November 2019 Issues

The newsletter is extra-long this month, a lot is happening as we approach a new filing season in 2020. We have been requested to discuss the New Form W-4 more in depth. We have discussed some of the changes in previous newsletters. It immediately became evident that in order to address your concerns a webinar would be the best way to explain the changes and impact on both employer and employee and time to address your questions online. Many use a computer-generated system for withholding and it also assists in providing the necessary forms, etc. But that system will not address questions from clients or employees that assist with payroll.

- Do you have employees who do payroll who may be asked questions about the New Form W-4?

- Is your firm providing training for those employees?

- Will your employees know how to withhold under the new W-4 format?

These and many more question need to be address as your firm provides services to employer clients, or address questions you may receive from your clients when they are presented with the New W-4?

Please let us know if you would be interested in a 1-2 hour W-4 webinar (in January) to cover the changes. Just email Claudine at: [email protected]

PTIN Renewal

Preparer Tax Identification Number (PTIN) applications and renewals for 2020 are now being processed. Anyone who prepares or assists in preparing federal tax returns for compensation must have a valid 2020 PTIN before preparing returns. All enrolled agents must also have a valid PTIN. There is no cost to renew.

Issue 1: Spend Less Time on the Phone with the IRS

A new GREAT resource was discovered by one of our instructors, Allison Boll-Fick – www.callenq.com

Calling the IRS is very time consuming, however this very inexpensive service seriously shortens call time. They have a free trial. Call 650-535-1040 or explore their website for more information.

Issue 2: Guidance on Form W-4 – Commentary on the Problems IRS Has Created

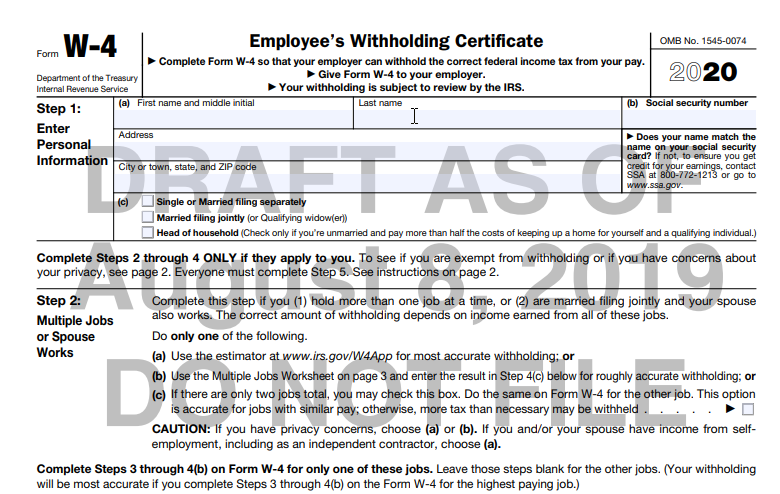

The 2020 Form W-4 has been redesigned to reduce the form’s complexity and to increase transparency and accuracy in the withholding system, as well as confuse not only employers but employees as well. That is all well and good, but the employee must actually read the W-4, to complete it properly.

Beginning with the 2020 Form W-4, employees will no longer be able to request adjustments to their withholding using withholding allowances, which most never understood anyway. Instead, using the new Form W-4, employees will provide employers with amounts to increase or reduce taxes and amounts to increase or decrease the amount of wage income subject to income tax withholding.

The 4 steps will require some tax knowledge on the part of both the employee and the employer.

Step 1 is basic knowledge of name, address and social security number. The employee must then choose a filing status. Considering filing status is a key component that determines, tax brackets and the standard deduction, choosing the wrong filing status could determine the wrong withholding from the very beginning.

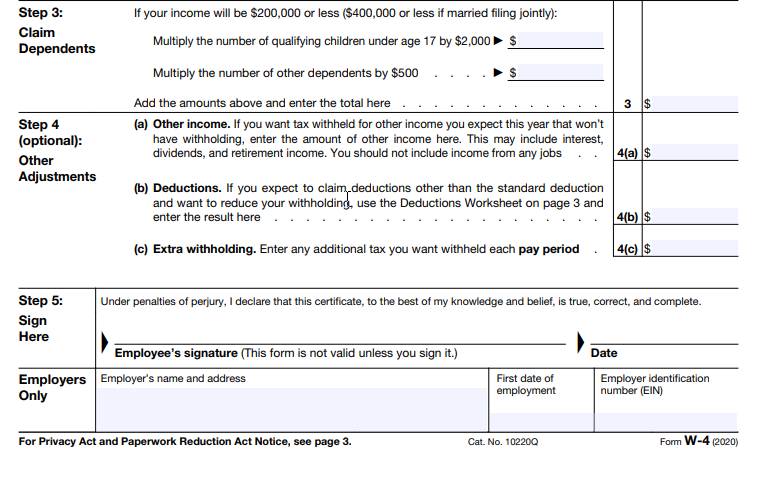

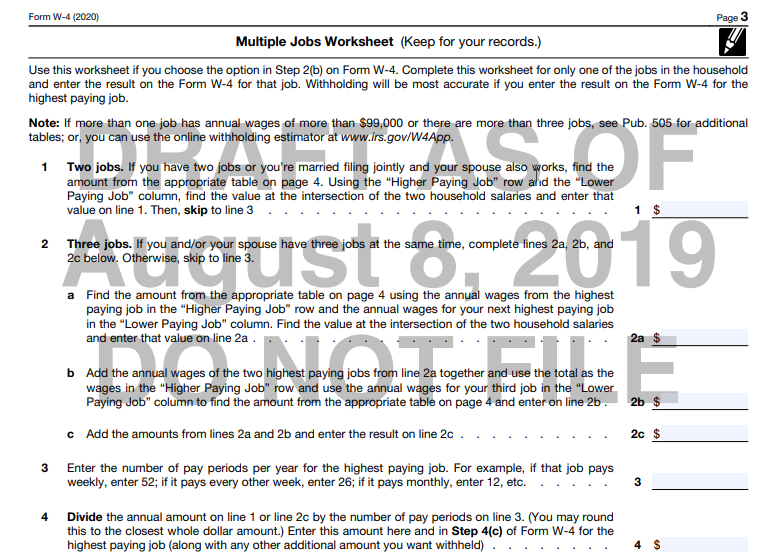

Step 2 is for Multiple Jobs and the Spouse Who Works. The Form instructions provide an estimator at IRS.gov to figure accurate withholding or the employee can go to a half page worksheet and tables are provided so employees can figure proper withholding. The issue is they must have some idea as to what kind of income they will make during the year. That is a problem in itself. Many people live paycheck to paycheck and do not think of long term. So even though the worksheet is available it will generate confusion as to how to complete and whether or not they have the knowledge to complete.

