Tax Newsletter: IRS Issues Guidance

Reminder: Register for the Virtual Tax Seminars: Each session includes 7 hours of Tax Law and 1 hour of Ethics

Virtual Tax Seminar Information is available here: Fall & Year-End Tax Seminars

In This Issue

- Issue 1: New Mailing Address for Some Western States as Fresno, California, Paper Tax Return Processing Center Closes

- Issue 2: IRS: Cost of Home Testing for Covid-19 is Eligible Medical Expense; Reimbursable Under FSAs, HSAs

- Issue 3: Discussion Draft Concerning the Tax Code Governing Partnership Under Discussion – Not Law – Potential Law Change

- Issue 4: Treasury, IRS Issues Guidance for 2021 on Reporting Qualified Sick and Family Leave Wages

- Issue 5: IRM Change Related to § 754 Election Procedures

- Issue 6: FIRE System Update Coming September 2021

- Issue 7: Bills from the Hill

- Issue 8: TIGTA Report – Effects of the COVID-19 Pandemic on Business Tax Return Processing Operations September 2, 2021, Report Number: 2021-46-064

- Issue 9: Special Per Diem Rates Notice 2021-52

- Issue10: TIGTA Evaluates IRS’s Efforts to Address Underreporting of S Corporation Officer Compensation

- Issue 11: What Employers Need to Know About Repayment of Deferred Payroll Taxes

- Issue 12: Interim Guidance for Initial Contact (IRM 5.1.10.3) – SBSE-05-0421-0018

- Issue 13: CCA 202129009 – §6695A question

- Issue 14: Verifying Identity When Calling IRS – IRS Tax Tip 2021-110

- Issue 15: Security Summit: Tax Pros Should Encourage Clients to Obtain IP PINs to Protect Against Tax-related Identity Theft

- Issue 16: U.S. Census Released 2020 – Income, Poverty and Health Insurance Coverage in the United States

- Issue 17: Fiscal Year 2021 Statutory Audit of Compliance with Legal Guidelines Restricting the Use of Records of Tax Enforcement Results

- Issue 18: Employee Retention Credit – Question from September Webinar

- Issue 19: Applicable Federal Rates for September 2021, Rev. Rul. 2021-18

Issue 1: New Mailing Address for Some Western States as Fresno, California, Paper Tax Return Processing Center Closes

The Internal Revenue Service will close its paper return processing center in Fresno, California, permanently at the end of September this year. Originally announced in 2016, this closure is part of a larger, ongoing efficiency strategy as most taxpayers now file electronically.

The number of individual returns taxpayers filed electronically has grown from 90 million in 2008 to over 145 million in 2020, which is more than 90% of all returns filed. The IRS expects this trend to continue for both individual and non-individual returns.

Where to Send Returns

Taxpayers located in Alaska, California, Hawaii, Ohio and Washington state who previously filed their federal return with Fresno should now mail their returns to the Ogden, Utah, processing center.

The Ogden address for filing paper individual returns is:

Department of Treasury

Internal Revenue Service

Ogden, UT 84201-0002

Fresno Operations

The IRS will maintain a presence in Fresno with many other operations still working at full capacity. When this consolidation was announced in September 2016, there were approximately 3,000 employees employed at the paper processing center in Fresno. Since that time, the IRS has taken steps to provide training and find continued employment opportunities for many of the impacted employees. Others have chosen to retire or separate from the IRS.

Issue 2: IRS: Cost of Home Testing for Covid-19 is Eligible Medical Expense; Reimbursable Under FSAs, HSAs

The cost of home testing for COVID-19 is an eligible medical expense that can be paid or reimbursed under health flexible spending arrangements (health FSAs), health savings accounts (HSAs), health reimbursement arrangements (HRAs), or Archer medical savings accounts (Archer MSAs). That is because the cost to diagnose COVID-19 is an eligible medical expense for tax purposes.

In addition, it was announced earlier that the costs of personal protective equipment, such as masks, hand sanitizer and sanitizing wipes, for the primary purpose of preventing the spread of COVID-19 are eligible medical expenses that can be paid or reimbursed under health FSAs, HSAs, HRAs, or Archer MSAs.

Issue 3: Discussion Draft Concerning the Tax Code Governing Partnership Under Discussion – Not Law – Potential Law Change

Changes would include:

- Mandate basis adjustments under § 734 and 743

for partnership distributions and partnership interest sales.

- Require all partnerships to use the remedial method for §704(c) allocations.

- Require partnerships to apply the partners’-interest-in-the-partnership (PIP) standard when determining partnership allocations, unless a new “consistent percentage method” applies.

- Require corporate tax treatment for all publicly traded partnerships.

- Generally, require partnership liabilities to be allocated based on the partners’ share of partnership profits.

Issue 4: Treasury, IRS Issues Guidance for 2021 on Reporting Qualified Sick and Family Leave Wages

Notice 2021-53, provides guidance to employers about reporting on Form W-2 the amount of qualified sick and family leave wages paid to employees for leave taken in 2021.

