This month we are including the Taxpayer Advocate annual report which defines many of the issues IRS faces and how they intend to improve on. It is worth a read, as it identifies key points which we as tax professional struggle with such as delays in correspondence and processing. It also acknowledges the improvements IRS has made since the COVID crises. We realize you are deep into filing season, and we hope things are going well, but this summary provides information on where IRS needs to improve and the stats are interesting.

Don’t forget to register for the Unlimited Webinar Package: https://www.cpehours.com/webinar-schedule/

In this Issue:

- Required Minimum Distributions

- IRS launches Simple Notice Initiative Redesign Effort

- A Message from IRS Commissioner Danny Werfel

- IRS Offering Additional Time at Taxpayer Assistance Centers for Face-to-Face Help

- TurboTax Advertising Found to be Deceptive.

- National Taxpayer Advocate Delivers Annual Report to Congress; Focuses on Taxpayer Impact of Paper Processing Delays

- Tax Pros: Be Aware of EFIN Email Scam; Special Webinars Offered

- Proc 2024-13 Depreciation Limits for Tax Year 2024

- IRS Employer-Provided Childcare Tax Credit Page Helps Employers Determine Eligibility for up to $150,000 Business Tax Credit

- IRS Revises and Updates Frequently Asked Questions About Form 1099-K

- S. House Votes to Expand Child Tax Credit – Stalled in the Senate

- FinCEN Adds to its BOI Reporting FAQs

- Businesses Should Review Employee Retention Credit Rules and Resolve Incorrect Claims Soon

- Many Farmers and Fishers Face March 1 Tax Deadline

Issue 1: Required Minimum Distributions

Beneficiaries of retirement plan and IRA accounts are subject to required minimum distribution (RMD) rules. The SECURE Act changed how beneficiaries of inherited retirement plans took RMDs based on when the original plan owner died.

The IRS provides more in-depth information on retirement plan beneficiaries on IRS.gov. There were no changes to the RMD requirements for beneficiaries where the account owner died prior to 2020 or to beneficiaries that are not individuals.

Distributions to beneficiaries from qualified retirement plans

If the required minimum distribution is from a qualified retirement plan, such as a 401(k) or profit-sharing plan, the plan document establishes the distribution options available to satisfy the RMD rules. A spousal beneficiary will generally have more options available to them in the plan than a non-spouse beneficiary. Beneficiaries should contact the plan administrator to learn about their distribution options in a qualified plan.

Issue 2: IRS launches Simple Notice Initiative Redesign Effort

Shorter, clearer letters to reduce taxpayer confusion; about 170 million notices are sent to individual taxpayers annually.

The Internal Revenue Service has announced work is underway on the Simple Notice Initiative, a sweeping effort to simplify and clarify about 170 million letters sent annually to taxpayers.

Part of the larger transformation work taking place at the IRS with Inflation Reduction Act funding, the Simple Notice Initiative will build off redesigned notice efforts in place for the 2024 tax season and expand on a recent successful pilot involving identity theft letters.

The Simple Notice Initiative will review and redesign hundreds of notices with an immediate focus on the most common notices that individual taxpayers receive. The redesign work will accelerate during the 2025 and 2026 filing seasons, improving common IRS letters going out to individual taxpayers and then expanding into notices going to businesses.

The IRS sends about 170 million notices to individual taxpayers every year, covering a range of issues from claiming the credits and deductions for which they are eligible as well as meeting their tax obligations. These notices are often long and difficult for taxpayers to understand. And they do not always clearly and concisely communicate the next steps a taxpayer must take.

This initiative builds on the IRS Paperless Processing initiative announced in August 2023 to advance the goal of providing world-class customer service to taxpayers. With these initiatives, taxpayers have the option to go paperless and conveniently submit necessary responses online, and taxpayers will receive clearer and more concise notices from the IRS, so they better understand the actions they need to take.

Filing season 2024: IRS reviewed, redesigned 31 notices.

- The Simple Notice Initiative builds on the IRS’s continuous effort to improve notices. During the last year, the IRS reviewed and redesigned 31 notices in time for this year’s tax season. The IRS sent about 20 million of these notices in the calendar year 2022.

- These include notices to taxpayers who served in combat zones that may be eligible for tax deferment, notices that remind a taxpayer that they may have unfiled returns and notices that remind a taxpayer about their balance due and where they can go for assistance.

Filing season 2025: IRS will review, redesign most common notices sent to individual taxpayers.

- By filing season 2025, the IRS will review and redesign the most common notices that individual taxpayers receive. The IRS will focus on up to 200 notices that make up about 90% of total notice volume sent to individual taxpayers. This represents about 150 million notices sent to individual taxpayers in 2022.

