In this Issue:

- IRS Announces Withdrawal Process for Employee Retention Credit Claims

- Proposed Regulations for R&D Credit Coming

- Requesting § 6103 Information from OPR

- FinCEN Requests Comments on Beneficial Ownership Information Reporting Deadline Extension Notice of Proposed Rulemaking

- IRS Extends Relief to Farmers and Ranchers in 49 states, Other Areas Impacted by Drought; More Time to Replace Livestock

- Guidance on New Energy Efficient Home Credit

- Tax Prep Companies Facing FTC Penalties

- IRS Delivers New Capabilities to Tax Pro Account

- The Innocent Spouse Program Needs Improved Guidance for Employees and Increased Communication with Taxpayers – Final Audit Report issued on October 2, 2023, Report Number 2024-300-001

- IRS Warns Taxpayers of Improper Art Donation Deduction Promotions; Highlights Common Red Flags

- IRS Issues Guidance for the Transfer of Clean Vehicle Credits and Updates Frequently Asked Questions

- Social Security Announces 3.2 Percent Benefit Increase for 2024

- IRS Updates Tax Gap Projections for 2020, 2021; Projected Annual Gap Rises to $688 billion

- IRS advances Innovative Direct File Project for 2024 Tax Season; Free IRS-run Pilot Option Projected to be Available for Eligible Taxpayers in 13 States

- IRS Chatbots Help Taxpayers with Key Notices – IR-2023-178

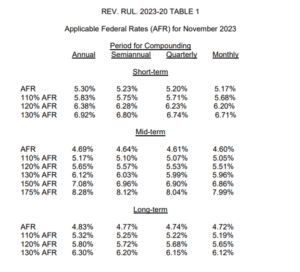

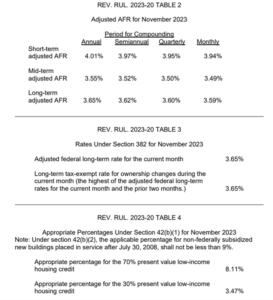

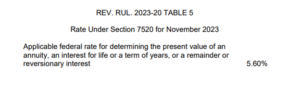

- Applicable Federal Rates for November 2023, Rev. Rul. 2023- 20

Issue 1: IRS Announces Withdrawal Process for Employee Retention Credit Claims – Special Initiative Aimed at Helping Businesses Concerned About an Ineligible Claim Amid Aggressive Marketing Scams

As part of a larger effort to protect small businesses and organizations from scams, the Internal Revenue Service announced the details of a special withdrawal process to help those who filed an Employee Retention Credit (ERC) claim and are concerned about its accuracy.

This new withdrawal option allows certain employers that filed an ERC claim but have not yet received a refund to withdraw their submission and avoid future repayment, interest, and penalties. Employers that submitted an ERC claim that’s still being processed can withdraw their claim and avoid the possibility of getting a refund for which they are ineligible.

The IRS created the withdrawal option to help small business owners and others who were pressured or misled by ERC marketers or promoters into filing ineligible claims. Claims that are withdrawn will be treated as if they were never filed. The IRS will not impose penalties or interest.

Those who willfully filed a fraudulent claim, or those who assisted or conspired in such conduct, should be aware that withdrawing a fraudulent claim will not exempt them from potential criminal investigation and prosecution.

When properly claimed, the ERC – also referred to as the Employee Retention Tax Credit or ERTC – is a refundable tax credit designed for businesses that continued paying employees during the COVID-19 pandemic while their business operations were fully or partially suspended due to a government order, or they had a significant decline in gross receipts during the eligibility periods. The credit is not available to individuals.

The ERC is a complex credit with precise requirements to help businesses during the pandemic, and since mid-September, the IRS has received approximately 3.6 million claims for the credit over the course of the program.

In July, the IRS said it was shifting its focus to review ERC claims for compliance concerns, including intensifying audit work and criminal investigations on promoters and businesses filing dubious claims. The IRS has hundreds of criminal cases being worked, and thousands of ERC claims have been referred for audit.

The new withdrawal process follows the Sept. 14 announcement of an immediate moratorium on processing new ERC claims. The moratorium, which will last until at least the end of this year, follows a flood of ineligible ERC claims. Payouts for claims submitted before Sept. 14 will continue during the moratorium period but at a slower pace due to more detailed compliance reviews. With stricter compliance reviews in place, existing ERC claims will go from a standard processing goal of 90 days to 180 days – and much longer if the claim faces further review or audit. The IRS may also seek additional documentation from the taxpayer to ensure the claim is legitimate.

Enhanced compliance reviews of existing claims submitted before the moratorium is critical to protect against fraud but also to protect businesses and organizations from facing penalties or interest payments stemming from bad claims pushed by promoters.

The IRS continues to warn taxpayers to use extreme caution before applying for the ERC as aggressive maneuvers continue by marketers and scammers.

The IRS is also working on guidance to help employers that were misled into claiming the ERC and have already received the payment. More details will be available this fall.

Who can ask to withdraw an ERC claim?

Employers can use the ERC claim withdrawal process if of all the following apply:

- They made the claim on an adjusted employment return (Forms 941-X, 943-X, 944-X, CT-1X).

- They filed the adjusted return only to claim the ERC, and they made no other adjustments.

- They want to withdraw the entire amount of their ERC claim.

- The IRS has not paid their claim, or the IRS has paid the claim, but they haven’t cashed or deposited the refund check.

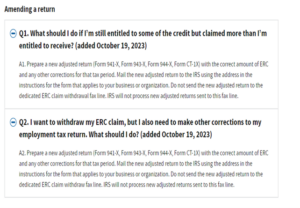

Taxpayers who are not eligible to use the withdrawal process can reduce or eliminate their ERC claim by filing an amended return. For details, see the Correcting an ERC claim – Amending a return section of the frequently asked questions about the ERC.

How to withdraw an ERC claim

To take advantage of the claim withdrawal procedure, taxpayers should carefully follow the special instructions at IRS.gov/withdrawmyERC, summarized below.

