Tax Newsletter: American Rescue Plan – Tax Credits Available to Provide Paid Leave to Employees Receiving the COVID-19 Vaccine

- Also:

- Treasury and IRS Provide Guidance on Tax Relief for Deductions for Food or Beverages from Restaurants

- Investing in the IRS and Improving Tax Compliance – American Family Plan Proposal

- IRS Releases Updated Practice Unit on Reasonable Cause Penalty Defense

- Bills from the Hill

- Temporary Deviation from Handwritten Signature Requirement for Limited List of Tax Forms

- Frequently Asked Questions About COBRA Assistance Under the American Rescue Plan Act

- Advance Child Tax Credit – What We Know Thus Far

- The 2021 Bentley Added to the List of Plug-In Electric Vehicles

- Dyed Diesel Fuel Penalty Relief Due to Disruptions of the Fuel Supply Chain

- IRS Issues Guidance on Taxability of Dependent Care Assistance Programs for 2021 and 2022

- IRS Processing Update

- Correction to the Form 1040 Line in Reference to Form 4797 Instructions

- Applicable Federal Rates for June 2021, Rev. Rul. 2021-09

Issue 1: American Rescue Plan – Tax Credits Available to Provide Paid Leave to Employees Receiving the COVID-19 Vaccine

The American Rescue Plan Act of 2021 (ARP) allows small and midsize employers, and certain governmental employers, to claim refundable tax credits that reimburse them for the cost of providing paid sick and family leave to their employees due to COVID-19, including leave taken by employees to receive or recover from COVID-19 vaccinations.

The ARP tax credits are available to eligible employers that pay sick and family leave for leave from April 1, 2021, through September 30, 2021.

Here are some basic facts about the employers eligible for the tax credits and how these employers may claim the credit for leave paid to employees who take leave to receive or recover from COVID-19 vaccinations.

Eligible Employers

An eligible employer is any business, including a tax-exempt organization, with fewer than 500 employees. An eligible employer also includes a governmental employer, other than the federal government and any agency or instrumentality of the federal government that is not an organization described in §501(c)(1).

Self-employed individuals are eligible for similar tax credits.

Paid Sick and Family Leave for Which Tax Credits Can be Claimed

Eligible employers are entitled to tax credits for wages paid for leave taken by employees who are not able to work or telework due to reasons related to COVID-19, including leave taken to receive COVID–19 vaccinations or to recover from any injury, disability, illness or condition related to the vaccinations. These tax credits are available for wages paid for leave from April 1, 2021, through September 30, 2021.

The Amount of the Tax Credits and How They Are Calculated

The paid leave credits under the ARP are tax credits against the employer’s share of the Medicare tax.

The tax credits are refundable, which means that the employer is entitled to payment of the full amount of the credits if it exceeds the employer’s share of the Medicare tax.

The tax credit for paid sick leave wages is equal to the sick leave wages paid for COVID-19 related reasons for up to two weeks (80 hours), limited to $511 per day and $5,110 in the aggregate, at 100% of the employee’s regular rate of pay.

The tax credit for paid family leave wages is equal to the family leave wages paid for up to twelve weeks, limited to $200 per day and $12,000 in the aggregate, at 2/3rds of the employee’s regular rate of pay.

The amount of these tax credits is increased by allocable health plan expenses and contributions for certain collectively bargained benefits, as well as the employer’s share of social security and Medicare taxes paid on the wages (up to the respective daily and total caps).

Claiming the Credit

Eligible employers may claim tax credits for sick and family leave paid to employees, including leave taken to receive or recover from COVID-19 vaccinations, for leave from April 1, 2021, through September 30, 2021.

Eligible employers report their total paid sick and family leave wages (plus the eligible health plan expenses and collectively bargained contributions and the eligible employer’s share of social security and Medicare taxes on the paid leave wages) for each quarter on their federal employment tax return, usually Form 941, Employer’s Quarterly Federal Tax Return.

Form 941 is used by most employers to report income tax and social security and Medicare taxes withheld from employee wages, as well as the employer’s own share of social security and Medicare taxes.

In anticipation of claiming the credits on the Form 941, eligible employers can keep the federal employment taxes that they otherwise would have deposited, including federal income tax withheld from employees, the employees’ share of social security and Medicare taxes and the eligible employer’s share of social security and Medicare taxes with respect to all employees up to the amount of credit for which they are eligible.

Note: You must include the full amount (both the nonrefundable and refundable portions) of the credit for qualified sick and family leave wages in gross income for the tax year that includes the last day of any calendar quarter in which a credit is allowed. You cannot use the same wages for the employee retention credit and the credits for paid sick and family leave.

If an eligible employer does not have enough federal employment taxes set aside for deposit to cover amounts provided as paid sick and family leave wages (plus the eligible health plan expenses and collectively bargained contributions and the eligible employer’s share of social security and Medicare taxes on the paid leave wages), the eligible employer may request an advance of the credits by filing Form 7200, Advance Payment of Employer Credits Due to COVID-19. The eligible employer will account for the amounts received as an advance when it files its Form 941, Employer’s Quarterly Federal Tax Return, for the relevant quarter.

Self-employed individuals may claim comparable tax credits on their individual Form 1040, U.S. Individual Income Tax Return.

Issue 2: Treasury and IRS Provide Guidance on Tax Relief for Deductions for Food or Beverages from Restaurants

Businesses can temporarily deduct 100% beginning January 1, 2021.

Notice 2021-25 provides guidance under the Taxpayer Certainty and Disaster Relief Act of 2020.

The Act added a temporary exception to the 50% limit on the amount that businesses may deduct for food or beverages. The temporary exception allows a 100% deduction for food or beverages from restaurants.

Beginning January 1, 2021, through December 31, 2022, businesses can claim 100% of their food or beverage expenses paid to restaurants as long as the business owner (or an employee of the business) is present when food or beverages are provided, and the expense is not lavish or extravagant under the circumstances.

Where Can Businesses Get Food and Beverages and Claim 100%?

Under the temporary provision, restaurants include businesses that prepare and sell food or beverages to retail customers for immediate on-premises and/or off-premises consumption.

However, restaurants do not include businesses that primarily sell pre-packaged goods not for immediate consumption, such as grocery stores and convenience stores.

Additionally, an employer may not treat certain employer-operated eating facilities as restaurants, even if these facilities are operated by a third party under contract with the employer.

Issue 3: Investing in the IRS and Improving Tax Compliance – American Family Plan Proposal

A well-functioning tax system requires that all taxpayers pay what they owe. An unfortunate characteristic of the current system, however, is an asymmetric adherence to tax law by the nature of income received. While roughly 99% of the taxes due on wages are remitted to the Internal Revenue Service, compliance across other forms of income is substantially less, as the IRS has difficulty verifying whether income from opaque sources is properly reported.

Noncompliance is concentrated at the top of the distribution: A recent study found that the top 1% failed to report 20% of their income and failed to pay nearly $175 billion in taxes owed annually.

Lower levels of compliance not only impact tax progressivity, but they also lower tax revenue and deteriorate our nation’s fiscal position. Left unaddressed, this tax gap— the difference between taxes owed to the government and taxes actually paid—will total about $7 trillion over the course of the next decade. This massive gap in revenue means policymakers must choose between higher taxes elsewhere in the tax system, lower spending on fiscal priorities, or rising budget deficits.

The tax gap has many underlying causes, chief among them being insufficient resources. Budget cuts over the past decade have resulted in an agency that lacks the capacity to address sophisticated tax evasion efforts. Over this period, audit rates for taxpayers making over $1 million in income have fallen by almost 80%

A robust and sustained investment in the IRS is necessary to ensure it can do its job of administering a fair and effective tax system. The IRS requires more resources to conduct investigations into underreported income and to pursue high-income taxpayers who evade their tax liability through complex schemes. It requires 21st century technology to unpack complex tax returns and track income across various opaque sources. And it requires access to better information so that the agency can target its efforts at the most egregious offenders, while helping compliant taxpayers avoid unnecessary and costly audits. This investment will also put the IRS in a position to provide taxpayers with timely answers to questions.

