In This Issue

Introduction to President Biden’s “Made in America Tax Plan”

What is a “Restaurant” for Purposes of the 2021-2022 100% Food/Beverage Deduction?

IRS to Recalculate Taxes on Unemployment Benefits

IRS Updates its Frequently Asked Questions About Lost, Stolen EIP2’s

Legislation Introduced to Keep Eyes on the Summer

IRS Appeals Requires Employees to Offer Virtual Conferences

In Notice 2021-21, IRS Postponed Certain Income Tax Deadlines for Individuals to May 17, 2021

New Due Diligence Requirements for Tax Professionals

IRS Adds Volkswagen Models to Plug-in Vehicle Credit List

Court Greenlights IRS to Serve John Doe Summons Related to Cryptocurrency Use

Estimated Tax Payment Issues

Personal Protective Equipment – Deductible Medical Expense

Several Payment P.O. Boxes Closing in 2022

IRS Answers Questions about Taxation of Emergency Rental Assistance Payments

Election to Use 2019 Income in 2020 Business Interest Deduction Calculation

Taxpayer Advocate Service’s Ability to Help with Delayed Refunds Is Limited

Did You File a Superseding Return for the Client?

IRS Suspends Requirement to Repay Excess Advance Payments of the 2020 Premium Tax Credit

Permanent Address not Required to Receive Economic Impact Payment

Applicable Federal Rates for May 2021, Rev. Rul. 2021-08

Issue 1: The Made in America Tax Plan

The current corporate income tax regime contains incentives for corporations to shift their production and profits overseas. The Made in America tax plan implements a series of corporate tax reforms to address profit shifting and offshoring incentives and to level the playing field between domestic and foreign corporations.

These include:

- Raising the corporate income tax rate to 28%.

- Strengthening the global minimum tax for U.S. multinational corporations.

- Reducing incentives for foreign jurisdictions to maintain ultra-low corporate tax rates by encouraging global adoption of robust minimum taxes.

- Enacting a 15% minimum tax on book income of large companies that report high profits, but have little taxable income.

- Replacing flawed incentives that reward excess profits from intangible assets with more generous incentives for new research and development.

- Replacing fossil fuel subsidies with incentives for clean energy production and

- Ramping up enforcement to address corporate tax avoidance.

These are the major elements of the Made in America tax plan, but the proposal contains several additional tax incentives that would directly benefit U.S. corporations, passthrough entities, and small businesses. These include, for example, a marked increase in the resources available through the Low-Income Housing Tax Credit and other housing incentives.

The President’s corporate tax agenda is aimed at encouraging investment and American job creation, while also investing in priorities that are intended to benefit American families, such as infrastructure and climate resiliency. It will, in summary, create a corporate tax regime that is fit for purpose: an engine for economic growth, international cooperation, and a more equitable society.

Increasing IRS’s enforcement budget. The Plan would increase the IRS’s enforcement budget. It envisions a well-resourced team of revenue agents that can be hired and trained to identify when corporations—and the wealthy individuals who own them—underpay taxes.

This proposal is part of a broader overhaul of tax administration that would give the IRS the resources it needs to collect the taxes that are owed by wealthy individuals and large corporations.

Issue 2: What is a “Restaurant” for Purposes of the 2021-2022 100% Food/Beverage Deduction?

Treasury and the IRS has issued Notice 2021-25 providing guidance under the Taxpayer Certainty and Disaster Relief Act of 2020. The Act added a temporary exception to the 50% limit on the amount that businesses may deduct for food or beverages. The temporary exception allows a 100% deduction for food or beverages from restaurants.

Beginning Jan. 1, 2021, through Dec. 31, 2022, businesses can claim 100% of their food or beverage expenses paid to restaurants as long as the business owner (or an employee of the business) is present when food or beverages are provided and the expense is not lavish or extravagant under the circumstances.

Under the temporary provision, restaurants include businesses that prepare and sell food or beverages to retail customers for immediate on-premises and/or off-premises consumption. However, restaurants do not include businesses that primarily sell pre-packaged goods not for immediate consumption, such as grocery stores and convenience stores.

The 50% limitation of §274(n)(1) continues to apply to the amount of any deduction otherwise allowable to the taxpayer for any expense paid or incurred for food or beverages acquired from such a business (unless another exception in §274(n)(1) applies to such expense).

