As the world comes to grips with the COVID-19 crisis, we as tax professionals are trying to learn the new law and determine how we can assist our clients if they qualify for any of the new credits, or the provisions of carryback of NOLs, etc.

Over the next 4 weeks Basics and Beyond will provide a series of 4 webinars to address key issues, especially those that have time constraints.

Tax Webinar Descriptions

COVID-19 Tax Law Implications Part 3 Retirement Update 2020: Both the Secure Act and the CARES Act made significant changes to Retirement and Planning for Retirement. Webinar topics will include: Repeals the maximum age for traditional IRA contributions, which is currently 70½. Increases the required minimum distribution (RMD) age for retirement accounts to 72 (up from 70½). Allows long-term, part-time workers to participate in 401(k) plans. Permits parents to withdraw up to $5,000 from retirement accounts penalty-free within a year of birth or adoption for qualified expenses. Allows parents to withdraw up to $10,000 from 529 plans to repay student loans. Small-business owners can receive a tax credit for starting a retirement plan, up to $5,000. The Act mandates that most non-spouses inheriting IRAs take distributions that end up emptying the account in 10 years. Waiver of 10% Early Withdrawal Penalty for Distributions of Up to $100,000 From Retirement Funds for Affected Individuals. Loan Rule Changes. Required Minimum Distribution Waiver. CPE Credit: 1

COVID-19 Tax Law Implications Part 4 Individual Update 2020: Individual Provisions of the CARES Act Webinar topics will include: Newly released Information on issues that impact Individuals, Updates on the Stimulus – On-Line IRS Programs to Provide Bank Information, Above the Line Charitable Deductions – 2020 Tax Form Change, Food Inventory Donation, Student Loan Payments, Secure Act Issues: Increase the age at which minimum distributions must begin to 72, Expansion of Section 529 education savings plans, Kiddie tax changes, Taxable non-tuition fellowship and stipend payments are, Tax-exempt difficulty-of-care payments are treated as compensation. Additional material on Form Changes as Released. us for a follow up session. CPE Credit: 1

COVID-19 Tax Law Implications Part 5 Business Update 2020: Our Business update will cover Recent Guidance on the CARES Act concerning: Business Charitable Contributions, Net operating Losses, Excess Business Losses, Qualified Improvement property, Corp 100% AMT Credit, Business Interest Easing, Recent guidance and FAQ that will help to understand issues. CPE Credit: 1

COVID-19 Tax Law Implications Part 6 IRS Updates 2020: Expanded due dates – a review – are you aware of all the new due dates and expanded guidance?, Where are we with estimates?, Installment Agreements, Enforcement Issues, IRS New Online Programs, State Extended Dates, Delay of Payments, Unemployment Issues, Get Up -to- Date on new guidance issued. CPE Credit: 1

Quarterly Tax Update: 3 Sessions (May, August & November): Join us as we explore significant tax announcement, procedure changes and other updates that have occurred since January 2020. This update will bring you current of Rev. Rul. and Procedures, Notices and additional guidance and other information needed to make sure you are at the top of your game with guidance and changes. This “fill in the Gaps” webinar is a must for your practice. CPE Credit/CE Hour: 1

Late Breaking News

Projections for the 2021 Social Security Wages Base were released in the Social Security Administration 2020 Annual Report.

The Final amount is generally released sometime in October or November Projections are as Follows:

Projections for 2021 and onward. The SSA provides three kinds of forecasts for the Social Security wage base (intermediate, low cost, and high cost). The intermediate and the high cost forecast predicts an increase from $137,700 in 2020 to $141,900 in 2021. The low cost forecast predicts the Social Security wage base will increase to $142,200 in 2021.

The SSA intermediate forecasts through 2029 are as follows:

- 2021 — $141,900

- 2022 — $147,000

- 2023 — $153,600

- 2024 — $159,900

- 2025 — $165,900

- 2026 — $172,200

- 2027 — $178,800

- 2028 — $185,700

- 2029 — $192,900

- The OCA is projecting that the Social Security trust fund will become insolvent in 2035.

- The OCA is projecting that the Disability Insurance (DI) trust fund will become insolvent in 2065.

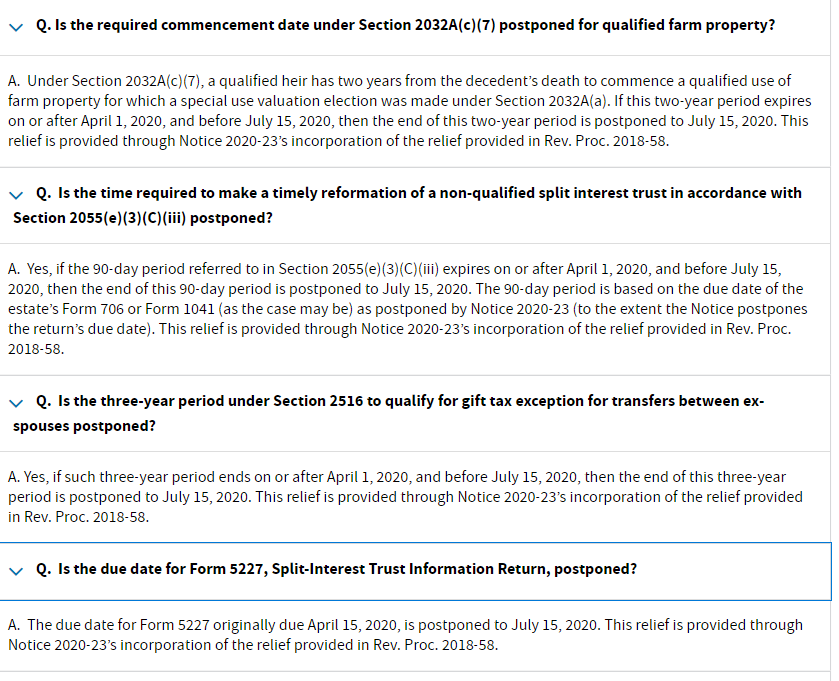

COVID Relief for Estate and Gift Tax

May 2020 Issues

In This Issue

- Answers to Your Questions from the April 23, 2020 Webinar on the Employee Retention Credit – Based on Current Information