- Taxpayers whose professional payroll company filed their ERC claim should consult with the payroll company. The payroll company may need to submit the withdrawal request for the taxpayer, depending on whether the taxpayer’s ERC claim was filed individually or batched with others.

- Taxpayers who filed their ERC claims themselves, haven’t received, cashed, or deposited a refund check and have not been notified their claim is under audit should fax withdrawal requests to the IRS. The IRS has set up a special fax line to receive withdrawal requests. This enables the agency to stop processing before the refund is approved. Taxpayers who are unable to fax their withdrawal can mail their request, but this will take longer for the IRS to receive.

- Employers who have been notified they are under audit can send the withdrawal request to the assigned examiner or respond to the audit notice if no examiner has been assigned.

Those who received a refund check, but haven’t cashed or deposited it, can still withdraw their claim. They should mail the voided check with their withdrawal request using the instructions at IRS.gov/withdrawmyERC.

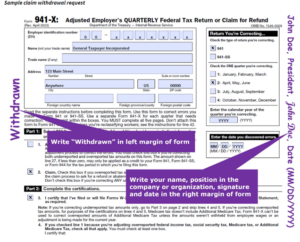

Section A: The has not received a refund and has not been notified the claim is under audit.

If you filed an adjusted return (Form 941-X, 943-X, 944-X, CT-1X) to claim the ERC and you would like to withdraw your entire claim, use the process below. If you filed adjusted returns for more than one tax period, you must follow the steps below for each tax period for which you are requesting a withdrawal.

To request a withdrawal, follow these steps:

- Make a copy of the adjusted return with the claim you wish to withdraw.

- In the left margin of the first page, write “Withdrawn.”

- In the right margin of the first page:

- Have an authorized person sign and date

- Write their name and title next to their signature.

4. Fax the signed copy of your return using your computer or mobile device to the IRS’s ERC claim withdrawal fax line at 855-738-7609. This is your withdrawal request. Keep your copy with your tax records.

If you cannot fax your withdrawal request, you can mail it to the address in the instructions for the adjusted return that applies to your business or organization. Before doing so you should make a copy of the signed and dated first page to keep for your records. It will take longer for the IRS to receive your request if you mail it. Track your package to confirm delivery.

Upcoming webinar and other resources for help

Tax professionals and others can register for a Nov. 2 IRS webinar, Employee Retention Credit: Latest information on the moratorium and options for withdrawing or correcting previously filed claims. Those who cannot attend can view a recording later.

The IRS unveiled a new question and answer checklist last month to help taxpayers understand if they’re eligible for the credit. Since then, the IRS evolved the checklist into an interactive IRS.gov feature to help employers – and the tax professionals working with them – check potential ERC eligibility.

New approach from scammers

Marketers and scammers have already revised their ERC pitches following the Sept. 14 moratorium announcement. Some are pushing employers who submit an ERC claim into agreeing to costly up-front loans in anticipation of a refund.

Issue 2: Proposed Regulations for R&D Credit Coming

An IRS and Treasury Department notice announced that they intend to issue proposed regulations addressing changes made to the treatment of specified research or experimental expenditures (SRE) under the 2017 Tax Cuts and Jobs Act. Notice 2023-63 says the proposed regulations will address changes to §174 that include requiring taxpayers to charge SRE expenditures to a capital account and amortize them over five years (15 if research performed outside of the U.S.).

The notice includes rules on:

- Capitalization and amortization of SRE expenses

- Treatment of SRE expenditures under §460

- Applying §482 to cost sharing arrangements involving SRE expenses.

IRS and Treasury also intend to provide procedures for taxpayers to obtain the automatic consent to changes in accounting method necessary to comply with the notice. Until then, taxpayers may rely on §7.02 of Rev. Proc. 2023-24 to change their methods of accounting under §174 to comply with the notice.

Issue 3: Requesting § 6103 Information from OPR

The Office of Professional Responsibility (OPR) is responsible for all matters relating to the regulation of individuals’ practice before the IRS under 31 CFR Subtitle A, Part 10 (Circular 230, Regulations Governing Practice before the Internal Revenue Service). Having exclusive responsibility for discipline imposed on “practitioners” (including appraisers), the OPR’s jurisdiction encompasses instituting disciplinary proceedings and pursuing sanctions (e.g., censures, suspensions or disbarments from practice, and appraiser disqualifications).

In carrying out these responsibilities, OPR works with other IRS business units to safeguard confidential taxpayer information from unauthorized disclosure. Information in the OPR’s case files includes information pertaining to practitioners who are the subjects of referrals to the OPR for possible misconduct.

The OPR has created a standard § 6103 information-request letter (accessible at irs.gov on News and Guidance from OPR) for practitioners and their representatives to use to request tax information maintained in OPR case files and obtained as part of an inquiry into possible violations of the regulations governing practice before the IRS (Circular 230).

The letter functions as a request under section 6013 of the Internal Revenue Code for access to tax returns and related tax information. A practitioner, or an authorized representative on a practitioner’s behalf, can use the letter to request copies of (1) the practitioner’s own tax information; (2) relevant tax information of other taxpayers, such as clients or former clients of the practitioner; or (3) both the practitioner’s own tax information and the tax information of third parties, depending on the case.

The section 6103 information-request letter is based on certain provisions of the statute, which vary in their coverage:

▪ § 6103(e)(1) and (7) provides a method for a practitioner, in their status as a taxpayer, to obtain disclosure of the practitioner’s tax information contained in the case file associated with the practitioner. More specifically, the provisions authorize a taxpayer, through a written request, to inspect and receive the taxpayer’s returns filed with the IRS and the taxpayer’s “return information” (defined in § 6103(b)(2)), unless the IRS determines that disclosure of some or all of the return information would seriously impair federal tax administration.

▪ With respect to another taxpayer’s returns and return information, § 6103(l)(4) authorizes disclosure, upon written request, to “any person . . . whose rights are or may be affected by an administrative action or proceeding” under Circular 230.

