Tax Newsletter: Updates & News

Once again news is abundant, so we had to pick and choose what we felt was most important to you and your practice. We’ll take a look at the New 1040. We will include last minute news in our fall seminars and more later in the year time-sensitive issues closer to the beginning of filing season.

Congress adjourned without an agreement concerning the fourth COVID-19 bill. This just pushes back potential “new” legislation we have to learn as we approach 2021 and the filing season.

IRS is trying to get its act together concerning unopened mail, so do not be surprised if your client gets a notice asking for payment when payment was made, Issue 16 addresses this issue. Patience is required by the client and ask them to sit tight for now. I would not be concerned unless they continue to get the same letter through year end. Dates on the notices may be correct, but the amount are potentially wrong. IRS can filter for envelopes which have checks and 11 million are still sitting there to be processed. IRS is waiving bad check penalties for dishonored checks the agency received between March 1st and July 15th due to delays in IRS processing.

Amended Return 1040X Can Now Be E-Filed

As mention last month, Form 1040X is now available for e-filing, so check your software provider to see if you have that capability in your software. Making the 1040-X an electronically filed form has been a goal for the tax software and tax professional industry for years. The new electronic option allows the IRS to receive amended returns faster while minimizing errors normally associated with manually completing the form.

Since the tax-filing software allows users to input their data in a question-answer format, it simplifies the process. It also makes it easier for IRS employees to answer taxpayer questions since the data is entered electronically and submitted to the agency almost simultaneously. For the initial phase, only tax year 2019 Forms 1040 and 1040-SR returns can be amended electronically. Additional improvements are planned for the future.

About 3 million Forms 1040-X are filed by taxpayers each year.

Taxpayers still have the option to submit a paper version of the Form 1040-X and should follow the instructions for preparing and submitting the paper form. Those filing their Form 1040-X electronically and on paper can use the “Where’s My Amended Return?” online tool to check the status of their amended return.

Fall seminars will start in the next few weeks and we as a Team have important information to share. Plus, we will also share “new” information on guidance as released. If not registered, NOW is the time to review the topics and consider joining us. The Team is excited about the new format and eager to share their expertise and information.

https://www.cpehours.com/income-tax-seminar-information/

2020 Fall Topical Income Tax Update

- 2020 Tax Legislation–New Developments, Including the Stimulus Payment Issues & COVID Legislation

- SECURE Act

- Retirement Planning: Highlights from the CARES and SECURE Acts

- Ethics & the Tax Client

- Assignment of Income

- 1065 Partnership / Distributions

- Basics of Trusts & Estates & Planning Strategies Trusts & Estate Planning

2020 Year-end Income Tax Update

- 2020 Tax Legislation–New Developments, Review of Cases, Rulings & IRS Pronouncements

- QBI, CARES and Secure Act Unique Year End Issues

- Meals & Entertainment under the TCJA

- IRC 121 and the Primary Residence

- Ethics – The Creative Tax Professional

- S-Corporation Basis Issues

- Centralized Partnership Audit Regime

- Preparing for the 2021 Tax Season and the Coronavirus Impact

In This Issue

- Failure to Deposit Penalties Sent in Error to Employers Claiming New Tax Credits

- Potential New Circular 230 in the Future

- Notice 2020-62: Updating Safe Harbor for Eligible Rollover Distribution Recipients

- IRS Updates Its Third-Party Authentication Procedures

- SBA Guidance on PPP Loan Forgiveness

- What is a Covered Employee for PPP Loan Purposes?

- E-file Application Revisions Requiring Resubmission

- Taxpayer Advocate Service Can Assist with Correcting Economic Impact Payment Amounts

- IRS Issues Proposed Regulations for TCJA’s Simplified Tax Accounting Rules for Small Business

- IRS Provides Guidance on Recapturing Excess Employment Tax Credits

- Treasury, IRS Issue Guidance on Reporting Qualified Sick and Family Leave Wages Paid

- The Joint Board for the Enrollment of Actuaries Announces Temporary Waiver of “Physical Presence” Education Requirement for Enrolled Actuaries

- Executive Order Defers Employee Social Security Taxes – But Not So Fast – It’s Voluntary – Caution Should Be Used

- IRS Updates Form 433-D to Reflect Two Changes

- S. Tax Court Update on Procedural Changes Due to COVID-19IRS Taking New Steps to Ensure People with Children Receive the $500 Economic Impact PaymentsIRS Pending Check Payments and Payment Notices

- Suspending Mailing of Collection Notices

- Identity Theft Form 14039-B Now Available for Business and Other Identitie

- Draft of 2020 Form 1040 Issued

- Applicable Federal Rates (AFR) for September 2020 – Rev. Rul. 2020-16

Issue 1A: Failure to Deposit Penalties Sent in Error to Employers Claiming New Tax Credits

The IRS is aware that a small population of employers that reduced their tax deposits in anticipation of claiming the sick and family leave credits, or employee retention credit, may have received a notice stating there was a failure to deposit penalty applicable to the Form 941 on which the credits were claimed.

Under Notice 2020-22, employers claiming the new tax credits may reduce their deposits throughout the tax period up to the amount of the credit. However, in reporting the schedule of liabilities on Form 941, the reported liabilities did not match the reduction in deposits for every pay date.

In these situations, they incurred a failure to deposit penalty on the difference in the reported liabilities and the reduced deposits (in situations where deposits were reduced by the amount of the anticipated credit(s) in excess of liability for the employer portion of social security for a given pay date).

Although the IRS has taken steps to implement rules that prevent the failure to deposit penalty from incurring on employers reducing their deposits in anticipation of these credits, we’ve become aware some employers may still have inadvertently received notice of the penalty.

The IRS is taking actions to identify these employer accounts and correct them as soon as possible. Employers that have recently received these notices do not need to take additional actions at this time. To avoid future receipts of these notices, please check IRS.gov/form941 for future guidance on reporting liabilities when reducing deposits.

Issue 1: Potential Updated Circular 230 in the Future

Circular 230 has not been updated since June 2014, before the Loving decision on the IRS regulation of tax professionals was ligated. The document contains ethical guidance and regulations that detail who is subject to Circular 230, as well as a summary description of certain obligations.

The wording needs to be updated to reflect the changes in the Registered Tax Return Preparers Program and the changes the Loving case brought to IRS. With no legislation that authorizes IRS to regulate tax professionals, many states have taken on that burden. Prior directors were relying on legislation to expand the office’s authority to regulate return preparers before updating Circular 230.

Issue 2: Notice 2020-62: Updating Safe Harbor for Eligible Rollover Distribution Recipients

The notice modifies the two safe harbor explanations in Notice 2018-74, that may be used to satisfy the requirement under § 402(f) that certain information be provided to recipients of eligible rollover distributions.

The safe harbor explanations as modified by this notice take into consideration certain legislative changes, including changes related to the Setting Every Community Up for Retirement Enhancement Act of 2019 (SECURE Act), which was enacted as part of the Further Consolidated Appropriations Act, 2020, Pub. L. 116-94. The SECURE Act adds § 72(t)(2)(H) of the Code as a new exception to the 10% additional tax under § 72(t)(1) for qualified birth or adoption distributions. The SECURE Act also includes an amendment to§ 401(a)(9)(C)(i)(I) of the Code that increases the age for required minimum distributions to age 72 for employees born after June 30, 1949.

To assist with the implementation of the modified safe harbor explanations, the notice includes an appendix with two model safe harbor explanations: one for distributions that are not from a designated Roth account, and the other for distributions from a designated Roth account.

