2023 Basics & Beyond Tax Blast- October 2023

In this Issue:

-

- ERC Moratorium on Processing New Claims through December 31, 2023

- IRS to hire 3,700 Employees Nationwide Large Case Revenue Agents

- Cash Payments Over $10k Must Be Reported Online Next Year

- IRS Issues Frequently Asked Questions for Pass-through Entities to Report Negative Amounts to the IRS on Part II of Schedules K-2 and K-3

- New Digital Asset Regs a ‘Huge Milestone,’ Crypto Tax Expert Says

- IRS Clarifies Rules for New Corporate Alternative Minimum Tax

- IRS Issues Guidance on State Tax Payments – IR-2023-23

- New School Year Reminder to Educators; Maximum Educator Expense Deduction is $300

- FinCEN Issues Alert on Prevalent Virtual Currency Investment Scam Commonly Known as “Pig Butchering” IRS Provides

- Updates on Additional Forms for IRIS and Amended 94X Electronic Filing – Checkpoint Author Debbie Tam

- Not All Powers Are the Same: Using a Durable Power of Attorney Rather than a Form 2848 in Tax Matters – Issue Number: 2023-08

- Question: An employer wants to pay the rent for housing for an employee assigned to work on-site at a project. The assignment is expected to last for two years. Is the employer-paid rent taxable income to the employee?

- FinCEN Issues Compliance Guide to Help Small Businesses Report Beneficial Ownership Information

- IRS Reducing Number of EITC Audits

- Builders of New Energy Efficient Homes May Qualify for an Expanded Tax Credit

- Home EV Charging Stations

Issue 1: ERC Moratorium on Processing New Claims through December 31, 2023

Amid rising concerns about a flood of improper Employee Retention Credit claims, the Internal Revenue Service announced effective September 14, 2023, an immediate moratorium through at least the end of the year on processing new claims for the pandemic-era relief program to protect honest small business owners from scams.The IRS continues to work on previously filed Employee Retention Credit (ERC) claims received prior to the moratorium but renewed a reminder that increased fraud concerns means processing times will be longer. With the stricter compliance reviews in place during this period, existing ERC claims will go from a standard processing goal of 90 days to 180 days – and much longer if the claim faces further review or audit. The IRS may also seek additional documentation from the taxpayer to ensure it is a legitimate claim.

On July 26, the agency announced it was increasingly shifting its focus to review these claims for compliance concerns, including intensifying audit work and criminal investigations on promoters and businesses filing dubious claims. The IRS stated that hundreds of criminal cases are being worked, and thousands of ERC claims have been referred for audit.

This enhanced compliance review of existing claims submitted before the moratorium is critical to protect against fraud but also to protect the businesses from facing penalties or interest payments stemming from bad claims pushed by promoters, Werfel said.

Withdrawal Option

In addition, the IRS is finalizing details that will be available soon for a special withdrawal option for those who have filed an ERC claim, but the claim has not been processed. This option – which can be used by taxpayers whose claim has not yet been paid– will allow the taxpayers, many of them small businesses who were misled by promoters, to avoid possible repayment issues and paying promoters contingency fees.

Filers of these more than 600,000 claims awaiting processing will have this option available. Those who have willfully filed fraudulent claims or conspired to do so should be aware, however, that withdrawing a fraudulent claim will not exempt them from potential criminal investigation and prosecution.

As part of the wider compliance effort, the IRS is working with the Justice Department to address fraud in the ERC program as well as promoters who have been ignoring the rules and pushing businesses to apply.

The IRS has trained auditors examining ERC claims posing the greatest risk, and the IRS Criminal Investigation division is actively working to identify fraud and promoters of fraudulent claims for potential referral for prosecution to the Justice Department.

IRS Criminal Investigation (IRS-CI) investigates a variety of COVID fraud allegations ranging from fraudulently obtained employee refund tax credits to falsified Paycheck Protection Program loans.

To date, IRS-CI has uncovered suspected pandemic fraud totaling more than $8 billion. As of July 31, 2023, IRS-CI has initiated 252 investigations involving over $2.8 billion of potentially fraudulent Employee Retention Credit claims. Of those, fifteen of the 252 investigations have resulted in federal charges. Of the 15 federally charged cases, so far six matters have resulted in convictions, four of those cases have reached the sentencing phase with the average sentence being 21 months.

Advice for Taxpayers: What to do as IRS Works to Help Businesses Facing Questionable ERC Claims

As the IRS continues working additional details on ERC, there are several steps that the agency recommends for businesses, depending on where they are in the process:

-

-

- For those currently awaiting an ERC claim. For those who currently have an ERC claim on file, the IRS will continue processing these claims during the moratorium period but at a greatly reduced speed due to the complex nature of these filings and the need to protect businesses from being improperly paid. Normal processing times could easily stretch to 180 days or longer. The IRS cautions that many applications will be facing additional compliance scrutiny, which means the payments could take even longer to be processed. While the IRS works on compliance measures during this period, the agency cautions businesses to expect extended wait times due to the large volume of claims and the complexity of the applications.

