New guidance has been issued in the form of FAQ’s related to handling Form 1099-K and sale of personal property, unrelated to business. This was discussed in our year-end sessions.

We have reproduced the FAQs for your convenience in this newsletter. Though IRS has announced a transition period for the new thresholds to become effective, many vendors may still report theses type of transactions on Form 1099-K.

In this issue:

- IRS Completes Automatic Corrections for Tax Year 2020 Accounts Related to Unemployment Compensation Exclusion

- IRS Announces New Deputy Chief for the Taxpayer Experience Office

- Legal Advice Discusses Payment of Legal Fees to Third Parties

- Announcement 2022-227, 12/23/2022, § 6045 – Digital Currency

- 1099-K FS-2022-41, December 2022

- Notice 2023-3, 12/29/2022, § 162 Business Use of Auto—Optional Standard Mileage Rates for 2023

- Frequently Asked Questions About New Hire Reporting

- No Tax Extenders in Budget Bill

- Applicable Federal Rates for February 2023, Rev. Rul. 2023-3

Issue 1: IRS Completes Automatic Corrections for Tax Year 2020 Accounts Related to Unemployment Compensation Exclusion – 12 million Refunds Issued

The Internal Revenue Service recently completed the final corrections of tax year 2020 accounts for taxpayers who overpaid their taxes on unemployment compensation they received in 2020.

The American Rescue Plan Act of 2021, which became law in March 2021, excluded up to $10,200 in 2020 unemployment compensation from taxable income calculations (up to $10,200 for each spouse if married filing joint). The exclusion applied to individuals and married couples whose modified adjusted gross income was less than $150,000.

To ease the burden on taxpayers, the IRS took steps to review the Forms 1040 and 1040-SR that were filed prior to the law’s enactment to identify taxpayers who had already reported unemployment compensation as income and were eligible for the correction. The IRS determined the correct taxable amount of unemployment compensation and tax.

Some taxpayers received refunds, while others had the overpayment applied to taxes due or other debts. In some cases, the exclusion only resulted in a reduction in their adjusted gross income. The IRS mailed a letter to these taxpayers to inform them of the corrections. Taxpayers should keep that letter with their tax records.

The IRS corrected approximately 14 million returns. This resulted in nearly 12 million refunds totaling $14.8 billion, with an average refund of $1,232.

Many of the adjustments included corrections to the:

- Earned Income Tax Credit

- Recovery Rebate Credit

- Additional Child Tax Credit

- American Opportunity Tax Credit

- Premium Tax Credit

- Advance Premium Tax Credit

If a taxpayer is eligible for the unemployment compensation exclusion and their account was not corrected by the IRS, they may need to file an amended 2020 tax return to claim the exclusion and any applicable non-refundable or refundable credits impacted by the exclusion.

Issue 2: IRS Announces New Deputy Chief for the Taxpayer Experience Office

The Internal Revenue Service has announced Courtney Kay-Decker as the new Deputy Chief Taxpayer Experience Officer.

Under the leadership of Chief Taxpayer Experience Officer Ken Corbin, Kay-Decker will lead IRS efforts to improve the taxpayer experience including driving the strategy for taxpayer interactions, monitoring and prioritizing the taxpayer experience, coordinating identification of taxpayer trends and best practices, and collaborating on the implementation of Service-wide taxpayer experience improvements.

Prior to her selection, Kay-Decker served as an attorney at Lane & Waterman LLP in Davenport, Iowa, where her areas of practice included tax and administrative matters. From 2011 to 2019, she served as Director of the Iowa Department of Revenue. As director, Kay-Decker focused on improving administrative rules, guidance, and processes to simplify and reduce compliance burdens for the taxpayers of Iowa. She also served on the Board of Trustees of the Federation of Tax Administrators.

Additionally, Kay-Decker served as the first state co-chair of the Identity Theft and Tax Refund Fraud Information Sharing Analysis Center, a collaboration among the IRS, state tax agencies and industry partners who work to develop tools and protocols to detect and prevent identity theft tax refund fraud. She’s served as a Volunteer Income Tax Assistance site coordinator and as a member of the Electronic Tax Administration Advisory Committee.

Kay-Decker received her B.A. in Economics from Northwestern University in Evanston, Illinois, and holds a J.D. with distinction from the University of Iowa College of Law where she also serves as an adjunct lecturer.

The Taxpayer Experience Office, formally established earlier this year, leads the effort to improve customer service at the IRS by focusing on six key strategies identified in the President’s Executive Order on Transforming Federal Customer Experience and Service Delivery to Rebuild Trust in Government, and the Taxpayer First Act Report to Congress.

Issue 3: Legal Advice Discusses Payment of Legal Fees to Third Parties – AM-2022-007 – Considered “Funded Compensation Payment”

Legal fees earned by a law firm that were paid to a third party are income to the law firm in the year the fees are transferred to the third party, according to IRS Chief Counsel. (AM-2022-007)

Facts: A cash basis law firm, taxed as a partnership, represented a client on a contingency fee basis. Before formally settling the client’s claim, the law firm arranged for a third party to receive the fees from the settlement it negotiated for the client.

In this case, the third party markets a deferred compensation product to law firms that features a purported income tax deferral and investment vehicle for the deferred amounts. The law firm agrees that the settlement payor will transfer 100% of the firm’s legal fees directly to the third party. In return, the third party agrees to pay a lump sum to the law firm in ten years. This arrangement purports to be irrevocable.

The law firm argued that it did not have to include the fees in its gross income in the year the third-party received the funds based on Childs, (1994) 103 TC 634.

Issue. When does the law firm include in income the fees income sent to the third party?

Conclusion. According to Chief Counsel, the law firm must include the fees in gross income in the year the funds representing those fees are transferred to the third party. The transaction creates a “funded compensation arrangement,” said Chief Counsel, which results in gross income to the law firm under the anticipatory assignment of income doctrine, the economic benefit doctrine, and § 83.

Alternatively, Chief Counsel notes, to the extent the arrangement constitutes unfunded deferred compensation, the arrangement is a nonqualified deferred compensation plan subject to §409A, and the law firm has gross income in the first year of the arrangement because the plan fails to comply with §409A.

