Tax Newsletter: COVID Updates

We could still see changes as the Senate considers its options with the HEROES Act. As previously stated, the Act will not clear the Senate in its current form, but the Senate could pick and choose certain provisions and push forward with different agenda items. As we put the final touches on the Fall Seminar textbook know that when Congress makes changes that become law, they will be incorporated into our discussion.

Much has changed with the PPP Loans, allowing more time to utilize if elected. In addition, a new PPP Forgiveness Loan Form was issued recently. As we count down the forgiveness timeframe, we will keep you posted on additional developments.

In This Issue

- 2nd Quarter Form 941 Preparation

- Special Enrollment Exam (SEE) Testing Begins June 1

- Extension of the Two-Year Carryover Period for SEE Candidates

- Glitch in the Transcript Delivery System

- Publication 3891 Lockbox Addresses

- OIC Procedures Due to Pandemic Issues

- FAQs on COVID-19 Retirement Plan Distribution and Loan Rule Changes

- DOL Announces Publication of Final E-Disclosure Rule

- Later this Summer we can E-file Forms 1040X

- IRS Announces Phased Openings of Taxpayer Assistance Centers

Issue 1: 2nd Quarter Form 941 Preparation

We attempted to provide some examples and guidance concerning the 2020 2nd Quarter 941. Unfortunately, there are just too many variables to adequately cover in the written form. Some of you may have sick leave, others family leave and still others the Employee Retention Credit and each must be handled on the 2nd Quarter Form 941.

The instructions are of some assistance, but to try and cover in a newsletter would leave more questions than answers.

There are at least fifteen new lines and reporting elements added to the Form 941 (plus new intermediate subtotal lines). Form 941 previously featured a total of 20 elements, so it was expanded from two pages to three. The following lines are new and related to the FFCRA and CARES Act programs:

- Qualified sick leave wages

- Qualified family leave wages

- Nonrefundable portion of credit for qualified sick and family leave wages from Worksheet 1

- Nonrefundable portion of employee retention credit from Worksheet 1

- Deferred amount of the employer share of Social Security tax

- Refundable portion of credit for qualified sick and family leave wages from Worksheet 1

- Refundable portion of employee retention credit from Worksheet 1

- Total advances received from filing Form(s) 7200 for the quarter

- Qualified health plan expenses allocable to qualified sick leave

- Qualified health plan expenses allocable to qualified family leave wages

- Qualified wages for the employee retention credit

- Qualified health plan expenses allocable to wages reported on Line 21

- Credit from Form 5884-C, Line 11, for this quarter

- Qualified wages paid March 13 through March 31, 2020, for the employee retention credit (second quarter 2020 only)

- Qualified health plan expenses allocable to wages reported on line 24 (second quarter 2020 only)

The revised Form 941 will contain extensive changes, including:

- Parts 1 and 3 of Form 941 were significantly expanded to account for the new credits eligible employers can claim for COVID-19-related qualified paid sick leave and expanded family and medical leave and the employee retention credit. Employers choosing to defer their portion of social security tax will also report the deferral on the Form 941.

- Employers will use the new Worksheet 1, Credit for Sick and Family Leave Wages and the Employee Retention Credit, to calculate these credits.

- Employers that requested an advance of the qualified leave credits and/or the employee retention credit by filing Form 7200, Advance Payment of Employer Credits Due to COVID-19, will report the amount of the advances on the revised Form 941.

Employee Retention Credit Wages Paid in March

Employers that paid qualified wages and qualified health plan expenses allocable to those wages between March 13-31, 2020, for the employee retention credit will report that information on their second quarter Form 941.

In addition, Form 7200 Advance Payment of Employer Credits Due to COVID-19 is also an option and is used to request advance payments from the IRS of tax credit amounts. This would generally be applicable to employers with significant reductions in employees in active work status, but that may be paying FFCRA paid sick or paid family leave wages to employees that are sick or caring for others due to COVID-19. If an employer estimates that tax credits arising from the Employee Retention Credit and/or FFCRA paid sick or family leave wages will be significantly higher that their expected total federal employment tax liability for the quarter, a request for advance payment via Form 7200 may result in faster receipt of funds.

You also must coordinate with the PPP Loans, as the instructions remind employers that once they receive a determination of forgiveness of a Paycheck Protection Loan, the employer may no longer defer employer Social Security taxes due after that date. Amounts deferred up to that date remain deferred until December 2021 and December 2022, in equal shares.

FFCRA Tax Credit for Employees That Have Met the Social Security Taxable Wage Limit

The instructions contain a new worksheet through which certain FFCRA and CARES Act provisions are addressed. For example, FFCRA Qualified sick and family leave wages are generally reported on Form 941, Part 1, Line 5a(i) and Line 5a(ii), respectively, Column 1, which implies that FFCRA Qualified sick and family leave wages paid to individuals that have already met the Social Security taxable wage limit for 2020 ($137,700) would result in no FFCRA credit. The worksheet provides Lines 2a(i) and 2e(i) to calculate the credit for such wages not included on Form 941, Part 1, Line 5a(i) or Line 5a(ii), Column 1, because the wages reported on that line were limited by the Social Security wage base.

The payroll tax provisions in each piece of legislation include:

- Employee retention credit:A maximum $5,000 per employee refundable payroll tax credit for certain employers that retain employees.

- Only those entities which are either (1) carrying on a trade or business during 2020 or (2) a § 501(c) organization are entitled to the credit. In addition, the eligible entity must be economically affected by the COVID-19 pandemic, which can be demonstrated in one of two ways:

- The entity’s operations must be fully or partially suspended as a result of a government order that imposes limitations upon travel, commerce, or group meetings due to the COVID-19 pandemic.

- For businesses, there must be a greater than 50% reduction in gross receipts for a calendar quarter when compared to the same quarter in the previous year.

- Employer payroll tax deferrals:Deferral of an unlimited amount of employer Social Security taxes to the end of 2021 and 2022.

- Payroll credit for required sick leave:A refundable payroll tax credit equal to any payments of the new required sick leave.

