In this Issue:

- Beneficial Ownership Information (BOI) & the Corporate Transparency Act (CTA) Resource Materials Developed by A.J. Reynolds

- Taxpayers Should Continue to Report All Cryptocurrency, Digital Asset Income

- Business Digital Asset Transaction Reporting Delayed – Form 8300

- E-file Unavailable for Form 990-T and Form 1120-POL until March 17, 2024. An Extension Can be Filed for Both Forms or Paper File with Form 1120-POL

- Emergency Savings Account Guidance Issued

- Reminder of IRS Rules on Stockpiled Returns

- IRS and Treasury Reach Major Milestone Implementing Key Provisions Using the IRS Energy Credits Online Elective Pay and Transferability Tool

- IRS Provides Tips for Applying to the ERC’s Voluntary Disclosure Program

- New Information Return Filing Threshold

- Reminder: Payers May Receive Notices CP2100 and 2100A if They Filed an Information Return with Errors

- IRS Extends Popular Flexibilities Set to Expire; Electronic Signatures and Encrypted Email Enhance the Taxpayer Experience

- Excess Social Security Withheld – How to Fix

- The Cave – IRS Underground Storage Facility – Take a Look – TIGTA Report

- EPA Updates List of Clean Vehicles for 2024

- Information on the Energy Efficient Home Improvement Credit

- EO Determination Letters New Procedure

- Two New Technical Guides Published

- IRS Provides Penalty Relief on Nearly 5 million 2020, 2021 Tax Returns; Restart of Collection Notices in 2024 Marks End of Pandemic-Related Pause

- Business Tax Account expands to S corporations, Partnerships.

- Applicable Federal Rates for February 2024, Rev. Rul. 2024-03

2024 Webinar Schedule Coming Soon!

Issue 1: Beneficial Ownership Information (BOI) & the Corporate Transparency Act (CTA) Resource Materials Developed by A.J. Reynolds

These documents are provided for your use.

There has been much discussion concerning this new reporting requirement. We urge you to check with your state accounting offices as to whether this is a “legal” issue and services can only be provided by an attorney or if a tax professional can choose to provide this service.

In addition, please check with your insurance provider to see if this reporting is covered by your insurance company. Some companies are not covering this required reporting.

There is no requirement for any attorney or tax professional to provide this service – the reporting can be done by the entity itself if they so choose.

AJ has provided documents for a notification of the new law and a summary of its requirements. The documents also include information that your practice will not be providing services and for those who chose to provide services, as well as basic information on the information needed to report and wording a separate engagement letter.

Summary of the Corporate Transparency Act (CTA)

January 1, 2024, the Beneficial Ownership Information (BOI) reporting went into effect. This reporting requirement is the result from the passage of the National Defense Authorization Act for Fiscal Year 2021, which included the Corporate Transparency Act (the CTA). This Act will affect every LLC, S Corporation, C Corporation, and any other entity required to be “registered” with their respective state. This act was developed to curve and expose illicit activity, money laundering, and concealment of ownership. Furthermore, this Act was developed to protect the United States and our National Security Interest.

The course will present tax professionals with up-to-date valuable knowledge on this act and how it will impact their practice and clients. In addition, we will provide a how to file the BOI reports either using FinCEN’s online filing or by completing a pdf document and uploading at a later date on FinCEN’s website.

Information letter to Clients regarding Beneficial Ownership Information (BOI) and that your Firm will NOT be providing BOI reporting services.

New Federal Reporting Requirement for Beneficial Ownership Information (BOI)

We are writing to you regarding new reporting requirements for many businesses, which can include Single member and multi member LLC’s, C and S Corporations. Starting January 1, 2024, certain businesses will be required to comply with the Corporate Transparency Act (CTA) which includes the filing of Beneficial Ownership (BOI) reports. These reports will be administered by the Financial Crimes Enforcement Network (FinCEN) and established a database of companies’ beneficial ownership information to be used by law enforcement. This is not an Internal Revenue Service (IRS) issue.

There are significant penalties for missing filing deadlines, including criminal (fines and /or imprisonment) or civil (monetary) penalties. There is a $500 per day penalty, up to $10,000, and imprisonment of up to two years for the WILLFUL failure to timely file initial or updated reports.

Assisting with compliance and or filing of the CTA, including BOI reporting, is not within the scope of the services we provide. It will be your exclusive responsibility to comply with CTA, including its BOI reporting requirements. Information can be found at https://www.fincen.gov/boi. Please consult with legal counsel on additional questions and or concerns regarding how BOI reporting requirements and issues affect your company.

As stated previously, compliance with the CTA, including the BOI reporting applies to most businesses including single member LLCs, which are treated as a disregarded entity for income tax reporting. A disregarded entity does have a filing requirement with the Internal Revenue Service and now also with the Financial Crimes Enforcement Network (FINCEN).

