Corporate Transparency Act

Can I refer all my LLC customers to a lawyer for the new “BOI” filing requirements and still be compliant?

You decide what forms you want to prepare. If you chose not to prepare the form, you would notify your clients. as such. I would recommend that you have something signed by the client that they acknowledge they received the information about CTA and their reporting requirements. One of my handouts can be adapted for that purpose.

Are inactive companies required to report. LLC was set up but is no longer in business.

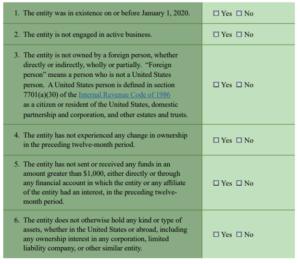

An entity qualifies for this exemption if all six of the following criteria apply:

Do non-profits have to file under the CTA?

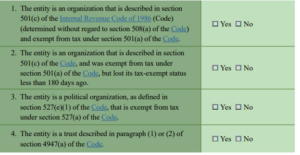

An entity qualifies for this exemption if any of the following four criteria apply:

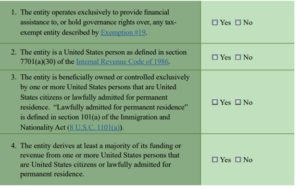

Entity assisting a tax-exempt entity (Exemption #20) An entity qualifies for this exemption if all four of the following criteria apply:

The textbook states that companies created before 1/1/24 have until 1/1/25 to report. Can you clarify?

The Reporting Rule requires that all “reporting companies” file BOI reports with FinCEN within the previously specified timeframes. A reporting company is any entity that meets the “reporting company” definition and does not qualify for an exemption. There are two categories of reporting companies: a “domestic reporting company” and a “foreign reporting company”. If your company is neither a “domestic reporting company” nor “foreign reporting company” because it does not meet either definition or it qualifies for an exemption, then it is not required to file a BOI report with FinCEN.

Unless otherwise specified, States and Indian tribes have the following meanings and the Reporting Rule. States means any State of the United States, the District of Columbia, the Commonwealth of Puerto Rico, the Commonwealth of the Northern Mariana Islands, American Samoa, Guam, the United States Virgin Islands, and any other commonwealth, territory, or possession of the United States. Indian tribes mean any Indian or Alaska Native tribe, band, nation, pueblo, village or community that the Secretary of the Interior acknowledges to exist as an Indian tribe. (See section 102 of the Federally Recognized Indian Tribe List Act of 1994 (25 U.S.C. 5130).

The Reporting Rule is effective on January 1, 2024. FinCEN will begin accepting BOI reports electronically through its secure filing system on this date. BOI reports will not be accepted prior to January 1, 2024. This chapter explains when your company should file its initial BOI report and how to do so in the following two sections:

If your company already exists as of January 1, 2024, it must file its initial BOI report by January 1, 2025.

If your company is created or registered to do business in the United States on or after January 1, 2024, and before January 1, 2025, it will have 90 calendar days after receiving actual or public notice that the company’s creation or registration is effective to file its initial BOI report. Specifically, this 90-calendar day deadline runs from the time the company receives actual notice that its creation or registration is effective, or after a secretary of state or similar office first provides public notice of its creation or registration, whichever is earlier. If your company is created or registered on or after January 1, 2025, it will have 30 calendar days from actual or public notice that its creation or registration is effective to file its initial BOI report. For example, your company may receive actual notice that its creation or registration is effective through a direct communication from the secretary of state or similar office. Your company could also receive public notice that its creation or registration is effective because it appears on a publicly accessible registry maintained by the secretary of state or similar office. Notice practices will vary by jurisdiction. If a jurisdiction provides both actual and public notice, the timeline for when an initial BOI report is due starts on the earlier of the two dates notice is received.

Are Partnerships and Sole Proprietorships that are not LLCs still subject to BOI?

Sole Proprietorships and General Partnerships are not required to report business ownership information because they are not registered legal entities. If the partnership as been registered with the Secretary of State then they would need to report. This would also include farms and Schedule E filers that are not LLC. If these entities are LLC’s there is a reporting requirement.

Is this an annual filing or only once/when changes happen?

This is a one-time filing. Then when changes occur those changes need to be reported. Once you are in the database, you need to update when changes occur within 30 days of change. We have provided a handout on this issue which requires the client to initial and sign acknowledging this time frame to update the information.

I was looking at the TCC application and they are asking for me to sign in with ID.me. I have one for my Social Security and my personal IRS Account.