- Payroll credit for required family leave:A refundable payroll tax credit equal to any payments of the new required family leave.

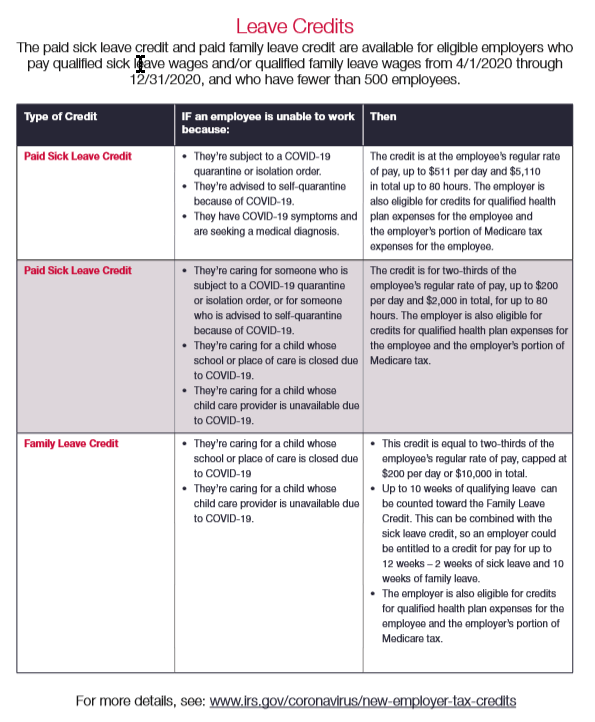

The IRS has issued a new Publication 5149 which can be found at https://www.irs.gov/pub/irs-pdf/p5419.pdf

We suggest you download a copy with the rules regarding the credits. Our reproduction here, is a sample only.

Issue 2: Special Enrollment Exam (SEE) Testing Begins June 1 – Must Wear a Mask Throughout Test – No Exceptions

Prometric will begin SEE testing, where permitted, starting June 1. Prometric test centers and staff will comply with local, state and federal regulations and guidelines to safeguard the health and well-being of test takers and staff. Candidates will be required to bring and wear a mask during the entirety of their time at the test center. Either a medical mask or cloth face covering is acceptable.

Any candidate that comes to the test center without a mask will not be allowed to test and will not be eligible for a free reschedule. Candidates must follow all safety procedures at their test center location. If you have a SEE exam scheduled for June 1 or after, your appointment may be impacted due to local, state or federal guidance and/or test center availability. If this occurs, you will receive an email informing you that your appointment has been rescheduled and it will include new appointment information. In addition, you will receive a second email explaining what to do if your new appointment date, time and location does not work for you. Currently, rescheduling fees are being waived.

All information provided is subject to change in the interest of ensuring the health, safety, and well-being of SEE candidates as well as Prometric test center staff. Please check regularly for testing updates, including test center status and safety requirements.

Issue 3: Extension of the Two-Year Carryover Period for SEE Candidates

Generally, candidates who pass a part of the examination can carry over a passing score up to two years from the date they passed that part of the examination. To provide candidates flexibility in testing during this period of global emergency, we are extending the two-year period to three years for any examination parts that had not expired as of February 29, 2020. Only those candidates who passed a part of the examination February 29, 2020 or earlier, will now have three years from the date they passed a part of the examination to pass the remaining parts.

For example, if a candidate passed Part 1 on November 15, 2019, they now have until November 15, 2022 to pass parts 2 and 3.

Issue 4: Extends Certain Deadline for Employment Taxes and Benefit Plans with Time Sensitivity Issues – Notice 2020-35 and 2020-25

On March 13, 2020, the President declared a federal disaster (Emergency Declaration) due to the emerging COVID-19 pandemic. The following deadlines have been extended to July 15 as follows:

- Employers correcting employment tax reporting errors using the interest-free adjustment process.

- Employers correcting employment tax underpayments or overpayments.

- Exempt organizations filing Form 990-N, e-Postcard.

- Exempt organizations commencing a declaratory judgment suit.

- Single employer defined benefit plans applying for a funding waiver.

- Multi-employer defined benefit plans: (1) certifying funded status and giving notice to interested parties of that certification; (2) adopting, and notifying the bargaining parties of the schedules under, a funding improvement or rehabilitation plan; and (3) providing the annual update of a funding improvement plan and its contribution schedules, or rehabilitation plan and its contribution schedules, and filing those updates with their annual return.

- Cooperative and small employer charity (CSEC) plans (1) making contributions required to be made for the plan year; (2) making required quarterly installments; (3) adopting a funding restoration plan; and (4) certifying funded status.

- Employee benefit plans filing Form 5330, Return of Excise Taxes Related to Employee Benefit Plans, and paying the associated excise tax.

Other deadlines were in place but passed on June 30, 2020. In addition, for the period beginning on March 30, 2020, and ending on July 15, 2020, IRS disregarded of any interest or penalty for failure to file the Form 5330 or to pay the excise tax postponed by the notice. Interest and penalties with respect to such postponed filing and payment obligations will begin to accrue on July 16, 2020.

Defined benefit plans have until July 31, 2020:

- To adopt a pre-approved defined benefit plan that was approved based on the 2012 Cumulative List.

- To submit a determination letter application under the second six-year remedial amendment cycle; and

- To take actions that are otherwise required to be performed regarding disqualifying provisions in a plan during the remedial amendment period that would otherwise have ended on April 30, 2020.

The due date for filing and furnishing Form 5498, IRA Contribution Information, Form 5498-ESA, Coverdell ESA Contribution Information, and the Form 5498-SA, HSA, Archer MSA, or Medicare Advantage MSA Information, is postponed to August 31, 2020. Penalties will be disregarded through this period and will begin on September 1, 2020.

Issue 5: FAQs for Aliens Claiming Medical Condition or Travel Exceptions to Substantial Presence Test

Q1. Will an alien individual who intended to but is or was unable to leave the United States on the individual’s planned departure date due to a medical condition or medical problem in calendar year 2020 be required to obtain a physician’s statement as required by Part V of Form 8843?