- IRS Announced Waivers of Offers for Compromise Applications

- State COVID-19 Updates

- TIGTA Unveils New Flyer Warning Taxpayers About Impersonation Scam

- Correction to 2018 and 2019 Worksheet 3, Figuring Net Self-Employment Income for Schedule SE

- Redesigned Withholding Compliance Lock-In Letters 2800C and 2808C Coming Soon

- Supreme Court will Hear ACA Case in the October Term

- I-9, Employment Eligibility Verification – New Revision Expires 10/31/2022

- Delivery of the Stimulus Payment

- More Answers to the Stimulus Payment Questions

- IRS has Provided Applicable Federal Rate Tables for May 2020 – Rev Rul 2020-11

Issue 1: Answers to Your Questions from the April 23, 2020 Webinar on the Employee Retention Credit – Based on Current Information

- I have read in another source, that you have a choice between the PPP loan, Employee Retention Credit or Delay of payment of payroll taxes, when you choose one, then the other two options are unavailable. Is this true? – If you receive the PPP, you are NOT entitled to Delay of Payment of payroll taxes, this is true. For example, the credits that are available under FFCRS for sick pay and medical family leave Acts only apply to wages from April 1, 2020 through 12/31/2020. If you apply these credits you can’t utilized the employee retention credit. However, any “qualifying wages” prior to 4/1/2020, then you may qualify for the employee retention credit.

- Employers are not required to pay sick pay or FMLA due to COVID 19? – It depends, if the employer closed the worksite before April 1, 2020 (the effective date of the FFCRA), can an employee still get paid sick leave or expanded family and medical leave? – No. If, prior to the FFCRA’s effective date, the employer sent the employee home and stops paying them because it does not have work for the employee to do, the employee will not get paid sick leave or expanded family and medical leave but they may be eligible for unemployment insurance benefits. This is true whether the employer closes the worksite for lack of business or because it is required to close pursuant to a Federal, State, or local directive. There are many variations concerning the prior to April 1 when the law became effective. You should access the DOL Frequently asked questions to review. The Emergency Paid Sick Leave Act imposes a new leave requirement on employers that is effective beginning on April 1, 2020. – Remember there is a Small Business Exemption for employers with fewer than 50 employees. — To elect this small business exemption, the employer should document why the business with fewer than 50 employees meets the criteria set forth by the Department, which will be addressed in more detail in forthcoming regulations. The employer should not send any materials to the Department of Labor when seeking a small business exemption for paid sick leave and expanded family and medical leave.

- There are people here trying to sign up kids that are 17 and older to get their own stimulus ck that shouldn’t because they are claimed on their parents…will something happen to those people? – We will have to wait for guidance, but IRS does have the capability to “filtering” for a variety of issues.

- If you still paid people thru this entire time frame, do you have to prove that you were affected by covid19 to take this credit? I am trying to do 941’s for first quarter, so can they get a credit for 3.13-3.31 wages? – The credit is applied on 2nd quarter 941. Yes, you have to prove that you were affected by either gross receipts down 50% from previous year for same period or were required to fully or partially shut down per federal or state law

- If someone is paid at the end of every month, like at end of March, does that payroll count? Because my client’s income was more than 50% down? The credit is applied on 2nd quarter Applies from March 13 – March 31 not the whole month, we don’t have guidance on this specific issue, but common sense would say you would need to prorate.

- How long will it take to process the 1040 paper returns? What we do know is that paper processing is suspended. Until IRS makes a decision that it is safe for employees to return to work, paper returns will set un-processed, we are all in a wait and see mode.

- So, if you filed a 7200 wrong, and there are no 7200x, do we file it again to correct it? The guidance we currently have is if an error was made on the Form 7200 the correction will be made when the quarterly Form 941 is filed. Employers that file Form(s) 941, 943, 944, or CT-1 may file Form 7200 to request an advance payment of the tax credit for qualified sick and family leave wages and the employee retention credit. You will need to reconcile any advance credit payments and reduced deposits on your employment tax return(s) that you will file for 2020. No employer is required to file Form 7200. Instead of filing Form 7200, you should first reduce your employment tax deposits to account for the credits. You can request the amount of the credit that exceeds your reduced deposits by filing Form 7200 or waiting to get a refund when you claim the credits on your employment tax return.

- My understanding from another source was that the company could defer the employer SS up to the date that the PPP is forgiven, then it must pay. – I wish we had more guidance on how the PPP and Employer Retention Credit interact. What we do know that you have to use up the PPP loan for 8 weeks of employee wages. During that time the Employer Retention Credit does not apply.

- Is a full-time employee 40 hours/week? Over 30 hours/week? – FTE is defined as 30 hours a week or 130 hours a month under other regulations, however, we will need additional information on this. Even the PPP FTE has not been truly defined.

- Why does the Form 7200 have a slightly different fax number? The Form 7200 will be processed in a special unit. The fax number is 855-248-0552.

- Can you qualify based on the 50% test even if not fully or partially closed? So still open, but meets the under 50% receipts rule? – The employer must meet the following criteria: Eligible Employers for the purposes of the Employee Retention Credit are those that carry on a trade or business during calendar year 2020, including a tax-exempt organization, that either:

- Fully or partially suspends operation during any calendar quarter in 2020 due to orders from an appropriate governmental authority limiting commerce, travel, or group meetings (for commercial, social, religious, or other purposes) due to COVID-19; or

- Experiences a significant decline in gross receipts during the calendar quarter.

Note: Governmental employers are not Eligible Employers for the Employee Retention Credit. Also, Self-employed individuals are not eligible for this credit for their self-employment services or earnings.

