In this Issue:

- 60 Tax Provisions for Tax Year 2024 – Revenue Procedure 2023-34 – IR-2023-208, Nov. 9, 2023

- Employee Retention Credit

- IRS reminder: Still Time to Withdraw Pending ERC Claims

- Credit for Builders of New Energy-Efficient Homes

- IRS: 2024 Flexible Spending Arrangement Contribution Limit Rises by $150

- Preparers Receiving Due Diligence Reminders

- OPR Issues FBAR Due Diligence Alert

- IRS Delivers New Capabilities to Tax Pro Account; Latest Expansion Part of Effort to Improve Technology, Tools to Help Tax Professionals Serve Clients

- 401(k) Rules Proposed for LTPT Employees

- Related Party Transaction Rules Proposed

- Form 4506-A – Request a Copy of a Return That’s not Available on IRS.gov

- IRS to Pilot New Security Self-Mailer to Deliver IP PINs

- New IRS Leadership Structure Announced

- IRS Updates Frequently Asked Questions Related to Wrongful Incarceration of a United States Service Member

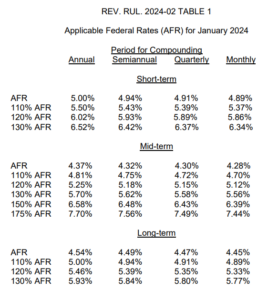

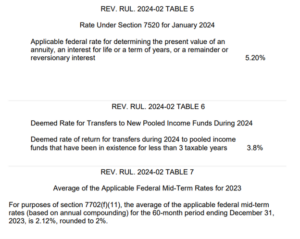

- Applicable Federal Rates for January 2024, Rev. Rul. 2024-02

2024 Webinar Schedule Coming Soon!

Issue 1: 60 Tax Provisions for Tax Year 2024 – Revenue Procedure 2023-34 – IR-2023-208, Nov. 9, 2023

Hazardous Substance Superfund Financing Rate

Starting in calendar year 2023, the Inflation Reduction Act reinstates the Hazardous Substance Superfund financing rate for crude oil received at U.S. refineries, and petroleum products that entered into the United States for consumption, use, or warehousing.

The tax rate is the sum of the Hazardous Substance Superfund rate and the Oil Spill Liability Trust Fund financing rate.

For calendar years beginning in 2024, the Hazardous Substance Superfund financing rate is adjusted for inflation. For calendar year 2024 crude oil or petroleum products entered after Dec. 31, 2016, will have a tax rate of $0.26 cents a barrel.

Highlights of changes in Revenue Procedure 2023-34:

The tax year 2024 adjustments described below generally apply to income tax returns filed in 2025. The tax items for tax year 2024 of greatest interest to most taxpayers include the following dollar amounts:

| Standard Deduction for 2024 |

| Filing Status | Tax Year 2024 | Tax Year 2023 | Tax Year 2022 |

| Married Filing Jointly | $29,200 | $27,700 | $25,900 |

| Single | $14,600 | $13,850 | $12,950 |

| Head of Household | $21,900 | $20,800 | $19,400 |

| Married Filing Separately | $14,600 | $13,850 | $12,950 |

| Tax Rates |

Marginal rates: For tax year 2024, the top tax rate remains 37% for individual single taxpayers with incomes greater than $609,350 ($731,200 for married couples filing jointly).

The other rates are:

35% for incomes over $243,725 ($487,450 for married couples filing jointly)

32% for incomes over $191,950 ($383,900 for married couples filing jointly)

24% for incomes over $100,525 ($201,050 for married couples filing jointly)

22% for incomes over $47,150 ($94,300 for married couples filing jointly)

12% for incomes over $11,600 ($23,200 for married couples filing jointly)

The lowest rate is 10% for incomes of single individuals with incomes of $11,600 or less ($23,200 for married couples filing jointly).