Administrators of qualified retirement plans are required to provide a written explanation of tax consequences when making distributions that are eligible for rollover. The explanation is often referred to as the “402(f) notice” after the relevant section of the Internal Revenue Code governing the requirement, or simply as the “special tax notice.”

Issue 3: IRS Updates Its Third-Party Authentication Procedures

IRM Procedural Update – 07/09/2020

NUMBER: wi-21-0720-0774 SUBJECT: Third Party Authentication Affected: IRM(s)/SUBSECTION(s): 21.1.3 CHANGE(s):

IRM 21.1.3.2.3(8) Added high risk criteria when call concerns lost, misplaced, or non-receipt of CP01A containing their IP PIN.

If a taxpayer requests account information and there is no open account issue or a notice has not been issued on the account, then more research is needed to prevent unauthorized disclosure. Examples of open account issues could include balance due issues, amended return, Taxpayer Delinquency Investigation (TDI), certain freeze codes, or IRS initiated correspondence. Review IRM 21.1.3.2.4, Additional Taxpayer Authentication, for additional information on the high-risk authentication process. Issues that require additional taxpayer authentication may include:

- Verbal account information other than refund status and taxpayer does not have any open account issues or notices.

- Requests for a transcript or tax account information sent to an address that is not the address of record and the taxpayer does not have any open account issues or notices. Transcript requests mailed to the current address of record with no verbal account information exchanged is not high-risk criteria.

NOTE: If the taxpayer is asking for transcripts (tax account, tax return, record of account, wage and income, verification of non-filing) and you are unable to verify required authentication, advise the caller to submit Form 4506-T, Request for Transcript of Tax Form, to the appropriate Return and Income Verification Services (RAIVS) unit. Review IRM 21.2.3.5.8.1, Authentication Procedures for Identity Theft, when the account contains an ID theft marker.

Verification of estimated tax payments on an account without a filed return can be made to the secondary taxpayer when the preceding year shows a joint return with that same secondary taxpayer and Remittance Transaction Register (RTR) shows the joint ES voucher or joint check showing the intent to make joint ES payments.

IRM 21.1.3.3(1) Added reminder to research CAF for faxed authorizations.

When responding to a third party (anyone other than the taxpayer) who indicates he/she has a third-party authorization on file, or states they are submitting an original authorization, complete the appropriate research. For Power of Attorney (POA), Form 2848 and Tax Information Authorization (TIA), Form 8821 research the Centralized Authorization File (CAF) using CC CFINK or via the IAT Disclosure tool, if applicable, before providing any tax account information.

IRM 21.1.3.3(3) Added information on updated exception policies on additional third-party authentication with Forms 8821 and Form 2848.

As part of an ongoing effort to combat identity theft, the IRS is requesting some personal information, in addition to the CAF number, from tax professionals, or anyone accessing tax related information via the Form 8821 or Form 2848.

The purpose is to confirm the identification of the person calling prior to releasing sensitive information. The intent is to enhance protections for tax professionals and their clients. After establishing the third-party authorization is valid for the account, you must validate the POA/TIA by performing an abbreviated authentication process on the caller’s SSN. The POA/TIA must pass authentication on their SSN to be validated as an authorized third party.

IRM 21.1.3.3.1(7) Clarified third party designee authority timeframe.

The third party designation will automatically expire no later than the due date (not counting extensions) for the filing year on all returns, with the exception of the Form 709, United States Gift Tax Return, that has a three year expiration period from the due date.

Issue 4: SBA Guidance on PPP Loan Forgiveness

The Small Business Administration (SBA), in consultation with the Department of the Treasury, is providing this guidance to address borrower and lender questions concerning forgiveness of Paycheck Protection Program (PPP) loans, as provided for under § 1106 of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), as amended by the Paycheck Protection Program Flexibility Act (Flexibility Act).

Borrowers and lenders may rely on the guidance provided in this document as SBA’s interpretation, in consultation with the Department of the Treasury, of the CARES Act, the Flexibility Act, and the Paycheck Protection Program Interim Final Rules (“PPP Interim Final Rules”).

General Loan Forgiveness FAQs

- Question: Which loan forgiveness application should sole proprietors, independent contractors, or self-employed individuals with no employees complete?

Answer: Sole proprietors, independent contractors, and self-employed individuals who had no employees at the time of the PPP loan application and did not include any employee salaries in the computation of average monthly payroll in the Borrower Application Form automatically qualify to use the Loan Forgiveness Application Form 3508EZ or lender equivalent and should complete that application.

- Question: Can PPP lenders use scanned copies of documents, E-signatures, or E-consents for loan forgiveness applications and loan forgiveness documentation?

Answer: Yes. All PPP lenders may accept scanned copies of signed loan forgiveness applications and documents containing the information and certifications required by SBA Form 3508, 3508EZ, or lender equivalent. Lenders may accept any form of E-consent or E-signature that complies with the requirements of the Electronic Signatures in Global and National Commerce Act (P.L. 106-229). If electronic signatures are not feasible, then when obtaining a wet ink signature without in-person contact, lenders should take appropriate steps to ensure the proper party has executed the document. This guidance does not supersede signature requirements imposed by other applicable law, including by the lender’s primary federal regulator.

- Question: If a borrower submits a timely loan forgiveness application, does the borrower have to make any payments on its loan prior to SBA remitting the forgiveness amount, if any?

Answer: As long as a borrower submits its loan forgiveness application within ten months of the completion of the Covered Period (as defined below), the borrower is not required to make any payments until the forgiveness amount is remitted to the lender by SBA. If the loan is fully forgiven, the borrower is not responsible for any payments. If only a portion of the loan is forgiven, or if the forgiveness application is denied, any remaining balance due on the loan must be repaid by the borrower on or before the maturity date of the loan. Interest accrues during the time between the disbursement of the loan and SBA remittance of the forgiveness amount. The borrower is responsible for paying the accrued interest on any amount of the loan that is not forgiven. The lender is responsible for notifying the borrower of remittance by SBA of the loan forgiveness amount (or that SBA determined that no amount of the loan is eligible for forgiveness) and the date on which the borrower’s first payment is due, if applicable.

Loan Forgiveness Payroll Costs FAQs

- Question: Are payroll costs that were incurred during the Covered Period1 or the Alternative Payroll Covered Period but paid after the Covered Period or the Alternative Payroll Covered Period eligible for loan forgiveness?

Answer: Yes, if the payroll costs are paid on or before the next regular payroll date after the Covered Period or Alternative Payroll Covered Period.

Example: A borrower received its loan before June 5, 2020 and elects to use a 24-week Covered Period. The borrower’s Covered Period runs from Monday, April 20 through Sunday, October 4. The borrower has a biweekly payroll cycle, with a pay period ending on Sunday, October 4. However, the borrower will not make the corresponding payroll payment until the next regular payroll date of Friday, October 9. Under these circumstances, the borrower incurred payroll costs during the Covered Period and may seek loan forgiveness for the payroll costs paid on October 9 because the cost was incurred during the Covered Period and payment was made on the first regular payroll date after the Covered Period.

- Question: Are payroll costs that were incurred before the Covered Period but paid during the Covered Period eligible for loan forgiveness?

Answer: Yes.

Example: A borrower received its loan before June 5, 2020 and elects to use a 24-week Covered Period. The borrower’s Covered Period runs from Monday, April 20 through Sunday, October 4. The borrower has a biweekly payroll cycle, with a payroll cycle ending on Saturday, April 18. The borrower will not make the corresponding payroll payment until Friday, April 24. While these payroll costs were not incurred during the Covered Period, they were paid during the Covered Period and are therefore eligible for loan forgiveness.