The notice provides guidance under recent legislation, including: the Families First Coronavirus Response Act (FFCRA), as amended by the COVID-Related Tax Relief Act of 2020, and the American Rescue Plan Act of 2021.

Employers will be required to report these amounts to employees either on Form W-2, Box 14, or in a separate statement provided with the Form W-2. The guidance provides employers with model language to use as part of the Instructions for Employee for the Form W-2 or on the separate statement provided with the Form W-2.

The wage amount that the notice requires employers to report on Form W-2 will provide employees who are also self-employed with the information necessary to determine the amount of any sick and family leave equivalent credits they may claim in their self-employed capacities.

Notice 2020-54, also provided guidance regarding W-2 reporting of qualified sick leave and family leave under FFCRA for wages paid to employees for leave taken in 2020.

Issue 5: IRM Change Related to § 754 Election Procedures

The memorandum outlines new procedures for use by LB&I and SB/SE employees when determining whether to approve or deny a request filed by a partnership to revoke its election to adjust the basis of partnership property under § 754.

A partnership with an § 754 election in place may revoke such election with the approval of the district director for the internal revenue district in which the partnership return is required to be filed. Review: Reg. § 1.754-1(c).

Districts were abolished with the 2000 IRS restructuring, and the regulations have not been updated to reflect the current IRS organizational structure.

Attached guidance applies to any partnership, whether subject to the unified rules under TEFRA (Tax Equity and Fiscal Responsibility Act of 1982), the centralized audit regime under BBA (Bipartisan Budget Act of 2015), or separate deficiency proceedings (ILSC – Individual Level Statute Control).

Guidance is based on a new process and new procedure where there is no related IRM section. Procedures will be housed in IRM 4.31, PassThrough Entity Handbook.

A partnership may elect to adjust the basis of its property after:

(1) a distribution of partnership property, or

(2) certain transfers of a partnership interest. § 754.

To make the election, a partnership must attach a statement to the partnership’s timely filed return (including extensions) for the tax year in which a distribution or transfer occurs. The statement must include:

(1) the name and address of the partnership, and

(2) a declaration that the partnership is making a § 754 election. Review: Reg. § 1.754-1(b)(1)).

Once this election is made, it applies to all distributions and transfers made during the tax year for which the election is initially filed, and to all such transactions in any subsequent tax year unless the election is revoked. This election can only be revoked with permission of the IRS Commissioner.

Revoking a § 754 Election

A partnership that wants to revoke its § 754 election should file its revocation request using Form 15254, Request for § 754 Revocation, no later than 30 days after the close of the partnership’s tax year.

Form 15254 must state the reason(s) for requesting a revocation. The regulations provide examples of situations that may warrant the IRS approving a partnership’s revocation application. Review: Reg. §1.754-1(c).

These examples include:

- a change in the nature of the partnership’s business.

- a substantial increase in the partnership’s assets.

- a change in the character of the partnership’s assets, or

- an increased frequency of retirements or shifts of partnership interests.

A revocation application will not be approved when the revocation’s purpose is primarily to avoid a reduction in the basis of partnership assets upon a transfer or distribution of partnership property.

Updated procedures for reviewing revocation applications. The IRS has provided detailed procedures for its employees to follow when reviewing Form 15254. These procedures cover:

Processing the Form 15254

Making the determination to approve or reject the revocation request.

- Getting managerial approval of the determination.

- Sending the recommended determination to Chief Counsel for review.

- Obtaining the proper signatures for the determination letter, and

- Document retention procedures.

This guidance expires on August 26, 2023, or upon its incorporation into the Internal Revenue Manual.

Issue 6: FIRE System Update Coming September 2021

Any filer, including corporations, partnerships, employers, estates or trusts who files 250 or more Forms 1097, 1042-S, 1098, 1099, 3921, 3922, 5498, 8027, 8955-SSA or W-2G for any calendar year must file their information returns electronically using Filing Information Returns Electronically (FIRE) System.

FIRE is the online tool used to transmit information returns and automatic extension requests to the IRS. Before filers can use FIRE, they must complete an online application to obtain a 5-digit alphanumeric code known as a Transmitter Control Code (TCC). Currently, Form 4419 is used to request a TCC.

A new online application, Information Returns (IR) Application for Transmitter Control Code, is scheduled to deploy on September 26, 2021, and will replace Form 4419.

Issue 7: Bills from the Hill

H.R.4817 — Affordable EVs for Working Families Act. To provide a credit for previously owned qualified plug-in electric drive motor vehicles.

H.R.4831 — Charitable Equity for Veterans Act of 2021. To provide for the deductibility of charitable contributions to certain organizations for members of the Armed Forces.

H.R.4852 — Residential Solar Opportunity Act of 2021. To make the credit for a residential energy efficient property permanent.

H.R.4902 — Improving Diaper Affordability Act of 2021. To treat diapers as qualified medical expenses; and to prohibit States and local governments to impose a tax on the retail sale of diapers.

H.R.4922 — RAISE the Roof Act. To expand the residential energy efficient property credit and energy credit, and for other purposes.

