As we approach the fall of 2020, the Senate is still considering its options with the HEROES Act. At last glance Congress was putting something together, but I am not sure anyone has a handle on the specifics. More stimulus, more unemployment compensation and more coronavirus legislation are under consideration. The Fall textbook in in the “bag” so to speak but know that when Congress makes changes that become law, they will be incorporated into our discussion.

News is abundant this month with quite a few pieces of guidance. We noticed our software has incorporated some instances of the reconciliation for the 2020 tax returns when dealing with the stimulus, just a taste in what is to come.

The longest tax season is history is finally over, but our firm is not seeing an end in sight. We still have our extensions, a few procrastinators as always and many collection and non-filer issues. As we head into the fall season, our Fall sessions and webinars will become important to register for timely to get the discount. August 14, 2020 is the deadline for the discount for our Fall and Year-end sessions.

Fall Update: $219

Year-End Update: $249

Register for Both: $329

Early Registration Discount through 8/14/2020

2020 Fall & Year-End Seminars

https://www.cpehours.com/income-tax-seminar-information/

2020 Fall Topical Income Tax Update (see details below):

- 2020 Tax Legislation–New Developments, Including the Stimulus Payment Issues & COVID Legislation

- SECURE Act

- Retirement Planning: Highlights from the CARES and SECURE Acts

- Ethics & the Tax Client

- Assignment of Income

- 1065 Partnership / Distributions

- Basics of Trusts & Estates & Planning Strategies Trusts & Estate Planning

2020 Year-end Income Tax Update (see details below):

- 2020 Tax Legislation–New Developments, Review of Cases, Rulings & IRS Pronouncements

- QBI, CARES and Secure Act Unique Year End Issues

- Meals & Entertainment under the TCJA

- IRC 121 and the Primary Residence

- Ethics – The Creative Tax Professional

- S-Corporation Basis Issues

- Centralized Partnership Audit Regime

- Preparing for the 2021 Tax Season and the Coronavirus Impact

In This Issue

- Security Issues

- IRS Announces 2021 PTIN Fees for Tax Professionals

- Letters Sent to Those Experiencing Delays with the New Advances Payment of Employer Credits, Form 7200

- Census Bureau Weekly Pulse Newsletter Has Some Interesting Statistics

- Another Aspect of the CARES Act Which May Impact Health Care Providers, such as Dentists and Doctors

- More on The Economic Impact Payment – What if Your Client Receives 2 Checks?

- Guidance for Consolidated Groups Regarding Net Operating Losses

- Treasury and IRS Resigned a Draft Partnership Form to Provide Greater Clarity on International Tax Reporting for 2021 (filing season 2022)

- Superseding Return Does Not Restart the Limitations Period for Assessments, Refunds – Chief Counsel Advice 202026002

- Remind Your Clients to Keep Notice 1444 Concerning their Economic Impact Payment – Needed for the 2021 Tax Season

- Reminder About IRS Letter 2800C and Employer Federal Income Tax Withholding

- Additional Retail Partners Accepting Cash Payments for Federal Taxes

- Deferral of Employment Tax Deposits and Payments Through December 31, 2020 FAQ’s

- Interest Payment Update on 2019 Refunds

- National Taxpayer Advocate Erin Collins Delivers Her First Report to Congress Identifying COVID – 19 Challenges, the CARES Act and the Taxpayer First Act Implementation as Priority Issues for Taxpayers – This Article Updates IRS Current Condition

- Update on IRS Liens and Levy Actions FAQ’s

- August Webinar Sessions

Issue 1: Security and Data Theft Tips

As more of us work from home, security issues should be a priority. The Financial Services Modernization Act of 1999, also known as Gramm-Leach-Bliley Act, requires certain entities – including tax return preparers – to create and maintain a security plan for the protection of client data.

- Learn to recognize phishing emails, especially those pretending to be from the IRS, e-Services, a tax software provider or cloud storage provider. Never open a link or any attachment from a suspicious email.

- Create a data security plan using IRS Publication 4557, Safeguarding Taxpayer Data, and Small Business Information Security

- Review internal controls: Install anti-malware/anti-virus security software on all devices (laptops, desktops, routers, tablets and phones) and keep software set to automatically update.

- Use strong and unique passwords of 8 or more mixed characters, password protect all wireless devices, use a phrase or words that are easily remembered and change passwords periodically.

- Encrypt all sensitive files/emails and use strong password protections.

- Back up sensitive data to a safe and secure external source not connected full time to a network.

- Make a final review of return information – especially direct deposit info – prior to e-filing.

- Wipe clean or destroy old computer hard drives and printers that contain sensitive data.

- Limit access to taxpayer data to individuals who need to know.

- Check IRS e-Services account weekly for number of returns filed with EFIN.

- Report any data thefts or losses to the appropriate IRS Stakeholder Liaison.

- Stay connected to the IRS through subscriptions to e-News for Tax Professionals, Quick Alerts and Social Media

Identity Theft Signs

- Client e-filed returns begin to reject because returns with their Social Security numbers were already filed.

- Clients who haven’t filed tax returns begin to receive authentication letters (5071C, 4883C, 5747C) from the IRS.

- Clients who haven’t filed tax returns receive refunds.

- Clients receive tax transcripts that they did not request.

- Clients who created an IRS online account receive an IRS notice that their account was accessed or IRS emails stating their account has been disabled; or, clients receive an IRS notice that an IRS online account was created in their names.

- The number of returns filed with tax practitioner’s Electronic Filing Identification Number (EFIN) exceeds number of clients.

- Tax professionals or clients responding to emails that practitioner did not send.

- Network computers running slower than normal.

- Computer cursors moving or changing numbers without touching the keyboard.

- Network computers locking out tax practitioners.

Stay Vigilant

- Stay ahead of the thieves by taking certain actions daily or weekly to ensure your clients and your business remain safe.