- Question: Are borrowers required to calculate payroll costs for partial pay periods?

Answer: If the borrower uses a biweekly or more frequent (e.g., weekly) payroll cycle, the borrower may elect to calculate eligible payroll costs using the eight-week (for borrowers that received their loans before June 5, 2020 and elect this Covered Period length) or 24-week period that begins on the first day of the first payroll cycle following the PPP Loan Disbursement Date (referred to as the Alternative Payroll Covered Period). However, if a borrower pays twice a month or less frequently, it will need to calculate payroll costs for partial pay periods. The Covered Period or Alternative Covered Period for any borrower will end no later than December 31, 2020.

Example: A borrower uses a biweekly payroll cycle. The borrower’s 24-week Covered Period begins on Monday, June 1 and ends on Sunday, November 15. The first day of the borrower’s first payroll cycle that starts in the Covered Period is June 7. The borrower may elect an Alternative Payroll Covered Period that starts on June 7 and ends on November 21 (167 days later). Payroll costs incurred (i.e., the pay was earned on that day) during this Alternative Payroll Covered Period are eligible for loan forgiveness if the last payment is made on or before the first regular payroll date after November 21.

- Question: For purposes of calculating cash compensation, should borrowers use the gross amount before deductions for taxes, employee benefits payments, and similar payments, or the net amount paid to employees?

Answer: The gross amount should be used when calculating cash compensation.

- Question: Are only salaries or wages covered by loan forgiveness, or can a borrower pay lost tips, lost commissions, bonuses, or other forms of incentive pay and have such costs qualify for loan forgiveness?

Answer: Payroll costs include all forms of cash compensation paid to employees, including tips, commissions, bonuses, and hazard pay. Note that forgivable cash compensation per employee is limited to $100,000 on an annualized basis.

- Question: What expenses for group health care benefits will be considered payroll costs that are eligible for loan forgiveness?

Answer: Employer expenses for employee group health care benefits that are paid or incurred by the borrower during the Covered Period or the Alternative Payroll Covered Period are payroll costs eligible for loan forgiveness. However, payroll costs do not include expenses for group health care benefits paid by employees (or beneficiaries of the plan) either pre-tax or after tax, such as the employee share of their health care premium. Forgiveness is not provided for expenses for group health benefits accelerated from periods outside the Covered Period or Alternative Payroll Covered Period.

If a borrower has an insured group health plan, insurance premiums paid or incurred during the Covered Period or Alternative Payroll Covered Period qualify as “payroll costs,” as long as the premiums are paid during the applicable period or by the next premium due date after the end of the applicable period. As noted, only the portion of the premiums paid by the borrower for coverage during the applicable Covered Period or Alternative Payroll Covered Period is included, not any portion paid by employees or beneficiaries or any portion paid for coverage for periods outside the applicable period. Loan Forgiveness Payroll Costs FAQ 8 outlines the rules that apply to owner health insurance.

- Question: What contributions for retirement benefits will be considered payroll costs that are eligible for loan forgiveness?

Answer: Generally, employer contributions for employee retirement benefits that are paid or incurred by the borrower during the Covered Period or Alternative Payroll Covered Period qualify as “payroll costs” eligible for loan forgiveness. The employer contributions for retirement benefits included in the loan forgiveness amount as payroll costs cannot include any retirement contributions deducted from employees’ pay or otherwise paid by employees. Forgiveness is not provided for employer contributions for retirement benefits accelerated from periods outside the Covered Period or Alternative Covered Period. Loan Forgiveness Payroll Costs FAQ 8 outlines the treatment of retirement benefits for owners, which are different from this general approach.

- Question: How is the amount of owner compensation that is eligible for loan forgiveness determined?

Answer: The amount of compensation of owners who work at their business that is eligible for forgiveness depends on the business type and whether the borrower is using an eight-week or 24-week Covered Period. In addition to the specific caps described below, the amount of loan forgiveness requested for owner-employees and self-employed individuals’ payroll compensation is capped at $20,833 per individual in total across all businesses in which he or she has an ownership stake. For borrowers that received a PPP loan before June 5, 2020 and elect to use an eight-week Covered Period, this cap is $15,385. If their total compensation across businesses that receive a PPP loan exceeds the cap, owners can choose how to allocate the capped amount across different businesses. The examples below are for a borrower using a 24-week Covered Period.

C Corporations: The employee cash compensation of a C-corporation owner-employee, defined as an owner who is also an employee (including where the owner is the only employee), is eligible for loan forgiveness up to the amount of 2.5/12 of his or her 2019 employee cash compensation, with cash compensation defined as it is for all other employees. Borrowers are also eligible for loan forgiveness for payments for employer state and local taxes paid by the borrowers and assessed on their compensation, for the amount paid by the borrower for employer contributions for their employee health insurance, and for employer retirement contributions to their employee retirement plans capped at the amount of 2.5/12 of the 2019 employer retirement contribution. Payments other than for cash compensation should be included on lines 6-8 of PPP Schedule A of the loan forgiveness application (SBA Form 3508 or lender equivalent), for borrowers using that form, and do not count toward the $20,833 cap per individual.

S Corporations: The employee cash compensation of an S-corporation owner-employee, defined as an owner who is also an employee, is eligible for loan forgiveness up to the amount of 2.5/12 of their 2019 employee cash compensation, with cash compensation defined as it is for all other employees. Borrowers are also eligible for loan forgiveness for payments for employer state and local taxes paid by the borrowers and assessed on their compensation, and for employer retirement contributions to their employee retirement plans capped at the amount of 2.5/12 of their 2019 employer retirement contribution. Employer contributions for health insurance are not eligible for additional forgiveness for S-corporation employees with at least a 2% stake in the business, including for employees who are family members of an at least 2% owner under the family attribution rules of 26 U.S.C. 318, because those contributions are included in cash compensation. The eligible non-cash compensation payments should be included on lines 7 and 8 of PPP Schedule A of the Loan Forgiveness Application (SBA Form 3508), for borrowers using that form, and do not count toward the $20,833 cap per individual.

Self-employed Schedule C (or Schedule F) filers: The compensation of self-employed Schedule C (or Schedule F) individuals, including sole proprietors, self-employed individuals, and independent contractors, that is eligible for loan forgiveness is limited to 2.5/12 of 2019 net profit as reported on IRS Form 1040 Schedule C line 31 (or 2.5/12 of 2019 net farm profit, as reported on IRS Form 1040 Schedule F line 34) (or for new businesses, the estimated 2020 Schedule C (or Schedule F) referenced in question 10 of “Paycheck Protection Program: How to Calculate Maximum Loan Amounts – By Business Type”3). Separate payments for health insurance, retirement, or state or local taxes are not eligible for additional loan forgiveness; health insurance and retirement expenses are paid out of their net self-employment income. If the borrower did not submit its 2019 IRS Form 1040 Schedule C (or F) to the Lender when the borrower initially applied for the loan, it must be included with the borrower’s forgiveness application.

General Partners: The compensation of general partners that is eligible for loan forgiveness is limited to 2.5/12 of their 2019 net earnings from self-employment that is subject to self-employment tax, which is computed from 2019 IRS Form 1065 Schedule K-1 box 14a (reduced by box 12 section 179 expense deduction, unreimbursed partnership expenses deducted on their IRS Form 1040 Schedule SE, and depletion claimed on oil and gas properties) multiplied by 0.9235.4 Compensation is only eligible for loan forgiveness if the payments to partners are made during the Covered Period or Alternative Payroll Covered Period. Separate payments for health insurance, retirement, or state or local taxes are not eligible for additional loan forgiveness. If the partnership did not submit its 2019 IRS Form 1065 K-1s when initially applying for the loan, it must be included with the partnership’s forgiveness application.

