Trump Signs COVID-19 Relief Bill with PPP Expansion

Basics and Beyond is ready to provide an update on the newest COVID-19 bill signed into law.

This webinar will review the COVID-19 Relief Bill: Coronavirus Relief Act of 2020, PPP loan funds and forgiveness, Business Meals, FFCRA, Employee Retention Credit, Tax Extenders, SBA Loans, etc.

Join AJ Reynolds and Kristy Maitre on January 7th from 2-4pm EST

In This Issue

- Issue 1: Update on PPP Loans – More Information at the January 7 webinar

- Issue 2: What’s New with 1099 Misc. and 1099 NEC?

- Issue 3: Notice 2020-61 – Defined Benefit Plan Contributions Have Until January 4, 2021 to be Made

- Issue 4: Dawson Pre-Launch – FAQ’s

- Issue 5: Nexus and State Guidance

- Issue 6: Common Error to Avoid When Claiming Employer Tax Credits

- Issue 7: REG-123652-18 – Treatment of Special Enforcement Matters

- Issue 8: Changes to Form 1065 for 2020 (Draft NOT Final)

- Issue 9: Remember February 1, 2021 Deadline for Form W-2, Other Wage statements

- Issue 10: IRS to Increase Focus on Tax Return Preparers Who Have Not Filed Their Own Returns

- Issue 11: Updated Information Concerning PPP Loans and Eligibility for the Employee Retention is Special Situations

- Issue 12: 2021 Online Tax Preparation Products to Offer Multi-factor Authentication for Taxpayers, Tax Pros

- Issue 13: Form 7200 IRS Delay in Payments

- Issue 14: IRS Updates FAQ’s for COVID-19 Tax Credits for The Families First Coronavirus Response Act

- Issue 15: IRS Mail Back Log and What to Expect as We Enter 2021

- Issue 16: SBA Information Notice 12/08/2020 – Note Your Clients with These Loans will Be Receiving a Form 1099 Misc. – NOTE – Changes in the Law May Impact This Issue

- Issue 17: Deductible Livestock Costs for Adjusting 2020 Income Tax Returns

- Issue 18: Notice 2020-78 IRS Extends the Work Opportunity Tax Credit Certification Deadline

- Issue 19: Electronic §501(c)(4) Applications to be Filed Electronically

- Issue 20: New Form 7202 Credits for Sick Leave and Family Leave for Certain Self-Employed Individuals – Draft Issued

- Issue 21: Applicable Federal Rates (AFR) for January 2021 – Rev. Rul. 20

Issue 1: Update on PPP Loans

Expenses paid with forgiven PPP loan funds will be deductible for tax purposes.

- Tax Professionals will need to check with respective states and if they will couple

- Subsection (i) of §1106 of CARES Act is amended

- The Emergency Coronavirus Relief Act of 2020 makes adjustments under §1106 of CARES Act and provides that “no deduction shall be denied or reduced, no tax attribute shall be reduced, and no basis increase shall be denied, by reason of the exclusion from gross income provided by paragraph (1)” of the CARES Act.

Senate Finance Committee member John Cornyn R-Texas states “By clarifying that expenses paid with a forgiven PPP loan can still be deducted from small businesses’ taxes, we can help ensure small businesses won’t be hit with yet another hardship during an already difficult year.

Simplified / Streamline PPP Forgiveness for loans up to $150,000.

- Simplified procedure requiring no documentation to be submitted to bank.

- Just one-page application with attestation of compliance with program requirements.

- Borrowers required to retain relevant records for employment for 4 years and other for 3 years.

- Inclusion of demographic information is discretionary

- Lenders held harmless

More expenses are eligible for forgiveness: {60% payroll & 40% limits still apply}

- Software, HR, and various accounting operations

- Covered Worker protection

- Covered supplier costs

- Covered property damage costs not covered by insurance

PPP Second Round {PPP2}:

$284 Billion in new PPP Loans

Eligibility:

- Fewer than 300 employees.

- Must have reduction in quarterly gross revenues of at least 25% compared to same quarter in 2019.

- First, second, or third quarter of 2020

- Must have used or will use the full amount of their first PPP

- Company not traded on a nation exchange.

- 501(c)(6) are eligible, with exception of lobbying comprises more than 15% of receipts or activities.

- 60% payroll costs and 40% other still apply

- Final Forgiveness amount will NOT be reduced by EIDL grant monies received.

- Max Loan = 2.5 times average monthly payroll or $2 million, whichever less.

- Max Loan for industries assigned to NAICS code 72 (Accommodations and Food Services) = 3.5 times average monthly payroll

- Interest rate if not forgiven = 1% for 5 years

New EIDL Advances = max equal to $10,000

Following are the two Rev. Proc. we discussed at the year-end session, and no longer are applicable

Revenue Procedure 2020-51: This revenue procedure provides a safe harbor for certain Paycheck Protection Program loan participants, whose loan forgiveness has been partially or fully denied, or who decide to forego requesting loan forgiveness, to claim a deduction for certain otherwise deductible eligible payments on (1) the taxpayer’s timely filed, including extensions, original income tax return or information return, as applicable, for the 2020 taxable year, or (2) an amended return or an administrative adjustment request (AAR) under §6227 of the Internal Revenue Code (Code) for the 2020 taxable year, as applicable. For taxpayers that decide to forego requesting loan forgiveness, the safe also allows these taxpayer to claim a deduction for the otherwise deductible eligible payments on an original income tax return or information return, as applicable, for the taxable year in which the taxpayer decides to forego requesting forgiveness.

Revenue Ruling 2020-27: This revenue ruling provides guidance on whether a Paycheck Protection Program (PPP) loan participant that paid or incurred certain otherwise deductible expenses can deduct those expenses in the taxable year in which the expenses were paid or incurred if, at the end of such taxable year, the taxpayer reasonably expects to receive forgiveness of the covered loan. The revenue ruling also provides guidance if, as of the end of the 2020 taxable year, the PPP loan participant has not applied for forgiveness, but intends to apply in the next taxable year.

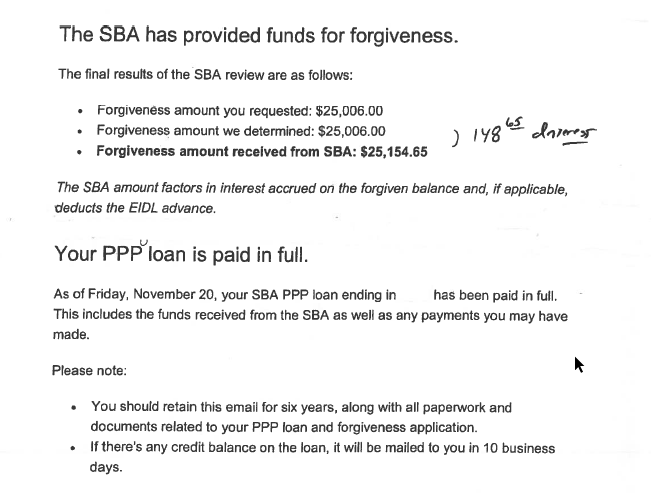

Sample of Forgiveness Letter

Regardless of the financial accounting classification, PPP loans are treated as debt for federal income tax purposes. The interest expense associated with the debt is deductible, similar to other types of debt.

If a PPP loan is forgiven, §1106(i) of the CARES Act specifically requires taxpayers to exclude canceled indebtedness from gross income and, accordingly, the debt forgiveness amount is nontaxable. Subsequent to the passage of the CARES Act, the IRS issued Notice 2020-32, which precludes a deduction for an expense that would otherwise be deductible if the payment results in the forgiveness of a loan, thereby preventing entities from claiming a double tax benefit on the qualifying expenses for PPP loans. However, there are indications that Congress may act to reverse the IRS Notice. Taxpayers will need to watch for guidance on this issue in any future stimulus packages enacted.

Issue 2: What’s New with 1099 Misc. and 1099 NEC?

1099-MISC Title Change

The title for Form 1099-MISC has been changed from Miscellaneous Income to Miscellaneous Information.

Form 1099-MISC, Box 1.

Box 11 includes any reporting under § 6050R, regarding cash payments for the purchase of fish for resale purposes, from an individual or corporation who is engaged in catching fish.

Form 1099-NEC, Box 1

Box 1 will not be used to report any items under §6050R with regards to buying fish for resale purposes.

Form 1099-NEC, Box 2

Payers may use box 2 on Form 1099-NEC or box 7 on Form 1099-MISC to report any sales totaling $5,000 or more of consumer products for resale, on buy-sell, deposit-commission, or any other basis.

Form 1099-NEC Resized

IRS has reduced the height of the form so it can accommodate 3 forms on a page.

Electronic Filing of Returns

The Taxpayer First Act of 2019, enacted July 1, 2019, authorized the Department of the Treasury and the IRS to issue regulations that reduce the 250-return requirement for 2021 tax returns. If those regulations are issued and effective for 2021 tax returns required to be filed in 2022, we will post an article at IRS.gov explaining the change.