Issue 4: Announcement 2022-227, 12/23/2022, § 6045 – Digital Currency

Treasury Department and IRS announced that brokers are not required to report additional information with respect to dispositions of digital assets until final regulations are issued under §§ 6045 and 6045A.

The Infrastructure Investment and Jobs Act, enacted in 2021, amended provisions in §§ 6045 and 6045A to clarify and expand the rules regarding the reporting of information on digital assets by brokers. Brokers are still required to comply with existing laws and regulations. This transitional guidance applies only to information returns filed or furnished by brokers. In contrast, clients are still required to report any income they receive from transactions involving digital assets.

What is a digital asset?

A digital asset is a digital representation of value which is recorded on a cryptographically secured, distributed ledger. Common digital assets include:

- Convertible virtual currency and cryptocurrency

- Stablecoins

- Non-fungible tokens (NFTs)

Everyone must answer the question.

Everyone who files Form 1040, Form 1040-SR or Form 1040-NR must check one box, answering either “Yes” or “No” to the digital asset question. The question must be answered by all taxpayers, not just those who engaged in a transaction involving digital assets in 2022.

When to check “Yes”

Normally, a taxpayer must check the “Yes” box if they:

- Received digital assets as payment for property or services provided;

- Transferred digital assets for free (without receiving any consideration) as a bona fide gift;

- Received digital assets resulting from a reward or award;

- Received new digital assets resulting from mining, staking and similar activities;

- Received digital assets resulting from a hard fork (a branching of a cryptocurrency’s blockchain that splits a single cryptocurrency into two);

- Disposed of digital assets in exchange for property or services;

- Disposed of a digital asset in exchange or trade for another digital asset;

- Sold a digital asset; or

- Otherwise disposed of any other financial interest in a digital asset.

IRS Memos Address Crypto Losses, Donation – OCC Memo – 202302011 and 202302012

National Association of Tax Professionals Update – no infringement intended

The IRS recently released Office of Chief Counsel (OCC) memorandums addressing the tax treatment of a taxpayer’s 2022 cryptocurrency losses and the deductibility of a cryptocurrency donation of more than $5,000 when there was no qualified appraisal. While OCC memorandums can’t be cited as precedent in IRS proceedings, they are often relied upon by IRS managers when deciding on how to proceed with certain taxpayer issues.

No deduction for taxpayer’s crypto losses

In the first memorandum the OCC found that a taxpayer who owned cryptocurrency that lost much of its value in 2022 can’t claim a deduction for losses under §165. The memorandum notes that §165 provides a deduction for losses evidenced by closed and completed transactions, fixed by identifiable events and actually sustained during a tax year.

Taxpayers who have seen their cryptocurrency lose substantial value have not abandoned or otherwise disposed of the asset, and the cryptocurrency is not worthless because it still retains some value, the memorandum explained. Additionally, even if the taxpayer sustained a §165 loss, the deduction would still be disallowed because §67(g) suspended miscellaneous itemized deductions for the 2018 through 2025 tax years.

No deduction for large crypto donation without appraisal

If a taxpayer claims a charitable deduction of more than $5,000 for a donation of cryptocurrency to an exempt organization, a qualified appraisal is required, a recent OCC memorandum stated. The memorandum also explained that the taxpayer’s valuation of the donated cryptocurrency based on a cryptocurrency exchange listing does not qualify for the reasonable cause exception in §170(f)(11)(A)(ii)(II) and will not excuse noncompliance with the qualified appraisal requirement.

Because the exception was intended to help taxpayers who made an unsuccessful, good-faith effort to comply with the appraisal requirement, the reasonable cause exception to the requirements of §170 do not apply to taxpayers who failed to get a qualified appraisal. According to the memorandum, cryptocurrency does not satisfy the qualified appraisal requirement simply because it is listed on an exchange.

Issue 5: 1099-K FS-2022-41, December 2022

This Fact Sheet issues frequently asked questions about Form 1099-K.

These FAQs are being issued to provide general information to taxpayers and tax professionals as expeditiously as possible. Accordingly, these FAQs may not address any particular taxpayer’s specific facts and circumstances, and they may be updated or modified upon further review.

Because these FAQs have not been published in the Internal Revenue Bulletin, they will not be relied on or used by the IRS to resolve a case. Similarly, if an FAQ turns out to be an inaccurate statement of the law as applied to a particular taxpayer’s case, the law will control the taxpayer’s tax liability.

Nonetheless, a taxpayer who reasonably and in good faith relies on these FAQs will not be subject to a penalty that provides a reasonable cause standard for relief, including a negligence penalty or other accuracy-related penalty, to the extent that reliance results in an underpayment of tax. Any later updates or modifications to these FAQs will be dated to enable taxpayers to confirm the date on which any changes to the FAQs were made. Additionally, prior versions of these FAQs will be maintained on IRS.gov to ensure that taxpayers, who may have relied on a prior version, can locate that version if they later need to do so.

Form 1099-K Frequently Asked Questions

Background

Form 1099-K, Payment Card and Third-Party Network Transactions, is an IRS information return used to report certain payment transactions to improve voluntary tax compliance.

On Dec. 23, 2022, the IRS announced that calendar year 2022 will be treated as a transition year for the reduced reporting threshold of more than $600. For calendar year 2022, third-party settlement organizations who issue Forms 1099-K are only required to report transactions where gross payments exceed $20,000 and there are more than 200 transactions.

General

Q1. Why am I receiving a Form 1099-K, from a payment card or third-party settlement organization? (Updated December 28, 2022)

A1. Third party information reporting for certain income is required by law. Third party information reporting has been shown to increase voluntary tax compliance, improve tax collections and assessments within the IRS, and thereby reduce the tax gap.

Q2. How is the IRS planning to address the changes to the Form 1099-K reporting requirements? (Updated December 28, 2022)

A2. As outlined in Notice 2023-10, the IRS is delaying the implementation of the requirement for third party business reporting more than $600 for the 2022 calendar year.

More specifically, the IRS is delaying the implementation of the provision of the American Rescue Plan Act of 2021 that:

- Lowered the threshold for reporting third party network transactions from aggregate payments exceeding $20,000 to aggregate payments exceeding $600 during the calendar year.

- Eliminated the 200-transaction threshold for reporting third party network transactions entirely.