Finally, we wish to emphasize that we are sending you this letter to make you aware of these new current reporting requirements, associated risks, and suggest you contact legal counsel to assist you with the CTA and related BOI filings for entities that you own or control.

Sincerely,

XXXXXXXX

My Tax Practice

______________________________________________________________________

Information letter to Clients regarding Beneficial Ownership Information (BOI) filings, regardless of your office plans on assisting your client with the BOI

New Federal Reporting Requirement for Beneficial Ownership Information (BOI)

This letter is to make you aware of reporting requirements that go into effect on January 1, 2024, that may require your business entity to report its beneficial ownership information to the Federal government.

Beginning on January 1, 2024, many companies in the United States will have to report information about their beneficial owners, i.e., the individuals who ultimately own or control the company. They will have to report the information to the Financial Crimes Enforcement Network (FinCEN). FinCEN is a bureau of the U.S. Department of the Treasury.

NOTE: This will be a free filing that companies can complete themselves. Be wary of official-looking mail from a third-party company offering to complete the beneficial ownership reporting on behalf of your company for a fee.

Do I Need to Report?

Most businesses are small businesses that may need to file. Your company may need to report information about its beneficial owners if it is:

- A corporation, a limited liability company (LLC), or was otherwise created in the United States by filing a document with a secretary of state or any similar office under the law of a state or Indian tribe; or

- A foreign company and was registered to do business in any U.S. state or Indian tribe by such a filing.

How Do I Report?

Reporting companies will have to report beneficial ownership information electronically through FinCEN’s website: www.fincen.gov/boi.

When Do I Report?

- Reports will be accepted starting on January 1, 2024.

- If your company was created or registered before January 1, 2024, you will have until January 1, 2025, to report BOI.

- If your company is created or registered on or after January 1, 2024, and before January 1, 2025, you must report BOI within 90 days of notice of creation or registration.

- If your company is created or registered on or after January 1, 2025, you must report BOI within 30 days of notice of creation or registration.

- If there is any change to the required information about your company or its beneficial owners in a BOI report that your company filed, your company must file an updated BOI report no later than 30 days after the date on which the change occurred. The same 30-day timeline applies to changes in information submitted by an individual in order to obtain a FinCEN identifier. A reporting company is not required to file an updated report for any changes to previously reported personal information about a company applicant.

There are significant penalties for missing filing deadlines, including criminal (fines and /or imprisonment) or civil (monetary) penalties. There is a $500 per day penalty, up to $10,000, and imprisonment of up to two years for the WILLFUL failure to timely file initial or updated reports.

It will be your exclusive responsibility to comply with CTA, including its BOI reporting requirements. Information can be found at https://www.fincen.gov/boi. Please consult with legal counsel on additional questions and or concerns regarding how BOI reporting requirements and issues affect your company.

Finally, we wish to emphasize that we are sending you this letter to make you aware of these new current reporting requirements, associated risks, and suggest you contact legal counsel to assist you with the CTA and related BOI filings for entities that you own or control.

Sincerely,

XXXXXXXXX

My Tax Practice

_________________________________________________________________________________________

Minimum language to be used in all tax preparation (1040, 1065, 1120S, and 1120) engagement letters:

Please be aware there are specific new reporting requirements involving certain types of companies regarding compliance with the Corporate Transparency Act (CTA), including Beneficial Ownership Information (BOI) reporting. Aiding with this compliance is Not within the scope of this engagement letter.

(Remember, this language should be placed in your regular engagement letter for the preparation of appropriate income tax returns, i.e. Forms 1040, 1065, 1120S, or 1120)

Additional language to be used with the above in all tax preparation (1040, 1065, 1120S, and 1120) engagement letters:

Our firm will Not assist with any BOI reporting. Furthermore, our firm will assume No liability stemming from your neglect on not filing this BOI report.

For additional information, please see https:/www.fincen.gov/boi and /or contact legal counsel.

____________________________________________________________________

Basic Sample Engagement Letter for preparing Beneficial Ownership Information (BOI) reports of U.S. formed companies: (legal review of this document before use is highly recommended)

General Engagement Letter for Beneficial Ownership Information (BOI) reports of United States formed companies

This engagement letter is to inform you, the taxpayer, of the services we will provide you, and the responsibilities you have for preparation of the BOI report.

Starting on January 1, 2024, BOI reports must be filed electronically using FinCEN’s secure filing system. FinCEN will store BOI reports in a centralized database and only share this information with authorized users for purposes specified by law. The database will use rigorous information security methods and controls typically used in the Federal government to protect non-classified yet sensitive information systems at the highest security level. _____Initial

Reporting companies created or registered to do business before January 1, 2024, will have additional time — until January 1, 2025 — to file their initial BOI reports. _____Initial

Reporting companies created or registered on or after January 1, 2024, and before January 1, 2025, have 90 calendar days after receiving actual or public notice that their company’s creation or registration is effective to file their initial BOI reports. Specifically, this 90-calendar day deadline runs from the time the company receives actual notice that its creation or registration is effective, or after a secretary of state or similar office first provides public notice of its creation or registration, whichever is earlier. _____Initial

Reporting companies created or registered on or after January 1, 2025, will have 30 calendar days from actual or public notice that the company’s creation or registration is effective to file their initial BOI reports. _____Initial

Tax Return Preparation

We will prepare your BOI report based on the information you provide. Services for preparation of your return do not include auditing or verification of information provided by you.