Do I need to do a new one for the Firm or do I want to use what I have for other?

If you already have an existing ID.me or IRS account, you can access IRS tools and applications by selecting Sign in with ID.me or Sign in with an existing IRS username and completing additional steps.

What are the penalties for not filing the CTA reports?

It is 500 a DAY, UP TO 10,000 MAX

Why do they not just ask BOI questions directly on tax returns, like 1120 or 1120s?

This process is not an IRS process. It is controlled by FinCen and is required to report through their system.

Is a FinCen identifier needed to file this by an individual company?

No. FinCEN expects that many, if not most, reporting companies will be able to submit their beneficial ownership information to FinCEN on their own using the guidance FinCEN has issued. An individual or reporting company is not required to obtain a FinCEN identifier.

Some states are considering this a legal issue and have stated only attorneys can prepare the BOI report? Is a reporting company required to use an attorney or a certified public accountant (CPA) to submit beneficial ownership information to FinCEN?

No. FinCEN expects that many, if not most, reporting companies will be able to submit their beneficial ownership information to FinCEN on their own using the guidance FinCEN has issued. Reporting companies that need help meeting their reporting obligations can consult with professional service providers such as lawyers or accountants.

But we must follow state law if we are not an attorney. We do not want to be considered practicing Law when it is prohibited by Circular 230.

We are awaiting Iowa Bar Association Guidance. AICPA said “No” to filing BOI. AICPA has suggested “not preparing” BOI paragraph for inclusion in engagement letters & a notification flier to forward to clients. Check with your individual states to determine whether the issue is considered practicing law.

Am I correct in assuming that these provisions only apply to LLC’s and not any other business entities?

No, these provisions apply to corporations, S Corporation, LLC – which can be a partnership or a single member LLC. Also, any business that has registered with the Secretary of State.

Is it anticipated that the BOI reporting will be done in conjunction with the tax return prep as part of the software or will it be a governmental login? IF the latter, would firms be better off bouncing the responsibility to the owner to prepare?

The reporting will be done through FinCen. This is not IRS reporting. The current version of Ultra Tax does not incorporate this filing, Yet. But it may not since this is a separate one-time initial filing, then only required updates. You will need a login for FinCen. Honestly, if left to the client – it probably will be ignored.

So, is this a tax form or a form to be filed with the Secretary of State?

I assume you are discussing the Corporate Transparency Act. This will be filed through FinCen (Financial Crimes Enforcement Network. The FinCen database will use the Secretary of State information to compare what was reported. https://www.fincen.gov/ Form will be filed directly with FinCEN on their website.

A husband and wife each own 20% of a business entity. Are both treated as a beneficial owner because of their marriage?

NO, based on the final regulations there is no related party attribution requirements.

In the previous example, Barb did not appear to have significant influence over the operations and she did not own minimum 25%. So, is she deemed to have influence because her husband owns 80%.

NO, based on the final regulations there is no related party attribution requirements. But this would be based on a fact and circumstances as well.

Wouldn’t S corps and partnerships be exempt since they report ownership interests in their respective returns?

No, this is not an IRS issue. It is a FinCen issue.

If someone owns a tattoo shop, they are not an LLC and 2 people are owners but it does not show on anything. One is on the health license and the the other partner has all the bills and place of their business. How would that work for filing. Do they both have a 1099 as self-employment.

Technically, they have a partnership. If not an LLC, then they Tattoo shop would NOT have filing Requirement with CTA, they are not an LLC, S Corp or a Corporation, they are just a small business filing Sch C no registration with the state was necessary as they are not an LLC. There is no reporting requirement with the Corporate Transparency Act, If there are 2 owners, they should be a partnership – what are they. A partnership would be issuing K-1’s. If there are 2 owners, they cannot file Sch C.

Point of confusion on CTA – Is a trust considered an entity for this reporting? So that the trustee is the beneficial owner?

Note for trusts: a trustee of a trust or similar arrangement may exercise substantial control over a reporting company. The following individuals may hold ownership interests in a reporting company through a trust or similar arrangement:

- A trustee or other individual with the authority to dispose of trust assets.

- A beneficiary who is the sole permissible recipient of trust income and principal or who has the right to demand a distribution of or withdraw substantially all of the trust assets.

- A grantor or settlor who has the right to revoke or otherwise withdraw trust assets.

This is a facts and circumstance issue. Also, we need some additional guidance from the IRS on this issue.