Step 3 Claiming Dependents

Maybe I have been doing this for too long, but anyone with children tries to claim them as dependents. Most claims are justified, but we as tax professional deal with those separated parents who both think they each deserve the dependent. Now we have a W-4 that lets them claim a credit for them on the W-4, this will be another confusing issue for some people and could result in under withholding in many cases.

Step 4 Optional Adjustments – Other income, deductions and extra withholding

The only concern in this area is itemized deductions. Unless the taxpayer has basic knowledge in tax law and they know the difference between the standard deduction and itemized deduction, this will be a confusing issue.

For employees who do not complete any steps other than Step 1 and Step 5, the signature area, employers will withhold the amount based on the filing status and wage amounts.

The new form also requires employers to have a better understanding of how the form functions. Employers will use the amounts in Step 3 as an annual reduction in the amount of withholding. If the Step 3 total is blank, but there are amounts entered on the left in Step 3, the employer should consider asking the employee if leaving the line blank was intended.

Steps 4(a) and 4(b) requires the employers to increase the annual amount of wages subject to income tax withholding by the annual amount shown on Step 4(a) and reduce the annual amount of wages subject to income tax withholding by the annual amount shown on Step 4(b). Employers must then increase withholding by the per pay period tax amount on Step 4(c).

Lovely, now we have a confused new employee, a confused employer and we will probably end up with a Step 1 and a Step 5 when all is said and done. Just the opposite of what IRS intended.

Beginning in 2020

All employers must use the new form for new employees. Also, old employees must use the new form if they wish to adjust their withholding. One good thing did come out of all of this. If an old employee does not submit a new Form W-4, employers must continue to withhold based on the W-4 previously submitted.

The final version of the 2020 Form W-4 will be released in November. Publication 15-T, the new corresponding Federal Income Tax Withholding Methods computational addition will assist employers in how to handle the form.

The IRS recommends employers follow the manual instructions in Publication 15-T if the employer’s automated system is not current for the new 2020 Form W-4.

Employer Guidance on Supplemental Wages and Bonuses

The 2020 Publication 15 has yet to be released and no draft is currently available. Chapter 7 covers supplemental wages and the withholding methods that are employed to calculate correct withholding. There are 4 methods available that remain unchanged even though the Form W-4 has been revamped.

- Withholding on supplemental wages when an employee receives more than $1 million of supplemental wages from an employer during the calendar year.

- Withholding on supplemental wage payments to an employee who doesn’t receive $1 million of supplemental wages during the calendar year.

- Supplemental wages combined with regular wages.

- Supplemental wages identified separately from regular wages.

These methods remain unchanged for now. The IRS has not indicated they intend to make changes to these methods.

Does Basic and Beyond need to provide a webinar in late December or early January to address practitioner concerns?

Let us know your thoughts!

Issue 3: Guidance on Virtual Currency Finally Updated

As part of a wider effort to assist taxpayers and to enforce the tax laws in a rapidly changing area, the Internal Revenue Service has issued two new pieces of guidance for taxpayers who engage in transactions involving virtual currency.

Expanding on guidance from 2014, the IRS is issuing additional detailed guidance to help taxpayers better understand their reporting obligations for specific transactions involving virtual currency. The new guidance includes Revenue Ruling 2019-24 and frequently asked questions (FAQs). The new revenue ruling addresses common questions by taxpayers and tax practitioners regarding the tax treatment of a cryptocurrency hard fork. In addition, a set of FAQs address virtual currency transactions for those who hold virtual currency as a capital asset.

The new guidance supplements the guidance the IRS issued on virtual currency in Notice 2014-21. In Notice 2014-21, the IRS applied general principles of tax law to determine that virtual currency is property for federal tax purposes.

The IRS is aware that some taxpayers with virtual currency transactions may have failed to report income and pay the resulting tax or did not report their transactions properly. The IRS is actively addressing potential non-compliance in this area through a variety of efforts, ranging from taxpayer education to audits to criminal investigations. In July of this year the IRS announced that it began mailing educational letters to more than 10,000 taxpayers who may have reported transactions involving virtual currency incorrectly or not at all. Taxpayers who did not report transactions involving virtual currency or who reported them incorrectly may, when appropriate, be liable for tax, penalties and interest. In some cases, taxpayers could be subject to criminal prosecution.

Revenue Ruling 2019-24

The ruling provides us with definitions of terms and needed guidance on how the process unfolds.

(1) Does a taxpayer have gross income under § 61 of the Internal Revenue Code

as a result of a hard fork of a cryptocurrency, the taxpayer owns, if the taxpayer does not receive units of a new cryptocurrency?

(2) Does a taxpayer have gross income under § 61 as a result of an airdrop of a new cryptocurrency following a hard fork if the taxpayer receives units of new cryptocurrency?

Virtual currency is a digital representation of value that functions as a medium of exchange, a unit of account, and a store of value other than a representation of the United States dollar or a foreign currency.

Foreign currency is the coin and paper money of a country other than the United States that is designated as legal tender, circulates, and is customarily used and accepted as a medium of exchange in the country of issuance

Cryptocurrency is a type of virtual currency that utilizes cryptography to secure transactions that are digitally recorded on a distributed ledger, such as a blockchain. Units of cryptocurrency are generally referred to as coins or tokens. Distributed ledger technology uses independent digital systems to record, share, and synchronize transactions, the details of which are recorded in multiple places at the same time with no central data store or administration functionality.