Issue 3: Notice 2020-61 – Defined Benefit Plan Contributions Have Until January 4, 2021 to be Made

IRS will treat contribution to single employer defined benefit pension plan with extended due date of 1/1/2021 pursuant to § 3608(a)(1) of CARES Act as timely if it is made no later than 1/4/2021, first business day after 1/1/21.

This deferral allows employers to not make payment until 2021, which is in keeping with intent of CARES Act legislation to afford relief from having to make these payments in 2020.

Without deferral, some employers might make payment in 2020, last business day before 1/1/2021.

Issue 4: Dawson Pre-Launch – FAQ’s

- What is DAWSON?

The U.S. Tax Court’s new case management system, DAWSON (Docket Access Within a Secure Online Network), is an electronic filing and case management system designed to make it easier for parties and the Court to start a Tax Court case, file and process documents, and manage cases.

- How do You Access DAWSON?

In December, when the system “goes live”, you will be able to access DAWSON from the Court’s website.

- Will I Need Special Software to Access DAWSON?

No. DAWSON is web-based, so all you need is access to the internet and an internet browser.

- Is DAWSON Compatible with All Internet Browsers?

DAWSON is compatible with most up-to-date browsers such as Chrome, Edge, Firefox, or Safari. It is not compatible with outdated browsers such as Internet Explorer.

- Who Can Register for a DAWSON Account?

Only parties with active cases and counsel may register for a DAWSON account. The general public will be able to access the Court’s orders and opinions for free through the Court’s website without needing a DAWSON account.

- If I Already Have a DAWSON Account, Will I Need a New DAWSON Account?

Yes. Your eAccess credentials will not work in the new system. In early December, DAWSON credentials will be emailed to eAccess system users. To ensure that this email is sent to your current email address, make sure your contact information is accurate before November 20, 2020.

- If I Do Not Currently Have an eAccess Account, Will I Need a DAWSON Account?

If you are a party, you will need a DAWSON account for free electronic access to your Court records. If you do not have a DAWSON account, you will receive case documents from the Court by U.S. mail instead of being able to access them electronically. If you are admitted to practice before the Court, you are generally required to file documents and receive service electronically. See Rule 26(b), Tax Court Rules of Practice and Procedure. Electronic filing and the electronic service of Court filings will take place through a DAWSON account.

- If I Currently Have a PACER Account, Will I Need a DAWSON Account?

Yes. DAWSON is not connected to PACER.

- How DO I Get a DAWSON Account?

In early December, practitioners and parties registered in the current eAccess system will receive an email with a link to establish new credentials in DAWSON. Practitioners and parties who do not have an eAccess account before November 20, 2020, will be able to register in DAWSON after it becomes active in December. When electronically filing a new petition, unrepresented petitioners will register for an account in DAWSON. Current petitioners who do not have an eAccess account can establish new credentials by emailing [email protected].

The Court will provide newly admitted practitioners with DAWSON credentials when they are assigned a Tax Court Bar number. Current practitioners whose eAccess credentials are inaccessible or who do not timely activate their DAWSON credentials can establish new credentials by emailing [email protected].

- What Happens November 20, 2020?

Beginning, at 5:00 PM ET on November 20, 2020, the eAccess system will become “read only”. Records in the eAccess system—including opinions and orders—will remain visible to parties and the public but no new electronic case filings will be permitted.

- What if I Need to File Something After November 20, 2020 and Before DAWSON is Active?

If you must file something with the Court after 5:00 PM Eastern Time on November 20, 2020 and before DAWSON “goes live” in December, you can do so by mailing your document to the United States Tax Court, 400 2nd Street NW, Washington DC 20217.

- Will the Court Still Issue Opinions and Orders During the Time Electronic Filing is Inaccessible?

The Court does not currently anticipate issuing any orders or opinions from 5:00 PM Eastern Time on November 20, 2020, until DAWSON goes live. If circumstances necessitate issuing an opinion or order, the Court will do so.

- How Will I Know When DAWSON is Active?

Check the Court’s website for up-to-date information. The Court will announce the launch date by Press Release.

- Is There Any Guidance or Training on How to Use DAWSON?

The Court’s website has a demonstration video and other helpful information.

Issue 5: Nexus and State Guidance

Wisconsin

Wisconsin will not consider an out-of-state business to have nexus in Wisconsin if its only Wisconsin activity is having an employee working temporarily from the employee’s home during this national emergency (COVID-19).

For an employee who is a resident of Wisconsin and telecommutes for an out-of-state employer, the employee’s income would be sourced to Wisconsin.

Facts and Question 1: An individual is a Wisconsin resident (i.e., is domiciled in Wisconsin). The individual commutes daily to her job in another state. Is the income earned in the other state taxable to Wisconsin?

Answer 1: Yes, the income earned in the other state is taxable to Wisconsin. Section 71.04(1)(a), Wis. Stats., provides that all income or loss of resident individuals shall follow the residence of the individual.

If the individual is required to pay an income tax to the other state on the same income that is taxable to Wisconsin, the individual may be allowed a credit on the Wisconsin income tax return for tax paid to that other state.

Facts and Question 2: An individual is a resident of Minnesota. The individual performed services for a Wisconsin corporation during the entire calendar year. The individual received total compensation of $60,000. During this period of time, the individual telecommuted from his home office located in Minnesota for 230 business days. The individual worked at the employer’s Wisconsin site for 10 business days during the year. What amount of income earned by the individual is taxable to Wisconsin?

Answer 2: The individual’s total compensation for the year was $60,000 for 240 days (230 days in Minnesota and 10 days in Wisconsin). The compensation was $250 per day ($60,000 ÷ 240 = $250). Because the individual worked 10 days in Wisconsin, $2,500 ($250 x 10) is taxable to Wisconsin. Because the amount subject to Wisconsin income tax is more than $1,500, the employer must withhold Wisconsin income tax from the individual’s wages. The individual must file a nonresident Wisconsin income tax return (Form 1NPR) to report the $2,500 of income taxable to Wisconsin. The individual must also file a Minnesota income tax return to report the $60,000 to Minnesota. Minnesota may allow a credit for tax paid to Wisconsin.

Note: The answer would be different in these examples if the individual was a resident of a state with which Wisconsin has a reciprocity agreement. Under a reciprocity agreement, Wisconsin will not tax the wages of an individual who is a resident of the other state working in Wisconsin, and the other state will not tax the wages of a Wisconsin resident working in that other state. If, for example, the individual was a resident of Illinois instead of Minnesota, the wages earned in Wisconsin by the Illinois resident would not be taxable to Wisconsin. (Wisconsin formerly had a reciprocity agreement with Minnesota, but that agreement ended on January 1, 2010.)

Facts and Question 3: An individual is a resident of Wisconsin who generally works in Wisconsin. The individual’s employer temporarily assigns her to work in Minnesota for four months to complete a project. The individual continues to receive her pay from her Wisconsin employer. The individual earns $5,000 per month. How much of the individual’s income is taxable to Minnesota?

Answer 3: Because the individual performed four months of service in Minnesota, $20,000 ($5,000 x 4 months) of her compensation is sourced to Minnesota and taxable to Minnesota. The total income for the year, $60,000 ($5,000 x 12 months) is taxable to Wisconsin. The individual must file a nonresident income tax return in Minnesota to report the $20,000 taxable to Minnesota. The individual must also file a resident Wisconsin income tax return (Form 1) and report the $60,000 of income taxable to Wisconsin. The individual may be able to claim a credit on the Wisconsin return for tax paid to Minnesota.

Facts and Question 4: An individual is a resident of Minnesota and works for a Minnesota company. The individual has a second home in Wisconsin. The individual telecommutes from her second home on Fridays and then spends the weekend in Wisconsin. During the year, the individual works 52 Fridays in Wisconsin. Her total annual salary is $50,000. What portion of the individual’s income is taxable to Wisconsin?

Answer 4: $10,000. The individual works 1/5 of her total work time in Wisconsin ($50,000 ÷ 5 = $10,000). If the Minnesota company does business in Wisconsin (has nexus in Wisconsin) and is required to file a Wisconsin income or franchise tax return, the employer must withhold Wisconsin income tax from the Wisconsin wages as those wages are more than $1,500. If the Minnesota company does not have nexus in Wisconsin, the employer is not required to withhold Wisconsin income tax but may voluntarily register and withhold Wisconsin income tax. If the employer does not withhold Wisconsin tax, the individual may be required to make estimated payments of Wisconsin income tax if the individual expects to owe $200 or more with her Wisconsin income tax return.

In this case, as a nonresident of Wisconsin the individual is required to file a Wisconsin income tax return using Form 1NPR to report the income taxable to Wisconsin ($10,000). The individual is also required to file a Minnesota income tax return to report the Minnesota income ($50,000). Minnesota may allow a credit for the tax paid to Wisconsin.