- These include notices to propose adjustments to a taxpayer’s income, payments, credits, and/or deductions, notices to correct mistakes on a taxpayer’s tax return and notices to remind a taxpayer of taxes owed.

- The IRS will be actively engaging with taxpayers and the tax professional community to gather feedback on how these notices should be redesigned.

Filing season 2026 and beyond: IRS will review, redesign notices sent to businesses taxpayers as well as less common notices sent to individual taxpayers.

- The IRS sends over 40 million notices to business taxpayers every year. In future filing seasons, the IRS will review, and redesign notices sent to business taxpayers.

- The IRS will also review and redesign less common notices sent to individual taxpayers.

- Additional detail on the plan to redesign these notices will be shared in future updates.

responding over the phone. See below for an overview of improvements that were made.

The IRS sent the redesigned Notice 5071C to 60,000 taxpayers. Compared to taxpayers who received the original notice, there was a 16% reduction in taxpayers who called the IRS as their first action, and a 6% increase in taxpayers who used the online option. The IRS will apply lessons learned from this pilot, among others, to the new initiative. These changes to this notice will be put in place during the coming months.

Issue 3: A Message from IRS Commissioner Danny Werfel

As we begin the 2024 filing season, I just wanted to take a moment to especially thank everyone in the nation’s tax professional community. The work you do to help taxpayers is a vital part of our nation’s tax system, and your efforts make a difference, not just for your clients, but for the IRS and the entire nation.

Tax professionals are a critical link between the IRS and the taxpaying public. That’s especially true considering the majority of people use a tax professional to help them with their taxes. We appreciate the important role you play helping your clients fulfill their tax obligations, and in doing so you help ensure the integrity of our tax system.

At the IRS, we cannot say this enough. The work done by you, and other tax professionals like you, is absolutely essential to taxpayers and tax administration. You have challenging jobs, between managing clients, navigating business issues and dealing with the latest tax law changes. You perform a public service for the nation, and the employees of the IRS greatly appreciate your hard work and continued dedication.

Please know that at the IRS, as we work to transform the agency, we will continue our efforts to improve service to tax professionals with the goal of providing a much better experience when you interact with the agency, to make it easier for you to help your clients fulfill their tax obligations.

So, as I open my first tax filing season as IRS Commissioner, I want you to know I deeply appreciate all your efforts, and I wish you a smooth and successful tax season in all the work you do for taxpayers.

Issue 4: IRS Offering Additional Time at Taxpayer Assistance Centers for Face-to-Face Help

Helped by Inflation Reduction Act funding, nearly 250 IRS Taxpayer Assistance Centers nationwide will have extended operating hours Tuesdays and Thursdays during the tax filing season.

The extended office hours will continue through Tuesday, April 16. To see if a nearby TAC is offering extended hours, taxpayers can visit Contact your local office to access the IRS.gov TAC Locator tool. The site lists services offered, including extended hours and directions to each office. Taxpayers can call 844-545-5640 to make an appointment or walk in to get help at designated TACs offering additional time. Normally, TACs are open from 8:30 a.m. to 4:30 p.m., Monday through Friday, and operate by appointment.

The expanded hours at the assistance centers reflect funding and staffing made possible under the Inflation Reduction Act, which is being used across the IRS to improve taxpayer service, add new technology and tools as well as help tax compliance efforts.

During these additional office hours, TACs will offer all regular services, however for cash payments, taxpayers must have an appointment. If a taxpayer needs in-person identity verification services, they must bring two forms of identification, and one must be a current government-issued photo ID. They should also bring a copy or digital image of the tax return in question if one was filed. Tax return preparation is not a service provided at any IRS TAC.

Issue 5: TurboTax Advertising Found to be Deceptive.

The Federal Trade Commission (FTC) issued an opinion and final order finding that Intuit Inc., which owns TurboTax, engaged in deceptive advertising when it ran ads for “free” tax products and services for which some consumers were ineligible. The decision upholds an administrative law judge’s opinion that Intuit violated the FTC Act by engaging in deceptive advertising.

The FTC order prohibits Intuit from advertising or marketing any of its services as free unless they are free for all consumers, or the company clearly discloses the percentage of taxpayers qualifying for the free product or service. In cases where most customers don’t qualify for the free service, Intuit also has the option of disclosing that most consumers don’t qualify.

Issue 6: National Taxpayer Advocate Delivers Annual Report to Congress; Focuses on Taxpayer Impact of Paper Processing Delays

National Taxpayer Advocate Erin M. Collins has released her 2023 Annual Report to Congress, describing 2023 as a year of “extraordinary transition for the IRS and therefore for taxpayers.”

The report credits the Internal Revenue Service with substantially improving taxpayer services and developing plans to transform the taxpayer experience in the coming years, but it identifies paper processing as an area of continuing weakness.