In addition, an employer may not treat as a restaurant for purposes of §274(n)(2)(D):

(1) any eating facility located on the business premises of the employer and used in furnishing meals excluded from an employee’s gross income under § 119 or

(2) any employer-operated eating facility treated as a de minimis fringe under §132( e )(2), even if such eating facility is operated by a third party under contract with the employer as described in Reg § 1.132-7(a)(3).

Issue 3: IRS to Recalculate Taxes on Unemployment Benefits

To help taxpayers, the Internal Revenue Service announced that it will take steps to automatically refund money this spring and summer to people who filed their tax return reporting unemployment compensation before the recent changes made by the American Rescue Plan.

The legislation, signed on March 11, allows taxpayers who earned less than $150,000 in modified adjusted gross income to exclude unemployment compensation up to $20,400 if married filing jointly and $10,200 for all other eligible taxpayers. The legislation excludes only 2020 unemployment benefits from taxes.

For those taxpayers who already have filed and figured their tax based on the full amount of unemployment compensation, the IRS will determine the correct taxable amount of unemployment compensation and tax. Any resulting overpayment of tax will be either refunded or applied to other outstanding taxes owed.

For those who have already filed, the IRS will do these recalculations in two phases, starting with those taxpayers eligible for the up to $10,200 exclusion. The IRS will then adjust returns for those married filing jointly taxpayers who are eligible for the up to $20,400 exclusion and others with more complex returns.

There is no need for taxpayers to file an amended return unless the calculations make the taxpayer newly eligible for additional federal credits and deductions not already included on the original tax return.

These taxpayers may want to review their state tax returns as well.

Issue 4: IRS Updates its Frequently Asked Questions About Lost, Stolen EIP2’s

The client received payment by check, but it was lost, stolen, or destroyed. How do they get a replacement check?

The client cannot get a replacement check. However, if the IRS sent the EIP 2 by check and the check was lost, stolen, or destroyed, the client should request a payment trace so the IRS can determine if the check was cashed and if it was cashed, who signed the check. If the IRS determines that the EIP 2 check was not cashed, or was cashed and the client did not sign the check, IRS will credit the client’s account for the amount of the EIP 2. In this case, if eligible, the client can claim the RRC 2 on the 2020 tax return.

If the client does not request a trace on the EIP 2 check, they may not be able to claim the RRC 2 on the 2020 tax return because the IRS’s records will show that they received an EIP 2.

The client was issued an EIP 2, but they haven’t received it yet. Should they request a payment trace?

They should only request a payment trace to track the EIP 2 if:

- They received Notice 1444- B, which was sent to each recipient within 15 days of the IRS issuing the EIP 2; or the online account shows the payment amount (if they set up an online account); and

- They haven’t received the EIP 2: (a) within 5 days of the direct deposit date on Notice 1444-B (and the bank says it hasn’t received the payment), or (b) by March 31, 2021, if the EIP 2 was mailed.

After these time periods expire, if the client still has not received the EIP 2, the client can request a payment trace on the EIP 2.

How do I request a payment trace on the EIP 2?

They can request a payment trace by:

- calling the IRS at 1-800-919-9835, or

- mailing or faxing to the IRS Form 3911, Taxpayer Statement Regarding Refund.

When completing Form 3911:

- Write “EIP2” on the top of the form to identify the EIP they want to trace.

- Complete the form answering all refund questions as they relate to your EIP 2.

- When completing item 7 under Section 1: Check the box for “Individual” as the Type of return; Enter “2020” as the Tax Period; and leave the Date Filed space blank.

- Be sure to sign the form. If they are a joint filer, both spouses must sign the form.

Mail the form to the Internal Revenue Service where a paper return would normally be filed.

Issue 4: Legislation Introduced to Keep Eyes on the Summer

Legislation in generally introduced in two ways, a large bill like the Made in American Plan, and small bills like below which can be added together in a “garbage bill” or added to a larger piece of legislation to get it passed. There are several other options but this is what we see quite often. Those listed below may never find their way to law individually but may “piggy back” into law.

H.R.1381 – Main Street Tax Certainty Act. To make permanent the deduction for qualified business income.

H.R.1380 – Permanent Tax Relief for Working Families Act. To make permanent certain changes made by the Tax Cuts and Jobs Act (PL 115-97) to the child tax credit.

S.618 – Universal Giving Pandemic Response and Recovery Act. To modify and extend the deduction for charitable contributions for individuals not itemizing deductions.

H.R.1346 – Hospitality and Commerce Job Recovery Act of 2021. To create a refundable tax credit for travel expenditures, and for other purposes.