These considerations provide the basis for a series of proposals in the American Families Plan that overhaul tax administration and provide the IRS the resources and information it needs to address tax evasion.

All told, these reforms will generate an additional $700 billion in tax revenue over the course of a decade, net of the investments made. Specifically, the tax administration reforms will:

- Provide the IRS the resources it needs to stop sophisticated tax evasion. Over the last decade, a declining IRS budget has deprived it of the resources it needs to effectively enforce our nation’s tax laws. After accounting for inflation, the IRS budget has fallen by about 20%, and its workforce has been depleted, with the number of complex revenue agents (who are dedicated to high-end evasion and large corporate cases) falling by 35%. As a result, IRS audits have fallen across the board, and particularly for the highest earners.

The IRS has made clear that it needs additional resources to pursue costly tax evasion. These are not easy cases to resolve; the average investigation of a high-wealth individual takes two years to complete and often requires the IRS to commit substantial resources. Moreover, the lack of adequate investment in compliance has significant revenue consequences. Indeed, several hundred taxpayers who committed the most egregious form of evasion—failing to file taxes all together—cost the federal government $10 billion over a period of just three years.

A key component of this initiative is the provision of a sustained, multi-year stream of funding. Altogether, the proposal directs roughly $80 billion to the IRS over a decade to fund an array of priorities—including overhauling technology to improve enforcement efforts, which is more effectively implemented with the assurance of a consistent funding stream. This investment will also facilitate the IRS hiring and training auditors to focus on complex investigations of large corporations, partnerships, and global high-wealth individuals. The President’s proposal directs that additional resources go toward enforcement against those with the highest incomes, rather than Americans with actual income of less than $400,000.

- Provide the IRS with more complete information. When the IRS has information from third parties, income is accurately reported, and taxes are fully paid. However, high-income taxpayers disproportionately accrue income in opaque sources—like partnership and proprietorship income—where the IRS struggles to verify tax filings. As a result, up to 55% of taxes owed on these less visible income streams is unpaid, with disproportionate levels of non-compliance for those at the top of the income distribution.

GAO and IRS research confirm that providing the IRS a mechanism for cross-checking the accuracy of such tax filings is a proven way to improve compliance. This reform aims to provide the IRS information on account flows so that it has a lens into investment and business activity—similar to the information provided on income streams such as wage, pension, and unemployment income. - Importantly, this proposal provides additional information to the IRS without any increased burden for taxpayers. Instead, it leverages the information that financial institutions already know about account holders, simply requiring that they add to their regular, annual reports information about aggregate account outflows and inflows.

- Providing the IRS this information will help improve audit selection so it can better target its enforcement activity on the most suspect evaders, avoiding unnecessary (and costly) audits of ordinary taxpayers.

- Overhaul outdated technology to help the IRS identify tax evasion. Elements of IRS IT systems are antiquated and make it difficult for the IRS to identify those who are not paying their taxes and to help those who want to comply. The President’s proposal provides the IRS much-needed resources to modernize its technological infrastructure. Leveraging 21st century data analytic tools will enable the IRS make use of new information about income that accrues to high-earners and will help revenue agents unpack complex structures, like partnerships, where income is not easily traced.

- Improve taxpayer service and deliver tax credits. A well-functioning tax system requires that taxpayers be able to interact with the IRS in an efficient and meaningful manner. Inadequate resources often mean that IRS service agents are unable to provide taxpayers timely answers to their tax questions. Service enhancement will improve the ability of the IRS to communicate with taxpayers securely and promptly. Importantly, the proposal also includes the necessary resources to ensure that the IRS effectively and efficiently delivers tax credits to families and workers, including newly expanded Child Tax Credits and Child and Dependent Care Tax Credits.

- Regulate paid tax preparers. Taxpayers often make use of unregulated tax preparers who lack the ability to provide accurate tax assistance. These preparers submit more tax returns than all other preparers combined, and they make costly mistakes that subject their customers to painful audits, sometimes even intentionally defrauding taxpayers for their own benefit. The President’s plan calls for giving the IRS the legal authority to implement safeguards in the tax preparation industry. It also includes stiffer penalties for unscrupulous preparers who fail to identify themselves on tax returns and defraud taxpayers (so called “ghost preparers”).

Issue 4: IRS Releases Updated Practice Unit on Reasonable Cause Penalty Defense

This Practice Unit supersedes the previously published Practice Unit with the same title published on July 2, 2020. The Practice Unit was updated to provide further detailed information on factors that should be considered when determining if reasonable cause exists.

Taxpayers may assert that the Service’s application of penalties is not warranted due to a variety of reasons. This unit addresses the taxpayer’s assertion that the return position was based on reasonable cause and that the taxpayer acted in good faith. How the Service evaluates this taxpayer defense depends on the particular penalty that was asserted. In addition to reasonable cause and good faith, certain penalty defenses involve other concepts such as an absence of willful neglect.

The burden is on the taxpayer to provide support to substantiate reasonable cause for penalty relief. Taxpayers are required to exercise ordinary business care and prudence in reporting their proper tax liability. Whether a taxpayer has met the reasonable cause and good faith exception is a facts and circumstances determination that the examiner must make test on a case-by-case basis.

The reasonable cause exception under §6664(c) applies to:

- Most accuracy related penalties under §6662

- Civil fraud under §6663.

The reasonable cause exception under §6664(d) applies to the penalty under §6662A for a reportable transaction understatement when the transaction was adequately disclosed.

The penalty under §6676 (erroneous claim for a refund or credit) also has a reasonable cause exception.

Reasonable cause exceptions for penalty relief also apply to other IRC penalties such as:

- 6651 -Failure to File and/or Failure to Pay

- 6676 -Erroneous Claim for Refund or Credit

- 6721 -Failure to File Correct Information Reporting Returns

- 6694 -Understatement of Taxpayer’s Liability by Return Preparer.

The reasonable cause exception does not apply to a penalty for an underpayment of tax that is due to transactions lacking economic substance as described in §6662(b)(6), or a gross valuation overstatement from a charitable deduction.

Relevant Key Factors

The most significant factor in determining whether a taxpayer has reasonable cause and acted in good faith is the taxpayer’s effort to report the proper tax liability. For Example:

- If a taxpayer reports amounts from an erroneous information return, but does not know the amounts are incorrect, reasonable cause may apply.

- Also, an isolated computation or transposition error by the taxpayer may indicate reasonable cause and a good faith effort.

Other factors to consider are:

- The taxpayer’s experience, knowledge, education, and reliance on the advice of a tax advisor.

- When considering the facts and circumstances, the taxpayer’s experience, education, and sophistication with respect to the tax laws are relevant in determining whether the taxpayer has reasonable cause.

- Reliance on advice from a tax professional must be objectively reasonable. The taxpayer must provide the advisor with all the necessary information to evaluate the tax matter. Additionally, the advisor must have knowledge and expertise related to the tax matter.

IRS will make the determination of whether the taxpayer acted with reasonable cause and in good faith on a case-by-case basis after considering all the facts and circumstances. The taxpayer must have exercised the care that a reasonably prudent person would have used under the circumstances.

Issue 5: Bills from the Hill

H.R.1459 – Ultra-Millionaire Tax Act of 2021. To impose a tax on the net value of assets of a taxpayer.

S.895 – Human Trafficking Survivor Tax Relief Act. To provide an exemption from gross income for mandatory restitution or civil damages as recompense for trafficking in persons.

S.975 – Securing America’s Clean Fuels Infrastructure Act. To extend and modify the credit for alternative fuel vehicle refueling property.

S.985 – Save America’s Clean Energy Jobs Act. To provide direct payments of the renewable electricity production credit, the energy credit, and the carbon oxide sequestration credit.

S.986 – Carbon Capture, Utilization, and Storage Tax Credit Amendments Act of 2021. To provide for a 5-year extension of the carbon oxide sequestration credit, and for other purposes.

S.991 – Corporate Tax Dodging Prevention Act. To modify the treatment of foreign corporations, and for other purposes.

S.994 – For the 99.5 Percent Act. To reinstate estate and generation-skipping taxes, and for other purposes.