LLC owners: LLC owners must follow the instructions that apply to how their business was organized for tax filing purposes for tax year 2019, or if a new business, the expected tax filing situation for 2020.

Loan Forgiveness Nonpayroll Costs FAQs

- Question: Are nonpayroll costs incurred prior to the Covered Period, but paid during the Covered Period, eligible for loan forgiveness?

Answer: Yes, eligible business mortgage interest costs, eligible business rent or lease costs, and eligible business utility costs incurred prior to the Covered Period and paid during the Covered Period are eligible for loan forgiveness.

Example: A borrower’s 24-week Covered Period runs from April 20 through October 4. On May 4, the borrower receives its electricity bill for April. The borrower pays its April electricity bill on May 8. Although a portion of the electricity costs were incurred before the Covered Period, these electricity costs are eligible for loan forgiveness because they were paid during the Covered Period.

- Question: Are nonpayroll costs incurred during the Covered Period, but paid after the Covered Period, eligible for loan forgiveness?

Answer: Nonpayroll costs are eligible for loan forgiveness if they were incurred during the Covered Period and paid on or before the next regular billing date, even if the billing date is after the Covered Period.

Example: A borrower’s 24-week Covered Period runs from April 20 through October 4. On October 6, the borrower receives its electricity bill for September. The borrower pays its September electricity bill on October 16. These electricity costs are eligible for loan forgiveness because they were incurred during the Covered Period and paid on or before the next regular billing date (November 6).

- Question: If a borrower elects to use the Alternative Payroll Covered Period for payroll costs, does the Alternative Payroll Covered Period apply to nonpayroll costs?

Answer: No. The Alternative Payroll Covered Period applies only to payroll costs, not to nonpayroll costs. The Covered Period always starts on the date the lender makes a disbursement of the PPP loan. Nonpayroll costs must be paid or incurred during the Covered Period to be eligible for loan forgiveness. For payroll costs only, the borrower may elect to use the Alternative Payroll Covered Period to align with its biweekly or more frequent payroll schedule.

- Question: Is interest on unsecured credit eligible for loan forgiveness?

Answer: No. Payments of interest on business mortgages on real or personal property (such as an auto loan) are eligible for loan forgiveness. Interest on unsecured credit is not eligible for loan forgiveness because the loan is not secured by real or personal property. Although interest on unsecured credit incurred before February 15, 2020 is a permissible use of PPP loan proceeds, this expense is not eligible for forgiveness.

- Question: Are payments made on recently renewed leases or interest payments on refinanced mortgage loans eligible for loan forgiveness if the original lease or mortgage existed prior to February 15, 2020?

Answer: Yes. If a lease that existed prior to February 15, 2020 expires on or after February 15, 2020 and is renewed, the lease payments made pursuant to the renewed lease during the Covered Period are eligible for loan forgiveness. Similarly, if a mortgage loan on real or personal property that existed prior to February 15, 2020 is refinanced on or after February 15, 2020, the interest payments on the refinanced mortgage loan during the Covered Period are eligible for loan forgiveness.

Example: A borrower entered into a five-year lease for its retail space in March 2015. The lease was renewed in March 2020. For purposes of determining forgiveness of the borrower’s PPP loan, the March 2020 renewed lease is deemed to be an extension of the original lease, which was in force before February 15, 2020. As a result, the lease payments made under the renewed lease during the Covered Period are eligible for loan forgiveness.

- Question: Covered utility payments, which are eligible for forgiveness, include a “payment for a service for the distribution of . . . transportation” under the CARES Act. What expenses does this category include?

Answer: A service for the distribution of transportation refers to transportation utility fees assessed by state and local governments. Payment of these fees by the borrower is eligible for loan forgiveness.

- Question: Are electricity supply charges eligible for loan forgiveness if they are charged separately from electricity distribution charges?

Answer: Yes. The entire electricity bill payment is eligible for loan forgiveness (even if charges are invoiced separately), including supply charges, distribution charges, and other charges such as gross receipts taxes.

Loan Forgiveness Reductions FAQs

- Question: Will a borrower be subject to a reduction to its forgiveness amount due to a reduction in FTE employees during the Covered Period if the borrower offered to rehire one or more laid off employees, but the employees declined?

Answer: In calculating its loan forgiveness amount, a borrower may exclude any reduction in FTE employees if the borrower is able to document in good faith the following:

(1) an inability to rehire individuals who were employees of the borrower on February 15, 2020 and

(2) an inability to hire similarly qualified individuals for unfilled positions on or before December 31, 2020.

Borrowers are required to inform the applicable state unemployment insurance office of any employee’s rejected rehire offer within 30 days of the employee’s rejection of the offer. The documents that borrowers should maintain to show compliance with this exemption include the written offer to rehire an individual, a written record of the offer’s rejection, and a written record of efforts to hire a similarly qualified individual.

- Question: If a seasonal employer elects to use a 12-week period between May 1, 2019 and September 15, 2019 to calculate its maximum PPP loan amount, what period in 2019 should be used as the reference period for calculating any reductions in the loan forgiveness amount?

Answer: A seasonal employer that elects to use a 12-week period between May 1, 2019 and September 15, 2019 to calculate its maximum PPP loan amount must use the same 12-week period as the reference period for calculation of any reduction in the amount of loan forgiveness.

- Question: When calculating the FTE Reduction Exceptions in Table 1 of the PPP Schedule A Worksheet on the Loan Forgiveness Application (SBA Form 3508 or lender equivalent), do borrowers include employees who made more than $100,000 in 2019 (those listed in Table 2 of the PPP Schedule A Worksheet)?

Answer: Yes. The FTE Reduction Exceptions apply to all employees, not just those who would be listed in Table 1 of the Loan Forgiveness Application (SBA Form 3508 or lender equivalent). Borrowers should therefore include employees who made more than $100,000 in the FTE Reduction Exception line in Table 1 of the PPP Schedule A Worksheet.

- Question: How do borrowers calculate the reduction in their loan forgiveness amount arising from reductions in employee salary or hourly wage?

Answer: Certain pay reductions during the Covered Period or the Alternative Payroll Covered Period may reduce the amount of loan forgiveness a borrower will receive. If the salary or hourly wage of a covered employee is reduced by more than 25% during the Covered Period or the Alternative Payroll Covered Period, the portion in excess of 25% reduces the eligible forgiveness amount unless the borrower satisfies the Salary/Hourly Wage Reduction Safe Harbor (as described in the Loan Forgiveness Application (SBA Form 3508 or lender equivalent)). The examples below assume that each employee is a “covered employee.”