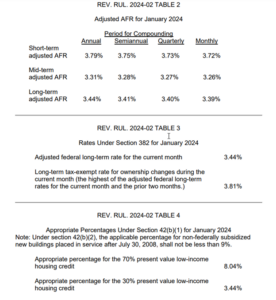

| Exemption Amounts for Alternative Minimum Tax 2024 | |

| Joint Returns or Surviving Spouses | $133,300 |

| Unmarried Individuals (other than Surviving Spouses) | $ 85,700 |

| Married Individuals Filing Separate Returns | $ 66,650 |

| Estates and Trusts | $ 29,900 |

For taxable years beginning in 2024, under § 55(b)(1), the excess taxable income above 11 which the 28 percent tax rate applies is:

| Married Individuals Filing Separate Returns | $116,300 |

| All Other Taxpayers | $232,600 |

For taxable years beginning in 2024, the amounts used under § 55(d)(2) to determine the phaseout of the exemption amounts are:

Kiddie Tax – Alternative Minimum Tax

Alternative Minimum Tax Exemption for a Child Subject to the “Kiddie Tax.” For taxable years beginning in 2024, for a child to whom the § 1(g) “kiddie tax” applies, the exemption amount under §§ 55(d) and 59(j) for purposes of the alternative minimum tax under § 55 may not exceed the sum of (1) the child’s earned income for the taxable year, plus (2) $9,250.

Dependent

For taxable years beginning in 2024, the standard deduction amount under § 63(c)(5) for an individual who may be claimed as a dependent by another taxpayer cannot exceed the greater of (1) $1,300, or (2) the sum of $450 and the individual’s earned income.

Aged or blind

For taxable years beginning in 2024, the additional standard deduction amount under § 63(f) for the aged or the blind is $1,550. The additional standard deduction amount is increased to $1,950 if the individual is also unmarried and not a surviving spouse.

Certain Expenses of Elementary and Secondary School Teachers

For taxable years beginning in 2024, under § 62(a)(2)(D) the amount of the deduction allowed under § 162 that consists of expenses paid or incurred by an eligible educator in connection with books, supplies (other than nonathletic supplies for courses of instruction in health or physical education), computer equipment (including related software and services) and other equipment, and supplementary materials used by the eligible educator in the classroom is $300.

Adoption Credit

For taxable years beginning in 2024, under § 23(a)(3) the credit allowed for an adoption of a child with special needs is $16,810. For taxable years beginning in 2024, under § 23(b)(1) the maximum credit allowed for other adoptions is the amount of qualified adoption expenses up to $16,810. The available adoption credit begins to phase out under § 23(b)(2)(A) for taxpayers with modified adjusted gross income in excess of $252,150 and is completely phased out for taxpayers with modified adjusted gross income of $292,150 or more. See section 3.19 of this revenue procedure for the adjusted items relating to adoption assistance programs.

Child Tax Credit

For taxable years beginning in 2024, the amount used in § 24(d)(1)(A) to determine the amount of credit under § 24 that may be refundable is $1,700.

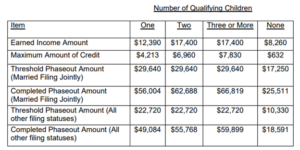

Earned Income Credit

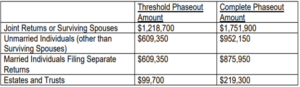

For taxable years beginning in 2024, the following amounts are used to determine the earned income credit under § 32(b). The “earned income amount” is the amount of earned income at or above which the maximum amount of the earned income credit is allowed.

The “threshold phaseout amount” is the amount of adjusted gross income (or, if greater, earned income) above which the maximum amount of the credit begins to phase out.

The “completed phaseout amount” is the amount of adjusted gross income (or, if greater, earned income) at or above which no credit is allowed.

The threshold phaseout amounts and the completed phaseout amounts shown in the table below for married taxpayers filing a joint return include the increase provided in § 32(b)(2)(B), as adjusted for inflation for taxable years beginning in 2024.

The threshold phaseout amounts and the completed phaseout amounts shown in the table below for taxpayers with all other filing statuses also apply to married taxpayers who are not filing a joint return and satisfy the special rules for separated spouses in § 32(d).