By law, the Advocate’s report is required to identify the 10 most serious problems taxpayers are experiencing in their dealings with the IRS and to make administrative and legislative recommendations to address those problems. Before cataloging taxpayer challenges, however, Collins praised the IRS for taking notable strides forward.

“Overall, the magnitude of successes exceeded the areas of weakness in 2023, and most metrics showed significant improvement from the depths of the [COVID-19] pandemic,” Collins wrote in the report’s preface. The report says the IRS virtually eliminated its backlog of unprocessed original individual income tax returns (Forms 1040) and substantially improved telephone service.

Taxpayer service challenges

“When I released the National Taxpayer Advocate’s 2020 report, I wrote that the IRS in most cases ‘can effectively handle whatever it can automate,’ and when I released our 2021 report, I wrote that ‘paper is the IRS’s kryptonite,’” Collins said in releasing the new report. “Those observations continued to hold true in 2023. The areas in which taxpayers continued to experience delays were primarily those that required employees to process tax returns and taxpayer correspondence.”

Extraordinary delays in assisting victims of identity theft. At the end of fiscal year (FY) 2023, nearly half a million taxpayers with cases pending in the IRS’s Identity Theft Victims Assistance (IDTVA) unit were waiting an average of almost 19 months for the agency to resolve their identity theft problems. “If it weren’t for the significant number of challenges affecting larger groups of taxpayers, this would be headline news, and it should be,” Collins wrote. “Many taxpayers depend on their tax refunds to meet their living expenses, particularly low-income taxpayers who receive Earned Income Tax Credit (EITC) benefits that [approached] $7,000 for tax year 2022.” Noting that 69% of taxpayers whose identity theft cases the IDTVA unit resolved had adjusted gross incomes at or below 250% of the federal poverty level, Collins called the delays “unconscionable” and urged the IRS to place a higher priority on resolving cases quickly.

Delays in processing amended tax returns and taxpayer correspondence. Despite the IRS’s success in eliminating its backlog of paper-filed Forms 1040, backlogs in processing amended individual income tax returns (Forms 1040-X), amended business tax returns and correspondence continued. At the end of calendar year 2019 (the most recent pre-pandemic year), the IRS’s backlog of unprocessed amended returns stood at 0.5 million. By comparison, the backlog as of late October 2023 was 1.9 million – nearly four times as much. Taxpayer correspondence and related cases more than doubled over the same period, from 1.9 million to 4.3 million. In addition, the percentage of correspondence cases classified as “overage” in 2023 reached its highest level in recent years, with nearly 70% of pending cases exceeding normal processing times as of late October. Delays in processing amended returns and correspondence harm taxpayers because processing delays cause delays in issuing refunds.

The report attributes much of the paper inventory backlog to the Treasury Department’s decision to prioritize answering telephone calls over processing amended returns and correspondence. Both tasks are performed by IRS customer service representatives (CSRs) in the agency’s Accounts Management (AM) function. For the 2023 filing season, Treasury set a goal of achieving an 85% “Level of Service” (LOS) on the IRS’s toll-free telephone lines, and that required staffing the telephone lines at levels capable of handling most calls during peak periods. However, the report says that meant CSRs often were “simply sitting around waiting for the phone to ring.” During the 2023 filing season alone, CSRs spent 1.27 million hours (34% of their time) waiting to receive calls. That translates to more than 650 unproductive staff years in which these employees could have been processing paper and reducing response times for amended returns and correspondence.

“The IRS cannot easily shuffle employees back and forth between answering phones and processing correspondence, so unproductive employee time was the price it had to pay to improve telephone service levels,” Collins wrote. “Going forward, the IRS needs to find a way to move employees between those two functions more nimbly. For present purposes, however, we need to keep in mind that backlogs in processing tax returns and taxpayer correspondence drive much of the phone volume. I encourage the IRS to put more emphasis on reducing its paper processing backlog in 2024.”

Challenges in receiving telephone assistance despite overall improvements. The report says the IRS deserves credit for achieving its goal of providing an 85% Level of Service on its AM telephone lines during the filing season, but it points out that the LOS is a highly technical measure that excludes the majority of calls the IRS receives from its calculation. During the same period that the IRS achieved an LOS of 85%, IRS employees answered only 35% of all calls received. For the full fiscal year, IRS employees answered 29% of all calls received.

The IRS maintains dozens of distinct telephone lines, and averages can mask significant variations among key lines. The report says service for tax professionals was below average, with a reported LOS of 34% in FY 2023 and an average wait time of 16 minutes before reaching a CSR. “Roughly 500,000 tax professionals prepare tax returns for more than 85 million taxpayers, so the IRS derives considerable benefit from working collaboratively with the pool of tax professionals,” the report says. “Requiring tax professionals to call back repeatedly and wait on hold not only inconveniences them but often results in additional costs to taxpayers for the time their tax professionals bill for waiting on hold.” The report recommends the IRS prioritize improving service on the practitioner telephone line. It also recommends the IRS develop better performance measures so it not only measures access to a CSR but also measures call quality (e.g., the percentage of taxpayer issues resolved with a single telephone call).