H.R.1200 – Stop CHEATERS Act. To provide appropriations for the Internal Revenue Service to overhaul technology and strengthen enforcement.

H.R.1360 – American Dream Down Payment Act of 2021. To establish qualified down payment savings programs.

H.R.1453 – Military Spouses Retirement Security Act. To allow a credit to small employers with respect to each employee who is a military spouse and eligible to participate in a defined contribution plan of the employer.

H.R.1484 – Rural Wind Energy Modernization and Extension Act of 2021. To modify the energy tax credit to apply to qualified distributed wind energy property.

H.R.1557 – Sunshine Forever Act. To extend certain credits related to solar energy.

H.R.1564 – Student Loan Tax Relief Act. To exclude from taxable income any student loan forgiveness or discharge.

S.766 – End Double Taxation of Successful Consumer Claims Act. To allow an above-the-line deduction for attorney fees and costs in connection with consumer claim awards.

S.788 – Firearms Safety Act. To establish a nonrefundable tax credit for the purchase of gun safes and gun safety courses.

S.794 – Tax Excessive CEO Pay Act of 2021. To impose a corporate tax rate increase on companies whose ratio of compensation of the CEO or other highest paid employee to median worker compensation is more than 50 to 1.

S.798 – To ensure that the 2021 Recovery Rebates are not provided to prisoners.

S.804 – SALT Deduction Fairness Act. To increase the limitation on the amount individuals filing jointly can deduct for certain State and local taxes.

S.817 – Wall Street Tax Act of 2021. To impose a tax on certain trading transactions.

S.823 – A bill to amend the American Rescue Plan Act of 2021 to provide for protection of recovery rebates.

S.842 – To ensure that the 2021 Recovery Rebates are not provided to illegal immigrants.

S.844 – PHIT Act of 2021. To treat certain amounts paid for physical activity, fitness, and exercise as amounts paid for medical care.

S.891 – Air Source Heat Pump Act of 2021. To establish a refundable tax credit for the installation of energy efficient air source heat pumps.

S.897 – Improving Child Care for Working Families Act of 2021. To increase the limitation of the exclusion for dependent care assistance programs.

S.905 – Freedom To Invest in Tomorrow’s Workforce Act. To permit certain expenses associated with obtaining or maintaining recognized postsecondary credentials to be treated as qualified higher education expenses for purposes of 529 accounts.

S.928 – To ensure that the 2021 recovery rebates as provided for in the American Rescue Plan Act are not provided to prison inmates and that such sums shall be redirected to the Department of Justice to be paid out in the form of restitution to compensate victims of crime.

S.929 – To ensure that the 2021 recovery rebates as provided for in the American Rescue Plan Act are not provided to prison inmates convicted of murder and that such sums shall be redirected to the Department of Justice to be paid out in the form of restitution to compensate victims of crime.

S.930 – To ensure that the 2021 recovery rebates as provided for in the American Rescue Plan Act are not provided to prison inmates convicted of rape and that such sums shall be redirected to the Department of Justice to be paid out in the form of restitution to compensate victims of crime.

S.931 – To ensure that the 2021 recovery rebates as provided for in the American Rescue Plan Act are not provided to prison inmates convicted of child sex abuse and that such sums shall be redirected to the Department of Justice to be paid out in the form of restitution to compensate victims of crime.

S.948 – To protect American small businesses, gig workers, and freelancers by repealing the burdensome American Rescue Plan Act of 2021 transactions reporting threshold.

H.R.1665 – Employee Profit-Sharing Encouragement Act of 2021. To deny the deduction for executive compensation unless the employer maintains profit-sharing distributions for employees.

H.R.1683 – To exclude certain student loan forgiveness from gross income.

H.R.1704 – Universal Giving Pandemic Response and Recovery Act. To modify and extend the deduction for charitable contributions for individuals not itemizing deductions.

H.R.1712 – Death Tax Repeal Act. To repeal the estate and generation-skipping transfer taxes.

H.R.1807 – Businesses Preparing for a Better Tomorrow Act. To provide a payroll tax credit for best practices training expenses associated with protecting employees from COVID-19.

H.R.1831 – Dependent Income Exclusion Act of 2021. To exclude certain dependent income when calculating modified adjusted gross income for the purposes of eligibility for premium tax credits.

H.R.1854 – RECRUIT Act of 2021. To allow for a credit against tax for employers of reservists.

H.R.1860 – Responsible Additions and Increases To Sustain Employee Health Benefits Act of 2021. To provide the opportunity for responsible health savings to all American families.

H.R.1944 – Healthy Workplaces Act. To provide tax credits for certain expenses associated with protecting employees from COVID-19.

S.1136 – Affordable Housing Credit Improvement Act of 2021. To reform the low-income housing credit, and for other purposes.

S.1149 – To permanently extend the depreciation rules for property used predominantly within an Indian reservation.

S.1156 – Adoption Tax Credit Refundability Act of 2021. To provide for a refundable adoption tax credit.

S.1157 – Tax Fairness for Workers Act. To allow workers an above-the-line deduction for union dues and expenses and to allow a miscellaneous itemized deduction for workers for all unreimbursed expenses incurred in the trade or business of being an employee.

S.1239 – A bill to provide an exclusion from gross income for certain wastewater management subsidies.

Issue 6: Temporary Deviation from Handwritten Signature Requirement for Limited List of Tax Forms

April 15, 2021 Control Number: NHQ-10-0421-0002 Expiration Date: 12/31/2021 This memorandum revises the memorandum issued on December 28, 2020 (Control Number NHQ-10-1220-000).

As part of our response to the COVID-19 situation, IRS has have taken steps to protect employees, taxpayers and their representatives by minimizing the need for in-person contact. Taxpayer representatives have expressed concerns with securing handwritten signatures during these times for forms that are required to be filed or maintained on paper.

To alleviate these concerns while promoting timely filing, we are implementing a deviation with this memorandum that allows taxpayers and representatives to use electronic or digital signatures when signing certain forms that currently require a handwritten signature. Such forms must be signed and postmarked on August 28, 2020 or later.

Form 11-C, Occupational Tax and Registration Return for Wagering.

Form 1066, U.S. Income Tax Return for Real Estate Mortgage Investment Conduit.

Form 637, Application for Registration (For Certain Excise Tax Activities).

Form 706, U.S. Estate (and Generation-Skipping Transfer) Tax Return.

Form 706-A, U.S. Additional Estate Tax Return.

Form 706-GS(D), Generation-Skipping Transfer Tax Return for Distributions.

Form 706-GS(D-1), Notification of Distribution from a Generation-Skipping Trust.

Form 706-GS(T), Generation-Skipping Transfer Tax Return for Terminations.

Form 706-QDT, U.S. Estate Tax Return for Qualified Domestic Trusts.

Form 706 Schedule R-1, Generation Skipping Transfer Tax.

Form 706-NA, U.S. Estate (and Generation-Skipping Transfer) Tax Return.

Form 709, U.S. Gift (and Generation-Skipping Transfer) Tax Return.

Form 730, Monthly Tax Return for Wagers.

Form 1120-C, U.S. Income Tax Return for Cooperative Associations.

Form 1120-FSC, U.S. Income Tax Return of a Foreign Sales Corporation.

Form 1120-H, U.S. Income Tax Return for Homeowners Associations.

Form 1120-IC DISC, Interest Charge Domestic International Sales – Corporation Return.

Form 1120-L, U.S. Life Insurance Company Income Tax Return.

Form 1120-ND, Return for Nuclear Decommissioning Funds and Certain Related Persons

Form 1120-PC, U.S. Property and Casualty Insurance Company Income Tax Return.

Form 1120-REIT, U.S. Income Tax Return for Real Estate Investment Trusts.

Form 1120-RIC, U.S. Income Tax Return for Regulated Investment Companies.

Form 1120-SF, U.S. Income Tax Return for Settlement Funds (Under Section 468B).

Form 1127, Application for Extension of Time for Payment of Tax Due to Undue Hardship.

Form 1128, Application to Adopt, Change or Retain a Tax Year.

Form 2678, Employer/Payer Appointment of Agent.

Form 3115, Application for Change in Accounting Method.