-

Due to the large volumes and the need for compliance checks to protect against fraud, the IRS is unable to expedite individual claims. The IRS believes many of the applications currently filed are likely ineligible, and tax professionals note anecdotally that they are seeing instances where 95 % or more of claims coming in recent months are ineligible as promoters continue to aggressively push people to apply regardless of the rules.

For those currently with a pending application at the IRS, they should review the options below to see if any of those could help with their current situation.

-

-

- For those who have not filed a claim yet, consider reviewing the guidelines and waiting to file: For those considering filing a claim, the IRS urges businesses to carefully review the ERC guidelines during the processing moratorium period. The IRS urges businesses to talk to a trusted tax professional – not a tax promoter or marketing firm looking to make money generating applications that takes a big chunk out of the ERC claim. The new question and answer guide below can also help. A careful review of the rules will show that many of these businesses do not qualify for the ERC, and avoiding a bad claim will avoid complications with the IRS.

-

-

-

- Withdraw an existing claim for businesses that have already filed: For those who have filed and have a pending claim, they should carefully review the program guidelines with a trusted tax professional and check the new question and answer guide. For example, the IRS is seeing repeated instances of people improperly citing supply chain issues as a basis for an ERC claim when a business with those issues will very rarely meet the eligibility criteria. Under any scenario, if a business claimed the ERC earlier and the claim has not been processed or paid by the IRS, they can withdraw the claim if they now believe it was submitted improperly – even if their case is already under audit or awaiting audit. More details will be available shortly.

-

Supply Chain

A supply chain issue by itself does not qualify you for the ERC.

The IRS provided a narrow, limited exception if an employer was not fully or partially suspended but their supplier was. However, it applied only when the employer absolutely could not operate without the supplier’s product and the supplier was fully or partially suspended themselves.

In addition to having the supplier’s governmental order, you will need to show that:

-

-

- The government order caused the supplier to suspend operations,

- You couldn’t obtain the supplier’s goods or materials elsewhere (regardless of cost), and

- It caused a full or partial suspension of your own business operations.

-

You should be wary of anyone who says you qualify for ERC based on supply chain issues without asking for specific information about how your business or organization was affected, your supplier’s situation and documentation. For more information and examples see legal memo AM-2023-005.

-

-

- Wait for the IRS ERC settlement program to be finalized: If a business has already received an ERC that they now believe is in error, the IRS will be providing additional details on the settlement program in the fall that will allow businesses to repay ERC claims. The settlement program will allow the businesses to avoid penalties and future compliance action. The IRS is continuing to assess options on how to deal with businesses that had a promoter contingency fee paid for out of the ERC payment.

-

New Eligibility Checklist

Issue 2: IRS to hire 3,700 Employees Nationwide Large Case Revenue Agents

These compliance positions will be open in more than 250 locations nationwide and is part of a larger effort to add fairness to the tax system and expand tax enforcement involving areas of concern with high-income earners, partnerships, large corporations and promoters. The hiring will be for higher-graded revenue agents, which are specialized technical positions that generally focus on audits.

Issue 3: Cash Payments Over $10k Must Be Reported Online Next Year

IR-2023-157, Aug. 30, 2023

The Internal Revenue Service has announced that starting Jan. 1, 2024, businesses are required to electronically file (e-file) Form 8300 Report of Cash Payments Over $10,000, instead of filing a paper return. This new requirement follows final regulations amending e-filing rules for information returns, including Forms 8300.

Businesses that receive more than $10,000 in cash must report transactions to the U.S. government. Although many cash transactions are legitimate, information reported on Forms 8300 can help combat those who evade taxes, profit from the drug trade, engage in terrorist financing or conduct other criminal activities. The government can often trace money from these illegal activities through payments reported on Forms 8300 that are timely filed, complete and accurate.

The new requirement for e-filing Forms 8300 applies to businesses mandated to e-file certain other information returns, such as Forms 1099 series and Forms W-2. Beginning with calendar year 2024, businesses must e-file all Forms 8300 (and other certain types of information returns required to be filed in a given calendar year) if they’re required to file at least 10 information returns other than Form 8300.

For example, if a business files five Forms W-2 and five Forms 1099-INT, then the business must e-file all their information returns during the year, including any Forms 8300. However, if the business files fewer than 10 information returns of any type, other than Forms 8300, then that business does not have to e-file the information returns and is not required to e-file any Forms 8300. However, businesses not required to e-file may still choose to do so.

Waivers

A business may file a request for a waiver from electronically filing information returns due to undue hardship. File Form 8508, Application for a Waiver from Electronic Filing of Information Returns. If the IRS grants a waiver from e-filing any information return, that waiver automatically applies to all Forms 8300 for the duration of the calendar year. A business may not request a waiver from filing only Forms 8300 electronically.

The business must include the word “Waiver” on the center top of each Form 8300 (Page 1) when submitting a paper filed return.