- Track your daily e-File acknowledgements. If there are more acknowledgements than returns you know you filed, dig deeper.

- Track your weekly EFIN usage. The number of returns filed with your Electronic Filing Identification Number (EFIN) is posted weekly. Go to your e-Services account, access your e-file application and check “EFIN Status.” If the numbers are off, contact the e-Help desk. Keep your EFIN application up-to-date with all phone, address or personnel changes.

- If you are a ‘Circular 230 practitioner’ or an ‘annual filing season program participant’ and you file 50 or more returns a year, you can check your PTIN account for a weekly report of returns filed with your Preparer Tax Identification Number (PTIN.) Access your PTIN account and select “View Returns Filed Per PTIN.” File Form 14157, Complaint: Tax Return Preparer, to report excessive using your PTIN or misuse of PTIN.

- If you have a Centralized Authorization File (CAF) Number, make sure you keep your authorizations up to date. Remove authorizations for taxpayers who are no longer your clients.

Issue 2: IRS Announces 2021 PTIN Fees for Tax Professionals

Final regulations set a $21 fee per PTIN application or renewal (plus a $14.95 fee payable to a contractor).

Anyone who prepares or substantially helps prepare any federal tax return or claim for refund for compensation must have a valid PTIN from the IRS. The PTIN must be used as the identifying number on returns prepared. Failure to have and use a valid PTIN may result in penalties. The IRS estimates that more than 800,000 tax return preparers will apply for or renew a PTIN this year.

The annual renewal of PTINs ensures the IRS has up-to-date identifying information about each return preparer, which is essential for timely communication of important information. The program helps protect both return preparers and taxpayers and prevent the unauthorized use of PTINs.

PTINs expire on December 31 of the year for which they are issued. PTINs generally can be renewed beginning in mid-October and are valid for the following calendar year. A tax return preparer can renew online at www.irs.gov/ptin by logging into the preparer’s PTIN account or by submitting a paper Form W-12 with the “Renewal” box checked.

Issue 3: Letters Sent to Those Experiencing Delays with the New Advances Payment of Employer Credits, Form 7200

The Internal Revenue Service has started sending letters to clients who have experienced a delay in the processing of their Form 7200, Advance Payment of Employer Credits Due To COVID-19 (PDF).

A client will receive Letter 6312 if the IRS either rejected Form 7200 or made a change to the requested amount of advance payment due to a computation error.

The letter will explain the reason for the rejection or, if the amount is adjusted, the new payment amount will be listed on the letter.

A client will receive Letter 6313 if the IRS needs written verification from a client that the address listed on their Form 7200 is the current mailing address for their business. The IRS will not process Form 7200 or change the last known address until the taxpayer provides it.

In addition, when signing the form there are additional signature requirements for reporting agents that sign/submit Forms 7200 on behalf of clients.

Reporting agents who sign and submit Form 7200, Advance Payment of Employer Credits Due to COVID-19, for a client for which it has the authority, via Form 8655, Reporting Agent Authorization, to sign and file the employment tax return (e.g., Form 941, Employer’s Quarterly Federal Tax Return) have a new requirement. The signatory for the reporting agent must sign, date, and print his or her name in the relevant boxes on Form 7200. In the box, “Printed Title,” the signatory must include the reporting agent company name or name of business as it appeared on line 9 of the Form 8655.

Issue 4: Census Bureau Weekly Pulse Newsletter Has Some Interesting Statistics

As we move into the fall, we need to be sensitive to issues such as those stated below. Some of our clients may have difficulty making estimated payments, struggling with finances and other daily issues as we move through the end of the year. Agencies aiding these individuals will also continue to struggle with lack of resources.

Based on responses collected July 2 through July 7, the Household Pulse Survey estimates that during the COVID-19 pandemic:

- 49.9% of American adults live in households which have experienced a loss in employment income.

- 34.9% of American adults expect to experience a loss in employment income.

- 10.8% of Americans lived in households where there was either sometimes or often not enough to eat in the previous 7 days.

- 40.1% of adults had delayed getting medical care in the previous 4 weeks.

- 24.5% of respondents reported having little interest or pleasure in doing things more than half the days/nearly every day last week.

- 22.7% of respondents reported feeling down more than half the days/nearly every day last week.

- 32.3% of respondents reported feeling anxious or nervous more than half the days/nearly every day last week.

- On average, households spent $214.19 a week to buy food at supermarkets, grocery stores, online, and other places to be prepared and eaten at home.

- 25.3% of adults either missed last months rent or mortgage payment, or had slight or no confidence that their household could make the next rent payment on time.

Issue 5: Taxation of Provider Relief Payments – Another Aspect of the CARES Act Which May Impact Health Care Providers, such as Dentists and Doctors

The Coronavirus Aid, Relief, and Economic Security Act (CARES Act), enacted on March 27, 2020, appropriated$100 billion for the Public Health and Social Services Emergency Fund (Provider Relief Fund). The Paycheck Protection Program and Health Care Enhancement Act, enacted on April 24, 2020, appropriated an additional$75 billion to the Provider Relief Fund. This funding will be used to reimburse eligible health care providers for health care-related expenses or lost revenues that are attributable to the COVID-19 pandemic.

Q1: May a health care provider that receives a payment from the Provider Relief Fund exclude this payment from gross income as a qualified disaster relief payment under § 139 of the Internal Revenue Code?

Answer: No. A payment to a business, even if the business is a sole proprietorship, does not qualify as a qualified disaster relief payment under §139. The payment from the Provider Relief Fund is includible in gross income under § 61 of the Code.

Q2: Is a tax-exempt health care provider subject to tax on a payment it receives from the Provider Relief Fund?

Answer: Generally, no. A health care provider that is described in §501(c) generally is exempt from federal income taxation under §501(a). Nonetheless, a payment received by a tax-exempt healthcare provider from the Provider Relief Fund may be subject to tax under §511 if the payment reimburses the provider for expenses or lost revenue attributable to an unrelated trade or business as defined in §513.