The instructions for the Form 1040 series provide tables showing the amount of the earned income credit for each type of taxpayer.

Excessive Investment Income

For taxable years beginning in 2024, the earned income tax credit is not allowed under § 32(i) if the aggregate amount of certain investment income exceeds $11,600.

Cafeteria Plans

For taxable years beginning in 2024, the dollar limitation under § 125(i) on voluntary employee salary reductions for contributions to health flexible spending arrangements is $3,200. If the cafeteria plan permits the carryover of unused 13 amounts, the maximum carryover amount is $640.

Qualified Transportation Fringe Benefit

For taxable years beginning in 2024, the monthly limitation under § 132(f)(2)(A) regarding the aggregate fringe benefit exclusion amount for transportation in a commuter highway vehicle and any transit pass is $315. The monthly limitation under § 132(f)(2)(B) regarding the fringe benefit exclusion amount for qualified parking is $315.

Adoption Assistance Programs

For taxable years beginning in 2024, under § 137(a)(2), the amount that can be excluded from an employee’s gross income for the adoption of a child with special needs is $16,810. For taxable years beginning in 2024, under § 137(b)(1) the maximum amount that can be excluded from an employee’s gross income for the amounts paid or expenses incurred by an employer for qualified adoption expenses furnished pursuant to an adoption assistance program for adoptions by the employee is $16,810. The amount excludable from an employee’s gross income begins to phase out under § 137(b)(2)(A) for taxpayers with modified adjusted gross income in excess of $252,150 and is completely phased out for taxpayers with modified adjusted gross income of $292,150 or more. (See section 3.04 of this revenue procedure for the adjusted 14 items relating to the adoption credit.)

Foreign Earned Income Exclusion

For tax year 2024, the foreign earned income exclusion is $126,500, increased from $120,000 for tax year 2023.

Estates Basic Exclusion

Estates of decedents who die during 2024 have a basic exclusion amount of $13,610,000, increased from $12,920,000 for estates of decedents who died in 2023.

Gifts

The annual exclusion for gifts increases to $18,000 for calendar year 2024, increased from $17,000 for calendar year 2023.

Items unaffected by indexing:

By statute, certain items that were indexed for inflation in the past are currently not adjusted.

- The personal exemption for tax year 2024 remains at 0, as it was for 2023. This elimination of the personal exemption was a provision in the Tax Cuts and Jobs Act.

- For 2024, as in 2023, 2022, 2021, 2020, 2019 and 2018, there is no limitation on itemized deductions, as that limitation was eliminated by the Tax Cuts and Jobs Act.

- The modified adjusted gross income amount used by taxpayers to determine the reduction in the Lifetime Learning Credit provided in § 25A(d)(2) is not adjusted for inflation for taxable years beginning after Dec. 31, 2020. The Lifetime Learning Credit is phased out for taxpayers with modified adjusted gross income in excess of $80,000 ($160,000 for joint returns).

2024 Standard Mileage Rate

The Internal Revenue Service issued the 2024 optional standard mileage rates used to calculate the deductible costs of operating an automobile for business, charitable, medical or moving purposes.

Beginning on Jan. 1, 2024, the standard mileage rates for the use of a car (also vans, pickups or panel trucks) will be:

- 67 cents per mile driven for business use, up 1.5 cents from 2023.

- 21 cents per mile driven for medical or moving purposes for qualified active-duty members of the Armed Forces, a decrease of 1 cent from 2023.

- 14 cents per mile driven in service of charitable organizations; the rate is set by statute and remains unchanged from 2023.

These rates apply to electric and hybrid-electric automobiles as well as gasoline and diesel-powered vehicles.

The standard mileage rate for business use is based on an annual study of the fixed and variable costs of operating an automobile. The rate for medical and moving purposes is based on the variable costs.

It is important to note that under the Tax Cuts and Jobs Act, taxpayers cannot claim a miscellaneous itemized deduction for unreimbursed employee travel expenses. Taxpayers also cannot claim a deduction for moving expenses, unless they are members of the Armed Forces on active duty moving under orders to a permanent change of station.