A hard fork is unique to distributed ledger technology and occurs when a cryptocurrency on a distributed ledger undergoes a protocol change resulting in a permanent diversion from the legacy or existing distributed ledger. A hard fork may result in the creation of a new cryptocurrency on a new distributed ledger in addition to the legacy cryptocurrency on the legacy distributed ledger. Following a hard fork, transactions involving the new cryptocurrency are recorded on the new distributed ledger and transactions involving the legacy cryptocurrency continue to be recorded on the legacy distributed ledger.

An airdrop is a means of distributing units of a cryptocurrency to the distributed ledger addresses of multiple taxpayers. A hard fork followed by an airdrop result in the distribution of units of the new cryptocurrency to addresses containing the legacy cryptocurrency. However, a hard fork is not always followed by an airdrop.

Cryptocurrency from an airdrop generally is received on the date and at the time it is recorded on the distributed ledger. However, a taxpayer may constructively receive cryptocurrency prior to the airdrop being recorded on the distributed ledger. A taxpayer does not have receipt of cryptocurrency when the airdrop is recorded on the distributed ledger if the taxpayer is not able to exercise dominion and control over the cryptocurrency. For example, a taxpayer does not have dominion and control if the address to which the cryptocurrency is airdropped is contained in a wallet managed through a cryptocurrency exchange and the cryptocurrency exchange does not support the newly-created cryptocurrency such that the airdropped cryptocurrency is not immediately credited to the taxpayer’s account at the cryptocurrency exchange.

If the taxpayer later acquires the ability to transfer, sell, exchange, or otherwise dispose of the cryptocurrency, the taxpayer is treated as receiving the cryptocurrency at that time.

Two situations are discussed in the ruling.

- Andrew holds 50 units of Crypto M, a cryptocurrency. On Date 1, the distributed ledger for Crypto M experiences a hard fork, resulting in the creation of Crypto N. Crypto N is not airdropped or otherwise transferred to an account owned or controlled by Andrew.

- Brenda holds 50 units of Crypto R, a cryptocurrency. On Date 2, the distributed ledger for Crypto R experiences a hard fork, resulting in the creation of Crypto S. On that date, 25 units of Crypto S are airdropped to Brenda’s distributed ledger address and Brenda has the ability to dispose of Crypto S immediately following the airdrop. Brenda now holds 50 units of Crypto R and 25 units of Crypto S. The airdrop of Crypto S is recorded on the distributed ledger on Date 2 at Time 1 and, at that date and time, the fair market value of B’s 25 units of Crypto S is $50. Brenda receives the Crypto S solely because B owns Crypto R at the time of the hard fork. After the airdrop, transactions involving Crypto S are recorded on the new distributed ledger and transactions involving Crypto R continue to be recorded on the legacy distributed ledger.

- 61(a)(3) provides that, except as otherwise provided by law, gross income means all income from whatever source derived, including gains from dealings in property. Under § 61, all gains or undeniable accessions to wealth, clearly realized, over which a taxpayer has complete dominion, are included in gross income. In general, income is ordinary unless it is gain from the sale or exchange of a capital asset or a special rule applies.

- 1011 provides that a taxpayer’s adjusted basis for determining the gain or loss from the sale or exchange of property is the cost or other basis determined under § 1012 of the Code, adjusted to the extent provided under § 1016. When a taxpayer receives property that is not purchased, unless otherwise provided in the Code, the taxpayer’s basis in the property received is determined by reference to the amount included in gross income, which is the fair market value of the property when the property is received.

- 451 of the Code provides that a taxpayer using the cash method of accounting includes an amount in gross income in the taxable year it is actually or constructively received. A taxpayer using an accrual method of accounting generally includes an amount in gross income no later than the taxable year in which all the events have occurred which fix the right to receive such amount.

Results in our two situations.

- Andrew did not receive units of the new cryptocurrency, Crypto N, from the hard fork; therefore, he does not have an accession to wealth and does not have gross income under § 61 as a result of the hard fork.

- Brenda received a new asset, Crypto S, in the airdrop following the hard fork; therefore, she has an accession to wealth and has ordinary income in the taxable year in which the Crypto S is received. Brenda has dominion and control of Crypto S at the time of the airdrop, when it is recorded on the distributed ledger, because she immediately has the ability to dispose of Crypto S. The amount included in gross income is $50, the fair market value of the 25 units of Crypto S when the airdrop is recorded on the distributed ledger. Brenda’s basis in Crypto S is $50, the amount of income recognized.

Key Holdings

(1) A taxpayer does not have gross income under § 61 as a result of a hard fork of a cryptocurrency the taxpayer owns if the taxpayer does not receive units of a new cryptocurrency.

(2) A taxpayer has gross income, ordinary in character, under § 61 as a result of an airdrop of a new cryptocurrency following a hard fork if the taxpayer receives units of new cryptocurrency.

The frequently asked questions can be found on the IRS website at: https://www.irs.gov/newsroom/frequently-asked-questions-on-virtual-currency-transactions

Issue 4: Social Security Announces 1.6 % Benefit Increase for 2020

Social Security and Supplemental Security Income (SSI) benefits for nearly 69 million Americans will increase 1.6 % in 2020.

The 1.6 % cost-of-living adjustment (COLA) will begin with benefits payable to more than 63 million Social Security beneficiaries in January 2020. Increased payments to more than 8 million SSI beneficiaries will begin on December 31, 2019.

Some other adjustments that take effect in January of each year are based on the increase in average wages. Based on that increase, the maximum amount of earnings subject to the Social Security tax (taxable maximum) will increase to $137,700 from $132,900.

The 7.65% tax rate is the combined rate for Social Security and Medicare. The Social Security portion (OASDI) is 6.20% on earnings up to the applicable taxable maximum amount. The Medicare portion (HI) is 1.45% on all earnings. Also, as of January 2013, individuals with earned income of more than $200,000 ($250,000 for married couples filing jointly) pay an additional 0.9 % in Medicare taxes.

Issue 5: Nearly 2 million Individual Taxpayer Identification Numbers (ITINs) are Set to Expire at the End of 2019

Under the Protecting Americans from Tax Hikes (PATH) Act, ITINs that have not been used on a federal tax return at least once in the last three consecutive years will expire Dec. 31, 2019. In addition, ITINs with middle digits 83, 84, 85, 86 or 87 that have not already been renewed will also expire at the end of the year. These affected taxpayers who expect to file a tax return in 2020 must submit a renewal application as soon as possible.