S.447 – Educational Opportunities Act. To allow a credit against tax for qualified elementary and secondary education tuition.

S.456 – New Markets Tax Credit Extension Act of 2021. To permanently extend the new markets tax credit, and for other purposes.

S.496 – Student Loan Tax Relief Act. To exclude from taxable income any student loan forgiveness or discharge.

S.499 – Improving Health Insurance Affordability Act of 2021. To expand eligibility for the refundable credit for coverage under a qualified health plan, to improve cost-sharing subsidies under the Patient Protection and Affordable Care Act, and for other purposes.

H.R.1040 – Flat Tax Act. To amend the Internal Revenue Code of 1986 to provide taxpayers a flat tax alternative to the current income tax system.

H.R.1081 – Charitable Giving Tax Deduction Act. To amend the Internal Revenue Code of 1986 to allow the deduction for charitable contributions as an above-the-line deduction.

H.R.1161 – Fairness in Social Security Act of 2021. To amend the Internal Revenue Code of 1986 to exclude the portion of a lump-sum social security benefit payment that relates to periods prior to the taxable year from the determination of household income.

H.R.1219 – ABLE Age Adjustment Act. To amend the Internal Revenue Code of 1986 to increase the age requirement with respect to eligibility for qualified ABLE programs.

H.R.1242 – Skills Investment Act of 2021. To amend the Internal Revenue Code of 1986 to provide for lifelong learning accounts, and for other purposes.

H.R.1243 – Skills Renewal Act. To amend the Internal Revenue Code of 1986 to establish a tax credit for training services received by individuals who are unemployed as a result of the coronavirus pandemic.

H.R.1271 – Electric CARS Act of 2021. To amend the Internal Revenue Code of 1986 to extend certain tax credits related to electric cars, and for other purposes.

S.380 – Health Savings Act of 2021. To amend the Internal Revenue Code of 1986 to improve access to health care through expanded health savings accounts, and for other purposes.

S.477 – Hospitality and Commerce Job Recovery Act of 2021. To amend the Internal Revenue Code of 1986 to create a refundable tax credit for travel expenditures, and for other purposes.

S.510 – Ultra-Millionaire Tax Act of 2021. To impose a tax on the net value of assets of a taxpayer, and for other purposes.

S.532 – Rural Wind Energy Modernization and Extension Act of 2021. To modify the energy tax credit to apply to qualified distributed wind energy property.

S.536 – Blue Collar Bonus Act of 2021. To provide a credit for wages received by individuals that are less than the median wage.

S.551 – Recovery Startup Assistance Act. To expand the Employee Retention Tax Credit to include certain startup businesses.

S.617 – Death Tax Repeal Act of 2021. To repeal the estate and generation-skipping transfer taxes, and for other purposes.

H.R.1431 – Hire A Hero Act of 2021. To allow the work opportunity credit to small businesses which hire individuals who are members of the Ready Reserve or National Guard, and for other purposes.

Issue 5: IRS Appeals Requires Employees to Offer Virtual Conferences

AP-08-0321-0009: Memorandum for Required Use of Virtual Conferences

The IRS Independent Office of Appeals (“Appeals”) has issued a procedural memo that requires Appeals employees to offer a virtual conference to taxpayers who request an in-person conference that cannot be accommodated. Offering a virtual Appeals conference previously wasn’t required in this situation.

For example, an Appeals employee is required to offer and conduct a virtual conference if the taxpayer (or their representative) has requested one. In addition, the Appeals employee should offer a virtual conference if the taxpayer (or their representative) has requested an in-person conference, but that request cannot be accommodated by Appeals.

- Appeals stopped conducting in-person conferences at the beginning of the COVID-19 pandemic and has not yet resumed holding them.

Appeals employees are not required to offer a virtual conference when a taxpayer (or their representative) has requested a phone or correspondence conference. In this case, the Appeals employee should use their judgment and experience to determine whether to voluntarily offer a virtual conference to that taxpayer.

If the taxpayer declines the offer of a virtual conference, then the Appeals employee should continue with normal case processing procedures.

The Memo notes that this procedural deviation doesn’t replace in-person conferences when Appeals begins holding them again. Appeals will still hold in-person conferences when Appeals can accommodate them and such conferences are appropriate.