- Additionally, the same returns and return information may also be disclosed to a “duly authorized legal representative” of the person. Disclosure under this provision is limited only to returns and return information that are or may be “relevant and material” to the action or proceeding under Circular 230. Thus, a practitioner, or a practitioner’s authorized representative may use subsection (l)(4) in a Circular 230 matter or proceeding to request disclosure of relevant third-party tax information.

It is important to note that any information disclosed under § 6103(l)(4) is solely for use in, or to prepare for, the OPR action or proceeding. Any other use or disclosure of the third-party tax data is prohibited. A practitioner or representative who makes an unauthorized disclosure is subject to potential civil and criminal liability. The § 6103 information-request letter includes acknowledgments by the requester(s) of the disclosure restrictions and potential penalties for violations.

The § 6103 information-request letter is distinct from a Freedom of Information Act (FOIA) request. The § 6103 information-request letter generally will be an easier (and quicker) way to obtain the information requested and most often result in greater release of information than a FOIA request.

OPR receives and directly handles § 6103 requests, whereas FOIA requests are received and processed, on a first-in, first-out basis, by Privacy, Governmental Liaison and Disclosure within the IRS, which must coordinate with OPR on the identification and release of records responsive to a FOIA request.

In addition, a § 6103 request is not subject to fees for search and review time or for photocopying that apply to FOIA requests. The most significant difference is that the IRS will not release any third-party tax information in response to a FOIA request, regardless of the relevance and materiality of the information to a pending or prospective action or proceeding that could affect the rights of the practitioner making the request or on whose behalf the request is made. The third-party tax information is required to be withheld under FOIA Exemption 3, in conjunction with § 6103.

Thus, a practitioner or representative’s submission of a FOIA request may be a waste of time and resources, to the extent it is necessary to submit a subsequent § 6103(l)(4) request to obtain all available information relevant to the case. Practitioners should be aware, however, that a § 6103 request submitted to the OPR will only yield responsive documents held by the OPR itself, not documents maintained in files elsewhere in the IRS.

Issue 4: FinCEN Requests Comments on Beneficial Ownership Information Reporting Deadline Extension Notice of Proposed Rulemaking

On September 28, 2023, the Financial Crimes Enforcement Network (FinCEN) published in the Federal Register a Notice of Proposed Rulemaking (NPRM) to extend the reporting deadline for certain filers of Beneficial Ownership Information Reports (BOIRs).

This NPRM proposes to extend the deadline to file BOIRs for certain entities created or registered to do business in the United States on or after January 1, 2024, and before January 1, 2025, from 30 to 90 days. No other changes to the reporting deadlines would be made, including for entities created or registered before January 1, 2024, or on or after January 1, 2025.

FinCEN believes the proposed extension will give reporting companies created or registered in 2024 additional time to understand their regulatory obligations, obtain the required information, and become familiar with FinCEN’s guidance and educational materials located at www.fincen.gov/boi.

News Release: https://www.fincen.gov/news/news-releases/fincen-issues-notice-proposed-rulemaking-extend-deadline-certain-companies-file

Federal Register Notice: https://www.federalregister.gov/public-inspection/2023-21226/beneficial-ownership-information-reporting-deadline-extension-for-reporting-companies-created-or

Issue 5: IRS Extends Relief to Farmers and Ranchers in 49 states, Other Areas Impacted by Drought; More Time to Replace Livestock

The Internal Revenue Service reminds eligible farmers and ranchers forced to sell livestock due to drought may have an extended period of time in which to replace the livestock and defer tax on any gains from the forced sales.

The IRS posted Notice 2023-67 listing the applicable areas, a county or other jurisdiction, designated as eligible for federal assistance on IRS.gov. This includes 49 states, the District of Columbia, two U.S. Territories and two independent nations in a Compact of Free Association with the United States.

The relief generally applies to capital gains realized by eligible farmers and ranchers on sales of livestock held for draft, dairy or breeding purposes. Sales of other livestock, such as those raised for slaughter or held for sporting purposes, or poultry, are not eligible.

The sales must be solely due to drought, causing an area to be designated as eligible for federal assistance. Livestock generally must be replaced within a four-year period, instead of the usual two-year period. The IRS is authorized to further extend this replacement period if the drought continues.

The one-year extension, announced in the notice, gives eligible farmers and ranchers until the end of their first tax year after the first drought-free year to replace the sold livestock. Details, including an example of how this provision works, can be found in Notice 2006-82.

The IRS provides this extension to eligible farmers and ranchers that qualified for the four-year replacement period, if the applicable region is listed as suffering exceptional, extreme or severe drought conditions during any week between Sept. 1, 2022, and Aug. 31, 2023. This determination is made by the National Drought Mitigation Center.

As a result, eligible farmers and ranchers whose drought-sale replacement period was scheduled to expire on December 31, 2023, in most cases, now have until the end of their next tax year to replace the sold livestock. Because the normal drought-sale replacement period is four years, this extension impacts drought sales that occurred during 2019. The replacement periods for some drought sales before 2019 are also affected due to previous drought-related extensions affecting some of these localities.

Issue 6: Guidance on New Energy Efficient Home Credit

Notice 2023-65 provides guidance on the new energy efficient home credit under § 45L of the Internal Revenue Code (§ 45L credit), as amended by the Inflation Reduction Act of 2022.

The § 45L credit is allowed to an eligible contractor that constructs a qualified new energy efficient home (qualified home) that is acquired by a person from the eligible contractor for use as a residence during the taxable year. A qualified home is a dwelling unit located in the United States, the construction of which is substantially completed after August 8, 2005, that meets the energy saving requirements of § 45L(c). The applicable amount of the credit is contingent on which set of energy saving requirements the dwelling unit meets, and is $500, $1,000, $2,500, or $5,000.

For certain dwelling units that meet the prevailing wage requirements of § 45L(g), the $500 amount is increased to $2,500 and the $1,000 amount is increased to $5,000. The energy saving requirements of § 45L(c) incorporate certain Energy Star program requirements (available on an Environmental Protection Agency (EPA) webpage) and certain zero energy ready home program requirements (available on a Department of Energy (DOE) webpage).