H.R.4962 — Shareholder Allocation for Rewards to Employees Plan Act (or the “SHARE” Plan). To provide that the stock of certain corporations is eligible for capital gains rates only if such corporation maintains a plan for distributing equity to employees, and for other purposes.

H.R.4986 — Refund to Rainy Day Savings Act. To establish the Refund to Rainy Day Savings Program.

H.R.5078 — First Time Homeowner Savings Plan Act. To increase the amount that can be withdrawn without penalty from individual retirement plans as first-time homebuyer distributions.

H.R.5082 — Cryptocurrency Tax Clarity Act. To clarify the definition of a broker, and for other purposes.

H.R.5083 — Cryptocurrency Tax Reform Act. To clarify the definition of a broker, and for other purposes.

H.R.5097 — V.E.T. Student Loan Act. To apply the exclusion of discharged student loan debt retroactively and perpetually for veterans killed or totally and permanently disabled in connection with their service to the United

S.2582 — Raise the Roof Act. To expand the residential energy efficient property credit and energy credit, and for other purposes.

S.2583 — To provide for rules for the use of retirement funds in connection with federally declared disasters.

S.2600 — Refund to Rainy Day Savings Act. To establish the Refund to Rainy Day Savings Program.

S.2602 — Retirement Security Flexibility Act of 2021. To provide for an additional nondiscrimination safe harbor for automatic contribution arrangements.

S.2680 — Real Corporate Profits Tax Act of 2021. To impose a tax on real profits of certain corporations.

H.R.4674 – Motorsports Fairness and Permanency Act of 2021. To make permanent the 7- year recovery period for motorsports entertainment complexes.

H.R.4714 – Disabled Access Credit Expansion Act of 2021. To expand the credit for expenditures to provide access to disabled individuals, and for other purposes.

H.R.4720 – Energy Sector Innovation Credit Act of 2021. To provide investment and production tax credits for emerging energy technologies, and for other purposes.

H.R.4726 – Student Loan Interest Deduction Act of 2021. To increase the deduction allowed for student loan interest.

S.2511 – Revitalizing Downtowns Act. To provide an investment credit for the conversion of office buildings into other uses.

S.2554 – Renters Tax Credit Act of 2021. To provide a refundable tax credit to taxpayers who provide reductions in rent to their tenants under State rental reduction programs, and for other purposes.

H.R.4750 – Performing Artist Tax Parity Act of 2021. To increase the adjusted gross income limitation for above-the-line deduction of expenses of performing artist employees, and for other purposes.

H.R.4759 – Revitalizing Downtowns Act. To provide an investment credit for the conversion of office buildings into other uses.

H.R.5155 – Taxpayer Penalty Protection Act of 2021. To provide for a temporary safe harbor for certain failures by individuals to pay estimated income tax.

H.R.5175 – Incentivizing Solar Deployment Act of 2021. To extend the production tax credit for electricity produced from solar energy.

S.2529 – IGNITE American Innovation Act. To provide for advance refunds of certain net operating losses and research expenditures relating to COVID-19, and for other purposes.

S.2581 – Automatic Relief for Taxpayers Affected by Major Disasters and Critical Events Act. To provide relief for taxpayers affected by disasters or other critical events.

S.2583 – To provide for rules for the use of retirement funds in connection with federally declared disasters.

S.2600 – Refund to Rainy Day Savings Act. To establish the Refund to Rainy Day Savings Program.

S.2645 – REDUCE Act of 2021. To amend the Internal Revenue Code of 1986 to establish an excise tax on plastics.

Issue 8: TIGTA Report – Effects of the COVID-19 Pandemic on Business Tax Return Processing Operations September 2, 2021, Report Number: 2021-46-064

Effects of the COVID-19 Pandemic on Business Tax Return Processing Operations (treasury.gov)

Why TIGTA Did This Audit?

This audit was initiated to provide selected information related to the IRS’s 2020 Filing Season, including information related to the impact of the Coronavirus Disease 2019 (COVID-19).

The overall objective of this review was to assess the IRS’s actions to address the backlog of unworked inventory affecting business taxpayers as a result of Tax Processing Center closures.

Impact on Taxpayers

In response to COVID-19, the IRS took unprecedented and drastic actions to protect the health and safety of its employees and the taxpaying public. These actions included closing its Tax Processing Centers nationwide as of April 6, 2020. In addition, on April 9, 2020, the Department of the Treasury extended the Federal income tax filing due date for various tax filing and payment deadlines that occurred starting on April 1, 2020, to July 15, 2020. As a result, affected businesses had until July 15, 2020, to file returns and pay any taxes that were originally due during this period.

What TIGTA Found

The closure of Tax Processing Centers created a significant backlog of business tax returns, correspondence, and other types of business taxpayer-related work that needed to be processed.

As of the week ending December 31, 2020, the IRS had more than 7.9 million paper-filed business returns that still needed to be processed.

In comparison, the IRS had 239,285 paper-filed business returns that were in process as of December 31, 2019.

Some penalties were inappropriately assessed due to delays in processing payments or tax forms.

- The IRS erroneously assessed 211 Failure to Pay penalties totaling $45,451 due to a programming error.

