Tax Newsletter: Are you Prepared for the May 17, 2021 Tax Deadline?

In This Issue:

Additional guidance on the New American Rescue Plan Act of 2021

New webinars coming in June! In the meantime, check out our webinar schedule.

Key Things to Act on at this Time:

- Changes between and House and Senate are discussed.

- Hold all returns, if possible, that have not been e-filed or paper filed where unemployment is present and software is updated. If the return has been signed it must be e-filed within the guidelines. IRS appears to have changed its mind on how the calculation is to be structured. The original IRS guidance said to include unemployment income when calculating the $150,000 modified adjusted gross income (AGI) limitation.

On March 23, 2021, the IRS provided updated instructions for the unemployment compensation exclusion worksheet which now states modified AGI does NOT include unemployment compensation.

IRS believes it can correct all returns filed with this issue through their math error authority – so no need to amend. The IRS will refigure the taxes using the excluded unemployment compensation amount and adjust the tax account accordingly. The IRS will send any refund amount directly to the taxpayer. BUT beware and check notices to make sure other adjustments are taken into account if needed such as Earned Income Tax Credit.

- EIDL Loans have been reactivated.

- Restaurants May Have a Chance at Grants Under the New Restaurant Revitalization Grant Program – we await guidance from SBA.

As we get down to the current May 17, 2021 tax deadline we may or may not have guidance on the issues presented here.

Issue 1: IRS Delivering Round 3 of Stimulus Checks

No action is needed by most taxpayers; the payments will be automatic and, in many cases, similar to how people received the first and second round of Economic Impact Payments in 2020. In general, most people will get $1,400 for themselves and $1,400 for each of their qualifying dependents claimed on their tax return. Remember the payments can be in the form of:

- Direct deposit

- Debit card or

- Check

Issue 2: 2020 Recovery Rebate Credit – Correcting Issues After the 2020 Tax Return Has Been Filed

- Q1: The client is eligible for a 2020 Recovery Rebate Credit but did not claim it on the 2020 return. Do they need to file an amended return?

- A1: If the client did not claim the credit on the original tax return, they will need to file an Amended U.S. Individual Income Tax Return, Form 1040-X. The IRS will not calculate the 2020 Recovery Rebate Credit for them if they did not enter any amount on the original tax return.

- DO NOT file an amended tax return if the client entered an incorrect amount for the 2020 Recovery Rebate Credit on the tax return. If an amount was entered on line 30 but a mistake was made in calculating the amount, the IRS will calculate the correct amount of the 2020 Recovery Rebate Credit, make the correction to the tax return and continue processing the return. If a correction is needed, there may be a slight delay in processing the return and the IRS will send a notice explaining any change made.

Issue 3: Tax Day End of Filing Season Extended to May 17, 2021

Treasury and IRS announced that the federal income tax filing due date for individuals for the 2020 tax year will be automatically extended from April 15, 2021, to May 17, 2021.

This postponement applies to individual taxpayers, including individuals who pay self-employment tax.

- No need to file forms or call for this automatic relief.

- Postponing federal tax payments.

- This does not apply to estimated tax payments which are still due on April 15, 2017.

- State tax returns – check your state for an update.

- Individual taxpayers can also postpone federal income tax payments for the 2020 tax year due on April 15, 2021, to May 17, 2021, without penalties and interest, regardless of the amount owed. This postponement applies to individual taxpayers, including individuals who pay self-employment tax.

- Penalties, interest and additions to tax will begin to accrue on any remaining unpaid balances as of May 17, 2021. Individual taxpayers will automatically avoid interest and penalties on the taxes paid by May 17.

Many States Jumping on The Extended Season Bandwagon – Please review Notices as Some States have other Rules Associated with the Extended Dates

NOTE: Many still require Estimated Payments by April 15, 2021 and times vary concerning when penalties and interest start to accrue. In addition, this is current as of April 1, 2021 and subject to change.

Issue 4: New Unemployment Guidance Exclusion up to $10,200 if Requirements are Met.

If modified adjusted gross income (AGI) is less than $150,000, the American Rescue Plan enacted on March 11, 2021, excludes from income up to $10,200 of unemployment compensation paid in 2020, which means the client does not have to pay tax on unemployment compensation of up to $10,200.

If married, each spouse receiving unemployment compensation does not have to pay tax on unemployment compensation of up to $10,200. Amounts over $10,200 for each individual are still taxable. If the modified AGI is $150,000 or more, the client cannot exclude any unemployment compensation.

The exclusion should be reported separately from the unemployment compensation.

When figuring the following deductions or exclusions from income, if asked to enter an amount from Schedule 1, line 7 enter the total amount of unemployment compensation reported on line 7 (unreduced by any exclusion amount) and if asked to enter an amount from Schedule 1, line 8, enter the amount from line 3 of the Unemployment Compensation.

If the client’s return has already been filed there is no need to file an amended return (Form 1040-X) to figure the amount of unemployment compensation to exclude. The IRS will refigure the tax using the excluded unemployment compensation amount and adjust accordingly.

Unemployment Compensation Exclusion Worksheet – Schedule 1, Line 8

- If filing Form 1040 or 1040-SR, enter the total of lines 1 through 7 of Form 1040 or 1040-SR. If filing Form 1040-NR, enter the total of lines 1a, 1b, and lines 2 through 7.

