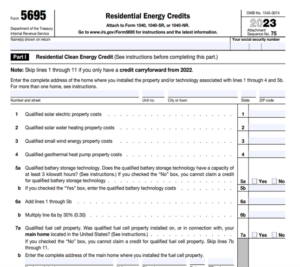

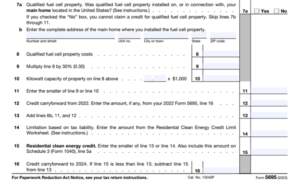

Use Form 5695 Residential Energy Credit. The 2024 Form 5695 is not currently available at the time of writing, but Part II Section A is where the credit will be calculated.

Limit

There is a $1,200 aggregate yearly tax credit maximum for all building envelope components, home energy audits, and energy property.

But for electric or natural gas heat pump water heaters, electric or natural gas heat pumps, and biomass stoves and biomass boilers have a separate aggregate yearly credit limit of $2,000.

Thus, the maximum total yearly energy efficient home improvement credit amount may be up to $3,200.

Examples

Example 1.

In one taxable year, a client purchases and installs the following: two exterior doors at a cost of $1,000 each, windows and skylights at a total cost of $2,200, and one central air conditioner at a cost of $5,000.

All property installed meets the applicable energy efficiency and other requirements for qualifying for the Energy Efficient Home Improvement Credit.

First, 30% of each $1,000 door’s costs are $300, but the per door limit of $250 applies to reduce the maximum possible credit for each door to $250 each.

Thus, the client’s expenditures for exterior doors potentially qualify the client to claim up to a $500 tax credit.

Next, 30% of the client’s total $2,200 of expenditures for windows and skylights is $660, but the $600 limit for all windows and skylights applies to limit the client’s credit for such expenditures to $600.

Thus, the client’s expenditures for windows and skylights potentially qualify the client to claim up to $600.

Finally, 30% of the client’s $5,000 cost paid for the central air conditioner is $1,500, but the $600 per item limit for energy property applies to limit the client’s credit for such expenditures to $600.

Adding these credit amounts yields a sum of $1,700 ($500 + $600 + $600), but the aggregate limit of $1,200 applies to limit the client’s total amount of Energy Efficient Home Improvement Credit to $1,200.

Note: Here is where planning ahead could have helped – the client loses $500 as the amount in excess of the $1,200 ($500) cannot be carried forward.

Important – No Carryforward for any Energy Efficient Home Improvement Credit

Under the Energy Efficient Home Improvement Credit: a client may not carry the credit forward. Thus, if a client does not have sufficient tax liability to claim all or a portion of the credit in the year in which the related property for which the qualifying expenditure is placed in service, the unused amount of the credit may never be claimed.

Example 2.

For this example, assume all the same facts as in Example 1, except that instead of purchasing and installing a central air conditioner at a cost of $5,000, the client purchases and installs an electric heat pump at a cost of $5,000.

The heat pump meets the applicable energy efficiency and other requirements for qualifying for the Energy Efficient Home Improvement Credit.

Here, 30 % of the client’s costs for the heat pump is $1,500, and since the heat pump is in a category of energy property exempted from both the $600 per item limit and the $1,200 aggregate limit, the client can claim an Energy Efficient Home Improvement Credit of $1,500 for the costs of the heat pump alone.

Accordingly, the client’s total Energy Efficient Home Improvement Credit is $2,600 ($500 for the exterior doors + $600 for the windows and skylights + $1,500 for the heat pump).

Example 3.

For this example, assume all the same facts as in Example 1 above, except that instead of purchasing and installing a central air conditioner at a cost of $5,000, the taxpayer purchases and installs an electric heat pump at a cost of $8,000.

The heat pump meets the applicable energy efficiency and other requirements for qualifying for the Energy Efficient Home Improvement Credit.

Assume further that the taxpayer spends $600 on home energy audits performed by a properly certified home energy auditor.

On these facts, 30 % of the client’s costs for home energy audits is $180, but the $150 limit on credits for home energy audits applies to limit the client’s credit for such expenditures to $150.

Adding this credit amount to the credit amounts for the doors, windows, and skylights yields a sum of $1,250 ($1,100 + $150), but the $1,200 aggregate limit applies to limit the client’s total potential credits for these expenses to $1,200.