Our fee will be based upon the amount of time expended plus out-of-pocket expenses. However, a minimum fee of $ 500.00 will be charged for the preparation of this BOI Report. Payment for these services will be due upon receipt. _____Initial

Any information provided to our office will be treated as confidential and is subject to disclosure by our firm only at your request or when required by law or regulatory matters.

Taxpayer Responsibilities

You agree to providing our office with the following information concerning your applicable Reporting Company, which can include a Single Member LLC, Multi Member LLC, S & C Corporation and any company created by the filing of a document with a secretary of state or any similar office under the law of a State or Indian tribe. Filing a document with a government agency to obtain (1) an IRS employer identification number, (2) a fictitious business name, or (3) a professional or occupational license does not create a new entity, and therefore does not make a sole proprietorship filing such a document a reporting company. _____Initial

- Reporting Company _____Initial

- Full legal name

- Any and all trade name or “doing business as” (DBA) name

- Complete current U.S. address

- State, Tribal, or foreign jurisdiction of formation

- Internal Revenue Service (IRS) Taxpayer Identification Number (TIN)

- Beneficial Owner _____Initial

- Full legal name

- Date of birth

- Complete current address (residential, no P.O. Boxes)

- Unique identifying number with image

- State Driver’s License

- S. Passport

- ID document issued by a state, local government, or tribe

- If none of the above, then foreign passport

- Company Applicant (‘Reporting Company’ formed January 1, 2024, or thereafter) _____Initial

- Full legal name

- Date of birth

- Complete current address (residential, no P.O. Boxes)

- Unique identifying number with image

- State Driver’s License

- S. Passport

- ID document issued by a state, local government, or tribe

- If none of the above, then foreign passport

Updates or Corrections

If there is any change to the required information about your company or its beneficial owners in a BOI report that your company filed, your company must file an updated BOI report no later than 30 days after the date on which the change occurred. The same 30-day timeline applies to changes in information submitted by an individual in order to obtain a FinCEN identifier. A reporting company is not required to file an updated report for any changes to previously reported personal information about a company applicant. _____Initial

Furthermore, the following must be reported to our office no later than 10 days after a particular change so we can file the updated report within 30 days to FinCEN. Some likely triggers and or examples (not inclusive) of the changes that would require an updated beneficial ownership information report:

- Any change to the information reported for the reporting company, such as registering a new business name, trade name or DBA. _____Initial

- A change in beneficial owners, such as a new CEO, or a sale that changes who meets the ownership interest threshold of 25 percent, or the death of a beneficial owner. _____Initial

- Note: When a beneficial owner dies, resulting in changes to the reporting company’s beneficial owners, report those changes within 30 days of when the deceased beneficial owner’s estate is settled. The updated report should, to the extent appropriate, identify any new beneficial owners. _____Initial

- Any change to a beneficial owner’s name, address, or unique identifying number previously provided to FinCEN. _____Initial Furthermore, if a beneficial owner obtained a new driver’s license or other identifying document that includes a changed name, address, or identifying number, the reporting company also would have to file an updated beneficial ownership information report with FinCEN, including an image of the new identifying document. _____Initial

- Keep in mind the update requirement related to the special reporting rule for a minor child. When a beneficial owner that was a minor child reaches the age of majority, you must file an updated BOI report, identifying the individual as a beneficial owner and, if warranted, replacing their parent or legal guardian’s information with their own. _____Initial

If an inaccuracy is identified in a BOI report that your company filed, your company must correct it no later than 30 days after the date your company became aware of the inaccuracy or had reason to know of it. This includes any inaccuracy in the required information provided about your company, its beneficial owners, or its company applicants. The same 30-day timeline applies to inaccuracies in information submitted by an individual in order to obtain a FinCEN identifier. _____Initial

Finally, our firm assumes no liability stemming from your neglect of not providing applicable information as detailed above for filing the BOI report. _____Initial

Signatures. By signing below, you acknowledge that you have read, understand, and accept your obligations and responsibilities and that you understand our responsibility in preparing your BOI report as explained above.

_______________________________ ___________________ ___________________

Taxpayer Signature Title Printed Name

___________________ ___________________________

Date Phone Number

_____________________________________

Email address

Issue 2: Taxpayers Should Continue to Report All Cryptocurrency, Digital Asset Income

The Internal Revenue Service is reminding taxpayers that they must again answer a digital asset question and report all digital asset related income when they file their 2023 federal income tax return, as they did for their 2022 federal tax returns.