Facts and Question 5: An individual is a resident of Wisconsin and works for a Wisconsin company. The individual has a second home in Minnesota. The individual telecommutes from her second home in Minnesota on Fridays. During the year, the individual works 52 Fridays in Wisconsin. Her total annual salary is $50,000. What portion of the individual’s income is taxable to Wisconsin?

Answer 5: $50,000. All income earned by a Wisconsin resident is taxable to Wisconsin. The individual works 1/5 of her total work time in Minnesota. Thus $10,000 ($50,000 ÷ 5 = $10,000) is also taxable to Minnesota.

Facts and Question 6: In the previous questions and answers, it is assumed the individual earns the income evenly throughout the year. What happens if income is not earned evenly throughout the year?

Answer 6: If income is not earned evenly throughout the year, the amount of income taxable to a state may have to be determined on a monthly, weekly, or hourly basis.

For example, a Minnesota resident earned $54,000 during the year. He was paid $4,000 a month for the first six months of the year and $5,000 a month for the last six months. The individual was required to work five months of the year in Wisconsin. During the first month he worked in Wisconsin, the individual was paid at the rate of $4,000 per month. He was paid $5,000 per month for the remaining four months he worked in Wisconsin. The amount of income taxable to Wisconsin is $24,000 (1-month x $4,000 + 4 months x $5,000).

Iowa – The State will not assert Nexus

Illinois – No specific guidance.

Minnesota – The Minnesota Department of Revenue will not seek to establish nexus for business income tax purposes solely because an employee is temporarily working from home due to the COVID-19 pandemic.

Missouri – No specific guidance issued.

Issue 6: Common Error to Avoid When Claiming Employer Tax Credits

Employers who are filing Form 941, Employer’s Quarterly Federal Tax Return and claiming an employer tax credit should read the instructions carefully and take their time when completing the form to avoid mistakes.

- Using a reputable tax preparer including certified public accountants, enrolled agents or other knowledgeable tax professionals

- Mistakes can result in a processing delay or a balance due notice, which could mean a delay or require filing an amended return

- Common mistakes to avoid when completing Form 941

- Reporting advances requested instead of the advance payments of credits received

- Incorrectly reconciling the advance payment of the credit requested and received

- Requirements when using third-party payers or reporting agents

- What third-party payers and reporting agents should also ask employers

Issue 7: REG-123652-18 – Treatment of Special Enforcement Matters

This document contains proposed regulations to except certain partnership-related items from the centralized partnership audit regime that was created by the Bipartisan Budget Act of 2015 and sets forth alternative rules that will apply. The centralized partnership audit regime does not apply to a partnership-related item if the item involves a special enforcement matter described in these regulations.

Additionally, these regulations propose changes to the regulations to account for changes to the Internal Revenue Code (Code). Finally, these proposed regulations also make related and clarifying amendments to the final regulations under the centralized partnership audit regime. The proposed regulations would affect partnerships and partners to whom special enforcement matters apply.

These regulations also propose several changes to regulations finalized in TD 9844 to provide clarity regarding certain provisions. Changes are required to the regulations finalized in TD 9844 to address the treatment of chapter 1 taxes, penalties,

additions to tax, additional amounts, and any imputed underpayments previously reported by the partnership adjusted as part of an examination under the centralized partnership audit regime to correspond to the addition of proposed §301.6241-7(g), which is discussed in part 5.F of this Explanations of Provisions. Additional edits are proposed to modify the rules implementing section 6241(7) regarding the treatment of

adjustments when a partnership ceases to exist to account for the addition of section 6232(f) to the Code. Finally, minor clarifying edits are proposed. In addition to the changes listed above, certain regulations have been reordered or renumbered, typographical errors have been corrected, and non-substantive editorial changes have been made.

- 301.6221(b)-1 Election out for certain partnerships with 100 or fewer partners

- 301.6225-1 Partnership adjustment by the Internal Revenue Service.

- 301.6225-2 Modification of imputed underpayment.

- 301.6225-3 Treatment of partnership adjustments that do not result in an imputed underpayment.

- 301.6226-2 Statements furnished to partners and filed with the IRS.

- 301.6241-3 Treatment where a partnership ceases to exist.

- 301.6241-7 Treatment of special enforcement matters.

Issue 8: Changes to Form 1065 for 2020 (Draft NOT Final)

Form 1065 is an information return used to report the income, gains, losses, deductions, credits, and other information from the operation of a partnership.

The revised instructions indicate that partnerships filing Form 1065 for tax year 2020 are to calculate partner capital accounts using the transactional approach for the tax basis method. Under the tax basis method outlined in the instructions, partnerships report partner contributions, the partner’s share of partnership net income or loss, withdrawals and distributions, and other increases or decreases using tax basis principles as opposed to reporting using other methods such as GAAP.

The Modified Outside Basis Method.

The Modified Previously Taxed Capital Method, or

The §704(b) Method, as described in the instructions, including special rules for publicly traded partnerships.

Other Changes

Page 1: Changes Related to the COVID Provisions

Line 7, Other income

Requires the amount of payroll tax credit taken by an employer for qualified paid sick leave and qualified paid family leave under §§7001 and 7003 of the Families First Coronavirus Response Act. It will be shown on Line 7 as additional income.

In addition, Line 7 also requires that the amount of self-employment tax credit taken by self-employed individuals for qualified sick leave equivalent and/or qualified family leave equivalent under §§7002 and 7004 of the Families First Coronavirus Response Act be included as additional income.

Line 15 has been changed to reflect the COVID-related legislative changes to the business interest deduction under §163(j).

Business interest expense is generally limited to the sum of business interest income, 30% of the adjusted taxable income, and floor plan financing interest.

The CARES Act retroactively increases the amount of business interest expense that may be deducted for tax years beginning in 2019 and 2020 by computing the §163(j) limitation using 50% of the adjusted taxable income (ATI) instead of 30%. Review Form 8990, Limitation on Business Interest Expense Under § 163(j). Business interest expense includes any interest expense properly allocable to a trade or business.

Page 3: Schedule B Question 27

The instruction to this question, about foreign partners being subject to §864(c)(8) as a result of their transfers of their partnership interest or receiving distributions, has been updated to reflect T.D. 9919.

Provide the number of foreign partners subject to §864(c)(8) as a result of transferring all or a portion of an interest in the partnership if the partnership is engaged in a U.S. trade or business.

- 864(c)(8) provides that gain or loss of a foreign transferor from the transfer of a partnership interest is treated as effectively connected with the conduct of a trade or business within the United States to the extent that the transferor would have had effectively connected gain or loss if the partnership sold all of its assets at fair market value on the date of transfer.

For purposes of §864(c)(8), a transfer of a partnership interest means a sale, exchange, or other disposition, and includes a distribution from a partnership to a partner to the extent that gain or loss is recognized on the distribution, as well as a transfer treated as a sale or exchange under §707(a)(2)(B).

- 864(c)(8) is applicable to transfers in which a foreign transferor transfers all or part of its interest in a partnership. It also applies to a foreign partner in a partnership that directly or indirectly transfers an interest in a partnership that engaged in a U.S. trade or business. If the partnership is a publicly traded partnership as defined in §469(k)(2) and has properly answered yes to question 5 on Form 1065, Schedule B, then it is not required to provide the information requested in Question 27 on Form 1065, Schedule B, relating to foreign partners.

Schedule B, Question 29

A new question was added regarding a foreign corporation’s direct or indirect acquisition of substantially all of the properties constituting a trade or business of the partnership.

Schedule K. Partners’ Distributive Share items.

Charitable contributions, Line 13a. These instructions have been amended to reflect COVID-related legislation, e.g., the ability to deduct certain cash contributions in amounts up to 100% of AGI.

Other credits, Line 15f. The employee retention credit and the employer credit for paid family and medical leave were not mentioned in the original version of the 2019 instructions but were added in the revised version of those instructions which were issued in the spring of 2020. They are again mentioned in the 2020 instructions as credits to be listed here.

Codes for Schedules K and K-1. Complete descriptions of codes for Schedules K and K-1 are provided in the Form 1065 instructions at “Specific Instructions (Schedules K and K-1, Part III, Except as Noted).” The codes are no longer listed on page 2 of Schedule K-1 (Form 1065).

Schedule L. Balance Sheets per Books

There is no longer a requirement to reconcile Schedule L to Schedule M-2 unless Schedule L is reported on a tax basis.

Additions to the Instructions, that don’t apply to a single line on the form. The instructions contain the following additions that do not refer to a single line on the form:

…Related-party payments to certain hybrid entities

…Disregarded entity and §743(b) Reporting

…Revocation of a §754 election using new Form 15254

…Technical terminations and §708 relating to the continuation of a partnership

…Substantial built-in loss rules for §743

…Additional instructions with respect to partnership audit procedures and administrative adjustment requests under the Bipartisan Budget Act of 2015

Issue 9: Remember February 1, 2021 Deadline for Form W-2, Other Wage statements

A 2015 law made it a permanent requirement that employers file copies of their Form W-2, Wage and Tax Statements, and Form W-3, Transmittal of Wage and Tax Statements, with the Social Security Administration by January 31. That is also the date the Forms W-2 are due to workers. This upcoming tax season, however, January 31 falls on a Sunday, pushing the due dates to the next business day, which is Monday, February 1.

