In this Issue:

- Corporate Transparency Act – New Requirement for Most Businesses Beginning January 1, 2024

- IRS Announces Administrative Transition Period for New Roth Catch‑up Requirement; Catch-up Contributions Still Permitted After 2023 – IR-2023-155, Aug. 25, 2023

- IRS Issues Prop Regs on Reporting by Brokers for Sales and Exchanges of Digital Assets – IR-2023-153, Aug. 25, 2023

- NATP Fee Study Shows Tax Becoming a ‘Graying Industry’

- 2024 ACA Premium Tax Credit Indexing Adjustments Issued – Rev. Proc. 2023-29

- IRS Issues Revised 2023 Instructions for Form 1042-S

- TIGTA Finds IRS’ Controls Over Taxpayer Data Stored on Microfilm in Shambles

- IR-2023-152 – Reminder to Employers and Employees: Educational Assistance Programs Can Be Used to Help Pay Workers’ Student Loans

- Taxes Owed on Returns Filed After Bankruptcy Not Discharged- Worrell (Bktcy, Fla.)

- TIGTA Finds Pattern of IRS Incorrectly Placing ‘Deceased’ on Taxpayer Accounts

- Supreme Court Petition: When Is a Return Filed for Limitations Purposes – Concerning Case We Will be Following.

- Wage Rules Issued for IRA Energy Credits

- Tax Tip 2023-101 – Everyone Has the Right to Finality When Working with the IRS

- IRS Obsoletes Notice on Exemptions, Waivers of Electronic Filing Requirements for Certain Returns – Notice 2023-60

- Individual Home Energy Tax Credits for 2023

- Highlights from the Crime Desk: July 2023 – This article comes from Checkpoint – it is Good to Know the Scammers are Being Caught

- IRS Cautions Plan Sponsors to be Alert to Compliance Issues Associated with ESOPS

- New Rules for Consolidated Returns Proposed

- IRS Ends Unannounced Revenue Officer Visits to Taxpayers

- Commissioner Signals New Phase of Employee Retention Credit Work

- IRS Selects New Chief Transformation and Strategy Officer to Lead Change Efforts Under the Inflation Reduction Act; David Padrino to Oversee Strategic Operating Plan Work to Help Taxpayers, Drive Agency Improvements

Applicable Federal Rates for September 2023, Rev. Rul. 2023- 16

Issue 1: Corporate Transparency Act – New Requirement for Most Businesses Beginning January 1, 2024

Beginning on January 1, 2024, many corporations, limited liability companies, and other entities created or registered to do business in the United States must report information about their beneficial owners—the persons who ultimately own or control the company—to the U.S. Department of the Treasury’s Financial Crimes Enforcement Network (FinCEN).

I have gathered some key links that will help to further understand these new filing responsibilities.

Link to Beneficial Ownership Reporting Ket Questions

https://www.fincen.gov/sites/default/files/shared/BOI_Reporting_Key_Questions_Published_508C.pdf

Beneficial Ownership Information on Report Key Filing Dates

Frequently Asked Questions

https://www.fincen.gov/boi-faqs

Fact Sheet

https://www.fincen.gov/beneficial-ownership-information-reporting-rule-fact-sheet

Issue 2: IRS Announces Administrative Transition Period for New Roth Catch‑up Requirement; Catch-up Contributions Still Permitted After 2023 – IR-2023-155, Aug. 25, 2023

The Internal Revenue Service announced an administrative transition period that extends until 2026 concerning the new requirement that any catch-up contributions made by higher‑income participants in 401(k) and similar retirement plans must be designated as after-tax Roth contributions.

At the same time, the IRS also clarified that plan participants who are age 50 and over can continue to make catch‑up contributions after 2023, regardless of income.

The announcement is included in Notice 2023-62 posted on IRS.gov. The notice provides initial guidance for § 603 of the SECURE 2.0 Act, enacted in December 2022. Under that provision, starting in 2024, the new Roth catch-up contribution rule applies to an employee who participates in a 401(k), 403(b) or governmental 457(b) plan and whose prior-year Social Security wages exceeded $145,000.

The administrative transition period will help taxpayers transition smoothly to the new Roth catch-up requirement and is designed to facilitate an orderly transition for compliance with that requirement. The notice also clarifies that the SECURE 2.0 Act does not prohibit plans from permitting catch-up contributions, so plan participants who are age 50 and over can still make catch-up contributions after 2023.

The Treasury Department and the IRS plan to issue future guidance to help taxpayers, and the notice describes several positions that are expected to be included.

Issue 3: IRS Issues Prop Regs on Reporting by Brokers for Sales and Exchanges of Digital Assets – IR-2023-153, Aug. 25, 2023

Treasury and the Internal Revenue Service has issued proposed regulations that would require brokers to report sales and exchanges of digital assets by customers.

The proposed regulations cover a range of digital asset issues where there have been questions, including defining brokers and requiring proceeds to be reported to the IRS on new Form 1099-DA. No draft issued by IRS as of September 1, 2023.