The question appears at the top of Forms 1040, Individual Income Tax Return; 1040-SR, U.S. Tax Return for Seniors; and 1040-NR, U.S. Nonresident Alien Income Tax Return, and was revised this year to update wording. The question was also added to these additional forms: Forms 1041, U.S. Income Tax Return for Estates and Trusts; 1065, U.S. Return of Partnership Income; 1120, U.S. Corporation Income Tax Return; and 1120S, U.S. Income Tax Return for an S Corporation.

Depending on the form, the digital assets question asks this basic question, with appropriate variations tailored for corporate, partnership or estate and trust taxpayers:

“At any time during 2023, did you: (a) receive (as a reward, award or payment for property or services); or (b) sell, exchange, or otherwise dispose of a digital asset (or a financial interest in a digital asset)?”

What is a digital asset?

A digital asset is a digital representation of value that is recorded on a cryptographically secured, distributed ledger or any similar technology. Common digital assets include:

- Convertible virtual currency and cryptocurrency.

- Stablecoins.

- Non-fungible tokens (NFTs).

Everyone must answer the question

Everyone who files Forms 1040, 1040-SR, 1040-NR, 1041, 1065, 1120, 1120 and 1120S must check one box answering either “Yes” or “No” to the digital asset question. The question must be answered by all taxpayers, not just by those who engaged in a transaction involving digital assets in 2023.

When to check “Yes”

Normally, a taxpayer must check the “Yes” box if they:

- Received digital assets as payment for property or services provided.

- Received digital assets resulting from a reward or award.

- Received new digital assets resulting from mining, staking and similar activities.

- Received digital assets resulting from a hard fork (a branching of a cryptocurrency’s blockchain that splits a single cryptocurrency into two).

- Disposed of digital assets in exchange for property or services.

- Disposed of a digital asset in exchange or trade for another digital asset.

- Sold a digital asset; or

- Otherwise disposed of any other financial interest in a digital asset.

How to report digital asset income

In addition to checking the “Yes” box, taxpayers must report all income related to their digital asset transactions. For example, an investor who held a digital asset as a capital asset and sold, exchanged or transferred it during 2023 must use Form 8949, Sales and other Dispositions of Capital Assets, to figure their capital gain or loss on the transaction and then report it on Schedule D (Form 1040), Capital Gains and Losses. A taxpayer who disposed of any digital asset by gift may be required to file Form 709, United States Gift (and Generation-Skipping Transfer) Tax Return.

If an employee was paid with digital assets, they must report the value of assets received as wages. Similarly, if they worked as an independent contractor and were paid with digital assets, they must report that income on Schedule C (Form 1040), Profit or Loss from Business (Sole Proprietorship). Schedule C is also used by anyone who sold, exchanged or transferred digital assets to customers in connection with a trade or business.

When to check “No”

Normally, a taxpayer who merely owned digital assets during 2023 can check the “No” box as long as they did not engage in any transactions involving digital assets during the year. They can also check the “No” box if their activities were limited to one or more of the following:

- Holding digital assets in a wallet or account.

- Transferring digital assets from one wallet or account they own or control to another wallet or account they own or control: or

- Purchasing digital assets using U.S. or other real currency, including through electronic platforms.

For a set of frequently asked questions (FAQs) and other details, visit the Digital Assets page on IRS.gov.

Issue 3: Business Digital Asset Transaction Reporting Delayed – Form 8300

Businesses are not required to report digital transactions on Form 8300, Report of Cash Payments over $10,000 Received in a Trade or Business, until the IRS and Treasury Department issue regulations on the topic. Statutory changes made by the Infrastructure Investment and Jobs Act that were to take effect Jan. 1 would have required businesses to file Form 8300 for a transaction, or series of transactions, where payment was received in digital assets with a fair market value of $10,000 or more within 15 days.

Announcement 2024-4 says the IRS and Treasury intend to issue proposed regulations on reporting the receipt of digital assets to give the public the opportunity for comment on the reporting procedures. The announcement does not affect the Form 8300 reporting requirements that were in place prior to the enactment of the Infrastructure Investment and Jobs Act.

Issue 4: E-file Unavailable for Form 990-T and Form 1120-POL until March 17, 2024. An Extension Can be Filed for Both Forms or Paper File with Form 1120-POL

News release 2024-15 announced that taxpayers will not be able to electronically file Form 990-T, Exempt Organization Business Income Tax Return, or Form 1120-POL, U.S. Income Tax Return for Certain Political Organizations, until March 17, 2024.

IRS system upgrades mean e-filing of Forms 990-T and Forms 1120-POL (including returns on extension) with due dates from Jan. 15, 2024, to March 15, 2024, is currently unavailable.

Taxpayers with due dates on April 15, 2024, and later will be able to e-file Forms 990-T and Forms 1120-POL on time.