- Enter the amount from Schedule 1, lines 1 through 6. Do not include any amount of unemployment compensation from Schedule 1, line 7 on this line.

- Use the line 8 instructions to determine the amount to include on Schedule 1, line 8, and enter here. Do not reduce this amount by the amount of unemployment compensation that may be able to exclude.

- Add lines 1, 2, and 3.

- If filing Form 1040 or 1040-SR, enter the amount from line 10c. If filing Form 1040-NR, enter the amount from line 10d.

- Subtract line 5 from line 4. This is the modified adjusted gross income.

- Is the amount on line 6, $150,000 or more?

[] Yes. Stop The client cannot exclude any of the employment compensation

b. [] No. Go to line 8. - Enter the amount of unemployment compensation paid to the client in 2020. Do not enter more than $10,200.

- If married filing jointly, enter the amount of unemployment compensation paid to the spouse in 2020. Do not enter more than $10,200. If filing Form 1040-NR, enter -0- .

- Add lines 8 and 9 and enter the amount here. This is the amount of unemployment compensation excluded from income.

- Subtract line 10 from line 3 and enter the amount on Schedule 1, line 8. If the result is less than zero, enter it in parentheses. On the dotted line next to Schedule 1, line 8, enter “UCE” and show the amount of unemployment compensation exclusion in parentheses on the dotted line. Complete the rest of Schedule 1 and Form 1040, 1040-SR, or 1040-NR.

Issue 5: IRS Resumes Delinquent Debt/Passport Certification Program

IRS is open and processing mail, tax returns, payments, refunds and correspondence. However, COVID-19 continues to cause delays in some of their services. The service delays include:

- Live phone support.

- Processing tax returns filed on paper.

- Answering mail from taxpayers.

- Reviewing tax returns, even for returns filed electronically.

International Mail Disruption and Form SSA-1099

If your client lives outside of the United States and receive Social Security Benefits, they may not receive Form SSA-1099 due to the temporary suspension of International mail to some locations. If they did not receive Form SSA-1099 or Form SSA-1042S, they may access the information through the SSA website.

Issue 6: What You Need to Know about Repayment of Deferred Payroll Taxes

The Coronavirus, Aid, Relief and Economic Security Act allowed employers to defer payment of the employer’s share of Social Security tax. IRS Notice 2020-65 allowed employers to defer withholding and payment of the employee’s Social Security taxes on certain wages paid in calendar year 2020. Employers must pay back these deferred taxes by their applicable dates.

The employee deferral applied to people with less than $4,000 in wages every two weeks, or an equivalent amount for other pay periods. It was optional for most employers, but it was mandatory for federal employees and military service members.

Repayment of the employee’s portion of the deferral started Jan. 1, 2021, and will continue through Dec. 31, 2021. Payments made by Jan 3, 2022, will be timely because Dec. 31, 2021, is a holiday. The employer should send repayments to the IRS as they collect them. If the employer does not repay the deferred portion on time, penalties and interest will apply to any unpaid balance.

Employers can make the deferral payments through the Electronic Federal Tax Payment System (EFTPS) or by credit or debit card, money order or with a check. These payments must be separate from other tax payments to ensure they are applied to the deferred payroll tax balance. IRS systems won’t recognize the payment if it is with other tax payments or sent as a deposit. EFTPS will soon have a new option to select deferral payment. The employer selects deferral payment and then changes the date to the applicable tax period for the payment.

If the employee no longer works for the organization, the employer is responsible for repayment of the entire deferred amount. The employer must collect the employee’s portion using their own recovery methods.

Issue 7: IRS Provides Guidance for Employers Claiming the Employee Retention Credit for 2020 as well as Eligibility Rules for PPP Borrowers

Guidance has been issued for employers claiming the employee retention credit under the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), as modified by the Taxpayer Certainty and Disaster Tax Relief Act of 2020 (Relief Act), for calendar quarters in 2020. Notice 2021-20 has similar information in the FAQ’s IRS has put out and also provides clarifications and describes retroactive changes under the new law applicable to 2020, primarily relating to expanded eligibility for the credit.

For 2020, the employee retention credit can be claimed by employers who paid qualified wages after March 12, 2020, and before January 1, 2021, and who experienced a full or partial suspension of their operations or a significant decline in gross receipts.

The credit is equal to 50% of qualified wages paid, including qualified health plan expenses, for up to $10,000 per employee in 2020. The maximum credit available for each employee is $5,000 in 2020.

PPP Loan Changes

A significant change for 2020 made by the Relief Act permits eligible employers that received a Paycheck Protection Program (PPP) loan to claim the employee retention credit, although the same wages cannot be counted both for seeking forgiveness of the PPP loan and calculating the employee retention credit. Notice 2021-20 explains when and how employers that received a PPP loan can claim the employee retention credit for 2020.

The Notice also provides answers to questions such as:

- Who are eligible employers?

- What constitutes full or partial suspension of trade or business operations?

- What is a significant decline in gross receipts?

- How much is the maximum amount of an eligible employer’s employee retention credit.

- What are qualified wages?

- How does an eligible employer claim the employee retention credit and

- How does an eligible employer substantiate the claim for the credit?

While the Relief Act also extended and modified the employee retention credit for the first two calendar quarters in 2021, Notice 2021-20 addresses only the rules applicable to 2020. The IRS plans to release additional guidance soon addressing the changes for 2021.