12.Under the Family Care Act for COVID related illness I believe there is an 80-hour limit on the Social Security employer exemption. If you have someone who takes sick to care for a spouse with COVID and then get COVID themselves, are they limited to 80 hours of the paid sick under the act or up to 80 for the care of spouse and up to 80 for being sick themselves? – The law states: An employee who is unable to work due to caring for someone with coronavirus, or caring for a child because the child’s school or place of care is closed, or the paid child care provider is unavailable due to the coronavirus, is entitled to paid sick leave for up to two weeks (up to 80 hours) at two-thirds the employee’s regular rate of pay or, if higher, the Federal minimum wage or any applicable State or local minimum wage, up to $200 per day, but no more than $2,000 in total. – the Sick Leave Provision

After the 80 hours the employee would fall under the Family Leave up to an additional 10 weeks An employee who is unable to work (including telework) because of coronavirus quarantine or self-quarantine or has coronavirus symptoms and is seeking a medical diagnosis, is entitled to paid sick leave for up to ten days at the employee’s regular rate of pay, or, if higher, the Federal minimum wage or any applicable State or local minimum wage, up to $511 per day, but no more than $5,110 in total.

13. Can employer short pay (Employer SS) for March 20 deposit? NO, I have to assume that this is for wages prior to March 13. We would need more information to address the question.

14. Could this credit be used for the wages in excess of the 100k PPP limit? – There is no mention on a wages cap for the Employer Retention Credit. You would not qualify for the Employer Retention Credit during the 8 weeks that the PPP Loan is effective, that is very clear in the guidance. I should also mention that the PPP Loan guidance has been sparse. The PPP Loan has been accepted and no Employer Retention Credit would apply for the period of the PPP Loan.

15. If the new form is not available, and the employer already filed the Q1 941, do they have to amend or is the credit lost for the late March payroll? – As mentioned above, the Employer Retention Credit must meet the requirements and the credit for March 13- March 31 would be claimed on the second quarter, not the first quarter. We await the revised Form 941.

16. What happens to a new business that just opened in January 2020? – I thought I read something on this issue, but have been unable to locate. I will watch the FAQ’s for information on this issue.

17. However, if you paid sick leave or FMLA to employees after April 1st, but didn’t receive your PPP loan until April 20th, are you to claim the money on your Form 7200 prior to April 20th? – We would need guidance on how this would be claimed. At this time, I suggest we wait to see what comes out between this time frame and the July 31 deadline for the Form 941.

18. So, the employer that gets PPP loan can’t use any other wages for ERC? – That is correct.

19. Do I use Form 7200 to request advanced payments of credits if I am self-employed? NO

20. What are qualified wages? – Qualified wages are wages (as defined in section 3121(a) of the Internal Revenue Code (the “Code”)) and compensation (as defined in section 3231(e) of the Code) paid by an Eligible Employer to employees after March 12, 2020, and before January 1, 2021. Qualified wages include the Eligible Employer’s qualified health plan expenses that are properly allocable to the wages.

The definition of qualified wages depends, in part, on the average number of full-time employees (as defined in section 4980H of the Code) employed by the Eligible Employer during 2019.

If the Eligible Employer averaged more than 100 full-time employees in 2019, qualified wages are the wages paid to an employee for time that the employee is not providing services due to either

(1) a full or partial suspension of operations by order of a governmental authority due to COVID-19, or

(2) a significant decline in gross receipts. For these employers, qualified wages taken into account for an employee may not exceed what the employee would have been paid for working an equivalent duration during the 30 days immediately preceding the period of economic hardship.

If the Eligible Employer averaged 100 or fewer full-time employees in 2019, qualified wages are the wages paid to any employee during any period of economic hardship described in (1) and (2) above.

Issue 2: IRS Announced Waivers of Offers for Compromise Applications

Final regulations were released that increase the Offer in Compromise application fee to $205 and provide an additional way for the IRS to waive the Offer in Compromise application fee for low-income taxpayers, based on their adjusted gross income (AGI). The IRS considers the taxpayer’s overall financial circumstances when considering an OIC in an effort to administratively resolve the amount due. Applicants who meet the definition of a “low-income taxpayer” receive a waiver of their OIC application fee.

A new provision from the Taxpayer First Act provides an additional way for low-income taxpayers to qualify for a waiver of the OIC application fee. Normally, the IRS determines if taxpayers fall at or below 250% of the poverty level by looking at their household’s size and gross monthly income. The new law provides an additional standard for the IRS to use in making the calculation. The IRS will now also look at a taxpayer’s AGI from the most recent tax return to determine whether it is at or below 250% of the poverty level.

Select State COVID-19 Updates

Issue 3: Nebraska COVID-19 Guidance

The State of Nebraska is providing the same income tax relief to state income taxpayers. The tax filing deadline will automatically be extended to July 15, 2020 for state income tax payments and estimated payments that were originally due on April 15, 2020.

Nebraskans who are able to pay earlier are encouraged to do so to help the State manage its cash flow. For Nebraskans affected by the COVID-19 pandemic in ways that impair their ability to comply with their state tax obligations for taxes administered by the Nebraska Department of Revenue, the Tax Commissioner may grant penalty or interest relief depending on individual circumstances. To request relief, please complete and mail a Request for Abatement of Penalty, Form 21, or Request for Abatement of Interest, Form 21A, with an explanation of how you were impacted.

Issue 4: Recent Ohio Law Change Affecting Servicemembers Who Receive Disability Severance Payments

H.B. 18 ensures that veterans’ disability severance payments are exempt from Ohio’s income tax. Disability severance payments awarded following honorable discharge or release are generally exempt from federal income tax and thus exempt from Ohio’s income tax.

If your client received such a payment in a prior year, they should have received a letter from the Defense Finance and Accounting Service (DFAS) on behalf of the Department of Defense (DoD).

If the client did not pay tax on this amount when the original return was filed, no action is required. However, if the income was reported, the Department of Taxation recommends the client file an amended federal return with the IRS to request a refund.

Issue 5: Pennsylvania Extends Personal Income Tax Return Filing Deadline to July 15, 2020, Plus Other COVID-19 News

The deadline for taxpayers to file their 2019 Pennsylvania personal income tax returns is extended to July 15, 2020. The Department of Revenue will also waive penalties and interest on 2019 personal income tax payments through the new deadline of July 15, 2020. This extension applies to both final 2019 tax returns and payments, and estimated payments for the first and second quarters of 2020. All taxpayers who received more than $33 in total gross taxable income in calendar year 2019 must file a Pennsylvania personal income tax return (PA-40) by midnight on Wednesday, July 15, 2020.