ITINs are used by people who have tax filing or payment obligations under U.S. law but who are not eligible for a Social Security number.

several languages, including English, Spanish, Traditional Chinese, Russian, Vietnamese, Korean and Haitian/Creole on IRS.gov.

Who Should Renew an ITIN?

- Taxpayers whose ITIN is expiring and who expect to have a filing requirement in 2020 must submit a renewal application. Others do not need to take any action. ITINs with the middle digits 83, 84, 85 or 86, 87 (For example: 9NN-83-NNNN) need to be renewed even if the taxpayer has used it in the last three years.

- ITINs with middle digits of 70 through 82 have previously expired. Taxpayers with these ITINs can still renew at any time, if they have not renewed already.

Family option remains available

Taxpayers with an ITIN that has middle digits 83, 84, 85, 86 or 87, as well as all previously expired ITINs, have the option to renew ITINs for their entire family at the same time. Those who have received a renewal letter from the IRS can choose to renew the family’s ITINs together, even if family members have an ITIN with middle digits that have not been identified for expiration. Family members include the tax filer, spouse and any dependents claimed on the tax return.

How to renew an ITIN

To renew an ITIN, a taxpayer must complete a Form W-7 and submit all required documentation. Taxpayers submitting a Form W-7 to renew their ITIN are not required to attach a federal tax return. However, taxpayers must still note a reason for needing an ITIN on the Form W-7.

Spouses and dependents residing outside of the U.S. only need to renew their ITIN if filing an individual tax return, or if they qualify for an allowable tax benefit (e.g., a dependent parent who qualifies the primary taxpayer to claim head of household filing status.) In these instances, a federal return must be attached to the Form W-7 renewal application.

There are three ways to submit the Form W-7 application package. Taxpayers can:

- Mail the form, along with original identification documents or copies certified by the agency that issued them, to the IRS address listed on the Form W-7 instructions. The IRS will review the identification documents and return them within 60 days.

Work with Certified Acceptance Agents (CAAs) authorized by the IRS to help taxpayers apply for an ITIN. - In advance, call and make an appointment at a designated IRS Taxpayer Assistance Center to have each applicant’s identity authenticated in person instead of mailing original identification documents to the IRS. Each family member applying for an ITIN or renewal must be present at the appointment and must have a completed Form W-7 and required identification documents.

As a reminder, the IRS no longer accepts passports that do not have a date of entry into the U.S. as a stand-alone identification document for dependents from a country other than Canada or Mexico, or dependents of U.S. military personnel overseas. The dependent’s passport must have a date of entry stamp, otherwise the following additional documents to prove U.S. residency are required:

- U.S. medical records for dependents under age 6,

- U.S. school records for dependents under age 18, and

- U.S. school records (if a student), rental statements, bank statements or utility bills listing the applicant’s name and U.S. address, if over age 18.

Issue 6: Information Letter Addresses Definition of “Full-time Life Insurance Salesman”

Number: 2019-0023 Release Date: 9/27/2019

GENIN-127292-18- UIL: 9999.98-00

Thank you for your inquiry concerning the impact that The Tax Cuts and Jobs Act, P.L. 115-9 has on insurance salespersons. Specifically, you note that commission-based salespersons historically treated as common law employees are now at a disadvantage to similarly situated salespersons that are either independent contractors or statutory employees. You ask that the Internal Revenue Service (IRS) reevaluate its historic position that limits the definition of a full-time life insurance salesman under § 3121(d)(3)(B) of the Internal Revenue Code to workers who primarily sell life insurance and annuity contracts for one insurance company, and allow such definition to include workers who also sell accident and health insurance.

A full-time life insurance salesman as described in § 3121(d)(3)(B) includes only those workers who are NOT common law employees. The criteria for determining a worker’s status as an employee or an independent contractor for taxes under the Federal Insurance Contributions Act, the Federal Unemployment Tax Act, and for federal income tax withholding purposes are found in §§ 31.3121(d)-1, 31.3306(c)-2 and 31.3401(c)-1 of the Employment Tax Regulations. These regulations provide, in general, that if the worker provides services under the direction and control of the service recipient, the worker is considered an employee for employment tax purposes. The rules reflect common law principles, developed and affirmed over decades by the courts, that govern IRS policy in this area. Under these common law principles, even a full-time life insurance salesman may properly be classified as a common law employee if he or she is subject to the direction and control of the service recipient. In other words, the type of insurance sold by a worker is not, by itself, determinative of the worker’s status as a common law employee, statutory employee, or independent contractor. Instead, the service recipient’s authority to exercise direction and control over the worker providing the services determines a worker’s status as a common law employee.

The term “full-time life insurance salesman” used in § 3121(d)(3)(B) is not defined in the Code but is defined in legislative history as “an individual whose entire or principal business activity is devoted to the solicitation of life insurance and annuity contracts primarily for one life-insurance company . . . [NOT] an individual who is engaged in the general insurance business under a contract or contracts of service which do not contemplate that the individual’s principal business activity will be the solicitation of life insurance and annuity contracts for one company, or any individual who devotes only part time to the solicitation of life insurance or annuity contracts . . .” You correctly note that the rulings that narrowly interpret statutory employee to only permit a de minimis amount of sales from accident and health insurance were written in the early 1950’s and have not been updated to reflect industry changes. However, they still reflect the IRS’s interpretation of the law.

Revenue Ruling 54-312, clarified by Rev. Rul. 59-103, provides that the entire or principal business activity of an individual is deemed to be devoted to the solicitation of life insurance or annuity contracts primarily for one life insurance company when, pursuant to the terms and conditions of the arrangement with the life insurance company or its general agent, it is mutually agreed or clearly contemplated by the parties that the individual’s entire or principal business activity is the solicitation of applications for life insurance or annuity contracts.

Rev. Rul. 59-103 clarifies that the reference to the sale of accident and health insurance in Rev. Rul. 54-312 was intended to relate only to the incidental sale of that type of insurance, and the definition of “full-time life insurance salesman” includes “only those individuals engaged primarily in the sale of life insurance and annuity contracts and not individuals engaged primarily in the sale of accident and health insurance.”