Returns due from Jan. 15, 2024, to March 15, 2024:

- Form 990-T, Exempt Organization Business Income Tax Return

Organizations subject to unrelated business income tax (UBIT) are required by law to file Form 990-T electronically. An organization with a Form 990-T due from Jan.15, to March 15, 2024, should request an automatic six-month extension of time to file by submitting Form 8868, Application for Extension of Time To File an Exempt Organization Return, by the due date of the return. The IRS estimates only about 2,000 of the 200,000 Form 990-T filers have a due date in this time period and are affected by this.

Any balance due must be submitted with Form 8868 to avoid interest and penalties. Beginning March 17, 2024, organizations will be able to timely e-file Form 990-T by the extended due date.

If an affected organization does not timely submit an extension, or if the extended due date falls within the period from Jan. 15, 2024, to March 15, 2024, and the organization consequently does not timely e-file its Form 990-T, it should include with its late e-filed Form 990-T a request that any penalties for late filing not be imposed due to reasonable cause. The reasonable cause request should reference that e filing was not available as of the due date of the return.

- Form 1120-POL, U.S. Income Tax Return for Certain Political Organizations. Organizations filing a Form 1120-POL that is due from Jan. 15, 2024, to March 15, 2024, (including returns on extension) may file on paper. An organization that wishes to e-file a return with an original due date during that period may request an automatic six-month extension of time to file Form 1120-POL by submitting Form 7004, Application for Automatic Extension of Time to File Certain Business Income Tax, Information, and Other Returns, and paying the full balance due with that form to avoid interest and penalties. Only a handful of these organizations typically file electronically in the affected time period.

Filing only to make an elective payment election for Clean Energy Credits

The electronic filing delay will not affect the ability of government entities and Indian tribal governments — that are not subject to UBIT — to timely file Form 990-T to make an elective payment election (EPE) for Clean Energy Tax Credits. EPE is available for tax years beginning in 2023, therefore the returns will not be due until after March 17.

In addition, under the law, an entity cannot receive the elective payment amount before the original due date of the return. Filing before the original due date for the return will not shorten the time for payment. While government entities and Indian tribal governments that are not subject to UBIT are not subject to the electronic filing mandate, the IRS encourages all taxpayers to e-file.

Issue 5: Emergency Savings Account Guidance Issued

Initial guidance for employers seeking to implement pension-linked emergency savings accounts (PLESAs) has been released. The guidance (Notice 2024-22) includes reasonable measures employers can take to discourage the potential manipulation of the PLESA matching contribution rules. PLESAs were authorized under the SECURE 2.0 Act and allow defined contribution plans to offer individual accounts designed to let employees save for financial emergencies.

Employers can offer PLESAs for plan years beginning after 2023, which means that some employees could have started contributing to their accounts on Jan. 1. If their employers offer a PLESA plan, eligible employees can contribute to the plan, even if they don’t participate in the employer’s defined contribution plan. The maximum balance for a participant’s PLESA plan attributable to contributions is $2,500, but employers can set a lower limit.

PLESAs are treated as a type of designated Roth accounts. Therefore, contributions are not deductible, but withdrawals are usually tax-free. Participants can withdraw PLESA funds, in whole or in part, at least once a month.

Issue 6: Reminder of IRS Rules on Stockpiled Returns

Electronic return originators (EROs) are reminded that the IRS does not consider returns to be stockpiled if they are for the current filing year and are held before the date the IRS begins accepting electronic submissions. The IRS will start accepting and processing 2023 returns on Jan. 29. This is an exception to the general rule that EROs must not stockpile returns.

According to the most recent versions of Pub. 1345, Authorized IRS e-file Providers of Individual Income Tax Returns, and Pub. 4163, Modernized e-File (MeF) Information for Authorized IRS e-File Providers for Business Returns, the IRS views stockpiling as:

- Collecting returns from taxpayer or another authorized e-file provider prior to official acceptance in IRS e-file; or

After being accepted to participate in IRS e-file, stockpiling refers to waiting more than three calendar days to submit the return to the IRS once the ERO has all necessary information for origination.

Issue 7: IRS and Treasury Reach Major Milestone Implementing Key Provisions Using the IRS Energy Credits Online Elective Pay and Transferability Tool

IRS and Treasury has reached a major milestone in implementation of key provisions in the Inflation Reduction Act with more than 1,000 projects registered through the new IRS Energy Credits Online (ECO) tool.

The Inflation Reduction Act created two new credit delivery mechanisms—elective pay (otherwise known as “direct pay”) and transferability — that enable state, local and Tribal governments; non-profit organizations, U.S. territories; and other entities to take advantage of clean energy tax credits.

To facilitate taxpayers receiving a direct payment, transferring a clean energy credit, or claiming a CHIPS credit, the IRS built ECO for taxpayers to complete the pre-file registration process and receive a registration number. The registration number must be included on the taxpayer’s annual return when making a direct payment or transfer election for a clean energy credit.