Employee Retention Credit (ERC) processing. Employers who file eligible ERC claims are often waiting six months or longer to receive their credits or refunds. TAS has received several thousand ERC cases, and some have involved non-profit organizations that provide medical or other critical services and are depending on ERC refunds to stay afloat. As of early December, the IRS had a backlog of approximately one million ERC claims. The IRS has said many of the submitted claims are fraudulent or otherwise non-qualifying.

The report acknowledges the IRS is between a rock and a hard place in handling ERC claims. “If it pays claims quickly without adequate review, it could pay billions of dollars to nonqualifying persons. If it takes the time to review claims carefully, eligible employers will experience significant delays in receiving the credit, and in extreme cases, employers who need the funds immediately could go out of business,” the report says.

Administrative recommendations

At the end of each of the ten “most serious problem” sections in the report, the Advocate makes administrative recommendations to address the problems. Among her key recommendations:

- Prioritize the improvement of online accounts for individual taxpayers, business taxpayers and tax professionals to provide functionality comparable to that of private financial institutions. Of all the steps the IRS can take to improve the taxpayer experience, Collins says that creating robust online accounts has the potential to be the most transformative and should receive the highest priority. However, the report states, online accounts must be significantly improved so more taxpayers will see the benefits of using them, and the IRS must do a much better job of promoting them. During 2023, individual taxpayers filed more than 160 million income tax returns, yet only 16.8 million users accessed individual online accounts. That’s just over 10%.

“To better serve these taxpayers and persuade the other 90% of taxpayers to consider creating and using online accounts, the IRS should aim to provide online accounts through which taxpayers and tax professionals, among other things, can see full information about their accounts, receive and respond to IRS notices, and elect to receive payment reminders,” the report says. “That will enable taxpayers and tax professionals to keep fully informed about federal tax matters and to interact more smoothly with the agency, and it will substantially reduce the volume of telephone calls and mail the IRS receives.”

- Improve the IRS’s ability to attract, hire and retain qualified employees. The report says the IRS continues to struggle to hire qualified candidates in many key areas. It says three of the main reasons are failure to advertise positions to the optimal target audience by job series, the slow pace of the hiring process and non-competitive pay. The report recommends the IRS devote more effort to identifying and conducting outreach to target audiences by job series, work to continue to shorten the clearance and onboarding process for selected applicants, and work with the Office of Personnel Management and Congress to obtain more pay flexibility for hard-to-fill positions.

- Ensure all IRS employees – particularly customer-facing employees – are well-trained. The report says the IRS has historically faced challenges providing adequate training to customer-facing employees, partly due to the complexity of the tax system and lack of funding. However, those challenges are greater when the agency is staffing up, as it is currently doing. Results from the recently concluded 2023 Federal Employee Viewpoint Survey show nearly a quarter of IRS employees provided a negative response to the statement, “I receive the training I need to do my job well.” The report says: “It is critical that the IRS make comprehensive training a priority and ensure that new hires receive adequate training before they are assigned to tasks with taxpayer impact.”

- Upgrade the back end of the “Document Upload Tool” (DUT) to fully automate the processing of taxpayer correspondence. The IRS has created and implemented the DUT to allow taxpayers to upload documents electronically in response to an IRS notice, letter, telephone conversation or visit. The report says that is “great news” for taxpayers. Once the documents reach the IRS, however, they are still processed as if they came in on paper. All documents go to a central location and then must be parceled out to the appropriate function for processing and response. As part of its Paperless Processing Initiative, the IRS said that “half of paper-submitted correspondence, non-tax forms, and notice responses will be processed digitally” by the 2025 filing season. Digital processing will shorten response times and enable the IRS to reassign employees to other high priority areas. The report recommends the IRS continue its efforts to digitize the processing of more taxpayer submissions and create back-end processes for DUT submissions.

- Enable all taxpayers to e-file their federal tax returns. While the significant majority of taxpayers e-file their tax returns, the IRS still received more than 11 million individual returns and 15 million business returns on paper last year. The processing of paper returns causes delays in delivering refunds and increases administrative costs for the IRS. Some taxpayers may prefer to file on paper, and the report says the IRS should continue to improve the filing experience for paper filers. But many taxpayers who would prefer to e-file their returns cannot do so for a variety of reasons. For example, about 150 to 200 IRS forms still are not eligible for e-filing. The report describes the main barriers to e-filing and recommends steps the IRS can take to remove them.