Although the filing deadline has been extended, the Department of Revenue is encouraging taxpayers who are able to file their returns electronically to do so. If additional time to file is needed, taxpayers still have the option to file a request for an extension to file their Pennsylvania personal income tax return. The extension is available for up to six months. As an important reminder, an extension of time to file does not extend the deadline to make a payment if you owe taxes to the commonwealth.

Estimated Payments

The deadline for taxpayers who make quarterly estimated personal income tax payments is also extended to July 15, 2020. That means estimated payments for the first and second quarters of 2020 will be due by July 15, 2020. Any individual who expects to receive more than $8,000 of Pennsylvania-taxable income not subject to withholding by a Pennsylvania employer must estimate and pay personal income tax quarterly. Estimated tax due dates for individuals are typically April 15, June 15, Sept. 15 and Jan. 15, or the first following business day if any deadline falls on a weekend or holiday.

Taxpayers who do submit their returns via paper should know that there will be delays in the processing of their returns, due to the fact that Department of Revenue’s offices are closed as part of mitigation efforts to help prevent the spread of COVID-19.

Appeal Deadline

Because commonwealth offices are currently closed to help prevent the spread of COVID-19, there will be additional time in certain cases for taxpayers who wish to appeal a tax assessment issued by the Department of Revenue or file a petition for a tax refund with the Board of Appeals. A petition for appeals of all tax types will be accepted as timely filed if it is filed by the later of the following dates:

- 30 days after the reopening of the Board of Appeals offices; or

- The original appeal deadline.

Please know that If the appeal deadline fell on a date prior to the closure of commonwealth offices (March 16, 2020), the original appeal deadline is still applicable. In other words, in these cases petitions will be considered as timely filed if they are filed by the last day of the appeal period. Additionally, the Board of Appeals will accept any submission of requested documentation as long as it is received within 30 days after the Board of Appeals offices reopen.

Reach the Department of Revenue Online

With the Department of Revenue’s call centers closed due to the mitigation efforts to help prevent the spread of COVID-19, the Department of Revenue is encouraging taxpayers to use its Online Customer Service Center, available at revenue-pa.custhelp.com. Clients can use this resource to electronically submit a question to a department representative. The department representative will be able to respond through a secure, electronic process that is similar to receiving an email.

Issue 6: Like the IRS, Wisconsin Extends Tax Filing Deadline to July 15

Both federal and Wisconsin income tax payment and return due dates are automatically extended to July 15, 2020. Wisconsin law will automatically extend time and waive interest and penalties for taxpayers due to a presidentially declared disaster.

- The Wisconsin Department of Revenue notes that most services are found online at www.revenue.wi.gov. Customer service phone numbers: Individuals: (608) 266-2486 Businesses: (608) 266-2776

Issue 7: Missouri COVID -19 Relief

Mirroring the federal guidance issued by the Internal Revenue Service, the Missouri Department of Revenue will provide special filing and payment relief to individuals and corporations:

- Filing deadline extended: The deadline to file income tax returns has been extended from April 15, 2020, to July 15, 2020.

- Payment relief for individuals and corporations: Income tax payment deadlines for individual and corporate income returns with a due date of April 15, 2020, are extended until July 15, 2020. This payment relief applies to all individual income tax returns, income tax returns filed by C Corporations, and income tax returns filed by trusts or estates. The Department of Revenue will automatically provide this relief, so filers do not need to take any additional steps to qualify.

- This relief for individuals and corporations will also include estimated tax payments for tax year 2020 that are due on April 15, 2020.

- Penalties and interest will begin to accrue on any remaining unpaid balances as of July 16, 2020. Individuals and corporations that file their return or request an extension of time to file by July 15, 2020, will automatically avoid interest and penalties on the tax paid by July 15.

Issue 8: Minnesota – Sales Tax Payment Extension for Eligible Businesses

The Minnesota Department of Revenue is providing additional time until July 15, 2020, for taxpayers to file and pay 2019 Minnesota Individual Income Tax without any penalty and interest.

First quarter 2020 estimated income tax payments for individuals, calendar year partnerships, S-corporations, and fiduciaries are still due April 15, 2020. This is different than the federal payment date. The due date for calendar year corporate franchise taxpayers was March 15, 2020.

Sales Tax Payment Grace Period

The Department is extending the grace period on Sales and Use Tax payments to May 20, 2020, for businesses required to suspend or reduce services under Executive Order 20-04. The Department will not assess penalties or interest on affected businesses that:

• Have monthly payments due March 20, and pay by May 20

• Have monthly or quarterly payments due April 20, and pay by May 20

Gambling Tax Payment Grace Period

We are extending the grace period on Lawful Gambling Tax payments to May 20, 2020, for organizations that request an extension for their March 20 or April 20 payment. The Department will not assess penalties or interest on affected businesses that:

• Have monthly payments due March 20, and pay by May 20

• Have monthly or quarterly payments due April 20, and pay by May 20

Business Income Taxes

The Minnesota due date has not changed for Corporation Franchise, S Corporation, Partnership, or Fiduciary taxes. However, under state law:

- C corporations receive an automatic extension to file their Minnesota return to the later of 7 months after the due date or the date of any federal extension to file.

- S corporations, partnerships, and fiduciaries receive an automatic extension to file their state return to the date of any federal extension to file.

The payment due dates for 2019 taxes and 2020 estimated taxes have not changed.

Issue 9: Iowa COVID-19 Relief

The Iowa Department of Revenue has announced conditional penalty relief for taxpayers required to make estimated payments. The changes, prompted by COVID-19, are the result of Order 2020-03, an order signed by Director of Revenue Kraig Paulsen.

Specifically, the order provides conditional penalty relief for taxpayers required to make estimated payments of individual, corporate, or franchise tax for a tax year beginning during the 2020 calendar year which have an installment due date on or after April 30, 2020, and before July 31, 2020.

