In This Issue

Issue 1: How A Client’s Custody Situation Affect Their Advanced Child Tax Credit Payments

Issue 2: Social Security Numbers for Amish Children – IRM 21.6.1.6.1

Issue 3: NTA Blog: Decoding IRS Transcripts and the New Transcript Format

Tax Planning Opportunities

Issue 4: Flexible Spending Arrangements

Issue 5: What Do We Need to Be Concerned About Related to Capital Gains?

Issue 6: Non-itemized Deduction: Charitable Contributions

Issue 7: 2021 Education Changes

Issue 8: Earned Income Tax Credit Changes

Issue 9: Retirement Plan Proposals

Issue 10: Gift Tax Changes

Issue 11: Health Savings Account – 2022 Changes – Rev. Proc. 2021-25

Issue 12: Extenders and Expiring Provisions 2021

Issue 13: Rev. Proc. 2021-45 Inflationary Adjustments to Key IRS Provisions for 2022

Issue 14: Tax Professional Can Order More Transcripts from IRS.

Issue 15: The Golden Rules of Quality

Issue 16: Applicable Federal Rates for December 2021, Rev. Rul. 2021-23

Issue 1: How A Client’s Custody Situation Affect Their Advanced Child Tax Credit Payments

Parents who share custody of their children should be aware of how the advance child tax credit payments are distributed. It is important to remember that these are advance payments of a tax credit that taxpayers expect to claim on their 2021 tax return.

Here are some of the most common questions about shared custody and the advance child tax credit payments.

If two parents share custody, how will the IRS decide which one receives the advance child tax credit payments?

Who receives 2021 advance child tax credit payments is based on the information on the taxpayer’s 2020 tax return, or their 2019 return if their 2020 tax return has not been processed. The parent who claimed the child tax credit on their 2020 return will receive the 2021 advance child tax credit payments.

If a parent is receiving 2021 advance child tax credit payments and they shouldn’t be, what should they do?

Parents who will not be eligible to claim the child tax credit when they file their 2021 tax return should go to IRS.gov and unenroll to stop receiving monthly payments. They can do this by using the Child Tax Credit Update Portal. Receiving monthly payments now could mean they have to return those payments when they file their tax return next year. If their custody situation changes and they are entitled to the child tax credit for 2021, they can claim the full amount when they file their tax return next year.

If parents alternate years claiming their child on their tax return, will the IRS send the 2021 advance child tax credit payments to the parent who claimed the child on their 2020 tax return even though they will not claim them on their 2021 tax return?

Yes. Because the taxpayer claimed their child on their 2020 tax return, the IRS will automatically issue the advance payments to them. When they file their 2021 tax return, they may have to pay back the payments over the amount of the credit they’re entitled to claim. Some taxpayers may be excused from repaying some or all of the excess amount if they qualify for repayment protection. If a taxpayer will not be claiming the child tax credit on their 2021 return, they should unenroll from receiving monthly payments using the Child Tax Credit Update Portal.

If one parent is receiving the advance child tax credit payments even though the other parent will be claiming the child tax credit on their 2021 tax return, will the parent claiming the qualifying child still be able to claim the full credit amount?

Yes. Taxpayers will be able to claim the full amount of the child tax credit on their 2021 tax return even if the other parent is receiving the advance child tax credit payments. The parent receiving the payments should unenroll, but their decision will not affect the other parent’s ability to claim the child tax credit.