- Extend eligibility for first-time penalty abatement to all international information return penalties. U.S. persons who receive gifts or inheritances from foreign persons or who own interests in certain foreign partnerships and corporations and engage in cross-border business activities are potentially subject to a wide range of U.S. reporting requirements. The report says many of these reporting requirements are obscure and complex, and they sometimes apply to lower-income taxpayers and immigrants who may not be aware of them. Yet taxpayers who do not comply with applicable reporting requirements are subject to penalties that “are automatically assessed, broadly applied, needlessly harsh, and often unexpected,” the report says. These penalties apply if a filing is late, incomplete or inaccurate. “Rather than promoting tax compliance through taxpayer education and support,” Collins wrote, “the IRS has opted to flex its administrative muscle and bring down the enforcement hammer on good-faith taxpayers and bad actors alike.” The report recommends that the IRS offer first-time penalty abatement in these cases in appropriate circumstances.

Legislative recommendations: The “Purple Book”

The National Taxpayer Advocate’s 2024 Purple Book proposes 66 legislative recommendations intended to strengthen taxpayer rights and improve tax administration. Among the recommendations:

- Require the IRS to timely process claims for credit or refund. Millions of taxpayers file claims for credit or refund with the IRS each year, yet under current law, there is no requirement that the IRS pay or deny them. It may simply ignore them. The taxpayers’ remedy is to file a refund suit in a U.S. district court or the U.S. Court of Federal Claims. For many taxpayers, that is not a realistic or affordable option, as full payment of the disputed amount is generally required, and there can be sizeable litigation fees. “The absence of a processing requirement is a poster child for non-responsive government,” the report says. While the IRS generally does process claims for credit or refund, the claims can, and sometimes do, spend months and even years in administrative limbo within the IRS. TAS recommends Congress require the IRS to act on claims for credit or refund in a timely manner and impose certain consequences for failing to do so.

- Authorize the IRS to establish minimum standards for paid tax return preparers and revoke the identification numbers of sanctioned preparers. The IRS receives over 160 million individual income tax returns each year, and most are prepared by paid tax return preparers. While some tax return preparers must meet licensing requirements (e.g., certified public accountants, attorneys and enrolled agents), most preparers are not credentialed. Numerous studies have found that non-credentialed preparers disproportionately prepare inaccurate returns, causing some taxpayers to overpay their taxes and others to underpay, which may lead to penalties and interest charges. In FY 2022, the IRS estimated the improper payments rate attributable to improper EITC claims was 32%, amounting to $18.2 billion. Among tax returns claiming the EITC prepared by paid tax return preparers, 94% of the total dollar amount of EITC audit adjustments was attributable to returns prepared by non-credentialed preparers.

The report says federal and state laws generally require lawyers, doctors, securities dealers, financial planners, actuaries, appraisers, contractors, motor vehicle operators and even barbers and beauticians to obtain licenses or certifications and, in most cases, to pass competency tests. Both to protect taxpayers and the public fisc, TAS recommends Congress authorize the IRS to establish minimum competency standards for tax return preparers and to revoke the Preparer Tax Identification Numbers of preparers who have been sanctioned for improper conduct.

- Expand the U.S. Tax Court’s jurisdiction to adjudicate refund cases. Under current law, taxpayers who owe tax and wish to litigate a dispute with the IRS without paying the tax first can go to the U.S. Tax Court, while taxpayers who have paid their tax liability and are seeking a refund must sue in a U.S. district court or the U.S. Court of Federal Claims. Although this dichotomy between deficiency cases and refund cases has existed for decades, TAS recommends Congress give taxpayers the option to litigate both deficiency and refund disputes in the U.S. Tax Court. Due to the tax expertise of its judges, the Tax Court is often better equipped to consider tax controversies than other courts. It is also more accessible than other courts to unsophisticated and unrepresented taxpayers because it uses informal procedures, particularly in disputes that do not exceed $50,000 per tax year or period.

- Extend the “reasonable cause” defense for the failure-to-file penalty to taxpayers who rely on return preparers to e-file their returns. A taxpayer who files a tax return after the filing deadline is subject to a penalty of up to 25% of the tax due unless the taxpayer can show the failure was due to “reasonable cause.” Most taxpayers hire tax professionals to prepare their returns, and tax professionals sometimes fail to meet filing deadlines without notifying the taxpayer. In 1985, when all returns were filed on paper, the Supreme Court held that a taxpayer’s reliance on a preparer to file a tax return did not constitute “reasonable cause” to excuse the failure-to-file penalty. In 2023, a U.S. Court of Appeals extended that holding to e-filed returns.