Issue 8: The American Rescue Plan Act (PL 117-2) Enhanced Child and Dependent Care Credit for Tax Year 2021 ONLY – Good Overview of the Credit in General and Law Changes

The credit is available for expenses a client pays for the care of qualifying individual(s) under the age of 13 so that the client can be gainfully employed.

For a care expense to qualify for the credit, the expense must be “employment-related,” i.e., it must enable the client and spouse to work, and it must be for the care of the child, stepchild, or foster child, or a brother or sister or step-sibling (or a descendant of any of these), who’s under 13, lives in the home for over half the year, and doesn’t provide over half of his or her own support for the year. The expense can also be for the care of the spouse or dependent who is handicapped and lives with the client for over half the year.

The cost of household services, e.g., domestic help, can also qualify as long as the cost at least in part goes towards the care of the individual.

The typical expenses that qualify for the credit are payments to a day-care center, nanny, or nursery school. Sleep-away camp does not qualify. The cost of kindergarten does not qualify because it’s primarily an education expense. However, the cost of before and after school programs may qualify as care expenses.

To claim the credit, married couples must file a joint return. For purposes of this rule, a valid same-sex marriage that is authorized under state or foreign law is recognized, but a registered domestic partnership or a civil union is not.

The 2021 credit is refundable as long as either the client or the spouse has a principal place of abode in the U.S. for more than one-half of the tax year.

The client also must provide the care-giver’s name, address, and social security number (or tax ID number if it’s a day-care center or nursery school). A day-care center must be in compliance with state and local regulations.

You also must include on the return the social security number of the children who receive the care. There is no credit without the social security number. Omission of the social security numbers while still claiming the credit will result in a summary assessment of tax liability.

When calculating the credit, several limits apply:

First, qualifying expenses are limited to the income the client or spouse earns from work, self-employment, or certain disability and retirement benefits—using the figure for whichever of them earns less. Under this limitation, if one of the individuals has no earned income, they will not be entitled to any credit.

However, under certain conditions, when one spouse has no actual earned income and that spouse is a full-time student or disabled, the spouse is considered to have monthly income of $250 (if the couple has one qualifying individual) or $500 (two or more qualifying individuals).

For 2021, the first $8,000 (increased from $3000) if the client has one qualifying individual, or $16,000 (up from $6000) if they have two or more qualifying individuals, of care expenses generally qualifies for the credit.

However, if the employer has a dependent care assistance program under which the client participates, they receive benefits excluded from gross income, the qualifying expense limits ($8,000 or $16,000) are reduced by the excludable amounts received.

Scenario 1: George pays $8,400 in qualified employment related expenses in 2021 to care for his two children while he is working. The children are both qualifying individuals.

George can take the entire $8,400 into account in calculating the child and dependent care

credit. For tax years other than 2021, the maximum amount of qualified employment related expenses that George could take into account for purposes of determining the credit would be $6,000.

The Calculation

The credit will be computed as a percentage of the client’s qualifying expenses depending on their AGI. The applicable percentage of qualifying expenses has been increased to 50% for 2021 (from 35%) but is reduced by 1% for each $2,000 (or fraction thereof) by which the AGI for 2021 exceeds $125,000 (up from $15,000). If the AGI is $125,000 or less, the maximum amount of the credit is $4,000 ($8,000 x 50%) for taxpayers with one qualifying individual and $8,000 ($16,000 x 50%) for individuals with two or more qualifying individuals.

New for the 2021 tax year is a further phaseout of the credit for high income individuals. The phaseout percentage is 20% (instead of 50%) reduced (but not below zero) by 1 % for each $2,000 (or fraction thereof) by which AGI for 2021 exceeds $400,000.

To summarize. the applicable percentage is 50% for clients with AGI of $125,000 or below. The applicable percentage decreases one percent for every $2,000 (or fraction thereof) by which the client’s AGI exceeds $125,000 until AGI reaches $185,000. The applicable percentage is 20% for clients with AGI greater than $185,000 but not greater than $400,000. For clients with AGI above $400,000, the applicable percentage again decreases one percent for every $2,000 (or fraction thereof). Thus, for clients with AGI greater than $440,000, the credit is phased out completely.

Scenario 2: Assume the same facts as in Scenario 1 but George has an AGI of $122,000. His applicable percentage is 50% and his credit mount if $4,200 ($8,400 X50%). Had George’s AGI been $132,000, his applicable percentage would be 46% and the credit amount would be $3,864 ($8,400 x 46%).

Scenario 3: Assume the same facts as introduced in Scenario 1. George’s AGI is $420,000. His applicable percentage is 10% (20% -($20,000/$2,000 X 1%) and his allowable credit is $840 ($8,400 x 10%).

Note that a credit reduces the tax bill dollar for dollar. Thus, in Scenario 2, George pays $4,200 (or $3,864 with AGI of $132,000) less in taxes by virtue of the credit.

Issue 9: Improvements and Expansion to the Earned Income Credit

For tax years beginning in 2021 only, ARPA expands and increases the EITC for clients with no qualifying children:

- Age requirements are broadened. The pre-ARPA requirement that a client with no qualifying children must be over 24 but under 65 years old to claim the EITC does not apply for tax year 2021. Instead, under ARPA, taxpayers with no qualifying children (other than students, see below) must be at least 19 years old, and there is no upper age limit.

