Tax Newsletter: Paid Leave Credits

Reminder: Register for the Virtual Tax Seminars: Each session includes 7 hours of Tax Law and 1 hour of Ethics

Virtual Tax Seminar Information is available here: Fall & Year-End Tax Seminars

In This Issue

- Paid Leave Credits Available for Providing Leave to Employees Caring for Individuals Obtaining or Recovering from COVID Immunization

- R. 3684: To Authorize Funds for Federal-aid Highways, Highway Safety Programs, and Transit Programs, and for Other Purposes

- CCA Say When an Employer May “Designate” a Payroll Tax Payment – Chief Counsel Advice 202129007

- Treasury, IRS Provide Additional Guidance to Employers Claiming the Employee Retention Credit for the Third and Fourth Quarters of 2021

- Treasury, IRS Provide Gross Receipts Safe Harbor for Employers Claiming the Employee Retention Credit

- IRS Announces a New Online Application to Access the FIRE System

- Bills from the Hill

- Revenue Procedure 2021-31 Depreciation of Passenger Automobile Tables

- IRS Assistance, Verification of Identity

- IRS Provides Relief for Certain Employers Claiming the Work Opportunity Tax Credit

- IRS Adds McLaren Model to Plug-in Vehicle Credit List

- SBSE-05-0421-0018 Interim Guidance for Initial Contact (IRM 5.1.10.3)

- Potential 2021 Federal Unemployment Tax Act (FUTA) Credit Reductions

- Updated Questions on Assisting an Individual with the Enrollment of the Advanced Child Tax Credit Payments

- Bankruptcy – What IRS Information is Available

- Update Business Information within 60 Days of Any Change

- IRS Closing P.O. Boxes in 2022

- Applicable Federal Rates for September 2021, Rev. Rul. 2021-16

Introduction to the New TaxPros Account

One of our latest efforts is the Tax Pro Account that launched in July. This new, groundbreaking application allows for all-digital interaction between tax professionals and taxpayers on authorizations and sets the stage for several advancements on third-party authorizations in the future.

As many taxpayers know, tax records with the IRS are private and secure. The IRS may only share a taxpayer’s data with the taxpayer’s designated third-party representative or designee. For years, the IRS has facilitated these third-party authorizations by using two forms, Form 2848, Power of Attorney and Declaration of Representative, and Form 8821, Tax Information Authorization. Power of Attorney (POA) is a designation given by the taxpayer to those tax professionals who are licensed to represent the taxpayer before the IRS on tax matters.

The Tax Information Authorization (TIA) gives designated third parties, often a tax professional, permission to access and view the taxpayer’s records held by the IRS. This is often used to resolve a tax issue or to prepare prior-year tax returns.

Until last year, the processing of these authorization forms was a paper operation. Forms were faxed or mailed to IRS at three locations nationwide, and employees worked from one of the three sites. Then the COVID-19 national emergency declaration resulted in nationwide office closures, leaving IRS unable to process Forms 2848 and 8821 and record the authorizations to the Centralized Authorization File (CAF) database as they normally would.

This emergency resulted in extended wait times that far exceeded the usual five-day turnaround on processing these forms. In the fall of 2020, IRS expanded telework options by quickly creating an e-fax process. The e-fax, which was invisible to tax professionals, allowed some of the work to be done by IRS employees remotely. Then, in January, IRS launched “Submit Forms 2848 and 8821 Online,” an online upload process that allows tax professionals to upload these forms and for the acceptance of images of electronic signatures.

While this alleviated some of the challenges, the mailed, faxed, or uploaded forms still had to be processed manually by employees and recorded to the CAF database.

In continued efforts to improve the taxpayer and tax pro experience, IRS recently introduced the Tax Pro Account on IRS.gov. Now, tax professionals can digitally initiate an online POA or TIA request for an individual taxpayer by entering the tax professional’s and taxpayer’s information. Upon submission of the authorization by the tax professional, the request is automatically sent to the individual taxpayer’s Online Account for approval and signature.

The taxpayer accesses their own Online Account, selects the “Authorization” tab at the top and can reject or digitally sign the request. When the taxpayer submits the signed request, if the request information is accurate and the tax professional is in good standing with the IRS, the POA or TIA will generally record immediately to the CAF database, though recording could take up to 48 hours. Approved online POAs and TIAs display in both the Tax Pro Account and the Online Account.

The key is for taxpayers who do not have an Online Account to set one up. IRS highly recommends taxpayers sign up for this secure online service, even if they do not use a tax professional. To get an Online Account, they must pass a rigorous identity proofing process to keep their account safe.

Each year, the Online Account gains more and more functionality. Now, clients/taxpayers can not only approve authorization requests, but they can see their past Economic Impact Payment amounts, get to the Child Tax Credit Update Portal, see selected IRS notices, and access transcripts plus perform other tasks. Clients can also see payment history and make payments online.

Issue 1: Paid Leave Credits Available for Providing Leave to Employees Caring for Individuals Obtaining or Recovering from COVID Immunization

IRS has updated the frequently asked questions (FAQ’s) on the paid sick and family leave tax credits under the American Rescue Plan Act of 2021 (ARP). The updates clarify that eligible employers can claim the credits for providing leave to employees to accompany a family or household member or certain other individuals to obtain immunization relating to COVID-19 or to care for a family or household member or certain other individuals recovering from the immunization.

The paid sick and family leave credits reimburse eligible employers for the cost of providing paid sick and family leave for reasons related to COVID-19. The revised FAQs make clear this includes leave taken by employees to care for certain individuals to obtain immunization relating to COVID-19 or to recover from immunization relating to COVID-19. This new reason for paid sick or family leave also applies for the comparable credits for self-employed individuals.

The FAQs include information on how eligible employers may claim the paid sick and family leave credits, including how to file for and compute the applicable credit amounts, and how to receive advance payments for and refunds of the credits. Under the ARP, eligible employers, including businesses and tax-exempt organizations with fewer than 500 employees and certain governmental employers, may claim tax credits for qualified leave wages and certain other wage-related expenses (such as health plan expenses and certain collectively bargained benefits).

Self-employed individuals may claim comparable credits on the Form 1040, U.S. Individual Income Tax Return.

The text of the 2,700+ page infrastructure bill (H.R. 3684) was released, and the package addresses public transit, highways, water systems, clean energy, and high-speed internet services.

What we are monitoring:

Cryptocurrency reporting. The bill requires brokers to report the basis and character of gain or loss of transactions involving “digital assets” (a new term that the bill uses to describe cryptocurrencies) just like brokers now report the basis and character of gain or loss of stock and bond sales. Brokers will also have to report certain other transfers of digital assets, even if the transfer is not a sale or exchange.