For several reasons, it is often much more difficult for taxpayers to verify that a return preparer has e-filed a return than to verify that a return has been paper-filed. “Penalizing taxpayers who engage preparers and do their best to comply with their tax obligations is grossly unfair and undermines the congressional policy that the IRS encourage e-filing,” the report says. “Under the recent Court of Appeals’ ruling, astute taxpayers would be well advised to ask their preparers to give them paper copies of their prepared returns and then transmit the returns by certified or registered mail themselves so they can prove compliance.” TAS recommends Congress clarify that reliance on a preparer to e-file a tax return may constitute “reasonable cause” for penalty relief and require the Treasury Department to issue regulations detailing what constitutes ordinary business care and prudence to evaluate reasonable cause requests.

- Enable the Low-Income Taxpayer Clinic (LITC) program to assist more taxpayers in controversies with the IRS. The LITC program effectively assists low-income taxpayers and taxpayers who speak English as a second language. When the LITC grant program was established in 1998, the law limited annual grants to a maximum of $100,000 per clinic. The law also imposed a 100% “match” requirement (meaning a clinic cannot receive more in LITC grant funds than it is able to obtain from other sources). The nature and scope of the LITC program has evolved considerably since 1998, and those requirements are limiting the number of taxpayers the program is able to assist. While the Consolidated Appropriations Act, 2023, raised the per-clinic cap to $200,000 for one year and that provision may be carried forward into 2024, TAS recommends that Congress remove or substantially increase the per-clinic cap permanently and allow the IRS to reduce the match requirement to 25% where doing so would expand coverage to additional taxpayers.

Research studies

On or about January 31, TAS will publish two research studies and detail the design of a third study at www.TaxpayerAdvocate.irs.gov.

Two-year bans on eligibility for refundable tax credits are often imposed without following required procedures. The tax code authorizes the IRS to ban a taxpayer from claiming the EITC, the Child Tax Credit, and the American Opportunity Tax Credit for two years if it determines the taxpayer claimed the credit recklessly or with intentional disregard of rules and regulations. It is a harsh sanction because it means a taxpayer cannot receive credits in the two years after an improper claim even if the taxpayer otherwise qualifies for the credits in those years. TAS found that the IRS often did not follow its own procedures in imposing the ban. Employees failed to secure managerial approval in 76% of cases where managerial approval was required, and it failed to provide an adequate explanation to the taxpayer regarding why the ban was imposed 81% of the time.

A review of online accounts offered by state and foreign tax agencies can help the IRS improve its own online accounts. Last year, TAS published a study that examined online accounts offered to individual taxpayers by state tax agencies and foreign tax agencies. For the new study, TAS surveyed state and foreign tax agency websites for information on accounts offered to businesses and tax professionals. The new study will also supplement last year’s survey on online accounts for individuals by reporting the results of interviews TAS conducted with individuals about their opinions of IRS online accounts and the identity authentication steps that should be required to protect the confidentiality of their accounts without imposing excessive burden.

IRS procedures for withholding tax refunds in suspected identity theft cases may be harming legitimate taxpayers. Each year, the IRS freezes several million refunds claimed on tax returns flagged by IRS filters for possible identity theft. However, the filters have false positive rates that generally exceed 50% overall. When the IRS flags a return, it sends a single letter to the taxpayer explaining why it has stopped the refund and informing the taxpayer that he or she must authenticate their identity before the IRS will release the refund. In most years, more than half of the taxpayers receiving this letter do authenticate their identities and receive their refunds, but if no response is received from a taxpayer, the IRS takes no further action. Given the risk of undelivered mail and the relatively low rate of response to IRS letters, TAS is concerned that some taxpayers are not receiving refunds for which they are eligible. TAS has mailed outreach letters to a significant number of taxpayers who did not receive a tax year 2020 refund because they did not respond to an IRS letter. TAS is offering to help these taxpayers complete the identity verification process. TAS plans to report on the results of this study later in 2024.

Issue 7: Tax Pros: Be Aware of EFIN Email Scam

Be on the lookout for scam emails that impersonate various software companies in an attempt to steal Electronic Filing Identification Numbers (EFINs). The IRS and its Security Summit partners warn that scammers are posing as tax software companies and requesting EFIN documents from tax professionals under the guise of a required verification to transmit tax returns.

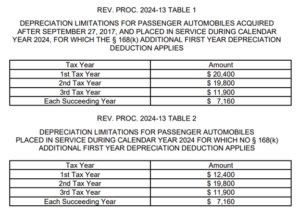

Issue 8: Rev. Proc 2024-13 Depreciation Limits for Tax Year 2024

This revenue procedure provides:

(1) two tables of limitations on depreciation deductions for owners of passenger automobiles placed in service by the taxpayer during calendar year 2024; and

(2) a table of dollar amounts that must be used to determine income inclusions by lessees of passenger automobiles with a lease term beginning in calendar year 2024. These tables reflect the automobile price inflation adjustments required by § 280F(d)(7) of the Internal Revenue Code. For purposes of this revenue procedure, the term “passenger automobiles” includes trucks and vans.