Next, 30% of the client’s $8,000 cost for the heat pump is $2,400, and even though the heat pump falls into a category of energy property exempted from both the $600 per item limit and the $1,200 aggregate limit, the category is still subject to a separate $2,000 aggregate limit for electric or natural gas heat pump water heaters, electric or natural gas heat pumps, and biomass stoves and biomass boilers.

Thus, the client can claim a $2,000 tax credit for the cost of the heat pump alone, and the client’s total Energy Efficient Home Improvement Credit is $3,200 ($1,200 for the maximum allowable credit for the doors, windows, skylights, and home energy audit + $2,000 for the maximum allowable credit for a heat pump).

What About Rebates, Subsidies and Incentives?

This section applies to both the:

- Energy Efficient Home Improvement Credit

- Residential Clean Energy Credit

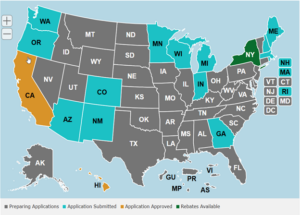

The most recent update concerning Rebates is dated June 14, 2024

- 48 states and territories have applied to DOE for early administrative or full program funding.

- 17 states have applied to DOE for full funding to launch their programs.

- These states and territories have applied for $2.21 billion in funding.

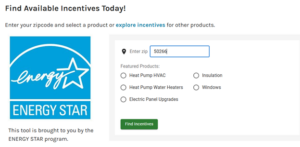

Energy.gov has some nice application concerning whether rebates are available and what qualifies for the tax credit – as we must meet the energy requirements to qualify for the credit. Home Upgrades | Department of Energy you will need to scroll down a bit to the section titled: Search for eligible appliances and home upgrades.

See “Find Incentives Today”.

By inputting my zip code and noting “Windows” the application provides additional information.

Summary

These expenses may qualify if they meet requirements detailed on energy.gov:

- Exterior doors, windows, skylights and insulation materials (5-year lifespan)- no labor.

- Central air conditioners, water heaters, furnaces, boilers and heat pumps – labor allowed

- Biomass stoves and boilers – labor allowed

- Home energy audits

Qualified components must be new.

The amount of the credit that can be taken is a percentage of the total improvement expenses in the year of installation:

- 2022: 30%, up to a lifetime maximum of $500

- 2023 through 2032: 30%, up to a maximum of $1,200 (heat pumps, biomass stoves and boilers have a separate annual credit limit of $2,000), no lifetime limit

Watch the labor issue as noted above.

No carryforwards are allowed under the Energy Efficient Homes Credit – so planning is important.

Finally, only – an existing home or for an addition to or renovation of an existing home, and not for a newly constructed home.

Non-refundable must have tax liability.

Residential Clean Energy Credit

The residential clean energy property credit is a 30 % credit for certain qualified expenditures made by a client for residential energy efficient property. The IRA extended the residential clean energy property credit through 2034, modified the applicable credit percentage rates, and added battery storage technology as an eligible expenditure.

The credit applies for property placed in service after December 31, 2021, and before January 1, 2033. The credit percentage rate phases down to 26 % for property placed in service in 2033, 22 % for property placed in service in 2034, and no credit is available for property placed in service after December 31, 2034.

The client may be able to take the credit if they made energy saving improvements to their home located in the United States.

The credit is nonrefundable, so the credit amount received cannot exceed the amount tax owed. The client can carry forward any excess unused credit, though, and apply it to reduce the tax due in future years.

Do not include interest paid including loan origination fees.

The credit has no annual or lifetime dollar limit except for credit limits for fuel cell property. The client can claim the annual credit every year that they install eligible property until the credit begins to phase out in 2033.

Credit limits for fuel cell property

Fuel cell property is limited to $500 for each half kilowatt of capacity. If more than one person lives in the home, the combined credit for all residents cannot exceed $1,667 for each half kilowatt of fuel cell capacity.

Who qualifies

The client may claim the residential clean energy credit for improvements to the main home, whether they own or rent it. The main home is generally where the client lives most of the time. The credit applies to new or existing homes located in the United States.

The client cannot claim the credit if they are a landlord or other property owner who does not live in the home.

The client may be able to claim a credit for certain improvements made to a second home located in the United States that they live in part-time and do not rent to others. They cannot claim a credit for fuel cell property for a second home or for a home that is not located in the United States.

