In this Issue:

- Taxpayers Face Deadline to Claim Tax Year 2019 Refunds

- Authorized IRS e-file Providers/EROs information Concerning Fingerprints

- Helpful Information for the Military Personnel Client – Reminder for Us

- Bipartisan Bill Would Move Estimated Tax Deadlines to Quarterly Basis – NOT LAW YET – Heads Up

- Chief Counsel Advice Discusses FICA Refunds

- Form I-9 Remote Flexibility Ends July 31

- House Republicans Introduce Broad Package of Tax Breaks – What is Under Consideration in Congress – Not Law but We will be Monitoring

- Updated Version of Offer in Compromise Form Released

- Improper IRS Payment Rates Still Too High – TIGTA Report 2023-40-032

- IRS Releases Report on Direct E-File Tool, Announces Pilot Program

- AICPA Endorses Legislation to Simplify Tax Filing Extension Process

- IRS Grants Penalty Relief for Corporations That Did Not Pay Estimated Tax Related to the New Corporate Alternative Minimum Tax – IR-2023-110, June 7, 2023

- Credit for Builders of Energy-Efficient Homes

Issue 1: Taxpayers Face Deadline to Claim Tax Year 2019 Refunds

An additional reminder that the deadline is approaching!!!!

Nearly 1.5 million people across the nation have unclaimed refunds for tax year 2019 but face a July 17, 2023, deadline to submit their tax return. Under the law, taxpayers usually have three years to file and claim their tax refunds. If they do not file within three years, the money becomes the property of the U.S. Treasury.

Click on the above link to see a breakdown of the states and the numbers of unfiled returns.

Issue 2: Authorized IRS e-file Providers/EROs information Concerning Fingerprints

The FBI may have updated its description of how it is using your fingerprints and associated information since you last accessed your Authorized IRS e-file Provider application. You can review the updated Privacy Act Statement by accessing your e-file application or going to the FBI Privacy Act Statement.

By participating in the Authorized IRS e-file Provider program, you consent to the uses described in the updated Privacy Act Statement. These uses include the retention of your fingerprints for continued comparison against other fingerprints retained by the FBI for purposes of identifying criminal activity, which the FBI may then report to the IRS to administer the IRS e-file program. This comparison and reporting process for the IRS continues as long as you remain in the e-file program.

Issue 3: Helpful Information for the Military Personnel Client – Reminder for Us

IRS Publication 3, Armed Forces’ Tax Guide, is a free booklet filled with valuable information and tips designed to help service members and their families take advantage of all the tax benefits allowed by law. Several of these key benefits include:

- Combat pay is partially or fully tax-free. Service members serving in support of a combat zone or in a qualified hazardous duty area may also qualify for this exclusion. In addition, U.S. citizens or resident aliens, such as spouses, who worked as contractors or employees of contractors supporting the U.S. armed forces in designated combat zones, may qualify for the foreign earned income exclusion.

- Members of the military, such as those who serve in a combat zone or are serving in contingency operations outside the United States, can postpone most tax deadlines. Those who qualify can get automatic extensions of time to file and pay their taxes.

- The Earned Income Tax Credit is worth up to $6,935 for tax year 2022. Low- and moderate- income service members who receive nontaxable combat pay can use a special computation method that may boost the EITC, meaning they may owe less tax or get a larger refund.

- Dependent care assistance programs for military personnel are excludable benefits and not included in the military member’s income.

- Members of the armed forces on active duty may be eligible to deduct unreimbursed moving expenses if their move was due to a military order and permanent change of station. Also, allowances paid to move members of the U.S. armed forces for a permanent change of station are not taxable.

Both spouses normally must sign a joint income tax return, but if one spouse is absent due to certain military duties or conditions, the other spouse may be able to sign for him or her.

Issue 4: Bipartisan Bill Would Move Estimated Tax Deadlines to Quarterly Basis – NOT LAW YET – Heads Up

Proposed legislation to set estimated tax due dates to even, quarterly intervals has resurfaced in the House and enjoys support from tax and accounting professional organizations.