- Students (other than “qualified foster youths” or “qualified homeless youths”) must be at least 24 years old. Qualified foster youths and qualified homeless youths must be at least 18.

- Increased maximum amount of credit and increased phaseout amounts. The pre-ARPA EITC for clients with no qualifying children for 2021 could be up to $543 if neither the client’s earned income nor their adjusted gross income (AGI) exceeded $8,800 ($14,820 for joint filers).

- Under ARPA, the 2021 EITC of a taxpayer with no qualifying children can be as much as $1,502 if neither the client’s earned income nor their AGI exceeds $11,610 ($16,610 for joint filers).

Individuals May Base Their 2021 EITC on 2019 Earned Income

The EITC equals a percentage of the client’s “earned income” for the year—wages, salaries, tips, and other compensation, as well as self-employment income. Under ARPA, in determining their EITC for 2021, taxpayers may use the greater of their 2019 or 2021 earned income.

This ARPA change applies only to the 2021 tax year. For joint returns, the taxpayer’s earned income for 2019 is the sum of each spouse’s earned income for 2019.

Client’s May Have Up to $10,000 of “Disqualified” (Investment) Income and Still Claim EITC

Under pre-ARPA law, a client who had “disqualified income” (certain types of investment income) over an inflation-adjusted amount ($3,650 for 2021) for the year could not claim the EITC. Under ARPA, the threshold amount for disqualified income increases to $10,000, effective for tax years beginning after 2020. This $10,000 amount will be adjusted for inflation after 2021.

EIC Available Even if Identification Requirements Not Met

The EITC cannot be claimed for a qualifying child unless the client provides the qualifying child’s name, age, and the identification number (TIN—generally, a Social Security number). A pre-ARPA rule said that a client who would have been able to claim the EITC for a qualifying child but could not do so because the above identification requirements were not met, could not claim the EITC that applies for clients with no qualifying children.

ARPA removes that rule, effective for tax years beginning after 2020. This means that if an otherwise eligible individual has qualifying children, but cannot provide proper identification for them, the individual is eligible for the EITC that applies for individuals who have no qualifying children.

EITC Rules Under Which Certain Separated Married People Need Not File Jointly, Are Liberalized

One requirement for claiming the EITC, that applies subject to exceptions, is that married taxpayers must file jointly. Pre-ARPA law provided an exception to the joint-return-filing requirement for individuals who were married but separated, and who met certain requirements, including living with a qualifying child and not living with the spouse during the last six months of the tax year.

Effective for tax years beginning after 2020, ARPA liberalizes the rules under which certain separated married people need not file jointly to claim the EITC. Under these new rules, as an alternative to meeting the requirement that the spouses not live together for the last six months of the year, if the client has a decree, instrument, or agreement (other than a decree of divorce) and is not a member of the same household with his or her spouse by the end of the tax year, a joint return need not be filed (assuming the other requirements, such as having a qualifying child, are met).

Application of the Earned Income Tax Credit to U.S. Possessions

Before ARPA, the EITC was not available to individuals in the following U.S. commonwealths and territories: Puerto Rico, U.S. Virgin Islands, Guam, the Commonwealth of the Northern Mariana Islands, and American Samoa.

Under ARPA, beginning in 2021, the EITC will apply in the above commonwealths and territories.

Issue 10: Temporary Expansion of the Child Tax Credit for 2021

Under pre-ARPA law, the CTC was $2,000 per “qualifying child.” A qualifying child was defined as an under-age-17 child whom the client could claim as a dependent (i.e., a child related to the client who, generally, lived with them for at least six months during the year), and who was a U.S. citizen or national, or a U.S. resident.

The $2,000 CTC was phased out (reduced) if the modified adjusted gross income (AGI) was over $200,000, or over $400,000 if the client filed jointly, at a rate of $50 per $1,000 (or part of a $1,000) by which modified AGI exceeded the threshold amount.

The CTC was also partially refundable—to the extent of 15% of the earned income in excess of $2,500. An alternative formula for determining refundability applied for clients with three or more qualifying children. But, the maximum refundable credit for 2021 was $1,400 per qualifying child.

A $500 nonrefundable credit (per dependent) (so called “family credit”) is also allowed for each qualified dependent who is not a qualifying child under the CTC definition.

Child Tax Credit Temporarily Expanded for 2021

For 2021, ARPA expands the CTC as to eligibility and amount, as follows:

(1) The definition of a qualifying child is broadened to include 17-year-olds (i.e., children who haven’t turned 18 by the end of 2021).

(2) The CTC is increased to $3,000 per child ($3,600 for children under age 6 as of the close of the year). But the increased credit amounts are subject to their own phase-out rule.

So, for 2021, the CTC is subject to two sets of phase-out rules:

- The increased CTC amount (the $1,000 or $1,600 amount) is phased out for clients with modified AGI of over $75,000 for singles, $112,500 for heads-of-households, and $150,000 for joint filers and surviving spouses; and

- After applying the phase-out rule to the increased amount, the remaining $2,000 of CTC is subject to the existing phase-out rules (i.e., the $2,000 of credit is phased out for clients with modified AGI of over $200,000/$400,000 for joint filers).

- If the client is not eligible to claim an increased CTC in 2021, they can still claim the regular $2,000 CTC, subject to the existing phase-out rules.