Issue 7: Tax Prep Companies Facing FTC Penalties

The Federal Trade Commission (FTC) has notified five tax preparation companies that they could face civil penalties if they use or disclose confidential data for unrelated purposes without obtaining the taxpayer’s consent. In July it was reported that several of the country’s largest online tax-prep companies had been sharing sensitive customer financial data with tech companies like Meta and Google for targeted advertisements.

The companies that received FTC notifications of possible penalty offenses concerning the misuse of confidential information were:

- H&R Block Inc.

- Intuit Inc.

- TaxAct Inc.

- TaxSlayer LLC

- The Lampo Group LLC (d/b/a Ramsey Solutions)

By sending these notices, the FTC is warning the companies that they could incur civil penalties of up to $50,120 per violation if they misuse personal data in ways that run counter to the original purpose for which it was collected. The commission specifically warned the companies that it considers the transfer of personal information without first obtaining the consumers’ express consent to be an unfair or deceptive practice.

Issue 8: IRS Delivers New Capabilities to Tax Pro Account; Latest Expansion Part of Effort to Improve Technology, Tools to Help Tax Professionals Serve Clients

As part of a larger effort to improve technology, the Internal Revenue Service announced today an expansion of the Tax Pro Account capabilities that allows tax professionals access to new services to help their clients.

New additions to Tax Pro Account, available through IRS.gov, will help practitioners manage their active client authorizations on file with the Centralized Authorization File (CAF) database. Other enhancements will allow tax professionals to view their client’s tax information, including balance due amounts. Tax Pro Account users can now also withdraw from their active authorizations online in real time.

These changes reflect ongoing transformation efforts made possible under the Inflation Reduction Act. Tax professionals are a critical part of the nation’s tax system, and the new IRS Strategic Operating Plan highlights the need to improve technology and services for taxpayers as well as tax professionals.

The new enhancements continue IRS efforts to improve the third-party authorization process. The IRS also continues to work on additional expansions to improve services to taxpayers and their tax professionals.

Tax Pro Account continues expanding with new features.

Tax Pro Account provides tax professionals with a digital self-service portal they can rely on to manage their authorization relationship with taxpayers and view the taxpayers’ information.

With the recent enhancements, tax professionals can now use Tax Pro Account to send Power of Attorney (POA) and Tax Information Authorization (TIA) requests directly to a taxpayer’s individual IRS Online Account. Upon the taxpayer’s approval and validation of the information, the authorization records immediately to the CAF database, which avoids faxing, mailing, uploading and long review and processing time by the CAF Unit.

Tax professionals must have a CAF number to use a Tax Pro Account; a CAF number cannot be requested through the Tax Pro Account. Currently, the digital authorization process is available only for individual taxpayers, not businesses or other entities.

More than 260,000 people have used Tax Pro Account since it launched in July 2021. The webpage has been viewed over 2.7 million times.

The future of Tax Pro Account

The IRS is committed to improving and expanding Tax Pro Account capabilities and engaging with the tax professional community as these efforts progress. This partnership will enhance the authorization request process and provide tax professionals with the tools they need to access relevant taxpayer information and the ability to address relevant tax-related issues for their clients quickly.

Issue 9: The Innocent Spouse Program Needs Improved Guidance for Employees and Increased Communication with Taxpayers – Final Audit Report issued on October 2, 2023, Report Number 2024-300-001

Why TIGTA Did This Audit?

This audit was initiated to assess whether the Innocent Spouse Program is effectively working claims in accordance with § 6015, including whether the IRS is protecting taxpayer rights when evaluating innocent spouse claims.

Impact on Tax Administration.

When married taxpayers elect to file a joint income tax return, they are held jointly and individually responsible for the tax, interest, or penalties due on the joint return, even if they later separate or divorce (i.e., one spouse can be held responsible for payment of all the tax due). This means that the IRS may look to either spouse or both spouses for the payment of the tax liability, regardless of who earned the income. Because joint and several liability may result in inequitable treatment to one spouse, § 6015 provides an exception to joint and several liability. § 6015 provides three types of relief from joint and several liability to spouses who filed a joint return: § 6015(b) Innocent Spouse Relief; § 6015(c) Separation of Liability; and § 6015(f) Equitable Relief. Taxpayers residing in “community property” States can request innocent spouse under I.R.C. § 66(c), Treatment of Community Income

What TIGTA Found.

The IRS could improve guidance for IRS employees working innocent spouse claims. TIGTA reviewed a statistical sample of 45 innocent spouse claims and determined that IRS employees in the Cincinnati Centralized Innocent Spouse Operations did not fully develop the facts and circumstances in 10 (22 %) of the claims. Further development of the facts and circumstances in nine of the 10 claims could have resulted in a change of determination.

The IRS disagreed or partially disagreed with six of the 10 exceptions, but in five instances, the IRS agreed that at least one factor was inadequately developed. A lack of specificity in Internal Revenue Manual sections related to equitable relief may have contributed to examiner subjectivity in equitable relief determinations.

Also, final determination letters did not fully inform taxpayers of IRS decisions about their tax accounts. The IRS also failed to take actions in certain situations to suspend only the requesting spouse’s Collection Statute Expiration Date rather than suspending it for both the requesting spouse and the non-requesting spouse.

Further, tax liabilities are not always collected due to freeze codes remaining on the account after the claim is closed, making the account uncollectible. Prior to the Coronavirus Disease 2019 (COVID-19) pandemic, innocent spouse claims already exceeded the IRS’s 240-day closure goal, taking approximately one year to close. However, after COVID-19 pandemic restrictions, the IRS took an average of 557 days (over 18 months) to close innocent spouse claims.

According to IRS management, these extended closure times were the result of staffing shortages and pandemic-related decisions to temporarily suspend enforcement activity; however, the IRS has not performed any analysis on the root cause of the extended claim closures.