Certain Forms 1099-MISC, Miscellaneous Income and Forms 1099-NEC, Nonemployee Compensation, are also normally due to taxpayers on January 31, but this tax season they too will be due on the next business day, February 1, 2021.

Issue 10: IRS to Increase Focus on Tax Return Preparers Who Have Not Filed Their Own Returns

The IRS will step up revenue officer contacts focused on tax return preparers who in prior years have failed to timely file one or more of their own tax returns. The purpose of these contacts is to remind tax return preparers of their own tax filing and paying obligations and bring them into compliance. As noted in a recent report by the Treasury Inspector General for Tax Administration:

When preparers cannot manage their own tax affairs, or worse, if they intentionally claim credits and deductions to which they are not entitled, they could undermine the tax administration system.*

These contacts will generally be conducted by telephone because the safety of IRS employees and the public remains a top priority for the IRS. Unlike face-to-face contacts, which are generally unannounced, these tax preparers will receive a letter from the revenue officer scheduling the contact.

IRS revenue officers will share information with tax return preparers about their tax filing and paying obligations and the consequences of failing to meet those obligations. For those tax return preparers who owe, revenue officers will identify appropriate ways to resolve their tax compliance issues.

Issue 11: Updated Information Concerning PPP Loans and Eligibility for the Employee Retention in Special Situations

- How is eligibility for the employee retention credit affected if an employer (Acquiring Employer) acquires the stock or other equity interests of an entity (Target Employer) that had received a PPP loan and, under the aggregation rules, the employers are treated as a single employer (Aggregated Employer Group) as a result of the transaction?

- If the Target Employer had received a PPP loan, but prior to the transaction closing date, the Target Employer fully satisfied the PPP loan, or submitted a forgiveness application to the PPP lender and established an interest-bearing escrow account in accordance with Small Business Administration (SBA) rules, then, after the closing date, the Aggregated Employer Group will not be treated as having received a PPP loan, provided that the Acquiring Employer (including any member of the Acquiring Employer’s pre-transaction Aggregated Employer Group) had not received a PPP loan before the closing date and no member of the Aggregated Employer Group receives a PPP loan on or after the closing date.

In this case, any employer that is a member of the Aggregated Employer Group, including the Target Employer, may claim the employee retention credit for qualified wages paid on and after the closing date, provided that the Aggregated Employer Group otherwise meets the requirements to claim the employee retention credit.

In addition, any employee retention credit claimed by the Acquiring Employer’s pre-transaction Aggregated Employer Group for qualified wages paid before the closing date will not be subject to recapture.

If the Target Employer had received a PPP loan, but prior to the transaction closing date, the PPP Loan is not fully satisfied and no escrow account was established in accordance with SBA rules, then, after the closing date, the Aggregated Employer Group (other than the Target Employer) will not be treated as having received a PPP loan, provided that the Acquiring Employer (including any member of the Acquiring Employer’s pre-transaction Aggregated Employer Group) had not received a PPP loan before the closing date and no member of the Aggregated Employer Group receives a PPP loan on or after the closing date.

Any employer (other than the Target Employer) that is a member of the Aggregated Employer Group may claim the employee retention credit for qualified wages paid on and after the closing date, provided that the Aggregated Employer Group otherwise meets the requirements to claim the employee retention credit.

In addition, any employee retention credit claimed by the Acquiring Employer’s pre-transaction Aggregated Employer Group for qualified wages paid before the closing date will not be subject to recapture. However, the Target Employer that received the PPP loan prior to the transaction closing date and that continues to be obligated on the PPP loan after the closing date is ineligible for the employee retention credit for any wages paid to any employee of the Target Employer before or after the closing date.

- How is eligibility for the employee retention credit affected if an Acquiring Employer acquires the assets of a Target Employer that received a PPP loan?

- An Acquiring Employer that acquires the assets of a Target Employer that had received a PPP loan will not be treated as having received a PPP loan by virtue of the asset acquisition, provided that the Acquiring Employer does not assume the Target Employer’s obligations under the PPP loan. In this case, the Acquiring Employer will be eligible for the employee retention credit after the transaction closing date if the employer otherwise meets the requirements to claim the credit. In addition, any employee retention credit claimed by the Acquiring Employer for qualified wages paid before the closing date will not be subject to recapture.

If, as part of the acquisition of the Target Employer’s assets and liabilities, the Acquiring Employer assumes the Target Employer’s obligations under the PPP loan, then after the transaction closing date, the Acquiring Employer generally will not be treated as having received a PPP loan, provided that the Acquiring Employer had not received a PPP loan before or on or after the closing date; however, the wages that may be treated as qualified wages after the closing date will be limited.

Specifically, the wages paid by the Acquiring Employer after the closing date to any individual who was employed by the Target Employer on the closing date shall not be treated as qualified wages. Subject to this limitation, the Acquiring Employer may claim the employee retention credit for qualified wages paid on and after the closing date, provided that the employer otherwise meets the requirements to claim the employee retention credit.

In addition, any employee retention credit claimed by the Acquiring Employer for qualified wages paid before the closing date will not be subject to recapture.

Issue 12: 2021 Online Tax Preparation Products to Offer Multi-factor Authentication for Taxpayers, Tax Pros

Designed to protect both taxpayers and tax professionals, multi-factor authentication means the returning user must enter two pieces of data to securely access an account or application. For example, taxpayers must enter their credentials (username and password) plus a numerical code sent as a text to their mobile phone.

Some online products previously offered multi-factor authentication. However, for 2021 all providers agreed to make it a standard feature and all agreed that it would meet requirements set by the National Institute of Standards and Technology. Multi-factor authentication may not be available on over-the-counter hard disk tax products.

Because the multi-factor authentication option is voluntary, Summit partners urged both taxpayers and tax professionals to use it. Multi-factor authentication can reduce the likelihood of identity theft by making it difficult for thieves to get access to sensitive accounts.

Users should check the security section in their online tax product account to make the change. It may be labeled as two-factor authentication or two-step verification or similar names.

Use of multi-factor authentication is especially important for tax professionals who continue to be prime targets of identity thieves. Of the numerous data thefts reported to the IRS from tax professional offices this year, most could have been avoided had the practitioner used multi-factor authentication to protect tax software accounts.

There are multiple options for multi-factor authentication. For example, taxpayers and tax practitioners can download an authentication app to their mobile device. These apps are readily available through Google Play or Apple’s App Store. Once properly configured, these apps will generate a temporary, single-use security code, which the user must enter into their tax software to complete authentication. Use a search engine for “Authentication apps” to learn more.

Other options include codes that may be sent to practitioner’s email or mobile phone via text but those are not as secure as an authentication app.

While no product is fool-proof, multi-factor authentication does dramatically reduce the likelihood that taxpayers or tax practitioners will become victims. Multi-factor authentication should be used wherever it is offered. For example, financial accounts, social media accounts, cloud storage accounts and popular email providers all offer multi-factor authentication options.

Issue 13: Form 7200 IRS Delay in Payments

Employers will experience a delay in receiving payments associated with Form 7200, Advance Payment of Employer Credits, processed between late-December and mid-January due to standard end-of-year close out. The IRS will continue to accept and process valid Forms 7200 during this time, and the payment of valid requests during this time will begin to be processed on January 21, 2021. Employers will still receive Letter 6312, Form 7200 Response, if the Form 7200 cannot be processed.

Issue 14: IRS Updates FAQ’s for COVID-19 Tax Credits for The Families First Coronavirus Response Act

Can an employee receive both “qualified sick leave wages” and “qualified family leave wages?”

Yes, but at different times. Qualified sick leave wages are available for up to 80 hours during which an employee cannot work or telework for any of six reasons related to COVID-19, including because the employee must care their child whose school or place of care is closed, or whose childcare provider is unavailable, for reasons related to COVID-19. By contrast, qualified family leave wages are available only because the employee must care for his or her child whose school or place of care is closed, or whose childcare provider is unavailable, for reasons related to COVID-19, and only after an employee has been unable to work or telework for this reason for 80 hours.

Who is an eligible self-employed individual for purposes of the qualified sick leave credit and the qualified family leave credit?

An eligible self-employed individual is an individual who regularly carries on any trade or business and would be entitled to receive qualified sick leave wages or qualified family leave wages under the FFCRA if the individual were an employee of an Eligible Employer. Eligible self-employed individuals are allowed an income tax credit to offset their federal self-employment tax for any tax year equal to their “qualified sick leave equivalent amount” or “qualified family leave equivalent amount.”

Can a self-employed individual receive both qualified sick or family leave wages and qualified sick or family leave equivalent amounts?