Form 3520, Annual Return to Report Transactions with Foreign Trusts and Receipt

of Certain Foreign Gifts.

Form 3520-A, Annual Information Return of Foreign Trust with a U.S. Owner.

Form 4421, Declaration – Executor’s Commissions and Attorney’s Fees.

Form 4768, Application for Extension of Time to File a Return and/or Pay U.S. Estate

(and Generation-Skipping Transfer) Taxes.

Form 8038, Information Return for Tax-Exempt Private Activity Bond Issues.

Form 8038-G, Information Return for Tax-Exempt Governmental Bonds.

Form 8038-GC; Information Return for Small Tax-Exempt Governmental Bond

Issues, Leases, and Installment Sales.

Form 8283, Noncash Charitable Contributions.

Form 8453 series, Form 8878 series, and Form 8879 series regarding IRS e-file

Signature Authorization Forms.

Form 8802, Application for U.S. Residency Certification.

Form 8832, Entity Classification Election.

Form 8971, Information Regarding Beneficiaries Acquiring Property from a

Decedent.

Form 8973, Certified Professional Employer Organization/Customer Reporting Agreement; and

Elections made pursuant to Internal Revenue Code §83(b).

Issue 7: Frequently Asked Questions About COBRA Assistance Under the American Rescue Plan Act

These FAQs answer questions from stakeholders are to assist individuals understand the law and benefit from it, as intended.

COBRA Continuation Coverage COBRA continuation coverage provides certain group health plan continuation coverage rights for participants and beneficiaries covered by a group health plan.

In general, under COBRA, an individual who was covered by a group health plan on the day before the occurrence of a qualifying event (such as a termination of employment or a reduction in hours that causes loss of coverage under the plan) may be able to elect COBRA continuation coverage upon that qualifying event. Individuals with such a right are referred to as qualified beneficiaries.

Under COBRA, group health plans must provide covered employees and their families with certain notices explaining their COBRA rights. ARP COBRA Premium Assistance §9501 of the ARP provides for COBRA premium assistance to help Assistance Eligible Individuals (as defined below in Q3) continue their health benefits. The premium assistance is also available for continuation coverage under certain State laws.

Assistance Eligible Individuals are not required to pay their COBRA continuation coverage premiums. The premium assistance applies to periods of health coverage on or after April 1, 2021 through September 30, 2021. An employer or plan to whom COBRA premiums are payable is entitled to a tax credit for the amount of the premium assistance.

General Information

Q1: I have heard that the ARP included temporary COBRA premium assistance to pay for health coverage. I would like more information.

The ARP provides temporary premium assistance for COBRA continuation coverage for Assistance Eligible Individuals (see Q3 to determine if the client is eligible). COBRA allows certain people to extend employment-based group health plan coverage, if they would otherwise lose the coverage due to certain life events such as loss of a job. Individuals may be eligible for premium assistance if they are eligible for and elect COBRA continuation coverage because of their own or a family member’s reduction in hours or an involuntary termination from employment. This premium assistance is available for periods of coverage from April 1, 2021 through September 30, 2021.

This premium assistance is generally available for continuation coverage under the Federal COBRA provisions, as well as for group health insurance coverage under comparable state continuation coverage (“mini-COBRA”) laws.

If the client was offered Federal COBRA continuation coverage as a result of a reduction in hours or an involuntary termination of employment, and they declined to take COBRA continuation coverage at that time, or they elected Federal COBRA continuation coverage and later discontinued it, they may have another opportunity to elect COBRA continuation coverage and receive the premium assistance, if the maximum period they would have been eligible for COBRA continuation coverage has not yet expired (if COBRA continuation coverage had been elected or not discontinued).

Q2: Which plans does the premium assistance apply to?

The COBRA premium assistance provisions apply to all group health plans sponsored by private-sector employers or employee organizations (unions) subject to the COBRA rules under the Employee Retirement Income Security Act of 1974 (ERISA). They also apply to plans sponsored by State or local governments subject to the continuation provisions under the Public Health Service Act. The premium assistance is also available for group health insurance required under state mini-COBRA laws.

Q3: How can the client tell if they are eligible to receive the COBRA premium assistance?

The ARP makes the premium assistance available for “Assistance Eligible Individuals.” An Assistance Eligible Individual is a COBRA qualified beneficiary who meets the following requirements during the period from April 1, 2021 through September 30, 2021:

- Is eligible for COBRA continuation coverage by reason of a qualifying event that is a reduction in hours (such as reduced hours due to change in a business’s hours of operations, a change from full-time to part-time status, taking of a temporary leave of absence, or an individual’s participation in a lawful labor strike, as long as the individual remains an employee at the time that hours are reduced) or an involuntary termination of employment (not including a voluntary termination); and

- Elects COBRA continuation coverage.

However, they are not eligible for the premium assistance if they are eligible for other group health coverage, such as through a new employer’s plan or a spouse’s plan (not including excepted benefits, a qualified small employer health reimbursement arrangement (QSEHRA), or a health flexible spending arrangement (FSA)), or if they are eligible for Medicare.

Note that if they have individual health insurance coverage, like a plan through the Health Insurance Marketplace, or if they have Medicaid, they may be eligible for ARP premium assistance.

However, if they elect to enroll in COBRA continuation coverage with premium assistance, they will no longer be eligible for a premium tax credit, advance payments of the premium tax credit, or the health insurance tax credit for their health coverage during that period.

Note: If the employee’s termination of employment was for gross misconduct, the employee and any dependents would not qualify for COBRA continuation coverage or the premium assistance.

Q4: If they are eligible for the premium assistance, how long will it last?

The premium assistance can last from April 1, 2021 through September 30, 2021. However, it will end earlier if:

- The client becomes eligible for another group health plan, such as a plan sponsored by a new employer or a spouse’s employer (not including excepted benefits, a QSEHRA, or a health FSA), or you become eligible for Medicare, or

- They reach the end of the maximum COBRA continuation coverage period.

If they continue the COBRA continuation coverage after the premium assistance period, they may have to pay the full amount of the premium otherwise due. Failure to do so may result in the loss of COBRA continuation coverage. Contact the plan administrator, employer sponsoring the plan, or health insurance issuer for more information.

When the COBRA premium assistance ends, they may be eligible for Medicaid or a special enrollment period to enroll in coverage through the Health Insurance Marketplace or to enroll in individual market health insurance coverage outside of the Marketplace. A special enrollment period is also available when they reach the end of the maximum COBRA coverage period. They may apply for and, if eligible, enroll in Medicaid coverage at any time.

Individuals receiving the COBRA premium assistance must notify their plans if they become eligible for coverage under another group health plan (not including excepted benefits, a QSEHRA, or a health FSA), or for Medicare. Failure to do so can result in a tax penalty.

Q5: Who is eligible for an additional election opportunity for COBRA continuation coverage?

A qualified beneficiary whose qualifying event was a reduction in hours or an involuntary termination of employment prior to April 1, 2021 and who did not elect COBRA continuation coverage when it was first offered prior to that date or who elected COBRA continuation coverage but is no longer enrolled (for example, an individual who dropped COBRA continuation coverage because he or she was unable to continue paying the premium) may have an additional election opportunity at this time. Individuals eligible for this additional COBRA election period must receive a notice of extended COBRA election period informing them of this opportunity.

This notice must be provided within 60 days of the first day of the first month beginning after the date of the enactment of the ARP (so, by May 31, 2021) and individuals have 60 days after the notice is provided to elect COBRA.

However, this additional election period does not extend the period of COBRA continuation coverage beyond the original maximum period (generally 18 months from the employee’s reduction in hours or involuntary termination).

COBRA continuation coverage with premium assistance elected in this additional election period begins with the first period of coverage beginning on or after April 1, 2021.

Individuals can begin their coverage prospectively from the date of their election, or, if an individual has a qualifying event on or before April 1st, choose to start their coverage as of April 1st, even if the individual receives an election notice and makes such election at a later date. In either case, please note that the premium assistance is only available for periods of coverage from April 1, 2021 through September 30,2021.

Q6: Does the ARP change any State program requirements or time periods for election of continuation coverage?