These expenses may qualify if they meet requirements detailed on energy.gov:

- Solar, wind and geothermal power generation

- Solar water heaters

- Fuel cells

- Battery storage (beginning in 2023)

Used (previously owned) clean energy property is not eligible.

Qualified expenses may include labor costs for onsite preparation, assembly or original installation of the property and for piping or wiring to connect it to the home.

Note: Traditional building components that primarily serve a roofing or structural function generally do not qualify. For example, roof trusses and traditional shingles that support solar panels do not qualify, but solar roofing tiles and solar shingles do because they generate clean energy.

The amount of the credit you can take is a percentage of the total improvement expenses in the year of installation:

- 2022 to 2032: 30%, no annual maximum or lifetime limit

- 2033: 26%, no annual maximum or lifetime limit

- 2034: 22%, no annual maximum or lifetime limit

Qualified clean energy property

Clean energy property must meet the following standards to qualify for the residential clean energy credit.

Solar water heaters must be certified by the Solar Rating Certification Corporation, or a comparable entity endorsed by your state.

Geothermal heat pumps must meet Energy Star requirements in effect at the time of purchase.

Battery storage technology must have a capacity of at least 3 kilowatt hours.

Fuel Property requires some additional information.

Summary

https://www.energystar.gov/about/federal-tax-credits

Nonrefundable but can carry forward.

New and existing homes, client must live in but no landlords.

Second home may qualify – must be located in the United States and live in parttime and do not rent it out.

Labor costs are included.

___________________________________________________________________

Clean Vehicle Credits

https://www.fueleconomy.gov/feg/tax2023.shtml

The federal government currently offers three tax credits that reduce clean vehicle purchase prices and thus may increase demand for clean vehicles (e.g., electric vehicles, plug-in hybrid vehicles, and fuel cell vehicles).

Each clean vehicle credit was created in the Energy Improvement and Extension Act of 2008 (Division B of P.L. 110-343) and subsequently modified by P.L. 117-169 (commonly referred to as the Inflation Reduction Act or IRA).

Clean Vehicle Credit (IRC §30D)

Clients purchasing a qualifying new clean vehicle may claim a nonrefundable tax credit of up to $7,500 for vehicles placed in service through the end of 2032.

The maximum potential credit ($7,500) is the sum of two amounts: the critical mineral amount ($3,750) and the battery component amount ($3,750), which went into effect for vehicles placed in service on or after April 18, 2023. (For vehicles placed in service in 2023 prior to April 18, 2023, the critical mineral and battery components were not applicable.)

Critical Mineral Portion

- To claim the critical mineral portion of the credit, a car’s battery must have at least a certain threshold percentage of its critical minerals that were extracted or processed in the United States or in a country with which the United States has a free trade agreement, or that were recycled in North America.

- The threshold percentage is 40% in 2023, 50% in 2024, 60% in 2025, 70% in 2026, and 80% thereafter.

- For vehicles placed in service after 2024, no applicable critical minerals in the vehicle’s battery may come from a “foreign entity of concern.”

Battery Component

To claim the battery component portion of the credit, at least a certain percentage of an electric vehicle battery’s component parts must be manufactured or assembled in North America.

The threshold percentage is 50% in 2023, 60% in 2024 and 2025, 70% in 2026, 80% in 2027, 90% in 2028, and 100% thereafter.

More Information

In addition, vehicles placed in service after 2023 cannot use battery components manufactured or assembled by a “foreign entity of concern.”

In addition to the critical minerals and battery component requirements, qualifying clean vehicles must meet other criteria.

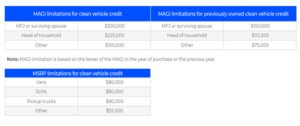

- These additional criteria include a manufacturer’s suggested retail price (MSRP) cap ($80,000 for vans, SUVs, and pickup trucks; $55,000 for other vehicles)

- A gross vehicle weight rating (GVWR) of less than 14,000 pounds and

- A battery capacity of at least 7 kilowatt hours.

- Additionally, all qualified vehicles must undergo final assembly in North America.

- To claim the credit, taxpayers’ modified adjusted gross incomes (MAGIs) for either the current or previous year must be at or below certain thresholds: $300,000 for married couples, $150,000 for single filers, and $225,000 for heads of household.