Q3. Is the gain or loss on the sale of a personal item used to compute my taxable income? Is that reported on a Form 1099-K? (Added December 28, 2022)

A3. Gain or loss on the sale of a personal item is generally the difference between the amount you paid for the item (the purchase price) and the amount you receive when you sell it (the sales price).

- For example, if you bought a refrigerator for $1,000 (the purchase price) and sold it for $600 (the sales price), you have a loss of $400. $600 sales price – $1,000 purchase price = ($400) loss amount.

- On the other hand, if you bought concert tickets for $500 (the purchase price) and sold them for $900 (the sales price), you have a gain of $400. $900 sales price – $500 purchase price = $400 gain amount.

- The gain on the sale of a personal item is taxable. You must report the transaction (gain on sale) on Form 8949, Sales and Other Dispositions of Capital Assets, and Form 1040, U.S. Individual Income Tax Return, Schedule D, Capital Gains and Losses. See Publication 551, Basis of Assets, for guidance in determining your basis.

- The gain on the sale of a personal item might be reported on a Form 1099-K. If you receive a Form 1099-K reporting the $900 that you received from the sale of your concert tickets that cost you only $500, you must report the gain on Form 8949 and Schedule D.

- The loss on the sale of a personal item is not deductible. For calendar year 2022 tax returns, if you receive a Form 1099-K, for the sale of a personal item that resulted in a loss, you should make offsetting entries on Form 1040, U.S. Individual Income Tax Return, Schedule 1, Additional Income and Adjustments to Income, as follows:

- Report your proceeds (the Form 1099-K amount) on Part I – Line 8z – Other Income, using the description “Form 1099-K Personal Item Sold at a Loss.”

- Report your costs, up to but not more than the proceeds amount (the Form 1099-K amount), on Part II – Line 24z – Other Adjustments, using the description “Form 1099-K Personal Item Sold at a Loss.”

- In the example of the refrigerator sale above, if you received a Form 1099-K for $600 for the refrigerator for which you originally paid $1,000, you should report the loss transaction as follows:

- Form 1040, Schedule 1, Part I – Line 8z, Other Income. List type and amount: “Form 1099-K Personal Item Sold at a Loss …. $600” to show the proceeds from the sale reported on the Form 1099-K and,

- Form 1040, Schedule 1, Part II – Line 24z, Other Adjustments. List type and amount: “Form 1099-K Personal Item Sold at a Loss…. $600” to show the amount of the purchase price that offsets the reported proceeds. Do not report the $1,000 you paid for the refrigerator because the loss on the sale of a personal item is not deductible.

Q4. How do I account for the fees I paid to an online marketplace related to the sale of my personal items? (Added December 28, 2022)

A4. You should include all fees (e.g., selling fees, payment processing fees, etc.) associated with the sale of the personal items in basis when computing gain or loss on the sale. In general, you should adjust the gain or loss on the sale of property by the amount of expenses and fees paid to facilitate the sale. If you realize a gain on the sale of property, report the selling expenses as a downward adjustment to the gain that you report on Form 8949 or Schedule D.

Box 1a of the Form 1099-K reports the gross amount of payment card/third party network transactions. This amount is not adjusted to account for fees, refunds, chargebacks, or other costs included in the unadjusted dollar amount of the payment transactions. If the Form 1099-K reports the total unadjusted dollar amount of the payment transactions and you separately paid selling expenses, you may need to make a separate adjustment to the resulting gain or loss. You should maintain and consult your own records to determine these amounts.

Q5. To make sure that I report properly on the Form 8949, how do I determine if the capital gain on the sale of my personal item is short-term or long-term? (Added December 28, 2022)

A5. Generally, if you hold a personal item for more than one year before you sell it, the capital gain is long-term. If you hold it one year or less before you sell it, the capital gain is short-term.

Q6. During the year, I sold my personal guitar for $800 on a social media platform’s marketplace and I received Form 1099-K. I purchased the guitar several years ago for $3,000. How do I prove how much I paid if requested by the IRS? (Added December 28, 2022)

A6. Generally, you should keep accurate records for personal items you may sell. If records are lost, destroyed, or are not available due to circumstances beyond your control and your return is audited, examiners may allow you to present reconstructed records. Additionally, examiners may accept oral testimony when records do not exist.

- In this example you have a nondeductible personal loss. $800 sales price – $3,000 purchase price = ($2,200) loss amount. You can offset the proceeds reported on the Form 1099-K using some of your purchase price as shown here:

- Form 1040, Schedule 1, Part I – Line 8z, Other Income. List type and amount: “Form 1099-K Personal Item Sold at a Loss…. $800” to show the proceeds from the sale reported on the Form 1099-K. and

- Form 1040, Schedule 1, Part II – Line 24z, Other Adjustments. List type and amount: “Form 1099-K Personal Item Sold at a Loss…. $800” to show the amount of the purchase price that offsets the reported proceeds. Do not report the $3,000 you paid for the purchase because a personal loss is not deductible.

Q7. In a single online transaction on an online marketplace, I sold two sets of four tickets (I bought for personal use) to two separate sporting events for $1,000 (one set for $800 and the second set for $200) and I received Form 1099-K. I purchased each set of tickets for $250 ($500 total) two months prior to selling them. How do I report the sale on my tax return? (Added December 28, 2022)

A7. You must report the gain and loss separately because the loss on the second set of tickets cannot offset the gain on the first set of tickets.

- The $550 gain from the sale of one set of tickets ($800 sales price – $250 purchase price = $550 gain) must be reported as short-term gain on Form 8949 and Schedule D.

- The $50 loss transaction from the other set of tickets ($200 sales price – $250 purchase price = ($50) loss) should be reported as follows:

- Form 1040, Schedule 1:

- Part I – Line 8z, Other Income. List type and amount: “Form 1099-K Personal Item Sold at a Loss…. $200” to show the proceeds from the sale reported on the Form 1099-K and

- Part II – Line 24z, Other Adjustments. List type and amount: “Form 1099-K Personal Item Sold at a Loss…. $200” to show the amount of the purchase price that offsets the reported proceeds.