In addition, any business that receives more than $10,000 of digital assets will have to report such receipt just as it must report the receipt of more than $10,000 of cash.

Employer retention credit ending early. The bill shortens the time frame for using the employer retention credit (ERC). While the American Rescue Plan Act of 2021 had just recently extended the time for taking the credit to December 31, 2021, the bill now says, except for wages paid by a recovery startup business, only wages paid until September 30 are to be taken into account for determining the ERC.

The bill will be taken up after congressional recess but faces a long haul for passage.

Issue 3: CCA Say When an Employer May “Designate” a Payroll Tax Payment – Chief Counsel Advice 202129007

IRS Chief Counsel was asked whether a particular taxpayer could designate a payment to the trust fund portion of certain past-due employment taxes.

The IRS indicated that the general rule is that a taxpayer may designate a voluntary payment—however, to be recognized by the IRS:

- The taxpayer must be specific.

- Must make the designation in writing and

- The designation must be made at the time the payment is made.

But if the payment is made through IRS collection measures, the IRS is not required to designate the payment according to the directions of the taxpayer.

The IRS also recognized that in many cases taxpayers may make partial payments towards assessments for more than one tax period. If the taxpayer fails to provide specific written instructions vis-à-vis the application of the payment, the IRS is permitted to apply the payment in a manner “serving the best interests of the government.” That is, the IRS may apply the payment to satisfy the non-trust fund portion of the employment taxes first with any balance being applied to the trust fund portion.

Issue 4: Treasury, IRS Provide Additional Guidance to Employers Claiming the Employee Retention Credit for the Third and Fourth Quarters of 2021

- 2301(a) of the Coronavirus Aid, Relief, and Economic Security Act created a refundable payroll tax credit (“the Employee Retention Credit” or “ERC”).

Phase 1:

For 2020, the ERC could be claimed by eligible employers who paid qualified wages after March 12, 2020, and before January 1, 2021, if they experienced a full or partial suspension of their operations or a significant decline in gross receipts (“eligible employers”). The credit is equal to 50% of qualified wages paid, including qualified health plan expenses. The maximum credit per employee is $5,000.

Phase 2

In December 2020, the Taxpayer Certainty and Disaster Tax Relief Act of 2020 extended the ERC to qualified wages paid after December 31, 2020, and before July 1, 2021, and modified the calculation of the ERC for qualified wages paid in 2021.

Phase 3

- 9651 of the American Rescue Plan Act of 2021 extended the ERC for wages paid after June 30, 2021, and before January 1, 2022, and made a few other changes to the ERC.

Guidance on the employee retention credit, including guidance for employers who pay qualified wages after June 30, 2021, and before January 1, 2022, and additional guidance on miscellaneous issues that apply to the employee retention credit in both 2020 and 2021 are included in Notice 2021-49. The notice amplifies prior guidance regarding the employee retention credit provided in Notice 2021-20 and Notice 2021-23.

Notice 2021-49 addresses changes made by the American Rescue Plan Act of 2021 (ARP) to the employee retention credit that are applicable to the third and fourth quarters of 2021.

Those changes include, among other things:

- Making the credit available to eligible employers that pay qualified wages after June 30, 2021, and before January 1, 2022.

- Under the new notice, an ERC may be claimed by an eligible employer for qualified wages paid in the third and fourth calendar quarters of 2021. An eligible employer is an employer carrying on a trade or business within the meaning of §162 of the Code,

- Whose trade or business’s operation is fully or partially suspended due to orders from a governmental authority limiting commerce, travel, or group meetings due to COVID-19.

- That experiences a decline in gross receipts (as defined in Notices 2021-20 and 2021-23); or

- Under the new notice, an ERC may be claimed by an eligible employer for qualified wages paid in the third and fourth calendar quarters of 2021. An eligible employer is an employer carrying on a trade or business within the meaning of §162 of the Code,

- Is a recovery startup business.

- Expanding the definition of eligible employer to include “recovery startup businesses.”

- A recovery startup business is an employer that:

- Is not otherwise an eligible employer under conditions (1) or (2) of the preceding sentence; that.

- Began carrying on a trade or business after February 15, 2020.

- A recovery startup business is an employer that:

- With average annual gross receipts for the three tax years preceding the quarter in which it claims the credit of no more than $1 million (with rules § 448(c)(3) for their calculation if the entity has not been in existence for three years and by reference to the entity’s predecessor.

- Accordingly, in the third and fourth calendar quarters of 2021, a recovery startup business that is a small eligible employer within the meaning of § 3134(c)(3)(A)(ii) may treat all wages paid with respect to an employee during the quarter as qualified wages. The determination of whether an employer is a recovery startup business is made separately for each calendar quarter.

- For example, if an eligible employer is a recovery startup business in the third quarter of 2021 but is not a recovery startup business in the fourth quarter of 2021 because it is an eligible employer due to a full or partial suspension or a decline in gross receipts during the fourth quarter of 2021, the $50,000 limitation applies to the third quarter of 2021 but does not apply to the fourth quarter of 2021.

- Also, the notice states that although §3134(c)(2)(C) (which prescribes how organizations exempt from tax under §§ 501(a) and (c) may qualify for the ERC) does not specifically provide that these organizations can be an eligible employer due to being a recovery startup business, the IRS and Treasury have determined it is appropriate to treat them as eligible employers if they meet the requirements to be a recovery startup.

- Similarly, although the statute does not specifically state that recovery startup businesses may be treated as small eligible employers (those with 500 employees or fewer), the notice provides that Treasury and the IRS have concluded it is appropriate to read the small eligible employer rule in § 3134(c)(3)(A)(ii)(II) as if it applies to recovery startup businesses.

- Modifying the definition of qualified wages for “severely financially distressed employers”. § 3134(c)(3)(C)(ii) defines a “severely financially distressed employer” as an employer that is an eligible employer based on a decline in gross receipts, but the gross receipts for the eligible employer for the calendar quarter are less than 10% of the gross receipts as compared to the same calendar quarter in calendar year 2019, instead of less than 80%.

- Accordingly, for purposes of the employee retention credit for the third and fourth calendar quarters of 2021, an eligible employer with gross receipts that are less than 10% of the gross receipts for the same calendar quarter in calendar year 2019 (or 2020, if the employer was not in existence in 2019) is a severely financially distressed employer.