The Tax Deadline Simplification Act was introduced May 25 in the House by representatives Debbie Lesko, Republican of Arizona, and Brad Schneider, Democrat of Illinois. It would establish that estimated tax installments for individuals, businesses, estates, and trusts are due 15 days after the end of each quarter, meaning the deadlines would be the 15th day of the months of January, April, July, and October.

If passed and signed into law, ultimate confusion may prevail until our clients get used to the new payments schedule. We will be watching to see if the proposal becomes law.

Issue 5: Chief Counsel Advice Discusses FICA Refunds

A U.S. employer that pays FICA taxes under a tax equalization program for an employee cannot claim a refund of excess FICA withholding without first repaying or reimbursing the employee’s share of the overpaid FICA tax or obtaining the employee’s permission to claim the refund. (Chief Counsel Advice 202323005)

Generally, to receive a refund for an overpayment of FICA tax, an employer must repay or reimburse the employee for their share of the overpaid FICA tax or obtain the employee’s permission to file the refund claim. If the employer obtains the employee’s permission, the consent must be included with the refund claim when it is filed.

https://www.irs.gov/pub/irs-wd/202323005.pdf

Issue 6: Form I-9 Remote Flexibility Ends July 31

The U.S. Department of Homeland Security (DHS) and U.S. Immigration and Customs Enforcement (ICE) are reminding employers that the flexibilities implemented in response to the COVID-19 pandemic that permitted employers to review the supporting documentation for Form I-9 purposes remotely will end on July 31, 2023.

Form I-9 is used to verify the identity and employment authorization of individuals hired for employment in the United States. All U.S. employers must properly complete Form I-9 for each individual they hire for employment in the United States. This includes citizens and noncitizens.

Pre-COVID-19 considerations, employers were required to physically examine the supporting documentation presented by new employees from the Lists of Acceptable Documents, or an acceptable receipt, to ensure that the presented documentation appears to be genuine and to relate to the individual who presents them. Employers must then complete Section 2, “Employer Review and Verification,” of the Form within three business days after the first day of employment.

However, during the pandemic, DHS and ICE instituted some flexibility and allowed documents to be reviewed remotely. While employers were not required to review the employee’s identity and employment authorization documents in the employee’s physical presence, the employers were required to inspect the supporting documents remotely (via such methods as video link, fax or email), etc.) Employers were allowed to enter “COVID-19” as the reason for the physical inspection delay in the Section 2 Additional Information field. Employers were then instructed to review the physical documents by a specified date.

With the winding down of the COVID-19 pandemic, DHS and ICE concur that flexibility is no longer needed, and that physical review of the documents should resume. Additionally, employers are required to perform an in-person, physical examinations of the documentation provided for individuals hired on or after March 20, 2020 who only received a virtual or remote examination of their Form I-9 documentation by August 30, 2023.

Issue 7: House Republicans Introduce Broad Package of Tax Breaks – What is Under Consideration in Congress?

House Ways and Means Republicans have introduced a package of mostly small business tax bills which include a subsequent extension of expired business tax provisions, a bonus standard deduction, and cuts to green energy provisions.

The three related tax bills introduced on June 9 are largely viewed as a starting point for negotiations on a tax bill both Democrats and Republicans expect to come up at the end of the year.

The package would extend and retroactively restore three expired business tax provisions from the Tax Cuts and Jobs Act (TCJA) (PL 115-97).

- Create a two-year individual bonus standard deduction.

- Increase the reporting threshold for forms 1099 and 1099-K and

- Repeal of some clean energy credits created by the Inflation Reduction Act (PL 117-169).

The first measure (HR 3938) of the American Families and Jobs Act, as the package is called, temporarily revives tax breaks including research spending, interest expenses, and equipment purchases. All three provisions expired last year as part of a planned phase out of tax cuts in the TCJA; a process that accelerates in 2025.

The second (HR 3936) would allow taxpayers earning less than $400,000 annually to claim a larger standard deduction for the next two years. Married couples who do not itemize would see their deductions rise by $4,000, while single filers would benefit from an extra $2,000.

The third bill would return the Form 1099-K (HR 3937) reporting threshold to $20,000.

Basically, all three bills are starting points for future discussion as we approach year end possible tax changes.