If a business is required to file fewer than 10 information returns, other than Forms 8300, during the calendar year, the business may file Forms 8300 in paper form without requesting a waiver.

If a business files less than 10 information returns, it can still choose to e-file the Forms 8300 electronically if it chooses to do so.

Exemptions

If using the technology required to e-file conflicts with a filer’s religious beliefs, they are automatically exempt from filing Form 8300 electronically. The filer must include the words “RELIGIOUS EXEMPTION” on the center top of each Form 8300 (page 1) when submitting the paper filed return.

Late returns

A business must self-identify late returns. A business must file a late Form 8300 in the same way as a timely filed Form 8300, either electronically or on paper. A business filing a late Form 8300 electronically must include the word “LATE” in the comments section of the return. A business filing a late Form 8300 on paper must write “LATE” on the center top of each Form 8300 (page 1).

Record Keeping

A business must keep a copy of every Form 8300 it files, as well as any supporting documentation and the required statement it sends to customers, for five years from the date filed.

Filing electronically will provide confirmation that the form was filed; however, e-file confirmation e-mails alone do not meet the record keeping requirement. When e-filing, filers must also save a copy of the form prior to finalizing the form submission. They should associate the confirmation number with the saved copy. Prior to finalizing the form for submission, businesses should save a copy of the form electronically or print a copy of the form.

E-filing

To file Forms 8300 electronically, a business must set up an account with the Financial Crimes Enforcement Network’s BSA E-Filing System. The IRS will ensure the privacy and security of all taxpayer data.

For more information, interested businesses can call the Bank Secrecy Act E-Filing Help Desk at 866-346-9478 or email them at [email protected]. For more information about the BSA E-Filing System, businesses can complete a technical support request at Self Service Help Ticket. The help desk is available Monday through Friday from 8 a.m. to 6 p.m. EST.

To help businesses prepare and file reports, the IRS created a video – How to Complete Form 8300 – Part I, Part II. The short video points out sections of Form 8300 for which the IRS commonly finds mistakes and explains how to accurately complete those sections.

Issue 4: IRS Issues Frequently Asked Questions for Pass-through Entities to Report Negative Amounts to the IRS on Part II of Schedules K-2 and K-3

FS-23-20, September 2023

These frequently asked questions (FAQs) are being issued to provide general information to taxpayers and tax professionals as expeditiously as possible. Accordingly, these FAQs may not address any particular taxpayer’s specific facts and circumstances, and they may be updated or modified upon further review. Because these FAQs have not been published in the Internal Revenue Bulletin, they will not be relied on or used by the IRS to resolve a case.

Similarly, if a FAQ turns out to be an inaccurate statement of the law as applied to a particular taxpayer’s case, the law will control the taxpayer’s tax liability. Nonetheless, a taxpayer who reasonably and in good faith relies on these FAQs will not be subject to a penalty that provides a reasonable cause standard for relief, including a negligence penalty or other accuracy-related penalty, to the extent that reliance results in an underpayment of tax.

Any later updates or modifications to these FAQs will be dated to enable taxpayers to confirm the date on which any changes to the FAQs were made. Additionally, prior versions of these FAQs will be maintained on IRS.gov to ensure that taxpayers, who may have relied on a prior version, can locate that version if they later need to do so.

These FAQs were announced in IR 2023-162.

Frequently asked question for pass-through entities to report negative amounts to the IRS on Part II of Schedules K-2 and K-3.

Q. For the 2022 tax year, a pass-through entity receives information (for example, a Schedule K-3 from a lower-tier pass-through entity) that certain gross income amounts to be reported on the Schedules K-2 and K-3 are negative. However, the current schema for electronic filing of the Schedules K-2 and K-3 does not permit negative values for certain line items in Part II, Section 1 of Schedules K-2 and K-3. How should these negative amounts be reported on Schedules K-2 and K-3 to the IRS and to the partners or members? (Added September 5, 2023)

A. A pass-through entity electronically filing the Schedules K-2 and K-3 for the 2022 tax year should enter zero on the line items in Schedules K-2 and K-3, Part II, Section 1 for which the schema does not permit negative values. A pass-through entity must attach a General Dependency (XML) schema to Schedule K-2 identifying the line items and the negative values for which the pass-through entity reported zero on Part II, Section 1.

Additionally, a pass-through entity should attach a list of the impacted line items and the negative numbers, partner by partner. A pass-through entity should report to its partners or members any changes to the amounts reported on the original Schedules K-3 issued to the partners or members. The IRS has not opined on whether it is legally appropriate to use negative values. page 1

Issue 5: New Digital Asset Regs a ‘Huge Milestone,’ Crypto Tax Expert Says – From Checkpoint Writer Tim Shaw

Long-awaited proposed regs clarifying information reporting and basis determination rules for digital asset transactions under the Infrastructure Investment and Jobs Act are a step in the right direction and demonstrate Treasury’s commitment to understanding the crypto ecosystem, according to a former senior IRS official.