- The IRS also incorrectly assessed 1,256 estimated tax penalties from April 1, 2020, through December 31, 2020.

- The IRS submitted an information technology work request on July 15, 2020, to update penalty processing, but the programming was not implemented until January 2021.

- As a result, estimated tax penalties assessed for business taxpayers with tax years ending between April 2020 and December 2020 and filed before January 2021 had penalties calculated without considering the relief.

- In addition, systemic payment processing limitations caused further delays in processing payments.

- The IRS’s system was limited to processing payments that were received within 30 days or less.

- However, upon the June 2020 reopening of the Tax Processing Centers, most payments exceeded this limit.

- The IRS did not revise the limit until October 1, 2020, because it was unaware that the programming could be changed.

What TIGTA Recommended

TIGTA recommended that the Commissioner, Wage, and Investment Division, ensure that the incorrectly assessed estimated tax penalties are corrected, and evaluate the feasibility to direct additional types of payments from Tax Processing Centers to lockbox sites.

management agreed with both recommendations. Corrections were made to the incorrectly assessed estimated penalties. The Lockbox Electronic Network Imaging Functional Specification Package has been updated to include processing capability for several additional notices. Analysis of the volumes of notices is being performed to determine if all notices can be directed to lockbox sites. However, management determined it was not feasible for payments received in field offices to be directed to lockbox sites.

Issue 9: Special Per Diem Rates Notice 2021-52

Notice 2021-52 announces the special per diem rates effective October 1, 2021, which taxpayers may use to substantiate the amount of expenses for lodging, meals, and incidental expenses when traveling away from home.

The notice provides the special transportation industry rate, the rate for the incidental expenses only deduction, and the rates and list of high-cost localities for purposes of the high-low substantiation method.

Rev. Proc. 2019-48 provides the rules for using per diem rates, rather than actual expenses, to substantiate the amount of expenses for lodging, meals, and incidental expenses for travel away from home. Taxpayers who use per diem rates to substantiate the amount of travel expenses under Rev. Proc. 2019-48 may use the federal per diem rates published annually by the General Services Administration.

Rev. Proc. 2019-48 allows certain taxpayers to use a special transportation industry rate or to use rates under a high-low substantiation method for certain high-cost localities. The IRS announces these rates and the rate for the incidental expenses only deduction in an annual notice.

Use of a per diem substantiation method is not mandatory. A taxpayer may substantiate actual allowable expenses if the taxpayer maintains adequate records or other sufficient evidence for proper substantiation.

Issue10: TIGTA Evaluates IRS’s Efforts to Address Underreporting of S Corporation Officer Compensation – Audit Report No. 2021-30-042)

The audit was initiated to determine whether the IRS’s policies are adequately ensuring that IRS examiners consider compensation paid by S corporations to their officers.

TIGTA analyzed all S corporation returns the IRS received between 2016 through 2018. It identified 266,095 returns that were not selected for examination that had

- profits greater than $100,000.

- a single shareholder and

- (3) no officer’s compensation claimed on the return.

Those 266,095 returns may not have reported almost $25 billion in compensation and may have avoided paying approximately $3.3 billion in employment taxes, TIGTA estimated.

TIGTA also identified 151, S corporations that were invalid because they had a nonresident alien shareholder. According to the report, the IRS could have converted these S corporations to C corporations and assessed $5 million in corporate income taxes.

TIGTA recommended that the IRS:

- Evaluate the risk of noncompliance associated with officer’s compensation in S corporation returns and update the examination plan.

- Evaluate the benefits to using a threshold and specific criteria as part of classification guidance.

- Use compliance results from established workstreams to inform decision-making around alternative treatments.

- Evaluate the 151, S corporations with nonresident alien shareholders to ensure that they meet the filing requirements for S corporations and

- Evaluate the benefits of creating controls to identify invalid S Corporations when shareholders are nonresident aliens.

The IRS agreed to issue letters to the 151, S corporations with nonresident alien shareholders asking them to review their eligibility status and to analyze this population after one year. The IRS did not agree with the other recommendations.

Issue 11: What Employers Need to Know About Repayment of Deferred Payroll Taxes

The Coronavirus, Aid, Relief and Economic Security Act – CARES Act – allowed employers to defer withholding and payment of the employee’s Social Security taxes on certain wages paid in calendar year 2020.

Repayment of the employee’s portion of the deferral started January 1, 2021, and will continue through December 31, 2021. The employer should send repayments to the IRS as they collect them. If the employer does not repay the deferred portion on time, penalties and interest will apply to any unpaid balance.

Employers can make the deferral payments through the Electronic Federal Tax Payment System (EFTPS) or by credit/debit card, money order or with a check.

These payments must be separate from other tax payments to ensure they are applied to the deferred payroll tax balance. IRS systems won’t recognize the payment if it is with other tax payments or sent as a deposit.

Also, there are special considerations in repaying the deferred taxes when an employer uses a third party payer that files aggregate Forms 941 and 943 under its own EIN.