(3) The CTC is fully refundable for 2021 for a client (either spouse for a joint return) with a principal place of abode in the U.S. for more than one-half of the tax year, or for a taxpayer who is a bona fide resident of Puerto Rico for the tax year.

A member of the U.S. Armed Forces stationed outside the U.S. while serving on extended active duty is treated as having a principal place of abode in the U.S.

The phase-out rules apply regardless of refundability, and the $500 family credit for dependents other than qualifying children remains nonrefundable.

Advance Payments of the 2021 CTC

IRS must establish a program to make monthly (periodic) advance payments (generally by direct deposits) which in total equal 50% of IRS’s estimate of the eligible clients 2021 CTC’s. These payments will be made in July 2021 through December 2021. To determine the advance CTC payments, IRS will look at the 2020 return, or, if it’s not yet filed, the 2019 return.

If the client receives advance CTC payments that are in excess of the CTC actually allowable to them for 2021, they have to repay those excess amounts (by increasing the tax liability reported on the 2021 returns).

For certain low- and moderate-income clients, the excess may be reduced by a safe harbor amount, limiting the amount by which they will have to increase tax liability, and allowing them to keep a portion of the excess amount.

Application of the CTC in U.S. territories

For 2021, the CTC is made fully refundable for clients who are Puerto Rico bona fide residents for the tax year, claimed by filing a tax return with the IRS. But IRS won’t make advance payments to residents of Puerto Rico.

Other special rules apply for residents of Guam, the Commonwealth of the Northern Mariana Islands, and the U.S. Virgin Islands (the so-called “Mirror Code territories”), and American Samoa.

Social Security Number Still Required to Claim CTCs for 2021

Not changing for 2021: to claim the CTC, the client must include each qualifying child’s name and social security number (SSN) on the tax return, and those SSNs must have been issued before the return’s filing due date.

If a qualifying child doesn’t have an SSN, the client will be able to claim the $500 family credit for that child—using an individual taxpayer identification number (ITIN) or adoption taxpayer identification number (ATIN).

Issue 11: Other Sections of the American Rescue Plan Act of 2021

§9641 – Credits for Paid Sick and Family Leave Extension of Credits

Extends the Families First Coronavirus Response Act paid sick time and paid family leave credits from March 31, 2021 through September 30, 2021.

§9642 – Increase in Limitations on Credits for Paid Family Leave

Increases the amount of wages for which an employer may claim the paid family credit in a year from $10,000 to $12,000 per employee and increases the number of days for which self-employed individuals can claim the credit from 50 to 60.

§9643 – Expansion of Leave to Which Paid Family Leave Credit Applies

Expands the paid family leave credit to allow employers to claim the credit for leave provided for the reasons included under the previous employer mandate for paid sick time (e.g., if the employee has contracted COVID-19 or is caring for someone with COVID-19).

§9644 – Paid Leave Credits Allowed for Leave for COVID-19 Vaccination

Expands the paid sick time and paid family leave credits to include leave taken to obtain a COVID-19 vaccine or to recover from an injury, disability, illness, or condition related to a COVID-19 immunization.

§9645 – Application of Non-Discrimination Rules

Prevents employers from claiming the credit if they make leave available in a manner that discriminates in favor of highly compensated employees, full time employees, or based on employment tenure with the employer.

§9646 – Reset of Limitation on Paid Sick Leave

Resets the ten-day limitation on the maximum number of days for which an employer can claim the paid sick leave credit with respect to wages paid to an employee.

The current ten-day limitation runs from the start of the credits in 2020 through March 31, 2021. The new ten-day limitation applies to sick days after March 31, 2021.

For self-employed individuals, the ten-day limitation resets on January 1, 2021.

§9647 – Credit Allowed Against Hospital Insurance Tax

Beginning after March 31, 2021, the credits for paid family and medical leave will be structured as a refundable payroll tax credit against the hospital insurance tax.

§9648 – Application of Credits to Certain Governmental Employers

Allows state and local governments as well as Federal governmental instrumentalities that are tax-exempt 501(c)(1) organizations to access the paid sick time and paid family leave credits.

§9649 – Gross Up of Credit in Lieu of Exclusion from Tax

Increases the value of the credits by the amount equal to the OASDI and HI employer-share tax imposed on qualified paid family and medical leave wages for purposes of this credit.

§9650 – Effective date

The provisions relating to the payroll tax credits included in this title become effective for amounts paid with respect to leave taken after March 31, 2021.

The provisions relating to self-employed individuals becomes effective retroactive beginning after December 31, 2021.

§9651– Employee Retention Credit

Extends the employee retention tax credit, as added by the CARES Act and expanded and extended in P.L. 116-260, through December 31, 2021.

Modifies the credit such that, beginning after June 30, 2021, the credit will be structured as a refundable payroll tax credit against the hospital insurance tax.

§9661 – Premium Tax Credit

Modifies the affordability percentages used for §36 (B) premium tax credits for 2021 and 2022 to increase credits for individuals eligible for assistance under current law and provides §36 (B) credits for taxpayers with income below 400% of the federal poverty line (FPL).

§9662 – Temporary Modification of Limitations on Reconciliation of Tax Credits for Coverage under a Qualified Health Plan with Advance Payments of Such Credit

For tax year 2020, modifies the repayment obligations for taxpayers receiving excess premium tax credits under §36 (B) so such payments are not subject to recapture.