Inclusions in Income of Lessees for Passenger Automobiles. A taxpayer must follow the procedures in § 1.280F-7(a) for determining the inclusion amounts for passenger automobiles with a lease term beginning in calendar year 2024. In applying these procedures, lessees of passenger automobiles should use Table 3 of this revenue procedure.

Issue 9: IRS Employer-Provided Childcare Tax Credit Page Helps Employers Determine Eligibility for up to $150,000 Business Tax Credit

The Internal Revenue Service has launched a new page on IRS.gov explaining the Employer-Provided Childcare Tax Credit, an incentive for businesses to provide child care services to their employees.

This tax credit is designed to help employers cover some of the qualified childcare facility and resource and referral expenditures associated with providing child care services to their employees. A qualified childcare facility is one that meets the requirements of all applicable laws and regulations of the state or local government in which it is located.

The credit is limited to $150,000 per year to offset 25% of qualified childcare facility expenditures and 10% of qualified child care resource and referral expenditures.

Employers should complete Form 8882, Credit for Employer-Provided Child Care Facilities and Services, to claim the credit for qualified child care facility and resource and referral expenditures. The credit is part of the general business credit subject to the carryback and carryforward rule. This means employers may carry back unused credit one year and then carryforward 20 years after the year of the credit. Taxpayers whose only source for the credit is from pass-through entities can report the credit directly on Form 3800, General Business Credit.

Issue 10: IRS Revises and Updates Frequently Asked Questions About Form 1099-K

In an effort to provide more resources for taxpayers during this filing season, the Internal Revenue Service has revised frequently asked questions (FAQs) for Form 1099-K, Payment Card and Third Party Network Transactions in Fact Sheet FS-2024-03.

The revised FAQs provide more general information for taxpayers, including common situations, along with more clarity for industry and what organizations should send Forms 1099-K. The FAQs are in addition to a recently updated Understanding your Form 1099-K on IRS.gov page and other communications resources.

Following feedback from taxpayers, tax professionals and payment processors, and to reduce taxpayer confusion, the IRS announced on Nov. 21, 2023, Notice 2023-74 to delay the new $600 Form 1099-K reporting threshold for third party settlement organizations for calendar year 2023.

As the IRS continues to work to implement the new law, the agency is treating 2023 as an additional transition year, which applies to taxes filed this year. As a result, reporting will not be required unless the taxpayer receives over $20,000 and has more than 200 transactions in 2023, although taxpayers may still receive a form for amounts less than the required reporting amount.

The updates to the FAQs contain substantial changes within each section:

- General Information

- What to Do If You Receive a Form 1099-K

- Common Situations

- Third Party Filers of Form 1099-K

- Should My Organization Be Preparing, Filing and Furnishing Form 1099-K?

More information about taxpayer reliance on guidance published in the Internal Revenue Bulletin and FAQs is available.

Issue 11: U.S. House Votes to Expand Child Tax Credit – Not Law Yet

The U.S. House of Representatives passed a bipartisan $78 billion tax package Jan. 31 that includes a temporary three-year expansion of the child tax credit and the restoration of several business tax breaks that were reduced under the Tax Cuts and Jobs Act. H.R. 7024, Tax Relief for American Families and Workers Act of 2024, now goes to the U.S. Senate where it faces an uncertain future.

While the package had strong support from both Republicans and Democrats in the House, some Senators have expressed strong opposition to the legislation. Many of the provisions are retroactive. We are monitoring and if passed by the Senate we will include in another newsletter.

Issue 12: FinCEN Adds to its BOI Reporting FAQs

The Financial Crimes Enforcement Network (FinCEN) added or updated 18 questions regarding the reporting of beneficial ownership information (BOI) on its frequently asked questions (FAQs) webpage. The questions that have been added or updated since Jan. 1 include:

- Under the Corporate Transparency Act (CTA), who can access beneficial ownership information?

- The company applicants of a reporting company include the individual “primarily responsible for directing the filing of the creation or registration document.” What makes an individual “primarily responsible” for directing such a filing?

- If a beneficial owner or company applicant’s acceptable identification document does not include a photograph for religious reasons, will FinCEN accept the identification document without the photograph?

- What residential address should be reported if a reporting company is required to report an individual’s residential address, but that individual does not have a permanent residence?

- What should a reporting company report if its ownership is in dispute?

- Who does a reporting company report as a beneficial owner if a corporate entity owns or controls 25% or more of the ownership interests of the reporting company?

- Can a company created or registered in a U.S. territory be considered a reporting company?