For sales or exchanges of digital assets that take place on or after January 1, 2025, the proposed regulations would require brokers, including digital asset trading platforms, digital asset payment processors and certain digital asset hosted wallet providers, to report gross proceeds on a newly developed Form 1099-DA and to provide payee statements to customers. Brokers, in certain circumstances, would also be required to include gain or loss and basis information for sales that take place on or after January 1, 2026, on these information returns and statements, so that customers have the information they need to prepare their tax returns.

The proposed regulations would also require real estate reporting persons, such as title companies, closing attorneys, mortgage lenders and real estate brokers, who are treated as brokers for dispositions of digital assets, to report the disposition of digital assets paid as consideration by real estate purchasers to acquire real estate in real estate transactions that close on or after January 1, 2025. These real estate reporting persons would also be required to include on Form 1099-S the fair market value of digital assets paid to sellers of real estate in real estate transactions that close on or after January 1, 2025.

Finally, the proposed regulations set forth gain (or loss) computation rules, basis determination rules and backup withholding rules applicable to digital asset sale and exchange transactions and propose many useful definitions.

Proposed Regulation § 1.6045-1

Proposed Regulation § 1.1001-1 – Basis Issue

Issue 4: NATP Fee Study Shows Tax Becoming a ‘Graying Industry’

NATP – email – no infringement intended.

NATP conducts a study every other year that analyzes tax professional fees charged for return preparation, bookkeeping, financial planning, and other services by surveying its members.

Overall, 70% of tax professionals’ gross revenue comes from return preparation, the next highest portion coming from monthly accounting and bookkeeping services (12%). All other categories come in at 5% or below. 65% of gross revenue is earned during tax season, 12% during extended periods, and the remaining 23% between tax seasons.

Many respondents said they are “slowing down” in their career or are instead focusing on “very, very complex” returns that take up time that would otherwise be used to prepare a higher quantity of simpler returns. This reinforces “what Congress already knows” and “are concerned about.” That is, the tax community is preparing less returns by choice, “not because there isn’t business out there.

The conclusion stated the tax industry is becoming a “graying industry,” and that the study adds to the narrative that “there are not enough people coming into” the tax world, indicating there are too many barriers to entry preventing younger talent from getting a foot in the door.

Issue 5: 2024 ACA Premium Tax Credit Indexing Adjustments Issued – Rev. Proc. 2023-29

The IRS has issued a revenue procedure containing the ACA premium tax credit indexing adjustments for tax year 2024. Individuals will use these numbers to calculate their 2024 premium tax credit.

The Code provides a premium tax credit (PTC or premium assistance credit) to eligible individuals and families to subsidize the purchase of health insurance plans through an Exchange or Marketplace. The PTC is available on a sliding-scale basis for individuals and families with household income between 100% and 400% of the Federal poverty line.

Note. The 400% limit does not apply for tax years 2021 through 2025.

Individuals who have lower income receive a larger credit. The applicable percentage multiplied by a taxpayer’s household income determines the taxpayer’s annual required share of premiums for the benchmark plan.

| Applicable Percentage Table | ||

| Household income percentage of Federal poverty line | Initial percentage | Final percentage |

| Less than 150% | 0.00% | 0.00% |

| 150% but less than 200% | 0.00% | 2.00% |

| 200% but less than 250% | 2.00% | 4.00% |

| 250% but less than 300% | 4.00% | 6.00% |

| 300% but less than 400% | 6.00% | 8.50% |

| 400% and higher | 8.50% | 8.5% |

The procedure also contains the required contribution percentage for plan years beginning in 2024. The required contribution percentage is used to determine whether an individual is eligible for affordable employer-sponsored minimum essential coverage.

The required contribution percentage for 2024 is 8.39%.

Issue 6: IRS Issues Revised 2023 Instructions for Form 1042-S

Form 1042-S. Withholding agents file Form 1042-S to report amounts paid to foreign persons (e.g., salaries, interest, dividends, premiums, pensions, scholarships, and grants) from sources within the U.S. during the preceding calendar year that are subject to withholding. Copy A of Form 1042-S must be filed with the IRS even if:

(1) no tax was withheld because the income was exempt from tax under a treaty or under the Internal Revenue Code, including the exemption for income effectively connected with conducting a trade or business in the United States; or

(2) the amount withheld was repaid to the recipient. Form 1042-S should not be filed if the amount is required to be reported on Form W-2 or 1099.

There are two revisions to the instructions. This is not an area that applies to many, so I urge those who issue Form 1042-S to please review the instructions changes.

Issue 7: TIGTA Finds IRS’ Controls Over Taxpayer Data Stored on Microfilm in Shambles

The Treasury Inspector General for Tax Administration (TIGTA) has released an inspection evaluation report conducted to assess the processes and procedures to account for and safeguard microfilm containing sensitive taxpayer information. (Report No. 2023-IE-R008)

As explained in the report, the IRS is required to create and store backups of both business and individual tax records to ensure that these records are available to conduct business, document activities adequately, and protect the interests of the federal government and taxpayers.

“Our review identified significant deficiencies in the IRS’ safeguarding, accounting for, and physical storage of its microfilm backup cartridges,” TIGTA said.