After careful consideration, we believe a legislative change is needed to expand the definition in the way that you request. Given the specific statutory language in §3121(d)(3)(B), i.e., “full-time life insurance salesman,” supported by the Senate Report indicating that such language does not include one in the general insurance business or one who only sells life insurance part-time, and in view of our position as reflected in published guidance, we think broadening the definition of a “full-time life insurance salesman” for purposes of § 3121(d)(3)(B) would require a legislative change. Because the Office of the Tax Legislative Counsel in the Treasury Department makes the recommendations for tax law changes, we have forwarded a copy of your letter to that office.

Issue 7: New Payment option Available to Taxpayers in Private Debt Collection Program

Internal Revenue Service announced that a new payment option has been added to the private debt collection program to make it easier for those who owe to pay their tax debts.

Taxpayers now can choose the convenient option of a preauthorized direct debit to make one payment or a series of payments toward their federal tax debt. With direct debit, the taxpayer will give their written permission to the private collection agency (PCA) to authorize a payment on the taxpayer’s behalf to the U.S. Department of the Treasury. This enables the taxpayer to conveniently and securely schedule multiple payments with the ease of a single phone call with their assigned PCA.

When taxpayers choose the preauthorized direct debit option, they’ll complete and sign a written authorization which can be submitted to the PCA by mail or fax. The authorization contains the payment schedule and bank account information.

Once the PCA receives the taxpayer’s signed authorization, it will send a confirmation letter containing the details of the preauthorized direct debit. The PCA will create a check according to the payment schedule made out to the U.S. Department of the Treasury. The check is securely mailed to the IRS within 24 hours.

The new direct debit supplements existing IRS-sponsored payment options and can be changed or canceled up to one business day prior to the scheduled payment. Taxpayers can still opt to use the electronic payment options available on IRS.gov/Paying Your Taxes. Payments by check should be payable to the U.S. Treasury and sent directly to the IRS, not the PCA.

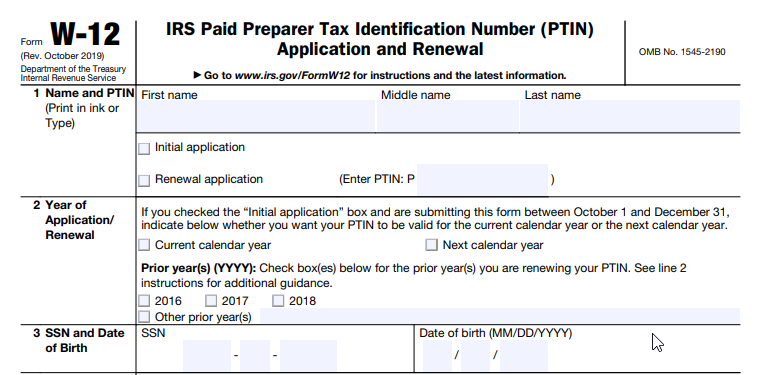

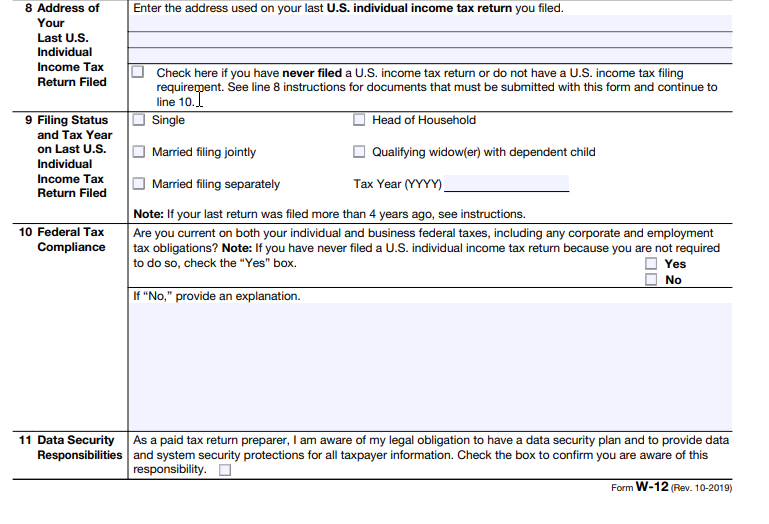

Issue 8: New Version of Preparer Tax Identification Number Application and Renewal Form Released – Form W-12, IRS Paid Preparer Tax Identification Number (PTIN) Application and Renewal

The IRS has released a new version of Form W-12, IRS Paid Preparer Tax Identification Number (PTIN) Application and Renewal and instructions (Rev. October 2019).

A person who prepares an income tax return or refund claim for pay must include his or her identifying number on that return or claim for refund. Before 2011, a paid tax return preparer (PTRP) used his or her Social Security Number (SSN) for this purpose. Since 2011, PTRPs must use a PTIN issued by the IRS, instead of their SSN, as an identifying number on income tax returns or claims for refund. A PTRP may obtain a PTIN through the online registration system on the Tax Professional’s page on the IRS’s website or by filing a paper application on Form W-12. It takes four to six weeks for the IRS to process a paper application.

New Form. Unlike the prior version of Form W-12, the new version contains a checkbox on line 11 that requires PTRPs to acknowledge their data security responsibilities. By checking this box, PTRPs confirm that they are aware of their legal obligation to have a data security plan in place and to provide data and system security protections for all taxpayer information. Enrolled agents who do not prepare returns can skip line 11.

Issue 9: Employers May Claim Tax Credit for Providing Paid Family and Medical Leave to Employees

Employers who provide paid family and medical leave to their employees may claim a credit for tax years 2018 and 2019. The Employer Credit for Paid Family and Medical Leave is a business credit based on a percentage of wages paid to qualifying employees while they’re on family and medical leave.

To claim the credit, eligible employers must have a written policy in place that satisfies certain requirements, including:

- At least two weeks of paid leave to full-time employees (prorated for part-time employees), and

- The paid leave must be at least 50% of the wages normally paid to the employee.

The credit is generally effective for wages paid in taxable years beginning after Dec. 31, 2017, and before Jan.1, 2020. Eligible employers use Form 8994, Employer Credit for Paid Family and Medical Leave, to calculate the credit.