Issue 12: Interim Guidance for Initial Contact (IRM 5.1.10.3) – SBSE-05-0421-0018

This memorandum provides interim guidance on the issuance of a third-party contact notice along with an appointment letter until Collection Policy revises IRM 5.1.10.3.

Purpose: The purpose of this memorandum is to provide uniform guidance in Revenue Officer (RO) case work as to whether an appointment letter (Letter 725)and a third-party contact notice (Letter 3164) may be mailed at the same time.

- 7602(c) directs IRS employees on how and when they may contact a third party in relation to the determination and collection of a tax liability.

Prior to the Taxpayer First Act (TFA) amendment, § 7602(c) required the Service to provide “reasonable notice in advance” that the Service may contact persons other than the taxpayer.

On July 1, 2019, the TFA amended § 7602(c)(1) to require the Service to provide a notice to taxpayers that it intends to contact third parties during a specified period (not to exceed a year) and to provide the notice at least 45 days in advance of making the contact, unless otherwise provided by the Secretary. The advance notice shall not be issued unless the IRS intends to make a third-party contact during the designated one-year period.

The new rules apply to contacts made after August 15, 2019.

Current Procedure: Internal Revenue Manual (IRM) 5.1.10.3(4) states that the RO may schedule a field visit with a taxpayer or representative by sending an appointment letter (Letter 725). A completed Form 9297, Summary of Taxpayer Contact, should also be included, letting the taxpayer or representative know which items will be needed at the time of the appointment.

Procedural Change:

Revenue officers may attempt scheduling a field visit with a taxpayer or representative by sending an appointment letter, such as Letter 725, Meeting Scheduled with Taxpayer.

A completed Form 9297, Summary of Taxpayer Contact, should also be included, letting the taxpayer or representative know which items will be needed at the time of the appointment.

The revenue officer should conduct the appointment to determine if a third-party contact is necessary. If third-party contact is necessary, they should follow the instructions in IRM 25.27.1.3, Notification Requirements.

A revenue officer may issue the third-party contact notice (Letter 3164) required by §7602(c)(1) at the same time the Letter 725 or other initial contact letter is issued under special circumstances when the revenue officer concludes that the third-party contact is the only means to obtain the necessary information.

Such special circumstances, for example, would include prior experience with the same taxpayer who has demonstrated a pattern of uncooperative or unresponsive behavior that delays the collection of the tax due where third-party contacts were needed to obtain or verify necessary information.

The revenue officer should consult with management prior to sending both letters simultaneously and document the case history (establishing why they intend to contact third parties).

Issuing an appointment letter does not represent taking a timely initial contact action unless it results in actual contact with the taxpayer or the representative within initial contact time frames as provided in IRM 5.1.10.3.1.

If the taxpayer and/or representative receives an appointment letter and calls to confirm or reschedule, the revenue officer should ensure the taxpayer has received IRS Publication 1 (Your Rights as a Taxpayer) and answer any questions, confirm contact information and secure one or more levy sources.

Effective date. These procedures took effect on April 22, 2021.

Issue 13: CCA 202129009 – §6695A Question

Can Penalty Examiners assess the § 6695A penalty without having sent the L4477/IDR and not conducted an interview? (e.g., short statute but we may be able to assess penalty through CCP)

There is no case law or guidance on the issue, but IRS’s position is that, in order to assess the § 6695A penalty, the IRS is not legally required to send the L4477, to send an IDR, or to conduct an interview with the appraiser, but it may be a good policy decision to do so.

Remember, the IRM is not legally binding on the IRS.

And in reading of § 6695A, there is that the exception in subsection (c), is a defense to the penalty, not a prerequisite to assessing it.

So as long as the IRS is able to establish the facts necessary to meet the requirements of § 6695A(a), then the IRS can assess the penalty. Thus, the IRS needs to establish that the person prepared an appraisal, the person knew or should have known it would be used in connection with a return, the reported amount resulted in at least a substantial valuation misstatement, and, for purposes of calculating the penalty, the person received some gross income.

Issue 14: Verifying Identity When Calling IRS – IRS Tax Tip 2021-110

Taxpayers and tax professionals calling the IRS will be asked to verify their identity. This is part of the agency’s ongoing efforts to keep taxpayer data secure from identity thieves. If a taxpayer decides to call, they should know that IRS phone assistors take great care to only discuss personal information with the taxpayer or someone the taxpayer authorizes to speak on their behalf.

To make sure that taxpayers do not have to call back, the IRS reminds taxpayers to have the following information ready:

- Social Security numbers (SSN) and birth dates for those who were named on the tax return.

- An Individual Taxpayer Identification Number (ITIN) letter if the taxpayer has one instead of an SSN.

- Their filing status: single, head of household, married filing joint or married filing separate.

- The prior-year tax return.

Phone assistors may need to verify taxpayer identity with information from the return before answering certain questions. Information they may request includes:

- Information from a copy of the tax return in question.

- Any IRS letters or notices received by the taxpayer

By law, IRS telephone assistors will only speak with the taxpayer or to the taxpayer’s legally designated representative.

If taxpayers or tax professionals are calling about someone else’s account, they should be prepared to verify their identities and provide information about the person they are representing.