- If an employer is a severely financially distressed employer, § 3134(c)(3)(C)(i) provides that, notwithstanding § 3134(c)(3)(A)(i) (which limits qualified wages for large eligible employers to wages paid to an employee for time the employee is not providing services due to a full or partial suspension or a decline in gross receipts), the term “qualified wages” means wages paid by such employer with respect to an employee during any calendar quarter. Accordingly, for the third and fourth calendar quarters of 2021, a severely financially distressed employer that is a large eligible employer may treat all wages paid to its employees during the quarter in which the employer is considered severely financially distressed as qualified wages.

- Providing that the employee retention credit does not apply to qualified wages taken into account as payroll costs in connection with a shuttered venue grant under § 324 of the Economic Aid to Hard-Hit Small Businesses, Non-Profits, and Venues Act, or a restaurant revitalization grant under § 5003 of the ARP.

- Another change under the ARPA rules for the ERC under § 3134 is that, for the third and fourth quarters of 2021, eligible employers claim the credit against the employer’s share of Medicare tax (or equivalent portion of Tier 1 tax under the Railroad Retirement Tax Act) rather than, as previously, against the employer’s share of Social Security tax (or its equivalent Railroad Retirement Tax Act portion).

- Although the limit on the maximum ERC in the first half of 2021 of 70% of up to $10,000 of an employee’s qualified wages per calendar quarter (i.e., $7,000) continues to apply to the third and fourth calendar quarters of 2021, the notice notes that a separate credit limit of $50,000 per calendar quarter applies to recovery startup businesses (after application of the $10,000 wage limit).

Notice 2021-49 also provides guidance on several miscellaneous issues with respect to the employee retention credit for both 2020 and 2021. This guidance responds to various questions that the Treasury Department and the IRS have been asked about the employee retention credit, including:

- The definition of full-time employee and whether that definition includes full-time equivalents – The definition of full-time employees for purposes of the ERC (full-time equivalents need not be included in determining whether an employer is large or small, and the notice notes that full-time status is irrelevant to identifying qualifying wages).

- The treatment of tips as qualified wages and the interaction with the § 45B credit – The treatment of tips as qualified wages (included, if treated as wages under § 3121(a) or compensation under § 3231(e)(3) and they otherwise meet the requirements for qualified wages qualify.

- The timing of the qualified wages deduction disallowance and whether taxpayers that already filed an income tax return must amend that return after claiming the credit on an adjusted employment tax return, and

- Whether wages paid to majority owners and their spouses may be treated as qualified wages.

- The timing of the disallowance of a deduction for wages by the amount of the ERC.

- The alternative quarter election in determining whether there has been a decline in gross receipts.

- How to calculate gross receipts of employers that came into existence in the middle of a calendar quarter for purposes of the gross receipts safe harbor in Section III.E of Notice 2021-20.

Reporting

Eligible employers will report their total qualified wages and the related health insurance costs for each quarter on their employment tax returns (generally, Form 941) for the applicable period. If a reduction in the employer’s employment tax deposits is not sufficient to cover the credit, certain employers may receive an advance payment from the IRS by submitting Form 7200, Advance Payment of Employer Credits Due to COVID-19.

How does an Eligible Employer obtain Form 7200 and where should it send its completed form to receive the advance credit? Is there a minimum advance amount that can be claimed on a Form 7200? (Updated July 2, 2020)?

An Eligible Employer may obtain the Form 7200, Advance Payment of Employer Credits Due to COVID-19 online and may fax its completed form to 855-248-0552.

After July 2, 2020, the minimum advance amount that can be claimed on a Form 7200 is $25. A Form 7200 requesting an advance payment of less than $25 will not be processed. Taxpayers can claim credits of less than $25 on the Form 941.

How do Eligible Employers report qualified leave wages? (Updated March 17, 2021)

Eligible Employers must report the amount of qualified sick and family leave wages paid to employees under the EPSLA and Expanded FMLA on Form W-2, Wage and Tax Statement, either in Box 14, or in a statement provided with the Form W-2. Eligible Employers must report qualified sick and family leave wages paid in 2020 on the 2020 Form W-2. Eligible Employers must report qualified sick and family leave wages paid in 2021 on the 2021 Form W-2.

Is an Eligible Employer that does not claim the tax credits for qualified leave wages required to report the sick leave wages and family leave wages paid to employees in Box 14 of Form W-2 or a separate statement? (Added March 15, 2021)

No. If an Eligible Employer does not claim the tax credits for qualified leave wages, it will be treated as having elected under §§ 7001(e)(2) and 7003(e)(2) of the FFCRA not to apply the tax credits available under §§ 7001 and 7003. Accordingly, the sick leave wages and family leave wages it paid to employees are not considered qualified sick leave wages or qualified family leave wages under the FFCRA and those wages do not have to be reported to employees in Box 14 of Form W-2, or in a statement provided with Form W-2.

Are governmental employers that are not permitted under the FFCRA to claim the tax credits for qualified leave wages required to report sick leave wages and family leave wages paid to employees in Box 14 of Form W-2 or a separate statement? (Added March 15, 2021)

No. The government of the United States, the government of any State or political subdivision thereof, or any agency or instrumentality of those governments (governmental employers) are not permitted to claim the tax credits under §§ 7001 and 7003 of the FFCRA. Because governmental employers cannot claim the tax credits, the sick leave wages and family leave wages paid to employees are not considered qualified leave wages under the FFCRA. Therefore, those wages do not have to be reported to employees in Box 14 of Form W-2, or in a statement provided with Form W-2.

This rule does not apply to Tribal governments that are Eligible Employers permitted to claim the tax credits for sick leave wages and family leave wages paid to employees.

Is an Eligible Employer that did not claim the tax credits for qualified leave wages, but reported the sick leave wages and family leave wages paid to employees in 2020 in Box 14 of Form W-2 or a separate statement required to issue a Form W-2c, Corrected Wage and Tax Statement, or provide a corrected statement? (Added March 15, 2021)

Yes. If an Eligible Employer that did not claim the tax credits for qualified leave wages reported the sick leave wages and family leave wages paid to employees in Box 14 of Form W-2 or in a statement provided with Form W-2, the Eligible Employer must either furnish a Form W-2c or provide a corrected statement to employees correcting the erroneous reporting. However, the Eligible Employer should not file Form W-2c with the SSA solely to correct the amount in Box 14.

Issue 5: Treasury, IRS Provide Gross Receipts Safe Harbor for Employers Claiming the Employee Retention Credit

Treasury and the Internal Revenue Service (IRS) issued a safe harbor allowing employers to exclude certain items from their gross receipts solely for determining eligibility for the Employee Retention Credit (ERC).