No. The ARP does not change any requirement of a State continuation coverage program. The ARP only allows Assistance Eligible Individuals who elect continuation coverage under State insurance law to receive premium assistance from April 1, 2021 through September 30, 2021. It also allows Assistance Eligible Individuals to switch to other coverage offered to similarly situated active employees if the plan allows it, provided that the new coverage is no more.

expensive than the prior coverage.

Q7: How do I apply for the premium assistance?

If the client was covered by an employment-based group health plan on the last day of their employment or a family member’s employment (or the last day before their or the family member’s reduction in hours causing a loss of coverage), the plan or issuer should provide them and their beneficiaries with a notice of their eligibility to elect COBRA continuation coverage and to receive the premium assistance.

The notice should include any forms necessary for enrollment, including forms to indicate that they are an Assistance Eligible Individual and that they are not eligible for another group health plan (this does not include excepted benefits, a QSEHRA, or a health FSA), or eligible for Medicare.

If the client believes they are (or may be, upon a COBRA election) an Assistance Eligible Individual and have not received a notice from their employer, they may notify the employer of the request for treatment as an Assistance Eligible Individual (for example, using the “Request for Treatment as an Assistance Eligible Individual Form” that is attached to the Summary of COBRA Premium Assistance Provisions under the American Rescue Plan Act of 2021) for periods of coverage starting April 1, 2021.

If they are an Assistance Eligible Individual, the ARP provides that they must be treated, for purposes of COBRA, as having paid in full the amount of such premium from April 1, 2021 through September 30, 2021.

Accordingly, plans and issuers should not collect premium payments from Assistance Eligible Individuals and subsequently require them to seek reimbursement of the premiums for periods of coverage beginning on or after April 1, 2021, and preceding the date on which an employer sends an election notice, if an individual has made an appropriate request for such treatment.

Q8: How will the premium assistance be provided to me?

The client will not receive a payment of the premium assistance. Instead, Assistance Eligible Individuals do not have to pay any of the COBRA premium for the period of coverage from April 1, 2021 through September 30, 2021. The premium is reimbursed directly to the employer, plan administrator, or insurance company through a COBRA premium assistance credit.

Q9: Am I required to pay any administrative fees?

If the client is an Assistance Eligible Individual, they will not need to pay any part of what they would otherwise pay for your COBRA continuation coverage, including any administration fee that would otherwise be charged.

Notices

Q10: Does the ARP impose any new notice requirements?

Yes, plans and issuers are required to notify qualified beneficiaries regarding the premium assistance and other information about their rights under the ARP, as follows:

- A general notice to all qualified beneficiaries who have a qualifying event that is a reduction in hours or an involuntary termination of employment from April 1, 2021 through September 30, 2021. This notice may be provided separately or with the COBRA election notice following a COBRA qualifying event.

- A notice of the extended COBRA election period to any Assistance Eligible Individual (or any individual who would be an Assistance Eligible Individual if a COBRA continuation coverage election were in effect) who had a qualifying event before April 1, 2021. This requirement does not include those individuals whose maximum COBRA continuation coverage period, if COBRA had been elected or not discontinued, would have ended before April 1, 2021 (generally, those with applicable qualifying events before October 1, 2019). This notice must be provided within 60 days following April 1, 2021 (that is, by May 31, 2021).

The ARP also requires that plans and issuers provide individuals with a notice of expiration of periods of premium assistance explaining that the premium assistance for the individual will expire soon, the date of the expiration, and that the individual may be eligible for coverage without any premium assistance through COBRA continuation coverage or coverage under a group health plan. Coverage may also be available through Medicaid or the Health Insurance Marketplace. This notice must be provided 15 – 45 days before the individual’s premium assistance expires.

Unless specifically modified by the ARP, the existing requirements for the manner and timing of COBRA notices continue to apply. Due to the COVID-19 National Emergency, DOL, the Department of the Treasury, and the IRS issued guidance extending timeframes for certain actions related to health coverage under private-sector employment-based group health plans.

The extensions under the Joint Notice and EBSA Disaster Relief Notice 2021-01 do not apply, however, to the notices or the election periods related to COBRA premium assistance available under the ARP. Therefore, plans and issuers must provide the notices according to the timeframes specified in the ARP (outlined above).

DOL is committed to ensuring that individuals receive the benefits to which they are entitled under the ARP. Employers or multiemployer plans may also be subject to an excise tax under the Internal Revenue Code for failing to satisfy the COBRA continuation coverage requirements.

This tax could be as much as $100 per qualified beneficiary, but not more than $200 per family, for each day that the taxpayer is in violation of the COBRA rules.

Q11: What information must the notices include?

The notices must include the following information:

- The forms necessary for establishing eligibility for the premium assistance.

- Contact information for the plan administrator or other person maintaining relevant information in connection with the premium assistance.

- A description of the additional election period (if applicable to the individual).

- A description of the requirement that the Assistance Eligible Individual notify the plan when he/she becomes eligible for coverage under another group health plan (not including excepted benefits, a QSEHRA, or a health FSA), or eligible for Medicare and the penalty for failing to do so.

- A description of the right to receive the premium assistance and the conditions for entitlement; and

- If offered by the employer, a description of the option to enroll in a different coverage option available under the plan.

Q12: Will there be model notices?

Yes. DOL has developed model notices that are available at https://www.dol.gov/cobra-subsidy.

Individual Questions for Employees and Their Families

Q13: How much time do I have to enroll in COBRA continuation coverage?

In general, individuals who are eligible for COBRA continuation coverage have 60 days after the date that they initially receive their COBRA election notice to elect COBRA continuation coverage. Due to the COVID-19 National Emergency, DOL, the Department of the Treasury, and the IRS issued guidance extending timeframes for certain actions related to health coverage under private-sector employment-based group health plans. The extensions under the Joint Notice and EBSA Disaster Relief Notice 2021-01 do not apply, however, to the notices or elections related to COBRA premium assistance available under the ARP.

Potential Assistance

Eligible Individuals therefore must elect COBRA continuation coverage within 60 days of receipt of the relevant notice or forfeit their right to elect COBRA continuation coverage with premium assistance.

Similarly, plans and issuers must provide the notices required under the ARP within the timeframe required by the ARP.

Assistance Eligible Individuals do not need to send any payments for the COBRA continuation coverage during the premium assistance period.

Q14: I am an Assistance Eligible Individual who has been enrolled in COBRA continuation coverage since December 2020. Will I receive a refund of the premiums that I have already paid?

No. The COBRA premium assistance provisions in the ARP apply only to premiums for coverage periods from April 1, 2021 through September 30, 2021. If you were eligible for premium assistance but paid in full for periods of COBRA continuation coverage beginning on or after April 1, 2021 through September 30, 2021, you should contact the plan administrator.

Note, however, that a potential Assistance Eligible Individual has the choice of electing COBRA continuation coverage beginning April 1, 2021 or after (or beginning prospectively from the date of your qualifying event if your qualifying event is after April 1, 2021), or electing COBRA continuation coverage commencing from an earlier qualifying event if the individual is eligible to make that election, including under the extended time frames provided under the Joint Notice and EBSA Notice 2021-01.

The election period for COBRA continuation coverage with premium assistance does not cut off the individual’s preexisting right to elect COBRA continuation coverage, including under the extended time frames provided under the Joint Notice and EBSA Notice 2021-01.

Note, that the premium assistance is only available for periods from April 1, 2021 through September 30,2021.

Q15: I am currently enrolled in COBRA continuation coverage, but I would like to switch to a different coverage option offered by the same employer. Can I do this?

Group health plans can choose to allow qualified beneficiaries to enroll in coverage that is different from the coverage they had at the time of the COBRA qualifying event. The ARP provides that changing coverage will not cause an individual to be ineligible for the COBRA premium assistance, provided that:

- The COBRA premium charged for the different coverage is the same or lower than for the coverage the individual had at the time of the qualifying event.

- The different coverage is also offered to similarly situated active employees; and

- The different coverage is not limited to only excepted benefits, a QSEHRA, or a health FSA.