Required annual inventories have not been performed, the report noted that IRS management was unable to provide a time frame of when the last required annual inventory was conducted. “The lack of adequate inventory controls also includes no reconciliation of the microfilm backup cartridges noted as being sent from closed Tax Processing Centers to what was physically shipped and received,” the report said.

TIGTA learned that microfilm cartridges stored at the Ogden Tax Processing Center “are not being adequately safeguarded to limit access to this information.” The microfilm cartridges are stored on open shelving in the middle of a large warehouse that is accessible to numerous personnel within the facility and is not “within eyesight” of agency personnel overseeing microfilm activities.

The IRS also is not in compliance with records management requirements, the report stated. According to agency management, 15 large pallets containing microfilm cartridges required to be sent to the Federal Records Center have been stored at the IRS’ National Distribution Center since 2018.

Finally, the IRS is not in compliance with microfilm destruction time frames. “TIGTA identified individual microfilm cartridges stored at all three Tax Processing Centers that exceed the 30-year storage requirement,” the report said.

Issue 8: IR-2023-152 – Reminder to Employers and Employees: Educational Assistance Programs Can Be Used to Help Pay Workers’ Student Loans

Though educational assistance programs have been available for many years, the option to use them to pay student loans has been available only for payments made after March 27, 2020, and, under current law, will continue to be available until Dec. 31, 2025.

Traditionally, educational assistance programs have been used to pay for books, equipment, supplies, fees, tuition and other education expenses for the employee. These programs can now also be used to pay principal and interest on an employee’s qualified education loans. Payments made directly to the lender, as well as those made to the employee, qualify.

By law, tax-free benefits under an educational assistance program are limited to $5,250 per employee per year. Normally, assistance provided above that level is taxable as wages.

Employers who do not have an educational assistance program may want to consider setting one up. In a tight labor market, worthwhile fringe benefits such as educational assistance programs can help employers attract and retain qualified workers.

These programs must be in writing and cannot discriminate in favor of highly compensated employees.

Issue 9: Taxes Owed on Returns Filed After Bankruptcy Not Discharged- Worrell (Bktcy, Fla.)

Chapter 13 bankruptcy discharge does not apply to the taxes owed on returns filed after they were due and after filing for bankruptcy, a bankruptcy judge has ruled. (In re Worrell, (Bktcy Fla.)

Denying Sharon Worrell’s motion to enforce the discharge order entered in her case, U.S. Bankruptcy Judge Tiffany P. Geyer of the Middle District of Florida on August 7 determined that Worrell’s post-petition filing of her returns met the timing requirement for excepting the debt from discharge.

Worrell received a Chapter 13 discharge on March 31. She subsequently moved to enforce the discharge order against the IRS, asserting that the agency was attempting to collect taxes that were discharged in her bankruptcy, Judge Geyer’s opinion said.

The IRS responded that its claim was not dischargeable under 11 USC 523(a)(1)(B), which prevents discharge of taxes “with respect to which a return… was filed… after the date on which such return… was last due… and after two years before the date of the filing of the petition.”

In addition, the taxes were not discharged because 11 USC 1328(a)(2) prevents a Chapter 13 discharge of debts specified in 11 USC 523(a)(1)(B).

The IRS said Worrell’s returns for 2012 through 2015 were filed on April 28, 2020—about six weeks after she filed for Chapter 13 relief.

Worrell did not contest the IRS’ allegations that her tax returns were filed after the due dates. Judge Geyer found that the returns also satisfied the second non-dischargeability requirement because they were filed “after two years before” her bankruptcy filing.

The judge cited in re: Harrell, 318 B.R. 692 (Bktcy Ark. 2005), in which the Bankruptcy Court said 11 USC 523(a)(1)(B)(ii) “contemplates a period that begins two years prior to the petition date, extends indefinitely into the future, and thus encompasses the post-petition period.”

Similarly, in In re Savaria, (BAP9), the 9th U.S. Circuit Bankruptcy Appellate Panel held that the phrase “after two years before the date of the filing of the petition” does not denote a two-year period that definitively ends with the filing, but contemplates a period of indefinite duration that begins two years before the bankruptcy filing.

Because Worrell’s filing of her tax returns fell within the prohibition against discharge under 11 USC 523(a)(1)(B) and 11 USC 1328(a), Judge Geyer concluded that the discharge order did not apply to the IRS.

This article originally appeared in Westlaw Today.

Issue 10: TIGTA Finds Pattern of IRS Incorrectly Placing ‘Deceased’ on Taxpayer Accounts

A Treasury Inspector General for Tax Administration (TIGTA) audit has revealed that indicators used by the IRS to prevent the filing of tax returns for deceased taxpayers were incorrectly placed on some taxpayer accounts. (Audit Report No. 2023-40-044)

The audit was initiated because of concerns that the IRS was improperly locking taxpayer accounts as deceased preventing taxpayers from filing returns and receiving refunds.

An analysis of tax account information through January 1, 2022, identified 77,868 taxpayers with potentially erroneous deceased account locks. “In these instances, the Social Security Administration’s (SSA) data did not indicate that the taxpayer was deceased, i.e., there was no date of death present,” the audit said. The problem was attributed to the filing of a return or other actions taken by the IRS.