Join us in July for a great webinar lineup:

- Short-Term Rentals

- Trust & Estates Part 2

- The Correspondence Audit

- Like-Kind Exchange

- Principal Residence Taxation Issues

https://www.cpehours.com/webinar-schedule/

Issue 8: Updated Version of Offer in Compromise Form Released

The IRS has released an April 2023 version of Form 656, Offer in Compromise booklet. Form 656 contains everything a taxpayer needs to know about submitting an offer to the IRS. Taxpayers should download and use the April 2023 version of the OIC booklet to avoid processing delays. (IRS Tax Tip 2023-58, 4/27/2023)

An offer in compromise is an agreement between a taxpayer and the IRS to settle the taxpayer’s tax debt for less than the full amount owed. The goal of an offer is a compromise that’s in the best interest of both the taxpayer and the IRS.

Taxpayers should make an offer to the IRS when they cannot pay their full tax liability due to income loss (unemployment) or large expenses (medical bills) or if paying would cause them financial hardship.

Generally, an individual taxpayer is eligible to make an Offer in Compromise when the taxpayer:

- has filed all required tax returns and made all required estimated payments,

- does not have an open bankruptcy case, and

- has a valid extension for a current year return (if applying for the current year)

An employer must also make required tax deposits for the current and past two quarters before making an offer.

Taxpayers can confirm their eligibility and prepare a preliminary offer using the IRS’ Offer in Compromise Pre-Qualifier Tool. Note. The tool is only a guide. The IRS will make the final decision on whether to accept the taxpayer’s offer.

The application fee for an offer in compromise is $205. But low-income taxpayers do not have to pay this fee.

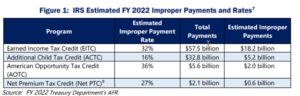

Issue 9: Improper IRS Payment Rates Still Too High – TIGTA Report 2023-40-032

This audit was initiated because TIGTA is required to annually assess and report on the IRS’s compliance with the reporting requirements contained in the Payment Integrity Information Act of 2019. The objective of this review was to determine whether the IRS complied with the annual improper payment reporting requirements for Fiscal Year (FY) 2022.

Impact on Tax Administration

The Office of Management and Budget (OMB) defines an improper payment as any payment that should not have been made, was made in an incorrect amount, or was made to an ineligible recipient.

The IRS currently has identified four programs that meet the OMB’s definition of a high-priority program susceptible to improper payments. The OMB defines high-priority programs as programs with improper payments resulting in monetary losses that exceed $100 million annually.

The IRS estimated the following improper payment rates:

- American Opportunity Tax Credit (AOTC): 36 percent.

- Earned Income Tax Credit (EITC): 32 percent.

- Net Premium Tax Credit: 27 percent.

- Additional Child Tax Credit (ACTC): 16 percent.

This is the first year the IRS has estimated an improper payment rate for the Net Premium Tax Credit.

For FY 2022, the IRS was largely compliant with the reporting requirements contained in the Payment Integrity Information Act of 2019. However, the IRS still has not satisfied the Payment Integrity Act goal to reduce improper payment rates to less than 10 %.

The IRS uses its National Research Program to measure reporting compliance for different types of taxes, including calculating estimated improper payment rates. For FY 2022, the IRS reduced the National Research Program sample size due to limited resources. The smaller sample size resulted in a wider confidence interval and a less precise estimated improper payment rate. Furthermore, to estimate the amount of improper payments, the IRS applied the estimated improper payment rate to returns on a tax year basis rather than a fiscal year basis as it has done in the past, which is more consistent with the filing and processing of tax returns.

Estimates of improper payment rates have risen since Fiscal Year 2020. However, refundable credit improper payments are not primarily the result of internal control weaknesses that the IRS can address. Eligibility rules differ for each credit and are often complex because they address complicated family relationships and residency arrangements to determine eligibility.

IRS management also advised TIGTA recently that there is a growing expectation for the IRS to notify individuals who are potentially eligible for but are not claiming refundable credits to encourage them to file a tax return and claim the credits. The same limitations that prevent the IRS from verifying refundable credit claims may also limit its ability to proactively identify eligible individuals who are not claiming these credits. This type of outreach could result in additional improper payments and increased taxpayer burden.