Issue 6: In Notice 2021-21, IRS Postponed Certain Income Tax Deadlines for Individuals to May 17, 2021

Does the relief provided in §III(B) of the Notice 2021-21 (the Notice) apply to payments by individuals of a §965(h) installment payment having an original due date of April 15, 2021?

The relief provided in §III(B) of the Notice postpones the due date of an Affected Taxpayer’s Form 1040 with an original due of April 15, 2021 to May 17, 2021, which also postpones the due date of an Affected Taxpayer’s §965(h) installment payment (if applicable) to May 17, 2021.

For purposes of the Notice, Affected Taxpayer means any person with a federal income tax return filed on Form 1040, Form 1040-SR, Form 1040-NR, Form 1040-PR, Form 1040-SS, or Form 1040(SP) (Form 1040 series), or a Federal income tax payment reported on or made in connection with one of these forms, that absent the Notice would be due April 15, 2021.

The relief provided in §III(B) of the Notice does not apply to § 965(h) installment payments with respect to taxpayers who are not Affected Taxpayers.

Issue 7: New Due Diligence Requirements for Tax Professionals

For tax year 2020, recent legislation allows eligible taxpayers to elect to use their 2019 earned income to figure the 2020 earned income credit (EIC) or additional child tax credit (ACTC) when their 2019 earned income is more than their 2020 year earned income. If you prepare a tax return in which the client elects to figure the EIC, ACTC, or both credits using 2019 earned income, the due diligence requirements set forth in Treasury Regulations apply to the preparer’s computation of earned income for two years.

- The 2020 tax year to determine that earned income has decreased from 2019, and

- The 2019 tax year to determine the earned income used to compute each credit claimed under the election.

Answer “Yes” to line 1 of the 2020 Form 8867 even if you used information for the 2019 tax year as a result of their taking the election. You do not have to recompute the 2019 earned income if you prepared the taxpayer’s 2019 tax return.

The IRS summarizes the four due diligence requirements as:

- Complete and submit Form 8867.

- Compute the credits.

- Not know or have reason to know that any information you used to claim the credits is incorrect.

- Keep records for three years.

Note: If the preparer did not prepare the taxpayer’s 2019 tax return, then the preparer cannot rely on the 2019 return for due diligence purposes and has to go back and compute the 2019 earned income himself or herself as if he or she were actually preparing the 2019 return.

Issue 8: IRS Adds Volkswagen Models to Plug-in Vehicle Credit List

| Model Year | Vehicle Description | Credit Amount |

| 2021 | Volkswagen ID.4 (First Edition, Pro, Pro S models) | $7,500 |

| 2015, 2016, 2017, 2018, 2019 | Volkswagen e-Golf | $7,500 |

Issue 9: Court Greenlights IRS to Serve John Doe Summons Related to Cryptocurrency Use

A federal court in the District of Massachusetts entered an order authorizing the IRS to serve a John Doe summons on Circle Internet Financial Inc., or its predecessors, subsidiaries, divisions, and affiliates, including Poloniex LLC (collectively “Circle”), seeking information about U.S. taxpayers who conducted at least the equivalent of $20,000 in transactions in cryptocurrency during the years 2016 to 2020. The IRS is seeking the records of Americans who engaged in business with or through Circle, a digital currency exchanger headquartered in Boston.

Cryptocurrency, as generally defined, is a digital representation of value. Because transactions in cryptocurrencies can be difficult to trace and have an inherently pseudo-anonymous aspect, clients may be using them to hide taxable income from the IRS. In the court’s order, U.S. Judge Richard G. Stearns found that there is a reasonable basis for believing that cryptocurrency users may have failed to comply with federal tax laws.

The court’s order grants the IRS permission to serve what is known as a “John Doe” summons on Circle. The United States’ petition does not allege that Circle has engaged in any wrongdoing in connection with its digital currency exchange business. Rather, according to the court’s order, the summons seeks information related to the IRS’s “investigation of an ascertainable group or class of persons” that the IRS has reasonable basis to believe “may have failed to comply with any provision of any internal revenue laws[.]” According to the copy of the summons filed with the petition, the IRS is requesting that Circle produce records identifying the U.S. taxpayers described above, along with other documents relating to their cryptocurrency transactions.

The IRS issued guidance regarding the tax treatment of virtual currencies in IRS Notice 2014-21, which provides that virtual currencies that can be converted into traditional currency are property for tax purposes. The guidance explains that receipt of virtual currency as payment for goods or services is treated as income and that a taxpayer can have a gain or loss on the sale or exchange of a virtual currency, depending on the taxpayer’s cost to purchase the virtual currency (that is, the client’s tax basis).