Do you think many practitioners will put reference to the CTA compliance in their engagement letters?

Unknown, but just based on the issue that not everyone takes CPE – there will be many who have no idea about CTA. An engagement letter that addresses this is recommended.

Does a sole-proprietor/Schedule C filer need to file a CTA report? This may have been covered previously, and if so, my apologies for asking.

If they are not an LLC, then a sole proprietorship has no CTA filing requirement.

By what means are you reporting this information? Is there some type of form that has to be completed?

You are talking about CTA here. The form has not been released to the public and must be e-filed with no exceptions. It will be released January 1, 2024.

Do you have an example standard engagement letter amongst your printouts that addresses the CTA and the 2022 cryptocurrency question?

No but we did provide a series of handouts in hightail. They cover CTA and can be used as you see fit.

Going back to CTA, the required reporting to FINCEN……is this just onetime reporting requirement or would future reporting be required if there are changes to the required reporting companies such as changes in ownership, location, etc.?

CTA is just a one-time initial reporting. Then once that is done updates need to be made.

We have provided handouts for CTA which will assist in hightail.

Sole proprietorships that are not established as an LLC are exempt from the reporting requirements. Right?

That is correct.

I have a question about CTA. I have 8 Partnership LLC’s all only owned by husband & wife. Do I file a separate CTA for each since each is under a different name even though the same ownership.

All 8 partnerships will file a separate CTA.

Is a single member LLC… filing a Sch C required to file?

Yes, due to the fact it is an LLC they must file a CTA report.

If a partnership has a 99% limited partner, and therefore passive, do we have to list them?

I assume this is CTA – the answer is Yes, they must file.

In Ohio you have to file a use of Trade Name form but not as an LLC with the secretary of the state. Does this make the sole proprietor a Reporting Company?

I do not think so. If the initial formation of company requires a registration with the state than yes. register Trade Name, probably not.

See FinCEN small compliance found FinCEN.gov/boi

https://www.fincen.gov/boi/small-entity-compliance-guide

Employee Retention Credit

What is the audit period for ERC?

Here is the audit deadline for the seven quarters during which this credit was available.

- Q2 2020 — April 15, 2024

- Q3 2020 — April 15, 2024

- Q4 2020 — April 15, 2024

- Q1 2021 — April 15, 2025

- Q2 2021 — April 15, 2025

- Q3 2021 — April 15, 2027

- Q4 2021 — April 15, 2027

Please note that if IRS implements the § 7405(b) then Any portion of a tax imposed by this title which has been erroneously refunded (if such refund would not be considered as erroneous under § 6514 may be recovered by civil action brought in the name of the United States. This would generally not extend the statute for the return.

ERC- client hasn’t received ERC money and we understand that it’s “on hold” but how do we amend 2020 tax return if we don’t get a final answer until after April 15, 2024?

This is a hard one. Hopefully IRS will come out with guidance on this issue when they announce a settlement program. If not, you will have to make a decision. Note that an amended return will generally not extend the statute.

We have amended a client’s 1040 for 2020 related to the ERC funds received on their S Corp. The client is now getting a notice for interest charged back to the original filing deadline. Is this something we can request a waiver for? Obviously, the taxpayer could not have paid this on the original filing.

Interest is by statute and cannot be abated. We are still waiting for the ERC Settlement Program – which may or may not address this issue.

The client obtained ERC after being solicited by one of “those” firms. Contractor who due to mask requirements needed to provide workers on jobs with an additional total of one-hour breaks per day. Given that amounts to 12.5% of day does that satisfy more than 10% disruption of business requirement? I think it’s not that easy but please provide your thoughts if possible.

I would say NO – they would not qualify. They were not under a government shutdown. And there is nothing about gross receipts reduction. Plus, as I look at this again, contract labor – are not employees.If employees, they would still not qualify under the criteria that needs to be met.

We have a Scottsdale client who received over $1,200,000 from ERC. We could not see how he qualified. Advised to put back the money. Comment on the possible penalties.

You gave them the best advice. As for penalties, we need to wait for the ERC Settlement Program to see how or if IRS addresses this issue on penalties.

I read an article that the IRS may be less aggressive in addressing EIC credit fraud. Is that true?

At this point I would say this is wishful thinking.

Charitable Contributions/Donations

If their income does not cover the donation, can they carry it(donation) forward?