If the plan permits individuals to change coverage options, the plan must provide the individuals with a notice of their opportunity to do so. Individuals have 90 days to elect to change their coverage after the notice is provided.

Q16: Only part of my family elected COBRA continuation coverage but all of us were eligible. Can I enroll the others and take advantage of the premium assistance?

Each COBRA qualified beneficiary may independently elect COBRA continuation coverage. If a family member did not elect COBRA continuation coverage when first eligible and that individual would be an Assistance Eligible Individual, that individual has an additional opportunity to enroll and qualify for the premium assistance. However, this extended election period does not extend the maximum period of COBRA continuation coverage had COBRA continuation coverage been originally elected.

Q17: I received my COBRA election notice. Can I change my coverage option from the one I had previously?

In general, COBRA continuation coverage provides the same coverage that the individual had at the time of the qualifying event. However, under the ARP, a plan may offer Assistance Eligible Individuals the option of choosing other coverage that is also offered to similarly situated active employees and that does not have higher premiums than the coverage the individual had at the time of the qualifying event.

Q18: I am currently enrolled in individual market health insurance coverage, but I am potentially an Assistance Eligible Individual. Can I switch to COBRA continuation coverage with premium assistance?

Yes, Potential Assistance Eligible Individuals can use the election period to change from individual market health insurance coverage (that they got either through a Health Insurance Marketplace, such as through HealthCare.gov, or outside of the Marketplace) to COBRA continuation coverage with premium assistance. Additionally, they may apply for and, if eligible enroll in Medicaid at any time. If they elect to enroll in COBRA continuation coverage with premium assistance, they will no longer be eligible for a premium tax credit, or advance payments of the premium tax credit, for Marketplace coverage they otherwise would qualify for during this premium assistance period.

They must contact the Marketplace to let them know that they have enrolled in other minimum essential coverage or they may have to repay some or all of the advance payments of the premium tax credit made on their behalf during the period they were enrolled in both COBRA continuation coverage and Marketplace coverage. This repayment would be required when filing the income tax return for 2021.

Q19: Can I end my individual health insurance coverage retroactively if I can qualify for COBRA with premium assistance starting on April 1?

Enrollees generally are not permitted to terminate coverage purchased through a Marketplace retroactively. They must do so prospectively. If they want to end coverage that they got from a Health Insurance Marketplace, such as on HealthCare.gov, because they want to change to COBRA continuation coverage with premium assistance, they must update their Marketplace application or call the Marketplace to do so.

If they enrolled in coverage through HealthCare.gov, they could call 1-800-318-2596 (TTY: 1-855-889-4325). If their state has its own Marketplace platform, find contact information for State Marketplace information here:

https://www.healthcare.gov/marketplace-in-your-state/

If they want to end individual health insurance coverage that they got outside of a Marketplace, such as directly from an insurance company, they must contact the insurance company to do so.

Q20: What should I consider when making a decision whether to continue with individual market health insurance coverage or change to COBRA continuation coverage with premium assistance?

The client should consider the factors they normally would when deciding on which health insurance coverage is right for them and their family. For example, in addition to premium cost, they may want to compare cost-sharing requirements such as plan deductibles and copays. They may also want to consider how much progress they have made toward their deductible and other plan accumulators, and compare different plans’ and coverage options’ provider networks and

prescription drug formularies based on their family’s medical care needs. Note, however, that if they are currently employed by the employer offering the COBRA continuation coverage with premium assistance, they may enroll in Marketplace coverage but are ineligible for a subsidy or a premium tax credit for the Marketplace coverage for the period they are offered the COBRA continuation coverage with premium assistance.

Q21: Can I qualify for a special enrollment period (SEP) to enroll in individual market health insurance coverage, such as through a Health Insurance Marketplace, when my COBRA premium assistance ends on September 30? What about if my COBRA continuation coverage ends sooner than that?

When their COBRA premium assistance ends, they may be eligible for a SEP to enroll in coverage through a Health Insurance Marketplace, or to enroll in individual health insurance coverage outside of the Marketplace. They may also qualify for a SEP when they reach the end of the maximum COBRA coverage period.

If their state has its own Marketplace platform, find contact information for their State Marketplace here:

https://www.healthcare.gov/marketplace-in-your-state/

Q21: How can I get more information on my eligibility for COBRA continuation coverage or the premium assistance, including help if my employer has denied my request for the premium assistance?

For group health plans sponsored by private-sector employers, guidance and other information is available on the DOL web site at https://www.dol.gov/cobra-subsidy. They can also contact one of EBSA’s Benefits Advisors at askebsa.dol.gov or 1.866.444.3272.

EBSA’s Benefits Advisors may also be able to assist if the client feels that their plan or employer has improperly denied their request for treatment as an Assistance Eligible Individual. Employers and plans may be subject to an excise tax under the Internal Revenue Code for failing to satisfy the COBRA continuation coverage requirements.

This tax could be as much as $100 per qualified beneficiary, but not more than $200 per family, for each day that the plan or employer is in violation of the COBRA rules. If they feel they may have been improperly denied premium assistance, contact EBSA at askebsa.dol.gov or 1.866.444.3272.

If they work for a state or local government employer and have questions regarding the premium assistance, please contact the Centers for Medicare & Medicaid Services via email at: [email protected] or call 410-786-1565

Issue 8: Advance Child Tax Credit – What We Know Thus Far

The first monthly payment of the expanded and newly advanceable Child Tax Credit (CTC) from the American Rescue Plan will be made on July 15.

Roughly 39 million households — covering 88% of children in the United States — are slated to begin receiving monthly payments without any further action required. CTC payments will be made on the 15th of each month unless the 15th falls on a weekend or holiday.

Eligible families will receive a payment of up to $300 per month for each child younger than age 6, and up to $250 per month for each child age 6 and older.

Special Procedures for Filing Simplified Paper or Electronic Tax Returns if the Individual is not Required to File a Federal Income Tax Return for the Year 2020, Rev. Proc. 2021-24

Under the simplified procedure set forth a simplified return may be filed on paper or electronically, on a Form 1040, U.S. Individual Income Tax Return, Form 1040-SR, U.S. Tax Return for Seniors, or Form 1040-NR, U.S. Nonresident Alien Income Tax Return.

A Federal income tax return for taxable year 2020 filed under the simplified procedure will result in the following:

(1) The Secretary will use the information provided on the simplified return to:

(i) estimate the annual advance amount for the simplified return filer, and

(ii) calculate the third-round economic impact payment for which the simplified return filer is eligible.

A nonresident alien is not eligible under § 6428B(c) to receive third-round economic impact payments.

(2) The simplified return filer may claim the 2020 recovery rebate credit and additional 2020 recovery rebate credit when filing Form 1040 or Form 1040-SR.

Again, a nonresident alien is not eligible under §§ 6428(d) and 6428A(d) to claim the 2020 recovery rebate credit or additional 2020 recovery rebate credit.

Definition of Simplified Return Filer

Aa “simplified return filer” is an individual who is not required to file a Federal income tax return for taxable year 2020 and has not filed a paper or electronic Federal income tax return for that taxable year.

A simplified return filer, however, does not include a resident of a U.S. territory.

Simplified Filing Method

In the case of a simplified return filer, the IRS will process the simplified return filer’s Form 1040, Form 1040-SR, or Form 1040-NR for taxable year 2020 to calculate the Federal income tax benefits.

The Form 1040, Form 1040-SR, or Form 1040-NR must include the following information:

- Write Rev. Proc. 2021-24 on form. A simplified return filer who files the Federal income tax return by mail must indicate “Rev. Proc. 2021-24” above the printed material at the top of page 1 of the Form 1040, Form 1040-SR, or Form 1040-NR.

- A simplified return filer must select their filing status for taxable year 2020 at the top of Form 1040, Form 1040-SR, or Form 1040-NR.

- A simplified return filer must enter their name, mailing address, and SSN or IRS individual taxpayer identification number (ITIN), and the name and SSN or ITIN of their spouse if filing a joint return, on the appropriate lines of Form 1040, Form 1040-SR, or Form 1040-NR.