Qualifying Employees

A qualifying employee is any employee under the Fair Labor Standards Act who has been employed by the employer for one year or more and who, in the preceding year, didn’t have compensation of more than a certain amount. For tax year 2018 and 2019, the employee’s prior year compensation from the employer must have been $72,000 or less. Additionally, any requirement that an employee work 12 consecutive months or a minimum number of hours to be a qualifying employee would not be viewed as a reasonable method for determining whether an employee has been employed for one year.

Family and Medical Leave

Family and medical leave is for one or more of the following:

- Birth of an employee’s child and to care for the child;

- Placement of a child with the employee for adoption or foster care;

- To care for the employee’s spouse, child or parent who has a serious health condition;

- A serious health condition that makes the employee unable to do the functions of their position;

- Any qualifying exigency due to an employee’s spouse, child or parent being on covered active duty (or having been notified of an impending call or order to covered active duty) in the Armed Forces; and

- To care for a service member who’s the employee’s spouse, child, parent or next of kin.

Employer paid vacation leave, personal leave, or medical or sick leave (other than leave specifically designated for one or more of the purposes stated above and that cannot be used for reasons other than FMLA purposes or for any other reason) is not considered family and

medical leave. Also, employers may not take into account any leave paid by a state or local government or required by state or local law when determining the amount of employer-provided paid family and medical leave.

Wages paid by a third-party payer, such as an insurance company or a professional employer organization, to a qualifying employee for services performed for an eligible employer are considered wages for purposes of the credit. But, only the eligible employer, not the third-party

payer, can take these wages into consideration when calculating the credit.

Calculation of Credit

The credit is a percentage of the amount of wages paid to a qualifying employee while on family and medical leave for up to 12 weeks per taxable year. The applicable percentage is equal to 12.5% and increases by 0.25% for each percentage point by which the amount paid to a qualifying employee exceeds 50% of the employee’s wages. The maximum applicable percentage is 25%. In certain cases, an additional limit may apply.

An employer may not deduct wages or salaries paid or incurred equal to the amount claimed as a credit. Also, the employer may not use wages considered in determining other business credits when calculating this credit.

When to Claim the Credit

An employer can claim the credit only for leave taken after the written leave policy is in place. The written policy is considered to be in place on the later of the policy’s adoption date or the policy’s effective date. A transition rule applies for the first taxable year of an employer beginning after Dec. 31, 2017.

Notice 2018-71 and the Frequently Asked Questions on IRS.gov has more information on the credit

Issue 10: IRS Makes Identity Protection PINs Available to More Taxpayers

The IRS is expanding the opt-in Identity Protection Personal Identification Number (IP PIN) program to taxpayers in an additional 10 states for the 2020 filing season. This brings the availability of IP PINs to taxpayers in a total of 19 states and the District of Columbia. The opt-in program is designed for taxpayers who are not victims of identity theft or refund fraud.

For 2020, IP PINs will be available to taxpayers who previously filed in:

- Arizona

- California

- Colorado

- Connecticut

- Delaware

- District of Columbia

- Georgia

- Florida

- Illinois

- Maryland

- Michigan

- Nevada

- New Jersey

- New Mexico

- New York

- North Carolina

- Pennsylvania

- Rhode Island

- Texas and Washington.

Issue 11: IRS Relief Provides Drought-Stricken Farmers, Ranchers More Time to Replace Livestock

Farmers and ranchers who were forced to sell livestock due to drought may have an additional year to replace the livestock and defer tax on any gains from the forced sales.

The farmer or rancher must be in an applicable region. This is a county designated as eligible for federal assistance plus counties contiguous to that county. The relief generally applies to capital gains realized by eligible farmers and ranchers on sales of livestock held for draft, dairy or breeding purposes. Sales of other livestock, such as those raised for slaughter or held for sporting purposes, or poultry, are not eligible.

To qualify, the sales must be solely due to drought, flooding or other severe weather causing the region to be designated as eligible for federal assistance. Livestock generally must be replaced within a four-year period, instead of the usual two-year period.

The one-year extension gives eligible farmers and ranchers until the end of the tax year after the first drought-free year to replace the sold livestock. Details, including an example of how this provision works, can be found in Notice 2006-82.

The IRS provides this extension to farmers and ranchers located in the applicable region who qualified for the four-year replacement period if any county that is included in the applicable region is listed as suffering exceptional, extreme or severe drought conditions during any week between Sept. 1, 2018, and Aug. 31, 2019. This determination is made by the National Drought Mitigation Center. All or part of 32 states, plus Guam, the U.S. Virgin Islands and the Commonwealths of Puerto Rico and the Northern Mariana Islands, are listed in

As a result, qualified farmers and ranchers whose drought-sale replacement period was scheduled to expire at the end of this tax year, Dec. 31, 2019, in most cases, now have until the end of their next tax year. Because the normal drought-sale replacement period is four years, this extension immediately impacts drought sales that occurred during 2015. The replacement periods for some drought sales before 2015 are also affected due to previous drought-related extensions affecting some of these localities.

Issue 12: IRS Finalizes Safe Harbor to Allow Rental Real Estate to Qualify as a Business for Qualified Business Income Deduction

The IRS issued Revenue Procedure 2019-38 that has a safe harbor allowing certain interests in rental real estate, including interests in mixed-use property, to be treated as a trade or business for purposes of the qualified business income deduction under § 199A.

If all the safe harbor requirements are met, an interest in rental real estate will be treated as a single trade or business for purposes of the § 199A deduction. If an interest in real estate fails to satisfy all the requirements of the safe harbor, it may still be treated as a trade or business for purposes of the § 199A deduction if it otherwise meets the definition of a trade or business in the § 199A regulations.

This safe harbor is available for taxpayers who seek to claim the § 199A deduction with respect to a “rental real estate enterprise.” Solely for purposes of this safe harbor, a rental real estate enterprise is defined as an interest in real property held to generate rental or lease income. It may consist of an interest in a single property or interests in multiple properties. The taxpayer or a relevant passthrough entity relying on this revenue procedure must hold each interest directly or through an entity disregarded as an entity separate from its owner, such as a limited liability company with a single member.