Yes, but the qualified sick or family leave equivalent amounts are offset by the qualified sick or family leave wages. So, if a self-employed individual is entitled to a refundable credit for a qualified sick leave equivalent amount the FFCRA, and also receives qualified sick leave wages as an employee, the FFCRA reduces the qualified sick leave equivalent amount for which the self-employed individual may claim a tax credit to the extent that the sum of the qualified sick leave equivalent amount described in the FFCRA and any qualified sick leave wages, exceeds $2,000 (or $5,110 in the case of any day any portion of which is paid sick time as described in paragraph (1), (2), or (3) the EPSLA).

Similarly, if a self-employed individual is entitled to a refundable credit for a qualified family leave equivalent amount, and also receives qualified family leave wages as an employee under the Emergency Family and Medical Leave Expansion Act (EFMLEA), the FFCRA reduces the qualified family leave equivalent amount for which the self-employed individual may claim a tax credit to the extent that the sum of the qualified family leave equivalent amount and the qualified family leave wages, exceeds $10,000.

How does a self-employed individual determine the sick and family leave equivalent tax credit that they may claim?

A self-employed individual will determine the sick and family leave equivalent tax credit to which he or she is entitled by completing Form 7202, Credits for Sick Leave and Family Leave for Certain Self-Employed Individuals. To complete the Form 7202, self-employed individuals who are also employees will need any amount of qualified sick and family leave wages that their employers reported on their Forms W-2, Wage and Tax Statement. For more information on the requirement for Eligible Employers to report the amount of qualified sick and family leave wages paid to employees on Form W-2, review Notice 2020-54, 2020-31 IRB 226.

How can a self-employed individual cover their qualified sick leave equivalent and qualified paid family leave equivalent amounts before filing their Form 1040?

The self-employed individual may cover sick leave and family leave equivalents by taking into account the credit to which the individual is entitled and will claim on Form 1040, U.S. Individual Income Tax Return, in determining required estimated tax payments. This means that a self-employed individual can effectively reduce payments of estimated income taxes that the individual would otherwise be required to make if the individual was not entitled to the credit on the Form 1040.

The Coronavirus Aid, Relief, and Economic Security Act (PL 116-136; “CARES Act”) provides that self-employed individuals may defer the payment of 50% of the social security tax imposed on net earnings from self-employment income for the period beginning on March 27, 2020 and ending December 31, 2020. Self-employed individuals may defer these taxes in addition to the credits for qualified sick leave equivalent amounts or qualified family leave equivalent amounts. Accordingly, if the self-employed individual is eligible for these credits, the individual should take into account these credits in addition to any amount of self-employment tax the individual plans to defer under the CARES Act in determining required estimated tax payments.

Can an independent contractor who generally performs services for multiple clients as a nonemployee claim the tax credit with regard to the lost services due to COVID-19?

Yes. If an individual is an independent contractor who generally performs services for multiple clients as a nonemployee, he or she is self-employed and is eligible for the tax credits for days he or she is not able to work or telework for reasons related to COVID-19.

Does an eligible self-employed individual who is allowed a credit under the FFCRA for the qualified sick leave equivalent amount or a credit for the qualified family leave equivalent amount include any amount of these credits in gross income?

No, the amount of the credits allowed under FFCRA §7002 and FFCRA §7004 are not included in the gross income of the eligible self-employed individual.

- How should a self-employed employer substantiate eligibility for tax credits for qualified leave wage equivalents?

Self-employed individuals should maintain documentation establishing their eligibility for the credits as a self-employed individual. That documentation should be similar to the documentation maintained by employers claiming the credits for qualified leave wages under FFCRA.

Issue 15: IRS Mail Back Log and What to Expect as We Enter 2021

The IRS has made significant progress opening backlogged mail. As of November 24, 2020, IRS had 7.1 million unprocessed individual tax returns and 2.3 million unprocessed business returns, the IRS expects to issue all refunds for 2019 individual tax returns in 2020 where there are no issues with the return.

For refunds that cannot be issued in 2020 because the tax return is being corrected, reviewed or awaiting correspondence from a taxpayer, the refund will be issued as a paper check in 2021 per our normal processes.

Clients should continue to check Where’s My Refund for their personalized refund status.

How long you may have to wait:

It depends on where they sent the tax return and where it is in the process. In some locations, IRS is caught up or almost caught up. In other locations they are processing returns received over the summer due to the extended July 15 tax filing due date and, in some cases, are processing tax returns dated as early as April 15, 2020. However, they are rerouting tax returns and taxpayer correspondence from locations that are behind to locations where more staff is available and are taking other actions to reduce this backlog. Tax returns are opened in the order it is received. As the return is processed, it may be delayed because it has a mistake, is missing information, or there is suspected identity theft or fraud. If they can fix it without contacting the client, they will. If they need more information or need the client to verify that it was the client who sent the tax return, they will write the client a letter. The resolution of these issues depends on how quickly and accurately the client responds, and the IRS staff trained and working under social distancing requirements to complete the processing of the return.

What should the client do?

Unfortunately, other than responding to any requests for information promptly, there’s no action clients can take. IRS is working hard to get through the backlog. They ask that individuals not file a second tax return or contact the IRS about the status of the return.

Received a Bill or Notice (updated December 1, 2020)

Because of the COVID-19 shutdown, IRS experienced a backlog in mailing notices. To save time and money, they did not generate new ones and many notices were mailed with past due payment or response dates. IRS included a Notice 1052, Important! You Have More Time to Make Your Payment, as an insert.

The insert provided new or updated pay or response dates. Due to an error, some notices were sent without the insert. If your client is among those who did not get the Notice 1052, they were sent a Letter 544 on August 7, 2020, with the appropriate information.

What they should do?

The letter explains why the notice was delayed and provides a new date to pay or respond. If the client received the notice, they should:

- Review the last page of the insert to determine if there is a new due date.

- Do nothing with the notice if they have already taken steps to resolve the issue.

- Contact IRS using the phone number on the notice if they have questions.

- Keep in mind that phone lines are extremely busy as the IRS resumes operations.

- If the notice was about a balance due and they are unable to pay, consider payment options to avoid getting additional penalties and interest.

IRS is now sending 500 series balance due notices:

Although the IRS continued to issue most agency notices, the 500 series were suspended temporarily due to COVID-19. Some taxpayers have started to receive the updated 500 series notices with current issuance and payment dates. The 500 series includes three different types of notices that alert taxpayers about varying stages of nonpayment — the CP501, the CP503 and the CP504.

Taxpayers who are unable to pay are encouraged to consider available payment options as penalties and interest continue to accrue. Taxpayers in this situation are particularly encouraged to first review the Online Payment Agreement tool, which offers an easy way to set up a payment plan.

Penalty relief due to reasonable cause:

If the client was affected by the pandemic or other circumstances, IRS may be able to remove or reduce some penalties due to reasonable cause, but only if the client tried to comply with the tax law but were unable to due to facts and circumstances beyond their control. If this applies to them have the necessary documentation to support the claim, call the toll-free number on the notice to request penalty relief due to reasonable cause.

Answered a Letter or Notice (updated December 1, 2020)

IRS is getting mail, but it’s taking them longer to process it. How long may the client have to wait: IRS is processing all responses in the order we received them and are opening mail within 40 days of arrival. The current delay for IRS to process these responses is more than 60 days. The exact timeframe varies depending on the type of issue. IRS is sending replies to letters and notices across IRS sites where they have more staff and taking other actions to reduce this backlog.

What the client should do?

Once the client has answered the notice, they do not need to answer it again. IRS is working through all taxpayer replies on a first-come, first-served basis and will process the reply as of the date it was received.

Sent a Missing Form or Document (updated December 1, 2020)

There is a high volume of tax returns with missing schedules needed to claim or reconcile credits. IRS is getting mail, but it’s taking them longer to process it. They are processing all responses in the order we received them. The current delay is more than 60 days. If the client has provided the information, no further action is needed. IRS is working through all taxpayer replies on a first-come, first-served basis.

Sent IRS a Check (updated December 1, 2020)

If the client mailed IRS a check, it may be in the backlog of unopened mail. IRS is opening mail as quickly as possible and expect to process any checks within 60 days of its arrival. They will apply the payment on the date received, not the date they processed it. To avoid penalties for a late payment:

- Do not cancel the check.

- Make sure funds available to cover it.

- They are forgiving Dishonored Check Penalties if the check doesn’t clear because of processing delays.

This applies to payments we received starting March 1, 2020 and may extend through December 31, 2020. Interest and other types of penalties may still apply.

Sent a Third-Party Authorization or Power of Attorney Form (updated December 1, 2020)

Due to site closures relating to COVID-19, IRS currently taking longer than 3-4 weeks for approval. The current timeframe for approval is approximately 25 business days. They expect to have full staffing in place soon and reduce the wait time. Please consider the additional approval time and plan for it. Do not submit duplicate authorizations. Duplicate filings will only cause more delays. They working on a solution to accept Forms 8821 and 2848 with electronic signature images by early 2021.