According to TIGTA, the IRS confirmed that 20,222 taxpayer accounts were locked in error due to both human and computer programming issues when identifying the appropriate taxpayer accounts to be locked. An updated analysis of deceased account locks for the period of January 2, 2022, through October 29, 2022, “found that taxpayer accounts continue to be erroneously locked,” the audit said, adding that it “identified an additional 14,193 taxpayer accounts that had been potentially erroneously locked during this time frame.”

The IRS acted to address the issue by implementing new programming on January 31, 2023, to conduct an annual systemic reconciliation of the date of death information between the SSA and the IRS, the audit noted.

In addition, the IRS confirmed that 6,821 of 9,646 tax accounts issued a CPO1H notice, Tax Return Submitted with Locked Social Security Number, “were inappropriately locked”—meaning the agency could not process their tax return.

Issue 11: Supreme Court Petition: When Is a Return Filed for Limitations Purposes – Concerning Case We Will be Following.

Seaview Trading LLC has asked the Supreme Court to review the Ninth Circuit’s holding that delivering a return to an IRS agent isn’t an official filing for purposes of the statute of limitations. (Seaview Trading, LLC,)

Facts. In July 2005, an IRS agent contacted Seaview claiming the IRS never received Seaview’s 2001 return. The agent asked Seaview to fax copies of its 2001 return and poof of mailing to the agent’s office in South Dakota.

Seaview Trading responded by claiming it filed its 2001 Form 1065, U.S. Return of Partnership Income, in July 2002. Its accountant then faxed the IRS agent a “copy” of the 2001 return along with a certified mail receipt as evidence that the original return was sent to the IRS in July 2005. In 2010, after disallowing the partnership’s $35.5 million loss, the IRS assessed Seaview additional taxes for the 2001 tax year.

Note. Seaview allegedly sent the IRS two returns in the envelope for which it had a certified mail return receipt. The IRS admitted that it received one of those returns but claimed it didn’t receive the other.

After receiving the additional assessment, Seaview sought an administrative review. During that review, Seaview mailed another copy of its 2001 return to an IRS attorney in Minnesota. Neither IRS employee forwarded the returns they received to the IRS’ processing center in Ogden and Seaview did not forward them to Ogden either.

Fax, mailed returns not filed. Seaview asked the Tax Court to review the new assessment claiming that it was issued after the assessment period closed. Citing Dingman TC Memo 2011-116 Seaview maintained that revenue agents were required to process delinquent returns that they receive from taxpayers. As a result, Seaview filed its 2001 return in July 2005 and the IRS’ additional tax assessment, issued in 2010, was barred.

However, the Tax Court found that Dingman did not apply because Seaview did not intend to file a return when it submitted its 2001 return to the IRS’ employees. This lack of intent was evidenced by its claim that it had filed the return in 2002 and the documents submitted to the IRS’ employees were “copies.” In Dingman, the Tax Court said, the taxpayer clearly intended the returns they submitted to the Criminal Investigation Division to be delinquent returns with payments.

Seaview first won then lost on appeal. On appeal to the Ninth Circuit, the panel judges reversed and remanded the Tax Court’s decision. But the panel’s decision was vacated after the IRS filed a petition for review en banc.

Ninth Circuit’s final word. After more litigation, the majority of the Ninth Circuit found that the IRS was not barred by the limitations period from adjusting the partnership’s 2001 tax liability because the 2001 submission was never properly filed at a service center. According to the Ninth Circuit, Seaview did not file its return with a designated service center as required by the regulations; thus, it never filed the 2001 return at all.

The IRS had the authority to promulgate the regulation Reg. § 1.6031(a)-1(e ) the Ninth Circuit said, because Congress has not spoken directly to the issue of where returns should be filed. And it was reasonable for the IRS to require all returns to be filed at a designated service center.

The dissent, however, found that the reg was not specific enough and was contradicted by the IRS’ other public guidance on the issue. In fact, the dissent noted that various forms of sub regulatory public guidance contradicts the IRS’ position in Seaview. The dissent also took issue with the majority reading the two paragraphs of the regulation separately arguing that the two paragraphs must be read together, and both only apply to timely filed returns.

Request for Supreme Court review. Seaview filed its request for Supreme Court review on August 9, 2023. The petition asks the Court to clarify whether a late-filed return is “filed” when it is submitted to an IRS employee who requests it.

This case information was taken from Checkpoint.

Issue 12: Wage Rules Issued for IRA Energy Credits

The U.S. Department of Labor (DOL) has finalized new rules that could impact taxpayers seeking “bonus credits” for renewable energy and carbon capture projects that were included in the Inflation Reduction Act (IRA) of 2022. Many of the IRA’s energy tax incentives include a bonus that increases the value of the tax credit substantially if the taxpayer meets DOL wage and apprenticeship rules. The DOL’s final rules were made public August 10, 2023, and include provisions regarding the prevailing wages and fringe benefits that companies must pay to certain workers for the company to be eligible for the bonus credit.

Issue 13: Tax Tip 2023-101 – Everyone Has the Right to Finality When Working with the IRS

By law, all taxpayers have the right to finality of tax matters. For example, taxpayers have the right to know when the IRS has finished an audit. This is one of ten basic rights — known collectively as the Taxpayer Bill of Rights.