Revenue Procedure 2021-33 provides a safe harbor permitting employers to exclude certain amounts from gross receipts solely for determining eligibility for the ERC. These amounts are:

- The amount of the forgiveness of a Paycheck Protection Program (PPP) Loan.

- Shuttered Venue Operators Grants under the Economic Aid to Hard-Hit Small Businesses, Non-Profits, and Venues Act; and

- Restaurant Revitalization Grants under the American Rescue Plan Act of 2021.

An employer elects to apply the safe harbor by excluding these amounts solely for determining whether it is an eligible employer for a calendar quarter for purposes of claiming the ERC on its employment tax return.

Revenue Procedure 2021-33 requires employers to apply the safe harbor consistently for determining eligibility for the ERC. The employer must exclude the amounts from their gross receipts for each calendar quarter in which gross receipts are relevant to determining eligibility to claim the ERC. The employer claiming the credit must also apply the safe harbor to all employers treated as a single employer under the aggregation rules.

An employer is not required to apply this safe harbor, and the safe harbor does not permit the exclusion of these amounts from gross receipts for any other federal tax purpose.

Issue 6: IRS Announces a New Online Application to Access the FIRE System

The IRS will be making significant improvements to the Filing Information Returns Electronically (FIRE) application process for new users. The new online Information Returns (IR) Application for Transmitter Control Code (TCC) is scheduled to deploy on September 26, 2021. The new application will be available on IRS.gov and will replace both the current Form 4419 and the Fill-in Form 4419 on the FIRE System.

New users will be required to authenticate their identities and create a new account through IRS Secure Access Account to access the new online IR Application for TCC. Details on what users need to verify their identities can be found at www.IRS.gov/SecureAccess. Existing Secure Access (SA) users will be able to use their existing SA account.

Any filer, including corporations, partnerships, employers, estates, and trusts, who files 250 or more Forms 1097, 1042-S, 1098, 1099, 3921, 3922, 5498, 8027, 8955-SSA or W-2G for any calendar year must file their information returns electronically.

In late 2022, to better secure the FIRE system, existing FIRE users will also be required to transition to a stronger identity proofing authentication process. The target timeframe for this move is Fall 2022.

A quick reminder that the Taxpayer First Act of 2019 (TFA) required the IRS to increase electronic filing. Counsel has now issued proposed regulations to reduce the current 250-return threshold to 100 in 2022 and to 10 in 2023.

Issue 7: Bills from the Hill

H.R.4016 – USER FEE Act. To impose a tax on the use of certain electric highway vehicles to fund the Highway Trust Fund.

H.R.4061 – Fair Accounting for Condominium Construction Act. To provide an exception to percentage of completion method of accounting for certain residential construction contracts.

H.R.4095 – Workforce Development Through Post-Graduation Scholarships Act of 2021. To exclude certain post-graduation scholarship grants from gross income in the same manner as qualified scholarships to promote economic growth.

H.R.4141 – Promotion and Expansion of Private Employee Ownership Act of 2021. To expand the availability of employee stock ownership plans in S corporations, and for other purposes.

H.R.4164 – Charitable Conservation Easement Program Integrity Act of 2021. To limit the charitable deduction for certain qualified conservation contributions.

H.R.4173 – Tax-Free Pell Grant Act. To extend and modify the American Opportunity Tax Credit, and for other purposes.

H.R.4174 – Expand American Educational Opportunity Act of 2021. To extend and modify the American Opportunity Tax Credit, and for other purposes.

H.R.4184 – Taxpayer Protection and Preparer Proficiency Act of 2021. To set minimum standards for tax return preparers.

S.2191 – Workforce Development Through Post-Graduation Scholarships Act of 2021. To exclude certain post-graduation scholarship grants from gross income in the same manner as qualified scholarships to

S.2206 – Young American Savers Act of 2021. To create Federal child savings accounts, and for other purposes.

S.2215 – Veterinary Medicine Loan Repayment Program Enhancement Act. To provide for an exclusion for assistance provided to participants in certain veterinary student loan repayment or forgiveness programs.

S.2256 – Charitable Conservation Easement Program Integrity Act of 2021. To limit the charitable deduction for certain qualified conservation contributions.

S.2455 – Tax-Free Pell Grant Act. To expand the exclusion of Pell Grants from gross income, and for other purposes.

H.R.4287 – USA Workforce Tax Credit Act. To allow a credit against tax for charitable donations to nonprofit organizations providing workforce training and education scholarships to qualified elementary and secondary students.

S.2387 – Small Business Tax Fairness Act. To improve the deduction for qualified business income.

S.2415 – Long-Term Care Affordability Act. To expand the use of retirement plan funds to obtain long-term care insurance, and for other purposes.

S.2452 – Encouraging Americans to Save Act. To provide matching payments for retirement savings contributions by certain individuals, and for other purposes.

H.R.4558 – Tax Fairness for the Self-Employed Act of 2021. To allow the deduction for health insurance costs in computing self-employment taxes.

H.R.4572 – Health Insurance Marketplace Affordability Act of 2021. To provide an age rating adjustment to the applicable percentage used to determine the credit for coverage under qualified health plans.

H.R.4585 – Everyday Philanthropist Act. To provide for flexible giving accounts, and for other purposes.

H.R.4672 – ABLE Employment Flexibility Act. To allow employers to contribute to ABLE accounts in lieu of retirement plan contributions.

S.2420 – E-BIKE Act. To provide a credit for the purchase of certain new electric bicycles.

S.2435 – Modern, Clean, and Safe Trucks Act of 2021. To repeal the excise tax on heavy trucks and trailers, and for other purposes.

S.2455 – Tax-Free Pell Grant Act. To expand the exclusion of Pell Grants from gross income, and for other purposes.

S.2465 – American Opportunity Tax Credit Enhancement Act of 2021. to make the American Opportunity Tax Credit fully refundable, and for other purposes.

S.2602 – Retirement Security Flexibility Act of 2021. To provide for an additional nondiscrimination safe harbor for automatic contribution arrangements.