Received a Failure to Deposit Penalty as an Employer (updated December 1, 2020)

If the client was an employer who reduced their tax deposits because they planned to claim the sick and family leave credits, or employee retention credit in the second quarter of 2020, they may have received a notice stating there was a Failure to Deposit Penalty for Form 941. Why they received this: When they reported the schedule of liabilities on Form 941, the liabilities did not match the reduction in deposits for every pay date. When this happened, they received a Failure to Deposit Penalty on the difference.

Issue 16: SBA Information Notice 12/08/2020 – Note Your Clients with These Loans will Be Receiving a Form 1099 Misc. – NOTE – Changes in the Law May Impact This Issue, we are still studying the bill.

In April 2020, SBA began making payments under §1112 of the CARES Act to cover, for a 6-month period, the principal, interest, and any associated fees that small businesses owe on 7(a), 504, and Microloans (“Section 1112 payments”). These §1112 payments relieve the small businesses of the obligation to pay that amount. SBA is providing the following information to 7(a) Lenders, Microloan Intermediaries, and Certified Development Companies with respect to information reporting issues arising from the §1112 payments:

Q: Who is responsible for filing Form 1099-MISC, Miscellaneous Income, with the IRS and furnishing Form 1099-MISC, Miscellaneous Income, to the small businesses for the Section 1112 payments?

- In accordance with §6041 of the Internal Revenue Code (“Code”) and the regulations thereunder, the following are responsible for issuing the Form 1099- MISC with respect to the §1112 payments:

- 7(a) Lenders are responsible for issuing the Form 1099-MISC for:

- (1) loans that have not been purchased by SBA, and

- (2) loans that have been purchased by SBA and are serviced by the 7(a) Lender.

- SBA is responsible for issuing the Form 1099-MISC for 7(a) loans that have been purchased, and are serviced, by SBA.

- Microloan Intermediaries are responsible for issuing the Form 1099-MISC for the Microloans serviced by the Intermediaries. SBA is responsible for issuing the Form 1099-MISC for the Microloans that are serviced by SBA.

- SBA is responsible for issuing the Form 1099-MISC for all 504 loans.

Lenders and Microloan Intermediaries should refer to the Instructions for Form 1099- MISC and the General Instructions for Certain Information Returns for more information about filing and furnishing the forms, including requirements to file electronically.

Microloan Intermediaries and 7(a) Lenders should contact IRS’s Stakeholder Liaison Local Contacts at https://www.irs.gov/businesses/small-businesses-self-employed/stakeholder-liaison-local-contacts (link provided to SBA by the U.S. Department of the Treasury) with any questions concerning the information reporting of the §1112 payments.

Q: What must be reported as income on the Form 1099-MISC?

- The total amount of the §1112 payments must be reported as income to the Borrower, including the principal, interest and any fees that were included in the §1112 payments. This total amount should be included in Box 3 of Form 1099-MISC.

Q: For the 7(a) Lenders and Microloan Intermediaries who are responsible for issuing the Form 1099-MISC, who should be identified as the “PAYER” and “RECIPIENT” in Form 1099-MISC?

- The 7(a) Lender and Microloan Intermediary should be identified as the PAYER in the “Payer” box in Form 1099-MISC, with its name, street address, city or town, state or province, country, ZIP code, and telephone number. The Borrower of the 7(a) loan or the Microloan should be listed as the “RECIPIENT” in Form 1099-MISC.

Q: With respect to Form 1098, Mortgage Interest Statement, should the form include the amount of interest that was paid on the loan by the §1112 payments?

- In accordance with §6050H of the Code and the regulations thereunder, the amount of interest paid on the loan by the § 1112 payments should be reported to the IRS, and furnished to small businesses, on Form 1098, Mortgage Interest Statement.

Questions

Questions on this Notice may be directed to the Lender Relations Specialists in the local SBA Field office. The local SBA Field office may be found at https://www.sba.gov/tools/local-assistance/districtoffices.

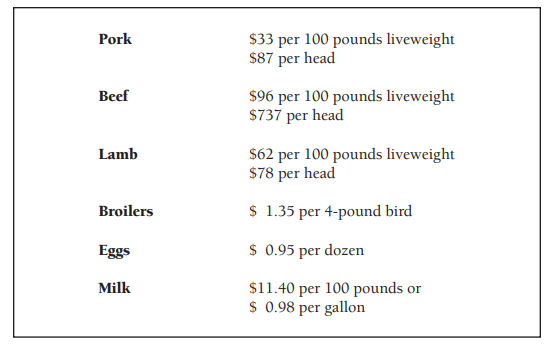

Issue 17: Deductible Livestock Costs for Adjusting 2020 Income Tax Returns

Estimated deductible costs of production for use in adjusting farm expenses to exclude the cost of producing home-consumed farm produce. The costs below include all cash costs, depreciation, and deductible production costs of home-raised feed. No charge is made for the farm operator’s labor. If hired labor or purchased grain and roughages are used to produce these products, or if high interest costs are incurred, the costs should be increased accordingly. In arriving at production costs, it was assumed that the young animals were raised and fed.

Issue 18: Notice 2020-78 IRS Extends the Work Opportunity Tax Credit Certification Deadline

Because the Taxpayer Certainty and Disaster Relief Act, extended the WOTC through December 31, 2020, and retroactively extended the period for which an empowerment zone designation is in effect under § 1391(d)(1) from December 31, 2017, to December 31, 2020, employers need additional time to comply with the DLA certification requirements of § 51(d)(13)(A)(ii).

The Treasury Department and the IRS understand that, due to the expiration of empowerment zone designations at the end of 2017 and the uncertainty of whether empowerment zone designations would be extended, some employers that hired members of targeted groups described in § 51(d)(5) and (7) may not have submitted Form 8850 to the DLA within 28 days of the individual beginning work. To be eligible for the relief provided by this notice, an employer that did not submit Form 8850 to the DLA within 28 days of an individual beginning work must submit the completed Form 8850 to the DLA by the date set forth in section IV.A of this notice.

In addition, the Treasury Department and the IRS are aware that some employers that hired members of targeted groups described in § 51(d)(5) and (7) may have submitted Form 8850 to the DLA within 28 days of an individual beginning work, regardless of the expiration of the empowerment zone designations. To be eligible for the relief provided by this notice, an employer that submitted Form 8850 to the DLA and subsequently received a denial letter from the DLA by reason of the expiration of the empowerment zone designations must re-submit the completed Form 8850 by the date set forth in section IV.A of this notice. In the event that an employer submitted Form 8850 to the DLA and was not issued a denial letter by the DLA, the employer does not need to re-submit Form 8850 to be eligible for the relief provided in this notice.

An employer that hired an individual who is a designated community resident described in § 51(d)(5), or a qualified summer youth employee described in § 51(d)(7), and who began work for that employer on or after January 1, 2018, and before January 1, 2021, will be considered to have satisfied the requirements of § 51(d)(13)(A)(ii), whether or not the employer submitted the completed Form 8850 to the DLA within 28 days of the individual beginning work for the employer, if the employer submits the completed Form 8850 to the DLA to request certification no later than January 28, 2021.

In the event that an employer submitted Form 8850 to the DLA and was not issued a denial notification by the DLA, the employer does not need to re-submit Form 8850.

Application of 28-day requirement to individuals hired on or after January 1, 2021.

An employer that hires a member of a targeted group described in § 51(d)(5) or (7), who begins work for the employer on or after January 1, 2021, is not eligible for the transition relief described in this notice with respect to that new employee.

Issue 19: Electronic §501(c)(4) Applications to be Filed Electronically

Organizations that choose to apply for recognition of exempt status under Internal Revenue Code (IRC) §501(a) as an organization described in §501(c)(4) should use the new Form 1024-A, Application for Recognition of Exemption under §501(c)(4) of the Internal Revenue Code.

Form 1024-A Application for Recognition of Exemption Under Section 501(c)(4) is being updated to allow electronic filing.

Organizations seeking recognition of exempt status under Section 501(a) as an organization described in Section 501(c)(2), (5), (6), (7), (8), (9), (10), (12), (13), (15), (17), (19) or (25) will continue to use Form 1024, Application for Recognition of Exemption Under Section 501(a).

Form 1024-A does not satisfy an organization’s separate requirement to notify the IRS that it’s operating under Section 501(c)(4). Instead, use Form 8976, Notice of Intent to Operate Under Section 501(c)(4).

Issue 20: New Form 7202 Credits for Sick Leave and Family Leave for Certain Self-Employed Individuals – Draft Issued

The Families First Coronavirus Response Act (FFCRA), enacted on March 18, 2020, is intended to help the United States combat coronavirus by requiring certain businesses to provide paid leave to workers who are unable to work or telework due to circumstances related to the coronavirus, and it offsets the costs of providing the leave with refundable tax credits against employment tax.

FFCRA extends equivalent credits to self-employed individuals.