Here’s what taxpayers should know about their right to finality:

- Taxpayers have the right to know:

- The maximum amount of time they have to challenge the IRS’s position.

- The maximum amount of time the IRS has to audit a particular tax year or collect a tax debt.

- When the IRS has finished an audit.

- The IRS generally has three years from the date taxpayers file their returns to assess any additional tax for that tax year.

- There are some limited exceptions to the three-year rule, including when taxpayers fail to file returns for specific years or file false or fraudulent returns. In these cases, the IRS can assess tax for that tax year at any time.

- The IRS generally has 10 years from the assessment date to collect unpaid taxes. The IRS cannot extend this 10-year period unless the taxpayer agrees to extend the period as part of an installment agreement to pay tax debt or a court judgment allows the IRS to collect unpaid tax after the 10-year period.

- There are circumstances when the 10-year collection period may be suspended. This can happen when the IRS cannot collect unpaid tax due to the taxpayer’s bankruptcy or there’s an ongoing collection due process proceeding involving the taxpayer.

- A statutory notice of deficiency is a letter proposing additional tax the taxpayer owes. This notice must include the deadline for filing a petition with the tax court to challenge the amount proposed.

- Generally, a taxpayer can be subject to only one audit per tax year. The IRS may reopen an audit for a previous tax year if the agency finds it necessary. This could happen, for example, if a taxpayer files a fraudulent return.

Issue 14: IRS Obsoletes Notice on Exemptions, Waivers of Electronic Filing Requirements for Certain Returns – Notice 2023-60

The IRS has obsoleted Notice 2010-13, which provided guidance on how certain filers could obtain administrative exemptions and waivers of the electronic filing requirements.

Notice 2010-13 provided guidance to corporations, electing small business corporations (S corporations), and tax-exempt organizations required to file returns under §6033, on how to request a waiver of the e-filing requirements for their returns. The Notice also provided guidance on how to cure the rejection of an e-filed return.

In February 2023, the IRS published final regs TD 9972

https://www.irs.gov/newsroom/irs-and-treasury-issue-final-regulations-on-e-file-for-businesses

that provided new e-filing requirements that will apply beginning January 1, 2024.

Among other things, the new e-filing rules allow for waivers of, and administrative exemptions from, the updated e-filing requirements. These exemptions and waivers include exemptions for individuals who don’t use technology due to their religious beliefs (religious exemption) and waivers for individuals who will experience undue hardship if required to e-file their returns (hardship waiver

Issue 15: Individual Home Energy Tax Credits for 2023

Taxpayers who make home energy improvements in 2023 may be able to take advantage of tax credits for a portion of the qualifying expenses. The credit amounts were increased, and types of qualifying expenses were expanded, by the Inflation Reduction Act of 2022.

Who can claim energy credits. There are two energy-related credits available to taxpayers making qualifying improvements to their home:

A taxpayer may claim these credits in the year the taxpayer makes a qualifying improvement to their primary home. Usually, a taxpayer’s primary home is where the taxpayer spends most of their time. In addition, to qualify for an EEHIC, the improved home must an existing home located in the United States.

Note. Generally, a taxpayer may claim these credits only for qualified improvements to their primary residence; however, a taxpayer may be able to claim energy-related credits for certain improvements to a second home if the taxpayer does not use the second home as a rental property. In addition, renters who purchase energy efficient appliances and other products for their rental home may be able to claim these tax credits.

What improvements qualify for the EEHIC. Taxpayers can claim an Energy Efficient Home Improvement Credit for many home improvements that meet certain energy efficiency requirements. This includes:

- Exterior doors,

- Windows, skylights,

- Insulation materials,

- Central air conditioners,

- Heat pumps and heat pump water heaters,

- Biomass stoves and boilers, and

- Home energy audits

Generally, the maximum credit a taxpayer may claim each year is:

- $1,200 for energy property costs and certain energy efficient home improvements, with limits on doors ($250 per door and $500 total), windows ($600) and home energy audits ($150)

- $2,000 per year for qualified heat pumps, biomass stoves or biomass boilers.

Note. The actual amount of the taxpayer’s credit is a percentage of the total cost of the improvements in the year of installation. In certain circumstances, the credit may be capped.

The EEHIC has no lifetime dollar limit. A taxpayer can claim the maximum annual credit every year they make eligible improvements until 2033.

Note. The EEHIC is not refundable and cannot be carried over to another tax year. So, it might make sense to take a large project, like replacing windows, and do some of it over several years.

What expenses qualify for the Residential Clean Energy Credit. Taxpayers who invest in renewable energy for their primary home may be able to claim the Residential Clean Energy Credit. Qualified RCE credit improvements include:

- Solar, wind and geothermal power generation,

- Solar water heaters,

- Fuel cells, and

- Battery storage

Generally, the credit amount is a percentage of the total cost of the improvement in the year of installation. For tax years 2022-2032 that percentage is 30%. Generally, there is no annual maximum or lifetime limit.

Note. There are credit limits for fuel cell property.