Q8. My friend and I went to a concert, and my friend reimbursed money to me for her concert ticket through an online application. If I get a Form 1099-K for the reimbursement, do I need to pay taxes on it? (Added December 28, 2022)

A8. Because the money is not payment for the sale of goods or the provision of services, generally the reimbursement would not be taxable to you.

- If you believe the information on Form 1099-K, is incorrect, the form has been issued in error, or you have a question relating to the form, contact the filer, whose name and contact information appears in the upper left corner on the front of the form. You may also contact the payment settlement entity whose name and phone number are shown in the lower left side of the form.

- If you cannot get the form corrected, the error should be reported on Form 1040, Schedule 1, Part I, Additional Income, Line 8z, Other Income, with an offsetting entry in Part II, Adjustments to Income, Line 24z, Other Adjustments.

- For example, if you received $800 from a friend reimbursing you for a concert ticket and you received a Form 1099-K reporting this as gross proceeds, your Schedule 1 should reflect the following:

- Form 1040, Schedule 1

- Part I – Line 8z, Other Income. List type and amount: “Form 1099-K Received in Error…. $800” to show the proceeds reported on the Form 1099-K.

- Part II – Line 24z, Other Adjustments. List type and amount: “Form 1099-K Received in Error…. $800” to offset the proceeds reported to you in error. Not reporting this adjustment could result in you improperly reporting gain on the reimbursement.

Q9. Does the delayed reporting requirement in Notice 2023-10 mean that I don’t have to report income reported to me on a Form 1099-K? (Added December 28, 2022)

A9. The IRS is delaying the requirement for third party settlement organizations to report income at the more than $600 threshold for calendar year 2022 (tax filing season 2023). However, the legal requirement for reporting income has not changed, regardless of the reporting threshold for providing a Form 1099-K.

Reporting does not impact a taxpayer’s responsibility to accurately report ALL income, whether or not they receive a Form 1099-K or other information return (e.g., Form 1099-MISC, Miscellaneous Information; Form 1099-NEC, Nonemployee Compensation; etc.).

Except as otherwise provided in the Internal Revenue Code, gross income includes income from whatever source derived. A taxpayer can receive income in the form of money, property, or services. Publication 525, Taxable and Nontaxable Income, discusses many kinds of income and explains whether they are taxable or nontaxable.

Q10. Who can a taxpayer call if they have a question about their Form 1099-K? (Updated December 28, 2022)

A10. Taxpayers who have questions about the information on a Form 1099-K they received should contact the filer. The contact information is in the upper left corner on the form. If a taxpayer does not recognize the filer shown in the upper left corner of the form, they should contact the payment settlement entity whose name and phone number are shown in the lower left corner of the form above their account number.

If you have general questions about the Form 1099-K, please consult the Instructions for Form 1099-K. If you have general questions about information returns, please consult the General Instructions for Certain Information Returns.

Q11. Who can a payment settlement entity, or electronic payment facilitator/other third-party call if they have a question on Form 1099-K? (Updated November 21, 2022)

A11. For questions about Form 1099-K, Payment Card and Third-Party Network Transactions, see the general instructions for information returns.

Definitions

Q1. What is Form 1099-K? (Added October 21, 2022)

A1. Form 1099-K, Payment Card and Third-Party Network Transactions, is an information return that reports the gross amount of reportable transactions for the calendar year to the IRS. See Understanding Your Form 1099-K for more information.

Q2. What qualifies as a payment card? (Updated December 28, 2022)

The term “payment card” includes credit cards, debit cards, and stored-value cards (including gift cards), as well as payment through any distinctive marks of a payment card (such as a credit card number).

A payment card is issued according to an agreement that provides all of the following: one or more issuers of the cards; a network of persons unrelated to each other, and to the issuer, who agree to accept the cards as payment; and standards and mechanisms for settling the transactions between a merchant acquiring entities and the persons who accept the cards as payment.

Q3. What is a Merchant Category Code (MCC)? (Added October 21, 2022)

An MCC is a four-digit number used by the payment card industry to classify businesses by the goods or services they provide. There are approximately 600 MCCs, representing different types of businesses. Some examples are: 4411- Cruise Lines; 5462 – Bakeries; and 5532 – Automotive Tire Stores. It is important that this code is correct as IRS uses this when determining an audit.

Q4. What is a third-party settlement organization? (Updated December 28, 2022)

A4. The Internal Revenue Code uses the term “third party settlement organization.” A third-party settlement organization is the central organization that has the contractual obligation to make payments to participating payees (generally, a merchant or business) of third party network transactions. An example could include apps used to handle the money transfer between buyers and sellers.

Q5. What are the characteristics of a third-party payment network? (Updated December 28, 2022)

A5. Characteristics of a third-party payment network include:

- The existence of a central organization with whom a substantial number of providers of goods and services (who are unrelated to the central organization) have established accounts,

- An agreement between the central organization and the providers to settle transactions between the providers and purchasers,

- The establishment of standards and mechanisms for settling such transactions, and

- The guarantee of payment in settlement of such transactions.

An example of a third-party settlement organization is an online auction payment facilitator like an online marketplace, which operates as an intermediary between buyer and seller by transferring funds from the buyer to the seller for the provision of goods or services and otherwise meets the characteristics described in the bullet points above.

Under the reporting requirements, these third-party settlement organizations must report the gross reportable transactions of the participating payee to which they make payments provided the payee has gross reportable transactions of more than $600, regardless of the number of transactions.

Q6. What are payment settlement entities? (Updated December 28, 2022)

A6. A payment settlement entity is an entity that makes payment in settlement of a payment card transaction or third-party network transaction. PSE’s may be domestic or foreign entities and they can take one of two forms:

- Merchant Acquiring Entity: A bank or other organization that has the contractual obligation to make payment to participating payees in settlement of payment card transactions.

- Third Party Settlement Organization: The central organization that has the contractual obligation to make payment to participating payees of third-party network transactions.

Q7. Does an automated clearing house qualify as a third-party settlement organization? (Updated December 28, 2022)

A7. No. An automated clearing house processes electronic payments between buyers and sellers through wire transfers, electronic checks, and direct deposits. Further, there is no contractual relationship between the automated- clearing house and payees. Thus, an automated clearing house does not qualify as a third-party settlement organization and payments made through its network are not reportable under IRC 6050W.