A1. Any alien individual who is eligible and fulfills the requirements to claim the Medical Condition Exception may file the Form 8843 without a physician’s statement to cover a single period of up to 30 consecutive calendar days in calendar year 2020 (30-Day Medical Condition). This FAQ does not modify the eligibility requirements to claim the Medical Condition Exception, only the procedures for claiming the exception on Part V of Form 8843 and only with respect to a single period of up to 30 consecutive calendar days of presence in the United States in calendar year 2020.

The exemption from the Form 8843 requirement to obtain a physician’s statement for a 30-Day Medical Condition can be claimed in addition to the relief provided in Rev Proc 2020-20. The instructions to Form 8843 for 2020 will reflect the 30-Day Medical Condition contemplated by this FAQ.

Q2. What types of documentary evidence should alien individuals retain to support their eligibility for the 30-Day Medical Condition?

A2. In lieu of a physician’s statement, alien individuals claiming the 30-Day Medical Condition should retain documentary evidence that substantiates their medical condition, their inability to leave due to the medical condition, and the period of the medical condition, such as:

- evidence of consultations with a heath care provider (e.g., a phone bill or a text message or email from the health care provider),

- (ii) receipts related to healthcare purchases,

- (iii) evidence of canceled or changed travel reservations, or (iv) official medical records or written healthcare correspondence that the individual received (e.g., automated responses instructing an individual to self-isolate).

These documents should not be submitted with the Form 8843, but alien individuals claiming the 30-Day Medical Condition should be prepared to produce these records if requested by IRS.

Q3. How should alien individuals who only claim the 30-Day Medical Condition Complete Part V of Form 8843 (the section of the form applicable to individuals claiming the Medical Condition Exception)?

A3. For those claiming a 30-Day Medical Condition without claiming relief under Rev Proc 2020-20 or any other excluded days pursuant to the Medical Condition Exception, the alien individual should write “30-Day Medical Condition” and then describe in detail the 30-Day Medical Condition that prevented the alien individual from leaving the US under Line 17a in Part V of Form 8843. When determining the information to include in line 17a, an alien individual should provide relevant information so that the individual can clearly demonstrate qualification for the Medical Condition Exception if the Form 8843 is later reviewed by IRS with the corresponding documentary evidence discussed in FAQ 2, as applicable. Lines 17b and 17c should be completed consistently with the form’s instructions. Line 18 of the form should be left blank.

As described in FAQ 2, third-party documentary evidence of an alien individual’s medical condition should not be submitted with the form but should be retained by the alien individual.

Q4. How should alien individuals who claim multiple Medical Condition Exceptions Complete Part V of Form 8843?

A4. An alien individual may be able to claim multiple Medical Condition Exceptions and should file a single Form 8843 enumerating all the applicable Medical Condition Exceptions on line 17a. The alien individual should attach a separate statement with respect to each Medical Condition Exception being claimed along with the relevant corresponding information as outlined in Rev Proc 2020-20, in FAQ 3, or the existing instructions, as applicable. As an example, line 17a could read: “Condition 1: COVID-19 MEDICAL CONDITION TRAVEL EXCEPTION; Condition 2: 30-DAY MEDICAL CONDITION,”

Lines 17b and 17c of Part V should be left blank, but the relevant information for each applicable exception, as described in Rev Proc 2020-20 and in FAQ 3, along with the dates that would otherwise be reflected under line 17b and line 17c, would be included in each separate statement. Neither of these conditions require a physician’s statement, and thus line 18 should be left blank.

Note, however, if an alien individual is also claiming a Medical Condition Exception that requires a physician’s statement, the signature and relevant information from line 18 should be included in the separate attachment related to that medical condition.

Q5. What types of documentary evidence should Eligible Individuals retain to support their eligibility for the relief provided under Rev Proc 2020-20?

A5. An Eligible Individual claiming relief under Rev Proc 2020-20 should retain evidence of the individual’s presence in the United States during the individual’s claimed COVID-19 Emergency Period (such as a Customs and Border Protection Form I-94 showing the individual’s entries into the United States, hotel receipts, or travel reservations, including confirmation of changes or cancellations). If the Eligible Individual was actually ill or advised to self-quarantine in the United States during the individual’s excluded days under the revenue procedure, he or she may also retain the documents described in FAQ 2 to demonstrate presence in the U.S. through U.S.-based medical records and treatments, though failure to document an actual illness will not affect eligibility to claim relief under Rev Proc 2020-20.

Issue 6: IRS Begins Processing Centralized Authorization File Requests

IRS has announced that it has begun processing Centralized Authorization File (CAF) requests on a limited basis.

Issue 7: Your Client Could Receive Old Balance Due Notices

IRS was unable to mail some previously printed balance due notices as a result of office closures. Rather than reprogram computers and reissue notices, these old notices are being mailed. Dates on notices will be past and due dates for a particular deadline will also be in the past. In an effort to avoid confusion each notice will includes an insert confirming that the due dates printed on the notices have been extended.

The new payment due date will be either July 10, 2020, or July 15, 2020, depending upon the type of tax return and original due date. Clients who have questions about their balance due should visit the website listed or call the number provided on their notice. IRS cautions that phone lines remain extremely busy as IRS resumes operations.