What TIGTA Recommended/

TIGTA made seven recommendations intended to improve guidance, communication, and the processing of innocent spouse claims to help protect taxpayer rights. In addition, TIGTA recommended monitoring and, if deemed necessary, conducting an analysis of the timeliness of working innocent spouse claims and ensuring that the freeze code is removed after the claim is closed.

The IRS agreed with three of our recommendations and plans to issue employee reminders regarding innocent spouse freeze codes and the Collection Statute Expiration Date for non-requesting spouses and to analyze cycle times. The IRS partially agreed with one recommendation and plans to update the Internal Revenue Manual but will not offer additional training to employees. The IRS also disagreed with three recommendations to make changes to employee reviews, final determination letters, and the mirroring policy that would have improved the administration of the Innocent Spouse Program.

Issue 10: IRS Warns Taxpayers of Improper Art Donation Deduction Promotions; Highlights Common Red Flags

The Internal Revenue Service is warning taxpayers to watch for promotions involving exaggerated art donation deductions that can target high-income filers and offered special tips for people to use to avoid getting caught in a scheme.

There are ways for taxpayers to properly claim donations of art. But some unscrupulous promoters may use direct solicitation to promise values of art that are too good to be true. These promoters persuade taxpayers, usually high-income taxpayers, to purchase the art, wait to donate the art and then take an incorrect deduction for the art donated. As part of a larger effort to increase compliance work on high-income individuals and corporations, and protect taxpayers from scams, the IRS has active promoter investigations and taxpayer audits underway in this area.

The IRS is using a variety of compliance tools to combat abusive art donations through audits of tax returns and civil penalty investigations. The IRS reminds taxpayers, including high-income filers that may be targets of these schemes, to watch out for aggressive promotions. In addition, following Inflation Reduction Act funding, the IRS is focused on increasing compliance efforts on high-income and high-wealth individuals to ensure filers pay the right amount of tax owed.

How the scheme works

Promoters encourage taxpayers to buy various types of art, often at a “discounted” price. This price may also include additional services from the promoter, such as storage, shipping and arranging the appraisal and donation of the art. The promotor promises the art is worth significantly more than the purchase price.

These schemes are designed to encourage purchasers to donate the art after waiting at least one year and to claim a tax deduction for an inflated fair market value, which is substantially more than they paid for the artwork. Promoters may suggest taxpayers donate art annually and allow them to buy a quantity of art that guarantees a specific deductible amount. Promoters may even arrange for certain charities to take the donations.

IRS conducting promoter investigations, taxpayer audits involving art donations

As the IRS works to increase compliance activity involving high-income and high-wealth areas as well as complex partnerships and corporations, abusive schemes like art donations are on the agency’s radar.

The IRS has multiple active abusive art donation promoter investigations underway and questionable art donations by taxpayers have been – and will continue to be — under audit when questions arise. These donations can involve art valued at millions of dollars. More than 60 taxpayer audits have been completed with more in the works; those audits that have produced more than $5 million in additional tax.

Watch for red flags

Taxpayers should be wary of buying multiple works by the same artist that have little to no market value outside of what the promoter might be advertising.

Another red flag in this scheme is that promoters might line up specific appraisers for participants to use. An appraisal that supports this scheme often fails to adequately describe the art. It may not address the value characteristics, such as rarity, age, quality, condition, stature of the artist, price paid, and the quantity purchased.

Taxpayers should remember they are always responsible for the accuracy of information reported on their tax return. Participating in an illegal scheme to avoid paying taxes can result in repayments of the taxes owed with penalties and interest and potentially even fines and imprisonment. Charities also need to be careful they don’t knowingly enable these schemes.

Properly claiming an art donation

To properly claim a charitable contribution deduction for an art donation, a taxpayer must keep records to prove:

- Name and address of the charitable organization that received the art.

- Date and location of the contribution.

- Detailed description of the donated art.

The above items are required to properly claim a charitable contribution deduction. There are additional requirements based on the value of the claimed deduction. If the claimed deduction for an art donation is:

- $250 or more, the taxpayer must obtain a contemporaneous written acknowledgement of the contribution from the charitable organization. They need to have that document on or before the earlier of the date on which they file a return for the taxable year in which they made the contribution, or the due date, including extensions, for filing such return.

- More than $500 but not over $5,000, the taxpayer must also complete a Form 8283, Noncash Charitable Contribution, Section A, and attach it to their tax return.

- More than $5,000, the taxpayer must complete Form 8283, Section B, including signatures of qualified appraiser and donee. They must also obtain a qualified written appraisal of the donated property.

- $20,000 or more, the taxpayer must do all the above and attach a complete copy of the qualified appraisal to their return. They should also have a high-resolution photo or digital image of the object and provide it, if asked.

IRS Art Appraisal Services (AAS)

The IRS has a team of professionally trained Appraisers in Art Appraisal Services who provide assistance and advice to the IRS and taxpayers on valuation questions in connection with personal property and works of art.

Although organized under the IRS Independent Office of Appeals, Art Appraisal Services assists IRS’ examination function, lawyers from the IRS Office of Chief Counsel and the Department of Justice, as well as Appeals Officers, on the valuation of personal property and works of art.

In certain cases, the Art Appraisal Service is advised by the Commissioner’s Art Advisory Panel. The panel is comprised of up to 25 renowned art experts who serve without compensation and provide advisory opinions. IRS Appraisers, the Director of Art Appraisal Services, and panel members meet regularly to discuss the valuation of art works submitted for review by Art Appraisal Services.

How to report tax schemes

Taxpayers can report tax-related illegal activities relating to charitable contributions of art using:

- Form 14242, Report Suspected Abusive Tax Promotions or Preparers, to report a suspected abusive tax avoidance scheme and tax return preparers who promote such schemes.

- They should also report fraud to the Treasury Inspector General for Tax Administration at 800-366-4484.

Issue 11: IRS Issues Guidance for the Transfer of Clean Vehicle Credits and Updates Frequently Asked Questions

WASHINGTON — The Internal Revenue Service has issued proposed regulations, Revenue Procedure 2023-33 and frequently asked questions for the transfer of new and previously owned clean vehicle credits from the taxpayer to an eligible entity for vehicles placed in service after December 31, 2023.