Q8. What is a merchant acquiring entity? (Added October 21, 2022)

A8. Often called an acquiring or merchant bank, a merchant acquiring entity is the bank or other organization that has the contractual obligation to make payment to participating payees in settlement of payment card transactions. Merchant acquiring entities are responsible for reporting reportable payment card transactions.

Q9. What is a participating payee? (Added October 21, 2022)

A9. A participating payee is:

- Any person who accepts a payment card as payment, or

- Any person who accepts payment made by a third-party settlement organization in settlement of a third-party network transaction.

Q10. What constitutes the gross amount of reportable transactions? (Added October 21, 2022)

A10. The “gross amount” means the total dollar amount of total reportable payment transactions for each participating payee without regard to any adjustments for credits, cash equivalents, discount amounts, fees, refunded amounts, or any other amounts. The dollar amount of each transaction is determined on the date of the transaction.

Q11. Do healthcare networks fit the definition of a third-party settlement organization? (Added December 28, 2022)

A11. Health carriers operating a healthcare network do not fit the definition of a third-party settlement organization because they do not operate a third-party payment network that enables purchasers to transfer funds to providers of goods and services. Rather, health carriers accept payment, in the form of premiums, from buyers (employers or persons covered under the carrier’s plan) to give those buyers access to a network of healthcare providers; separately, health carriers then pay compensation to the medical professionals within their networks pursuant to predetermined rates. Accordingly, healthcare networks are not third-party settlement organizations.

Q12. Do accounts payable departments fit the definition of a third-party settlement organization? (Added December 28, 2022)

A12. No. In-house accounts payable departments do not fit the definition of a third-party settlement organization because they are internal processors of payments. They are not a third party.

Individuals

Q1. What do I do with the information on Form 1099-K? (Added October 21, 2022)

A1. Form 1099-K, Payment Card and Third-Party Network Transactions, is an information return. Use this information return in conjunction with your other tax records to determine your correct tax. To get further information on recordkeeping, check out Publication 583, Starting a Business and Keeping Records.

Q2. What do I do if I think my Form 1099-K is incorrect? (Updated December 28, 2022)

A2. If you believe the information on Form 1099-K, Payment Card and Third-Party Network Transactions, is incorrect, the form has been issued in error, or you have a question relating to the form, contact the filer, whose name and contact information appears in the upper left corner on the front of the form.

You may also contact the payment settlement entity whose name and phone number are shown in the lower left side of the form.

If you cannot get the form corrected, the error should be reported on Form 1040, Schedule 1, Additional Income and Adjustments to Income, Part I, Additional Income, Line 8z, Other Income, with an offsetting entry in Part II, Adjustments to Income, Line 24z, Other Adjustments.

For example, you took a trip with your friend, and you paid for the airline tickets. If your friend reimburses you $2,500 for their airline tickets, and you received a Form 1099-K reporting the $2,500 as gross proceeds, your Schedule 1 should reflect the following:

Form 1040, Schedule 1, Additional Income and Adjustments to Income

Part I – Line 8z, Other income. List type and amount: “Form 1099-K Received in Error …. $2,500” to show the proceeds reported on the Form 1099-K. and

Part II – Line 24z, Other adjustments. List type and amount: “Form 1099-K Received in Error…. $2,500” to offset the proceeds reported to you in error.

Q3. If I use a payment card or pay through a third-party settlement organization for a purchase, will I receive a Form 1099-K? (Updated December 28, 2022)

A3. No. Individuals and businesses should not receive a Form 1099-K, Payment Card and Third-Party Network Transactions, for making a purchase.

Q4. If I have a holiday craft business, will I receive a Form 1099-K? (Updated December 28, 2022)

A4. You may receive a Form 1099-K depending on the type of transactions.

If you accept payment cards (for example, credit card or debit cards) as a form of payment for goods you sell or services you provide, you will receive a Form 1099-K for the gross amount of the payments made to you through the use of a payment card during the calendar year. This reporting requirement has not changed, and there is no minimum reporting threshold for these payments to trigger a reporting requirement. Further, for calendar years after 2021, if you accept payments from a third-party settlement organization, you may receive Form 1099-K from that organization. A third-party settlement organization connects the parties together (for example, an internet sales site).

You would receive a Form 1099-K if you accepted payments from a third-party settlement organization where,

- the total number of your transactions exceeded 200, and

- the aggregate amount of payments you received with respect to any participating payee exceeded $20,000 in the calendar year.

Note: The American Rescue Plan Act lowered the threshold to trigger a reporting requirement on a Form 1099-K to from more than $20,000 to more than $600 (regardless of the number of transactions). The IRS issued Notice 2023-10, which temporary delays the enforcement of the lowered reporting requirement. However, you may receive a Form 1099-K in error at the lower threshold, despite Notice 2023-10.

Q5. I own a small business and have a not-for-profit hobby. I do not accept payment cards for either, but I do use a credit card and third-party settlement organizations to make purchases for both. Will I receive a Form 1099-K? (Updated December 28, 2022)

A5. No, you should not receive Form 1099-K, Payment Card and Third-Party Network Transactions, for your purchases.

Reporting

Q1. What requires payment card and third-party network reporting? (Added October 21, 2022)

A1. § 6050W, Returns Relating to Payments Made In Settlement Of Payment Card And Third Party Network Transactions, requires payment settlement entities (merchant acquiring entities and third party settlement organizations) to report payment card and third party network transactions.

Q2. How do I report Form 1099-K on my tax return? (Added October 21, 2022)

A2. Information on your Form 1099-K may be used to compute your gross receipts or sales. You should follow the return instructions on the form you are completing to report your gross receipts or sales.

Q3. How are reportable transactions reported to IRS? (Added October 21, 2022)

A3. Gross payment card and third-party network transaction amounts are reported to the IRS on Form 1099-K, Payment Card and Third-Party Network Transactions.

Q4. When are Forms 1099-K due? (Added October 21, 2022)

A4. Form 1099-K information is required to be filed with the IRS by February 28 of the year following the transactions if filed on paper. If filing electronically, it is required to be filed by the last day of March of the year following the transactions.