§9663 – Application of Premium Tax Credit in Case of Individuals Receiving Unemployment Compensation During 2021

For 2021, provides advanced premium tax credits as if the taxpayer’s income was no higher than 133§ of the federal poverty line (FPL) for individuals receiving unemployment compensation as defined in §85(B) of the Internal Revenue Code.

§9672 – Tax Treatment of Targeted EIDL Advances

Exempts Economic Injury Disaster Loan (EIDL) grants from tax and provides that such exclusion shall not result in a denial of deduction, reduction of tax attributes, or denial of increase in basis by reason of this exclusion from income.

Directs the Secretary to prescribe rules for determining a partner’s distributive share of amounts received through an EIDL grant.

§9673 – Tax treatment of Restaurant Revitalization Grants

Exempts Restaurant Revitalization Grants from tax and provides that such exclusion shall not result in a denial of deduction, reduction of tax attributes, or denial of increase in basis by reason of this exclusion from income.

Directs the Secretary to prescribe rules for determining a partner’s distributive share of amounts received through a Restaurant Revitalization Grant.

Clients must maintain appropriate documentation establishing their eligibility for the credits as an eligible self-employed individual.

The business interest expense limitation of §163(j) increased from 30% to 50% of adjusted taxable income for tax year 2020, and retroactively for 2019.

Every client who deducts business interest is required to file Form 8990, Limitation on Business Interest Expense Under Section 163(j), unless an exception for filing is met.

Issue 12: Qualified Business Income Deduction FAQ’s Updated (Added the Following)

Q6. What if a single trade or business has multiple sources of income, some from specified service activities and some from other activities?

A6. There is a de minimis rule for a single trade or business that has income from both specified service activities and other activities.

Under the de minimis rule, if a trade or business has gross receipts of $25 million or less and less than 10% of its gross receipts are attributable to specified service activities, or gross receipts of more than $25 million and less than 5% of its gross receipts are attributable to specified service activities, the trade or business as a whole is not an SSTB.

However, if the gross receipts from specified service activities exceed the percentage specified above, the entire trade or business is treated as an SSTB.

Q9. What are the “W-2 wages” for purposes of applying the W-2 wage limitation? Do W-2 wages paid to the officer of an S corporation qualify as QBI and towards the W-2 wage limitation?

A9. For purposes of the W-2 wage limitation, W-2 wages include:

(1) the total amount of wages paid to employees; and

(2) certain deferred compensation. Both wages and deferred compensation must be reported to the Social Security Administration (SSA) on a timely filed return. Additionally, the W-2 wages must be properly allocable to QBI. W-2 wages are properly allocable to QBI if the associated wage expense is taken into account in computing QBI for the trade or business.

W-2 wages paid to an S corporation officer will generally not qualify as a source of QBI to the employee. However, such wages will generally be included in the employer’s QBI. Additionally, W-2 wages paid to an S corporation officer that are (1) properly allocable to QBI, and (2) are reported to the SSA on a timely filed return, will qualify as W-2 wages attributable to a trade or business identified by the S corporation for purposes of applying the W-2 wage limitation.

Q10. What is the unadjusted basis immediately after acquisition (UBIA) of qualified property?

A10. A client’s UBIA of qualified property is its basis in the qualified property on its placed-in-service date before any adjustments except an adjustment to reflect a reduction in basis for personal use of the property during the tax year.

“Qualified property” for purposes of the QBID is any depreciable tangible property:

(1) which is held by, and available for use in, the clients trade or business at the close of the tax year;

(2) which is used at any point during the tax year in the production of QBI, and

(3) the depreciable period for which has not ended before the close of the tax year.

The depreciable period ends on the later of 10 years after the property is first placed in service, or on the last day of the last full year in the applicable recovery period.

Q17. Is there a form for reporting the QBID? And if so, where can I find it?

A17. Yes, for tax years 2019 and after, Form 8995, Qualified Business Income Deduction Simplified Computation, and Form 8995-A, Qualified Business Income Deduction, are used to compute and report the QBID. Before 2019, there was no specific form; however, worksheets were available in the Form 1040 Instructions and Publication 535, Business Expenses, to assist with the calculations in 2018.

Q28. What requirements must be met to make an election to aggregate multiple trades or businesses as one QTB and how does such aggregation election effect any election made to “group” activities under another Code section?

A28. To aggregate multiple trades or businesses, the following requirements must be met:

(1) The same person or group of persons, directly or by attribution, own 50% or more of each trade or business for more than half of the tax year, including the last day of the tax year,

2) All the items attributable to each trade or business are reported on returns with the same tax year, without regard to short-tax years,

3) None of the trades or businesses is an SSTB, and

4) Two of the following three factors are met:

- The trades or businesses provide products, property, or services that are the same or customarily offered together,

- The trades or businesses share facilities or share significant centralized business elements, such as personnel, accounting, legal, manufacturing, purchasing, human resources, or information technology resources, and/or

- The trades or businesses are operated in coordination with, or reliance upon, one or more of the businesses in the aggregated group.

Once an aggregation election is made, the aggregation must be consistently applied to the trades or businesses unless there has been a significant change to the facts and circumstances that would render the aggregation no longer appropriate.

An election to aggregate for QBID purposes has no effect on the election to “group” under another Code section.

Q33. Does QBID reduce the adjusted basis of a shareholder in a S corporation or the adjusted basis of a partner in a partnership?