Yes, there is a carryforward provision. You can carryover your contributions that you are not able to deduct in the current tax year because they exceed your adjusted-gross-income limits. You can deduct the excess in each of the next 5 years until it is all used but not beyond that time.

Form 1099/IRIS System

If a client does not have 100% information for all their 1099NEC recipients, should we wait to file? I have clients who are usually missing one person’s tax id.

No, you need to file 1099 NEC with IRS by January 31, after that penalties can be assessed. File the stray later.

Is the TCC only for the person who is transmitting the 1099s or is it for each client that has to eFile the 1099?

You can be an issuer or a transmitter. A small business just filing for themselves can be a issuer. They would select issuer when applying.

If an accountant or tax preparer just wants to transmit the 1099’s which are f-filed through the IRIS system then they would select transmitter. They can then transmit to the client.

If we use CFS to eFile 1099s, does it use the FIRE system to where clients are not required to have an EIN and can use their SSN?

CFS uses the FIRE system.

Why would we move to IRIS if we could still use FIRE?

FIRE will be phased out over the next few years and IRIS expands its capability.

We can still use the FIRE system, correct?

That is correct. The FIRE system will be phased out over time, 3-5 years would be my guess.

Can you still use your SSN Number for filing 1099’s through the FIRE system?

Yes

We have the TCC and we file the 1099’s for our clients. We have many clients who are not required to have the EIN number and file it all under their SSN number. We use the FIRE system and have never had a problem filing their 1099’s under their SSN. We can still do that right? Just not through the IRIS System?

You should be able to use the SSN in IRIS.

How long does the IRIS application process take? Can I start it now and be able to file the 1099’s by January?

45 days

Kristy was talking about the TCC application and single member LLC’s are required to provide two responsible officials. This applies to me so as a result I had to include my spouse as an RO. What’s up with this requirement? I then had to enroll him in ID.ME and last I checked it was in pending status awaiting his signature. I found it to be a confusing process.

In the fine print, a one owner are only require to have one RO, I missed it first time around.

For 2023, can I still use my software to file 1099s?

Yes

Does IRIS complete the 1096 filing requirement? Or is it necessary to prepare and send 1096?

If you use IRIS no 1096 is needed.

For IRIS, must one apply to the IRS to obtain permission to e-file?

Yes, the book provides the process. First you must get a TCC code for IRIS.

Does this include 1096?

1096s are used only to paper file 1099 forms.

What happens if we filed the 1099’s Through the IRIS system for our client and then 2 days after we submitted the information, they tell us they missed one 1099 and we need to file another one. Can we still do that?

Yes

If I obtain a TCC number for my business, do I need to have my employees use my log on info or is there a way to give access to my employees?

As far as I know now – you would have to give employees log in information. Based on the program information there does not seem to be a way to delegate this authority. Maybe in the future.

Are you saying single member LLC without TIN should obtain one?

If the client wants to participate in IRIS – they will need an Employer Identification Number. If they have no 1099’s to file IRIS would not apply to them.

Cell Phone

Was the cell phone reimbursement under an accountable plan $60 a month? Or whatever amount is reasonable?

I assume this was the amount the business set as a reimbursement by the company. IRS has no stated amount. Must be reasonable.

Self-Employed Health Insurance

Will you still be able to deduct the Medicare insurance on your social security income for self-employment insurance deduction?

Yes, as long as you have a profit with the business, which has always been a requirement.

Social Security

Can I draw half of my husband Social Security and let my set until I turn 70, full retirement age will be 66 and 6 months. Which is coming soon!

You would have to address this issue with the Social Security Administration. Please call your local office. Use their search engine and put in “local office”. https://www.ssa.gov/locator/

Short-Term Rentals

When you pay a security deposit does that get, included or excluded from the Form 1099-MISC in the rental box?

Yes

If you do Air B&B very infrequently, can you opt for Hobby less direct expenses to avoid Sch C w/ SE?

No, hobby loss expenses were suspended with the Tax Cuts and Jobs Act from 2018-2025.

If a client owns a condo, uses a management company to handle bookings, and average time is less than 7days. What would I need to determine if it was Sch C or Sch E?

It would depend on what services were provided as discussed in the book. The services provided income would be a Sch C reporting and subject to self-employment taxes.

When pro-rating dual use property expenses, do you use the actual “rental days” or the “available for rent days”?

Depends on what method you use, “Tax Regular Method” or the Tax Court case of “Bolton”.

Is short term rental reported on Schedule C?

If services are provided, then Schedule C is required.