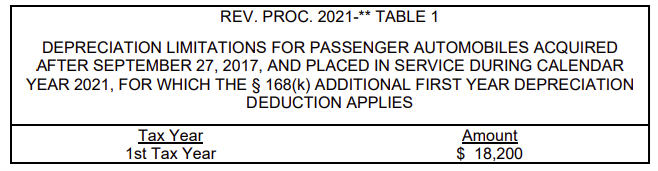

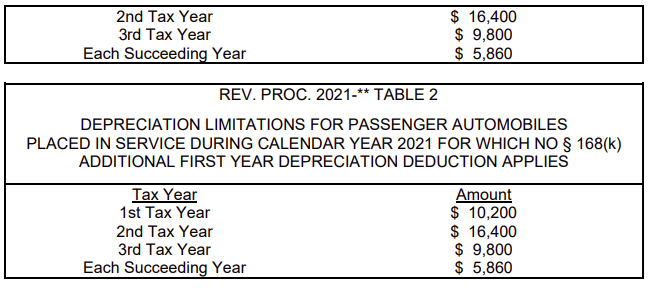

Issue 8: Revenue Procedure 2021-31 Depreciation of Passenger Automobile Tables

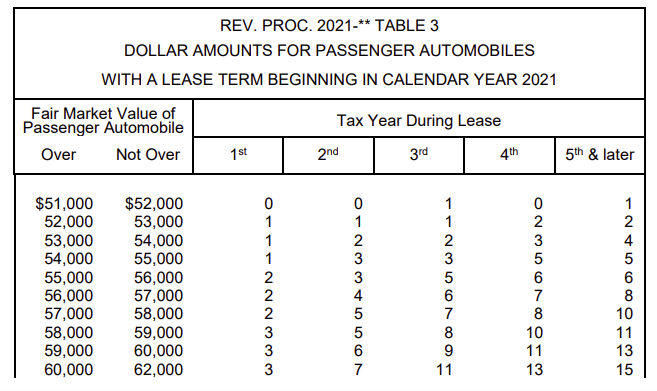

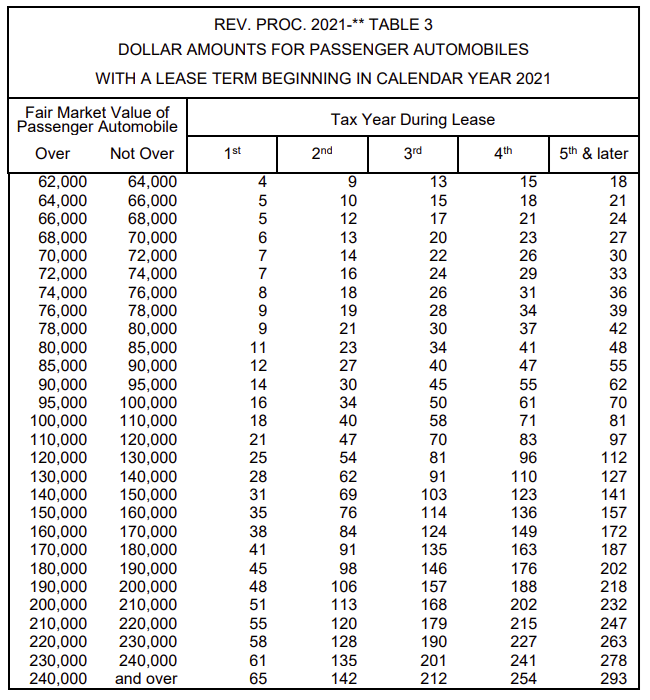

Revenue Procedure 2021-31 provides: (1) two tables of limitations on depreciation deductions for owners of passenger automobiles placed in service by the taxpayer during calendar year 2021; and (2) a table of dollar amounts that must be used to determine income inclusions by lessees of passenger automobiles with a lease term beginning in calendar year 2021. The tables detailing these depreciation limitations and amounts used to determine lessee income inclusions reflect the automobile price inflation adjustments required by § 280F(d)(7). For purposes of this revenue procedure, the term “passenger automobiles” includes trucks and vans.

Inclusions in Income of Lessees of Passenger Automobiles. A taxpayer must follow the procedures in § 1.280F-7(a) for determining the inclusion amounts for passenger automobiles with a lease term beginning in calendar year 2021. In applying these procedures, lessees of passenger automobiles should use Table 3 of this revenue procedure.

Issue 9: IRS Assistance, Verification of Identity

Taxpayers and tax pros should be ready to verify their identity when calling the IRS. Clients and tax professionals calling the IRS will be asked to verify their identity. This is part of the agency’s ongoing efforts to keep taxpayer data secure from identity thieves. To make sure that taxpayers do not have to call back, the IRS reminds taxpayers to have the following information ready:

- Social Security numbers (SSN) and birth dates for those who were named on the tax return.

- An Individual Taxpayer Identification Number (ITIN) letter if the taxpayer has one instead of an SSN.

- The filing status: single, head of household, married filing joint or married filing separate.

- The prior-year tax return.

Phone assistors may need to verify taxpayer identity with information from the return before answering certain questions

- A copy of the tax return in question.

- Any IRS letters or notices received by the taxpayer.

By law, IRS telephone assistors will only speak with the client or to the client’s legally designated representative. If taxpayers or tax professionals are calling about someone else’s account, they should be prepared to verify their identities and provide information about the person they are representing.

Before calling about a third-party, they should have the following information available:

- Verbal or written authorization from the third-party to discuss the account.

- The ability to verify the taxpayer’s name, SSN or ITIN, tax period, and tax forms filed Preparer Tax Identification Number or PIN if a third-party designee. One of these forms, which is current, completed and signed: Form 8821, Tax Information Authorization Form 2848, Power of Attorney and Declaration of Representative

Issue 10: IRS Provides Relief for Certain Employers Claiming the Work Opportunity Tax Credit

The Internal Revenue Service it is providing transition relief to certain employers claiming the Work Opportunity Tax Credit (WOTC). The WOTC is a federal income tax credit available to employers that hire certified members of certain groups specified in the Internal Revenue Code who face significant barriers to employment, including Designated Community Residents or Qualified Summer Youth Employees.

The IRS Notice 2021-43, which extends the 28-day deadline for employers to submit a request to a designated local agency (DLA) to certify that an employee hired between January 1 and October 8 of this year is a Designated Community Resident or a Qualified Summer Youth Employee. To be certified as a Designated Community Resident or a Qualified Summer Youth Employee under the WOTC, an employee must have a principal place of residence within an Empowerment Zone where the employee continuously resides.

Empowerment Zone designations terminated on Dec. 31, 2020, but the Taxpayer Certainty and Disaster Tax Relief Act of 2020, enacted as Division EE of the Consolidated Appropriations Act, 2021, permitted the designations to be extended through 2025. On May 26, 2021, all Empowerment Zone designations were extended from Dec. 31, 2020 to Dec. 31, 2025. The transition relief under this notice allows employers to submit Form 8850 (Pre-Screening Notice and Certification Request for the Work Opportunity Credit) for these employees until Nov. 8, 2021.