A33. No. The QBID has no effect on an S corporation shareholder’s adjusted basis in its S corporation stock or a partner’s adjusted basis in its partnership interest.

Q40. Are charitable contributions attributable to a trade or business for purposes of determining QBI?

A40. No. For purposes of QBI, QBI is not reduced by amounts that constitute charitable contributions under 170.

Issue 13: IRS Reminds Taxpayers of Recent Changes in Retirement Plans

A retirement plan account owner must normally begin taking an RMD annually starting the year he or she reaches 70 ½ or 72, depending on their birthdate and maybe the year they retire. Retirement plans requiring RMDs include traditional, Simplified Employee Pension Plan (SEP) and Savings Incentive Match Plan for Employees (SIMPLE) Individual Retirement Accounts; 401(k), 403(b), 457(b), profit sharing and other defined contribution plans.

The Setting Every Community Up for Retirement Enhancement (SECURE) Act changed the age when individuals must begin taking withdrawals from their retirement accounts. Someone born on or before June 30, 1949, was required to start getting RMDs for the year they reached the age of 70½.

However, under the SECURE Act, if a person’s 70th birthday is July 1, 2019, or later, they do not have to take their first RMD until the year they reach age 72.

The Coronavirus, Aid, Relief and Economic Security (CARES) Act waived RMDs during 2020 so seniors and retirees, including beneficiaries with inherited accounts, were not required to take money out of IRAs and workplace retirement plans. The waiver included RMDs for individuals who turned age 70½ in 2019 and took their first RMD in 2020.

Individuals who reached age 70 ½ before 2020 and were still employed, but terminated employment in 2020, would normally have a 2020 RMD due by April 1, 2021, from their workplace retirement plan. This RMD is also waived as part of the CARES Act relief. Roth IRAs do not require withdrawals until after the death of the owner.

2021 RMDs

Individuals who reached 70 ½ in 2019 or earlier, did not have an RMD due for 2020.

For 2021, they will have an RMD due by Dec. 31, 2021. Individuals who did not reach age 70 ½ in 2019 will reach age 72 in 2021 will have their first RMD due by April 1, 2022, and their second RMD due by Dec. 31, 2022. To avoid having both amounts included in their income for the same year, the client can make the first withdrawal by Dec. 31, 2021, instead of waiting until April 1, 2022. After the first year, all RMDs must be made by Dec. 31.

An IRA trustee must either report the amount of the RMD to the IRA owner or offer to calculate it for the owner. Calculating the amount of the RMD depends on the type of IRA or if they are from multiple accounts. Not taking a required distribution, or not withdrawing enough, could mean a 50% excise tax on the amount not distributed.

Some can delay RMDs

Though the April 1 deadline for taking the first RMD is mandatory for all owners of traditional IRAs, participants in workplace retirement plans who are still working usually can, if their plan allows, wait until April 1 of the year after they retire to start receiving distributions from these plans. Individuals who reached age 70 ½ before 2020 and were still employed, but terminated employment in 2020, would normally have a 2020 RMD due by April 1, 2021 from their workplace retirement plan. This RMD is also waived as part of the CARES Act relief.

Employees of public schools and certain tax-exempt organizations should check with their employer, plan administrator or provider to see how to treat these accruals.

Coronavirus-Related Distributions and Loans

Distributions: Certain distributions made from Jan. 1, 2020, through Dec. 30, 2020, from IRAs or workplace retirement plans to qualified individuals may be treated as coronavirus-related distributions. These distributions are not subject to the 10% additional tax on early distributions (including the 25% additional tax on certain SIMPLE IRA distributions).

Taxes on coronavirus-related distributions are includible in taxable income:

- Over a three-year period, one-third each year, or

- If elected, in the year you take the distribution.

Coronavirus-related distributions may be repaid to an IRA or workplace retirement plan within three years.

If the client had an outstanding loan balance in when they left employment, the plan sponsor will usually offset the loan balance against their benefit.

- For loan offsets in 2020, the client has until the due date of the tax return (plus extensions) to repay that amount to another retirement plan or IRA.

- If the client is a qualified individual, they can treat the loan offset as a coronavirus-related distribution and have three years to repay to an IRA or include in income tax ratably over three years.

RMDs

An IRA owner or beneficiary who received an RMD in 2020 had the option of returning it to their account or other qualified plan to avoid paying taxes on that distribution. RMDs in 2020 that were not rolled over or repaid may be eligible to be treated as coronavirus-related distributions if the individual is a qualified individual. A 2020 RMD that otherwise qualifies as a coronavirus-related distribution may be repaid over a 3-year period or have the taxes due on the distribution spread over three years.

A withdrawal from an inherited IRA to a qualified individual may also be a coronavirus-related distribution. Income from the withdrawal may be spread over three years for income inclusion; however, the withdrawal may not be repaid to the inherited IRA.

IRS Notice 2020-51 provided that the one rollover per 12-month period limitation and the restriction on rollovers to inherited IRAs did not apply to repayments made by Aug. 31, 2020. The RMD suspension did not apply to qualified defined benefit plans.

The CARES Act included special rules for plan loans made to qualified individuals. Plans could suspend loan repayments for up to one year, although, typically, repayments resumed in January 2021. This effectively gives up to six years (instead of five) to repay a typical plan loan.

