How to Navigate IRS Form 4797 and the Sale of Business Assets

Whether you’re an enrolled agent, a CPA, or a dedicated tax preparer, there’s one thing that holds true come tax time: preparing a client’s tax returns is rarely simple. Depending on the client, there may or may not be a big stack of forms, tables, and spreadsheets that you’ll have to navigate. Some clients bring you the proverbial shoebox full of receipts and expect you to simply go through them and sort out their entire prior year’s transactions. Others simply have no records whatsoever, and don’t know where to even begin.

When you’re working with a business, though, there’s one thing that often throws a wrench in the works for a tax preparer, even if the client has kept excellent and highly detailed records. We’re talking about the sale of business assets, and the accompanying IRS form 4797 that goes along with them.

There are plenty of complicated and often dreaded IRS tax forms out there, but form 4797 stands apart from the crowd as a particularly challenging form to understand. Simply looking at IRS form 4797 itself on the IRS website, you might be surprised to hear this. After all, it’s only two pages long, and it looks fairly straightforward at first glance. As it turns out, though, trying to determine which assets belong on which part of the form can quickly become a bt of a headache.

At Basics & Beyond™, we always encourage accounting and tax professionals to keep up with their ongoing tax education and training with online taxation courses. It’s not just that these CPE hours are required by law in the vast majority of states — it’s also a matter of keeping yourself up to date so that you can offer top tier services to your clients. Learning more about the 2018 tax reform bill with a tax reform webinar, for example, is an excellent way to ensure that you’re prepared to help your clients navigate the coming tax season with minimal bumps in the road.

When it comes to something like IRS form 4797, though, we place particular emphasis on just how helpful an online taxation course can be. While the guide below is a helpful introduction to form 4797, it doesn’t take the place of an in-depth webinar taught by one of our accounting experts. We highly recommend signing up for a webinar today in addition to reviewing the material below.

With that in mind, the following guide to IRS form 4797 will cover the following topics:

- Overview of IRS form 4797

- How to determine amount realized and tax basis

- Where different types of property belong on form 4797

- IRC section 1231, 1245, and 1250 property

Ready to learn more about IRS form 4797? Let’s get started.

IRS Form 4797 Overview

Before we go any further with reviewing and understanding form 4797, it’s a good idea to take a moment to discuss what it is and what it’s used for.

Put simply, IRS form 4797 is a tax form that’s used specifically for reporting the gains or losses made from the sale or exchange of certain kinds of business property or assets. The types of property that often show up on form 4797 include things like property used for generating rental income, as well as property that’s employed as part of industrial or agricultural enterprises.

If you sell a home that you were renting out full-time, for instance, you will likely need to report any gains or losses on form 4797. The same goes for the sale of a house that you were using strictly for business purposes. Similarly, any gains or losses coming from the sale of natural resources such as minerals, gas, or oil will need to be included on form 4797. However, the sale of property — such as a home — which was used for both business purposes and as a primary residence may not need to be reported on form 4797. This is because any gains from such a sale could be eligible for capital gains tax exclusion.

So far, so good, right? On the surface, it seems like all you need to do is calculate whether a gain or loss was realized on a particular piece of property, whether or not that property is subject to tax treatment via form 4797, and then report it if need be.

When you drill down a little bit, though, things quickly become more complicated. When you go to fill out the form, one of the first things that will occur to you is the need to calculate the actual capital gain itself. If you were to purchase a piece of property and immediately sell it for more than it’s worth — literally the same day, perhaps — then determining this calculating would be pretty straightforward. However, this kind of scenario is rarely the case in real life. Instead, it’s common to have claimed depreciation on an asset over the course of a number of years by the time you go to sell it and calculate any gains or losses and taxes due from the sale. That’s where calculating the amount realized and tax basis comes in.

Calculating Amount Realized and Tax Basis

In order to determine how much of a gain or loss you might need to report on IRS form 4797, you’ll to do a bit of math.