Issue 10: Estimated Tax Payment Issues

There is some question as to whether there will be an underpayment of estimated tax penalty where:

- a) a taxpayer files an individual income tax return by May 17 but after April 15;

- b) there is an overpayment on that return that the taxpayer elects to have applied to his/her 2021 tax liability;

- c) he/she needs to make a first quarter 2021 estimated tax payment in order to avoid an underpayment-of-estimated tax penalty;

- d) his/her actual first quarter 2021 estimated tax payment made by April 15 is insufficient to avoid that penalty; and

- e) the amount of the 2020 overpayment, when added to the first quarter 2021 estimated payment, is sufficient to avoid that penalty.

In other words, will the overpayment be considered to be applied on the date the 2020 return is filed, which is after the April 15 due date of the first quarter 2021 estimated payment, or will it be considered to be applied on April 15?

If the former, there would be liability for an underpayment of estimated tax penalty, while, if the latter, there will be no penalty.

IRS has not yet made a specific statement on this issue. And, there does not appear to be precedent for a Year 1 original return due date being after the Year 2 first quarter estimate due date.

Historically, IRS has provided that where a taxpayer overpays the tax due for Year 1 via withholding and/or estimated tax payments, the overpayment can be applied to the first quarter Year 2 estimate even if the Year 1 return is filed after the due date of the first quarter Year 2 estimate. For example, the House Report for the Tax Reform Act of 1984 (PL 98-369) provided:

Thus, for example, assume a taxpayer makes estimated tax payments (including withholding) of $10,000 in 1984 and receives an extension of time to file the 1984 return until August 15, 1985. Also assume that a return is filed on August 15, 1985, showing a liability of $8,000 for 1984. The taxpayer may elect to credit the $2,000 overpayment to the April 15 estimated tax payment of his or her 1985 tax.

Issue 11: Personal Protective Equipment – Deductible Medical Expense

The IRS issued Announcement 2021-7 clarifying that the purchase of personal protective equipment for the primary purpose of preventing the spread of coronavirus are deductible medical expenses. In addition to masks, this includes times such as hand sanitizer and sanitizing wipes.

The amounts paid for personal protective equipment are also eligible to be paid or reimbursed under health flexible spending arrangements (health FSAs), Archer medical savings accounts (Archer MSAs), health reimbursement arrangements (HRAs), or health savings accounts (HSAs).

Issue 12: Several Payment P.O. Boxes Closing in 2022

IRS is closing several individual payment P.O. boxes (or Lockbox addresses) in the San Francisco, Calif., and Hartford, Conn., areas beginning Jan. 1, 2022.

Payments are currently being forwarded to Louisville, Ky., and Cincinnati, Ohio, through Dec. 31, 2021. However, payments mailed to these closed payment locations after Jan. 1, 2022, will be returned to sender.

To help ensure timely receipt, IRS encourages you to avoid mailing to these closing addresses as there could be mail delays. Please check Where to File on irs.gov for active addresses, before mailing your payments. If you receive an IRS payment letter, send your payment to the address located in the letter.

IRS encourages taxpayers to use IRS Direct Pay. It’s fast, secure and easy to pay a tax bill or estimated tax payment directly from a checking or savings account. Users receive instant confirmation that their payment has been made.

See Publication 3891, Lockbox Addresses for 2021, for more information.

Issue 13: IRS Answers Questions about Taxation of Emergency Rental Assistance Payments

Emergency Rental Assistance Frequently Asked Questions § 501, Division N, of the Consolidated Appropriations Act, 2021, enacted December 27, 2020, allows States and political subdivisions, U.S. territories, Indian Tribes, and the Department of Hawaiian Home Lands (“Distributing Entity”) to use certain funds allocated by the Department of the Treasury to provide emergency rental assistance (“Section 501 Emergency Rental Assistance”) to households that require financial assistance to pay rent, utilities, home energy expenses, and other related expenses.

Q1: I am a renter who received §501 Emergency Rental Assistance payments from a Distributing Entity for use in paying my rent. Are these payments includible in my gross income?

A1: No. § 501 Emergency Rental Assistance payments made to eligible households are not considered income to members of the household.

Q2: I am a renter who received §501 Emergency Rental Assistance payments from a Distributing Entity for use in paying my utilities or home energy expenses. Are these payments includible in my gross income?