Enacted almost two years ago in November 2021, the IIJA established first-of-their-kind digital asset transaction reporting requirements as Congress took a crack at pinning down who exactly is responsible for furnishing information to the IRS and cryptocurrency customers. The bill included definitions for digital assets and “digital asset brokers,” the latter of which was criticized for being unhelpfully broad in scope.

As such, the IRS delayed digital asset broker provisions originally set to go online this year until the issuance of final regs. After much speculation and anticipation from the crypto and tax communities, proposed regs were released at the end of August to clear up confusion surrounding what the IRS expects to be supplied from brokers moving forward. Prop Reg REG-122793-19.

https://public-inspection.federalregister.gov/2023-17565.pdf

The proposed regs provide that digital asset brokers include any person that provides facilitative services that effectuate sales of digital assets by customers, provided the nature of the person’s service arrangement with customers is such that the person ordinarily would know or be in a position to know the identity of the party that makes the sale and the nature of the transaction potentially giving rise to gross proceeds.

Fuller was unsurprised that centralized exchanges were included in the digital asset broker bucket, something “everyone was comfortable with,” but there was an anxiousness over if crypto miners and stakers would be as well. According to Fuller, “the regulations very clearly say they are not included, so that’s good.” The gray area, he continued, is with digital asset wallet providers and decentralized financial protocols. The line in the sand Treasury attempted to draw was the degree of autonomy, or in other words, a lack of human oversight.

As for decentralized finance, or colloquially known as “DeFi,” Fuller said the government has created a “multifactor test” reliant on a “facts and circumstances analysis” to determine if a protocol is truly autonomous. Such an autonomous protocol “gets created and pushed out into the ether on a blockchain somewhere and runs with no connection to any person anywhere or any company.”

Curiously missing from the proposed regs is mention of a Form 1099-DA, a digital asset-specific information return that has been teased by the IRS. But Fuller believes the regs “allude to” a new form that will be used to report the different data points brokers will need to collect, especially items not currently asked about on Form 1099-B like “transaction hashes or wallet addresses.”

It should be noted, though, that the regs phase in reporting requirements over time to, firstly, promote voluntary compliance, and then ease into the new rules. Digital asset brokers will need to know cost basis information for transactions beginning January 1, 2023. Starting tax year 2025, gross proceeds reporting will be mandatory, as well as adjusted cost basis reporting beginning tax year 2026. Where Form 1099-DA fits into this roadmap remains to be seen.

Issue 6: IRS Clarifies Rules for New Corporate Alternative Minimum Tax

Treasury and the has issued Notice 2023-64 to provide additional interim guidance designed to help corporations determine whether the new corporate alternative minimum tax (CAMT) applies to them and how to compute the tax. Notice 23-64 (irs.gov)

Notice 2023-64, clarifies and supplements Notice 2023-07 and Notice 2023-20, issued earlier this year. Treasury and IRS anticipate that forthcoming proposed regulations will be consistent with this interim guidance.

The Inflation Reduction Act created the CAMT, which imposes a 15% minimum tax on the adjusted financial statement income (AFSI) of large corporations for taxable years beginning after Dec. 31, 2022. The CAMT generally applies to large corporations with an average annual financial statement income exceeding $1 billion.

Considering the challenges of determining CAMT liability, Notice 2023-42, provides that the IRS will waive the penalty for a corporation’s estimated income tax with respect to its CAMT for a taxable year that begins after Dec. 31, 2022, and before Jan. 1, 2024.

Among other things, today’s notice provides a list of financial statements that meet the definition of an applicable financial statement (AFS) as well as priority rules for identifying a taxpayer’s AFS.

The guidance also provides general rules for determining a taxpayer’s financial statement income and AFSI, including when the taxpayer’s financial results are reported on a consolidated financial statement.

Finally, the notice includes guidance on when corporations are subject to CAMT, CAMT foreign tax credits, tax consolidated groups, foreign corporations, depreciable property, wireless spectrum, duplications and omissions of certain items, and financial statement net operating losses.

Issue 7: IRS Issues Guidance on State Tax Payments – IR-2023-23

The Internal Revenue Service provided details clarifying the federal tax status involving special payments made by 21 states in 2022.

The IRS has determined that in the interest of sound tax administration and other factors, taxpayers in many states will not need to report these payments on their 2022 tax returns.

During a review, the IRS determined it will not challenge the taxability of payments related to general welfare and disaster relief. This means that people in the following states do not need to report these state payments on their 2022 tax return: California, Colorado, Connecticut, Delaware, Florida, Hawaii, Idaho, Illinois, Indiana, Maine, New Jersey, New Mexico, New York, Oregon, Pennsylvania and Rhode Island. Alaska is in this group as well, but please see below for more nuanced information.

In addition, many people in Georgia, Massachusetts, South Carolina and Virginia also will not include state payments in income for federal tax purposes if they meet certain requirements. For these individuals, state payments will not be included for federal tax purposes if the payment is a refund of state taxes paid and either the recipient claimed the standard deduction or itemized their deductions but did not receive a tax benefit.