Notices that will include the insert:

- CP11, Math Error on Return – Balance Due

- CP14, Balance Due, No Math Error

- CP15, Civil Penalty Notice

- CP15B, Civil Penalty Notice for Trust Fund Recovery Penalty

- CP15H, Shared Responsibility Payment Due

- CP21A, Data Processing Adjustment Notice, Balance Due of

- CP22A, Data Processing Adjustment Notice, Balance Due of

- CP23, Estimated Tax Credits Discrepancy – We Changed Your Return to Match Your Credits or Payments Posted to Your Account – Balance Due

- CP23T, Estimated Tax Discrepancy, Balance Due of $5 or More

- CP47A, Tax Assessed- Notification of the Requested Credit Elect/Refund Being Applied to Section 965 Tax Liability

- CP47B, Tax Assessed- Notification of a Credit Elect/Refund Being Applied to Section 965 Tax Liability

- CP47C, Tax Assessed- Including Section 965 Tax Liability

- CP51A, We’ve Calculated Your Income Tax For You – Balance Due

- CP60, We Removed a payment Erroneously Applied to Your Account. – Balance Due

- CP94, Criminal Restitution Final Demand Notice

- CP101, Math Error, Balance Due of $5 or More on Form 940

- CP102, Math Error, Balance Due of $5 or More on Forms 941, 941SS, 943, 944, 944SS, 945

- CP103, Math Error, Balance Due – Form CT-1

- CP104, Math Error, Balance Due of $5 or More – Form 720

- CP105, Math Error, Balance Due of $5 or More – Forms 11C, 2290, 706, 709, 730

- CP107, Math Error, Balance Due of $5 or More – Form 1042

- CP126, Math Error, Balance Due or Overpayment Less Than $1 on Forms 990PF, 4720, 5227

- CP132, Math Error, Balance Due on Forms 990C, 990T,1041, 1120, 8804

- CP134B, Federal Tax Deposit(s) (FTD) Discrepancy – Balance Due

- CP141L, We Charged a Penalty Under Internal Revenue Code Section 6652(c) – Form Filed Late

- CP161, No Math Error, Balance Due (Except Form 1065)

- CP162, Untimely Filing Penalty – Partnership

- CP165, Penalty Assessed for Dishonored Check

- CP210, Examination (Audit) or Data Processing Tax Adjustment – Balance Due, Overpayment, or Even Balance

- CP215, Civil Penalty – 500 and 600 Series

- CP220, Examination (Audit) or Data Processing Tax Adjustment – Balance Due, Overpayment, or Even Balance

- CP220J, Employer Shared Responsibility Payment (ESRP) 4980H Adjustment – Balance Due, Even Balance or Overpayment Notice

- CP230, Combined Annual Wage Reporting – CAWR/DP Tax Adjustment Amended Return Filed

- CP233J, 4980H Adjustment balance due, even balance or overpayment Notice (ESRP)

- CP240, Combined Annual Wage Reporting – CAWR/DP Discrepancy Tax Adjustment

- CP260, An Erroneous Payment Previously Applied to Your Account Has Been Reversed – Balance Due

- CP283, Penalty Charged on Your Form 5500 – Late or Incomplete Form

- CP711, Spanish Math Error – Balance Due – Error en la Planilla – Saldo Adeudado

- CP714, Spanish Balance Due – No Math Error – Planilla Radicada – Saldo Adeudado

- CP721A, Data Processing Adjustment Notice, Balance Due (Spanish) – Cambios a su Planilla – Saldo Adeudado

- CP722A, Spanish Data Processing Adjustment Notice, Balance Due of $5 or more – Cambios a su Planilla – Saldo Adeudado

- CP802, Spanish BMF Math Error, Balance Due of $5 or More on Forms 941PR, 943PR – Hemos Hecho Cambios a su Planilla Porque Creemos que hay un Error de Cálculo

- CP834B, Federal Tax Deposit(s) (FTD) Discrepancy – Balance Due (Spanish)

- CP865, Spanish Penalty for Dishonored Check on Forms 94XPR FTD

Issue 8: IRS Provides Guidance on Leave-Sharing Programs – IR 2020-119 and Notice 2020-46

In the Notice, the IRS has provided guidance on employer leave-sharing programs that aid victims of the COVID-19 pandemic. The Notice provides that cash payments employers make, under a leave-sharing program, to tax-exempt charitable organizations providing relief to victims of the COVID-19 pandemic, will not be treated as wages or compensation to the employees for federal tax purposes.

To qualify under the Notice, the employer’s payments must be:

(1) made to a §170(c) organization for the relief of victims of the COVID-19 pandemic in the affected geographic areas – all 50 states, the District of Columbia, and the five U.S. territories and

(2) paid to the §170(c) organization before January 1, 2021.

Employees electing to forgo leave may not claim a charitable contribution deduction for the value of their forgone leave.

However, an employer may deduct cash payments made pursuant to a leave-sharing program as a charitable contribution or as a business expense, provided the employer otherwise meets the requirements for taking such deductions.

An employer should not include any cash payments made pursuant to a leave-sharing program in Box 1, 3 or 5 of the Form W-2 of an employee forgoing leave.

Issue 9: IRS Updates Economic Impact payments to Include FAQs on Prepaid Debit Cards

Q10. I am a citizen or resident of one of the Freely Associated States (Federated States of Micronesia, the Republic of the Marshall Islands, and the Republic of Palau). Can I be eligible to receive a Payment?

A10. Citizenship or residency status in the Freely Associated States, by itself, does not entitle you to a Payment. However, if you are a resident of a U.S. territory for the tax year 2020 for U.S. territory income tax purposes, you can be eligible for a Payment from the U.S. territory tax agency. To determine whether you are eligible for a Payment from a U.S. territory tax agency, consult with your U.S. territory tax agency. Alternatively, if you are not a resident of a U.S. territory for the tax year 2020 but you are a U.S. citizen or U.S. resident for federal income tax purposes, you may be eligible for a Payment from IRS.

Q11. What does it mean if I received a Payment from both IRS and a U.S. territory tax agency?

A11. In general, eligible individuals should not receive a Payment from both IRS and a U.S. territory tax agency. If you have received a Payment from more than one jurisdiction and you are a resident of a U.S. territory for the 2020 tax year, please consult your U.S. territory tax agency concerning information about Payments received by U.S. territory residents from IRS, including incorrect or duplicate Payments. If you have received a Payment from more than one jurisdiction and you are a NOT a resident of a U.S. territory for the 2020 tax year, you should return any incorrect or duplicate Payments received from the U.S. territory tax agency to IRS.

Q20. Who should NOT use Non-Filers: Enter Payment Info Here?