Issue 6: More on The Economic Impact Payment – What if Your Client Receives 2 Checks?

Most individuals receive only one Economic Impact Payment. If your client believes they received more than one Economic Impact Payment (EIP) make sure that one is not:

Their tax year 2019 tax refund. Check the refund amount on the Form 1040 or 1040-SR for tax year 2019.

Their unemployment compensation payment. Some states are issuing back payments in a single check or direct deposit.

An EIP for someone else in the household. For example, they may have a family member who receives federal benefits or have an adult child who shares the same name or bank account.

Each economic impact payment made will have a Notice 1444 mailed to the individual who has received the payment, the notice includes the recipient name and amount received. If after checking the items above the client believes they received a payment in error, return one of the payments, using the instructions in the FAQs about returning an Economic Impact Payment. Question #65 of the FAQ provides information and addresses on returning a payment.

Issue 7: Guidance for Consolidated Groups Regarding Net Operating Losses

The Department of the Treasury and the Internal Revenue Service today issued proposed regulations (REG-125716-18) and temporary regulations (TD 9900) that provide guidance for consolidated groups regarding net operating losses (NOLs).

The Tax Cuts and Jobs Act (TCJA) and the Coronavirus Aid, Relief, and Economic Security Act (CARES Act) amended the rules for NOLs. After amendment, the NOL deduction is the sum of:

- The total of the NOLs arising before January 1, 2018 (pre-2018 NOLs) that are carried to that year; plus

- The lesser of:

- The total of the NOLs arising after December 31, 2017; or

- 80% of taxable income less pre-2018 NOLs (the 80% limitation).

The TCJA generally eliminated NOL carrybacks and permitted NOLs to be carried forward indefinitely. The TCJA also provides special rules for nonlife insurance companies and farming losses. Nonlife insurance companies are permitted to carry back NOLs two years and forward 20 years, and the 80% limitation does not apply. Farming losses are permitted to be carried back two years and carried forward indefinitely, subject to the 80% limitation.

The CARES Act effectively delays the application of the TCJA amendments until January 1, 2021. Additionally, the CARES Act permits a five-year carryback for NOLs, including farming losses and NOLs of nonlife insurance companies, for taxable years beginning after December 31, 2017 and before January 1, 2021.

The proposed regulations provide guidance to consolidated groups on the application of the 80% limitation. Additionally, the proposed regulations would remove obsolete provisions from the rules for consolidated groups that contain both life insurance companies and nonlife insurance companies.

Because the CARES Act allows certain NOLs to be carried back five years, the temporary regulations allow certain acquiring consolidated groups to make an election to waive all or a portion of the pre-acquisition portion of the extended carryback period for certain losses attributable to certain acquired members.

Issue 8: Treasury and IRS Resigned a Draft Partnership Form to Provide Greater Clarity on International Tax Reporting for 2021 (filing season 2022)

The redesigned form and instructions provide guidance to partnerships on how to report international tax information to their partners in a standardized format. This proposed form would apply to a partnership required to file Form 1065 only if the partnership has items of international tax relevance (generally foreign activities or foreign partners). The proposed changes would not affect domestic partnerships with no international tax items to report.

This early release is intended to afford time for stakeholder input and engagement. Treasury and IRS invite comments from affected stakeholders through Sept. 14, 2020. Written comments should be sent to the following email address: [email protected] with the subject line: “International Form Changes.”

Currently, partners are required to report international tax information on their tax returns on several tax forms and schedules. Partners generally obtain the information required to be reported from their partnerships, usually through narrative statements attached to K-1s. Those statements are compiled in a variety of formats and may be difficult for partners to translate on to their own returns. The proposed changes intend to ease this burden through a standard format that offers greater clarity to both partnerships and their partners.

The standard format of the new partnership schedules is designed to better align the information that partnerships provide on the schedules with the tax forms used by partners, allowing partners to more easily prepare their tax returns and the IRS to more efficiently verify taxpayer compliance. It is intended that all of the information to be reported on the new schedules is already necessary for the partnership to provide to partners or is available to the partnership.

The Treasury Department and the IRS are releasing the draft new Schedule K-2 (Form 1065), Partners’ Distributive Share Items – International and Schedule K-3 (Form 1065), Partner’s – Share of Income, Deductions, Credits, etc. – International, both for tax year 2021 (filing season 2022), and the draft instructions, to allow partnerships and other stakeholders time to consider the proposed changes and to provide comments that can be taken into account in finalizing the schedules and instructions.

The proposed parts included in new Schedule K-2 (Form 1065) replace portions of existing Form 1065, Schedule K, lines 16(a) through 16(r). The proposed schedule provides for international tax information to be reported in a standardized manner generally corresponding to the tax forms listed above.

The proposed parts included in new Schedule K-3 (Form 1065) replaces portions of Schedule K-1, Part III, Boxes 16 and 20, and provides information to the partner generally in the format of the following forms that might be completed by the partner:

- Form 1040 (U.S. Individual Income Tax Return)

- Form 1040-NR (U.S. Nonresident Alien Income Tax Return),

- Form 1116 (Foreign Tax Credit (Individual, Estate, or Trust)),

- Form 1118 (Foreign Tax Credit – Corporations),

- Form 1120 (U.S. Corporation Income Tax Return)

- Form 1120-F (U.S. Income Tax Return of a Foreign Corporation),

- Form 4797 (Sales of Business Property)

- Form 8949 (Sales and Other Dispositions of Capital Assets)

- Form 8991 (Tax on Base Erosion Payments of Taxpayers with Substantial Gross Receipts),

- Form 8992 (U.S. Shareholder Calculation of Global Intangible Low-Taxed Income (GILTI)), and

- Form 8993 (Section 250 Deduction for Foreign Derived Intangible Income (FDII) and Global Intangible Low-Taxed Income (GILTI)).