The notice also provides guidance to certain employers who submitted a Form 8850 to a DLA for these employees during the period of transition relief and received a denial due to the termination of Empowerment Zone designations on Dec. 31, 2020, or who received a certification before Empowerment Zone designations were extended.

The WOTC has been subject to several legislative extensions and modifications since its enactment by the Small Business Job Protection Act of 1996. The amount of the tax credit under WOTC equals a percentage of qualified wages paid in a given tax year to an employee certified by the DLA as being a member of the one of the groups specified in the law.

Issue 11: IRS Adds McLaren Model to Plug-in Vehicle Credit List

The IRS has added a McClaren model to the list of vehicles that are eligible for the plug-in electric drive motor vehicle credit.

Taxpayers purchasing one of the vehicles on the qualifying vehicle list can claim the Code Sec. 30D(a) credit using Form 8936, Qualified Plug-in Electric Drive Motor Vehicle Credit (Including Qualified Two- or Three-Wheeled Plug-in Electric Vehicles).

| McLaren | ||

| Model Year | Vehicle Description | Credit Amount |

| 2022 | Artura | $4,585 |

2022 Audi, BMW. and Lincoln models now listed. The list of vehicles eligible for the qualified plug-in electric drive motor vehicle credit now includes the following:

The 2022 Audi e-tron Sportback, Audi e-tron, Audi A7 TFSI e Quattro, and Audi Q5 TFSI e Quattro. These models qualify for a $7500 credit.

The 2022 BMW 330e, BMW 330e drive, BMW 530e, BMW 530e xDrive, BMW 740e xDrive. These models qualify for a $5836 credit.

The 2022 Lincoln Aviator Grand Touring. This model qualifies for a $6534 credit.

Issue 12: SBSE-05-0421-0018 Interim Guidance for Initial Contact (IRM 5.1.10.3)

This memorandum provides interim guidance on the issuance of a third-party contact notice along with an appointment letter until Collection Policy revises IRM 5.1.10.3.

The purpose of this memorandum is to provide uniform guidance in Revenue Officer (RO) case work as to whether an appointment letter (Letter 725)and a third-party contact notice (Letter 3164) may be mailed at the same time.

Background: § 7602(c) directs IRS employees on how and when they may contact a third party in relation to the determination and collection of a tax liability. Prior to the Taxpayer First Act (TFA) amendment, § 7602(c) required the Service to provide “reasonable notice in advance” that the Service may contact persons other than the taxpayer.

On July 1, 2019, the TFA amended § 7602(c)(1) to require the Service to provide a notice to taxpayers that it intends to contact third parties during a specified period (not to exceed a year) and to provide the notice at least 45 days in advance of making the contact, unless otherwise provided by the Secretary. The advance notice shall not be issued unless the IRS intends to make a third-party contact during the designated one-year period.

The new rules apply to contacts made after August 15, 2019.

Current Procedure: Internal Revenue Manual (IRM) 5.1.10.3(4) states that the RO may schedule a field visit with a taxpayer or representative by sending an appointment letter (Letter 725). A completed Form 9297, Summary of Taxpayer Contact, should also be included, letting the taxpayer or representative know which items will be needed at the time of the appointment.

Procedural Change:

The following changes are effective April 22, 2021, and will remain in effect until incorporated in IRM 5.1.10.3, Initial Contact. IRM 5.1.10.3 (4)

A Revenue Officer may attempt scheduling a field visit with a taxpayer or representative by sending an appointment letter, such as Letter 725, Meeting Scheduled with Taxpayer. A completed Form 9297, Summary of Taxpayer Contact, should also be included, letting the taxpayer or representative know which items will be needed at the time of the appointment.

The revenue officer should conduct the appointment to determine if a third-party contact is necessary. If third-party contact is necessary, see IRM 25.27.1.3, Notification Requirements.

In special circumstances a revenue officer may issue the third-party contact notice (Letter 3164) required by section 7602(c)(1) at the same time the Letter 725 or other initial contact letter is issued when the revenue officer concludes that the third-party contact is the only means to obtain the necessary information.

Such special circumstances, for example, would include prior experience with the same taxpayer who has demonstrated a pattern of uncooperative or unresponsive behavior that delays the collection of the tax due where third-party contacts were needed to obtain or verify necessary information. The revenue officer should consult with management prior to sending both letters simultaneously and document the ICS case history (establishing why they intend to contact third parties).

Issuing an appointment letter does not represent taking a timely initial contact action unless it results in actual contact with the taxpayer or the representative within initial contact time frames as provided in IRM 5.1.10.3.1. If the taxpayer and/or representative receives an appointment letter and calls to confirm or reschedule, the officer should at a minimum ensure the taxpayer has received Pub 1 and answer any questions, confirm contact information, and secure one or more levy sources.

Note: During the scheduled field visit, the officer is required to follow initial contact procedures, located in IRM 5.1.10.3.2. For initial contact procedures on ATAT cases, see IRM 5.20.12.2, Initial Contact.

Issue 13: Potential 2021 Federal Unemployment Tax Act (FUTA) Credit Reductions

Virgin Islands had a Title XII advance balance on January 1, 2021, so employers in this jurisdiction are potentially subject to a reduction in FUTA credit on their IRS Form 940 for 2021, if the outstanding advance is not repaid by November 10, 2021:

2021 Potential

(1) Virgin Islands has passed at least two consecutive January 1’s with an outstanding Federal advance and employers are therefore subject to a

FUTA credit reduction.

(2) For each consecutive January 1 a state passes with an outstanding advance, following the second one, employers in the state are subject to an additional 0.3% reduction in their FUTA credit.

(3) Following their third consecutive January 1 with an outstanding advance states are subject to an additional FUTA credit reduction called the 2.7 add-on. A description of this add-on is in FUTA 3302(c)(2)(B). This value is based on wages and tax contributions for the calendar year of 2020.

(4) Virgin Islands is also potentially subject to the Benefit Cost Rate (BCR) additional credit reduction formula for having passed five consecutive January 1’s with an outstanding Federal advance- FUTA section 3302 (c) (2). This value is based on wages and tax contributions for calendar year 2020.

(5) The potential FUTA credit reduction for 2021 is calculated by adding the credit reduction due to having an outstanding advance plus the reduction from the 2.7% add-on or the BCR add-on, which can be waived and replaced by the 2.7 add-on, FUTA § 3302(c)(2)(C).

(6) Provisions in regulations describe circumstances under which states may qualify for relief from FUTA credit reductions through avoidance, caps on reductions and fifth year waivers.