In addition to any other applicable exceptions to penalties for underpayment of estimated tax provided by Iowa law, for Iowa residents or other taxpayers doing business in Iowa and required to make quarterly estimated Iowa individual income, corporate income, or franchise tax payments for a tax year beginning during the 2020 calendar year, the taxpayer shall not be subject to penalties for underpayment of estimated tax under Iowa Code §§ 422.16 or 422.88 with respect to a 2020 estimated tax installment with a due date on or after April 30, 2020, and before July 31, 2020, if the tax payments made on or before that due date satisfy the following provisions as applicable:

- For individuals with 2018 federal adjusted gross income as modified for Iowa purposes of $150,000 ($75,000 for married filing separate) or less, the tax payments shall be equal to or greater than the following percentage of the taxpayer’s total tax shown due or required to be shown due on the taxpayer’s 2018 Iowa income tax return if the return covered a period of 12 months:

- 25% of the tax with respect to the first installment due during the period covered by this Order.

- 50% of the tax with respect to the second installment due during the period covered by this Order.

2. For individuals with a 2018 federal adjusted gross income as modified for Iowa purposes of greater than $150,000 ($75,000 for married filing separate), the tax payments shall be equal to or greater than the following percentage of the taxpayer’s total tax shown due or required to be shown due on the taxpayer’s 2018 Iowa income tax return if the return covered a period of 12 months:

- 5% of the tax with respect to the first installment due during the period covered by this order.

- 55% of the tax with respect to the second installment due during the period covered by this order.

3. For corporations or financial institutions, the tax payments are equal to or greater than the following percentage of the taxpayer’s total tax shown due or required to be shown due on the taxpayer’s 2018 Iowa income tax or franchise tax return if a return showing a liability for tax was filed by the taxpayer for the 2018 taxable year and such 2018 taxable year covered a period of 12 months:

- 25% of the tax with respect to the first installment due during the period covered by this Order.

- 50% of the tax with respect to the second installment due during the period covered by this order.

For any qualifying taxpayer who takes advantage of the underpayment penalty relief provided, the difference, if any, between the total 2020 income or franchise tax installment payments otherwise required to be made prior to July 31, 2020 less the tax payment required to be made prior to July 31, 2020 shall be added to and made part of the taxpayer’s next 2020 income or franchise installment payment due July 31, 2020, and failure to pay such increased required installment by that due date shall be considered an underpayment of estimated taxes for that installment.

The Iowa Department of Revenue has extended the filing and payment deadline for several state tax types, including income tax. The changes, prompted by COVID-19, are designed to provide flexibility to hard-working Iowans whose lives have been disrupted. The changes are a result of an order signed earlier today by Director of Revenue Kraig Paulsen.

The order extends filing and payment deadlines for income, franchise, and moneys and credits taxes with a due date on or after March 19, 2020, and before July 31, 2020, to a new deadline of July 31, 2020.

Specifically, the order includes:

- IA 1040 Individual Income Tax Return and all supporting forms and schedules

- IA 1040C Composite Return and all supporting forms and schedules

- IA 1041 Fiduciary Return and all supporting forms and schedules

- IA 1120 Corporation Income Tax Return and all supporting forms and schedules

- IA 1120F Franchise Tax Return for Financial Institutions and all supporting forms and schedules

- IA 1065 Iowa Partnership Return and all supporting forms and schedules

- IA 1120S S Corporation Return and all supporting forms and schedules

- Credit Union Moneys and Credits Tax Confidential Report

The tax returns listed above and any tax due associated with those returns if the due date is on or after March 19 but before July 31 of this year. The extension does not apply to estimated tax payments.

Iowa residents or other taxpayers doing business in Iowa who are required to file the Iowa returns listed above.

No late-filing or underpayment penalties shall be due for qualifying taxpayers who comply with the extended filing and payment deadlines in this order. Interest on unpaid taxes covered by this order shall be due beginning on August 1, 2020.

Issue 10: Indiana COVID-19 Relief

The Indiana Department of Revenue announced several tax filing and payment deadline extensions as a result of the COVID-19 pandemic, however, filing and payment requirements and dates for taxes collected by businesses remain unchanged.

Business taxes, including sales, withholding income, food and beverage, county innkeeper’s and heavy equipment rental excise tax remain due on the standard due dates as listed on DOR’s website at dor.in.gov/3344.htm. Interest and penalties will apply if filing and payment deadlines are missed and will not be automatically waived.

Filing on time is critical. After completing the required filing, if a business owner is unable to make a scheduled payment, payment plans are available.

Individual tax returns and payments, along with estimated payments originally due by April 15, 2020 are now due on or before July 15, 2020. Returns included are the IT-40, IT-40PNR, IT-40RNR, IT-40ES, ES-40 and SC-40.

Corporate tax returns and payments, along with estimated payments originally due by April 15 or April 20 are now due on or before July 15, 2020. Those originally due on May 15, 2020, are now due on August 17, 2020. Returns included are the IT-20, IT-41, IT-65, IT-20S, FIT-20, URT-1, IT-6, FT-QP and URT-Q.

All other tax return filings and payment due dates remain unchanged.

If Hoosiers need additional time to file, they can request an extension. Instructions for those extensions can be found on DOR’s website. If an individual request a federal extension, Indiana automatically extends the state deadline and there is no need to file anything additional.

Issue 11: COVID-19 Relief – Illinois

The filing deadline for Illinois income tax returns has been extended from April 15, 2020, to July 15, 2020. This filing and payment relief includes:

- The 2019 income tax filing and payment deadlines for all taxpayers who file and pay their Illinois income taxes on April 15, 2020, are automatically extended until July 15, 2020. This relief applies to all individual returns, trusts, and corporations. This relief is automatic, taxpayers do not need to file any additional forms or call IDOR to qualify.

- Penalties and interest will begin to accrue on any remaining unpaid balances as of July 16, 2020. The client will automatically avoid interest and penalties on the taxes paid by July 15, 2020.

- The fastest, most secure way to receive a refund is to file tax returns electronically and request direct deposit into a checking or savings account.

- This does NOT impact the first and second installments of estimated payments for 2020 taxes that are due April 15 and June 15. Taxpayers are required to estimate their tax liability for the year and make four equal installments. Taxpayers will not be assessed a late estimated payment penalty if the amount of the installments equals 90% or more of the current year’s liability or 100% of the previous year’s liability.