The Treasury Department and the IRS plan similar revisions, as applicable, to Form 1120-S (U.S. Income Tax Return for an S Corporation) and Form 8865 (Return of U.S. Persons With Respect to Certain Foreign Partnerships). The Treasury Department and the IRS welcome comments on similar changes to be made to Forms 1120-S and 8865 for the 2021 tax year.

https://www.irs.gov/businesses/1065-form-changes

Issue 9: A Superseding Return Does Not Restart the Limitations Period for Assessments, Refunds – Chief Counsel Advice 202026002

Chief Counsel has determined that when a “superseding return” is filed, the original return is the “return” that starts the statutory period for assessing the tax due or claiming a refund of an overpayment. A superseding return is a return filed after a taxpayer files a return (“original return”) and before the due date (including extensions) for the original return. In contrast, an amended return is a return filed after an original or superseding return is filed and after the expiration of the filing period (including extensions) for the original return.

Per §6501(a) the IRS must assess additional tax for a given tax year within three years after “the return” for that year was filed. The Beard Test has become the standard for what is considered a valid return. To qualify as a “return” under the Beard test, a document must (1) purport to be a return; (2) be signed under penalty of perjury; (3) contain enough information to allow the tax to be calculated; and (4) represent an honest and reasonable attempt to satisfy the tax laws.

Issue 10: Remind Your Clients to Keep Notice 1444 Concerning their Economic Impact Payment – Needed for the 2021 Tax Season

The IRS mails the notice, Notice 1444, Your Economic Impact Payment, to your client’s address of record within a few weeks after the Payment was issued. Individuals should keep the letter for their tax records. The Economic Impact Payment is considered an advance credit against 2020 tax. Taxpayers will not include the payment in taxable income on their 2020 tax return or pay income tax on the payment. It will not reduce a taxpayer’s refund or increase the amount of tax a taxpayer owes when the taxpayer files a 2020 Federal income tax return next year. When a taxpayer files a 2020 tax return next year, the taxpayer may claim any additional credit for which the taxpayer is eligible. The IRS is not able to correct or issue an additional payment at this time and will provide further details on IRS.gov on the action individuals may need to take in the future.

Issue 11: Reminder About IRS Letter 2800C and Employer Federal Income Tax Withholding

IRS sends Letter 2800C, also called a “lock-in” letter, to instruct employers to follow a specific federal income tax withholding arrangement for an employee who doesn’t have enough income taxes withheld from their wages. The employee has 60 days from the date of the letter to discuss the determination with the IRS before the withholding arrangement takes effect. Starting 60 days after the date of the letter, the withholding rate in Letter 2800C is locked in and the employer must begin withholding from the employee at that new rate.

There are two situations in which the employer may withhold at a rate that is different from the rate in Letter 2800C.

- The first occurs if the employee submits a new Form W-4 with a statement supporting a decrease in their withholding rate and the IRS approves. In this situation, the IRS will inform the employer and the employee with a Letter 2808C. Letter 2808C specifies the changes to the employee’s withholding rate that have been approved by the IRS. The changes in Letter 2808C are effective immediately. There is no 60-day waiting period.

- The second situation involves increasing the rate of withholding above what is stated in the “lock-in” letter. This situation occurs if the employee submits a new Form W-4 that results in more withholding than the rate in the “lock-in” letter. In this situation, the employer may accept and process the employee’s request. The employer must disregard any new Form W-4 the employee submits that decreases the amount of withholding.

Employers should block the employee’s access to make changes to online Forms W-4 if that access may allow the employee to decrease their withholding below the rate specified in a Letter 2800C.

Employers that do not withhold federal income tax from their employee as instructed by a “lock-in” letter will be liable for paying the additional tax required to be withheld.

Issue 12: Additional Retail Partners Accepting Cash Payments for Federal Taxes

Additional retail partners are accepting cash payments for federal taxes for both individual and business taxpayers.

The IRS’s continuing partnership with ACI Worldwide’s OfficialPayments.com and the PayNearMe Company allows taxpayers to make a payment without a bank account or credit card at participating 7-Eleven stores, Ace Cash Express and Casey’s General Stores nationwide.

Individuals wishing to take advantage of this payment option should visit the IRS.gov/payments, select the cash option in the “Other Ways You Can Pay” section and follow the instructions. There is a $1,000 payment limit per day and a $3.99 fee per payment.

Because PayNearMe involves a three-step process, the IRS urges taxpayers choosing this option to start the process well ahead of the tax deadline to avoid interest and penalty charges.

Issue 13: Deferral of Employment Tax Deposits and Payments Through December 31, 2020 FAQ’s

The Coronavirus, Aid, Relief and Economic Security Act (CARES Act) allows employers to defer the deposit and payment of the employer’s share of Social Security taxes and self-employed individuals to defer payment of certain self-employment taxes. These FAQs address specific issues related to the deferral of deposit and payment of these employment taxes. These FAQs will be updated to address additional questions as they arise.

- What deposits and payments of employment taxes are employers entitled to defer? 2302 of the CARES Act provides that employers may defer the deposit and payment of the employer’s portion of Social Security taxes and certain railroad retirement taxes. These are the taxes imposed under §3111(a) and, for Railroad employers, so much of the taxes imposed under §3221(a) as are attributable to the rate in effect under §3111(a) (collectively referred to as the “employer’s share of Social Security tax”).

- When can employers begin deferring deposit and payment of the employer’s share of Social Security tax without incurring failure to deposit and failure to pay penalties? The deferral applies to deposits and payments of the employer’s share of Social Security tax that would otherwise be required to be made during the period beginning on March 27, 2020, and ending December 31, 2020. (§2302 of the CARES Act calls this period the “payroll tax deferral period.”) The Form 941, Employer’s QUARTERLY Federal Tax Return, was revised for the second calendar quarter of 2020 (April – June, 2020). In no case will Employers be required to make a special election to be able to defer deposits and payments of these employment taxes.