The Inflation Reduction Act provides taxpayers with credits for qualified new and previously owned clean vehicles acquired and placed in service during the taxable year. Beginning Jan. 1, 2024, in certain situations, taxpayers will be able to transfer the new and previously owned clean vehicle credits to eligible entities.

Today’s guidance clarifies how taxpayers can elect to transfer new and previously owned clean vehicle credits to dealers who are eligible to receive advance payments of either credit. The proposed regulations and revenue procedure also provide guidance for dealers to become eligible entities to receive advance payments of new or previously owned clean vehicle credits.

The proposed regulations also provide guidance for the recapturing of the credit.

The revenue procedure includes procedures for how a dealer would register with the IRS to be eligible to receive the credit transfers from taxpayers and provides details on the registration process through IRS Energy Credits Online.

It also provides procedures for the revocation and suspension of a registration if a dealer fails to comply with the program’s requirements, and for the establishment of an advanced payment program to eligible entities. Finally, the revenue procedure provides new information for the timing and manner of submission of seller reports, as well as providing updated information on submission of written agreements by manufacturers to the IRS to be considered qualified manufacturers and on the method of submission of monthly reports by qualified manufacturers.

As a result of this guidance, the IRS updated the frequently-asked-questions (FAQs) for the clean vehicle credits.

Fact Sheet 2023-22 updates FAQs related to new, previously owned and qualified commercial clean vehicles.

The FAQs revisions are as follows:

- Topic A: Eligibility Rules for the New Clean Vehicle Credit: Updated Questions 1, 2, 4 and 7; added Question 12

- Topic B: Income and Price Limitations for the New Clean Vehicle Credit: Updated Questions 1, 3, 7, 8, 9, 10, and 11

- Topic C: When the New Requirements Apply to the New Clean Vehicle Credit: Updated Question 2

- Topic D: Eligibility Rules for the Previously Owned Clean Vehicles Credit: Updated Questions 1, 2, 3, 7, 9; added Questions 11, 12

- Topic E: Income and Price Limitations for Previously Owned Clean Vehicles: Updated Question 2

- Topic F: Claiming the Previously Owned Clean Vehicles Credit: Updated Questions 2, 3

- Topic G: Qualified Commercial Clean Vehicles Credit: Updated Question 4

- Topic H: Transfer of New Clean Vehicle Credit and Previously Owned Clean Vehicles Credit: Added Questions 1 through 21

- Topic I: Registering a Dealer/Seller for Seller Reporting and Clean Vehicle Tax Credit Transfers: Added Questions 1 through 17

- Topic J: Seller Report Information for Buyers of New and Previously Owned Clean Vehicle Tax Credits Beginning in 2024: Added Questions 1 through 2

These FAQs are being issued to provide general information to taxpayers and tax professionals as expeditiously as possible.

Revenue Procedure 2023-33 sets forth the procedures under §§ 30D(g) and 25E(f) of the Internal Revenue Code for the transfer of the clean vehicle credit or previously owned clean vehicle credit from the taxpayer who elects to transfer such credit to an eligible entity. These procedures will apply to transfers of credits after December 31, 2023. These procedures include registration procedures with the Internal Revenue Service (IRS) for qualified manufacturers and sellers, as well as procedures for dealer registration and the suspension and revocation of that registration.

This revenue procedure also establishes a program to make advance payments of credit amounts to registered dealers. In addition, this revenue procedure supersedes sections 5.01 and 6.03 of Rev. Proc. 2022-42, 2022-52 I.R.B. 565, providing new information for the timing and manner of submission of seller reports, respectively; as well as sections 6.01 and 6.02 of Rev. Proc. 2022-42, providing updated information on submission of written agreements by manufacturers to the IRS to be considered qualified manufacturers, as well as the method of submission of monthly reports by qualified manufacturer.

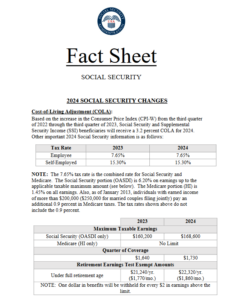

Issue 12: Social Security Announces 3.2 Percent Benefit Increase for 2024

Social Security and Supplemental Security Income (SSI) benefits for more than 71 million Americans will increase 3.2 % in 2024, the Social Security Administration announced today. On average, Social Security retirement benefits will increase by more than $50 per month starting in January.

More than 66 million Social Security beneficiaries will see the 3.2 % cost-of-living adjustment (COLA) beginning in January 2024. Increased payments to approximately 7.5 million people receiving SSI will begin on December 29, 2023. (Note: some people receive both Social Security and SSI benefits).

Some other adjustments that take effect in January of each year are based on the increase in average wages. Based on that increase, the maximum amount of earnings subject to the Social Security tax (taxable maximum) will increase to $168,600 from $160,200.

Social Security begins notifying people about their new benefit amount by mail starting in early December. Individuals who have a personal my Social Security account can view their COLA notice online, which is secure, easy, and faster than receiving a letter in the mail. People can set up text or email alerts when there is a new message–such as their COLA notice–waiting for them in my Social Security.

People will need to have a my Social Security account by November 14 to see their COLA notice online. To get started, visit www.ssa.gov/myaccount.

Information about Medicare changes for 2024 will be available at www.medicare.gov.

https://www.ssa.gov/news/press/factsheets/colafacts2024.pdf

Issue 13: IRS Updates Tax Gap Projections for 2020, 2021; Projected Annual Gap Rises to $688 billion

The Internal Revenue Service has released new tax gap projections for tax years 2020 and 2021 showing the projected gross tax gap increased to $688 billion in tax year 2021, a significant jump from previous estimates.

The new estimate reflects a rise of more than $192 billion from the prior estimates for tax years 2014-2016 and a rise of $138 billion from the revised projections for tax years 2017-2019. This marks the first-year tax gap projections have been provided for single tax years and also marks the beginning of tax gap updates on an annual basis.