For a special event if you were to rent out for more than the FMV for 14 or less would it still be nontaxable?

I believe that 14-day rule would trump the excess FRV and the income would exclude. Another approach the IRS may take is that the FRV portion would be excluded, the excess would be characterized as income or gift.

The client purchased a bed and breakfast – business only – no real estate. They are keeping their current residence and operate the business on the weekends as they have bookings. Since they do not live in the bed and breakfast, do they have to allocate a portion of the lease, expenses, etc. to personal use? Would the IRS look at this as a second home, or would it look at it as a necessary expense to operate the business that they be there on the weekend?

Based on the information you have provided – I would consider this a business. BUT, it would depend on the intent and income as well. You will have to prove it is a business and not just a write-off. Do they make a profit in 3 out of five years? If all losses, IRS could look at as a hobby or a non-business.

If a partnership donates half of beef to a charity, is that also personal use? Or free gutter cleaning? If not, then why is the rental considered personal use?

Different code section, different rules relating to 280A rules and personal use.

If taxpayer owns a home and rents rooms out to her daughter and another college (at FMV) student, but visits a few days a month, can the income and expenses all be counted? My daughter pays for electric and gas utilities. The taxpayer lives out of state, only goes to do maintenance and visit daughter.

Daughter pays less than FMV, hence, this portion is hobby income. other roommate would be regular Schedule E. If daughter paid a discounted rate (up to 15% discount) then her portion of rental income could go on Schedule E. Since Daughter income is well below FMV, then this is considered hobby income reported on Form 1040, Schedule 1, Part 1.

PTIN

Do you need a new PTIN if you incorporate?

You only need a PTIN if you are a tax preparer who prepares a return for compensation. The type of entity you are does not enter into this. If you are a corporation, you should have an EIN – Employer Identification Number.

Is it easier to renew the PTINs on Pay.gov? I was having difficulty yesterday on [email protected]

Must be done through the PTIN app as far as I know.

Retirement

Page 15 of the textbooks says that you CAN make a QCD from a SEP or Simple IRA.

This applies to “inactive plans” only. While many IRAs are eligible for QCDs—Traditional, Rollover, Inherited, SEP (inactive plans only), and SIMPLE (inactive plans only) —there are requirements:

- You must be 70½ or older to be eligible to make a QCD.

- QCDs are limited to the amount that would otherwise be taxed as ordinary income.

- This excludes non-deductible contributions.

- The maximum annual amount that can qualify for a QCD is $100,000.00

- (Indexed starting in 2024).

- This applies to the sum of QCDs made to one or more charities in a calendar year.

- (If, however, you file taxes jointly, your spouse can also make a QCD from his or

- her own IRA within the same tax year for up to $100,000.)

- For a QCD to count towards your current year’s RMD, the funds must come out

- of your IRA by your RMD deadline, generally December 31.

- Contributing to an IRA may result in a reduction of the QCD amount you can deduct.

- (The aggregate amount of deductible IRA contributions you make to your IRA after you

- turn 70 1/2 will reduce the amount of the QCD that is not includible in your gross income.)

Are SEP IRA’s convertible to a Roth?

Yes

I have read that beneficiary ROTH IRA’s still have a RMD requirement, though not taxable if over 5 years. My colleague said no, you never take RMD from beneficiary ROTH IRA? Which is correct?

No RMD required for the ROTH IRA.

What happens to the RMD, if the beneficiary of an IRA, disclaims the IRA? Does the estate then have to take an RMD, or is the whole amount required to be distributed to the estate?

Wow, good question! I have no idea – I imagine it would depend on what beneficiary ends up with the money. It’ll go to someone at some point.

Miscellaneous

Do you think that the IRS will upgrade their system for E-filing so that they can do away with the annual MeF shutdown of the E-file system?

Not without funding, which will never be stable.

How would we best handle a situation where an LLC Member in an active business has been issued a W-2 in addition to a K-1 for their share of the annual net income, if the LLC Member has engaged us to prepare their 1040, other than letting them know that they shouldn’t be receiving a W-2 because they are an LLC Member?

Provide some education to the person. Declare it on the tax return and then backout the W-2 as a duplicate on Schedule 1 page 2 Line 24z. Report K-1 as should be. Did they take out taxes on Form W-2, then did they file Forms 941?

Another webinar I attended mentioned malpractice insurance may not want us to do this for our clients even if we did the LLC for them. Your thoughts?

This is correct, so I would check with my insurance provider.

If your principal place of business is your home, then do “home office rules” apply?