Taxpayers always have the option of calculating the actual costs of using their vehicle rather than using the standard mileage rates.

Taxpayers can use the standard mileage rate but generally must opt to use it in the first year the car is available for business use. Then, in later years, they can choose either the standard mileage rate or actual expenses.

Leased vehicles must use the standard mileage rate method for the entire lease period (including renewals) if the standard mileage rate is chosen.

Notice 2024-08 contains the optional 2024 standard mileage rates, as well as the maximum automobile cost used to calculate the allowance under a fixed and variable rate (FAVR) plan. In addition, the notice provides the maximum fair market value of employer-provided automobiles first made available to employees for personal use in calendar year 2024 for which employers may use the fleet-average valuation rule in or the vehicle cents-per-mile valuation rule.

Issue 2: Employee Retention Credit

As part of continuing efforts to combat dubious Employee Retention Credit (ERC) claims, the Internal Revenue Service is sending an initial round of more than 20,000 letters to taxpayers notifying them of disallowed ERC claims. IRS is disallowing claims to entities that did not exist or did not have paid employees during the period of eligibility to prevent improper ERC payments from being made to ineligible entities.

The letters are being sent as the IRS continues increased scrutiny of ERC claims in response to misleading marketing campaigns that have targeted small businesses and other organizations. The IRS mailing is the latest in an expanded compliance effort that includes a special withdrawal program for those with pending claims who realize they may have filed an inaccurate tax return.

Later this month, a separate voluntary disclosure program will be unveiled allowing those who received questionable payments to come in and avoid future IRS action.

After an initial review this fall, the IRS determined that a large block of taxpayers did not meet basic criteria for credit. Starting this week, taxpayers who are ineligible for credit will begin receiving copies of Letter 105 C, Claim Disallowed.

This group of letters will cover taxpayers ineligible for the ERC either because their entity did not exist or did not have employees for the time period when the credit was claimed.

Following concerns about aggressive ERC marketing from tax professionals and others, the IRS announced Sept. 14 a moratorium on processing new ERC claims through at least the end of 2023. The IRS noted that enhanced compliance reviews of existing claims submitted before the moratorium is critical to protect against fraud and also to protect businesses and organizations from facing penalties or interest payments stemming from bad claims pushed by promoters.

When properly claimed, the ERC is a refundable tax credit designed for businesses that continued paying employees during the COVID-19 pandemic while their business operations were either fully or partially suspended due to a government order or had a significant decline in gross receipts during the eligibility periods.

In July, the IRS said it was shifting its focus to review ERC claims for compliance concerns, including intensifying audit work and criminal investigations on promoters and businesses filing dubious claims. The IRS has hundreds of criminal cases being worked, and thousands of ERC claims have been referred for audit.

20,000 Letters Focus on Two ERC Problem Areas

The mailing reflects just part of the ongoing IRS review of these claims. In this group, two categories of claims have been identified and are being disallowed:

- Entity not in existence during period of eligibility: TheERC applies to qualified wages for periods between March 13, 2020, and Dec. 31, 2021. Entities established after Dec. 31, 2021, are not entitled to the ERC under the law passed by Congress.

- There are no paid employees during the period of eligibility: TheERC is intended as a credit against qualified wages paid. Entities that did not pay any wages are not eligible for ERC.

The IRS respects taxpayer rights, and the disallowance letter will explain that a taxpayer that disagrees with the disallowance can respond with documentation that supports their eligibility or claim amount, or they can file an administrative appeal.

The disallowance letters that identify ineligible claims before they’re paid serve several purposes that help taxpayers and tax administration. They:

- Help ineligible taxpayers avoid audits, repayment, penalties and interest,

- Protect taxpayers by preventing an incorrect refund from going to an ERCpromoter, and

- Save IRS resources by disallowing incorrect credits before they enter the audit process.