Before calling about a thirdparty, they should have the following information available:

- Verbal or written authorization from the third-party to discuss the account.

- The ability to verify the taxpayer’s name, SSN, or ITIN.

- Tax period and

- Tax forms filed.

- Preparer Tax Identification Number or PIN if a third-party designee.

- One of these forms, which is current, completed and signed: Form 8821, Tax Information Authorization Form 2848, Power of Attorney and Declaration of Representative.

Issue 15: Security Summit: Tax Pros Should Encourage Clients to Obtain IP PINs to Protect Against Tax-related Identity Theft

Internal Revenue Service Security Summit partners today called on tax professionals to increase efforts to inform clients about the Identity Protection PIN Opt-In Program that can protect against tax-related identity theft.

The IRS, state tax agencies and the nation’s tax industry – working together as the Security Summit – need assistance from tax professionals to spread the word to clients that the IP PIN is now available to anyone who can verify their identity.

An Identity Protection PIN prevents someone else from filing a tax return using your Social Security number.

The IRS created Publication 5367, IP PIN Opt-In Program for Taxpayers, in English and Spanish, so that tax professionals could print and share the IP PIN information with clients. There are also special posters available in English and Spanish.

For security reasons, tax professionals cannot obtain an IP PIN on behalf of clients. Taxpayers must obtain their own IP PIN.

Taxpayers should share their IP PIN only with their trusted tax prep provider. Tax professionals should never store clients’ IP PINs on computer systems. Also, the IRS will never call, email, or text either taxpayers or tax preparers to request the IP PIN.

Tax professionals who experience a data theft can assist clients by urging them to quickly obtain an IP PIN. Even if a thief already has filed a fraudulent return, an IP PIN would still offer protections for later years and prevent taxpayers from being repeat victims of tax-related identity theft.

Here are a few things taxpayers should know about the IP PIN:

- It’s a six-digit number known only to the taxpayer and the IRS.

- The opt-in program is voluntary.

- The IP PIN should be entered onto the electronic tax return when prompted by the software product or onto a paper return next to the signature line.

- The IP PIN is valid for one calendar year; taxpayers must obtain a new IP PIN each year.

- Only dependents who can verify their identities may obtain an IP PIN.

- IP PIN users should never share their number with anyone but the IRS and their trusted tax preparation provider. The IRS will never call, email, or text a request for the IP PIN.

Currently, taxpayers may obtain an IP PIN for 2021, which should be used when filing any federal tax returns during the year. New IP PINs will be available starting in January 2022.

To obtain an IP PIN, the best option is the Get an IP PIN, the IRS online tool. Taxpayers must validate their identities through Secure Access authentication to access the tool and their IP PIN.

If an individual is unable to validate your identity online and if your income is $72,000 or less, you may file Form 15227, Application for an Identity Protection Personal Identification Number. The IRS will call the telephone number provided on Form 15227 to validate your identity. However, for security reasons, the IRS will assign an IP PIN for the next filing season. The IP PIN cannot be used for the current filing season.

Taxpayers who cannot validate their identities online, or on the phone with an IRS employee after submitting a Form 15227, or who are ineligible to file a Form 15227 may call the IRS to make an appointment at a Taxpayer Assistance Center. They will need to bring one picture identification document and another identification document to prove their identity. Once verified, the taxpayer will receive an IP PIN via U.S. Postal Service within three weeks.

The IP PIN process for confirmed victims of identity theft remains unchanged. These victims will automatically receive an IP PIN each year.

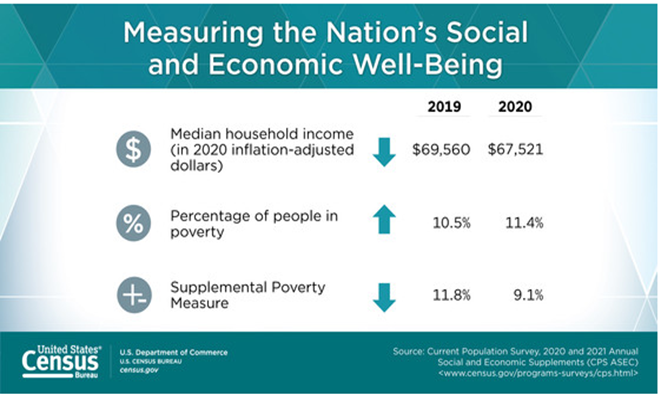

Issue 16: U.S. Census Released 2020 – Income, Poverty and Health Insurance Coverage in the United States

The U.S. Census Bureau announced that median household income in 2020 decreased 2.9% between 2019 and 2020, and the official poverty rate increased 1.0 percentage point. Meanwhile, the percentage of people with health insurance coverage for all or part of 2020 was 91.4%. An estimated 8.6% of people, or 28.0 million, did not have health insurance at any point during 2020, according to the 2021 Current Population Survey Annual Social and Economic Supplement (CPS ASEC).