For the IRS ECO direct pay, transferability, and CHIPS functionality, as of this week approximately 145 entities have requested registration numbers for more than 1,290 projects or facilities located in 40 states and territories, with more than 1,170 projects or facilities pursuing transferability and more than 110 projects or facilities pursuing direct pay. The value of the tax credits for these projects will be determined when the credit recipient files their taxes.

The IRS has published detailed information on how to complete pre-filing registration, including Publication 5884, Inflation Reduction Act (IRA) and CHIPS Act of 2022 (CHIPS) Pre-Filing Registration Tool — User Guide.

The IRS updated Fact Sheet 2023-29 to provide guidance related to critical mineral and battery component requirements for the new, previously owned and qualified commercial clean vehicle credits. Find more information about reliance.

Issue 8: IRS Provides Tips for Applying to the ERC’s Voluntary Disclosure Program

As part of an ongoing initiative aimed at combating dubious Employee Retention Credit (ERC) claims, the IRS recently launched a Voluntary Disclosure Program to help businesses who want to pay back the money they received after filing ERC claims in error. Qualifying clients interested in this program have until March 22 to apply using Form 15434, Application for Employee Retention Credit Voluntary Disclosure Program.

To use this IRS fillable smart form, applicants must:

• Have the current version of Adobe Reader or Acrobat Pro to use the form. See Downloading and Printing tips if you need help getting the most recent free version of Adobe Reader.

• Right-click the link to the form.

• Choose “Save link as” to download the form to their computer.

• Open, fill out, sign and save the Form 15434.

• Submit the application form to the IRS using the IRS Document Upload Tool.

Issue 9: New Information Return Filing Threshold

Business taxpayers and their tax preparers need to remember that as of Jan. 1, the IRS decreased the threshold at which information returns must be electronically filed from 250 to 10.

Until this year, the 250-return e-filing requirement was applied separately to each type of return. Now, e-filing is required if the combined total of information returns is greater than 10.

Those required to file fewer than 10 returns during a calendar year may still do so on paper. To make it easier for businesses to e-file their information returns, the IRS recently launched its Information Returns Intake System (IRIS) to provide a free filing option.

Issue 10: Reminder: Payers May Receive Notices CP2100 and 2100A if They Filed an Information Return with Errors

When banks, credit unions, businesses and other payers file information returns with data that does not match IRS records, the IRS sends them a CP2100 or CP2100A notice. The notices tell payers that the information returns they submitted have a missing or incorrect Taxpayer Identification Number, name or both.

Each notice has a list of payees with the issues the IRS found. Payers need to compare the accounts on the notice with their account records and correct or update their records, if necessary. Payee may also need to correct their backup withholding on payments made to payees.

Tax Tip 2023-75 provides a list of the most common information returns with errors, as well as additional links to further guidance on backup withholding.

Issue 11: IRS Extends Popular Flexibilities Set to Expire; Electronic Signatures and Encrypted Email Enhance the Taxpayer Experience

The Internal Revenue Service has extended certain temporary flexibilities. The acceptance of digital signatures is extended indefinitely until more robust technical solutions are deployed, and encrypted email when working directly with IRS personnel has been extended until Oct. 31, 2025.

The flexibilities, which were put in place during the COVID-19 pandemic, promoted secure and effective communications and were well received by tax professionals and taxpayers who reported that allowing for the use of electronic or digital signatures saved time and resources.

Internal Revenue Manual (IRM) 10.10.1 IRS Electronic Signature (e-Signature) Program was updated to include acceptance of alternatives to handwritten signatures for certain tax forms and the ability to accept images of signatures and digital signatures in compliance interactions.

For a list of allowable signature options, refer to IRM Exhibit 10.10.1-2 on IRS.gov.

In addition, Interim Guidance Memorandum PGLD-10-1023-0002 (PDF) provides temporary guidance on using email with encryption when working person-to-person with IRS personnel to address compliance or resolve issues in ongoing or follow-up authenticated interactions.

Issue 12: Excess Social Security Withheld – How to Fix

The Social Security wage base in an employer’s payroll system was inadvertently updated when the wage base for 2024 was announced in October 2023. This was not caught until early January 2024, and it became apparent that employees who had earned more than the 2023 wage base had too much Social Security tax withheld. How should the employer correct this?

Answer: For this error, it is important that the employer and the affected employees understand that this is an underpayment of cash and not an underpayment of wages. The amount of wages was not affected. The excess withholding was constructively received by the employees but was paid to the IRS instead. To correct the error, the employer should refund the excess withholding to the employees and adjust its deposits for the fourth quarter of 2023.

The excess Social Security withholding should not be converted to income tax withholding, because that would constitute a misapplication of the funds. Nor should the employee recover the funds on the employee’s income tax return. That method is used only when the overpaid employee share of tax is due to multiple employers. Neither of these methods address the overpayment of the employer’s share of the tax.

Ideally, the correction should be made before the employer issues Forms W-2, Wage and Tax Statement, to employees and files the fourth-quarter Form 941, Employer’s Quarterly Federal Tax Return. However, unless the employer is a monthly schedule depositor, it likely deposited the excess taxes with the IRS prior to discovering the error.