A2: No. §501 Emergency Rental Assistance payments, including payments for utilities or home energy expenses, made to eligible households are not considered income to members of the household.

Q3: I am a renter who received §501 Emergency Rental Assistance from a Distributing Entity for use in paying my rent, utilities, and/or home energy expenses, but the Distributing Entity made the payments directly to my landlord and/or my utility companies on my behalf. Are these payments includible in my gross income?

A3: No. §501 Emergency Rental Assistance payments made on behalf of an eligible household are not considered income to members of the household.

Q4: I am a landlord and I have a tenant who qualifies for §501 Emergency Rental Assistance. A Distributing Entity sent me a rental payment on my tenant’s behalf under a Section 501 Emergency Rental Assistance program. Is this payment includible in my gross income?

A4: Yes. §501 Emergency Rental Assistance is intended to help eligible households that require financial assistance to pay for rent, utilities, home energy expenses, and other related expenses, and the payments are excluded from income only for those households. Rental payments you receive, whether from your tenant or from a Distributing Entity on your tenant’s behalf through a Section 501 Emergency Rental Assistance program, are includible in your gross income.

Q5: I run a utility company that has a customer who qualifies for §501 Emergency Rental Assistance. A Distributing Entity sent my company a utility payment on my customer’s behalf under a §501 Emergency Rental Assistance program. Is this payment includible in my company’s gross income?

A5: Yes. §501 Emergency Rental Assistance is intended to help eligible households that require financial assistance to pay for rent, utilities, home energy expenses, and other related expenses, and the payments are excluded from income only for those households. Utility payments your company receives, whether from a customer or from a Distributing Entity on the customer’s behalf through a Section 501 Emergency Rental Assistance program, are includible in your company’s gross income.

Issue 14: Election to Use 2019 Income in 2020 Business Interest Deduction Calculation

On March 27, 2020, §163(j) was amended by §2306 of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act).

The CARES Act allows taxpayers to elect to use its 2019 adjusted taxable income (ATI) in determining the taxpayer’s §163(j) limitation for any tax year beginning in 2020, subject to modifications for short tax years.

If this election is made, complete line 22, adjusted taxable income, on Form 8990, and leave lines 6 through 21 blank. No formal statement is required to make this election.

Please refer to section 6.02 of Rev. Proc. 2020-22 for additional information regarding this election under new §163(j)(10), as amended by the CARES Act.

Issue 15: Taxpayer Advocate Service’s Ability to Help with Delayed Refunds Is Limited

The Taxpayer Advocate Service (TAS) is aware that taxpayers are experiencing more refund delays this year than usual. Typically, the IRS processes electronic returns and pays refunds within 21 days of receipt. However, the high-volume of 2020 tax returns being filed daily, backlog of unprocessed 2019 paper tax returns, IRS resource issues, and technology problems are causing delays.

This is due, in part, to the IRS’s need to manually verify large numbers of Refund Recovery Credits (RRCs), as well as Earned Income Tax Credit (EITC) and Advance Child Tax Credit (ACTC) 2019 adjusted income lookback claims.

Once a return is processed by the IRS and loaded on to the IRS systems, TAS may be able to assist with delayed refunds if the client meets the case criteria.

Currently, the vast majority of processing delays result from tax returns not loaded onto the IRS system or in “suspense” status awaiting IRS action. To date, over 6 million electronic returns have been “suspended” due to issues requiring manual processing or return inconsistencies.

- Until these returns move out of suspense status, neither the IRS nor TAS can access these cases to work them or provide taxpayers with any additional information.

- TAS cannot accept refund delay cases that are in suspense, including requests for assistance made through the Systemic Advocacy Management System (SAMS).

- Until the tax return is posted on the IRS system, neither TAS nor the IRS can see or access the return information.

- And until TAS can see the return on the system, they cannot advocate to resolve any issues.

Issue 16: Did You File a Superseding Return for the Client?

IRS Counsel Reverses Course: Superseding Returns Filed on Extension Do Not Supersede for Purposes of Which Return Controls Assessment and Refund Claim Dates

The IRS must assess tax within three years after the return for that year was filed unless extended by one of the exceptions in § 6501. A taxpayer must file a claim for refund of any tax within three years from the time “the return” was filed, or two years from the time the tax was paid, whichever period expires later (unless the taxpayer and the IRS agree to extend the period).

In situations where a taxpayer files a second return before the filing deadline, the second return will be referred to as a superseding return, a term used regardless of whether the second return is filed before the original deadline or before an extended deadline.