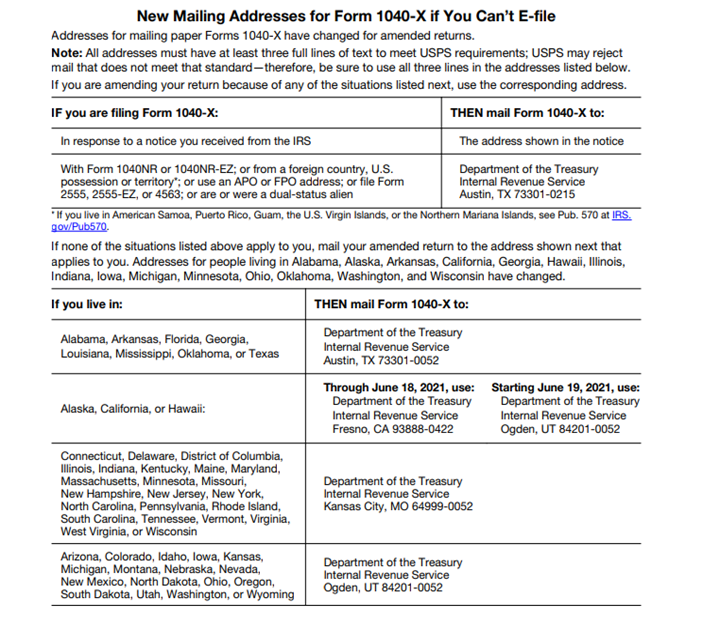

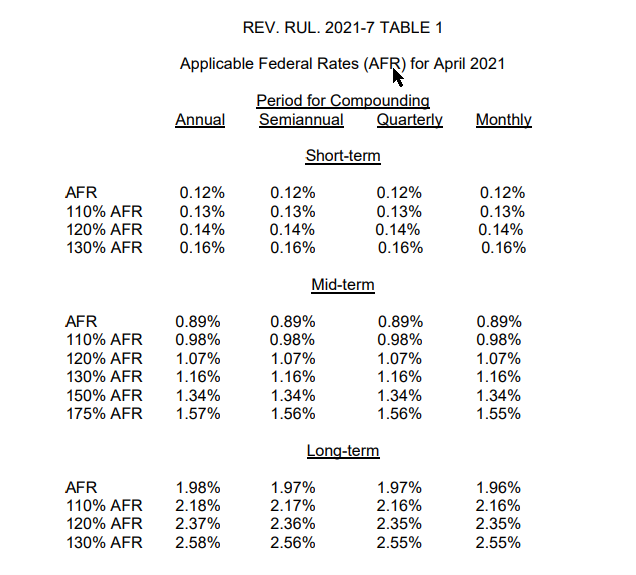

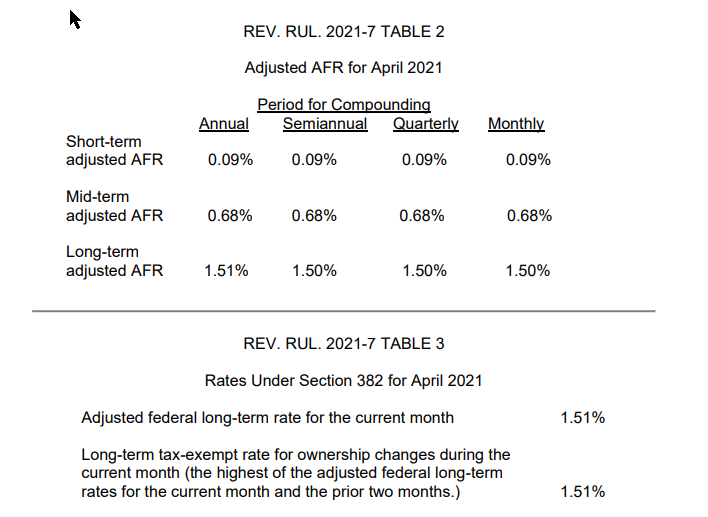

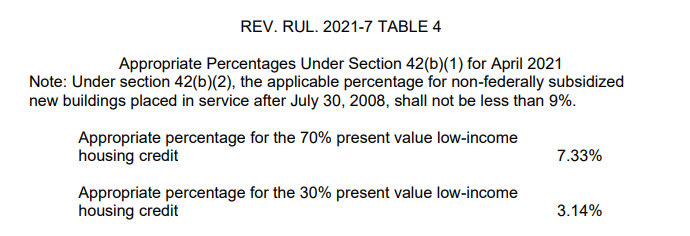

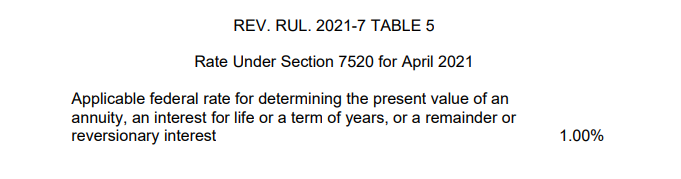

Issue 14: Applicable Federal Rates for April 2021

Rev Rul. 2021-7, 2021-14 IRB

![]() Basics & Beyond Resources

Basics & Beyond Resources

- Blog Page

- Resource List

- Webinar & Seminar Schedules

- Get Registered!

- Note: Paid attendees can request a link to the replay of any previously recorded webinar presentations by emailing us at [email protected]