Tax gap details: late payments and IRS enforcement generated $63 billion in 2021.

The $688 gross tax gap is the difference between estimated ‘true’ tax liability for a given period and the amount of tax that is paid on time. The gross tax gap covers three key areas – nonfiling of taxes, underreporting of taxes and underpayment of taxes.

The IRS notes that the tax gap estimates and projections cannot fully account for all types of noncompliance. In addition, the projections released today are based largely upon the compliance behavior estimated from the most recent set of completed audits (from tax years 2014-2016). That estimated compliance behavior is projected forward to taxpayers in tax years 2020 and 2021.

Late payments and IRS enforcement efforts are projected to generate an additional $63 billion on tax year 2021 returns, resulting in a projected net tax gap of $625 billion. Between tax years 2014-2016 and tax year 2021, the estimated tax liability increased by about 38 percent, roughly the same increase as the gross and net tax gaps. Much of these increases in tax liability and the tax gap can be attributed to economic growth.

The voluntary compliance rate remains relatively steady.

The tax year 2020 and 2021 tax gap projections translate to about 85% of taxes paid voluntarily and on time, which is in line with recent levels. After IRS compliance efforts are factored in, the projected share of taxes eventually paid is 86.3% for tax year 2021, down slightly from the 87.0% for tax years 2014-2016. This drop in compliance does not factor in any changes in compliance behavior; instead, it is due to changes in the types of income and how that income is reported to the IRS.

The gross tax gap comprises three components:

- Nonfiling, which means tax not paid on time by those who do not file on time:

- $77 billion in tax year 2021, up from $41 billion in tax years 2017-2019.

- Underreporting, which reflects tax understated on timely filed returns.

- $542 billion in tax year 2021, up from $445 billion in tax years 2017-2019.

- Underpayment, or tax that was reported on time, but not paid on time).

- $68 billion in tax year 2021, up from $64 billion in tax years 2017-2019.

With the help of Inflation Reduction Act resources, the IRS will be taking a variety of steps to help improve voluntary compliance by improving taxpayer services and offering new technology tools to work in concert with additional compliance work. In 2022, the latest year for which data is available, the IRS collected more than $4.9 trillion in taxes, penalties, interest, and user fees.

Tax gap studies through the years have consistently demonstrated that third-party reporting of income significantly raises voluntary compliance with the tax laws. And voluntary compliance rises even higher when income payments are also subject to withholding. The IRS also has an array of other taxpayer service programs aimed at supporting accurate tax filing and helping address the tax gap. These range from working with businesses and partner groups to a variety of education and outreach efforts.

The voluntary compliance rate of the U.S. tax system is vitally important for the nation. A one-percentage-point increase in voluntary compliance would bring in about $46 billion in additional tax receipts.

The tax gap estimates provide insight into the historical scale of tax compliance and to the persisting sources of low compliance.

Projecting the tax gap; offshore, digital assets, pandemic credits not fully represented

Given the complexity of the tax system and available data, no single approach can be used for estimating each component of the tax gap. Each approach is subject to measurement or nonsampling error; the component estimates that are based on samples are also subject to sampling error.

For the individual income tax underreporting tax gap, Detection Controlled Estimation is used to adjust for measurement errors that result when some existing noncompliance is not detected during an audit. Other statistical techniques are used to control bias in estimates based on operational audit data. Because multiple methods are used to estimate different subcomponents of the tax gap and then are projected into future tax years, no standard errors are reported. Those reviewing these projections should be mindful of these limitations.

Given available data, these projections of the tax gap components presented do not represent the full extent of potential non-compliance. There are several factors to keep in mind:

- The projections cannot fully represent noncompliance in some components of the tax system including offshore activities, issues involving digital assets and cryptocurrency as well as corporate income tax, income from flow-through entities and illegal activities because data are lacking.

- Projections rely upon estimates of compliance behavior. No such estimates are available for pandemic credits, so there is no reliable method of representing noncompliance for pandemic credits.

- The tax gap associated with illegal activities has been outside the scope of tax gap estimation because the objective of government is to eliminate those activities, which would eliminate any associated tax.

- For noncompliance associated with digital assets and other emerging issues, it takes time to develop the expertise to uncover associated noncompliance and for examinations to be completed that can be used to measure the extent of that noncompliance.

The IRS continues to actively work on new methods for estimating and projecting the tax gap to better reflect changes in taxpayer behavior as they emerge.

Issue 14: IRS advances Innovative Direct File Project for 2024 Tax Season; Free IRS-run Pilot Option Projected to be Available for Eligible Taxpayers in 13 States

As part of larger transformation efforts underway, the Internal Revenue Service announced key details about the Direct File pilot for the 2024 filing season with several states planning to join the innovative effort.

The IRS will conduct a limited-scope pilot during the 2024 tax season to further assess customer support and technology needs. It will also provide a platform for the IRS to evaluate successful solutions for potential operational challenges identified in the report the IRS submitted to Congress earlier this year.

Arizona, California, Massachusetts and New York have decided to work with the IRS to integrate their state taxes into the Direct File pilot for filing season 2024. Taxpayers in nine other states without an income tax – Alaska, Florida, New Hampshire, Nevada, South Dakota, Tennessee, Texas, Washington and Wyoming — may also be eligible to participate in the pilot. Washington has also chosen to join the integration effort for the state’s application of the Working Families Tax Credit. All states were invited to join the pilot, but not all states were in a position to join the pilot at this time.

People in those 13 states may be eligible to participate in the 2024 Direct File pilot, a new service that will provide taxpayers with the choice to electronically file their federal tax return directly with the IRS for free.

Taxpayer eligibility to participate in the pilot will be limited by the state in which the taxpayer resides and will be limited to taxpayers with certain types of income, credits and deductions – taxpayers with relatively simple returns. The IRS announced it anticipates specific income types, such as wages on a Form W-2, and important tax credits, like the Earned Income Tax Credit and the Child Tax Credit, will be covered by the Direct File pilot.