The Supplemental Poverty Measure (SPM) rate in 2020, also released today, was 9.1%. This was 2.6 percentage points lower than the 2019 SPM rate. The SPM estimates reflect post-tax income that include stimulus payments. The SPM provides an alternative way of measuring poverty in the United States and serves as an additional indicator of economic well-being.

Median household income was $67,521 in 2020, a decrease of 2.9% from the 2019 median of $69,560. This is the first statistically significant decline in median household income since 2011.

Between 2019 and 2020, the real median earnings of all workers decreased by 1.2%, while the real median earnings of full-time, year-round workers increased 6.9%. The total number of people with earnings decreased by about 3.0 million, while the number of full-time, year-round workers decreased by approximately 13.7 million.

The official poverty rate in 2020 was 11.4%, up 1.0 percentage point from 2019. This is the first increase in poverty after five consecutive annual declines. In 2020, there were 37.2 million people in poverty, approximately 3.3 million more than in 2019.

Issue 17: Fiscal Year 2021 Statutory Audit of Compliance with Legal Guidelines Restricting the Use of Records of Tax Enforcement Results

TIGTA is required under § 7803(d)(1) to annually determine whether the IRS complied with restrictions on the use of enforcement statistics to evaluate employees as set forth in § 1204 of the IRS Restructuring and Reform Act of 1998 (RRA 98).

RRA 98 requires the IRS to ensure that managers do not evaluate enforcement employees using any record of tax enforcement results (ROTER) or base employee successes on meeting ROTER goals or quotas. Use of ROTERs to manage IRS employees is unlawful and may create the misperception that safeguarding taxpayer rights is secondary to IRS enforcement results.

TIGTA identified instances of noncompliance with RRA 98 § 1204 requirements related to each of the following subsections of the law:

- 1204(a) – Four instances in which a ROTER was used to evaluate an employee.

- 1204(b) – Six instances in which IRS management failed to either maintain the retention standard documentation or ensure that it was appropriately signed.

- 1204(c) – The IRS also self-reported one instance of § 1204(a) noncompliance and 14 instances of §1204(b) noncompliance.

TIGTA also determined that the accuracy of § 1204 employee designations can be improved. For Fiscal Year 2020, 272 individuals were erroneously designated as § 1204. In addition, §1204 parts of the Internal Revenue Manual have not been updated with changes because §1204 program ownership transitioned from the Chief Financial Officer to the Human Capital Office in October 2017. Also, in Fiscal Year 2020, 395, § 1204 employees failed to complete the § 1204 training.

TIGTA made eight recommendations to mitigate the issues identified during the audit and to improve management of the program. These included:

- Ensuring that statute violations and instances of noncompliance are discussed with the responsible employees and/or managers.

- Applicable performance documents are updated to include a warning on using quantity measures when evaluating managers and

- A control is established for all employees and managers to validate their § 1204 designation.

IRS management agreed with all eight recommendations and:

- Will discuss statute violations and instances of noncompliance with responsible employees and managers.

- Determine a course of action to revise Form 12450 to include a warning on the use of quantity measures when evaluating managers.

- Consider establishing a control that instructs 1204 managers to update their own and/or their employees HR Connect profile and

- Establish an annual reminder to all employees and management to review their § 1204 designation.

IRS management also agreed to ensure that internal procedures are documented, established, and implemented. Finally, IRS management verified that the Integrated Talent Management System issued training reminders to § 1204 employees and managers.

Issue 18: Employee Retention Credit – Question from September Webinar

Does a new business that is formed after February 15, 2020, that buys a business that was operating before February 15, 2020, and none of the owners of the business acquired have ownership or even work in the newly formed business qualify for the Employee Retention Credit?

This question is related to After March 12, 2020, and before January 1, 2021

The Employee Retention Credit is a refundable tax credit against certain employment taxes equal to 50% of the qualified wages an eligible employer pays to employees after March 12, 2020, and before January 1, 2021.

First, employers including tax-exempt organizations, are eligible for the credit if they operate a trade or business during calendar year 2020 and experience either:

- the full or partial suspension of the operation of their trade or business during any calendar quarter because of governmental orders limiting commerce, travel, or group meetings due to COVID-19, or

- a significant decline in gross receipts.

A significant decline in gross receipts begins:

- on the first day of the first calendar quarter of 2020

- for which an employer’s gross receipts are less than 50% of its gross receipts

- for the same calendar quarter in 2019.

The significant decline in gross receipts ends:

- on the first day of the first calendar quarter following the calendar quarter

- in which gross receipts are more than of 80% of its gross receipts

- for the same calendar quarter in 2019.

The credit applies to qualified wages (including certain health plan expenses) paid during this period or any calendar quarter in which operations were suspended.

Second, does the business qualify under the above rules?

Notice 2021-20 Page 51

Question 28: How does an employer that acquires a trade or business during the 2020 calendar year determine if the employer experienced a significant decline in gross receipts?

Answer 28: For purposes of the employee retention credit, to determine whether an employer experiences a significant decline in gross receipts, an employer that acquires (in an asset purchase, stock purchase, or any other form of acquisition) a trade or business during 2020 (an acquired business) is required to include the gross receipts from the acquired business in its gross receipt’s computation for each calendar quarter that it owns and operates the acquired business.