A20. You should not use the Non-Filers: Enter Payment Info Here tool if any of the following apply:

- You already filed a 2019 tax return.

- You are required to file a 2019 tax return.

- You already received your Economic Impact Payment based on your 2018 or 2019 return, even if you think you did not receive the full amount (for example, because you have a newly born child in 2020 who was not reported on your 2019 return).

- You are not required to file a return and already received your Payment based on your 2019 Social Security retirement, survivor or disability benefits (SSDI), Railroad Retirement benefits, Supplemental Security Income (SSI) and Veterans Affairs benefits even if you think you did not receive the full amount. Someone claimed you as a dependent on their 2019 tax return.

- You were not a U.S. citizen or U.S. permanent resident (green card holder) in 2019. Those who were resident aliens in 2019 because they satisfied the “substantial presence test” and qualify for the Payment must file a tax return to receive the Payment.

- You do not have a Social Security Number valid for employment.

Q42. My address is different from the last tax return I filed. How can I change my address?

A42. If you need to change your address, see IRS’s Address Changes website, https://www.irs.gov/faqs/irs-procedures/address-changes/address-changes.

If IRS receives your payment back because the Post Office was unable to deliver it, we will update your payment status to “Need More Information,” on the Get My Payment application at which point you will be able to enter your bank account information.

If you do not provide your bank account information, IRS will hold your Economic Impact Payment until we receive your updated address.

Q49. Can I transfer money from my debit card to my bank account?

A49. Yes. The limit on ACH transfers to a bank account is $2,500 per transaction. This is an increase from the previously announced amount of $1,000 per transfer. You can easily transfer the money from your Card to an existing bank account online at EIPcard.com or using the Money Network Mobile App. You will need the Routing and Account number for your bank account. To transfer funds:

- Call 800-240-8100 (TTY: 800-241-9100) to activate your Card.

- Register for online or mobile app access by going to EIPCard.com or the Money Network Mobile App and click on “Register”. Follow the steps to create your User ID and Password. Be sure to have your EIP Card handy.

- Select Move Money Out and follow the steps to set up your ACH transfer. Transfers should post to your bank account in 1-2 business days.

Q51. What do I do if my prepaid debit card was lost or destroyed?

A51. Individuals who have lost or destroyed their EIP Card may request a free replacement through MetaBank Customer Service. The standard fee of $7.50 will be waived for the first reissuance of any EIP Card. Any initial reissuance fee charged to a customer from an earlier date will be reversed. Individuals do not need to know their card number to request a replacement. Individuals may request a replacement by phone at 800-240-8100 (option 2 from main menu).

Q52. I received the prepaid debit EIP Card as my Payment, but my name is incorrect. What should I do?

A52. If the issue is with the last name on the card (i.e., issued in a previous name such as a maiden or married name), the payee with the first name on the first line can still activate the card and/or validate identity to continue activation. For other name related issues or questions (i.e., incorrect spelling), contact MetaBank, N.A at 800-240-8100, or visit EIPcard.com.

Q53. I received my Payment by check, but it was lost, stolen, or destroyed. How do I get a new one?

A53. If you received your Payment by check and it was either lost, stolen or destroyed, you should initiate a trace on your Payment by calling IRS at 800-919-9835 or you may submit Form 3911 (Taxpayer Statement Regarding Refund). If you call, please be advised that you may experience long wait times or recorded assistance due to limited staffing. If you submit the form and you are Married Filing Joint, both spouses must sign the form.

Your claim for a missing Payment is processed in one of two ways:

- If the check was not cashed, you will receive a replacement check once the original check is canceled.

If you find the original check and receive a replacement, you MUST return the original as soon as possible.

- If the refund check was cashed, the Bureau of the Fiscal Service (BFS) will provide you with a claim package that includes a copy of the cashed check. Follow the instructions for completing the claim package. BFS will review your claim and the signature on the canceled check before determining whether they can issue you a replacement check.

Do not request a Payment trace if you are trying to determine eligibility for the Payment or the amount of Payment you should have received.

Q54. I received Notice 1444 in the mail saying my Payment was issued, but I have not received my Payment. What should I do?

A54. If you received Notice 1444 in the mail and have not received your Payment as mentioned in the notice, see https://www.irs.gov/coronavirus/get-my-payment-frequently-asked-questions#lost.

Do not request a Payment trace if you are trying to determine eligibility for the Payment or the amount of Payment you should have received. You must have been issued Notice 1444 or received a payment date from Get My Payment to perform a trace.

Q62. How will IRS send my Economic Impact Payment if I have a representative payee or I am a representative payee? (added June 10, 2020)

A62. If you filed a 2019 or 2018 tax return: Your Payment was or will be sent to the bank account provided on your tax return for a direct deposit of your tax refund, or mailed to the address we have on file if a tax refund was mailed or there was no refund on your tax return. If you did not file a 2019 or 2018 tax return:

- An Individual Representative Payee should be receiving EIPs to the same direct deposit account or Direct Express card as the recipient’s monthly benefit payment. The mailing of these Payments to payees is underway.

- For an Organizational Representative Payee, the schedule above is the same, except that the payee may receive the EIP electronically or by mail.

Q64. How do I return an Economic Impact Payment (EIP) that was received as an EIP Card (debit card) if I do not want the payment re-issued?

A64. If you received your EIP as a debit card and want to return the money to IRS and NOT have the payment re-issued, send the card along with a brief explanation stating you don’t want the payment and do not want the payment re-issued: Money Network Cardholder Services 5565 Glenridge Connector NE Mail Stop GH-52 Atlanta, GA 30342.

Issue 10: No 2020 Employer Correction Request Notices (EDCOR)

The purpose of the letter is to advise employers that corrections are needed in order for the Social Security Administration to properly post employee’s earnings to the correct record. There are a number of reasons why reported names and SSNs may not agree with SSA records, such as typographical errors, unreported name changes, and inaccurate or incomplete employer records.