The following requirements must be met by taxpayers or RPEs to qualify for this safe harbor:

- Separate books and records are maintained to reflect income and expenses for each rental real estate enterprise.

- For rental real estate enterprises that have been in existence less than four years, 250 or more hours of rental services are performed per year. For other rental real estate enterprises, 250 or more hours of rental services are performed in at least three of the past five years.

- The taxpayer maintains contemporaneous records, including time reports, logs, or similar documents, regarding the following: hours of all services performed; description of all services performed; dates on which such services were performed; and who performed the services.

- The taxpayer or RPE attaches a statement to the return filed for the tax year(s) the safe harbor is relied upon.

Issue: 13 IRS Updates Remedial Amendment Periods for Correcting 403(b) Plan Defects – Rev. Proc. 2019-39, 2019-42 IRB

IRS has issued guidance establishing remedial amendment periods that allow eligible employers to retroactively correct form defects by timely adopting a pre-approved §403(b) plan or by otherwise timely amending their individually designed §403(b) plan.

Rev. Proc. 2019-39 provides a limited extension of the initial remedial amendment period for certain form defects and establishes a system of §403(b) pre-approved plan cycles under which a pre-approved plan sponsor may submit a proposed § 403(b) pre-approved plan for IRS review and approval. Once approved, the pre-approved plan may be adopted by eligible employers. In addition, the revenue procedure sets out deadlines for the adoption of plan amendments. The revenue procedure provides guidance on the following:

Recurring remedial amendment periods for individually designed plans

End of remedial amendment period—nongovernmental plans.

- New plan

- Amendment to existing plan.

- Change in Sec. 403(b) requirements.

End of remedial amendment period—governmental plans.

- New Plan

- Amendment to existing plan.

- Change in Sec. 403(b) requirements.

Terminating plans

Retroactive Limited Corrections

Plan amendment deadlines.

Plan amendment deadlines for discretionary amendments.

Limited extension of initial remedial amendment period.

Issue 14: Early Reporting Replaces Form W-2 Verification Code

Because of new wage and income reporting requirements, the IRS is discontinuing the Form W-2 Verification Code pilot for the 2019 tax year. Federal law now requires employers to submit Forms W-2 by January 31 each year, which helps the IRS combat fraud and identity theft and superseded the need for a verification code. The Form W-2 Verification Code marked an unprecedented cooperative effort between payroll service providers, employers, tax software providers, tax professionals, the Social Security Administration and the IRS to identify new avenues to ensure the accuracy of information reported on tax returns and to identify fraudulent tax returns. The pilot project was voluntary and appeared only on electronic tax returns. March 31. The new January 31 deadline enables the IRS to more quickly verify information on the Form W-2 to information on the Form 1040.

Issue 15: IRS Releases New Tax Gap Estimates

Generally, the IRS uses tax gap estimates to determine the historical scale of tax compliance and to help find persistent sources of low tax compliance. Tax gap estimates also inform policymakers of potential areas that need to be addressed, including how to allocate resources used to administer the tax code.

Tax year 2011-2013 estimates. According to IRS’s information release, the average gross tax gap was estimated at $441 billion per year for 2011, 2012, and 2013. The average net tax gap was estimated at $381 billion.

Broken down into the separate components:

- $39 billion was the estimated non-filing tax gap,

- $352 billion was the underreporting tax gap, and

- $50 billion was the underpayment tax gap.

- Broken down by the various types of taxes:

- $314 billion was the estimated gross tax gap for individual income tax,

- $42 billion was the estimated gross tax gap for corporate income tax,

- $81 billion was the gross tax gap for employment taxes, and

- $3 billion was the gross tax gap for estate and excise tax combined.

The tax gap estimates reflected that about 83.6% of taxes were paid voluntarily and on time. That percentage remained virtually unchanged from the tax year 2008-2010 estimate of 83.8%. After enforcement efforts were factored in, the estimated percentage of taxes paid was 85.8% for both the 2008-2010 period and the 2011-2013 period.

Issue 16: Data Security Message from the IRS Return Preparer Office

The IRS Return Preparer Office sent the following message this week to all registered holders of PTINs (Preparer Tax Identification Numbers):

Dear Tax Professional,

Summer is over, and it won’t be long until you’re sitting down at your computer to renew your preparer tax identification number (PTIN) for 2020. In mid-October when renewal season begins, you will notice a data security responsibilities statement has been added to the PTIN renewal process. It serves as a reminder of your legal responsibility to have a data security plan and to provide data and system security protections for all taxpayer information. When completing your PTIN renewal, a checkbox will be available to confirm your awareness of these data security responsibilities.

Data security continues to be a hot topic. That’s because tax professionals remain a top target of identity thieves and data breaches continue to affect tax professionals at an alarming rate. Cybercriminals use sophisticated and ever evolving techniques to gain access to your systems. These criminals steal sensitive taxpayer data to file fraudulent tax returns and create financial havoc for your clients. There are simple steps you can incorporate in your daily operations to minimize your vulnerability and protect client data, including:

- Protect email accounts with strong passwords and two-factor authentication if available.

- Install an anti-phishing tool bar to help identify known phishing sites.

- Use anti-phishing tools that are included in security software products.

- Use security software to help protect systems from malware and scan emails for viruses.

- Never open or download attachments from unknown senders, including potential clients. They should instead make contact first by phone.

- Send only password-protected and encrypted documents when files must be shared with clients over email.

- Never respond to suspicious or unknown emails.

- Back up sensitive data to a safe and secure external source.

- Properly dispose of old computer hard drives that contain sensitive data.

You should also make sure to have a written data security plan in accordance with the Federal Trade Commission’s Safeguard Rule. Remember, protecting your clients is not only good for business, it’s also the law. While the hope is that you’re never the victim of a data breach, preparation and education will go a long way in helping to protect your clients and yourself.

You should also make sure to have a written data security plan in accordance with the Federal Trade Commission’s Safeguard Rule. Remember, protecting your clients is not only good for business, it’s also the law. While the hope is that you’re never the victim of a data breach, preparation and education will go a long way in helping to protect your clients and yourself.