Q5. What are payee statements and when are they due? (Added October 21, 2022)

A5. Entities required to file Form 1099-K, Payment Card and Third-Party Network Transactions, must also furnish a statement to the payee with the same information reported to the IRS. Statements may be furnished in paper format (i.e., Copy B of Form 1099-K, Payment Card and Third-Party Network Transactions) or electronically with the consent of the payee in accordance with Treas. Reg. 1.6050W-2. The statements must be furnished to the payee by January 31, of the year following the transactions.

Q6. What information must the payment settlement entity report on Form 1099-K? (Added October 21, 2022)

A6. The gross amount of reportable payment transactions by month and the calendar year are required to be reported for each participating payee. The name, address and taxpayer identification number of each participating payee must also be reported on the form.

Q7. Do payment settlement entities adjust the gross amount to account for fees, refunds, chargebacks or other costs and refunded amounts? (Added October 21, 2022)

A7. No. The gross amount is the total unadjusted dollar amount of the payment transactions for a participating payee. It is not adjusted to account for any fees, refunds, or any other amounts.

Q8. Why do merchant acquiring entities report the gross amount of transactions instead of the net amount without fees, chargebacks, etc.? (Added October 21, 2022)

A8. § 6050W(a)(2) requires entities report the gross amount of the reportable payment transactions.

Filing Form 1099-K

Q1. Can Forms 1099-K be filed electronically? (Added October 21, 2022)

A1. Yes. Forms 1099-K can be filed electrically through the FIRE (Filing Information Returns Electronically) system. Any person that files 250 or more Forms 1099-K for any calendar year must file those Forms 1099-K electronically. The IRS encourages filers who have less than 250 information returns to file electronically as well.

For more information, review Publication 1220, Specifications for Filing Forms 1097, 1098, 1099, 3921, 3922, 5498, 8935, and W-2G Electronically. If you are considering filing on paper, review General Instructions for Certain Information Returns.

Q2. Can payee statements be furnished to participating payees electronically? (Added October 21, 2022)

A2. Yes. With the participating payee’s prior consent, payee statements may be provided electronically. This consent must be made electronically in a way that shows the recipient can access the statement in the electronic format in which it will be furnished (see Treas. Reg. § 1.6050W-2, Electronic furnishing of information statements for payments made in settlement of payment card and third-party network transactions, for instructions for receiving consent from participating payees). If a payee statement is furnished electronically, an email address for the payment settlement entity may be provided in lieu of a phone number.

Q3. Who is responsible for reporting payment card transactions? (Added October 21, 2022)

A3. The merchant acquiring entity that transfers funds to the participating payee is responsible for reporting the gross amount of reportable transactions.

A merchant acquiring entity can outsource the processing of the transactions to a processor that may share the contractual obligation to pay the merchant. When both a merchant acquiring entity and a processor have a contractual obligation to pay the merchant, the entity that submits the instructions to transfer funds to the merchant’s account is responsible for preparing and furnishing a payee statement to the participating payee and filing Form 1099-K, Payment Card and Third-Party Network Transactions, with the IRS.

Q4. Who is responsible for reporting third party network transactions? (Added October 21, 2022)

A4. The third-party settlement organization or its electronic payment facilitator is responsible for reporting the gross amounts of reportable transactions paid to participating payees in their network.

Q5. Is there a de minimis exception for reporting payments to participating payees of third-party network transactions on Forms 1099-K for a third-party settlement organization? (Added October 21, 2022)

A5. Yes. There is a de minimis exception from reporting for third party settlement organizations with respect to third party network transactions. For returns for calendar years beginning after 2021, if payments to a participating payee for goods and services during the calendar year do not exceed $600, there is no filing requirement with respect to that participating payee.

Note: For calendar years beginning prior to 2022, if payments to a participating payee exceed $20,000 during the calendar year, and the total number of transactions exceeds 200, there is a filing requirement for that participating payee. If either (or both) of the limitations are not met, then there is no reporting requirement with respect to that participating payee.

Q6. Is there a de minimis exception for reporting on Forms 1099-K for payment card transactions? (Added October 21, 2022)

A6. No. There is not a de minimis exception for reporting payment card transactions. ALL payment card transactions must be reported on Form 1099-K.

Q7. Are sales paid for by stored-value cards or gift cards reportable payment card transactions? (Added October 21, 2022)

A7. It depends. Sales paid for by stored-value cards or gift cards are: • Reportable if the card is accepted by a network of persons unrelated to the issuer and each other. • Not reportable when the card is only accepted as payment by the issuer or someone who is related to the issuer of the card (e.g., a subsidiary company or the company itself). Under these circumstances, the stored-value cards do not fit the definition of a payment card and sales made with such cards are therefore not reportable.

For the definition of unrelated persons see § 267(b), Relationships, of the Internal Revenue Code, and § 267(e)(3), Constructive Ownership in the Case of Partnerships, or § 707(b)(1), Certain Sales or Exchanges of Property with Respect to Controlled Partnerships, Losses Disallowed.

Q8. How is reporting conducted when multiple payees receive allocable revenue from a person to whom payments are made by a payment settlement entity? (Added October 21, 2022)

A8. The most common example of this situation is when a franchisor processes all the merchant card transactions of multiple franchisees and distributes payments accordingly. For example, when a corporation receives payments from a bank on behalf of multiple payees, the corporation is treated as a participating payee with respect to the bank and as a payment settlement entity with respect to the payees to whom the corporation distributes the payments. The bank is required to report the gross amount of reportable transactions settled through the corporation. In turn, the corporation is required to report the allocable transactions of the payees to whom the corporation distributes the payments. Under the statute and regulations, the corporation is an “aggregated payee.

Q9. Can the entity responsible for filing Form 1099-K contract with a third party to prepare and file these returns? (Added October 21, 2022)

A9. Yes. However, the entity responsible for filing (i.e., the entity that submits the instructions to transfer funds) is liable for any applicable penalties under § 6721, Failure to File Correct Information Returns, and § 6722, Failure to Furnish Correct Payee Statements, if the reporting requirements are not met. In addition, the name, address and Taxpayer Identification Number of the entity responsible for filing must be reported on Form 1099-K, Payment Card and Third-Party Network Transactions, in the box for the filer’s information.