- A nonresident or resident alien simplified return filer who does not have and is not eligible to receive an SSN and does not have an ITIN must attach Form W-7, 15 Application for IRS Individual Taxpayer Identification Number, to Form 1040, Form 1040-SR, or Form 1040-NR to apply for an ITIN. Such nonresident alien simplified return filer is not eligible for the 2020 recovery rebate credit, additional 2020 recovery rebate credit, or third-round economic impact payments. Unless filing a joint return with someone who has an SSN, such resident alien simplified return filer is not eligible for the 2020 recovery rebate credit or additional 2020 recovery rebate credit. Unless a return includes a dependent, who has an SSN or an ATIN or is filed jointly with someone who has an SSN, such resident alien simplified return filer is not eligible for third-round economic impact payments.

- A simplified return filer must check all applicable boxes in the area immediately below the virtual currency line for each individual who could be claimed as a dependent by any other individual for taxable year 2020.

General Information Regarding Dependents

A simplified return filer should provide information on the appropriate lines of Form 1040, Form 1040-SR, or Form 1040-NR regarding each dependent at the end of taxable year 2020 who has an SSN or an ATIN.

For each dependent, a simplified return filer must provide the name, SSN or ATIN, and relationship to the individual.

A simplified return filer should check the child tax credit box in Column (4) for each dependent who has an SSN that is valid for employment and is a 2020 CTC qualifying child of the simplified return filer for taxable year 2020.

A simplified return filer must leave blank lines 1 through 38 of Form 1040 or Form 1040-SR, even if the values for these lines are in fact not zero.

A simplified return filer who files their Federal income tax return electronically must enter $1 on lines 2b, 9, and 11.

A simplified return filer must enter the applicable standard deduction amount, if any, for their filing status on line 12.

Form 1040-NR filers who file their Federal income tax return electronically must enter $1 on lines 7 and 8 of Schedule A (Form 1040-NR) and line 12 of Form 1040-NR.

A simplified return filer must enter $0 on line 15.

Lines 30, 32, 33, 34, and 35a (2020 recovery rebate credit entries). A simplified return filer who files Form 1040 or Form 1040-SR may enter the sum of the filer’s 2020 recovery rebate credit and additional 2020 recovery rebate credit on lines 30, 32, 33, 34, and 35a. The credit amounts should be computed using the Recovery Rebate Credit Worksheet for line 30 in the 2020. Providing the correct amount will speed up the payment of the 2020 recovery rebate credit and additional 2020 recovery rebate credit, as well as the third-round economic impact payment. If any amount is incorrect on line 30, 32, 33, 34, or 35a, the IRS will correct that amount claimed on these lines, but the correction will delay processing of the return and therefore enrollment for advance child tax credit payments.

A simplified return filer should not check the box on line 35a because neither advance child tax credit payments, nor third-round economic impact payments, may be divided among multiple accounts.

A simplified return filer may request the direct deposit of their advance child tax credit payments and any future third-round economic impact payment into their account at a bank or other financial institution by entering their direct deposit information on lines 35b through 35d.

A simplified return filer must not request their advance child tax credit payment or third round economic impact payment to be deposited into an account that is not in the name of that simplified return filer (for example, a simplified return filer must not request a direct deposit of their advance child tax credit payment or third-round economic impact payment into their tax return preparer’s account).

A simplified return filer must sign the return under penalties of perjury, including the filer’s identity protection personal identification number (that is, the filer’s IP PIN), if applicable, as part of the filer’s signature. In addition, a simplified return filer may enter the identifying information of any third-party designee, if applicable, at the bottom of page 2 of Form 1040, Form 1040-SR, or Form 1040-NR.

A simplified return filer who has been assigned an IP PIN, but has misplaced it, may retrieve the IP PIN at https://www.irs.gov/identity-theft-fraud-scams/retrieve-your-ip-pin.

A simplified return is a Federal income tax return for all purposes, whether filed electronically or on paper.

Individuals who report incorrect information regarding qualifying children or other dependents or otherwise provide incorrect information on simplified returns may be liable for civil or criminal penalties. However, the IRS will not challenge the accuracy of the items of income reported by simplified return filers on a simplified return filed.

Electronic filing procedure:

A zero AGI filer may file electronically Form 1040, Form 1040- SR, or Form 1040-NR for taxable year 2020. A Federal income tax return for taxable year 2020 filed under the procedure in this section 5, will result in the following:

The Secretary will use the information provided in the electronic return to:

(i) estimate the annual advance amount for the zero AGI filer, and

(ii) calculate the third-round economic impact payment for which the zero AGI filer is eligible.

The special procedure applies only to an electronically filed return for a zero AGI filer and does not apply to a return filed on paper.

A “zero AGI filer” is an individual who is not required to file a Federal income tax return for taxable year 2020, has zero AGI for taxable year 2020 (that is, the individual has zero AGI for taxable year 2020 reportable on line 11 of Form 1040, Form 1040-SR, or Form 1040- NR), and has not yet filed a Federal income tax return for taxable year 2020. A zero AGI filer, however, does not include a resident of a U.S. territory. .

In addition to all other information required to be entered on Form 1040, Form 1040-SR, or Form 1040-NR, a zero AGI filer must enter the following:

- $1 as taxable interest on line 2b of the form.

- $1 as total income on line 9 of the form.

- $1 as AGI on line 11 of the form; and

- $1 as itemized deductions on lines 7 and 8 of Schedule A (Form 1040-NR) and line 12 of Form 1040-NR (Form 1040-NR filers only).

A zero AGI filer must sign the return under penalties of perjury including the filer’s IP PIN, if applicable, as part of the filer’s signature. In addition, a zero AGI filer may enter the identifying information of any third-party designee, if applicable. A zero AGI filer who has been assigned an IP PIN, but has misplaced it, may retrieve the IP PIN at https://www.irs.gov/identity-theft-fraud-scams/retrieve-your-ip-pin.20

Individuals who report incorrect information regarding qualifying children or other dependents or otherwise provide incorrect information on their returns may be liable for civil or criminal penalties. However, the IRS will not challenge the accuracy of the items of income reported by zero AGI filers on their returns.

Issue 9: The 2021 Bentley Added to the List of Plug-In Electric Vehicles

2020, 2021 – Bentayga Hybrid SUV – $7,500

Issue 10: Dyed Diesel Fuel Penalty Relief Due to Disruptions of the Fuel Supply Chain

In response to disruptions of the fuel supply chain, IRS will not impose a penalty when dyed diesel fuel is sold for use or used on the highway in the states of Alabama, Delaware, Georgia, Florida, Louisiana, Maryland, Mississippi, North Carolina, Pennsylvania, South Carolina, Tennessee, Virginia, and the District of Columbia.

This relief is retroactive to May 7, 2021 and will remain in effect through May 21, 2021.

This penalty relief is available to any person that sells or uses dyed diesel fuel for highway use. In the case of the operator of the vehicle in which the dyed diesel fuel is used, the relief is available only if the operator or the person selling such fuel pays the tax of 24.4 cents per gallon that is normally applied to diesel fuel for highway use.

The IRS will not impose penalties for failure to make semimonthly deposits of this tax.

Ordinarily, dyed diesel fuel is not taxed, because it is sold for uses exempt from excise tax, such as to farmers for farming purposes, for home heating use, and to local governments.

Issue 11: IRS Issues Guidance on Taxability of Dependent Care Assistance Programs for 2021 and 2022

Guidance on the taxability of dependent care assistance programs for 2021 and 2022, clarifies that amounts attributable to carryovers or an extended period for incurring claims generally are not taxable. The guidance also illustrates the interaction of this standard with the one-year increase in the exclusion for employer-provided dependent care benefits from $5,000 to $10,500 for the 2021 taxable year under the American Rescue Plan Act.

Because of the pandemic, many people were unable to use the money they set aside in their dependent care assistance programs in 2020 and 2021. Generally, under these plans, an employer allows its employees to set aside a certain amount of pre-tax wages to pay for dependent care expenses. The employee’s expenses are then reimbursed from the dependent care assistance program.