The IRS is aware of questions involving special tax refunds or payments made by certain states related to the pandemic and its associated consequences in 2022. A variety of state programs distributed these payments in 2022 and the rules surrounding their treatment for federal income tax purposes are complex. While in general payments made by states are includable in income for federal tax purposes, there are exceptions that would apply to many of the payments made by states in 2022.

To assist taxpayers who have received these payments file their returns in a timely fashion, the IRS is providing the additional information below.

Refund of State Taxes Paid

If the payment is a refund of state taxes paid and either the recipient claimed the standard deduction or itemized their deductions but did not receive a tax benefit (for example, because the $10,000 tax deduction limit applied) the payment is not included in income for federal tax purposes.

Payments from the following states in 2022 fall in this category and will be excluded from income for federal tax purposes unless the recipient received a tax benefit in the year the taxes were deducted.

-

-

- Georgia

- Massachusetts

- South Carolina

- Virginia

-

General Welfare and Disaster Relief Payments

If a payment is made for the promotion of the general welfare or as a disaster relief payment, for example related to the outgoing pandemic, it may be excludable from income for federal tax purposes under the General Welfare Doctrine or as a Qualified Disaster Relief Payment. Determining whether payments qualify for these exceptions is a complex fact intensive inquiry that depends on a number of considerations.

The IRS has reviewed the types of payments made by various states in 2022 that may fall in these categories and given the complicated fact-specific nature of determining the treatment of these payments for federal tax purposes balanced against the need to provide certainty and clarity for individuals who are now attempting to file their federal income tax returns, the IRS has determined that in the best interest of sound tax administration and given the fact that the pandemic emergency declaration is ending in May, 2023 making this an issue only for the 2022 tax year, if a taxpayer does not include the amount of one of these payments in its 2022 income for federal income tax purposes, the IRS will not challenge the treatment of the 2022 payment as excludable for income on an original or amended return.

Payments from the following states fall in this category and the IRS will not challenge the treatment of these payments as excludable for federal income tax purposes in 2022.

For a list of the specific payments to which this applies, please see the chart you can link to below.

State Payments | Internal Revenue Service (irs.gov)

Other payments

Other payments that may have been made by states are generally includable in income for federal income tax purposes. This includes the annual payment of Alaska’s Permanent Fund Dividend and any payments from states provided as compensation to workers.

Issue 8: New School Year Reminder to Educators; Maximum Educator Expense Deduction is $300

IR-2023-150, Aug. 17, 2023

As the new school year begins, the Internal Revenue Service reminds teachers and other educators that they’ll be able to deduct up to $300 of out-of-pocket classroom expenses for 2023 when they file their federal income tax return next year.

This is the same limit that applied in 2022, the first year this provision became subject to inflation adjustment. Before that, the limit was $250. The limit will rise in $50 increments in future years based on inflation adjustments.

This means that an eligible educator can deduct up to $300 of qualifying expenses paid during the year. If they’re married and file a joint return with another eligible educator, the limit rises to $600. But in this situation, not more than $300 for each spouse.

Who qualifies?

Educators can claim this deduction, even if they take the standard deduction. Eligible educators include anyone who is a kindergarten through grade 12 teacher, instructor, counselor, principal or aide who worked in a school for at least 900 hours during the school year. Both public and private school educators qualify.

What’s deductible?

Educators can deduct the unreimbursed cost of:

-

-

- Books, supplies and other materials used in the classroom.

- Equipment, including computer equipment, software and services.

- COVID-19 protective items to stop the spread of the disease in the classroom. This includes face masks, disinfectant for use against COVID-19, hand soap, hand sanitizer, disposable gloves, tape, paint or chalk to guide social distancing, physical barriers, such as clear plexiglass, air purifiers and other items recommended by the Centers for Disease Control and Prevention.

- Professional development courses related to the curriculum they teach or the students they teach. But the IRS cautions that, for these expenses, it may be more beneficial to claim another educational tax benefit, especially the lifetime learning credit.

-

Qualified expenses do not include the cost of home schooling or for nonathletic supplies for courses in health or physical education. As with all deductions and credits, the IRS reminds educators to keep good records, including receipts, cancelled checks and other documentation.

Issue 9: FinCEN Issues Alert on Prevalent Virtual Currency Investment Scam Commonly Known as “Pig Butchering”

The Financial Crimes Enforcement Network (FinCEN) issued an alert to highlight a prominent virtual currency investment scam known as “pig butchering.” The alert explains the scam’s methodology; provides behavioral, financial, and technical red flags to help financial institutions identify and report related suspicious activity; and reminds financial institutions of their reporting requirements under the Bank Secrecy Act.

News Release: https://www.fincen.gov/news/news-releases/fincen-issues-alert-prevalent-virtual-currency-investment-scam-commonly-known

Alert: https://www.fincen.gov/sites/default/files/shared/FinCEN_Alert_Pig_Butchering_FINAL_508c.pdf

Issue 10: IRS Provides Updates on Additional Forms for IRIS and Amended 94X Electronic Filing – Checkpoint Author Debbie Tam

During the September 7 IRS payroll industry call, the IRS provided updates on its latest modernization efforts that payroll practitioners have been eyeing.