Q10. How can payee Taxpayer Identification Numbers (TIN) be verified? (Added October 21, 2022)

A10. Verification of payee TINs is done through the Taxpayer Identification Number (TIN) Matching Program. For further information please visit General Instructions for Certain Information Returns – Introductory Material or call 866-255-0654

Q11. Whose merchant card payments must be reported? (Added October 21, 2022)

A11. Merchant acquiring entities must report the gross amount of reportable payment transactions of any participating payee for whom they settle payment card transactions. A payment card transaction is any transaction in which a payment card or any indicia thereof (such as a credit card number) is accepted as payment.

Q12. Whose third-party network transactions must be reported? (Added October 21, 2022)

A12. For calendar years beginning after 2021, third party settlement organizations must report the gross amounts of reportable payment transactions of any participating payee for whom they settle payments using their third-party payment network provided that the gross amount of the payee’s third-party network transactions exceed $600 during the calendar year, regardless of the number of transactions.

Note: For calendar years prior to 2022, third party settlement organizations reported the gross amount of reportable payment transactions of any participating payee for whom they settled payments using their third-party payment network provided that a payee’s third-party network.

Q13. Who reports payment card transactions when a payment settlement entity contracts with a third party, such as an electronic payment facilitator, to settle reportable transactions? (Added October 21, 2022)

A13. The entity submitting the instructions to transfer funds to the participating payee’s account is responsible for reporting payment card transactions. In this case, the third-party entity is responsible for reporting, because it is the entity submitting the instructions to transfer the funds in settlement of the transactions.

Q14. If transactions are already reportable under § 6041 or § 6041A, must they be reported again by payment settlement entities (PSE)? (Added October 21, 2022)

A14. No, these transactions are not reported twice. If a transaction is reportable by a PSE under both § 6041, Information at Source, or § 6041A(a), Returns Regarding Payments Of Remuneration For Services And Direct Sales, and under § 6050W, Returns Relating To Payments Made In Settlement Of Payment Card And Third Party Network Transactions, the transaction must be reported on Form 1099-K, Payment Card and Third Party Network Transactions. They are not reported on Form 1099-MISC, Miscellaneous Income.

Q15. Can the person required to make the information return under § 6050W and to secure the TIN necessary to make the return shift the economic burden to the participating payee? (Added October 21, 2022)

A15. No. The Internal Revenue Code (IRC) requires payment settlement entities or in some cases an electronic payment facilitator to file information returns and to furnish payee statements with respect to each participating payee to whom payments in settlement of reportable payment transactions are made. These statutory obligations apply regardless of whether the participating payee pays a fee. Moreover, if a payment settlement entity or an electronic payment facilitator fails to comply with these statutory obligations, it is subject to penalties under § 6721, Failure To File Correct Information Returns, and § 6722, Failure To Furnish Correct Payee Statements. Because federal law requires payment settlement entities or electronic payment facilitators to file information returns and to furnish payee statements, such entities are precluded from collecting fees for costs incurred in fulfilling these requirements.

Q16. How should a merchant acquiring entity report transactions if a payee has receipts classified under more than one Merchant Category Code (MCC)? (Added October 21, 2022)

A16. If a payee has receipts classified under more than one MCC, the merchant acquiring entity may either:

- File separate Form 1099-K, Payment Card and Third-Party Network Transactions, reporting the gross reportable transaction amounts attributable to each MCC, or

- File a single Form 1099-K reporting gross reportable transaction amounts and the MCC that corresponds to the largest portion of total gross receipts.

Additionally, if a merchant acquiring entity (or its processor) employs an industry classification system other than or in addition to MCCs, the merchant acquiring entity should assign to each payee an MCC that most closely corresponds to the description of the payee’s business.

Q17. Does a third-party settlement organization have to report Merchant Category Codes (MCC)? (Added October 21, 2022)

A17. No. Third party settlement organizations do not use MCC codes to classify payees. Therefore, they do not complete Box 2 of Form 1099-K, Payment Card and Third-Party Network Transactions.

Q18. If another code provision already requires backup withholding of a reportable transaction, does the backup withholding provision under § 6050W still apply? (Added October 21, 2022)

A18. The regulations do not eliminate the backup withholding requirements under § 6050W, Returns Relating to Payments Made In Settlement Of Payment Card And Third Party Network Transactions, under any circumstances, even where the potential for duplicate withholding exists.

Q19. Are payment settlement entities required to report the transactions of governmental units, whether state or federal? (Added October 21, 2022)

A19. Yes. The term participating payees includes any governmental unit.

Q20. Are foreign payment settlement entities subject to the reporting requirements? (Added October 21, 2022)

A20. Yes. A payment settlement entity may be a domestic or foreign entity.

Issue 6: Notice 2023-3, 12/29/2022, § 162 Business Use of Auto—Optional Standard Mileage Rates for 2023

Beginning on January 1, 2023, the standard mileage rates for the use of a car (also vans, pickups or panel trucks) will be:

- 65.5 cents per mile driven for business use, up 3 cents from the midyear increase setting the rate for the second half of 2022.

- 22 cents per mile driven for medical or moving purposes for qualified active-duty members of the Armed Forces, consistent with the increased midyear rate set for the second half of 2022.

- 14 cents per mile driven in service of charitable organizations; the rate is set by statute and remains unchanged from 2022.

These rates apply to electric and hybrid-electric automobiles, as well as gasoline and diesel-powered vehicles.

Notice 2023-03 contains the optional 2023 standard mileage rates, as well as the maximum automobile cost used to calculate the allowance under a fixed and variable rate (FAVR) plan. In addition, the notice provides the maximum fair market value of employer-provided automobiles first made available to employees for personal use in calendar year 2023 for which employers may use the fleet-average valuation rule in or the vehicle cents-per-mile valuation rule.

Issue 7: Frequently Asked Questions About New Hire Reporting

On December 21, 2022, the Office of Child Support Enforcement (OCSE) published a list of answers to employer questions about new hire reporting.

Federal law states that an “employer” for new hire reporting purposes is the same as for federal income tax purposes – as defined by § 3401(d) – and includes any governmental entity or labor organization. At a minimum, in any case where an employer is required to have an employee complete a Form W-4 (Employee Withholding Certificate), the employer must meet the New Hire reporting requirements.

Importance of a national directory. According to the OSCE’s questions and answers, more than 30% of child support cases involve parents who do not live in the same state as their children. By matching this new hire data with child support case participant information at the national level, the OCSE assists states in locating parents who are living in other states.