Example 1: A borrower received its PPP loan before June 5, 2020 and elected to use an eight-week covered period. Its full-time salaried employees pay was reduced during the Covered Period from $52,000 per year to $36,400 per year on April 23, 2020 and not restored by December 31, 2020. The employee continued to work on a full-time basis with a full-time equivalency (FTE) of 1.0. The borrower should refer to the “Salary/Hourly Wage Reduction” section under the “Instructions for PPP Schedule A Worksheet” in the PPP Loan Forgiveness Application Instructions. In Step 1, the borrower enters the figures in 1.a, 1.b, and 1.c, and because annual salary was reduced by more than 25%, the borrower proceeds to Step 2. Under Step 2, because the salary reduction was not remedied by December 31, 2020, the Salary/Hourly Wage Reduction Safe Harbor is not met, and the borrower is required to proceed to Step 3. Under Step 3.a., $39,000 (75% of $52,000) is the minimum salary that must be maintained to avoid a penalty. Salary was reduced to $36,400, and the excess reduction of $2,600 is entered in Step 3.b. Because this employee is salaried, in Step 3.e., the borrower would multiply the excess reduction of $2,600 by 8 (if it had instead selected a 24-week Covered Period, it would multiply by 24) and divide by 52 to arrive at a loan forgiveness reduction amount of $400. The borrower would enter on the PPP Schedule A Worksheet, Table 1, $400 as the salary/hourly wage reduction in the column above box 3 for that employee.

Example 2: A borrower received its PPP loan before June 5, 2020 and elected to use a 24-week Covered Period. An hourly employee’s hourly wage was reduced from $20 per hour to $15 per hour during the Covered Period. The employee worked 10 hours per week between January 1, 2020 and March 31, 2020. The borrower should refer to the “Salary/Hourly Wage Reduction” section under the “Instructions for PPP Schedule A Worksheet” in the PPP Loan Forgiveness Application Instructions. Because the employee’s hourly wage was reduced by exactly 25% (from $20 per hour to $15 per hour), the wage reduction does not reduce the eligible forgiveness amount. The amount on line 1.c would be 0.75 or more, so the borrower would enter $0 in the Salary/Hourly Wage Reduction column for that employee on the PPP Schedule A Worksheet, Table 1.

If the same employee’s hourly wage had been reduced to $14 per hour, the reduction would be more than 25%, and the borrower would proceed to Step 2. If that reduction were not remedied as of December 31, 2020, the borrower would proceed to Step 3. This reduction in hourly wage in excess of 25% is $1 per hour. In Step 3, the borrower would multiply $1 per hour by 10 hours per week to determine the weekly salary reduction. The borrower would then multiply the weekly salary reduction by 24 (because the borrower is using a 24-week Covered Period). The borrower would enter $240 in the Salary/Hourly Wage Reduction column for that employee on the PPP Schedule A Worksheet, Table 1. If the borrower applies for forgiveness before the end of the 24-week Covered Period, it must account for the salary reduction (the excess reduction over 25%, or $240) for the full 24-week Covered Period.

Example 3: An employee earned a wage of $20 per hour between January 1, 2020 and March 31, 2020 and worked 40 hours per week. During the Covered Period, the employee’s wage was not changed, but his or her hours were reduced to 25 hours per week. In this case, the salary/hourly wage reduction for that employee is zero, because the hourly wage was unchanged. As a result, the borrower would enter $0 in the Salary/Hourly Wage Reduction column for that employee on the PPP Schedule A Worksheet, Table 1. The employee’s reduction in hours would be taken into account in the borrower’s calculation of its FTE during the Covered Period, which is calculated separately and may result in a reduction of the borrower’s loan forgiveness amount.

- Question: For purposes of calculating the loan forgiveness reduction required for salary/hourly wage reductions in excess of 25% for certain employees, are all forms of compensation included or only salaries and wages?

Answer: For purposes of calculating reductions in the loan forgiveness amount, the borrower should only take into account decreases in salaries or wages.

Issue 5: What is a Covered Employee for PPP Loan Purposes?

The Covered Period is either:

(1) the 24-week (168-day) period beginning on the PPP loan disbursement date, or

(2) if the borrower received its PPP loan before June 5, 2020, the borrower may elect to use an eight-week (56-day) Covered Period.

For example, if the borrower is using a 24-week Covered Period and received its PPP loan proceeds on Monday, April 20, the first day of the Covered Period is April 20 and the last day of the Covered Period is Sunday, October 4. In no event may the Covered Period extend beyond December 31, 2020. 2 Borrowers with a biweekly (or more frequent) payroll schedule may elect to calculate eligible payroll costs using the 24-week (168-day) period (or for loans received before June 5, 2020 at the election of the borrower, the eight-week (56-day) period) that begins on the first day of their first pay period following their PPP loan disbursement date (i.e., the “Alternative Covered Period”). For example, if the borrower is using a 24-week Alternative Payroll Covered Period and received its PPP loan proceeds on Monday, April 20, and the first day of its first pay period following its PPP loan disbursement is Sunday, April 26, the first day of the Alternative Payroll Covered Period is April 26 and the last day of the Alternative Payroll Covered Period is Saturday, October 10. In no event may the Alternative Payroll Covered Period extend beyond December 31, 2020.

Issue 6: E-file Application Revisions Requiring Resubmission

If you have an active e-file application on file and have made changes such as adding a Provider option, Principal or Responsible Official and it has not been resubmitted it will be deleted in 90 days.

If the application is not resubmitted and the 90 days has not elapsed since the changes were made, the application can be resubmitted by an authorized individual. Prior to resubmission, Principals and/or Responsible Officials are required to sign the Terms of Agreement when adding individual(s) and/or Provider Option(s) to an e-file application. The Terms of Agreement include the Privacy Act and Paperwork Reduction Act Notice, and the FBI Privacy Act Statement.

If 90 days has elapsed and your application has been deleted, contact the e-help Desk at 866-255-0654 for assistance with resubmitting your application.

Issue 7: Taxpayer Advocate Service Can Assist with Correcting Economic Impact Payment Amounts

While the IRS has taken steps to quickly issue almost 160 million Economic Impact Payments (EIPs) to eligible individuals, many eligible individuals are still waiting to receive their EIP or the full amount for which they are eligible. Over the past several months, TAS has been working with taxpayers on non-EIP issues as best it could in light of limited IRS operations, but they have not been able to address taxpayer concerns with EIP issues.

TAS has established procedures and has committed to correct EIPs in the following five scenarios:

Scenario #1: Eligible individuals who used the Non-Filer Tool and claimed at least one qualifying child but did not receive the qualifying child portion of the EIP. The IRS will issue supplemental EIPs with respect to those qualifying children in the coming weeks.

Scenario #2: Eligible individuals who filed Form 8379, Injured Spouse Allocation (or can complete and return the Form 8379) and did not receive their EIP. The IRS will issue the injured spouse’s portion of the EIP in the coming weeks.

Scenario #3: Eligible individuals whose EIP was based on a 2018 or 2019 tax return where the IRS adjusted the return for a math error that negatively impacted the original amount of the EIP ( e.g., Qualifying Child, Adjusted Gross Income, filing status). The IRS can work with the taxpayer to resolve the math error and, if appropriate, issue a payment for the additional EIP amount.

Scenario #4: Eligible individuals who were victims of identity theft and did not receive an EIP or did not receive the correct EIP amount. The IRS will adjust the EIP once the identity theft issue is resolved.

Scenario #5: Eligible individuals who did not receive an EIP because they filed a joint return with a deceased or incarcerated spouse and their EIP payment was not issued, was returned, or was canceled. The IRS will recalculate the EIP and issue it only to the non-deceased/non-incarcerated spouse.

The IRS will begin making direct deposits and mailing checks in the upcoming weeks. For those taxpayers who received a prior payment, the additional payment generally will be made in the same manner as the first. If the taxpayer previously received a debit card, however, the reissued EIP will be sent via paper check.

Previously, the IRS did not have a process to resolve EIP cases, so there was nothing TAS could do to assist taxpayers. However, given these recent changes, TAS will now accept cases for taxpayers whose EIP issues fall within one of the categories described and otherwise meet TAS criteria above beginning August 10, 2020.