- The clean vehicle credit is nonrefundable, meaning clients may not claim credits in excess of their tax liabilities.

Transfers

Starting in 2024, clients may elect to transfer the clean vehicle credit to the vehicle dealer. The transferred credit may exceed the client’s income tax liability, effectively making transferred credits fully refundable.

Clients who transfer the credit but later exceed the MAGI limits must pay back the credit (to the IRS) when filing their taxes.

Credit for Previously Owned Clean Vehicles (IRC §25E)

Clients purchasing a qualifying previously owned clean vehicle may claim a nonrefundable tax credit equal to 30% of the vehicle’s sales price, up to a maximum credit of $4,000.

This credit is commonly referred to as the “used clean vehicle credit.” Qualifying used vehicles must be acquired before 2033. Credit can only be claimed once per vehicle, and the vehicle must satisfy other criteria.

- The vehicle must be purchased from a licensed dealer for $25,000 or less

- Have a GVWR rating of less than 14,000 pounds, and

- Have a battery capacity of at least 7 kilowatt hours.

In addition, the vehicle’s model year must be at least two years before the year of purchase, and the dealer must produce a report of the transaction for both the buyer and the IRS.

- Only clients with MAGIs at or below $150,000 for married couples

- $75,000 for single filers, and

- $112,500 for heads of household in either the current or previous year qualify for this tax credit.

Taxpayers can claim the credit at most once every three years. Rules for credit transfers under the used clean vehicle credit are similar to those under the clean vehicle credit.

Credit for Qualified Commercial Clean Vehicles (IRC §45W)

By purchasing a qualified clean vehicle, businesses and tax-exempt organizations can qualify for a tax credit of up to $40,000.

For hybrid vehicles, the credit equals the lesser of the incremental cost of the vehicle (the difference between its price and the price of a gas- or diesel-powered vehicle of similar size and use) or 15% of the vehicle’s cost basis.

For electric vehicles and fuel cell vehicles, the credit equals the lesser of the incremental cost of the vehicle or 30% of the vehicle’s cost basis.

The credit may not exceed $7,500 for vehicles with a GVWR of less than 14,000 pounds.

The credit for qualified commercial clean vehicles can only be claimed once per vehicle and must satisfy multiple other criteria.

The vehicle must be used for business purposes, be used primarily in the United States, have a battery capacity of at least 7 kilowatt hours if the GVWR is less than 14,000 pounds or 15 kilowatt hours otherwise, and be produced by a qualified manufacturer.

In addition, the vehicle must be either mobile machinery as defined in §4053(8) or a motor vehicle for use on public roads for purposes of Title II of the Clean Air Act.

- Mobile machinery is defined to include vehicles such as electric tractors while excluding vehicles such as electric golf carts.

The commercial clean vehicle credit is nonrefundable, meaning that businesses may not claim tax credits in excess of their tax liabilities. Any unused credits may be carried back 1 year or carried forward up to 20 years to offset other years’ tax liabilities, however.

Tax-exempt organizations are eligible to receive the credit as a direct cash payment instead of as a nonrefundable tax credit.

Complementary Provisions to the Clean Vehicle Tax Credits Federal tax policy also contains a provision that indirectly promotes the adoption of clean vehicles.

The Alternative Fuel Vehicle Refueling Property Credit (IRC §30C) can be claimed by individuals and businesses that install property used to store or dispense clean-burning fuel or to recharge electric motor vehicles in qualifying census tracts.

Qualifying census tracts are those designated as low income for the New Markets Tax Credit (generally having a poverty rate greater than 20% or median family income less than 80% of the statewide or metropolitan area family income) or those located in nonurban areas.

The credit for individuals is equal to 30% of the cost of the property with a maximum credit of $1,000.

For businesses the credit is equal to 30% of the cost of the property if prevailing wage and qualified apprenticeship requirements are met (6% otherwise) with a maximum credit of $100,000 per piece of property.

Federal tax incentives may complement the clean vehicle market in other ways as well. For example, the clean hydrogen production credit ( §45V) subsidizes the production of hydrogen fuel which may be used in fuel cell vehicles, and the advanced manufacturing production credit ( §45X) subsidizes production of battery components which may be used in clean vehicles.