The Residential Clean Energy Credit can be claimed for qualified improvements to a taxpayer’s new or existing home located in the United States.

Issue 16: Highlights from the Crime Desk: July 2023 – This article comes from Checkpoint – it is Good to Know the Scammers are Being Caught

Highlights From the Crime Desk is Checkpoint’s monthly roundup of criminal tax cases. This month’s round up contains the usual mix of tax preparers preparing false returns and employers who don’t pay their trust fund taxes, along with a few embezzlers and a financial professional promoting a charitable deduction tax fraud scheme and ERC fraud.

Employment tax credit fraud.

A New Jersey tax preparer was charged with fraudulently filing over 1,000 tax returns falsely claiming COVID-19-related employment tax credits. Those returns sought over $124,000,000 from the IRS. According to the government, Leon Haynes allegedly prepared and submitted approximately 1,387 false refund claims to the IRS for COVID-related tax credits. Haynes allegedly told his clients that the government was giving out COVID-relief money for businesses and that they were eligible for the money simply because they had a business. Haynes then submitted refund claims to the IRS on behalf of his own and his clients’ businesses that grossly overstated the number of employees and amount of wages paid by the businesses. The IRS allegedly mailed Haynes multiple tax refund checks totaling $1,007,966 for his own companies and disbursed a total of $31.6 million in refunds to Haynes’ clients based on the false refund claims that Haynes submitted. Haynes allegedly charged his clients fees up to 15% of the refund they received.

Employment taxes.

A Colorado businessman was sentenced to 15 months in prison for failing to pay more than $700,000 in employment taxes he withheld from his employees’ pay. The businessman, Frank Stevens, not only failed to pay over the withheld payroll taxes to the IRS, but he also failed to file the required quarterly employment tax returns for his businesses. Then, after the IRS imposed a trust fund penalty, Stevens kept his bank balances near zero to avoid paying the penalty. In total, Stevens caused a tax loss of approximately $737,128.

Tax preparers.

A Minneapolis tax preparer was sentenced to 12 months and one day in prison for continuing to e-filing returns after he was suspended from the IRS’ e-file program for failing to file his own returns. For almost a decade, Sue Yang operated surreptitiously as an e-filing tax preparer by enlisting others to obtain unique electronic filing identification numbers (EFINs) that Yang used to file thousands of tax returns for customers. Yang received approximately $765,000 from his tax preparation business, which he didn’t report. Yang caused a tax loss of about $214,297.

Another tax preparer, this one from Houston, was sentenced to 12 years for helping to prepare false tax returns. At the sentencing hearing, the court heard additional evidence describing Cheryl Christin Kissentaner’s history of failing to pay her own taxes and civil penalties imposed on her for failing to use due diligence in preparing tax returns. Kissentaner’s conduct caused a tax loss of approximately $1.9 million.

Embezzlers.

A former bank vice president pleaded guilty to one count of embezzlement by a bank employee and one count of filing a false federal tax return. Angela Flippin was the vice president and chief operating officer and board secretary at the People’s Bank of Moniteau County. Flippin embezzled at least $550,000 from the bank over a six-year period by claiming improper comp time disbursements and more than $8,000 in improper expense reimbursements. Flippin also admitted that she failed to report the amounts that she embezzled from the bank on her 2014, 2015, and 2016 federal income tax returns, which resulted in a total tax loss to the federal government of $96,434.

A California woman was sentenced to 66 months in prison for embezzling more than $1 million from her employer and filing false tax returns. According to court documents, Mai Houa Xiong was employed as a financial manager for a Minneapolis-based property management company that provided financial services to homeowners’ associations (HOAs). Between February 2015 and February 2022, Xiong devised and executed a fraud scheme to embezzle funds directly from the accounts to which she had access. As part of the scheme, Xiong repeatedly accessed the HOAs’ bank accounts and conducted electronic transfers of funds directly into her personal bank accounts. Xiong then disguised these transfers by mis-labeling them to make it appear as if they were legitimate HOA expenses.

Tax scheme promoters.

An Ohio financial planner pleaded guilty to conspiracy to defraud the United States and helping to file a false tax return. Rao Garuda, the President and Chief Executive Officer of Associated Concepts Agency, Inc. (“ACA”), engaged in a scheme known as the Advanced Legacy Plan or the Ultimate Tax Plan (see below). Garuda marketed the scheme despite being warned by several attorneys that the scheme was illegal; one attorney described the scheme as “clearly fraudulent.” Garuda scheme caused or intended to cause a tax loss of more than $2.7 million.

Note. The Ultimate Tax Plan scheme was marketed as a way for clients to claim charitable contribution deductions without giving up control over the assets they allegedly donated to charity. The scheme promoters advised clients they could still access their donated assets for their own personal use through tax-free loans and could “buy back” their donated property at a significantly discounted rate.

Florida attorney, Michael L. Meyer, was indicted for conspiracy to defraud the United States, mail and wire fraud conspiracy, helping to prepare false tax returns, conspiracy to obstruct an official proceeding, and other crimes arising out of his promotion of an illegal tax shelter scheme, the “Ultimate Tax Plan,” which involved creating false charitable contribution tax deductions. According to the government, Meyer and his co-conspirators allegedly have earned more than $10 million from selling the Ultimate Tax Plan.