The IRS plans additional letters beyond the disallowance letters. Plans are also being finalized for a special voluntary disclosure program involving ERC claims that will be announced later this month.

The IRS is also continuing to review ERC claims and may request more information from taxpayers to support their ERC claim.

Issue 3: IRS reminder: Still Time to Withdraw Pending ERC Claims

The IRS is also continuing to accept and process requests to withdraw a taxpayer’s full ERC claim under the special withdrawal process. Taxpayers have until at least the end of the year to request a withdrawal.

This withdrawal option allows certain employers that filed an ERC claim but have not yet received a refund to withdraw their submission and avoid future repayment, interest, and penalties.

Employers that submitted an ERC claim that has not yet been paid can withdraw their claim and avoid the possibility of getting a refund for which they are ineligible. They can also withdraw their claim if they have received a check but have not yet deposited or cashed it.

The IRS created the withdrawal option to help small business owners and others who were pressured or misled by ERC marketers or promoters into filing ineligible claims. Claims that are withdrawn will be treated as if they were never filed. The IRS will not impose penalties or interest.

During this period, the IRS warns taxpayers to use extreme caution before applying for the ERC as aggressive maneuvers continue by marketers and scammers. In addition, the IRS continues to urge taxpayers who submitted claims to review the ERC requirements and talk to a trusted tax professional about their eligibility amid misleading marketing around the credit.

Issue 4: Credit for Builders of New Energy-Efficient Homes

Eligible contractors who build or substantially reconstruct qualified new energy-efficient homes may be able to claim tax credits up to $5,000 per home. The amount of the credit depends on factors including the type of home, its energy efficiency, and the date when the home is acquired.

Who is eligible?

Eligible contractors must meet all requirements under § 45L before they claim the credit. Find guidance interpreting section 45L in Notice 2008-35 (and Notice 2008-36 for manufactured homes).

Homes that qualify?

For homes acquired in 2023 through 2032: The credit amount is up to $5,000 based on the applicable program and program requirements under which the home was built. (Energy Star or Zero Energy Ready Home).

For homes acquired before 2023: The credit amount is $1,000 or $2,000, depending on the energy savings requirements.

Find details in About Form 8908, Energy Efficient Home Credit.

Issue 5: IRS: 2024 Flexible Spending Arrangement Contribution Limit Rises by $150

During open enrollment season for Flexible Spending Arrangements (FSAs), the Internal Revenue Service reminds taxpayers that they may be eligible to use tax-free dollars to pay medical expenses not covered by other health plans through their FSA.

For 2024, there is a $150 increase to the contribution limit for these accounts.

An employee who chooses to participate in an FSA can contribute up to $3,200 through payroll deductions during the 2024 plan year. Amounts contributed are not subject to federal income tax, Social Security tax or Medicare tax.

If the plan allows, the employer may also contribute to an employee’s FSA. If the employee’s spouse has a plan through their employer, the spouse can also contribute up to $3,200 to that plan. In this situation, the couple could jointly contribute up to $6,400 for their household.

For FSAs that permit the carryover of unused amounts, the maximum 2024 carryover amount to 2025 is $640. For unused amounts in 2023, the maximum amount that can be carried over to 2024 is $610.

Eligible employees of companies that offer a health flexible spending arrangement (FSA) need to act before their medical plan year begins to take advantage of an FSA during 2024. Self-employed individuals are not eligible.

Expenses to Consider

Throughout the year, taxpayers can use FSA funds for qualified medical expenses not covered by their health plan. These can include co-pays, deductibles and a variety of medical products. Also covered are services ranging from dental and vision care to eyeglasses and hearing aids. Interested employees should check with their employer for details on eligible expenses and claim procedures.

Before enrollment (if an employer offers an FSA), review any expected health care expenses projected for the year. Participating employees should plan for healthcare activities when they calculate their contribution amounts. Consider:

- Updating medicine cabinet with necessary supplies.

- Big ticket expenses.

- Seasonal needs such as allergy products, sunscreen or warm steam vaporizers.