Carryovers of unused dependent care assistance program amounts generally are not permitted (although a 2½ month grace period is allowed). However, recent coronavirus-related legislation (the Taxpayer Certainty and Disaster Tax Relief Act of 2020) allowed employers to amend their plans to permit the carryover of unused dependent care assistance program amounts to plan years ending in 2021 and 2022, or to extend the permissible period for incurring claims to plan years over the same period.

Notice 2021-26 clarifies for taxpayers that if these dependent care benefits would have been excluded from income if used during taxable year 2020 (or 2021, if applicable), these benefits will remain excludible from gross income and are not considered wages of the employee for 2021 and 2022.

Notice 2021-15, issued in February 2021, states that if an employer adopted a carryover or extended period for incurring claims, the annual limits for dependent care assistance program amounts apply to amounts contributed, not to amounts reimbursed or available for reimbursement in a particular plan or calendar year. Therefore, participants in dependent care assistance programs may continue to contribute the maximum amount to their plans for 2021 and 2022.

Issue 12: IRS Processing Update

The IRS is now opening mail within normal timeframes. The IRS has also made significant progress in processing prior year returns. As of May 15, 2021, IRS had 300,000 individual tax returns received prior to 2021 in the processing pipeline. Including current year returns, as of May 15, 2021, IRS had 16.4 million unprocessed individual returns in the pipeline.

Unprocessed returns include those requiring correction to the Recovery Rebate Credit amount or validation of 2019 income used to figure the Earned Income Tax Credit (EITC) and Additional Child Tax Credit (ACTC). This work does not require IRS to correspond with taxpayers but does require special handling by an IRS employee so, in these instances, it is taking the IRS more than 21 days to issue any related refund.

If, as a result, a correction is made to any RRC, EITC or ACTC claimed on the return, the IRS will send taxpayers an explanation.

The IRS understands the importance of timely processing of tax returns and refund issuance. They are processing returns received over the summer and fall in 2020 due to the extended July 15, 2020 tax filing due date. While the majority of 2019 refund returns have been processed, in some cases, they are processing tax returns that were mailed with a payment even though payment associated with these returns have been processed by the IRS.

However, they are rerouting tax returns and taxpayer correspondence from locations that are behind to locations where more staff is available, and are taking other actions to minimize any delays. Tax returns are opened in the order received. As the return is processed, it may be delayed because it has a mistake including errors concerning the Recovery Rebate Credit, is missing information, or there is suspected identity theft or fraud. If IRS can fix it without contacting the client, they will. If they need more information or need the client to verify that it was them who sent the tax return, they will issue a letter to the client. The resolution of these issues depends on how quickly and accurately the client responds, and the ability of IRS staff trained and working under social distancing requirements to complete the processing of the return.

If the client filed electronically and received an acknowledgement, they do not need to take any further action other than promptly responding to any requests for information.

If they filed on paper, check Where’s my refund? If it tells them that IRS has received the return or are processing or reviewing it, they are processing the return, but it may be under review.

Please don’t file a second tax return or contact the IRS about the status of the return.

Status of Processing Form 941, Employer’s Quarterly Federal Tax Return and Form 941-X, Adjusted Employer’s Quarterly Federal Tax Return or Claim for Refund:

The IRS is now opening mail within normal timeframes. The IRS has also made significant progress in processing Forms 941. As of May 6, 2021, we had about 200,000 Forms 941 received prior to 2021 in the processing pipeline. Including current year returns, as of May 6, 2021, they had 1.9 million unprocessed 941s in the pipeline. And are rerouting tax returns and taxpayer correspondence from locations that are behind to locations where more staff is available and are taking other actions to minimize any delays.

Tax returns are opened in the order received. As of May 7, 2021, our inventory of unprocessed Forms 941-X was approximately 100,000 which cannot be processed until the related 941s are processed. While not all of these returns involve a COVID credit, the inventory is being worked at two sites (Cincinnati and Ogden) that have trained staff to work possible COVID credits.

Payment Processing Issues

IRS has identified a delay in processing Form 1040 balance due, Form 1040-X amended, and Form 1040-ES estimated tax payment requests submitted via Modernized e-File. The issue has been resolved, and pending payments are being processed. The taxpayer’s account will be credited with the original requested payment date(s).

Taxpayers should not re-resubmit these payments. If a taxpayer re-submitted any of these payment requests due to the delay in processing, they may cancel them by calling 888-353-4537.

Cancellation requests must be received no later than 11:59 p.m., Eastern Time, at least two business days prior to a scheduled payment date.

Issue 13: Correction to the Form 1040 Line in Reference to Form 4797 Instructions

Page 3 of the 2020 Instructions for Form 4797, Sales of Business Property, includes an incorrect reference to a line on Form 1040. On page 3, in the third column, under “§ 197(f)(9)(B)(ii) Election,” the instructions state to report the additional tax on Form 1040, line 12a.

For 2020, the additional tax should be reported on Form 1040, line 16.

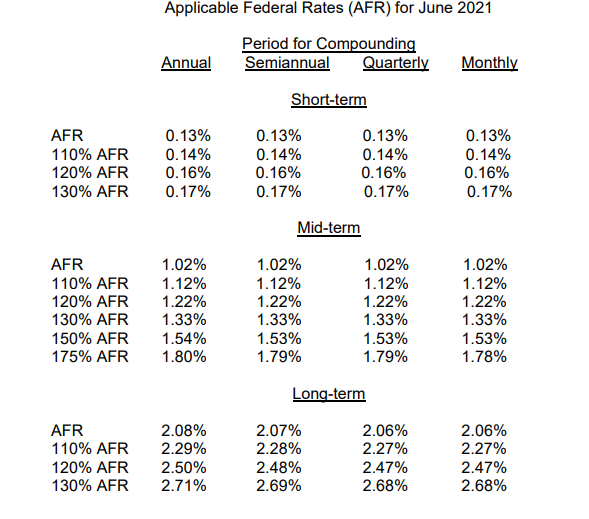

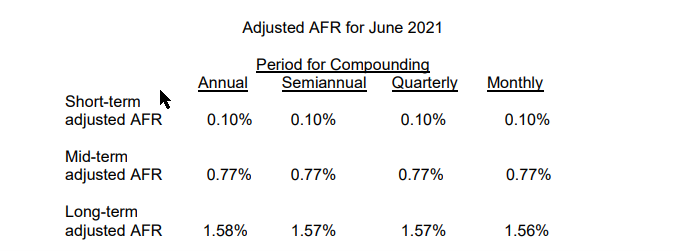

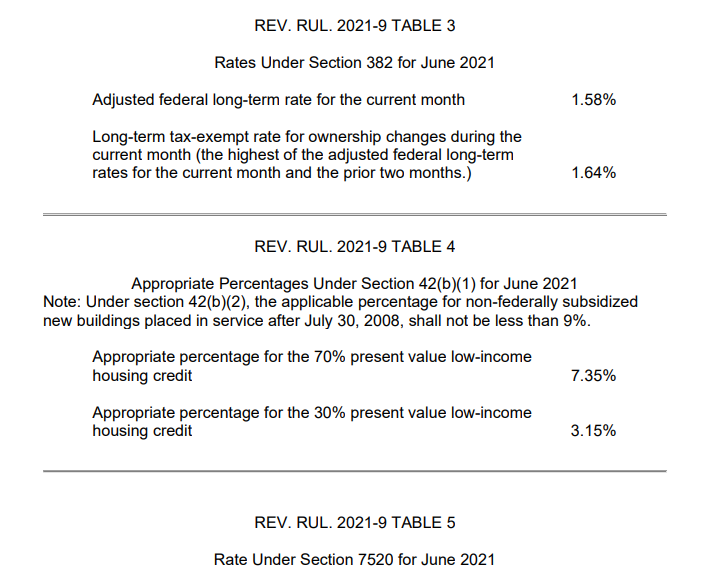

Issue 14: Applicable Federal Rates for June 2021, Rev. Rul. 2021-09

Rev. Rul. 2021-9 Table 1

![]() Basics & Beyond Resources

Basics & Beyond Resources

- Blog Page

- Resource List

- Webinar & Seminar Schedules

- Get Registered!

- Note: Paid attendees can request a link to the replay of any previously recorded webinar presentations by emailing us at [email protected]