- Which employers may defer deposit and payment of the employer’s share of Social Security tax without incurring failure to deposit and failure to pay penalties? All employers may defer the deposit and payment of the employer’s share of Social Security tax.

- May an employer that receives a loan under the Small Business Administration Act, as provided in §1102 of the CARES Act (the Paycheck Protection Program (PPP)), defer the deposit and payment of the employer’s share of Social Security tax even if the loan has been forgiven (or partially forgiven) in accordance with paragraph (g) of §1106 of the CARES Act, as amended by § 3 of the Paycheck Protection Program Flexibility Act of 2020 (PPP Flexibility Act)? Yes. The PPP Flexibility Act, enacted on June 5, 2020, amends §2302 of the CARES Act by striking the rule that would have prevented an employer from deferring the deposit and payment of the employer’s share of Social Security tax after the employer receives a decision that its PPP loan was forgiven by the lender. Therefore, an employer that receives a PPP loan is entitled to defer the payment and deposit of the employer’s share of Social Security tax, even if the loan is forgiven. Prior to the enactment of the PPP Flexibility Act, an employer that received a PPP loan was not permitted to defer deposit and payment of the employer’s share of Social Security tax after the receipt of the lender’s decision forgiving all or a portion of the employer’s PPP loan.

- Is this ability to defer deposits of the employer’s share of Social Security tax in addition to the relief provided in Notice 2020-22 for deposit of employment taxes in anticipation of the Families First Coronavirus Relief Act (FFCRA) paid leave credits and the CARES Act employee retention credit? Yes. Notice 2020-22 provides relief from the failure to deposit penalty under §6656 of the Code for not making deposits of employment taxes, including taxes withheld from employees, in anticipation of the FFCRA paid leave credits and the CARES Act employee retention credit. The ability to defer deposit and payment of the employer’s share of Social Security tax under §2302 of the CARES Act applies to all employers, not just employers entitled to paid leave credits and employee retention credits.

- Can an employer that is eligible to claim refundable paid leave tax credits or the employee retention credit defer its deposit and payment of the employer’s share of Social Security tax prior to determining the amount of employment tax deposits that it may retain in anticipation of these credits, the amount of any advance payments of these credits, or the amount of any refunds with respect to these credits? Yes. An employer is entitled to defer deposit and payment of the employer’s share of Social Security tax prior to determining whether the employer is entitled to the paid leave credits under §§7001 or 7003 of FFCRA or the employee retention credit under §2301 of the CARES Act, and prior to determining the amount of employment tax deposits that it may retain in anticipation of these credits, the amount of any advance payments of these credits, or the amount of any refunds with respect to these credits.

- What are the applicable dates by which deferred deposits of the employer’s share of Social Security tax must be deposited to be treated as timely (and avoid a failure to deposit penalty)? The deferred deposits of the employer’s share of Social Security tax must be deposited by the following dates (referred to as the “applicable dates”) to be treated as timely (and avoid a failure to deposit penalty):

-

- On December 31, 2021, 50% of the deferred amount; and

- On December 31, 2022, the remaining amount.

- What are the applicable dates when deferred payment of the employer’s share of Social Security tax must be paid (to avoid a failure to pay penalty under § 6651 of the Code)? The deferred payment of the employer’s share of Social Security tax is due on the “applicable dates” as described in FAQ 7.

- Are self-employed individuals eligible to defer payment of self-employment tax on net earnings from self-employment income? Yes. Self-employed individuals may defer the payment of 50% of the Social Security tax on net earnings from self-employment income imposed under §1401(a) of the Code for the period beginning on March 27, 2020, and ending December 31, 2020. (§2302 of the CARES Act calls this period the “payroll tax deferral period.”)

- Is there a penalty for failure to make estimated tax payments for 50% of Social Security tax on net earnings from self-employment income during the payroll tax deferral period? No. For any taxable year that includes any part of the payroll tax deferral period, 50% of the Social Security tax imposed on net earnings from self-employment income during that payroll tax deferral period is not used to calculate the installments of estimated tax due under §6654 of the Code.

- What are the applicable dates when deferred payment amounts of 50% of the Social Security tax imposed on self-employment income must be paid? The deferred payment amounts are due on the “applicable dates” as described in FAQ 7.

Issue 14: Interest Payment Update on 2019 Refunds

Interest on individual 2019 refunds reflected on returns filed by July 15, 2020 will generally be paid from April 15, 2020 until the date of the refund. Interest payments may be received separately from the refund. By law, the interest rate on both overpayment and underpayment of tax is adjusted quarterly. The interest rate for the second quarter, ending on June 30, 2020, is 5% per year, compounded daily. The interest rate for the third quarter, ending September 30, 2020, is 3% per year, compounded daily.

Issue 15: National Taxpayer Advocate Erin Collins Delivers Her First Report to Congress Identifying COVID – 19 Challenges, the CARES Act and the Taxpayer First Act Implementation as Priority Issues for Taxpayers – This Article Updates IRS Current Condition

The report praises the IRS for acting quickly to postpone over 300 filing, payment, and other time-sensitive deadlines, provide broad relief from compliance actions under its “People First Initiative,” and disburse some 160 million Economic Impact Payments (EIPs) authorized by the CARES Act, enacted on March 27, 2020.

However, the report says that despite the IRS’s best efforts, there have been notable adverse taxpayer impacts, including:

- Taxpayers who filed a 2019 paper return and are entitled to refunds may be in for a long wait. The IRS had to suspend the processing of paper tax returns, and as of May 16, it estimated it had a backlog of 4.7 million paper returns. Although the IRS is reopening some of its core operations, it is not clear when it can open and process all the returns sitting in mail facilities.