A taxpayer who files a second return after the due date (whether original or extended) has filed an amended return (i.e., IRS Form 1040-X, Amended U.S. Individual Income Tax Return).

Each year, approximately 20,000 superseding returns are filed on or before extended deadlines. In these situations, which date starts the assessment and refund clocks: the filing date of the first (i.e., original) return, or the date the superseding return was filed? And what if the taxpayer subsequently files an amended return?

Make Sure the Claim for Refunds Are Timely

First, let’s deal with amended returns. This question can easily be disposed of, as the filing of an amended return does not impact the assessment or refund statutes.

Now let’s analyze how a superseding return may affect the time for filing a refund claim. A superseding return corrects the initial return, and those corrections are, in effect, incorporated into and treated as relating back to and modifying the original return. If the superseding return is filed on or before the original due date, it is deemed filed on the last day prescribed for filing. Thus, the periods for the IRS to make an assessment and for the taxpayer to claim a refund will begin to run on the original due date, even if that day falls on a weekend or holiday.

Generally, when a return is filed during an extension period, the return is treated as filed on the day it is received.

So, the question as to which return controls for purposes of filing a refund claim becomes a bit more complex when the taxpayer has filed for an extension, timely files a return, and then, before the extended deadline, files one or two superseding returns correcting the original return.

Spoiler Alert: The IRS’s position is that the original return, not the superseding return filed during the extended period, controls the statutory period both for assessment and for filing a refund claim.

Until this past summer, the IRS was inconsistent in whether it treated the original return or superseding return as the controlling return for statutory assessment and refund purposes when both were filed before an extended due date.

In June 2020, IRS Chief Counsel released advice providing that the original return controlled the statutory periods for assessment and refund. In October 2020, Internal Revenue Manual (IRM) 25.6.1.6.15, When a Document Is Treated As Filed Under the IRC, was updated to reflect the IRS’s change of position, providing that “neither the ASED (Assessment Statute of Expiration Date) nor the RSED (Refund Statute of Expiration Date) should be reset by the filing of a superseding return during the period of extension to file a return.” So even though a superseding return is considered “the return” for many reasons, it is still viewed as supplementing an already-filed return for purposes of statutes of limitation.

In Light of This Change, the First Valid Return Filed After the Prescribed Due Date but Before an Extended Due Date Controls the Period for Assessment and Timely Filed Refund Claim

Let’s consider an example where a taxpayer received an extension to file his 2018 tax return until October 15, 2019. On September 20, 2019, he timely files an original return, and then files a timely superseding return on October 15, 2019. Under the new Chief Counsel advice and IRM, the original return filed on September 20, 2019, would start both the assessment and refund claims periods, provided the return was valid.

An invalid return — for example, one missing a signature — would not begin the statutory periods.

Note: a return is deemed invalid if it is missing one of the following four elements:

- the information on the return is sufficient for the IRS to calculate the tax liability.

- the filed document purports to be a tax return.

- the return makes an honest and reasonable attempt to comply with the tax laws; and

- the taxpayer executes the return under penalties of perjury.

The validity of such returns is considered under the facts and circumstances and may prove essential to determining statutory deadlines going forward.

Part Two: The “Look-back” Rule Limits the Amount of Refund Paid

A word of caution. When a taxpayer relies on the three-year period under IRC § 6511(a) for filing a refund claim, the refund is limited or prohibited by the “look-back” rule, even when a refund claim is timely filed. The look-back rule can be confusing. Where the taxpayer relies on the three-year period under IRC § 6511(b)(2)(A), the amount that can be refunded to the taxpayer is limited to the tax paid during the three-year period immediately preceding filing the claim, plus any extension of time for filing the return. If the taxpayer relies on the two-year period under IRC § 6511(a) (that is, two years after the tax is paid), the refund is limited to the tax paid within two years from the filing of the claim. There are additional complexities when the taxpayer agrees to extend the statute. An upcoming blog will explore this issue in greater depth.

So, What Does This All Mean?

The statutory deadlines for the IRS to assess a tax liability and for a taxpayer to claim a refund are two of the most important time periods for taxpayers to consider. Once these periods have passed, the tax year, in most circumstances, is closed from both the IRS’s and taxpayer’s positions. Therefore, knowing the controlling date for when these will occur is critical.

I urge taxpayers who filed superseding returns to pay close attention to how the IRS’s recent change regarding superseding returns affects these time periods for assessment and filing a refund claim, and how the look-back rule may impact your particular circumstances.