- Since taxpayers may not know their prior year’s tax liability if they do not file by the original due date, the Department is providing for an additional option upon which taxpayers can base their 2020 estimated tax payments. For 2020, estimated tax payments can be based upon either:

- 100 % of their estimated liability for the year 2020.

- 100 % of their actual liability for year 2019 or

- 100 % of their actual liability for year 2018.

- Note: If the client plans to base their estimated payments on a previous year’s actual liability and have filed your 2019 return, we encourage you to use your actual liability for 2019.If taxpayers timely pay in four equal installments, the lesser of 90 percent of their liability for the year 2020 or 100 percent of their liability for the years 2019 or 2018, they can avoid estimated late payment penalties.

Estate Tax

Due to closures related to COVID-19, the Attorney General’s Office will be operating with reduced staff. In recognition of this, Estates with returns and payments due between March 16, 2020 and April 15, 2020 will receive a 30-day extension for filing and payment. Please be aware that an extension of time to pay does not waive or abate statutory interest and that payments must be sent to the Illinois State Treasurer.

Estate Tax Section

100 West Randolph Street

13th Floor

Chicago, Illinois 60601

Telephone: (312) 814-2491

Estate Tax Section

500 South Second Street

Springfield, Illinois 62701

Telephone: (217) 524-5095

Inheritance Tax Releases: An Illinois Inheritance Tax Release may be necessary if a decedent died before January 1, 1983. If a release is required, please call Chicago (312) 814-2491 or Springfield (217) 524-5095 for further assistance.

Short-Term Relief from Penalties for Late Sales Tax Payments Due to COVID-19 Virus Outbreak

All Registered Illinois Retailers Operating Eating and Drinking Establishments

In an effort to assist eating and drinking establishments impacted by the COVID-19 outbreak, effective immediately, the Illinois Department of Revenue (IDOR) is waiving any penalty and interest that would have been imposed on late Sales Tax payments from qualified taxpayers.

Who is a qualified taxpayer eligible for relief? Taxpayers who are eligible for relief from penalties and interest on late Sales Tax payments are those operating eating and drinking establishments that incurred a total Sales Tax liability of less than $75,000 in calendar year 2019.

What are the reporting periods for which qualified taxpayers are allowed relief? Qualified taxpayers will not be charged penalties or interest on late payments for Sales Tax liabilities reported on Form ST-1, Sales and Use Tax and E911 Surcharge Return, that are due for the February, March, and April 2020 reporting periods.

What must qualify taxpayers do to request relief? For most qualified taxpayers, IDOR will automatically waive penalties and interest. If you receive a notice from IDOR that imposes penalties and interest that you believe should have qualified for a waiver, you can respond to the notice to indicate that you believe you should have qualified for relief. IDOR will review the response and grant relief, if appropriate. Qualified taxpayers are required to file Form ST-1 for each reporting period by their original due dates, even if they are unable to make a payment. To qualify for relief, taxpayers must pay their liabilities due in March, April, and May 2020.

Issue 12: TIGTA Unveils New Flyer Warning Taxpayers About Impersonation Scam

The Treasury Inspector General for Tax Administration (TIGTA), has released a new flyer as a reminder to taxpayers about fraudulent calls they may receive from individuals impersonating Internal Revenue Service (IRS) and Treasury employees.

Since October 2013, TIGTA has been tracking and investigating this scam, in which criminals impersonate IRS employees in order to extort money from individual taxpayers. To date, more than 2.5 million people have reported to TIGTA that they have received an impersonation call. More than 15,800 victims have reported that they paid the criminal impersonators a total amount of more than $80 million.

On January 9, 2020, the operator of an Indian-based call center pled guilty to one count of wire fraud conspiracy, one count of conspiracy, and admitted to causing a total loss of $25 million to $65 million through use of IRS impersonation scam tactics. This is the latest of 16 individuals recently charged in Federal court in connection with the IRS Impersonation scam, bringing the total number of individuals charged through TIGTA’s efforts in Federal court in connection with this scam to 170 people (from 2013 through January 31, 2020). Ninety-three of those individuals have been sentenced and collectively received a total of more than 393 years’ imprisonment.

TIGTA’s new flyer contains the following information to educate taxpayers:

- The IRS generally first contacts people by mail – not by phone – about unpaid taxes

- The IRS may attempt to reach you by telephone, but will not insist on payment using an iTunes card, gift card, prepaid debit card, money order, or wire transfer.

- The IRS will never request personal or financial information by e-mail, text, or any social media.

If you receive a call from someone claiming to be with the IRS asking for a payment, take the following action:

- If you owe Federal taxes, or think you might owe taxes, just hang up and call the IRS at 1-800-829-1040. IRS employees can help you with your payment questions.

- If you do not owe taxes, fill out the “IRS Impersonation Scam” form on TIGTA’s website, www.tigta.gov, or call TIGTA at 1-800-366-4484.

- The flyer can be viewed on TIGTA’s public https://www.treasury.gov/tigta/

Issue 13: Correction to 2018 and 2019 Worksheet 3, Figuring Net Self-Employment Income for Schedule SE

Unreimbursed employee business expenses incurred by a minister, or clergy member, can be deducted from gross income when calculating SE tax. This line was inadvertently removed from Worksheet 3, Figuring Net Self-Employment Income from Schedule SE, in the 2018 and 2019 Publication 517.

The 2018 and 2019 worksheets, lines after 5 should be replaced with the following.

- Total unreimbursed employee business expenses.

- Total business expenses not deducted in lines 1 and 2 above (add lines 5 and 6).

- Net self-employment income. Subtract line 7 from line 4. Enter here and on Schedule SE, Section A, line 2; or Section B, line 2.

The removed line from 2018 and 2019 will be added back for the 2020 revision.

Issue 14: Redesigned Withholding Compliance Lock-In Letters 2800C and 2808C Coming Soon

The Tax Cuts and Job Act of 2017 (TCJA) changed withholding calculations by eliminating allowances, and in response, the IRS redesigned Form W-4, Employee’s Withholding Certificate. The Service is also redesigning the Withholding Compliance Lock-in Letters to reflect these changes.