New companies created or registered in 2024 have 90 days from receiving notice of the entity’s creation or registration to file a BOI report with FinCEN. Companies created or registered before 2024 must file BOI reports by Jan. 1, 2025.

Issue 13: Businesses Should Review Employee Retention Credit Rules and Resolve Incorrect Claims Soon

The IRS urges businesses to review their eligibility for the Employee Retention Credit because there’s limited time for them to voluntarily resolve incorrect claims and avoid future issues, such as penalties and interest.

Some honest businesses were misled into filing claims for the Employee Retention Credit by promoters who often misrepresented or oversimplified eligibility rules. Businesses that received the credit but don’t meet the ERC rules should consider applying for the ERC Voluntary Disclosure Program before the March 22 deadline. The IRS also offers a withdrawal program for those whose claims haven’t yet been paid.

The ERC, sometimes called ERTC, is a refundable tax credit for certain eligible businesses and tax-exempt organizations that had employees and were affected during the COVID-19 pandemic. The requirements vary depending on the time of claim, and it is not available to individuals.

ERC Voluntary Disclosure Program open until March 22, 2024

Businesses that filed a claim in error and received a payment may be able to apply to the IRS Voluntary Disclosure Program. The special program runs through March 22, 2024, and lets taxpayers repay just 80% of the claim received.

Withdrawal program still available for pending ERC claims

The IRS continues to accept and process requests to withdraw a full ERC claim. Employers that claimed an ERC that hasn’t been paid can withdraw their claim so they don’t get a refund for which they’re ineligible and can avoid penalties and interest. They can also withdraw their claim if they’ve received a check but haven’t deposited or cashed it.

ERC information for businesses with questions

IRS offers resources online to answer questions and help employers check whether they’re eligible for the credit. They can review the ERC frequently asked questions and the ERC Eligibility Checklist, which is available as an interactive tool or as a printable guide. The IRS also has free recorded webinars for the withdrawal process and the VDP.

Moratorium status

Following concerns from tax professionals and others about aggressive ERC marketing, the IRS announced on Sept. 14 a moratorium on processing new ERC claims. In the coming months, the IRS plans to continue steps on fraud protection measures, which are necessary before the IRS anticipates resuming processing of claims submitted after the Sept. 14 moratorium. A date hasn’t been determined.

The IRS continues to process ERC claims submitted before the moratorium, but with higher scrutiny and at a much slower rate.

Issue 14: Many Farmers and Fishers Face March 1 Tax Deadline

The Internal Revenue Service today reminds farmers and fishers who chose to forgo making estimated tax payments by January that they must generally file their 2023 federal income tax return and pay all taxes due by Friday, March 1, 2024.

The special March 1, 2024, deadline allows farmers and fishers to avoid any estimated tax penalties. Though several tax-payment options are available, a taxpayer can use a quick, easy and free option to pay from their bank account by using their Online Account or schedule payments in advance using IRS Direct Pay.

The special March 1, 2024, deadline applies to anyone who qualifies as a farmer or fisher and did not make an estimated tax payment by Jan. 16, 2024. Those who made a qualifying payment by Jan. 16, 2024, can wait until the regular April 15, 2024, deadline to file and still avoid estimated tax penalties. See Publication 505, Tax Withholding and Estimated Tax, for details. The deadline is April 17, 2024, in Maine and Massachusetts.

For this purpose, a farmer or fisher is anyone who received at least two-thirds of their gross income from farming or fishing during either 2022 or 2023.

Special rules for disaster areas

Disaster-area taxpayers, including farmers and fishers, have more time to file and pay. Currently, individuals and businesses in parts of Connecticut, Maine, Michigan, Rhode Island, Tennessee and West Virginia, have until June 17, 2024, to file their 2023 return and pay any tax due. This extension is automatic; taxpayers don’t need to file any paperwork or call the IRS to get it.

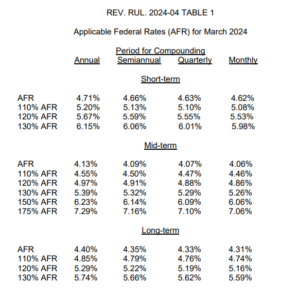

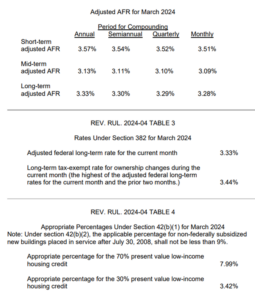

Issue 15: Applicable Federal Rates for March 2024, Rev. Rul. 2024-04

REV. RUL. 2024-04 TABLE 2

REV. RUL. 2024-04 TABLE 5

Rate Under Section 7520 for March 2024

Applicable federal rate for determining the present value of an annuity, an interest for life or a term of years, or a remainder or reversionary interest 5.00%