The over withheld tax should be refunded to the employees as soon the error is discovered, and the employer should obtain receipts from the employee documenting the refund. The employer should also adjust its payroll records to the correct tax amounts.

If the fourth quarter Form 941 has not been filed, the correct amounts of employee Social Security wages and the computation of the combined employee and employer shares of Social Security tax should be used to compute the amount of Social Security tax reported on Form 941. Employee Forms W-2 should also report the correct amounts of Social Security wages and withheld tax even if the forms are prepared prior to issuing the refunds.

The excess withholding should not affect the wage and tax amounts reported for income tax, Medicare, or Additional Medicare tax withholding. If the employer is a monthly schedule depositor and the fourth-quarter deposit has not been made, the December deposit should be reduced by the amount of excess withholding.

If the taxes have already been deposited, the fourth-quarter Form 941 will show an overpayment, and the employer should request a refund or apply the overpayment to the tax liability for the first quarter of 2024. If the excess is applied to the first-quarter liability, the employer will recover the repaid employee funds and the employer share of tax by reducing tax deposits during the first quarter of 2024.

If the fourth-quarter Form 941 has already been filed reporting the incorrect amounts, corrections can be made by filing Form 941-X, Adjusted Employer’s Quarterly Federal Tax Return or Claim for Refund. The employer may elect either a refund or an adjustment of the overpaid tax and must obtain the written employee statements as required in Part 2 of Form 941-X.

If Forms W-2 have already been filed and issued to employees, the employer must also prepare Forms W-2c, Corrected Wage and Tax Statement, to issue to the affected employees and file with the Social Security Administration. If Forms W-2 were issued to employees but not filed with the SSA, then the employer should correct the electronic file or void the original Copy A if filing on paper and prepare a new Form W-2 with the correct information. The employer should print “CORRECTED” at the top of the employee copies and furnish them to the employee.

Issue 13: The Cave – IRS Underground Storage Facility – Take a Look – TIGTA Report

The IRS stores millions of tax forms in a cave in Missouri. But first – is it really a cave?

The IRS calls it the “C-site.” It’s part of a larger man-made cave complex in Independence, Missouri. The IRS leases 26,000 square feet of the cave to store certain tax forms (one of which they are required to keep for 75 years).

What’s it like working in the cave?

In August 2022, IRS employees working at the C-site reported safety concerns, like rocks falling from the ceiling and poor air quality. IRS management temporarily closed the site soon after, fixed various issues, and then reopened it.

The biggest safety concern is the ladders. Despite not meeting safety standards, they are used sometimes to retrieve boxes that can weigh up to 50 lbs. from shelves as high as 13 feet. In fact, at the time of our visit, three of the five IRS employees were on light duty because of workplace injuries.

The IRS’s lease expires in October 2024, and it’s unclear if they will extend it or find another storage site. The IRS could digitize the more than 143 million pages of documents estimated in storage before the lease expires, but that would require 5 scanners scanning 14,000 pages every hour.

Read the full report to check out the recommendations we made to improve the safety of the cave.

Issue 14: EPA Updates List of Clean Vehicles for 2024

The Environmental Protection Agency (EPA) has updated its website to include 19 models of electric, plug-in hybrid and fuel cell vehicles that may be eligible for a clean vehicle tax credit if they are placed in service in 2024. According to the EPA, 10 models are eligible for up to the full $7,500 credit, while nine are eligible for a credit of up to $3,750. However, because some manufacturers have yet to submit their information to the EPA, the list should not be viewed as final; the agency may add additional models throughout the year.

Beginning Jan. 1, clean vehicle tax credits must be initiated and approved at the time of sale. It is recommended that buyers obtain a copy of the IRS’s confirmation that a time of sale report was successfully submitted by the dealer.

Issue 15: EO Determination Letters New Procedure

Revenue Procedure 2024-5, released on January 2, 2024, provides that EO Determinations will now issue a determination letter to an organization currently recognized as described in Section 501(c)(3) that seeks recognition as described in a different paragraph of Section 501(c).

Section 3.01(1) of Rev. Proc. 2024-5 provides that EO Determinations will issue a determination letter to an organization currently recognized as described in Section 501(c)(3) that seeks recognition as described in a different paragraph of Section 501(c) if the organization establishes that as of the submission date of its application, it:

- Has distributed its assets to another Section 501(c)(3) organization or government entity, and

- Otherwise meets the requirements for the Section 501(c) status requested.

It further provides that the new determination letter will only be effective from the submission date of the new application.