An EDCOR letter is mailed to an employer identified as having at least one name and Social Security Number (SSN) combination submitted on Form W-2 (Wage and Tax Statement) that does not match SSA records. The decision was made not to send these letters to employers in 2020 due to the impact of COVID-19 on the SSA and employers.

At this point, the SSA representative said there are currently no plans to send out the 2020 letters in 2021. This does not mean the SSA would not do that but at this point there are no such plans. When the letters are resumed, it’s likely to be for 2021, the SSA representative added.

The SSA was recently able to get its toll-free phone number up and running again that goes directly to people who can assist with employer-related SSA issues. That number is (800) 772-6270 (325-0778 for TTY) and people can call from Monday through Friday from 7:00 a.m. to 7:00 p.m.

Issue 11: Economic Impact Payments Belong to Recipient, NOT Nursing Home or Care Facilities

The IRS alerted nursing homes and other care facilities that Economic Impact Payments (EIPs) belong to the recipients, not the organizations providing the care. The IRS issued this reminder following concerns that people and businesses may be taking advantage of vulnerable populations who received the EIPs.

The payments are intended for the recipients, even if a nursing home or other facility or provider receives the person’s payment, either directly or indirectly by direct deposit or check. The Social Security Administration (SSA) has issued FAQs on this issue, including how representative payees should handle administering the payments for the recipient. The IRS also noted the Economic Impact Payments do not count as resources that have to be turned over by benefit recipients, such as residents of nursing homes whose care is provided for by Medicaid. The Economic Impact Payment is considered an advance refund for 2020 taxes, so it is considered a tax refund for benefits purposes.

Issue 12: Remind Your Clients to Keep Notice 1444 Concerning their Economic Impact Payment – Needed for the 2021 Tax Season

The IRS mails the notice, Notice 1444, Your Economic Impact Payment, to your client’s address of record within a few weeks after the Payment was issued. Individuals should keep the letter for their tax records. The Economic Impact Payment is considered an advance credit against 2020 tax. Taxpayers will not include the payment in taxable income on their 2020 tax return or pay income tax on the payment. It will not reduce a taxpayer’s refund or increase the amount of tax a taxpayer owes when the taxpayer files a 2020 Federal income tax return next year. When a taxpayer files a 2020 tax return next year, the taxpayer may claim any additional credit for which the taxpayer is eligible. The IRS is not able to correct or issue an additional payment at this time and will provide further details on IRS.gov on the action individuals may need to take in the future.

Issue 13: Additional FAQ’s Concerning the Stimulus Payment Issued

- My payment was mailed weeks ago, but the Post Office was unable to deliver it. What should I do?

- If you have not received your payment within 14 days of the payment date, check the Get My Payment tool periodically. If the IRS receives your payment back because the Post Office was unable to deliver it, the IRS will update your payment status on the Get My Payment tool to “Need More Information,” at which point you will be able to enter your bank account information.

If you don’t provide your bank account information, then the IRS will hold your EIP until it receives your updated address. To update your address, go to the IRS’s webpage “Address changes.”

- My address has changed or is incorrect. What can I do to change or correct it to receive my EIP?

- The Get My Payment tool will not allow you to change your address. If you need to change your address, go to the IRS’s webpage “Address changes.”

If the IRS receives your payment back because the Post Office was unable to deliver it, the IRS will update your payment status to “Need More Information,” at which point you will be able to enter your bank account information.

If you don’t provide your bank account information, the IRS will hold your EIP until it receives your updated address.

- Get My Payment shows that my EIP was issued but I never received it. How do I get a new one?

- If Get My Payment shows your EIP was issued but you have not received it and it has been more than five days since the scheduled deposit date (or more than four weeks since it was mailed by check; six weeks if you have a forwarding address on file with the local post office; nine weeks if you have a foreign address), you should initiate a trace on your EIP by calling the IRS at 800-919-9835 or you may submit Form 3911 (Taxpayer Statement Regarding Refund). If you call, please be advised that you may experience long wait times or recorded assistance due to limited staffing. If you submit the form and you are Married Filing Joint, both spouses must sign the form.

You must have been issued Notice 1444, Your Economic Impact Payment, or received a payment date from Get My Payment to perform a trace.

The IRS notes that if the EIP payment was made via direct deposit, check with your bank before initiating a trace to verify they did not receive the deposit. Do not request an EIP trace if you are trying to determine eligibility for the EIP or the amount of EIP you should have received.

Your claim for a missing EIP made by check is processed one of two ways:

- If the check was not cashed, you’ll receive a replacement check once the original check is canceled. (If you find the original check and receive a replacement, you must return the original as soon as possible.)

- If the refund check was cashed, the Bureau of the Fiscal Service (BFS) will provide you with a claim package that includes a copy of the cashed check. Follow the instructions for completing the claim package. BFS will review your claim and the signature on the canceled check before determining whether they can issue you a replacement check.

- I never received my EIP after it was issued or I received it and it was lost, stolen, or destroyed. Can I initiate a trace on my EIP using Get My Payment?

- No. Get My Payment cannot be used to initiate a trace on your EIP.

Issue 14: IRS Clarifies the Effect of the Cares Act NOL Carrybacks with New FAQ’s When Calculating UBTI

Q1. When determining the UBTI of an EO with more than one unrelated trade or business in a tax year beginning after December 31, 2017, are CARES Act NOLs required to be siloed so that each unrelated trade or business calculates its NOL separately?

A1. Yes. §512(a)(6) requires an EO with more than one unrelated trade or business to silo CARES Act NOLs arising in tax years beginning after December 31, 2017, so that each trade or business calculates its NOL separately.

Q2. Can an EO with CARES Act NOLs carry back and deduct those NOLs against the aggregate UBTI in a tax year beginning before January 1, 2018?

A2. Yes. An EO subject to §512(a)(6) can deduct CARES Act NOLs against the aggregate UBTI in a tax year beginning before January 1, 2018, because §512(a)(6) does not apply to tax years beginning before January 1, 2018. Also, an EO may carry back CARES Act NOLs attributable to an unrelated trade or business, even if the EO would not have a CARES Act NOL if the deduction was calculated on an aggregate basis.