Issue 17: IRS Suspends Requirement to Repay Excess Advance Payments of the 2020 Premium Tax Credit

Taxpayers with excess advance payments of the Premium Tax Credit (excess APTC) for 2020 are not required to file Form 8962, Premium Tax Credit, or report an excess APTC repayment on their 2020 Form 1040 or Form 1040-SR, Schedule 2, Line 2, when they file. The American Rescue Plan Act of 2021 suspends the requirement that taxpayers increase their tax liability by all or a portion of their excess advance payments of the Premium Tax Credit (PTC) for tax year 2020. The process remains unchanged for taxpayers claiming a net PTC for 2020. They must file Form 8962 when they file their 2020 tax return. Taxpayers who have already filed their 2020 tax return and who have excess APTC for 2020 don’t need to file an amended tax return or contact the IRS. The IRS will reduce the excess APTC repayment amount to zero with no further action needed by the taxpayer.

Issue 18: Permanent Address not Required to Receive Economic Impact Payment

The IRS continues its efforts to help those experiencing homelessness during the pandemic by reminding people who don’t have a permanent address or a bank account that they may still qualify for Economic Impact Payments (EIP) and other tax benefits.

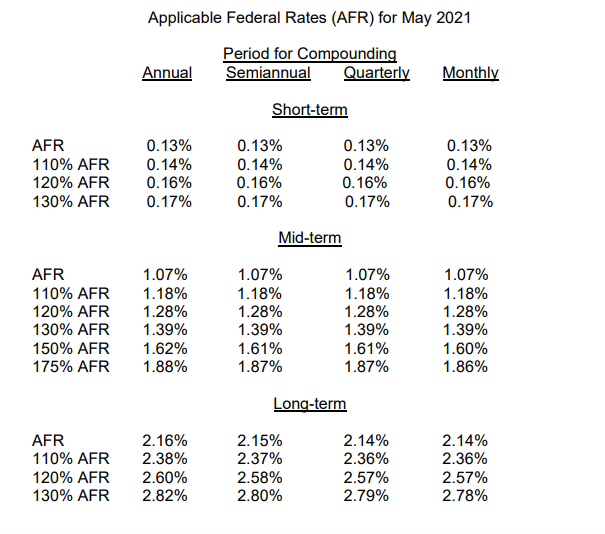

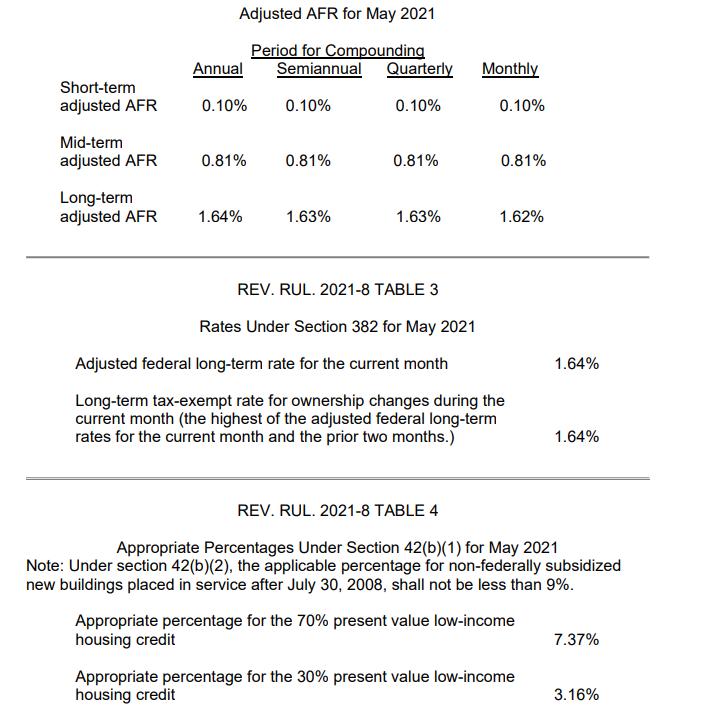

Issue 19: Applicable Federal Rates for May 2021, Rev. Rul. 2021-08

REV. RUL. 2021-8 TABLE

REV. RUL. 2021-8 TABLE 5

Rate Under Section 7520 for May 2021

Applicable federal rate for determining the present value of an annuity, an interest in life or a term of years, or a remainder or reversionary interest 1.2%.