IRIS. In January 2023, the IRS launched IRIS, the 1099 filing portal. The portal allows users to prepare and file Forms 1099 electronically and maintain tax records. The Application to Application (A2A) bulk filing option is also available for the 2022 tax year.

Unlike the FIRE system, IRIS uses an XML format. The IRS emphasized that it is prioritizing performance over adding more forms to the IRIS system. It continues to modernize the backend processing to increase the number of forms processed per second.

As a result, the IRS does not anticipate new forms to be processed through the IRIS system for the upcoming filing season. The IRS will be creating a recurring working group with partners, similar to the sessions for MeF, that would include IRIS A2A users, transmitters, and states. It is tentatively scheduled for the second Wednesday of every month.

Amended 94X electronic filing. The IRS continues to expect that amended Form 94X electronic filing will be available for the 2024 filing season. While no definitive news was available, the IRS noted that it continues to work out modified schemas. While there’s a slight chance at a March 2024 release, the IRS said it was more likely that a release would occur in June 2024, after the filing season.

Issue 11: Not All Powers Are the Same: Using a Durable Power of Attorney Rather than a Form 2848 in Tax Matters – Issue Number: 2023-08

Normally, a taxpayer must sign an IRS Form 2848, Power of Attorney and Declaration of Representative, to allow someone to represent them in a tax matter with the IRS — the representative must also have certain professional credentials.

In some cases, however, a taxpayer is unable to complete and sign a Form 2848 because they become physically or mentally incompetent. What can you do to prepare for the day when you or someone you know may be in that situation? Plan ahead! In many cases, you may be able to use a “durable power of attorney” — often used for estate planning or other purposes — to overcome a legally incompetent taxpayer’s inability to complete a Form 2848.

Durable powers of attorney created for estate planning or other purposes give your designated agent or “attorney-in-fact” authority to make healthcare and financial decisions.

The word “durable” means the power of attorney has staying power and will remain in effect if you later become incompetent. Needless to say, the durable power of attorney must be created before you become physically or mentally incompetent. For a durable power of attorney to work for federal tax matters, however, specific information required under the Internal Revenue Code and regulations needs to be included. The requirements related to use of durable power of attorneys in federal tax matters are stated in Reg. 601.503(b), which can be found in Publication 216.

If care is not taken in preparing the durable power of attorney, it may not be sufficient to authorize your agent to act for you in tax matters for the IRS. In that case, your agent may also have to be designated a guardian or similar fiduciary, which is typically done by a state court and can be a lengthy process. Once your agent is designated a guardian or similar fiduciary, they would then have to file an additional form (Form 56) with the IRS that informs the IRS of the fiduciary relationship.

National Taxpayer Advocate Blog: When to Use a Durable Power of Attorney to Authorize Representation Before the IRS

IRS Office of Professional Responsibility: Can You Use that Durable Power of Attorney before the IRS? Form 2848 vs. Durable Power of Attorney

Form 2848, Power of Attorney and Declaration of Representative, and Instructions for Form 2848

Publication 216, Conference and Practice Requirements

Form 56, Notice Concerning Fiduciary Relationship

Issue 12: Trusts Marketed Online Misconstrue Tax Law

The promoters of non-grantor, irrevocable, complex, discretionary, spendthrift (NICDS) trust schemes that are marketed online as removing certain trust income from taxation are misinterpreting §643, according to an Office of Chief Counsel (OCC) memorandum. The memorandum was limited to rebutting the promoters’ misinterpretation of §643 and did not address whether the structures could be recharacterized as §671 grantor trusts. If necessary, the OCC said it would address the recharacterization issue in a supplemental memorandum.

In reviewing the trusts, the OCC said it looked at the materials used to market NICDS trusts that claimed almost none of the income generated by the trust is subject to federal income tax if the trustee allocates such income to corpus and refrains from making distributions to beneficiaries.

The OCC found the claims made by the promoters of NICDS trusts to support their position read §643 out of context. It also said the materials looked to §643(a) for guidance on the definition of “taxable income” and ignored provisions at the beginning of that section, which expressly state that it defines “distributable net income” rather than taxable income.

Issue 13: Question: An employer wants to pay the rent for housing for an employee assigned to work on-site at a project. The assignment is expected to last for two years. Is the employer-paid rent taxable income to the employee?

Answer: Generally, the provision of housing to an employee by the employer is taxable income to the employee unless it meets one of two exceptions.

Under the first exception, employer-provided housing may be excluded from taxable income when the housing qualifies as a travel expense. Travel expenses are excludable from the employee’s income if the employee is traveling away from their tax home. The employee’s tax home is the location of their principal place of work rather than the location of their personal residence.