- Routine checkups or visits with specialists that regular insurance plans do not cover.

- Many over-the-counter items are FSA eligible.

- Eye exams or dental visits: Out-of-pocket costs for dental and vision care are also covered by an FSA.

Employers are not required to offer FSAs. Interested taxpayers should check with their employer to see if they offer an FSA.

Issue 6: Preparers Receiving Due Diligence Reminders

The IRS is sending out educational letters and making phone calls to paid preparers to remind them of their due diligence requirements for tax returns claiming refunds for:

- Earned income tax credit.

- Child tax credit, additional child tax credit or credit for other dependents.

- American opportunity tax credit.

- Head of household filing status.

Letters will be sent to paid preparers who fail to include Form 8867, Paid Preparer’s Due Diligence Checklist, with submitted returns that have a high likelihood of errors claiming the above-listed benefits. The IRS also sends letters to the preparer’s clients to let them know their returns may contain errors regarding the benefits. The agency makes telephone calls to preparers who received a letter and appear to be continuing to file returns with errors. The IRS will discuss the due diligence rules and the consequences of not following them.

Issue 7: OPR Issues FBAR Due Diligence Alert

The IRS Office of Professional Responsibility (OPR) issued an alert to remind Circular 230 tax professionals of their responsibilities regarding the filing of Reports of Foreign Bank and Financial Accounts (FBARs).

Preparers subject to Circular 230 who prepare income or information returns have a duty of due diligence, including collecting the information necessary to correctly respond to questions related to foreign accounts on client tax returns.

If a practitioner learns of unreported foreign accounts, they have an obligation to advise the client about the need to file an FBAR and the possible penalties for failing to do so. However, they are not obligated to prepare an FBAR on behalf of the client unless the client has agreed to the service and the practitioner believes they are competent to do so.

Issue 8: IRS Delivers New Capabilities to Tax Pro Account; Latest Expansion Part of Effort to Improve Technology, Tools to Help Tax Professionals Serve Clients

As part of a larger effort to improve technology, the Internal Revenue Service announced today an expansion of the Tax Pro Account capabilities that allows tax professionals access to new services to help their clients.

New additions to Tax Pro Account, available through IRS.gov, will help practitioners manage their active client authorizations on file with the Centralized Authorization File (CAF) database.

Other enhancements will allow tax professionals to view their client’s tax information, including balance due amounts. Tax Pro Account users can now also withdraw from their active authorizations online in real time.

These changes reflect ongoing transformation efforts made possible under the Inflation Reduction Act. Tax professionals are a critical part of the nation’s tax system, and the new IRS Strategic Operating Plan highlights the need to improve technology and services for taxpayers as well as tax professionals.

The new enhancements continue IRS efforts to improve the third-party authorization process. The IRS also continues to work on additional expansions to improve services to taxpayers and their tax professionals.

With the recent enhancements, tax professionals can now use Tax Pro Account to send Power of Attorney (POA) and Tax Information Authorization (TIA) requests directly to a taxpayer’s individual IRS Online Account.

Upon the taxpayer’s approval and validation of the information, the authorization records immediately to the CAF database, which avoids faxing, mailing, uploading and long review and processing time by the CAF Unit.

Tax professionals must have a CAF number to use a Tax Pro Account; a CAF number cannot be requested through the Tax Pro Account. Currently, the digital authorization process is available only for individual taxpayers, not businesses or other entities.

More than 260,000 people have used Tax Pro Account since it launched in July 2021. The webpage has been viewed over 2.7 million times.

Issue 9: 401(k) Rules Proposed for LTPT Employees

The IRS and U.S. Treasury Department have issued proposed regulations that provide guidance on recent statutory changes to 401(k) plans with respect to long-term, part-time (LTPT) employees. Proposed regulation REG-104194-23 reflects changes made to §401(k) under the SECURE Act and SECURE. 2.0 Act, including the provisions that shorten the time LTPT employees must work before an employer must allow them to participate in a sponsored plan. The new rules would be incorporated into Treasury Regulation §1.401(k)-5 for plan years beginning on or after Jan. 1, 2024.