Effective January 1, 2020, TCJA mandated withholding calculations to consider credits, adjustments and deductions to factor a dollar value. The allowance withholding method and the TCJA withholding method use the same tax tables. For now, employers and payroll providers will use the allowance method as directed in the letters they receive to calculate employees’ withholding per pay period. After the lock-in letters redesign is complete, they should follow the new TCJA directions.

Withholding Compliance Lock-In Letters 2800C and 2808C are being redesigned to include the new lock-in rate instructions. Instead of providing the employer with the number of allowances by which withholding would be reduced, the letters will provide employers with the withholding status and withholding rate and any annual reductions to withholding or additional amount to withhold per pay period as a dollar value.

The format shown below is what the withholding instructions will look like on the redesigned 2800C lock-in letter:

Withholding Status (Filing Status): Single Withholding rate: Form W-4, Step 2(C), Checkbox (higher withholding rate)

Annual reductions from withholding (Form W-4 line 3): $0.00 Other income (Form W-4 line 4(a)): $0.00 Deductions (Form W-4 line 4 (b)): $0.00 Additional amount to withhold per paycheck (Form W-4 line 4(c)): $0.00

Issue 15: Supreme Court will Hear ACA Case in the October Term

Checkpoint has reported that the U.S. Supreme Court has placed the latest case challenging the constitutionality of the Affordable Care Act on its docket for the October term.

On January 21, 2020, the Supreme Court denied motions to expedite its decision on whether to hear the case. The petition for certiorari asked the Supreme Court to decide whether reducing the individual mandate to zero made that provision unconstitutional, and if so, whether that provision was severable from the rest of the ACA.

In December 2018, the Fifth Circuit Court of Appeals held that the individual mandate in the ACA is unconstitutional because it is no longer a tax and no other provision justifies the exercise of congressional power (Texas v. United States, No. 19-10011 (5th Cir. Dec. 18, 2019). The Fifth Circuit remanded the question of whether the individual mandate was severable from the ACA back to the district court.

Issue 16: I-9, Employment Eligibility Verification – New Revision Expires 10/31/2022

Use Form I-9 to verify the identity and employment authorization of individuals hired for employment in the United States. All U.S. employers must properly complete Form I-9 for each individual they hire for employment in the United States. This includes citizens and noncitizens. Both employees and employers (or authorized representatives of the employer) must complete the form.

On the form, an employee must attest to his or her employment authorization. The employee must also present his or her employer with acceptable documents evidencing identity and employment authorization. The employer must examine the employment eligibility and identity document(s) an employee presents to determine whether the document(s) reasonably appear to be genuine and to relate to the employee and record the document information on the Form I-9. The list of acceptable documents can be found on the last page of the form. Employers must retain Form I-9 for a designated period and make it available for inspection by authorized government officers.

The revised I-9 has a new expiration date of 10/31/2022. Employers should use this version when hiring new employees.

Issue 17: Delivery of the Stimulus Payment

Treasury and the Internal Revenue Service released state-by-state figures for Economic Impact Payments, with 88 million individuals receiving payments worth nearly $158 billion in the program’s first three weeks.

As of April 17, the IRS issued 88.1 million payments to taxpayers across the nation. More payments are continuing to be delivered each week.

More than 150 million payments will be sent out, and millions of people who do not typically file a tax return are eligible to receive these payments. Payments are automatic for people who filed a tax return in 2018 or 2019, receive Social Security retirement, survivor or disability benefits (SSDI), Railroad Retirement benefits, as well as Supplemental Security Income (SSI) and Veterans Affairs beneficiaries who didn’t file a tax return in the last two years.