Solely for purposes of the employee retention credit, when an employer compares its gross receipts for a 2020 calendar quarter when it owns an acquired business to its gross receipts for the same calendar quarter in 2019, the employer may, to the extent the information is available, include the gross receipts of the acquired business in its gross receipts for the 2019 calendar quarter.

Under this safe harbor approach, the employer may include these gross receipts regardless of the fact that the employer did not own the acquired business during that 2019 calendar quarter.

An employer that acquires a trade or business in the middle of a calendar quarter in 2020 and that chooses to use this safe harbor approach must estimate the gross receipts it would have had from that acquired business for the entire quarter based on the gross receipts for the portion of the quarter that it owned and operated the acquired business.

However, an employer that chooses not to use this safe harbor approach is required to include only the gross receipts from the acquired business for the portion of the quarter that it owned and operated the acquired business.

Example: Employer D acquired all of the assets of a trade or business in a taxable transaction on January 1, 2020. The gross receipts of the acquired business were $50,000 for the quarter beginning January 1, 2020, and ending March 31, 2020, and $200,000 for the quarter beginning January 1, 2019, and ending March 31, 2019.

Employer D has access to the books and records from the prior owner of the acquired trade or business and can determine the amount of gross receipts attributable to the trade or business for the quarter beginning January 1, 2019 and ending March 31, 2019.

For purposes of the employee retention credit, Employer D must include $50,000 in its gross receipts computation for the quarter beginning January 1, 2020 and ending March 31, 2020 (because Employer D actually owned the trade or business) and may include $200,000 in its gross receipts computation for the quarter beginning January 1, 2019 and ending March 31, 2019.

Please note: It appears that the business would qualify under the original rules of the Employee Retention Credit, based on the information detailed above. The original question had to do with the “recovery startup business.” There is no provision that would apply to this situation under the Recovery Start Up Rules.

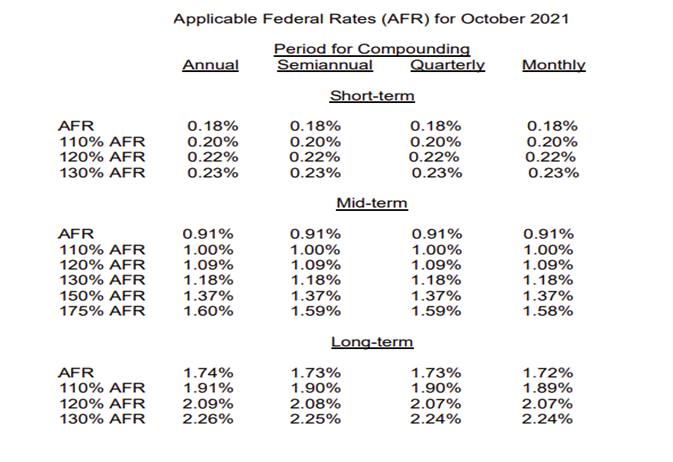

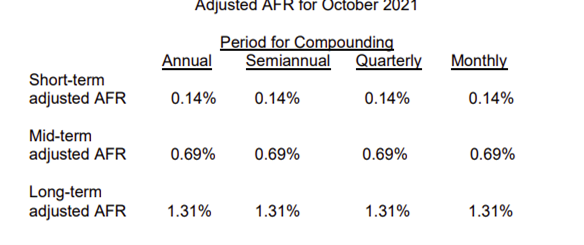

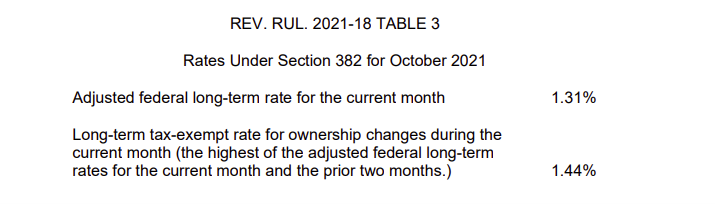

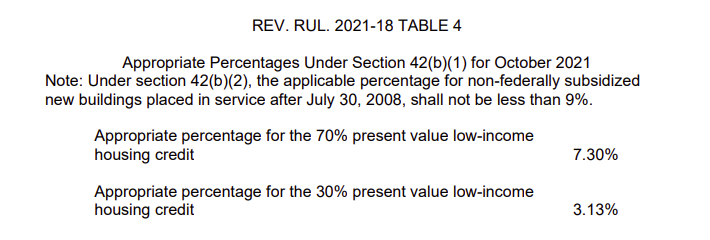

Issue 19: Applicable Federal Rates for September 2021, Rev. Rul. 2021-18

Rate Under § 7520 for October 2021

Applicable federal rate for determining the present value of an annuity, an interest for life or a term of years, or a remainder or reversionary interest 1.0%

![]() Basics & Beyond Resources

Basics & Beyond Resources

- Blog Page

- Resource List

- Webinar & Seminar Schedules

- Get Registered!

- Note: Paid attendees can request a link to the replay of any previously recorded webinar presentations by emailing us at [email protected]