IR-2020-192 50,000 Spouses to Get Catch-Up Economic Impact Payments

The Internal Revenue Service will soon send catch-up Economic Impact Payment checks to about 50,000 individuals whose portion of the EIP was diverted to pay their spouse’s past-due child support.

These catch-up payments are due to be issued in early-to-mid-September. They will be mailed as checks to any eligible spouse who submitted Form 8379, Injured Spouse Allocation, along with their 2019 federal income tax return, or in some cases, their 2018 return. These spouses do not need to take any action to get their money. The IRS will automatically issue the portion of the EIP that was applied to the other spouse’s debt.

The IRS is aware that some individuals did not file a Form 8379, Injured Spouse Allocation, and did not receive their portion of the EIP for the same reason above. These individuals also do not need to take any action and do not need to submit a Form 8379. The IRS does not yet have a timeframe but will automatically issue the portion of the EIP that was applied to the other spouse’s debt at a later date.

Issue 8: IRS Issues Proposed Regulations for TCJA’s Simplified Tax Accounting Rules for Small Business

The Internal Revenue Service today issued proposed regulations updating various tax accounting regulations to adopt the simplified tax accounting rules for small businesses under the Tax Cuts and Jobs Act (TCJA).

For tax years beginning in 2019 and 2020, these simplified tax accounting rules apply for taxpayers having inflation-adjusted average annual gross receipts of $26 million or less (known as the gross receipts test).

Taxpayers classified as tax shelters cannot use the simplified rules even if they would meet the gross receipts test.

Prior to the TCJA, certain taxpayers could determine whether they were eligible to figure taxable income under the cash method of accounting by meeting a different gross receipts test. That gross receipts test was met if the taxpayer’s average annual gross receipts for all prior taxable years did not exceed $5 million.

After the TCJA, a taxpayer meets the gross receipts test and can use the cash method if average annual gross receipts for the three-taxable year period ending immediately before the current taxable year are $25 million (adjusted for inflation) or less.

The TCJA also exempted taxpayers meeting the gross receipts test from the uniform capitalization rules. Tax reform also added an exception to the requirement to use an inventory method if their inventory is treated as non-incidental materials and supplies, or in accordance with the applicable financial statement (AFS). If they do not have an AFS, taxpayers can use their books and records.

In addition, guidance is provided for small businesses with long-term construction contracts and the requirements for exemption from the percentage-of-completion method and the uniform capitalization rules. For taxpayers with income from long-term contracts reported under the percentage-of-completion method, guidance is provided for applying the look-back method after repeal of the corporate alternative minimum tax and enactment of the base erosion and anti-abuse tax (BEAT).

Issue 9: IRS Provides Guidance on Recapturing Excess Employment Tax Credits

The Internal Revenue Service has issued a temporary regulation and a proposed regulation to reconcile advance payments of refundable employment tax credits and recapture the benefit of these credits when necessary.

The regulations authorize the assessment of erroneous refunds of the credits paid under both the Families First Coronavirus Response Act (Families First Act) and Coronavirus Aid, Relief and Economic Security Act (CARES Act).

The Families First Act generally requires employers with fewer than 500 employees to provide paid sick leave for up to 80 hours and paid family leave for up to 10 weeks if the employee is unable to work or telework due to COVID-19 specific related reasons. Eligible employers are entitled to fully refundable tax credits to cover the cost of the leave required to be paid.

The CARES Act provides an additional credit for employers experiencing economic hardship due to COVID-19. Eligible employers who pay qualified wages to their employees are entitled to an employee retention credit.

The IRS has revised the Form 941, Form 943, Form 944 and Form CT-1, so that employers may use these returns to claim the paid sick and family leave and employee retention credits.

Employers may also receive advance payment of the credits up to the total allowable amounts. The IRS has created Form 7200, Advance Payment of Employer Credits Due To COVID-19, which employers may use to request an advance of the credits. Employers are required to reconcile any advance payments claimed on Form 7200 with total credits claimed and total taxes due on their employment tax returns.

Any refund of these credits paid to a taxpayer that exceeds the amount the taxpayer is allowed is an erroneous refund for which the IRS must seek repayment.

Issue 10: Treasury, IRS Issues Guidance on Reporting Qualified Sick and Family Leave Wages Paid

Treasury and IRS provided guidance in Notice 2020-54 to employers requiring them to report the amount of qualified sick and family leave wages paid to employees under the Families First Coronavirus Response Act (FFCRA) on Form W-2.

Employers will be required to report these amounts either on Form W-2, Box 14, or in a statement provided with the Form W-2. The guidance provides employers with optional language to use in the Form W-2 instructions for employees.

The wage amount that the notice requires employers to report on Form W-2 will provide self-employed individuals who are also employees with the information necessary to determine the amount of any sick and family leave equivalent credits they may claim in their self-employed capacities.

Issue 11: The Joint Board for the Enrollment of Actuaries Announces Temporary Waiver of “Physical Presence” Education Requirement for Enrolled Actuaries

The Joint Board for the Enrollment of Actuaries has provided enrolled actuaries with notice that it is waiving the physical presence requirement for continuing professional education (CPE) credit for any formal programs conducted from Jan. 1, 2020, through Dec. 31, 2022. The Joint Board made this decision due to the hardships that the COVID-19 pandemic has caused, particularly those involving traveling to and participating in gatherings requiring close contact with others.

This waiver applies to all enrolled actuaries, whether they are in active or inactive status. Joint Board regulations require that no less than 1/3 of the total hours of continuing professional education credit required for an enrollment cycle must be obtained by participation in a formal program or programs. Without this waiver, an enrolled actuary earning credit hours for a formal program would have to participate in the program in the same physical location with at least two other participants engaged in substantive pension service.

Enrolled actuaries are still required to earn the same number of credit hours under formal programs that would otherwise be required. Although the physical presence requirement is temporarily waived, the other requirements for a formal program continue to apply, including all requirements for a qualifying program under the Joint Board regulations, attendance by at least three participants engaged in substantive pension service, and an opportunity for participants to interact with the instructor during the program. In addition, the certificate of completion or instruction issued by a qualifying sponsor of the program must indicate that the program is a formal program.

An active or inactive enrolled actuary who did not receive a waiver notice by email should contact the Joint Board at [email protected].

Issue 12: Executive Order Defers Employee Social Security Taxes – But Not So Fast – It’s Voluntary – Caution Should Be Used

There are several aspects of the order (below) employers should consider with great caution:

- There is an expectation that the legality of the order will be challenged through litigation.

- If the deferral is applied, it is not clear when the deferred amount would be required to be paid (although the order directs the secretary to explore “avenues” to eliminate the obligation).

Normally, payroll tax is a 6.2% tax on an employee’s salary (up to $137,700 annually for 2020) that is withheld from their paycheck to fund Social Security, and the employer pays another 6.2%. The CARES Act gave businesses the option to defer their share of this year’s payroll taxes, and now, Trump’s recent executive order instructs the Treasury Department to defer collection of the employee-side payroll tax payment for those making up to about $104,000 during the period of Sept. 1 to Dec. 31.

Note: This is only a deferral of collection and voluntary on the employee’s request. The amount will have to be collected later unless Congress see fit to forgive. A portion of the Executive Order is below.