The 2022 Inflation Reduction Act provided the IRS with long-term funding for the agency to transform its operations and improve taxpayer service, enforcement, and technology. It also directed the IRS to study the possibility of a free, direct e-file program, which the IRS submitted in a report to Congress in May 2023. Projects like Direct File represent a goal of the IRS Strategic Operating Plan, to give taxpayers choices in how they interact with the tax agency. This includes choices in how they prepare and file their taxes, whether it’s through a tax professional, commercial tax software or free filing options. Direct File is one more potential option from which qualifying taxpayers will be able to choose to file a 2023 federal tax return during the 2024 filing season.

Since the delivery of the Direct File report in May – as directed by the Treasury Department – the IRS has been working to develop a pilot for the upcoming filing season, paying special attention to issues identified in the report related to customer support and state taxes. This limited-scale pilot will allow the IRS to evaluate the costs, benefits and operational challenges associated with providing a voluntary Direct File option to taxpayers.

Direct File pilot basics

Eligible taxpayers may choose to participate in the pilot next year to file their tax year 2023 federal tax return for free, directly with the IRS.

Direct File will be a mobile-friendly, interview-based service that will work as well on a mobile phone as it does on a laptop, tablet or desktop computer. The service will be available in English and Spanish for the pilot.

The Direct File pilot will be a limited, phased pilot. It will not be available to all eligible taxpayers when the IRS begins accepting tax returns. Because the IRS wants to make sure the program works effectively, Direct File will first be introduced to a small group of eligible taxpayers in filing season 2024. As the filing season progresses, more and more eligible taxpayers will be able to access the service to file their 2023 tax returns.

Direct File does not replace existing filing options like tax professionals, Free File, free return preparation sites, commercial software and authorized e-file providers. Taxpayers will continue to have choices, whether they want to use a tax professional, a software product, Free File, free tax preparation services like Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE) as well as a paper tax return or Direct File.

Taxpayers participating in the pilot will have access to help by IRS employees staffing the Direct File customer support function. IRS customer service representatives will provide technical support and provide basic clarification of tax law related to the tax scope of Direct File. Questions related to issues other than Direct File will be routed to other IRS customer support, as appropriate.

Pilot eligibility is limited

Eligibility for the pilot is limited by the types of income, tax credits and deductions that the product can initially support. Taxpayers who fall outside the pilot’s eligibility limits will be unable to participate in the pilot in 2024.

Direct File will cover only individual federal tax returns during the pilot. Also, Direct File will not prepare state returns. However, once a federal return is completed and filed, Direct File will guide taxpayers who want to file a state return to a state-supported tool that taxpayers can use to prepare and file a stand-alone state tax return. For the pilot in 2024, where taxpayers may have state or local tax obligations, the IRS will limit eligibility to states that are actively partnering with the IRS on the pilot.

Eligibility to participate in the pilot will be limited to taxpayers who reside in certain states where the pilot is available. Taxpayers in Alaska, Florida, New Hampshire, Nevada, South Dakota, Tennessee, Texas, Washington, and Wyoming may be eligible to participate in the pilot as their states do not levy a state income tax. Washington has also chosen to join the integration effort as a partner for the state’s application of the Working Families Tax Credit. For states that do levy a state income tax, Arizona, California, Massachusetts, and New York have chosen to partner with the IRS for the 2024 Direct File pilot. The IRS anticipates the pilot will be available in those states as well in 2024.

The IRS and the Departments of Revenue in Arizona, California, Massachusetts, New York, and Washington entered into separate Memorandums of Understanding in September for the purposes of collaboration on the IRS’s Direct File pilot for filing season 2024.

This approach will test the IRS’s ability to successfully integrate with a handful of states and the IRS will continue to work with all states to secure feedback and share what it learns through the course of its work on the pilot.

2024 Direct File pilot eligibility expected to cover key income, tax credits.

Eligibility to participate in the 2024 pilot will be limited to reporting only certain types of income and claiming limited credits and adjustments. The tax scope for the pilot is still being finalized and is subject to change, but the IRS currently anticipates it will include:

Income reporting

- W-2 wage income.

- Social Security and railroad retirement income

- Unemployment compensation

- Interest of $1,500 or less

Credits

- Earned Income Tax Credit

- Child Tax Credit

- Credit for Other Dependents

Deductions

- Standard deduction

- Student loan interest

- Educator expenses

Evaluating the Direct File Pilot

The purpose of the Direct File pilot is to test the system the IRS has developed and to learn from that test. This includes testing the technology, customer support, state integration, fraud detection and the overall taxpayer experience. The best way to test a new service offering such as Direct File is in a limited, controlled environment that will allow the IRS to identify issues and make changes prior to any potential large-scale launch in the future.

The 2024 filing season serves as a pilot for Direct File, and the purpose is to learn about the Direct File service itself and the needs of taxpayers who use it. By starting with a pilot, the IRS can efficiently learn about Direct File’s effectiveness, identify areas of improvement for future iterations and ensure it meets the needs of taxpayers who want to use it.

Issue 15: IRS Chatbots Help Taxpayers with Key Notices – IR-2023-178

The IRS has expanded its use of chatbots to assist taxpayers who receive under-reporter, according to a September 26 Information Release. The new chatbots will help taxpayers who receive specific notices (CP2000, CP2501, and CP3219A) that their reported income doesn’t match the information the IRS received from third parties.

The new chatbots, which simulate human interaction with taxpayers through a web or mobile app on a computer or mobile screen, respond to taxpayer questions or requests about a notice they received. These chatbots will be able to answer questions such as:

- What a taxpayer should do if they receive a notice.

- What they should do if they need more time to respond to a notice.

- How to find out if the IRS received their response to a notice.

At the end of the conversation, or if the chatbot has not been able to help, the taxpayer can press the representative button in the chat box to speak to a live assistor.

The IRS plans to continue adding bot technology features in the future to assist taxpayers with more complex issues.

Issue 16: Applicable Federal Rates for November 2023, Rev. Rul. 2023- 20