Q3. Can an EO deduct CARES Act NOLs against aggregate UBTI in tax years beginning after December 31, 2017, if any CARES Act NOLs remain after being carried back to tax years beginning before January 1, 2018?

A3. No. When deducting CARES Act NOLs against UBTI in tax years beginning after December 31, 2017, the CARES Act NOLs must be siloed consistent with §512(a)(6).

Issue 15: IRS Will Not Accept Group Tax-Exempt Status Letter Request After June 16, 2020 Pending Final Regulations

This notice contains a proposed revenue procedure that sets forth updated procedures under which recognition of exemption from federal income tax for organizations described in §501(c) of the Internal Revenue Code (Code) may be obtained on a group basis for subordinate organizations affiliated with and under the general supervision or control of a central organization.

The proposed revenue procedure also sets forth updated procedures a central organization must follow to maintain a group exemption letter. The proposed revenue procedure would modify and supersede Rev. Proc. 80-27, 1980-1 C.B. 677 (as modified by Rev. Proc. 96-40, 1996-2 C.B. 301).

The old procedures for obtaining group exemption letters, in Rev Proc 80-27 continue to apply pending publication of the final revenue procedure.. It also provided that IRS will not accept any requests for group exemption letters starting on June 17, 2020 until publication of the final revenue procedure or other guidance in the IRB.

Issue 16: Social Security Unveils Redesigned Retirement Benefits Portal at socialsecurity.gov

The Social Security Administration announced the first of several steps the agency is taking to improve the public’s experience on its website. The newly redesigned retirement benefits portal, at www.socialsecurity.gov/benefits/retirement, will help millions of people prepare for and apply for retirement.

The redesigned portal will make it easier for people to find and read about Social Security retirement benefits, with fewer pages and condensed, rewritten, and clearer information. The portal also is optimized for mobile devices so people can learn and do what they want from wherever they want, and the portal now includes the ability to subscribe to receive retirement information and updates.

Click on www.socialsecurity.gov/benefits/retirement to find out how to Learn, Apply, and Manage retirement benefits, and learn how to create a personal my Social Security account online.

Issue 17: FAQ’s for Nonresident Alien Individuals and foreign businesses with Employees or Agents Impacted by COVID-19 Emergent Travel Interruptions

Q1. Will a nonresident alien or foreign corporation, not otherwise engaged in a USTB, be treated as engaged in a USTB as a result of services or other activities conducted by one or more individuals temporarily present in the United States if, but for COVID-19 Emergency Travel Disruptions, those services or other activities would not have been conducted in the United States?

A1. A nonresident alien, foreign corporation, or a partnership in which either is a partner (Affected Person) may choose an uninterrupted period of up to 60 calendar days, beginning on or after February 1, 2020, and on or before April 1, 2020 (the COVID-19 Emergency Period), during which services or other activities conducted in the United States will not be taken into account in determining whether the nonresident alien or foreign corporation is engaged in a USTB, provided that such activities were performed by one or more individuals temporarily present in the United States and would not have been performed in the United States but for COVID-19 Emergency Travel Disruptions.

For purposes of these FAQs, an “individual temporarily present in the United States” means an individual who is present in the United States on or after February 1, 2020, and on or before April 1, 2020, and is a nonresident alien, or a U.S. citizen or lawful permanent resident who had a tax home as defined in §911(d)(3) outside the United States in 2019 and reasonably expects to have a tax home outside the United States in 2020. In addition, to determine the nonresident status of an alien, the relief provided in Rev. Proc. 2020-20 is applicable.

Q2. If a nonresident alien or foreign corporation is engaged in a USTB (taking into account the application of the treatment in Question 1) but otherwise does not carry on such USTB through a PE under an applicable income tax treaty, will the nonresident alien or foreign corporation be treated as conducting business through a PE due to services or other activities conducted by individuals temporarily present in the United States that would not have been conducted in the United States but for COVID-19 Emergency Travel Disruptions?

A2. During an Affected Person’s COVID-19 Emergency Period, services or other activities performed by one or more individuals temporarily present in the United States will not be taken into account to determine whether the nonresident or foreign corporation has a PE, provided that the services or other activities of these individuals would not have occurred in the United States but for COVID-19 Emergency Travel Disruptions.

General Information

An Affected Person’s income earned during the COVID-19 Emergency Period will not be subject to the 30% gross basis tax imposed under §871(a) or §881(a) solely because the Affected Person is not treated as having a USTB or PE under these FAQs. In all events, the Affected Person should retain contemporaneous documentation to establish the period chosen as the COVID-19 Emergency Period and that the relevant business activities conducted by individuals temporarily present in the United States during the COVID-19 Emergency Period would not have been undertaken in the United States but for COVID-19 Emergency Travel Disruptions.

The Affected Person should be prepared to provide that documentation upon request by the IRS. Nonresident aliens and foreign corporations (including those that are partners in partnerships) may make protective filings of their annual U.S. tax returns, even if they believe they are not required to file for the 2020 taxable year because they were not engaged in a USTB, to avail themselves of the benefits and protections that arise from such filings (such as those relating to deductions, statutes of limitations, and claiming tax treaty-based relief).

Issue 18: IRS Sending Out Old Notices with Updated Insert

Due to the COVID-19 pandemic, the IRS was unable to mail some previously printed balance due notices as a result of office closures. As IRS operations continue to reopen, these notices will be delivered to taxpayers in the next few weeks.

Some of the notices may reflect due dates that have already passed. The IRS assures taxpayers the due dates have been extended to July 10 or July 15, 2020, depending on the type of tax payment and original due date. The correct due date will appear on an additional insert mailed with each notice. Taxpayers who have questions can call the number provided on their notice.

Issue 19: IRS Announces Phased Openings of Taxpayer Assistance Centers (IRS Walk-In Offices)

Beginning June 29, 2020, IRS will begin the phased in openings of their walk-in offices.

As before appointments will be needed, the number to call for an appointment is 844-545-5640.