- Some taxpayers whose returns were mistakenly flagged by IRS processing filters are experiencing lengthy delays in receiving their refunds. All tax returns claiming refunds are passed through filters designed to detect identity theft and other types of refund fraud. As TAS has documented, some of these filters produce “false positive rates” of more than 50% (meaning that more than half the taxpayers whose returns are stopped by certain filters are entitled to the refunds they claimed). Affected taxpayers are often asked to mail in documentation to substantiate their claims, but the IRS has not opened or processed many of their responses, delaying their refunds. Refund delays can have a significant financial impact on low-income taxpayers, as refunds often constitute a significant percentage of their annual household incomes. Notably, some of the refund delays have been generated by claims for the earned income tax credit or additional child tax credit.

- Taxpayers who have needed help from the IRS have had difficulty obtaining it. The IRS shut down its Accounts Management telephone lines, so taxpayers could not reach a live assistor by telephone. The IRS shut down its Taxpayer Assistance Centers, making it impossible for taxpayers to obtain in-person assistance. The IRS also shut down its mail facilities, so it was unable to log or process taxpayer responses to compliance notices. The only resources readily available were irs.gov and automated telephone lines. The IRS has begun reopening its operations, but it will take some time before they are restored to full capacity.

- IRS systems prepared over 20 million notices during the pandemic that could not be mailed due to closure of notice production centers between April 8 and May 31. The IRS is mailing these notices now. However, some collection notices bear old dates and include response deadlines that often have passed. The IRS plans to include “inserts” with these notices explaining that response deadlines have been postponed, but the report expresses concern that receiving compliance notices with response deadlines that have passed will be confusing and concerning to many taxpayers who may not read the inserts.

- Individuals who did not receive some or all of their EIPs may have to wait until next year to receive them. To date, the IRS has taken the position that most taxpayers who did not receive their full payments must wait until they file their 2020 income tax returns to claim the amounts as credits against their 2020 tax liabilities, even though there is no legal constraint on the IRS’s ability to issue additional EIP amounts as advance refunds during 2020.

- Employers are struggling to determine whether they qualify for the Employee Retention Credit (ERC) and in what amounts. The ERC is a complex, refundable tax credit that requires employers to determine when a trade or business was fully or partially suspended by government order; the employer’s number of full-time employees; what constitutes qualified wages; whether a business’s operations post-COVID-19 are comparable to its pre-COVID-19 operations; and the application of aggregation rules. To address these complexities, the IRS has provided considerable guidance regarding when and how to claim the ERC. However, several areas require further clarification. If clarity is not provided, taxpayers will be more likely to make unintentional errors, increasing the risk of an audit. Having to untangle these issues in an audit environment would drain the limited resources of both the IRS and the businesses affected by the COVID-19 pandemic. TAS will continue to advocate that the IRS further clarify the rules governing when and how employers should claim this credit.

- Businesses are facing challenges when seeking to utilize the CARES Act provision that authorizes the use of net operating losses to offset taxable income in prior years (and in some cases to receive refunds). For businesses to determine the optimal application of the CARES Act provisions so they can exercise their right to pay no more than the correct amount of tax, they may need to create and run complex financial models involving multiple tax years. The report says the IRS has provided timely guidance in the form of frequently asked questions (FAQs), but it expresses concern that FAQs are not authoritative or binding on the IRS.

Issue 16: Update on IRS Liens and Levy Actions FAQ’s

Question: Will IRS Field Collection activities be modified? (updated July 10,2020)

Answer: The IRS suspended new Notices of Federal Tax Lien (NFTLs) and levies initiated by field revenue officers until July 15, 2020, unless the IRS determines there are pressing circumstances, or the taxpayer has agreed to the action. However, importantly, field revenue officers will continue to pursue high-income non-filers and perform other similar activities where warranted. Taxpayers should be aware that revenue officers can contact taxpayers by phone, and that the revenue officer will provide resources if asked, including a direct phone line to call to verify that they are an IRS employee. Generally, the IRS will first mail a bill if a taxpayer owes any taxes. Taxpayers should also be advised of their rights as a taxpayer.

Question: Is the Collection Statute Expiration Date (CSED) affected by the People First Initiative or COVID-19 relief? (updated July 10, 2020)

Answer: No. The COVID-19 relief does not change the Collection Statute Expiration Date (CSED). All activities affecting the CSED still apply based on law and regulation. The IRS will continue to take necessary steps to protect all applicable statutes of limitations. In instances when statutes are in jeopardy of expiring, IRS encourages taxpayers to cooperate in extending such statutes. Otherwise, the IRS may pursue actions to protect the interests of the Government.

Question: Are new levies being issued? (updated July 10, 2020)

Answer: The IRS suspended new automated levies, and new systemic NFTL requests and levies until at least July15, 2020. The IRS will not issue new levies unless there are pressing circumstances, or the taxpayer has agreed to the action.

Question: What is the date that the IRS considers a lien or levy new? (updated July 10, 2020)

Answer: Beginning March 30, 2020, the IRS generally suspended the initiation of levies and NFTLs until at least July15, 2020. “New” levies and NFTLs will not be initiated until after July 15, 2020, unless there are pressing circumstances.

Question: If the IRS issues a release of levy, how long will it take until the funds are available to me?

Answer: Generally, the IRS will mail or fax a release of levy to the levy source. The timeframe for the release to take effect will be dependent on mail and processing times once received by the levy source. If the levy source will accept a release of levy via fax, the taxpayer may provide a contact or fax number and request a copy of the release be sent via fax.