Issue 14: Updated Questions on Assisting an Individual with the Enrollment of the Advanced Child Tax Credit Payments

An individual who is not required to file a tax return has asked me to assist them as they input their information into the Child Tax Credit Non-Filer Signup Tool. May I provide assistance?

Yes. You may assist another person, such as a friend or family member or through a volunteer tax return preparation service like VITA or TCE, as long as you have that individual’s permission. You may provide them assistance by helping them understand how to use the Child Tax Credit Non-filer Sign-up Tool or inputting their information into the tool for them. Do not complete the Child Tax Credit Non-Filer Sign-up Tool without an individual’s direct participation because the tool requires the individual to declare that the information entered is true, correct, and complete and enter his or her own signature.

If you are in the business of preparing tax returns for other people, you must follow the rules governing the disclosure or use of tax return information provided in §§ 6713 and 7216 of the Code.

IRS Wages and Investment Update WI-21-0821-1042 Internal Memo on the Child Tax Credit – Instructions for IRS Employees Who May Receive Questions

IRM 21.6.3.4.2.8 – Clarified alternate income rule to show if claiming EITC, they may use prior earned income, but are not required.

- Certain individuals who get less than the full amount of the nonrefundable child tax credit is entitled to this refundable credit. The additional child tax credit may result in a refund even if no tax is owed. See IRM 21.6.3.4.1.24, Child Tax Credit, for rules and regulations pertaining to the child tax credit

prior to addressing Additional Child Tax Credit.

- Taxpayers must claim the qualifying child as a dependent to be a qualifying child for the Child Tax Credit.

- Earned income generally does not include workfare payments to the extent subsidized under a state program for work experience (including work associated with the refurbishing of publicly assisted housing if sufficient

private sector employment is not available), work in community service programs, or certain Medicaid waiver payments (see IRM 21.6.6.4.37,

Qualified Medicaid Waiver Payments/Difficulty of Care Payments, for more information). However, the taxpayer may include certain Medicaid waiver payments received as wages or self-employment income in earned income if

they benefit from the inclusion (even if this payment is excluded on Schedule 1).

- For tax year 2015 and subsequent, filers of Form 2555 or Form 2555-EZ cannot claim the credit.

- For taxpayers indicating a religious (e.g., Amish/Mennonite) or conscience-based objection to obtaining a TIN, refer to IRM 21.6.1.6.1, Determining the Exemption/Dependent Deduction.

- A bona fide resident of Puerto Rico must have 3 or more children to qualify for the Additional Child Tax Credit if the taxpayer is excluding all of their income under § 933.

- Bona fide residents of Puerto Rico do not have taxable income if it is excluded under § 933, which applies to income derived from sources within Puerto Rico.

- Amounts received for services performed as an employee of the United States or any agency thereof is not subject to exclusion under § 933.

- If a taxpayer has U.S. Government wages, they must file Form 1040 or Form 1040A and use Schedule 8812 to claim the additional child tax credit. If the taxpayer has excluded income under § 933, they must use the worksheet in Publication 972, Child Tax Credit and Credit for Other Dependents, to compute the child tax credit. Depending on the circumstances, the taxpayer may be entitled to claim the child tax credit, as well as the additional child tax credit, even if they have fewer than three qualifying children.

- See IRM 3.38.147.9.3, Additional Child Tax Credit, (ACTC)(Refundable), for additional information. If the taxpayer calls regarding additional child tax credit on a Form 1040PR, prepare a Form 4442, if applicable.

NOTE: Bona fide residents of the other U.S. territories (American Samoa, the Commonwealth of the Northern Mariana Islands, Guam, and the U.S. Virgin Islands) who are eligible for the CTC or ACTC would claim those credits on an income tax return filed with the U.S. territory, not with the IRS.

- A special rule applies for certain taxpayers affected by disaster areas shown below. Qualified individuals whose earned income in the applicable taxable year is less than the earned income in the preceding taxable year may elect to use their earned income of the preceding taxable year when figuring ACTC. Taxpayers who do not claim EITC should enter “PYEI” and the dollar amount of the prior year earned income on the dotted line for ACTC.

Taxpayers who also claim EITC must follow the election they made when they figured EITC.

The main home of qualified individuals must have been in:

- the Hurricane Harvey disaster area on August 23, 2017.

- the Hurricane Irma disaster area on September 4, 2017.

- the Hurricane Maria disaster area on September 16, 2017.

- the California wildfire disaster area on October 8, 2017.

- any Presidentially declared disaster that occurred in 2018 or 2019, but before December 21, 2019.

NOTE: Verify the taxpayer was in the qualified disaster area via the IRS Disaster Assistance Program.

These claims are centralized in Austin and Philadelphia (International). Reassign the case per the AM Site Specialization Temporary Holding Numbers. Use category code KATX and OFP 710-82365 when processing these claims.

- As part of the Taxpayer Certainty and Disaster Tax Relief Act of 2020, individuals whose earned income for tax year 2020 is less than the earned income for 2019 may elect to use their 2019 earned income when figuring ACTC. Taxpayers should enter “PYEI” and the dollar amount of the prior year

earned income on the dotted line for ACTC. Taxpayers who elect to use PYEI in figuring their 2020 ACTC, and who also claim EITC, may also elect to use PYEI when figuring their 2020 EITC, but they are not required to do so.

Issue 15: Bankruptcy – What IRS Information is Available

If the client owes past due federal taxes that they cannot pay, bankruptcy may be an option. Other options include an IRS payment plan or an offer in compromise.

For individuals, the most common type of bankruptcy is a Chapter 13. Before considering filing a Chapter 13 here are some things you should know:

- The client must file all required tax returns for tax periods ending within four years of your bankruptcy filing.

- During the bankruptcy they must continue to file, or get an extension of time to file, all required returns.

- During the bankruptcy case they should pay all current taxes as they come due.

- Failure to file returns and/or pay current taxes during the bankruptcy may result in the case being dismissed.

Partnerships and corporations file bankruptcy under Chapter 7 or Chapter 11 of the bankruptcy code. Individuals may also file under Chapter 7 or Chapter 11.

For additional tax information on bankruptcy, refer to Publication 908, Bankruptcy Tax Guide and Publication 5082, What You Should Know about Chapter 13 Bankruptcy and Delinquent Returns.

Other types of bankruptcy include Chapters 9, 12 and 15. Cases under these chapters of the bankruptcy code involve municipalities, family farmers and fisherman, and international cases.

https://www.irs.gov/businesses/small-businesses-self-employed/declaring-bankruptcy

- How can the client notify the IRS that they have filed bankruptcy?