Appointments for in-person assistance will be available for:

- Authentication of identity and document validation related to tax return filing or application for Individual Taxpayer Identification Number.

- Sailing clearances required for foreign travel by resident and nonresident aliens leaving the U.S.

- Assistance with Economic Impact Payment issues; and

- Cash tax payments.

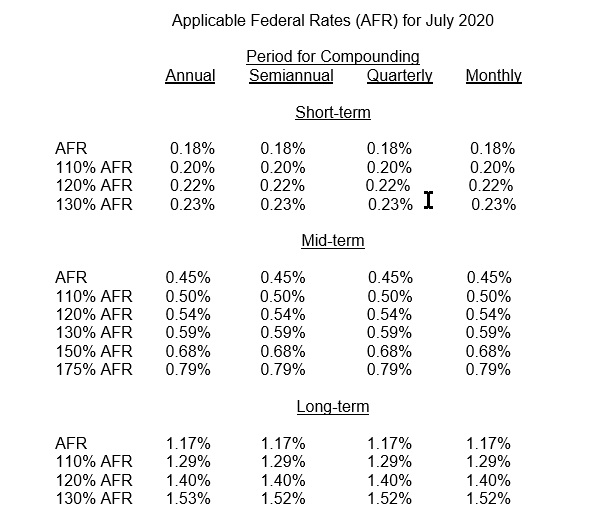

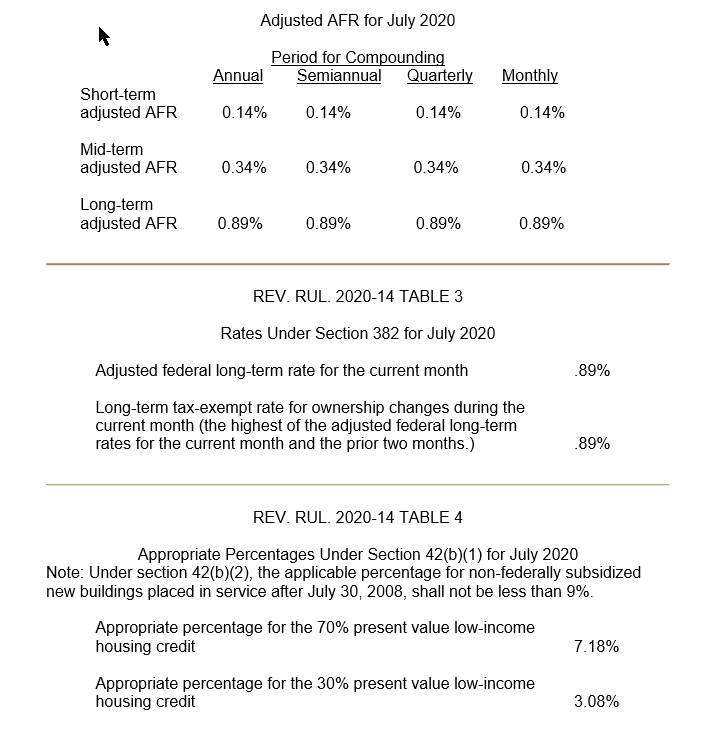

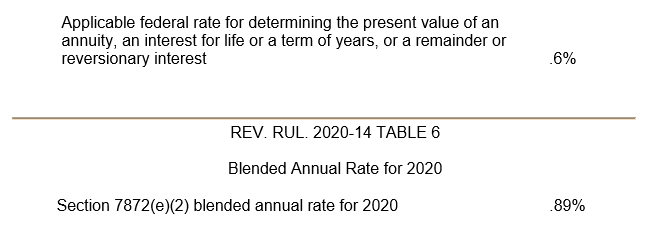

Issue 20: Applicable Federal Rates (AFR) for July 2020

Check out our July Webinars!

7/9/20 Correcting Depreciation Form 3115 & the Qualified Improvement Property Fix: When depreciation errors are detected on previously filed tax returns, most spontaneously want to amend the return and correct this error. However, amending previously filed returns usually is not an accurate or beneficial way to proceed. There are procedures, which will be clarified, that will allow us to fix these depreciation omission and or oversights. Furthermore, this webinar will deliver a comprehensive example on making changes to previously missed or incorrect depreciation. The when and how of IRC Section 481(a) adjustments will be discussed. Also, what changes were brought about under TCJA regarding changes in accounting methods and how it applies to Form 3115. Finally a “deep dive” into the Qualified Improvement Property “Fix” from the CARES Act will be examined.

7/21/20 Injured Spouse and Innocent Spouse: A Basic Overview: What is the difference? One is fairly straight forward and the other more difficult. Join us as we learn how to file and when to file for these two often confused IRS programs. We will spend some time on “equitable relief” as it related to innocent spouse.

7/22/20 Installment Agreements, OIC, & Payments: Installment agreements are simple and easier to implement than ever before. But, there are several things to consider concerning the type of agreement, how to qualify and more importantly keeping the agreement in force. How can you provide your client with a fresh start? We will discuss issues concerning Offer in Compromise – an overview on types of OIC, payment options, and how to calculate an amount that the IRS will agree to. What deductions are allowed? Join this discussion on implementing installment agreements that your client can adhere to and at the same time stay in compliance.

7/23/20 Volunteer Classification Settlement Program and the Independent Contractor vs. Employee: Save your client some money and headaches if you have repeatedly counseled them on the issue of employee vs. independent contractor. The Voluntary Classification Settlement Program may be the right choice to get your client into compliance with treating their workers as employees. Learn about the process, how to qualify for the program and examples of tax savings your client will benefit from. Be the hero for your client and show them the ins and outs of this IRS program, and gain a new client for payroll taxes.

Single session pricing: $22.50/hour

OR Take advantage of the Unlimited Package for $199.

![]() Basics & Beyond Resources

Basics & Beyond Resources

- Blog Page

- Resource List

- Webinar & Seminar Schedules

- Get Registered!

- Note: Paid attendees can request a link to the replay of any previously recorded webinar presentations by emailing us at [email protected]