Issue 10: Related Party Transaction Rules Proposed

The IRS and Treasury Department have proposed regulations for related-person partnership transactions that result in a gain or loss on the sale or exchange of property or in a difference in the timing of income and deduction recognition due to different methods of accounting. Proposed regulation REG-131756-11 would address statutory changes to §§267 and 707(b) that have been enacted since 1982 and indicate that Congress intended for a partnership to be viewed as an entity and not an aggregate of partners for the purposes of the rules in those sections. As a result, the rules will be applied at the partnership level and not at the partner level.

Issue 11: Form 4506-A – Request a Copy of a Return That’s not Available on IRS.gov

Complete Form 4506-A, Request for Copy of Exempt or Political Organization IRS Form, to request copies of Form 990, 990-EZ, 990-PF, 990-T (for IRC Section 501(c)(3) organizations), or 5227. Form 4506-A can be submitted by mail or fax; email submissions are not accepted.

Form 4506-B – Request a Copy of an Organization’s Exemption Application for determination Letter from the IRS

Use TEOS to view determination letters issued in 2014 or later online.

To request a copy of a determination letter issued before 2014, submit Form 4506-B, Request for a Copy of Exempt Organization IRS Application or Letter, using the email feature on the form. No faxed or mailed submissions will be accepted.

You may use Form 4506-B to request a copy of an organization’s application for recognition of tax-exempt status (Forms 1023, 1023-EZ, 1024, 1024-A, etc.) or an affirmation letter affirming the current exempt status of the organization.

Submitting Form 4506-B

The IRS will only process a request for copies submitted on the current Form 4506-B (updated August 2023). Requests must include a complete Form 4506-B and the correct Employer Identification Number (EIN) and must be used for an exempt organization.

If a request is not accepted, you will receive a letter explaining why and describing the correct method for resubmitting a request, where applicable.

Issue 12: IRS to Pilot New Security Self-Mailer to Deliver IP PINs

Taxpayers who typically receive a CP01A, We Assigned You an Identity Protection Personal Identification Number (IP PIN), may notice a change in the look of their mailed IP PINs in 2024.

In addition to the traditional delivery of IP PINs in an envelope, the IRS is piloting the use of a security self-mailer for delivery of the IP PINs. Security self-mailers have perforated borders that recipients remove to open the correspondence. You may have received a security self-mailer in the form of your bank PIN or other private correspondence.

Approximately 70% of taxpayers who receive the IP PIN will receive them in the new format. With identify theft on the rise, the IRS is working to make correspondence safer and more secure, ensuring the protection of taxpayer data remains a top priority. Some of these notices will include a survey to help determine the effectiveness of the pilot. If pilot feedback is positive, future use will expand to all CP01As. The way taxpayers use the IP PIN to file their taxes will not change.

Issue 13: New IRS Leadership Structure Announced

IRS Commissioner Danny Werfel announced plans for a new leadership structure at the agency, a step designed to reflect new transformation goals and update the top of the organization for the first time in two decades. The new organizational structure will feature a single IRS deputy commissioner and four new IRS chief positions to oversee taxpayer service, tax compliance, information technology and operations. The changes will streamline operational efficiencies and align with major transformation work underway at the agency through the Inflation Reduction Act funding.

Issue 14: IRS Updates Frequently Asked Questions Related to Wrongful Incarceration of a United States Service Member

The Internal Revenue Service issued frequently asked questions (FAQs) on Fact Sheet 2023-26 updating question 9 to reflect that wrongfully incarcerated United States service members cannot exclude certain payments from gross income.

Updated FAQ 9 now provides that a United States military service member who is a wrongfully incarcerated individual and who receives back pay following the reversal of a court martial conviction may not exclude the payments under the Wrongful Incarceration Exclusion if the payments are merely the restoration of pay and allowances to which the service member is entitled under the law.

Issue 15: Applicable Federal Rates for January 2024, Rev. Rul. 2024-02