Accordingly, an organization currently recognized as described in Section 501(c)(3) that seeks recognition as described in a different paragraph of Section 501(c) must:

- Represent that its assets have been distributed as of the submission date of its application and provide a description of the assets distributed, the date of distribution and the name, EIN, and address of the recipient and

- Agree to submission (postmark) date for recognition under the new paragraph of Section 501(c)

The required representation may be included with the organization’s supplemental responses in the single PDF file submitted with its Form 1024, Application for Recognition of Exemption Under Section 501(a) or Section 521 of the Internal Revenue Code, or Form 1024-A, Application for Recognition of Exemption Under Section 501(c)(4) of the Internal Revenue Code.

This procedure also applies to an organization automatically revoked under Section 6033(j) that was described in Section 501(c)(3) that seeks retroactive reinstatement as described in a different paragraph of Section 501(c).

Section 501(c)(3) organizations seeking to be recognized as described in Section 501(c)(4) are subject to the same requirement to file Form 8976 within 60 days of formation as new Section 501(c)(4) organizations.

An organization previously described in Section 501(c)(3) that submits Form 8976 within 60 days of seeking to be described in Section 501(c)(4) may have reasonable cause for not filing Form 8976 within 60 days of formation. Such an organization may seek reasonable cause relief from any penalty for late filing Form 8976 by following the instructions in the correspondence from the IRS regarding the penalty.

Issue 16: Information on the Energy Efficient Home Improvement Credit

Notice 2024-13: Beginning January 1, 2023, the energy efficient home improvement credit allows for a credit, subject to certain limitations and caps, equal to 30% of a taxpayer’s expenses for certain energy efficiency improvements and related costs.

Beginning on January 1, 2025, taxpayers claiming the credit must also satisfy a product identification number (PIN) requirement for certain categories of products. Notice 2024-13 requests comments on several general and specific questions relating to this PIN requirement and outlines a PIN assignment system that the IRS is considering.

IR-2023-253 – Treasury, IRS request public comments on product identification number requirement to claim the Energy Efficient Home Improvement Credit

The Department of the Treasury and the Internal Revenue Service issued Notice 2024-13 announcing that the IRS intends to propose regulations to implement the product identification number (PIN) requirement with respect to the energy efficient home improvement credit.

Issue 17: Two New Technical Guides Published

Exempt Organizations and Government Entities have published two new Technical Guides (TG). These guides are comprehensive, issue-specific documents that update and combine the Audit Technique Guides (ATG) with other technical content. Once completed, the TGs replace corresponding ATGs.

The two latest TGs are:

- TG 48: Unrelated Business Income Tax

- TG 14: Credit Unions and Mutual Reserve Funds IRC Section 501(c)(14)

TG 48 provides information on unrelated business income (UBI) and unrelated business income tax (UBIT). The UBIT provisions are found in Sections 511 through 515.

TG 14 discusses the distinct tax exemption criteria of credit unions under Section 501(c)(14)(A) and mutual reserve fund organizations described under Sections 501(c)(14)(B) and (C).

Issue 18: IRS Provides Penalty Relief on Nearly 5 million 2020, 2021 Tax Returns; Restart of Collection Notices in 2024 Marks End of Pandemic-Related Pause

In a major step to help people who owe back taxes, the IRS is providing new penalty relief for approximately 4.7 million individuals, businesses and tax-exempt organizations that were not sent automated collection reminder notices during the pandemic.

Due to the unprecedented effects of the COVID-19 pandemic, the IRS temporarily suspended the mailing of automated reminders to pay overdue tax bills starting in February 2022. Although these reminder notices were suspended, the failure-to-pay penalty continues to accrue for taxpayers who did not fully pay their bills in response to the initial balance due notice.

Given this unusual situation, the IRS is taking several steps in advance of resuming normal collection notices for tax years 2020 and 2021 to help taxpayers with unpaid tax bills. The IRS has also released Notice 2024-07, which explains how the agency is providing failure-to-pay penalty relief to eligible taxpayers affected by the COVID-19 pandemic to help them meet their federal tax obligations.

Issue 19: Business Tax Account expands to S corporations, Partnerships.

As part of continuing transformation work, the IRS recently launched the second phase of a new online self-service tool for businesses that expands the business tax account capabilities and eligible entity types.

As a result, individual partners of partnerships and individual shareholders of S corporation businesses are now eligible for a business tax account in addition to sole proprietors. Available at IRS.gov/businessaccount, the new business tax account is a key part of the agency’s continuing service improvement initiative.

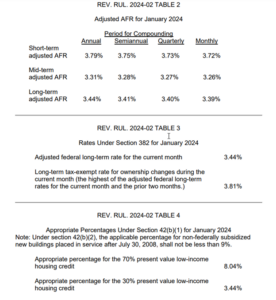

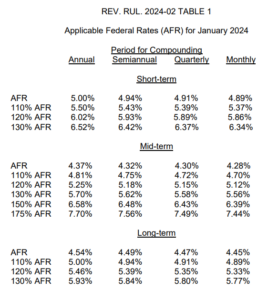

Issue 21: Applicable Federal Rates for February 2024, Rev. Rul. 2024-03

REV. RUL. 2024-03 TABLE 2