Tax evaders and false return filers.

The owner of a concrete company agreed to plead guilty one count of tax evasion related to a multi-year scheme to underreport income on his tax returns. According to the government, Cleber Gomes Pecanha cashed customer checks and did not deposit the receipts in his business bank accounts. Pecanha also failed to tell his tax preparer that he was cashing checks from customers and only gave the tax preparer his bank statements as support for his tax filings. Hiding his income in this manner resulted in a tax loss of more than $1.8 million.

The owner of an artificial turf company pleaded guilty to failing to report nearly $9 million in business income and attempting to evade more than $946,000 in federal income taxes. According to the government, Craig Steven Voyton’s business made more than $1.5 million per year. Voyton attempted to conceal this income from the IRS by providing his customers with false Forms W-9, Request for Taxpayer Identification Number and Certification. While Voyton was hiding his business income from the IRS, he purchased over $60,000 in cryptocurrency and real estate using company funds. Voyton’s failure to report all his business’s income produced a tax loss of approximately $946,479.

A New York woman pleaded guilty to helping to prepare a false tax return. According to the government, Alice Bixuan Zhang of Queens, New York, co-owned and operated two acupuncture businesses with locations throughout New York City. Zhang created fake business deductions by cashing checks, drawn on the business accounts and made payable to fake management companies, at a check-cashing business and then using the money for personal expenses. Zhang did not disclose the cash to her tax preparer. This scheme resulted in a tax loss of over $784,000.

A Michigan insurance salesman was sentenced to 36 months in prison for filing false tax returns, making false statements to a bankruptcy court, and making false statements to the Justice Department’s Tax Division. According to the government, Donald Stanley LaVigne did not report insurance commissions and other income he earned on tax returns he filed with the IRS over a six-year period. In letters he sent to the IRS, LaVigne falsely claimed that the commissions were not income to him. When LaVigne filed for bankruptcy, he did not disclose the IRS as a creditor on the schedules attached to his bankruptcy petition even though he knew he owed the IRS taxes for several years.

A New Jersey businessman was sentenced to one year and one day in prison for filing a false corporate income tax return with the IRS. According to the government, Gabriel Ferrari of Edison, who owned an automotive repair business, used business funds to pay for personal items, including gambling on horse races. Ferrari concealed this diversion of business income by not disclosing it to his return preparer, thus causing the preparation and filing of a false corporate tax return. In addition, Ferrari failed to pay employment taxes in the amount of $291,600 based on an unreported cash payroll.

Issue 17: IRS Cautions Plan Sponsors to be Alert to Compliance Issues Associated with ESOPS – IR 2023-144, August 9, 2023

As part of an expanded focus on ensuring high-income taxpayers pay what they owe, the Internal Revenue Service are warning businesses and tax professionals to be alert to a range of compliance issues that can be associated with Employee Stock Ownership Plans (ESOPs).

“The IRS is focusing on this transaction as part of the effort to ensure our tax laws are applied fairly and high-income filers pay the taxes they owe,” IRS Commissioner Danny Werfel said. “This means spotting aggressive tax claims as they emerge and warning taxpayers. Businesses and individual taxpayers should seek advice from an independent and trusted tax professional instead of promoters focused on marketing questionable transactions that could lead to bigger trouble.”

Werfel noted the IRS is working to ensure high-income filers pay the taxes they owe. Prior to the Inflation Reduction Act, more than a decade of budget cuts prevented IRS from keeping pace with the increasingly complicated set of tools that the wealthiest taxpayers may use to hide their income and evade paying their share.

“The IRS is now taking swift and aggressive action to close this gap,” Werfel said. “Part of that includes alerting higher-income taxpayers and businesses to compliance issues and aggressive schemes involving complex or questionable transactions, including those involving ESOPs.”

ESOPs are retirement plans that allow employees to own stock in their employer’s company. Any company that has stock can sponsor an ESOP for its employees as long as the ESOP invests primarily in the securities of the employer. ESOPs can be complex arrangements since the ESOP can borrow funds from the employer or a third party to purchase shares of the employer.

In light of the complexity of ESOPs, the IRS has and will continue to undertake enforcement strategies to ensure compliance with tax law requirements by employers sponsoring an ESOP. In its current compliance efforts, the IRS has identified numerous issues, such as valuation issues with employee stock; prohibited allocation of shares to disqualified persons; and failure to follow tax law requirements for ESOP loans causing the loan to be a prohibited transaction.

Additionally, the IRS has seen promoted arrangements using ESOPs that are potentially abusive. For instance, the IRS has seen schemes where a business creates a “management” S corporation whose stock is wholly owned by an ESOP for the sole purpose of diverting taxable business income to the ESOP. The S corporation purports to provide loans to the business owners in the amount of the business income to avoid taxation of that income. The IRS disagrees with how taxpayers interpret this transaction and emphasizes that these purported loans should be taxable income to the business owners. These transactions also impact whether the ESOP satisfies several tax law requirements which could result in the management company losing its S corporation status.