Deferring Certain Payroll Tax Obligations. The Secretary of the Treasury is hereby directed to use his authority pursuant to 26 U.S.C. 7508A to defer the withholding, deposit, and payment of the tax imposed by 26 U.S.C. 3101(a), and so much of the tax imposed by 26 U.S.C. 3201 as is attributable to the rate in effect under 26 U.S.C. 3101(a), on wages or compensation, as applicable, paid during the period of September 1, 2020, through December 31, 2020, subject to the following conditions:

(a) The deferral shall be made available with respect to any employee the amount of whose wages or compensation, as applicable, payable during any bi-weekly pay period generally is less than $4,000, calculated on a pre-tax basis, or the equivalent amount with respect to other pay periods.

(b) Amounts deferred pursuant to the implementation of this memorandum shall be deferred without any penalties, interest, additional amount, or addition to the tax.

Authorizing Guidance. The Secretary of the Treasury shall issue guidance to implement this memorandum.

Tax Forgiveness. The Secretary of the Treasury shall explore avenues, including legislation, to eliminate the obligation to pay the taxes deferred pursuant to the implementation of this memorandum.

Issue 13: IRS Updates Form 433-D to Reflect Two Changes

- The instructions add the following: If a low-income taxpayer (at or below 250% of Federal poverty guidelines) defaults on an installment agreement, then the reinstatement fee is $43. The reduced reinstatement fee is waived if the taxpayer agrees to make electronic payments through a debit instrument. For low-income taxpayers unable to make electronic payments through a debit instrument, the reduced reinstatement fee is reimbursed upon completion of the installment agreement.

- The instructions add the following term to the agreement: The taxpayer authorizes the IRS to contact third parties and to disclose the taxpayer’s tax information to third parties in order to process and administer the installment agreement over its duration.

Issue 14: U.S. Tax Court Update on Procedural Changes Due to COVID-19

1) The Court will accept electronically filed stipulated decisions bearing digital image signatures. The Court’s Practitioners’ Guide to Electronic Case Access and Filing and the Petitioners’ Guide to Electronic Case Access and Filing have been revised to reflect this adjustment.

2) The Court has provided additional guidance on procedures related to the submission of documentary evidence.

3) The Court has provided additional guidance on procedures related to subpoenas.

4) A practitioner admitted to practice, in good standing, and with informed consent by petitioner(s) may limit an appearance to a specific date or activity listed on the Limited Entry of Appearance form.

The Court has updated Administrative Order 2020-03 to clarify that limited entries of appearance may be filed with respect to those trial sessions that were canceled due to COVID-19.

These procedures will remain in effect until further notice.

Issue 15: IRS Taking New Steps to Ensure People with Children Receive the $500 Economic Impact Payments

The Internal Revenue Service continues to look for ways to help people who were unable to provide their information in time to receive Economic Impact Payments for their children. As part of that effort, the Internal Revenue Service announced today it will reopen the registration period for federal beneficiaries who didn’t receive $500 per child payments earlier this year.

The IRS urges certain federal benefit recipients to use the IRS.gov Non-Filers tool starting Aug. 15 through Sept. 30 to enter information on their qualifying children to receive the supplemental $500 payments.

Those eligible to provide this information include people with qualifying children who receive Social Security retirement, survivor or disability benefits, Supplemental Security Income (SSI), Railroad Retirement benefits and Veterans Affairs Compensation and Pension (C&P) benefits and did not file a tax return in 2018 or 2019.

The IRS anticipates the catch-up payments, equal to $500 per eligible child, will be issued by mid-October.

Used the Non-Filers tool after May 5? No action needed.

For those Social Security, SSI, Department of Veterans Affairs and Railroad Retirement Board beneficiaries who have already used the Non-Filers tool to provide information on children, no further action is needed. The IRS will automatically make a payment in October.

Didn’t use the IRS Non-Filers tool yet? Provide information by Sept. 30

For those who received Social Security, SSI, RRB or VA benefits and have not used the Non-Filers tool to provide information on their child, they should register online by Sept. 30 using the Non-Filers: Enter Payment Info Here tool, available exclusively on IRS.gov. Remember, anyone who filed or plans to file either a 2018 or 2019 tax return should file the tax return and not use this tool.

For those unable to access the Non-Filers tool, they may submit a simplified paper return following the procedures described in this FAQ on IRS.gov.

Any beneficiary who misses the Sept. 30 deadline will need to wait until next year and claim it as a credit on their 2020 federal income tax return.

Those who received their original Economic Impact Payment by direct deposit will also have any supplemental payment direct deposited to the same account. Others will receive a check.

Eligible recipients can check the status of their payments using the Get My Payment tool on IRS.gov. In addition, a notice verifying the $500-per-child supplemental payment will be sent to each recipient and should be retained with other tax records.

Other Non-Filers can still get a payment; must act by Oct. 15

Though most Americans have already received their Economic Impact Payments, the IRS reminds people with little or no income and who are not required to file tax returns that they remain eligible to receive an Economic Impact Payment.

People in this group should also use the Non-Filers’ tool – but they need to act by Oct. 15 to receive their payment this year.

Anyone who misses the Oct. 15 deadline will need to wait until next year and claim it as a credit on their 2020 federal income tax return.

Some EIPs to spouses of deceased taxpayers were cancelled. The IRS is actively working on a systemic solution to reissue payments to surviving spouses of deceased taxpayers who were unable to deposit the initial EIPs paid to the deceased and surviving spouse. For EIPs that have been cancelled or returned, the surviving spouse will automatically receive their share of the EIP.

Issue 16: IRS Pending Check Payments and Payment Notices

If your client mailed a check with or without a tax return, it may still be unopened in the backlog of mail the IRS is processing due to COVID-19. Any payments will be posted as the date IRS received them rather than the date the agency processed them. To avoid penalties and interest, taxpayers should not cancel their checks and should ensure funds continue to be available so the IRS can process them. To provide fair and equitable treatment, the IRS is providing relief from bad check penalties for dishonored checks the agency received between March 1 and July 15 due to delays in IRS processing. However, interest and penalties may still apply.

Due to high call volumes, the IRS suggests waiting to contact the agency about any unprocessed paper payments still pending. See www.irs.gov/payments for options to make payments other than by mail.

16A. The IRS has suspended the mailing of three notices – the CP501, the CP503 and the CP504 – that go to taxpayers who have a balance due on their taxes. As the IRS works to stop these mailings at their processing centers, some taxpayers and tax professionals may still receive these notices during the next few weeks due to delivery of existing mailings.

Issue 17: Identity Theft Form 14039-B Now Available for Business and Other Identities

Form 14039-B, an identity theft affidavit for businesses and other entities, will make it easier for businesses, estates, trusts and tax-exempt organizations to report identity theft to the IRS. The form is now publicly available under the “Business” tab on the Identity Theft Central page on IRS.gov.