Question: Will levies and wage garnishments remain in place or will these be paused until July 15, 2020? Can the taxpayer request a pause? If so, how? (updated July 10, 2020)

Answer: The IRS will not automatically release levies. The IRS will consider a taxpayer’s request to release a levy on a case-by-case basis if the levy is causing an economic hardship. “Economic hardship” means the levy prevents the taxpayer from meeting basic, reasonable living expenses. The IRS may ask for additional financial information to determine if a levy is causing an economic hardship. If the taxpayer is working with a revenue officer and wants to request a release of levy, they should contact the revenue officer. Taxpayers requiring a levy release who are not assigned to work with a revenue officer should call the telephone number on the notice of levy. If a taxpayer is unable to get through, they should fax their request to 855-796-4524. The fax should include their name, address and social security number. If they filed jointly please include both social security numbers. In addition, include the name, address and fax number of the taxpayer’s employer or bank that is processing the levy. Note: This fax number is only used to address emergency levy release requests. Due to current limited staffing, the IRS will not respond to other issues sent to this fax line.

Question: Will the IRS file Notices of Federal Tax Lien (NFTLs) during the suspension period? (updated July 10, 2020)

Answer: Generally, the IRS has not filed new NFTLs unless there was a risk of permanent loss to the Government due to pressing circumstances. However, previously filed NFTLs were refiled, amended, withdrawn, or released if appropriate.

Question: What happens with Notice of Federal Tax Lien filings after July 15,2020? (updated July 10, 2020)

Answer: The IRS will resume making NFTL determinations and filing new NFTLs following standard procedures after July 15, 2020.

Question: Will the IRS discharge property from the federal tax lien or subordinate its lien interest during the suspension period?

Answer: The IRS continued to process requests for lien certificates and issue the certificates based on each case’s merits. The timeframe to work these requests may be longer than normal due to resource constraints impacted by COVID-19.

Question: What should a taxpayer do if they need a Federal lien release, certificate of discharge, or have another Federal tax lien issue? (updated July 10, 2020)

Answer: The IRS continues to process all electronically submitted lien certificate applications normally. The IRS requests taxpayers use the E-Fax line for our ACR site (844-201-8382) for certificates such as: discharge of property from the Federal tax lien; withdrawal of the Notice of Federal Tax Lien; and subordination of the Federal tax lien. Publication 4235, Collection Advisory Group Numbers and Addresses, and IRS.gov have additional information on the process for submitting applications for lien certificates.

Question: What is a CP504 Notice? (updated July 10, 2020)

Answer: The CP504 Notice lets a taxpayer know if they have an unpaid amount due on their account. If they do not pay the amount due immediately, the IRS will seize (levy) their state income tax refund and apply it to pay the amount they owe. The IRS will still issue CP504 Notices during the relief period, but the IRS will not issue the Final Notice of Intent to Levy Letter 1058 or LT11, unless there are pressing circumstances, which is required before a levy can be issued. The IRS will not issue Notices of Levy during the collection suspension period, unless there are pressing circumstances. This includes automated levy programs such as: The Federal Payment Levy Program; the State Income Tax Levy Program; and the Municipal Income Tax Levy Program.

Question: What should I do if I receive a CP 504 Notice? (updated July 10,2020)

Answer: Pay the amount due shown on the notice. Taxpayers may pay their balance online or mail their payment to the IRS in the envelope they received. Include the bottom part of the notice to make sure the IRS correctly credits the account. If a taxpayer can’t pay the whole amount now, they can resolve outstanding liabilities by entering into a monthly payment agreement.

Question: How does this initiative affect the Private Debt Collection program? (updated July 10, 2020)

Answer: During the suspension period the IRS did not forward new delinquent accounts to Private Collection Agencies (PCAs). PCA interaction with taxpayers is limited to inbound telephone calls (outbound calls only when requested in a voicemail or correspondence) until July 15, 2020. When the taxpayer indicates their ability to pay was affected by COVID, the PCA will place a hold on the account through July 15, 2020. The PCAs will not terminate or modify existing payment arrangements during the suspension period. Taxpayers should resume their payments with the first payment due on or after July 16, 2020 to avoid defaulting.

Question: Are taxpayers with payment arrangements made through IRS contracted Private Collection Agencies allowed to suspend those payments during the COVID-19 suspension period?

Answer: Taxpayers can make payments on their account at any time. If a taxpayer is not able to make payments during the suspension period from April 1 to July 15, 2020 under the People First Initiative, relief is provided. The private collection agencies (PCAs) will: restrict outbound calls to only when the taxpayer requests a return call in correspondence or via voice message not terminate or restructure an existing payment arrangement suspend payment reminder or missed/late payment letters and telephone calls continue to send reminder notices for the taxpayer’s preauthorized direct debit payments which includes instruction on how to cancel or change payments.

Question: Can taxpayers request to have their Private Collection Agency account transferred back to the IRS?

Answer: Taxpayers can request in writing that their account be returned to the IRS and have no further contact from the private collection agency at any time, which is a protection provided under the Fair Debt Collection Practices Act.

Question: Will the IRS continue to work bankruptcy-related issues?

Answer: Yes. The IRS continues to file Proofs of Claim, address automatic stay violations, apply payments, and process and discharge orders.