Over the next year, the IRS will continue to use a range of compliance tools, including education, outreach and additional examinations to address compliance issues associated with ESOPs.

Issue 18: New Rules for Consolidated Returns Proposed

The IRS has proposed amendments to the regulations for consolidated returns to reflect statutory changes over the past 50 years and remove regulations that “have no practical applicability to taxpayers,” such as the transition rules for transactions occurring in or before 2009. The proposed regulations (REG – 134420-10) would also update consolidated return regulations and regulations under §1563 to eliminate antiquated or regressive terminology. Finally, the proposed regulations would withdraw or partially withdraw a number of notices of proposed rulemaking.

https://public-inspection.federalregister.gov/2023-14098.pdf

Issue 19: IRS Ends Unannounced Revenue Officer Visits to Taxpayers

As part of a larger transformation effort, the IRS will end most unannounced visits to taxpayers by agency revenue officers to reduce public confusion and enhance overall safety measures for taxpayers and employees. The change reverses a decades-long practice by IRS revenue officers, the unarmed agency employees whose duties include visiting households and businesses to help taxpayers resolve their account balances by collecting unpaid taxes and unfiled tax returns. Effective immediately, unannounced visits will end except in a few unique circumstances and will be replaced with mailed letters to schedule meetings.

Issue 20: Commissioner Signals New Phase of Employee Retention Credit Work

With the IRS making substantial progress in the ongoing effort related to the Employee Retention Credit (ERC) claims, the agency has entered a new phase of increasing scrutiny on dubious submissions while renewing consumer warnings against aggressive marketing.

Speaking Tuesday at a special roundtable session of tax professionals in Atlanta, IRS Commissioner Danny Werfel noted the IRS has shifted efforts after successfully clearing the backlog of valid ERC claims.

Now, the agency is intensifying compliance work and putting in place additional procedures to deal with fraud in the program.

Issue 21: IRS Selects New Chief Transformation and Strategy Officer to Lead Change Efforts Under the Inflation Reduction Act; David Padrino to Oversee Strategic Operating Plan Work to Help Taxpayers, Drive Agency Improvements

The Internal Revenue Service announced the selection of David Padrino to serve as the Chief Transformation and Strategy Officer, a recently created role at the agency that will spearhead improvement efforts under Inflation Reduction Act funding.

- Padrino joins the IRS after serving as Chief Transformation Officer at the federal Office of Personnel Management (OPM). He has spent more than two decades working in a variety of other leadership roles across local, state and federal governments as well as on transformation efforts in the private sector.

- “David brings critical experience and insight that the IRS needs to help transform the agency and make improvements for taxpayers at a critical time for our nation’s tax system,” IRS Commissioner Danny

Werfel said. “He will work closely with our IRS leadership teams to focus on making short-term and long-term improvements called for under our new Strategic Operating Plan. With his long track record of success, David will be a key part of our efforts to help the IRS move forward on essential taxpayer service improvements, compliance changes to ensure fairness and strengthening IRS technology to serve taxpayers.” - Padrino has an extensive background in transformation efforts, ranging from work with Fortune 50 corporations in the private sector to a variety of roles across government.

- “I am excited to join the IRS during this critical period of transformation and work alongside so many dedicated public servants,” Padrino said.

- Since last year, Padrino served as OPM’s Chief Transformation Officer, where his work included rolling out an agency-wide transformation effort. Prior to that role, he worked in 2021 and 2022 at OPM to help revitalize the Office of Human Capital Data Management & Modernization.

- Padrino’s previous roles covered a range of activities. He served as the Chief Recovery Officer for the Colorado Attorney General in 2020 and 2021, working on pandemic response efforts including broadband access issues for Colorado schools.

- From 2014-2019, Padrino worked with then Colorado Gov. John W. Hickenlooper, serving as Chief Performance Officer as well as Chief of Staff to the Lieutenant Governor and Chief Operating Officer. Padrino led a number of initiatives to improve government service delivery, which ultimately led national non-profit Results for America to name Colorado one of the best states at using data and evidence to deliver results for residents.

- Prior to that, he worked in the private sector with the Boston Consulting Group from 2007-2014. During this period, his extensive portfolio included working on more than 25 projects in 10 countries, where he served clients across the private, public and non-profit sectors, including the technology, consumer goods, financial services and health care industries.

- Padrino graduated from the Wharton School at the University of Pennsylvania with a Master of Business Administration and received a Bachelor of Arts degree from Vassar College.

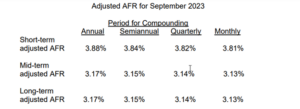

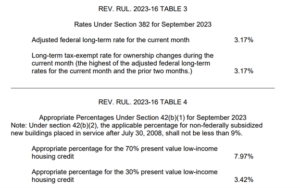

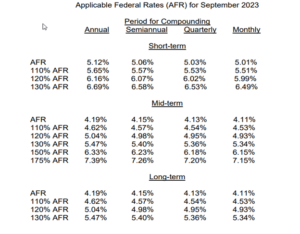

Issue 22: Applicable Federal Rates for September 2023, Rev. Rul. 2023- 16

REV. RUL. 2023-16 TABLE 2