You are not required to use the office in the home rules if your business is run from your home. But if you choose you must meet the regular and exclusive rules. Review Publication 587.

Do you have a sample from your firm for a letter firing a client?

The letter has been loaded into “hightail” and can be downloaded. https://spaces.hightail.com/space/jvA8cS5oj6

Is the current amortization period for software 3 years? Did it used to be 5 years? When did it change, if so?

Software development expenses paid or incurred after 2021 are no longer deductible as research expenses. Instead, they must be amortized over a five-year period (15 years for foreign expenses). This is the development of software. Whereas “off the shelf” software where you buy the program is 3 years.

How is QCD reported on tax return?

QCDs are reported along with other distributions from an IRA account on IRS Form 1099-R. They are aggregated with other taxable distributions and reported on Lines 1 and 2 on Form 1099-R.Nowhere on Form 1099-R is the amount of QCDs indicated. You must supply that, and your software has a place to designate the distribution is a QCD. I would talk to the software provider for assistance.

Are state refunds taxable?

It depends on the state law.

Elderly Client scammed for 2 years by sending money overseas to a man to bring to the US. This woman took out over $700K out of her IRA. She now owes approx. 60K to IRS since she didn’t have taxes taken out. Is there any form of deduction like theft loss?

At this time, no – The Tax Cuts and jobs Act suspended theft loss from 2018-2025. Whether this provision will be extended is unknown.

If A & B had a Partnership, 50% each. If A buys out B, does this terminate the partnership? If so, Does A have to get a new EIN?

Once a partner leaves in a 2-person partnership, this will terminate the partnership. A final partnership return must be filed, and the EIN retired with that final return. The remaining partner is now a, one owner and must choose a business entity in which to operate. Depending on the entity, they may need a new EIN.

Consider a scenario where a taxpayer sells a dual use property. How would the capital gains be calculated, and are there any tax implications based on the proportion of business and personal use?

Capital gain would apply to business use. So, you will need to determine business vs. personal use and prorate accordingly between capital gain and personal use.

How long do you have to request an abatement of penalty for a first-time offense of not reporting income? Client prepared own return & did not include income from the 1099 R in 2015. She entered an installment plan, but owed money with her 2019 return, so the IRS ended the installment plan. She has since paid it off. Can we request an abatement?

I assume this is an understatement penalty which is not eligible for the first-time penalty abatement. Since it is 2015, it is out of statute – so a refund would be barred if a reasonable cause argument is approved to the 2 years from the tax is paid amount. If it was paid off in 2022 or 2023 you are limited to what was paid in those years as a refund.

The State of Iowa takes and condemns land of a clients on US Hwy 20 in SC. Can replacement property for this land be concrete added to land at this location?

No this would not qualify as replacement property.

If I find an error in a self-prepared return of a new client, do I need to amend that return? What if I have to amend that return for another issue?

10.21 requires you to notify the client of the error and its affect if any in the long term. The decision to amend is the clients choice not yours. If they do not want to amend, you must decide whether to keep the client or turn them away. I send a letter to the client with the information, identifying the error, how to fix and the penalties involved to reiterate your position and to protect yourself from a he said she said scenario. I would strongly suggest a discussion with the client concerning playing the audit lottery, and would also inform them that you will not perpetuate the error into future returns.

My business buys crypto @$5/unit. 3 months later FMV is $20.

I use crypto to buy advertising and am given $20/unit as currency. How do I report these two transactions?

You will have an expense for what crypto you used report on Schedule C and than a capital asset transaction reported on 8949.

TP passed away 1/22/22. Filed 1041 Sept 23 using 12/31/22 end of year. Distributions were made March 23. Can I amend 1041 creating a short year 1/22/22 to 4/30/22 after filing calendar year?

This would be a change in a calendar year filing. Once you have adopted your tax year, you may have to get IRS approval to change it. To get approval, you must file Form 1128. If you qualify for an automatic approval request, a user fee is not required. If you do not qualify for automatic approval, a ruling must be requested and a user fee is required. See the instructions for Form 1128 for information about user fees if you are requesting a ruling.

Do you have to cancel a corporation due to death of a sole owner.

It would be business prudent to take this course of action.

I have a client that is selling many items stored in her home which she considers “Collections” but most of the items sold at a loss. She wishes to record these items as a business on Schedule C. A painting sold for $50,000 but she only paid $3,000 – what schedule should this be recorded.

Schedule D – capital gain.