Summary

Businesses and tax-exempt organizations that buy a qualified commercial clean vehicle may qualify for a clean vehicle tax credit of up to $40,000 under § 45W.

Credit amount

Follow these steps to calculate the credit amount:

- Find the maximum credit amount based on the gross vehicle weight rating (GVWR) of the vehicle:

- Less than 14,000 pounds (typically cars, vans, trucks, and similar passenger-sized vehicles): maximum credit $7,500

- 14,000 pounds or more (typically larger vehicles like school buses and semi-trucks): maximum credit $40,000

- Calculate a percentage of the basis (the amount of investment for tax purposes) in the vehicle based on engine type:

- 30% of basis for a vehicle that is not powered by a gasoline or diesel internal combustion engine, such as an electric vehicle (EV) or fuel cell electric vehicle (FCEV).

- 15% of basis for a vehicle that is powered (even partially) by a gasoline or diesel internal combustion engine, such as a plug-in-hybrid electric vehicle (PHEV).

- Find the incremental cost of the vehicle (the excess of its purchase price over that of a comparable vehicle powered only by gas or diesel internal combustion). For electric vehicles placed in service in 2024, use the Department of Energy’s incremental cost analysis for the appropriate class of vehicle:

- $7,000 for compact plug-in hybrid electric vehicles (PHEVs) (includes mini compact and subcompact cars) with a GVWR of less than 14,000 pounds

- $7,500 for all street electric vehicles, other than compact car PHEVs, with a GVWR of less than 14,000 pounds

- $40,000 for all other vehicles with a GVWR of 14,000 pounds or more

- Compare the maximum credit amount, percentage of basis, and incremental cost. The smallest figure is your credit amount.

Who qualifies

Businesses and tax-exempt organizations qualify for the credit.

There is no limit on the number of credits a business can claim. For businesses, the credits are nonrefundable, so they cannot get back more on the credit than owed in taxes. A §45W credit can be carried over as a general business credit.

Vehicles that qualify

To qualify, a vehicle must be subject to a depreciation allowance, with an exception for vehicles placed in service by a tax-exempt organization and not subject to a lease.

The vehicle must also:

- Be made by a qualified manufacturer as defined in § 30D(d)(1)(C ) (see the index of qualified manufacturers)

- Be for use in a business, not for resale

- Be for use primarily in the United States

- Not have been allowed a credit under §§ 30D or 45W

In addition, the vehicle must either be:

- Treated as a motor vehicle for purposes of title II of the Clean Air Act and manufactured primarily for use on public roads (not including a vehicle operated exclusively on a rail or rails); or

- Mobile machinery as defined in §4053(8) (including vehicles that are not designed to perform a function of transporting a load over a public highway)

The vehicle or machinery must also either be:

- A plug-in electric vehicle that draws significant propulsion from an electric motor with a battery capacity of at least:

- 7 kilowatt hours if the gross vehicle weight rating (GVWR) is under 14,000 pounds

- 15 kilowatt hours if the GVWR is 14,000 pounds or more; or

- A fuel cell motor vehicle that satisfies the requirements of § 30B(b)(3)(A) and (B).

How to claim the credit

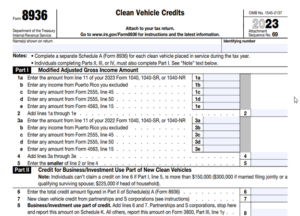

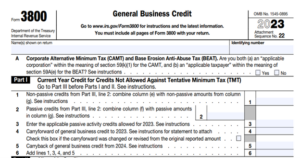

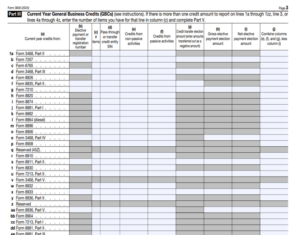

Partnerships and S corporations must file Form 8936, Clean Vehicle Credits.

All other taxpayers report this credit on line 1y in Part III of Form 3800, General Business Credit.

tax-electric-vehicles-credits-summary

![]() Basics & Beyond Resources

Basics & Beyond Resources

- Blog Page

- Resource List

- Webinar & Seminar Schedules

- Get Registered!

- Note: Paid attendees can request a link to the replay of any previously recorded webinar presentations by emailing us at [email protected]