Issue 10: IRS Releases Report on Direct E-File Tool, Announces Pilot Program

Fulfilling its statutorily required report on the popularity, cost, and feasibility of developing an in-house free electronic filing system as mandated by the Inflation Reduction Act (PL 117-169), the IRS and an independent third party determined that there is enough potential benefit to taxpayers and support to move forward with a test pilot.

The highly anticipated 100-page report on a possible IRS-run Direct e-File Tax Return System (Direct File) was released May 16, nine months after the enactment of the Inflation Reduction Act.

Currently, the IRS partners with some outside tax software providers via its Public-Private Partnership (PPP) with the Free File Alliance per certain terms set forth in the Memorandum of Understanding, a renewable agreement between the agency and commercial participants to allow eligible taxpayers under a certain income threshold to electronically file their taxes for free in a collaboration between the IRS and the tax preparation industry.

However, the new report shows that a majority of testers are interested in using an IRS-provided tool to prepare and file their taxes.

The IRS will launch a pilot program next tax filing season in 2024 “to gather data to further assess issues identified in the report before deciding whether to deploy a full-scale direct file solution,” said Werfel.

Issue 11: AICPA Endorses Legislation to Simplify Tax Filing Extension Process

The American Institute of CPAs (AICPA) has endorsed bipartisan legislation introduced by Representatives Judy Chu (D-CA) and Mike Carey (R-OH) to simplify the tax filing extension process.

The Simplify Automatic Filing Extensions (SAFE) Act of 2023 would assist the Internal Revenue Service (IRS) with receiving extensions earlier in the year, providing taxpayers, CPAs and the IRS with a streamlined process and reducing the need for many penalty abatement requests.

The IRS frequently faces challenges in administering the tax filing season, which includes the:

(1) late enactment of tax legislation;

(2) delays in the release of tax forms that are needed before tax returns can be finished;

(3) anticipating and planning for resolution of expired provisions;

(4) software interruptions; and

(5) staffing issues.

In addition, taxpayers and their preparers must often obtain records from third parties to properly determine their tax liability. It is often impossible to collect the information needed for a complete and accurate return by the original due date.

To cope with these obstacles, taxpayers and tax professionals often request extensions of time to file tax returns. These extensions allow taxpayers an additional six months – from April 15 to October 15 – to prepare their tax return.

Penalties may apply if certain amounts are not paid with the extension request and first quarter estimated payment by April 15. As a result of the missing information, tax professionals and individual taxpayers filing for extensions perform time-consuming calculations and estimates of tax owed for the current year. This typically means putting hours of work into this initial estimation and then a second calculation, preparation, and review process later when the final tax return is ultimately filed.

As indicated by IRS statistics, the number of extensions filed each year is increasing and is predicted to continue to do so going forward. “For decades, the AICPA has advocated for and promoted the principles of good tax policy before members of Congress, Treasury and the IRS – the SAFE Act is a reflection of good tax policy for taxpayers and practitioners,” said AICPA Vice President of Taxation, Edward Karl, CPA, CGMA. “Complicated tax returns are often time-consuming for taxpayers and their advisors; simplification of these processes relieves stress on the taxpayer and supports tax compliance.

We appreciate the leadership of Representatives Chu and Carey to simplify automatic filings of extensions and we strongly support this legislation.”

Issue 12: IRS Grants Penalty Relief for Corporations That Did Not Pay Estimated Tax Related to the New Corporate Alternative Minimum Tax – IR-2023-110, June 7, 2023

The Department of Treasury and the Internal Revenue Service today issued Notice 2023-42 which will grant penalty relief for corporations that did not pay estimated tax in connection with the new corporate alternative minimum tax (CAMT).

The Inflation Reduction Act created the CAMT, which imposes a 15% minimum tax on the adjusted financial statement income of large corporations for taxable years beginning after Dec. 31, 2022. CAMT generally applies to large corporations with an average annual adjusted financial statement income exceeding $1 billion.

Considering the challenges associated with determining the amount of a corporation’s CAMT liability and whether a corporation is an applicable corporation subject to the CAMT, the IRS will waive the penalty for a corporation’s failure to pay estimated income tax with respect to its CAMT for a taxable year that begins after Dec. 31, 2022, and before Jan. 1, 2024.