If the employee is temporarily assigned to a location that is not the employee’s tax home, the payment of the rent at the temporary location likely qualifies as a travel expense.

A “temporary assignment” is defined as one that is expected to and does last less than one year. Ordinary and necessary business-related travel and temporary living expenses paid or reimbursed by the employer under an accountable reimbursement plan may be excluded from the employee’s income. This includes employer-provided housing.

However, the assignment creates a new principal work location when it is indefinite or permanent and is expected to last more than one year, even if it does not. This creates a new tax home for the employee.

Since the assignment in question is expected to last for two years, the assignment is “permanent” or “indefinite” from a tax standpoint. This establishes a tax home for the employee at the job location; so, the exemption for travel expenses at a temporary job site does not apply.

Under a second exception, the value of housing may be excludable from the employee’s pay if the housing is on the employer’s business premises, is furnished for the employer’s convenience, and the employee accepts the housing as a condition of employment.

Generally, “the employer’s premises” means the employee’s usual workplace. “Employer convenience” means there must be a substantial business reason for providing the lodging other than providing the employee with additional pay.

The exclusion does not apply if the employee may choose additional pay instead of the housing or may choose not to live in the employer-provided housing.

Examples of employer convenience include situations in which the employee must be available on site at all times. For example, a building superintendent of an apartment building or miners working at a remote mining operation where employees could not do the job properly without being furnished the lodging.

Author Information

Patrick Haggerty is the owner of a tax practice in Chapel Hill, North Carolina, and an enrolled agent licensed to practice before the Internal Revenue Service. The author may be contacted at [email protected].

Issue 14: Tax Professionals Must Act Fast After Discovering a Data Breach – Issue Number: Tax Tip 2023-106

Anyone can be a target of cybercriminals and scammers. Unfortunately, tax professionals can seem like the big fish in a sea of potential targets because of how much financial data they use to conduct their business. Even a careful, prepared tax pro may fall victim to a crime. If that happens, there are several key things they should do to protect their clients and their business.

Their clients

It is vitally important that tax professionals inform all their clients of a breach and encourage them to apply to the IRS for an Identity Protection Personal Identification Number, or IP PIN. The Electronic Tax Administration Advisory Committee called the IP PIN, “The number one security tool currently available to taxpayers from the IRS.”

Preparers should work with law enforcement to determine when it’s best to send an individual letter to all potential victims to inform them of a breach.

How to report a data breach

-

-

- Contact the IRS – The tax preparer should report client data theft to their local IRS Stakeholder Liaison. The liaison will notify IRS Criminal Investigation and others within the agency on the tax professional’s behalf. If reported quickly, the IRS can take steps to block fraudulent returns in clients’ names.

- Call local police – The taxpayer should contact police to file a report on the data breach.

- File a complaint with the FBI’s Internet Crime Complaint Center.

- File a report with the nearest office of the Secret Service.

- To help tax professionals find where to report data security incidents at the state level, the Federation of Tax Administrators has created a special page with state-by-state listings.

- The preparer should contact the Attorneys General for each state in which the tax professional prepares returns.

-

Help from Other Experts

-

-

- Security expert – Tax preparers should consult an expert who can help determine the cause and scope of the breach to stop the breach and prevent further breaches from occurring.

- Insurance company – Tax preparers should report the breach to their insurance company and check if the insurance policy covers data breach mitigation expenses.

- Federal Trade Commission – Preparers and other businesses can go to the FTC for guidance. For more individualized guidance, preparers can email the FTC.

- Credit and identity theft protection agency – Certain states require that preparers offer credit monitoring and identity theft protection to victims of identity theft.

- Credit bureaus – Preparers should notify them if there is a compromise and clients may seek their services.

-

Review security measures used to protect client data

Data protection is key in helping avoid data breaches. To help tax pros protect their clients and their business, the IRS, state tax agencies and the tax industry partners who make up the Security Summit created a Taxes-Security-Together Checklist. Whether a one-person shop or partner in a large firm, everyone can take several relatively simple steps to protect their clients and their business data.

Issue 15: FinCEN Issues Compliance Guide to Help Small Businesses Report Beneficial Ownership Information

The U.S. Department of the Treasury’s Financial Crimes Enforcement Network (FinCEN) published a Small Entity Compliance Guide to assist the small business community in complying with the beneficial ownership information (BOI) reporting rule. Starting in 2024, many entities created in or registered to do business in the United States will be required to report information about their beneficial owners—the individuals who ultimately own or control a company—to FinCEN. The Guide is intended to help businesses determine if they are required to report their beneficial ownership information to FinCEN.

The Guide is now available on FinCEN’s beneficial ownership information reporting webpage.

Among other things, the Guide:

-

-

- Describes each of the BOI reporting rule’s provisions in simple, easy-to-read language;

- Answers key questions; and

- Provides interactive checklists, infographics, and other tools to assist businesses in complying with the BOI reporting rule.