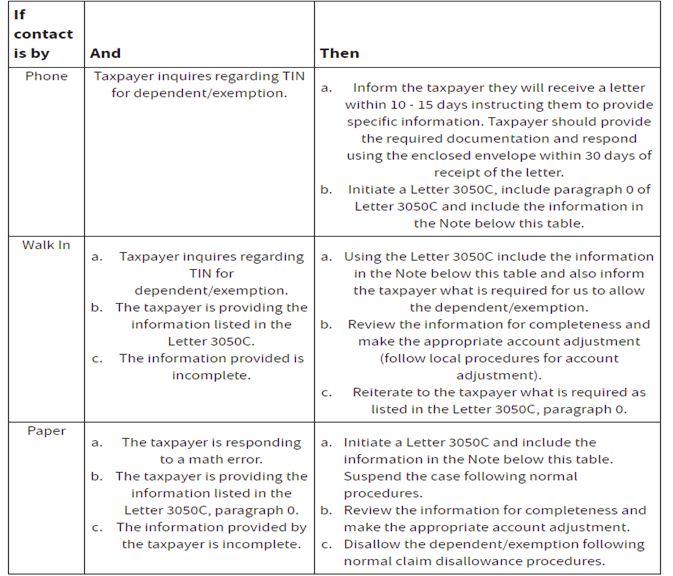

Issue 2: Social Security Numbers for Amish Children – IRM 21.6.1.6.1

For 2021, a legal dependent who is age 17 or younger (as of December 31, 2021) can qualify for the child tax credit. This is the first year that 17-year-olds qualify for the CTC (the previous age limit was 16). Children also must have a Social Security number (SSN) to qualify for the 2021 child tax credit. This requirement is the same as in previous years. Children with ITINs are not eligible for the child tax credit in 2021. Parents do not need to have SSNs, only the children do.

IRS Process

The IRS will allow primary, secondary and dependent taxpayers identified as having a religious or conscience-based objection, even if the taxpayer fails to provide a valid TIN. If the taxpayer was NOT allowed during original processing, adjust the account.

Note: For TY 2017 and prior, secondary and/or dependent exemptions were not initially allowed if the religious objector did not identify as Amish, Mennonite, or a Form 4029 filer.

The IRS will initially disallow any TIN related credits claimed on a return indicating a religious or conscience-based objection to providing TINs for the “qualifying” dependent(s). Beginning in TY 2018, this includes Amish, Mennonite, and Form 4029 filers claiming the Child Tax Credit. Taxpayers will receive a math error notice stating their TIN related credit was not allowed because a TIN was not furnished.

In some cases, taxpayers claiming a religious or conscience-based objection to obtaining a TIN will be allowed the dependent/exemption or related credits when they provide specific documentation. Refer to IRM 21.6.3, Credits, for information on specific credits.

Note: Do not allow EIC unless the taxpayer(s) and qualifying dependent(s) have a valid SSN and all other qualifications are met. For Tax Years 2018-2025, do not allow the CTC unless the qualifying child(ren) has a required SSN, and all other qualifications are met.

If the taxpayer contacts IRS stating they have a religious or conscience-based objection to providing a TIN, follow the procedures listed below:

Issue 3: NTA Blog: Decoding IRS Transcripts and the New Transcript Format

Many individuals may not know they can request, receive, and review their tax records via a tax transcript from the IRS at no charge. Transcripts are often used to validate income and tax filing status for mortgage applications, student loans, social services, and small business loan applications and for responding to an IRS notice, filing an amended return, or obtaining a lien release. Transcripts can also be useful to taxpayers when preparing and filing tax returns by verifying estimated tax payments, Advance Child Tax Credits, Economic Income Payments/stimulus payments, and/or an overpayment from a prior year return.

The IRS maintains records for all taxpayers – individuals, businesses, and other entities – and provides five types of transcripts. A requested transcript may provide information regarding the date the IRS received a return; payment history including refunds, transfers between tax years and overpayment credits; balance due amounts; interest assessed; refundable credits allowed; basic examination information; and Forms W-2 or 1099 information.

Taxpayers may be able to get answers to their questions quickly and efficiently by requesting and reviewing their transcript – that is, if they can decipher them. Taxpayers can request a transcript online through the IRS’s Get Transcript Online portal or their online account; by mail; or by calling the IRS’s automated phone transcript service at 800-908-9946.

What Transcript Should the Clients Ask For?

There are several types of transcripts that can meet a client’s needs.