Use Form 7202 to figure the amount of credit to claim for qualified sick and family leave credits under FFCRA on the 2020 tax return. These credits are available to eligible self-employed individuals if they were unable to work or had to care for family members for reasons related to the coronavirus and are refundable. These credits are equivalent to the amount of paid sick or family leave the self-employed individual would be entitled to receive under the Emergency Paid Sick Leave Act or the Emergency Family and Medical Leave Expansion Act, two separate provisions of the FFCRA, if the individual were an employee of an employer (other than himself or herself). Attach Form 7202 to the tax return.

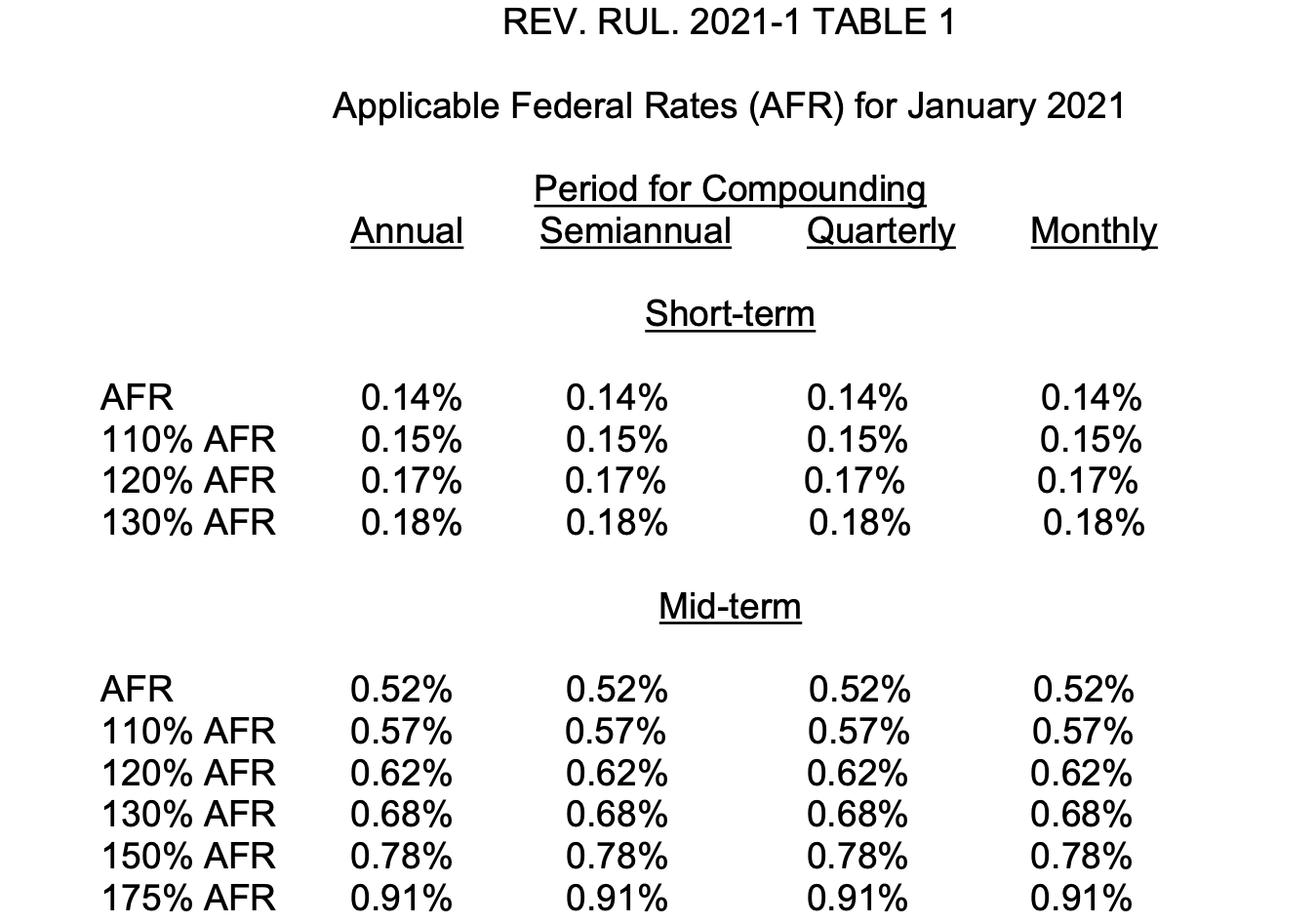

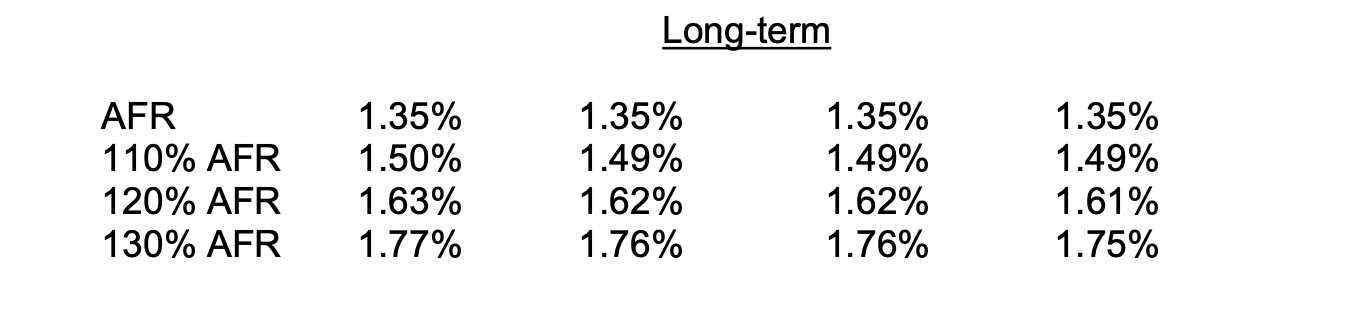

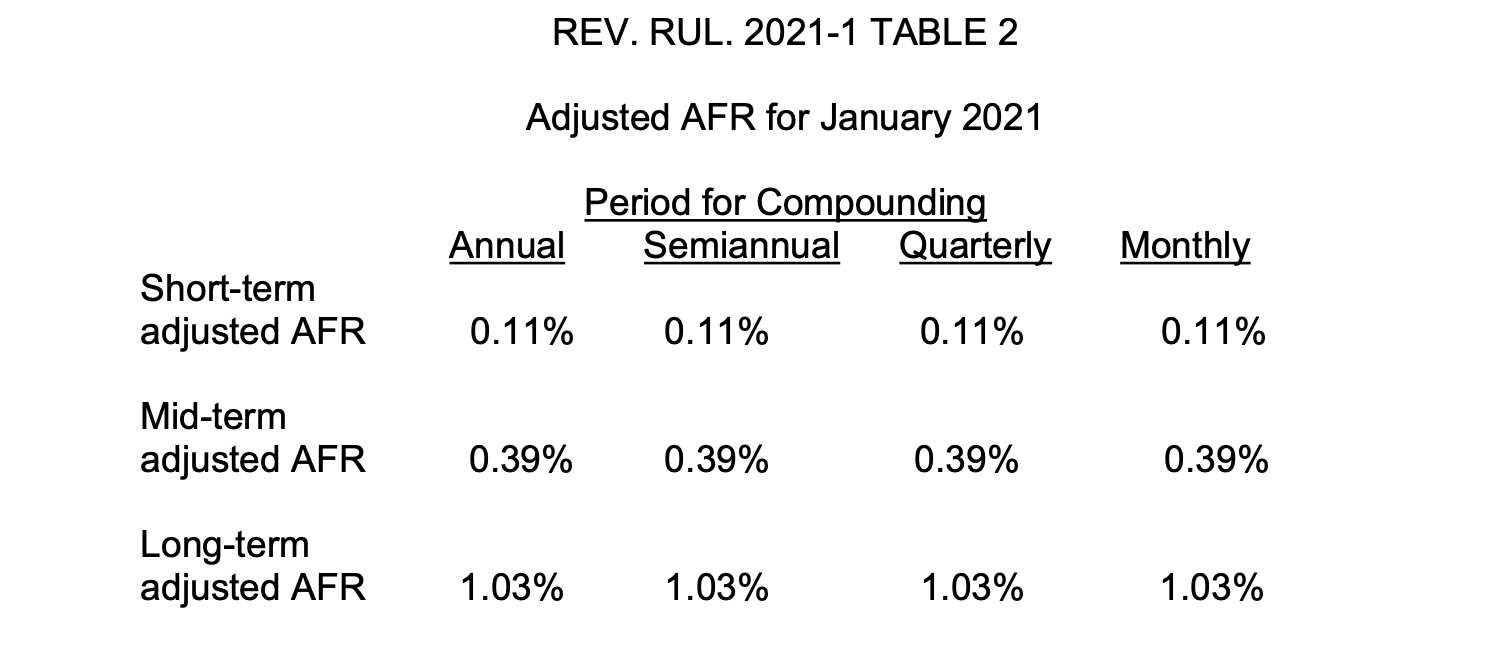

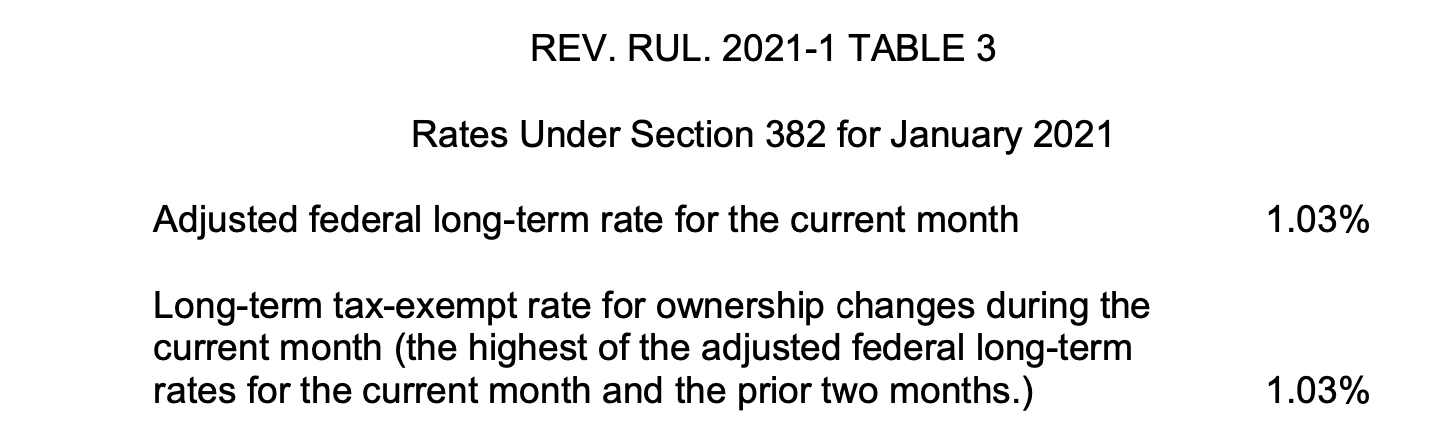

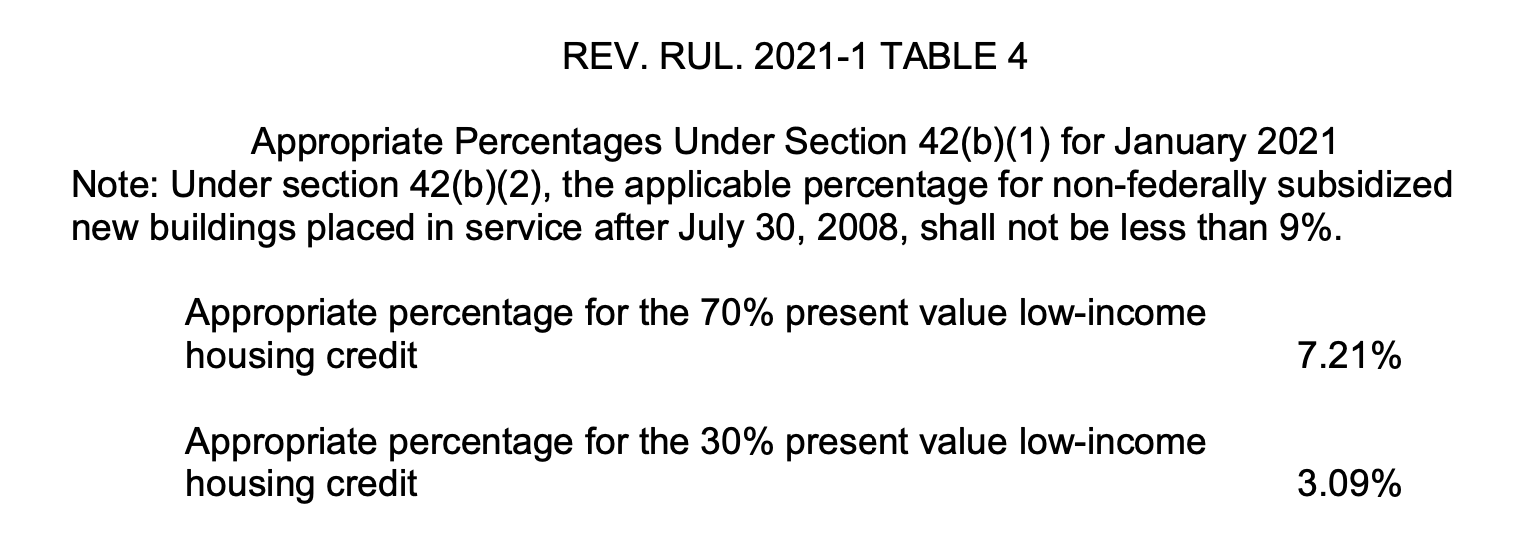

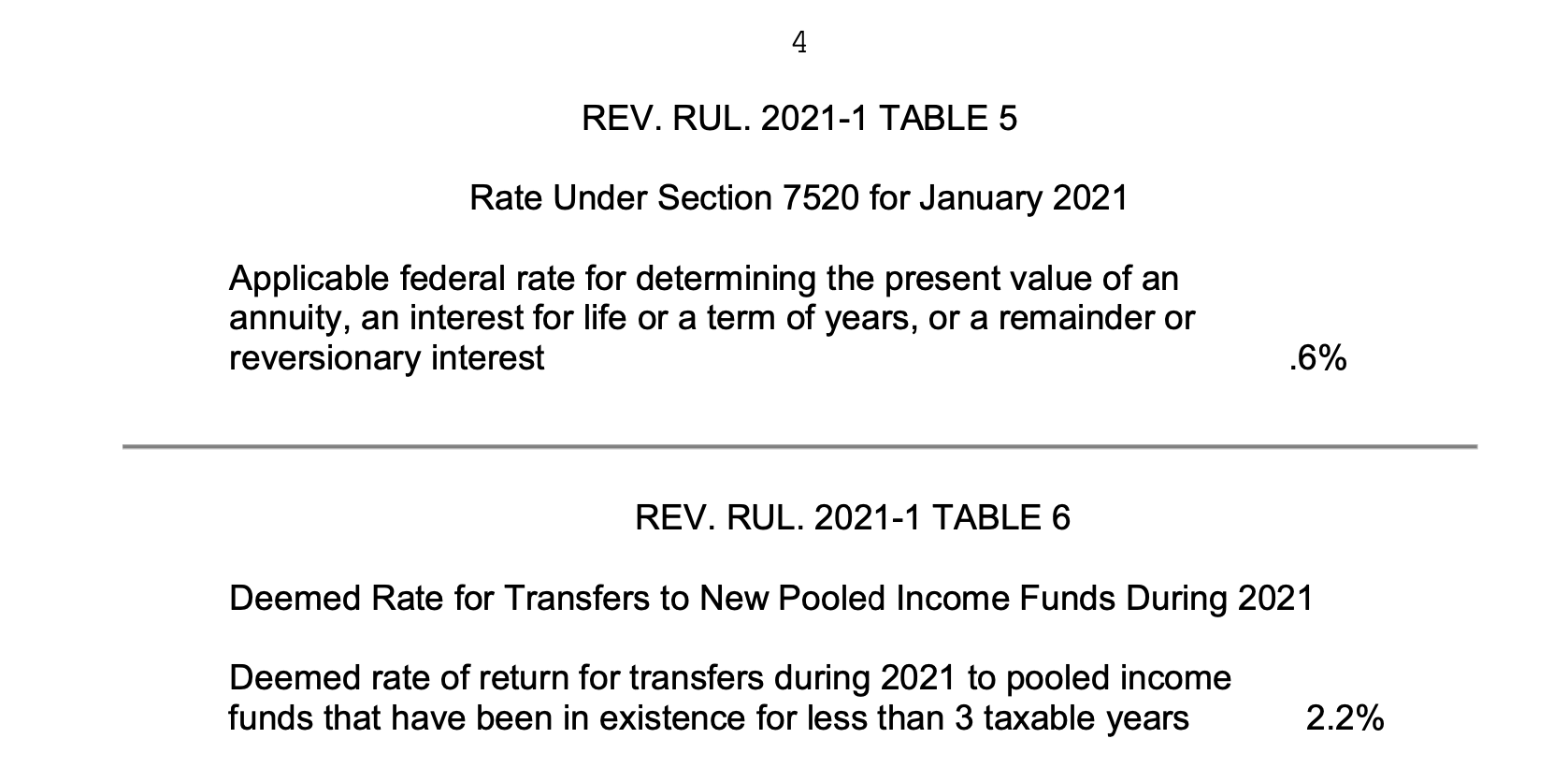

Issue 21: Rev. Rul. 2021-1 Applicable Federal Rates (AFR) January 2021