- If the client is listed the IRS as a creditor in the bankruptcy, the IRS will receive electronic notice about the case from the U.S. Bankruptcy Courts within a day or two of the petition date. If the client is not sure if IRS received notice, they may call the Centralized Insolvency Operation at 800-973-0424and give them the bankruptcy case number.

- How can the client find out about a refund when the client is in bankruptcy?

- Call 800-973-0424with the bankruptcy case number and ask to be referred to a bankruptcy specialist.

- What if the client does not know the bankruptcy case number?

- Call 800-222-8029 – at the U.S. Bankruptcy Courts and follow the prompts.

Issue 16: Update Business Information within 60 Days of Any Change

Calling it a key security issue, the IRS urged businesses, charities and other entities with an Employer Identification Numbers (EIN) to update their information when there has been a change in the responsible party or contact information, such as their address. It is critical that the IRS have accurate information in cases of identity theft or other fraud issues related to EINs or business accounts.

IRS regulations require EIN holders to update responsible party information within 60 days of any change by filing Form 8822-B, Change of Address or Responsible Party – Business. It is critical that the IRS have accurate information in cases of identity theft or other fraud issues related to EINs or business accounts.

The data around the “responsible parties” for business-type entities is often outdated or incorrect, meaning that the IRS does not have accurate records of who to contact for identity theft issues. This means a time-consuming process to identify the point of contact so the IRS can inquire about a suspicious filing.

As a result, the IRS intends to step up its awareness efforts aimed at businesses, partnerships, trusts and estates, charities and other entities that are EIN holders. Starting in August, the IRS will begin sending letters to approximately 100,000 EIN holders where it appears the responsible party is outdated.

All EIN applications (mail, fax, electronic) must disclose the name and Taxpayer Identification Number (Social Security number, Individual Taxpayer Identification Number or EIN) of the true principal officer, general partner, grantor, owner, or trustor.

The IRS defines the responsible party as the individual or entity who “controls, manages, or directs the applicant entity and the disposition of its funds and assets.”

Unless the applicant is a government entity, the responsible party must be an individual, not an entity. If there is more than one responsible party, the entity may list whichever party the entity wants the IRS to recognize as the responsible party.

EINs are to be used strictly for tax administration purposes.

Issue 17: IRS Closing P.O. Boxes in 2022

The IRS is closing several individual payment P.O. boxes (or lockbox addresses) in the San Francisco, Calif., and Hartford, Conn., areas beginning Jan. 1, 2022. Payments mailed to these closed payment locations after Jan. 1 will be returned to sender.

To help ensure timely receipt, encourage your clients to avoid mailing to these closing addresses. Check Where to File on IRS.gov for active addresses before mailing payments. If you or your client receive an IRS payment letter, send payment to the address found in the letter. The IRS also encourages taxpayers to use IRS Direct Pay. Users receive instant confirmation that their payment has been made.

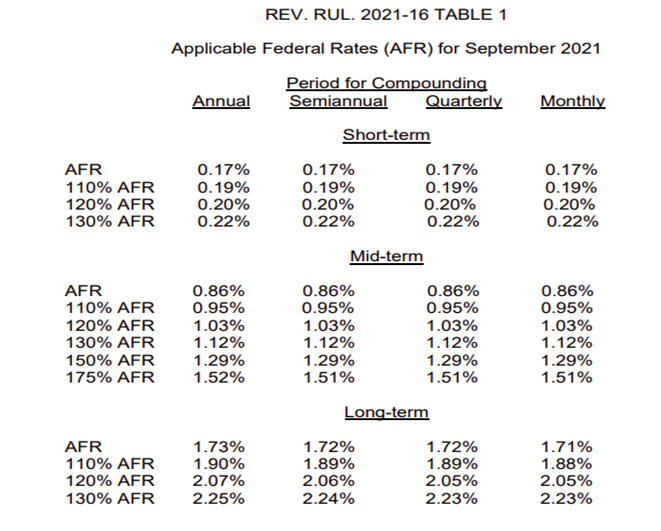

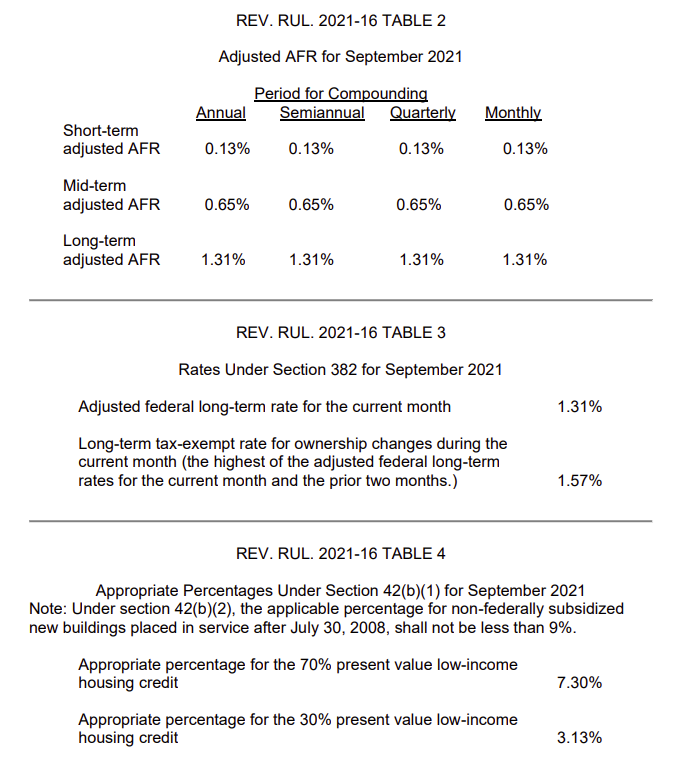

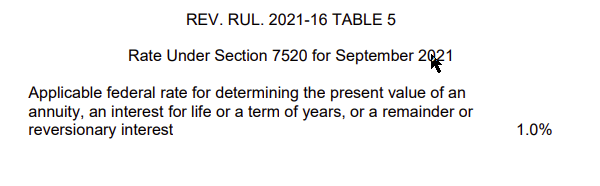

Issue 18: Applicable Federal Rates for September 2021, Rev. Rul. 2021-16

![]() Basics & Beyond Resources

Basics & Beyond Resources

- Blog Page

- Resource List

- Webinar & Seminar Schedules

- Get Registered!

- Note: Paid attendees can request a link to the replay of any previously recorded webinar presentations by emailing us at [email protected]