More information:

Publication 4557, Safeguarding Taxpayer Data

Publication 5293, Data Security Resource Guide for Tax Professionals

Identity Theft Information for Tax Professionals

Issue 17: IRS Launches New Tool to Help Workers with Self-Employment Income

The new Tax Withholding Estimator online tool includes a feature designed to make it easier for employees who also receive self-employment income to accurately estimate the correct amount of tax to have withdrawn from their pay.

The Tax Withholding Estimator is an online tool that replaces the Withholding Calculator. The new tool offers self-employed taxpayers a more accurate way to calculate the amount of income tax they want to have withheld from their wages.

Issue 18: New Addresses for Employee Plans Submissions

The addresses for Employee Plans submissions for determination letters, letter rulings, and IRA opinion letters have changed. The new addresses apply to Forms 5300, 5306, 5306-A, 5307, 5308, 5310, 5310-A, 5316, and 8717.

The new mailing address is as follows:

Internal Revenue Service

TE/GE Stop 31A

Team 105 P.O. Box 12192

Covington, KY 41012-0192

For submissions sent by private delivery service, the new address is as follows:

Internal Revenue Service

7940 Kentucky Drive

TE/GE Stop 31A Team 105

Florence, KY 41042

Please note that the mailing address for pre-approved plan submissions has not changed.

Issue 19: An Information Letter Provides Insight as it Explains Why Taxpayers with a Religious Objection to Social Security May No Longer Claim the Child Tax Credit for a Child without a Social Security Number

Background—religious objections to Social Security. Certain recognized religious sects are conscientiously opposed to accepting the benefits of any public or private insurance for old age, death, disability, retirement, or medical care. Members of these religious sects may be exempted from paying Social Security, Medicare and self-employment taxes. These individuals are not required to obtain a Social Security Number (SSN) for themselves or their dependent children. (§ 1402(g))

Background—child tax credit. Before the enactment of the Tax Cuts and Jobs Act, § 24 allowed a taxpayer to claim a child tax credit (CTC) of up to $1,000 per qualifying child. To receive the CTC, the taxpayer was required to provide each child’s taxpayer-identification number (TIN). Thus, pre-TCJA § 24 did not require a qualifying child’s SSN, and taxpayers who had religious objections to applying for an SSN could claim the CTC using the qualifying child’s TIN, instead of the qualifying child’s SSN.

However, the TCJA added special rules governing the administration of the CTC for tax years 2018 through 2025. Under one of these special rules, a taxpayer can’t claim a CTC unless the taxpayer includes the qualifying child’s SSN on the taxpayer’s return. For this purpose, the child’s SSN must be issued before the due date of the return by the Social Security Administration to a U.S. citizen or an alien authorized to work in the U.S. § 24(h)(7))

Background—Religious Freedom Restoration Act of 1993. The Religious Freedom Restoration Act (RFRA) prohibits the federal government from substantially burdening a person’s exercise of religion unless it demonstrates that application of the burden to the person (1) furthers a compelling governmental interest, and (2) is the least restrictive means of furthering that compelling governmental interest.

Children without SSNs don’t qualify for CTC. The Information Letter points out that the RFRA does not require the IRS to provide administrative relief to taxpayers who have religious or conscience-based objections to obtaining SSNs. The IRS could provide such relief before the amendment of § 24 only because the statute allowed taxpayers to claim the credit by providing a TIN (which the IRS can issue) not an SSN (which only the SSA can issue) for each qualifying child. But, in enacting the new CTC rules, Congress unequivocally declared that only taxpayers who provide a qualifying child’s SSN should be allowed the CTC. Therefore, children without SSNs don’t qualify for the CTC.

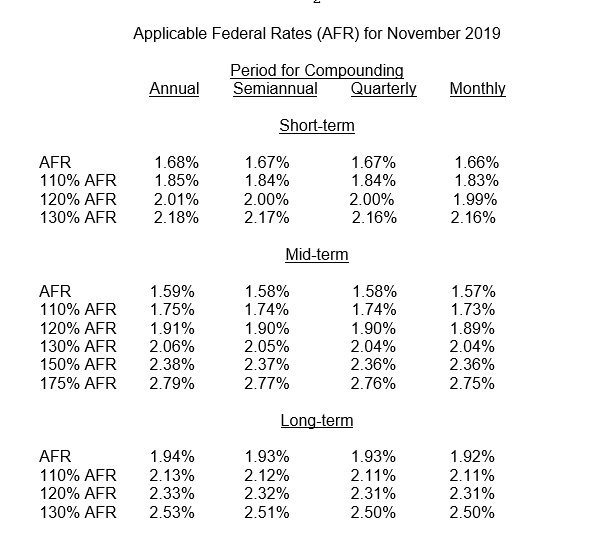

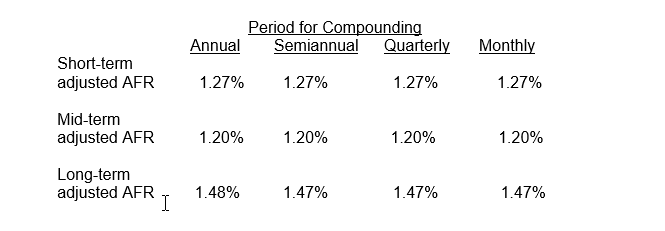

Issue: 20 Rev. Rul. 2019-25 – Applicable Federal Rates for November 2019

REV. RUL. 2019-25 TABLE 2

Adjusted AFR for November 2019

REV. RUL. 2019-25 TABLE 3

Rates Under § 382 for November 2019

Adjusted federal long-term rate for the current month 1.48%

Long-term tax-exempt rate for ownership changes during the current month (the highest of the adjusted federal long-term rates for the current month and the prior two months.) 1.68%

REV. RUL. 2019-25 TABLE 4

Appropriate Percentages Under § 42(b)(1) for November 2019 Note: Under §42(b)(2), the applicable percentage for non-federally subsidized new buildings placed in service after July 30, 2008, shall not be less than 9%.

Appropriate percentage for the 70% present value low-income housing credit 7.40%

Appropriate percentage for the 30% present value low-income housing credit 3.17%

REV. RUL. 2019-25 TABLE 5

Rate Under § 7520 for November 2019

Applicable federal rate for determining the present value of an annuity, an interest in life or a term of years, or a remainder or reversionary interest 2.0%