Quarterly data outdated. The OCSE explains that quarterly wage data is often outdated when the child support office receives it. There can be as much as a six-month lag between the time the data is submitted and when it is available to the child support office. The OCSE explains that with new hire reporting, data are available within a significantly shorter time period. Because data is more current, noncustodial parents can be located more quickly, allowing child support orders to be established and/or enforced more quickly.

Secure data. The OCSE says that the security and privacy of new hire data are important issues for all those involved in this nationwide program. Federal law requires all states to establish safeguards for confidential information handled by the state agency. All state data is transmitted over secure and dedicated lines to the National Directory of New Hire (NDNH). Federal law also requires that the Secretary of Health and Human Services (HHS) establish and implement safeguards to protect the integrity and security of information in the NDNH and restrict access to and use of the information to authorized persons and for authorized purposes.

Submitting data. New Hire reports should be sent to the State Directory of New Hire in the state where the employee works. Federal law identifies three methods for submitting New Hire information: (1) first class mail, (2) magnetic tapes, or (3) electronically. Some states also offer additional options, such as fax, email, phone, and website transmissions. The employer’s state new hire contact can provide instructions on where and how to send new hire information. Federal employers report New Hire data directly to the NDNH.

Report timing. Employers sending new hire reports by magnetic tape or electronically must make two monthly transmissions not less than 12 or more than 16 days apart. The OCSE says that employers should contact the state where the new hire reports are submitted for all technical information regarding electronic reporting.

What to submit? Federal law requires employers to collect and report these seven data elements:

(1) employee’s name,

(2) employee’s address,

(3) Social Security number,

(4) date of hire (the date the employee first performs services for pay),

(5) employer’s name,

(6) employer’s address, and

(7) federal employer identification number (EIN).

Penalties. States have the option of imposing civil monetary penalties for noncompliance. Federal law mandates that if a state chooses to impose a penalty on employers for failure to report, the fine may not exceed $25 per newly hired employee. If there is a conspiracy between the employer and employee not to report, that penalty may not exceed $500 per newly hired employee. States may also impose non-monetary civil penalties under state law for noncompliance.

Multi-state employer reporting. Multi-state employers have the following two reporting options: (1) report newly hired employees to the states where they work, or (2) select one state where the employees work and report all new hires to the selected state. If the employer chooses the second option, it must register with the HHS as a multi-state employer, designate the state that it will report, submit the new hires electronically or by magnetic tape to the chosen state chosen no more than twice a month (12 to 16 days apart

The OCSE’s list contains several other questions and answers on new hire reporting.

Issue 8: IRS Opens Free File Portal for Information Returns – IR 2023-14

Businesses can now file Form 1099 series information returns using a new online portal, available free from the IRS. Known as the Information Returns Intake System (IRIS), this electronic filing service is free, secure and requires no special software. Available to any business of any size, IRIS may be especially helpful to any small business that currently submits its 1099 forms on paper to the IRS.

Filers can use the platform to create, upload, edit and view information and download completed copies of 1099-series forms for distribution and verification.

With IRIS, businesses can e-file both small and large volumes of 1099-series forms by either keying in the information or uploading a file with the use of a downloadable template.

Currently, IRIS accepts Forms 1099 only for tax year 2022 and later.

The IRS encourages any business, especially those that now file on paper, to switch to e-filing through the platform and share in its benefits.

These benefits include:

- E-file security standards keep information safe and protected.

- The portal is an accurate filing method that automatically detects filing errors and provides alerts for missing information.

- Filers can submit automatic extensions and make corrections to information returns filed through the platform.

- The IRS acknowledges receipt of the return in as early as 48 hours.

- The platform keeps issuer information from year to year, and prior years filed through this platform, providing convenience to 1099 filers.

- E-filing eliminates trips to the post office and can reduce office expenses for paper, postage and storage space.

- Enrollment for the IRIS filing platform is now open. Filers should begin the enrollment process immediately.

The Filing Information Returns Electronically (FIRE) system will remain available for bulk filing Form 1099 series and the other information returns through at least the 2023 filing season.

To enroll in IRIS, users must first apply for a Transmitter Control Code (TCC) and will need to log in with their ID.me account or with an existing IRS username. According to the IRIS taxpayer portal user guide, application processing may take up to 45 calendar days, and statuses can be checked on the application summary page.

User Guide- Publication 5717 (Rev. 11-2022) (irs.gov)

Issue 9: No Tax Extenders in Budget Bill

While many tax professionals hoped the Consolidated Appropriations Act would include extensions of several expiring tax benefits, Congressional negotiators could not agree on the provisions to be included in the legislation sent to President Biden to sign. The pandemic-related tax changes that were considered for extension included:

- Expansion of the child tax credit.

- Expansion of the child and dependent care credit.

- Election to defer last in, first out (LIFO) accounting provisions.

- Deferral of cancellation of debt income.

- Deferral of income from built-in gains.

Congress also declined to add provisions to the legislation that would have postponed the implementation of some aspects of the Tax Cuts and Jobs Act of 2017 that went into effect for the 2022 and 2023 tax years. Those changes include the following:

- Requiring businesses to deduct their R&D expenses over five years beginning in 2022.

- Reducing bonus depreciation from the full cost of the asset to 80% for 2023 and eliminating it by 2027.

- Setting limits on the number of interest payments on debt that can be deducted by a corporation starting in 2022.

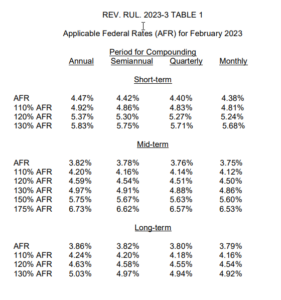

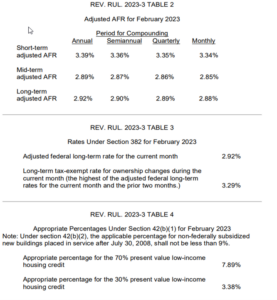

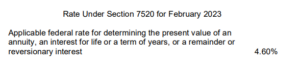

Issue 10: Applicable Federal Rates for February 2023, Rev. Rul. 2023-3