First off, you’ll have to calculate the so-called “amount realized” for the sale of the asset. This isn’t as simple as taking into account the sales price. Instead, calculating the amount realized involves determining and taking into account each of the following:

- The total of all money received from the buyer for the asset in question

- The fair market value of the property or services received by the buyer

- Any liabilities associated with the property which the buyer has assumed

- Any liabilities that the asset in question might be subject to, such as real estate taxes or an outstanding mortgage

Once you’ve taken all of those items into considering, you’ll know the total amount realized for the asset that you’ve sold.

Now, you’ll need to deduct the “cost basis” from the amount realized in order to determine whether or not there has been a gain or loss in connection with the sale of the asset in question. Take note: the cost basis isn’t just the amount that you originally paid for the item. Calculating the cost basis is significantly more complicated than that, in fact.

When determining the cost basis of an asset, you’ll need to start with the original cost of the item. Then, you’ll add and/or subtract other amounts from this initial cost in determining the final cost basis.

The following amounts should be added to the original costs, as “increases to basis.” These are things which you can consider as added expenses, and which therefore increased the overall cost of owning the asset:

- Capital improvements to the asset

- Any assessments for local improvements

- Legal fees

- Zoning costs

- Restoration in the event of property damage

Once the above are taken into account, the cost basis of your asset may be significantly higher. Before you can proceed any further, though, you’ll also need to deduct the following “decreases to basis” from the cost of the asset:

- Insurance reimbursements

- Bonus depreciation and section 179

- Credits

- Refunds

- Regular depreciation and amortization

Depreciation in particular will likely have a large impact on the overall cost basis of your asset, particularly for an item that is relatively old and has accumulated depreciation over the course of a number of years.

Once you’ve added and subtracted the above amounts, you can subtract the total cost basis from the amount realized. Whatever you come up with, you’ll need to report that gain or loss on form 4797.

Property Types and Form 4797 Parts I, II and II

If you’ve been following along up until this point, you’ve got a gain or loss in mind that you’re ready to report on form 4797. The question is, though: where does it go?

IRS form 4797 is comprised of three parts. Depending on the type of asset you’re claiming, you’ll need to account for the asset in either part I, part II, or part III. When you look at each part of the form, though, you’re directed to the IRS form 4797 instructions to determine what type of property belongs in that section. And a quick look at the instructions will reveal that they’re relatively complicated.

In order to simplify things, we’ll break down each of the parts according to particular property types.

- Depreciable Tangible Trade or Business Property

- If sold at a gain and held for one year or less, report in part II

- If sold at a gain and held for more than one year, report in part III (1245)

- If sold at a loss and held for one year or less, report in part II

- If sold at a loss and held for more than one year, report in part I

- Depreciable Real Trade or Business Property

- If sold at a gain and held for one year or less, report in part II

- If sold at a gain and held for more than one year, report in part III (1250)

- If sold at a loss and held for one year or less, report in part II

- If sold at a loss and held for more than one year, report in part I

- Farmland Held Less than 10 Years With Soil, Water, or Land Clearing Expenses Deducted

- If sold at a gain and held for one year or less, report in part II

- If sold at a gain and held for more than one year, report in part III (1252)

- If sold at a loss and held for one year or less, report in part II

- If sold at a loss and held for more than one year, report in part I

- Real or Tangible Trade or Business Property Deducted Under the De Minimis Safe Harbor

- If sold at a gain, report in part II regardless of how long property was held for

- All Other Farmland Used in Trade or Business

- If held for one year or less, report in part II

- If held for more than one year, report in part I

- Cost Sharing Property, Section 126

- If held for one year or less, report in part II

- If held for more than one year, report in part III (1255)

- Cattle and Horses Used in Trade or Business for Draft, Breeding, Sporting, or Dairy

- If sold at a gain and held for less than 24 months, report in part II

- If sold at a gain and held for more than 24 months, report in part III (1245)

- If sold at a loss and held for less than 24 months, report in part II

- If sold at a loss and held for more than 24 months, report in part I

- If cattle and horses raised and sold at a gain after holding for less than 24 months, report on part II

- If cattle and horses raised and sold at a gain after holding for more than 24 months, report on part I