-

The requirements become effective on January 1, 2024, and companies will be able to begin reporting beneficial ownership information to FinCEN at that time. FinCEN will provide additional guidance on how to submit beneficial ownership information soon. Small businesses can continue to monitor FinCEN’s website for more information or subscribe to FinCEN updates.

Issue 16: IRS Reducing Number of EITC Audits

The IRS is reducing its audit rates for taxpayers claiming the earned income tax credit (EITC) while it addresses the racial disparities in its audit rates for Black taxpayers, according to a letter from IRS Commissioner Danny Werfel to the chairman of the Senate Committee on Finance. The IRS recently confirmed studies that found Black taxpayers are audited at rates of three to five times of those for non-Black taxpayers, with most of the disparities driven by differences in correspondence audit rates among taxpayers claiming the EITC.

Werfel noted that its Strategic Operating Plan committed the IRS to conducting research to understand systemic bias in compliance strategies and treatments. He added that the IRS will be prioritizing the ongoing evaluation of the EITC audit selection algorithms and that the agency is committed to transparency regarding its research findings.

Holding unscrupulous preparers accountable

Werfel’s letter also mentioned that the IRS is working to hold accountable the unscrupulous preparers who do not exercise due diligence and who put taxpayers at a disadvantage through bad advice. It added that the IRS is accelerating its research efforts aiming to detect and ensure compliance among “ghost preparers” who are paid to prepare returns, but do not identify themselves to the IRS. Initial evidence shows that unscrupulous and ghost preparers disproportionately target minority communities.

Issue 17: Builders of New Energy Efficient Homes May Qualify for an Expanded Tax Credit

Eligible contractors who build or substantially reconstruct qualified new energy efficient homes may be eligible for a tax credit up to $5,000 per home. The actual amount of the credit depends on eligibility requirements such as the type of home, the home’s energy efficiency and the date when someone buys or leases the home.

Contractors must meet eligibility requirements:

-

-

- Construct or substantially reconstruct a qualified home.

- Own the home and have a basis in it during construction.

- Sell or rent it to a person for use as a residence.

-

To qualify, a home must be:

-

-

- A single-family (including manufactured homes) or multifamily home, as defined under certain Energy Star program requirements.

- Located in the United States.

- Purchased or rented for use as a residence.

- Certified to meet applicable energy saving requirements based on home type and acquisition date.

-

Requirements and credit amounts for 2023 and after:

For homes acquired in 2023 through 2032, the credit amount ranges from $500 to $5,000, depending on the standards met, which include:

-

-

- Energy Star program requirements.

- Zero energy ready home program requirements.

- Prevailing wage requirements.

-

Requirements and credit amounts before 2023:

For homes acquired before 2023, the credit amount is $1,000 if the 30% standard is met or $2,000 if the 50% standard is met. The standards include:

-

-

- For the 50% standard, certifying that the home has an annual level of heating and cooling energy consumption that is at least 50% less energy than a comparable home and gets at least 1/5 of its energy savings from building envelope improvements.

- For the 30% standard, certifying that the home has an annual level of hearing and cooling energy consumption that is at least 30% less energy than a comparable home.

- Meeting certain federal manufactured home rules.

- Meeting certain Energy Star requirements.

-

Properly claiming the credit:

Eligible contractors must meet all requirements before claiming the credit. Eligible contractors should review the Instructions for Form 8908, Energy Efficient Home Credit, for full details about these requirements. They must complete Form 8908, Energy Efficient Home Credit, and submit it with their tax return to claim the credit.

Issue 18: Home EV Charging Stations

Essentially, if you install a home EV charging station, the tax credit is 30% of the cost of hardware and installation, up to $1,000.

Also, beginning this year (i.e., 2023), the EV charger tax credit for business and home installations applies to other EV charger equipment like bidirectional (i.e., two-way) chargers.

To claim the federal tax credit for the home EV charger, or other EV charging equipment, file Form 8911 with the IRS when you file your federal income tax return.

You will need your receipts that show the purchase price of the EV charger and any fees for installation of the charger.

You will also need to know your tax liability for the year that you’re claiming the credit. That’s because the EV charger tax credit is subtracted from any federal tax that you might owe on that year’s return.

Also, the EV charger tax credit isn’t refundable, so you won’t receive cash back as a result of claiming the credit.

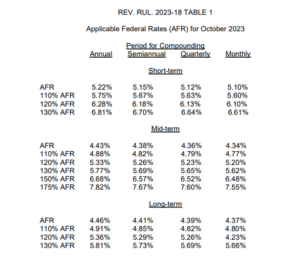

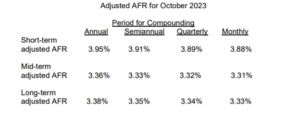

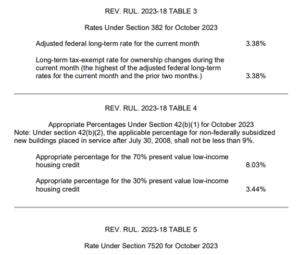

Issue 19: Applicable Federal Rates for October 2023, Rev. Rul. 2023- 18