| State | Number of EIP Payments | Amount of EIP Payments |

| Alabama | 1,306,879 | $2,432,903,249 |

| Alaska | 209,626 | $384,976,728 |

| Arkansas | 778,710 | $1,484,876,413 |

| Arizona | 1,868,529 | $ 3,408,327,214 |

| California | 9,127,137 | $15,894,426,934 |

| Colorado | 1,532,632 | $2,697,948,990 |

| Connecticut | 961,464 | $1,631,719,992 |

| District of Columbia | 179,738 | $255,501,803 |

| Delaware | 275,688 | $484,493,248 |

| Florida | 6,348,503 | $11,067,476,416 |

| Georgia | 2,785,534 | $5,041,819,449 |

| Hawaii | 378,200 | $677,850,427 |

| Iowa | 901,609 | $1,709,391,510 |

| Illinois | 3,561,467 | $6,288,620,441 |

| Indiana | 2,047,079 | $3,801,302,228 |

| Kansas | 806,471 | $1,527,129,168 |

| Kentucky | 1,247,465 | $2,352,784,094 |

| Louisiana | 1,265,581 | $2,297,891,337 |

| Massachusetts | 1,774,172 | $2,951,357,726 |

| Maryland | 1,561,936 | $2,662,114,660 |

| Maine | 400,919 | $722,201,531 |

| Illinois | 3,561,467 | $6,288,620,441 |

| Indiana | 2,047,079 | $3,801,302,228 |

| Kansas | 806,471 | $1,527,129,168 |

| Kentucky | 1,247,465 | $2,352,784,094 |

| Louisiana | 1,265,581 | $2,297,891,337 |

| Massachusetts | 1,774,172 | $2,951,357,726 |

| Maryland | 1,561,936 | $2,662,114,660 |

| Maine | 400,919 | $722,201,531 |

| Michigan | 2,945,568 | $5,338,452,373 |

| Minnesota | 1,568,913 | $2,857,063,159 |

| Missouri | 1,737,013 | $3,220,707,956 |

| Mississippi | 804,317 | $1,481,695,852 |

| Montana | 295,589 | $547,319,262 |

| North Carolina | 2,774,379 | $5,057,006,091 |

| North Dakota | 215,321 | $399,771,434 |

| Nebraska | 562,422 | $1,070,565,880 |

| New Hampshire | 407,786 | $714,166,522 |

| New Jersey | 2,245,299 | $3,861,741,262 |

| New Mexico | 596,433 | $1,072,887,126 |

| Nevada | 892,115 | $1,561,690,988 |

| New York | 5,481,796 | $9,283,821,196 |

| Ohio | 3,504,529 | $6,258,547,152 |

| Oklahoma | 1,074,373 | $2,056,089,347 |

| Oregon | 1,098,231 | $1,945,572,937 |

| Pennsylvania | 3,725,334 | $6,628,241,748 |

| Rhode Island | 319,156 | $541,849,017 |

| South Carolina | 1,361,971 | $2,489,898,415 |

| South Dakota | 255,301 | $487,326,070 |

| Tennessee | 1,997,548 | $3,683,938,147 |

| Texas | 7,812,382 | $14,398,065,881 |

| Utah | 818,700 | $1,676,956,785 |

| Vermont | 188,076 | $332,111,224 |

| Virginia | 2,312,429 | $4,146,024,506 |

| Washington | 2,058,899 | $3,680,595,622 |

| Wisconsin | 1,690,733 | $3,093,584,754 |

| West Virginia | 522,573 | $984,826,539 |

| Wyoming | 166,195 | $316,335,903 |

| Territories and Overseas* | 267,573 | $501,071,680.00 |

| Total | 88,183,614.00 | $157,969,767,489 |

Issue 18: More Answers to the Stimulus Payment Questions

The IRS has issues a group of Frequently Asked Questions (FAQ) that are updated with new information when it comes available. To keep up to date you need to access the website – an amazing number of questions have been posted. Copy and paste this address into your browser for access. https://www.irs.gov/coronavirus/economic-impact-payment-information-center

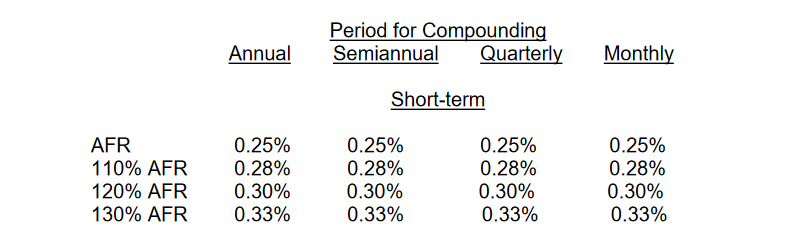

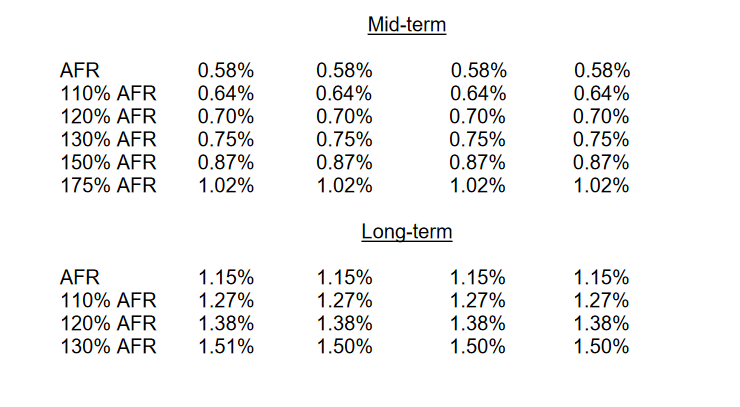

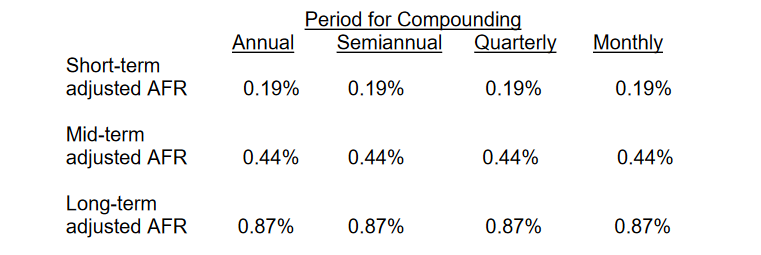

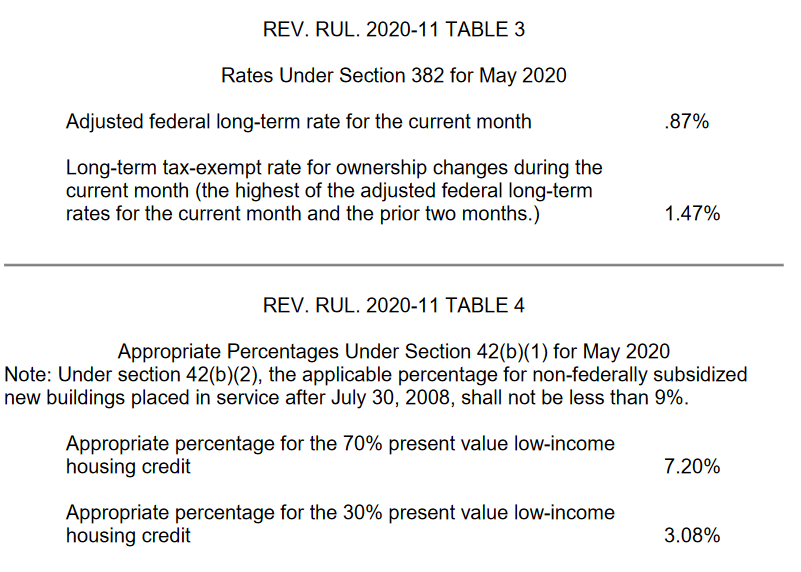

Issue 19: IRS has Provided Applicable Federal Rate Tables for May 2020 – Rev Rul 2020-11

Table 1

Applicable Federal Rates (AFR) for May 2020

REV. RUL. 2020-11 TABLE 1

REV. RUL. 2020-11 TABLE 2 Adjusted AFR for May 2020

REV. RUL. 2020-11 TABLE 5

Rate Under Section 7520 for May 2020

Applicable federal rate for determining the present value of an annuity, an interest for life or a term of years, or a remainder or reversionary interest.