- Livestock Other than Cattle and Horses Used in a Trade or Business for Draft, Dairy, Sporting, or Breeding

- If sold at a gain and held for less than 12 months, report in part II

- If sold at a gain and held for more than 12 months, report in part III (1245)

- If sold at a loss and held for less than 12 months, report in part II

- If sold at a loss and held for more than 12 months, report in part I

- If raised livestock sold at a gain after holding for less than 12 months, report on part II

- If raised livestock sold at a gain after holding for more than 12 months, report on part I

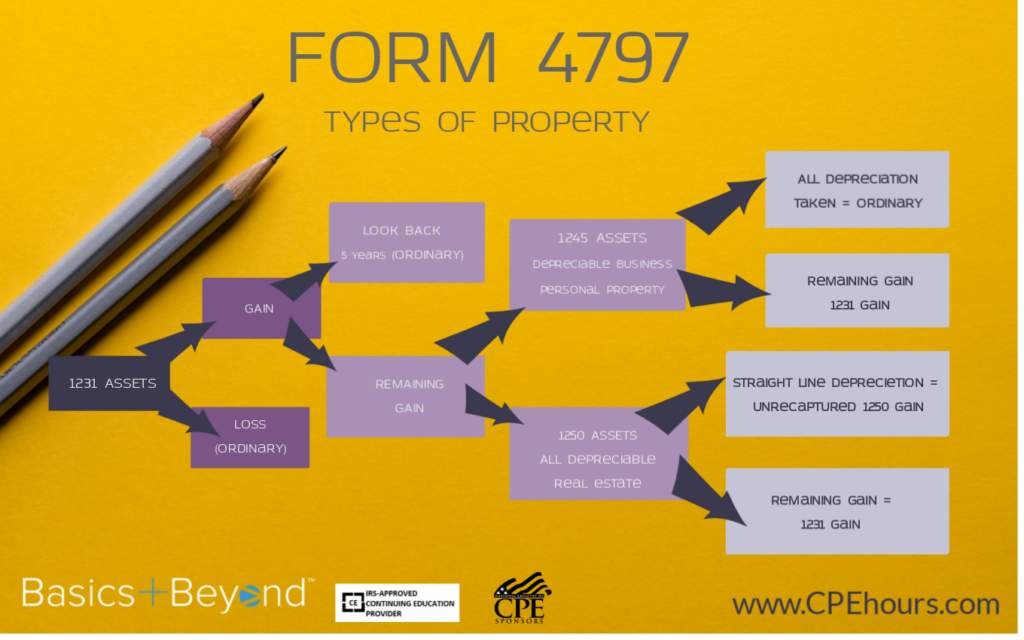

IRC Section 1231 vs. 1245 vs. 1250 Property

Once you’ve determined where a particular type of property belongs on the form, you can account for gains and losses there. However, this is where things can become even more complicated.

Generally speaking, the best section under which to account for the sale of business assets is as section 1231 property. This type of property allows net losses to be fully deductible as ordinary losses, while capital gain treatment occurs when an asset is sold as a gain.

Meanwhile, you’ll notice that certain types of property above must be reported under part III of IRS form 4797 as either 1245 or 1250 property. So, what’s the difference?

Put simply, section 1231 regulated the tax treatment of both gains and losses of depreciable property that’s been held for more than a year in a trade or business. Meanwhile, sections 1245 and 1250 include rules for recapturing depreciation applying to gains from dispositions.

Things get complicated, though, when you have to account for 1231 losses from prior years. This is because capital gains treatment for the current year under section 1231 is limited, and you could end up with ordinary income as a result.

Online Taxation Course

Determining whether you have ordinary gains or a capital gains — and whether you may end up with ordinary income as a result of previous 1231 losses — can quickly become tricky. In order to fully understand the in’s and out’s of these kinds of details on IRS form 4797, we highly recommend signing up for an online taxation course. Here at Basics & Beyond, we offer affordable, entertaining, and engaging online tax webinars on a range of topics, including form 4797. To browse our upcoming webinar schedule, click here!