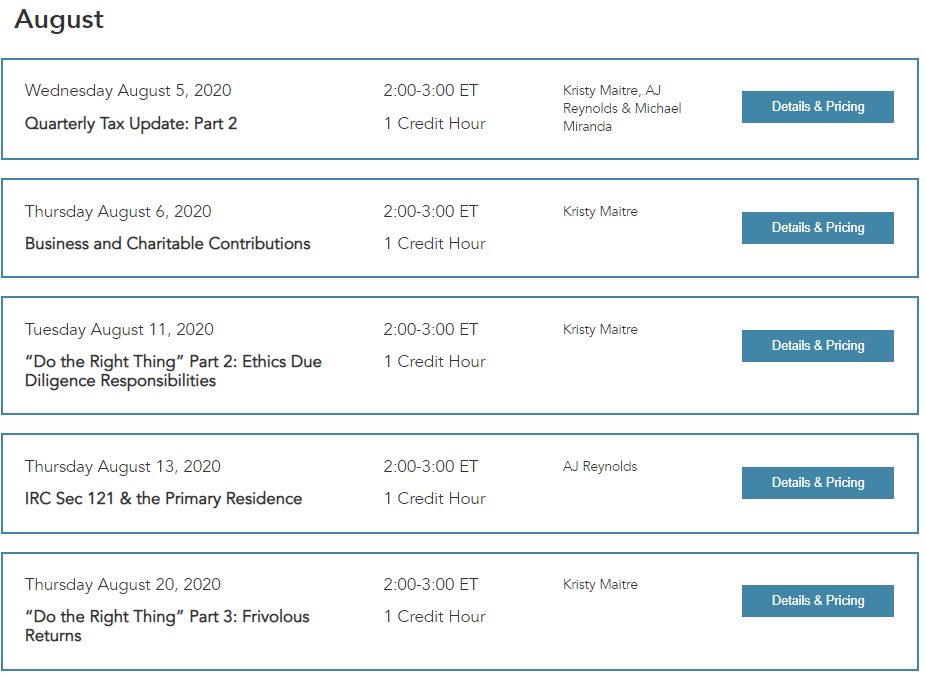

Issue 17: August 2020 Webinars

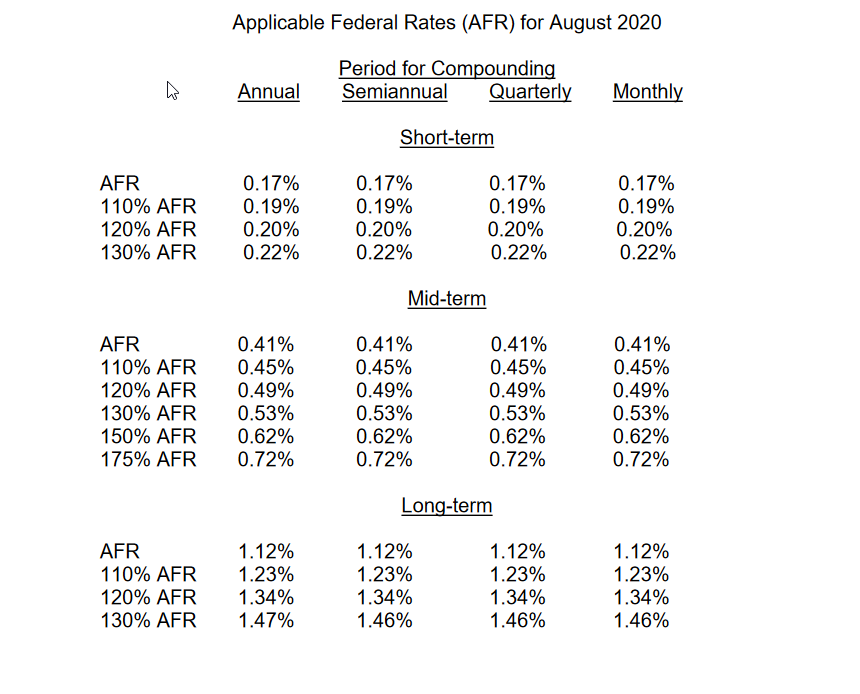

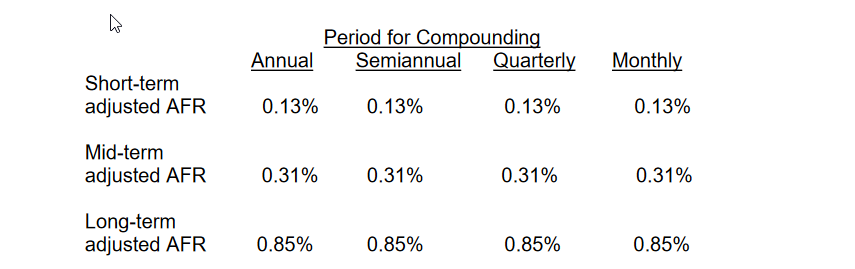

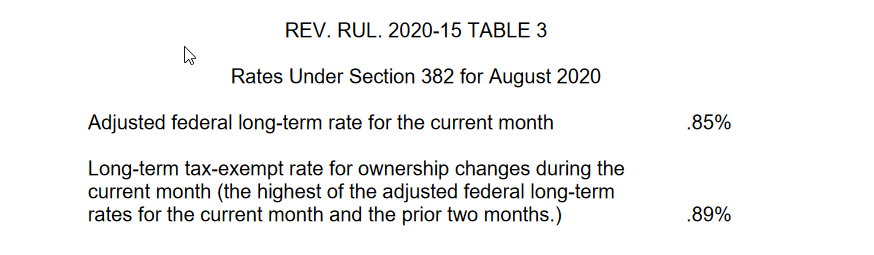

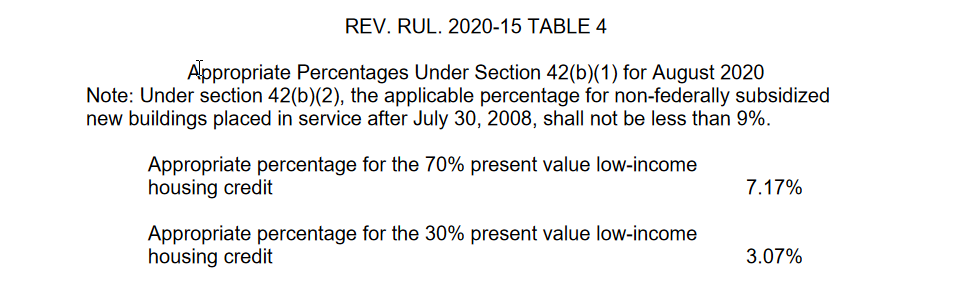

Issue 18: Applicable Federal Rates (AFR) for August 2020

REV. RUL. 2020-15 TABLE 5Rate Under Section 7520 for August 2020

Applicable federal rate for determining the present value of an annuity, an interest for life or a term of years, or a remainder or reversionary interest. 4%