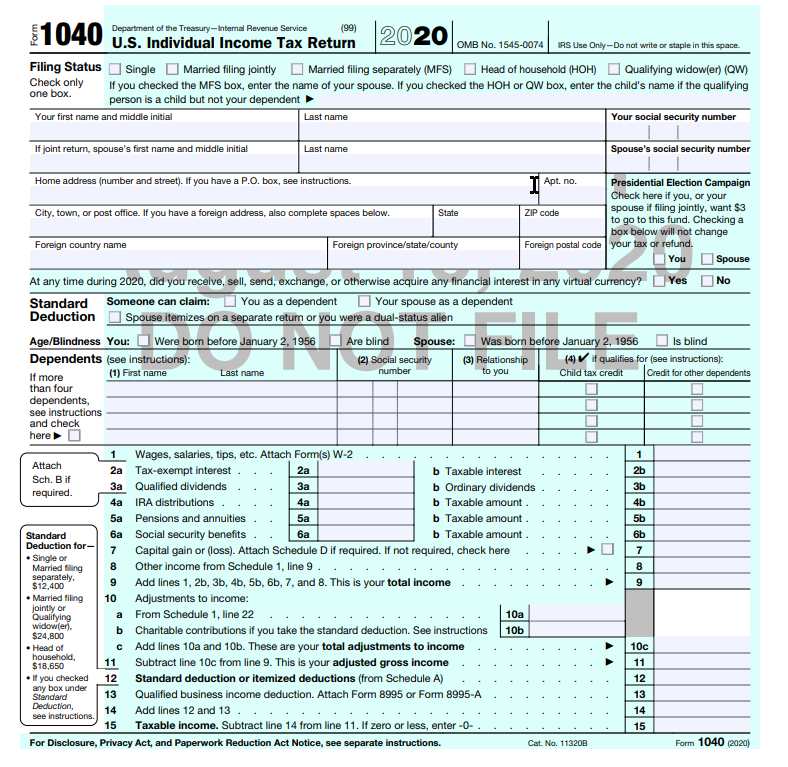

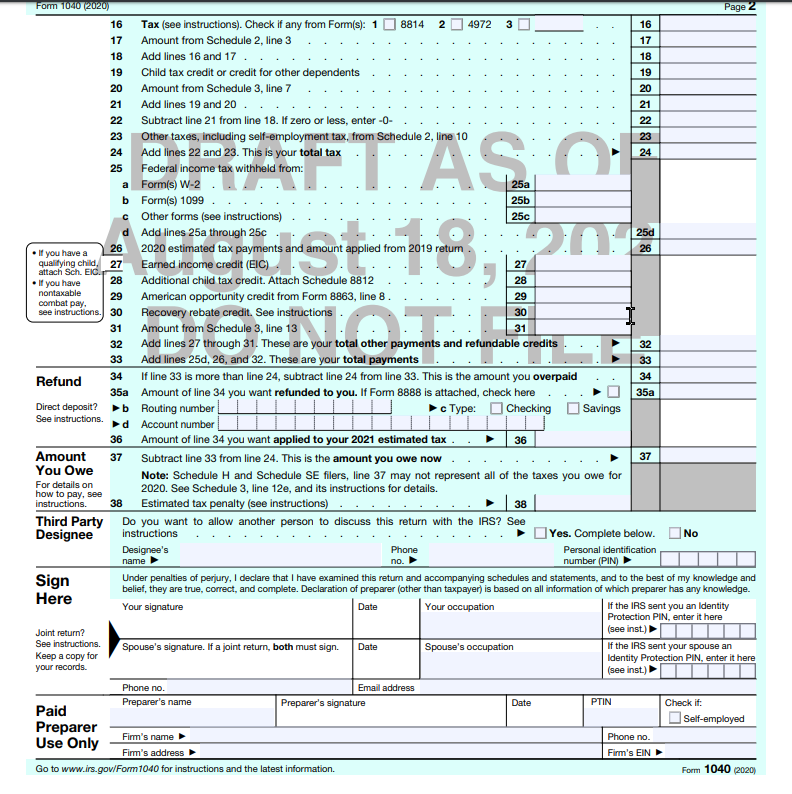

Issue 18: 2020 Draft of Form 1040 Issued

Note: Changes

- Virtual currency question just before the Standard Deduction area

- Line 10b for Charitable Contribution of up to $300.00 cash has been added.

- Line 30 Recovery Rebate Reconciliation line has been added – Letter 1444 can assist.

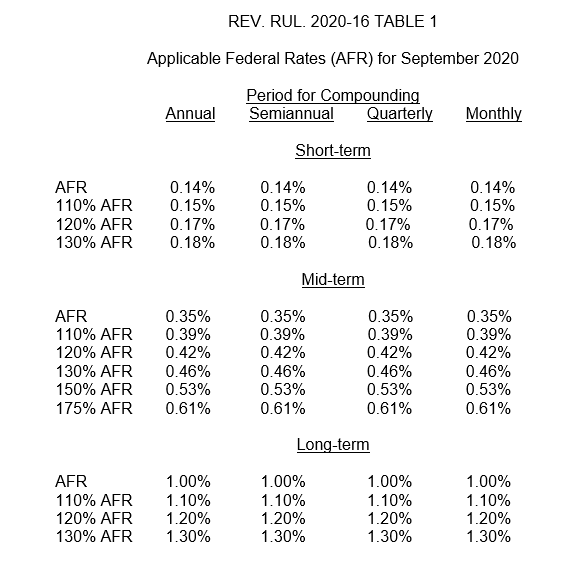

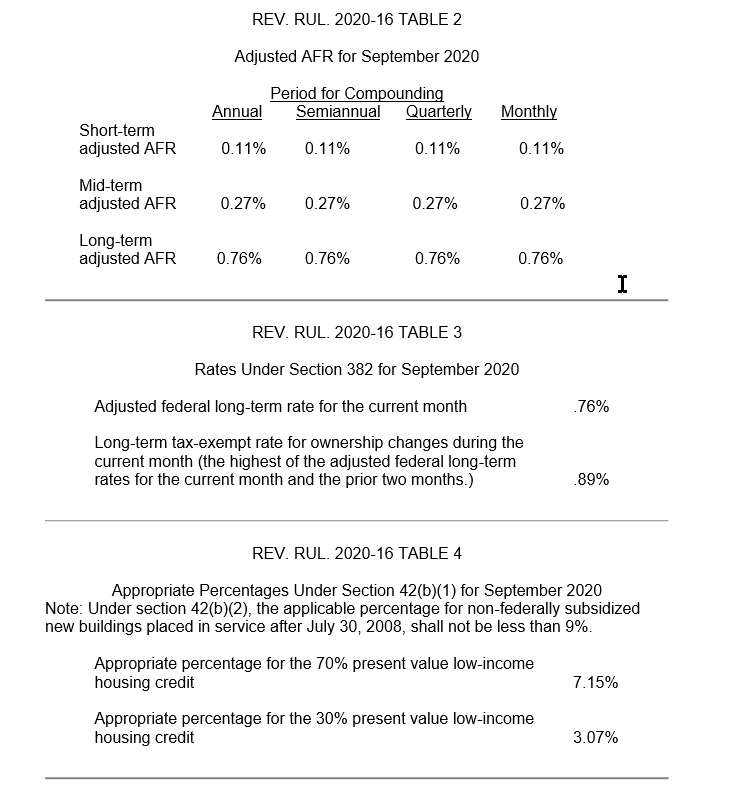

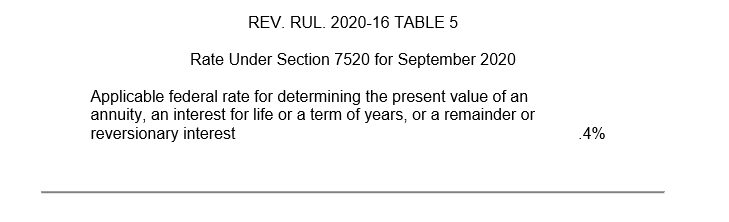

Issue 19: Applicable Federal Rates (AFR) for September 2020 – Rev. Rul. 2020-16

![]() Basics & Beyond Resources

Basics & Beyond Resources

- Blog Page

- Resource List

- Webinar & Seminar Schedules

- Get Registered!

- Note: Paid attendees can request a link to the replay of any previously recorded webinar presentations by emailing us at [email protected]