Issue 13: Credit for Builders of Energy-Efficient Homes

Contractors who build or substantially reconstruct qualified energy-efficient homes may be eligible for tax credits up to $5,000 per home. The amount of the credit depends on factors including the type of home, its energy efficiency rating, and the date when someone buys or rents it.

Eligible Builders

To qualify, a builder must:

- Construct or substantially reconstruct a qualified energy-efficient home.

- Own the home and have a basis in it during construction.

- Sell or rent it to an individual for use as a residence.

Eligible Homes

To qualify, a home must be:

- A single-family or multifamily home (includes a manufactured home)

- Located in the United States.

- Purchased or rented by someone to use as a residence.

- Certified to meet applicable energy requirements based on home type and sale date.

Credit Amount for 2023 and After

For 2023 through 2033, the credit amounts are as follows.

$5,000 per home for new single-family and manufactured homes that are:

- Eligible for the ENERGY STAR program.

- Certified by the Zero Energy Ready Home Program.

$1,000 per unit for new multifamily homes that are:

- Part of an ENERGY STAR-eligible building

- Certified by the Zero Energy Ready Home Program

A $5,000 per unit credit may be available to builders who construct qualified multifamily homes if they also meet prevailing wage requirements.

Base Credit Amount

$2,500 for new homes meeting Energy Star standards; $5,000 for certified zero-energy ready homes. For multifamily, base amounts are $500 per unit for Energy Star and $1000 per unit for zero-energy ready.

Bonus Credit Amount

For multifamily homes, 5 times the base amount if prevailing wage requirements are met.

Credit Amount for 2022 and Before

For 2022 and before, the Inflation Reduction Act extended the previously expired credit to equal $2,000 for each home that:

- Uses at least 50% less energy than a comparable home.

- Gets at least 1/5 of its energy savings from building envelope improvements.

Manufactured homes that meet these standards plus the Federal Manufactured Home Construction and Safety Standards (FMHCSS) may qualify for the full $2,000 credit.

Manufactured homes that don’t meet the standards for the full credit may still qualify for a $1,000 credit under a different 30% standard.

Claim the Credit

Before claiming the credit, builders must certify that their homes meet all requirements under IRC Section 45L.

Then they can claim the credit on the appropriate form:

- Eligible contractors use Form 8908, Energy Efficient Home Credit

- Exception: If your only source to claim the credit is from a partnership or S corporation, use Form 3800, General Business Credit.

Issue 14: Federal Levy

I just received a federal tax levy for an employee. I’m not sure how to calculate the applicable amount for the levy and how much of the employee’s wages is exempt from the levy. The employee did complete Form 668-W and indicated married filing joint with four dependents. They are paid bi-weekly. How do I calculate the amount I need to send to the IRS?

Answer: Let’s first calculate the amount the IRS considers exempt from a federal tax levy. This information can be found in IRS Publication 1494. https://www.irs.gov/pub/irs-pdf/p1494.pdf

Looking at the table, first locate the area that matches the employee’s status. In this case “Married Filing Joint Return.” Under the Pay Period column, locate “bi-weekly” and the corresponding number of dependents, in this case, four. The box that intersects contains the amount that is exempt from the levy.

Now determine the employee’s take home pay. Take home pay is gross wages minus:

- Federal, state, and local taxes.

- Deductions that were in effect before the levy was received, including voluntary (401(k) contribution) and involuntary deductions (such as child support). This may also include union dues.

If the employee’s take home pay is greater than the exempt amount, subtract the take home pay from the exempt amount and remit the difference to the IRS. The exempt amount is paid to the employee.

If the employee’s take home pay is less than the exempt amount, nothing is remitted to the IRS. In this case, the entire take home pay would be paid to the employee because the entire payment is exempt from the levy.

Join us in July for a great webinar lineup:

- Short-Term Rentals

- Trust & Estates Part 2

- The Correspondence Audit

- Like-Kind Exchange

- Principal Residence Taxation Issues

Special Series – 1040 Basics

This 6-hour mini-series outlines the basics of tax preparation with a step-by-step analysis of Form 1040, U.S. Individual Income Tax Return, and its accompanying schedules.

https://www.cpehours.com/webinar-schedule/