Tax Return Transcript: This shows most items reflected on a taxpayer’s original tax return, including adjusted gross income, and accompanying forms and schedules for the current year and three prior years. This transcript will often be accepted by lending institutions for student loan or mortgage purposes. Note: the secondary spouse on a joint return must use Get Transcript Online or Form 4506-T to request this transcript type. When using Get Transcript by Mail or phone, the primary taxpayer on the return must make the request.

Wage and Income Transcript: This provides data from the third-party information statements the IRS has received for a specific taxpayer, such as Forms W-2, 1099, 1098, or 5498, and can be useful if the client did not receive or retain a copy of these documents. Wage and Income Transcripts are available for up to ten years. While the Wage and Income transcript provides federal withholding amounts, it does not reflect state tax withholdings, which may limit its use when preparing state income tax returns.

Tax Account Transcript: This provides basic tax return data (marital status, adjusted gross income, taxable income) along with listing the activity on a tax account, such as tax adjustments, payments, etc., for the current year and up to ten prior years using Get Transcript Online. When using Get Transcript by Mail or phone, taxpayers are limited to the current tax year and returns processed during the prior three years.

Record of Account Transcript: This is the most comprehensive transcript. It combines the Tax Return Transcript and the Tax Account Transcript to provide a more complete picture of a taxpayer’s tax return and subsequent account activity for the current year and for returns processed in the three prior years.

Verification of Non-Filing Letter: This provides proof that the IRS has no record of a filed Form 1040-series tax return for the year requested. However, it doesn’t indicate whether a client was required to file a return for that year. This letter is available after June 15 for the current tax year or any time for the prior three tax years using Get Transcript Online.

Another Option: Log into the Client’s Personal Online Account

Individual clients with an Online Account can immediately access the above transcript options for the current filing year and three prior years and in some cases up to ten years of data. They can also see the total amount owed, balance details by year, payment history and any scheduled or pending payments; key information from the most recent tax return; payment plan details, if the taxpayer has one; digital copies of select notices from the IRS; Economic Impact Payments received, if any; the address on file; and any authorization requests from tax professionals.

If clients have not created an online account, this may be the impetus to do so, but be aware many taxpayers are not able to pass the authentication process. The IRS will be updating its authentication process by the end of the year, which is anticipated to reduce the unsuccessful attempts to establish an online account.

Tax Professionals’ Access to Client’s Transcript

Tax professionals with an authorized power of attorney on file can review a client’s transcript by accessing the IRS’s e-Services Transcript Delivery System to obtain a masked Wage and Income Transcript. If employer information is needed for tax return preparation, tax practitioners may order an unmasked Wage and Income Transcript if the client does not have the employment information. The practitioner must have a Centralized Authorization File (CAF) number in good standing and have an e-Services account and access to the SOR, the e-Services secure mailbox.

Tax practitioners who meet those requirements should:

- Call the Practitioner Priority Service line.

- Authenticate identity with CAF number, name, Social Security number, and date of birth.

- Fax a completed authorization form (if needed).

- Request an unmasked Wage and Income Transcript; and

- Access the e-Services secure mailbox to receive the unmasked Wage and Income Transcript.

Tax practitioners who do not have an e-Services account or SOR access may request that the unmasked Wage and Income Transcript is mailed to the client’s address of record.

Reading and Understanding IRS Transcripts

The IRS’s processing system, the Integrated Data Retrieval System (IDRS), uses a system of codes to identify a transaction the IRS is processing and to maintain a history of actions posted to a taxpayer’s account. These Transaction Codes (TCs) basically provide processing instructions to the IRS’s system. To make IRS transcripts user-friendly for the public, the IRS provides a literal description of each TC shown on a taxpayer’s IRS transcript. Although helpful, sometimes these descriptions don’t adequately explain the account transaction. Document 11734, Transaction Code Pocket Guide, is a summarized list of TCs taken from Section 8A of the IRS’s Document 6209, ADP and IDRS Information Reference Guide, both of which may be helpful when reviewing an IRS transcript.

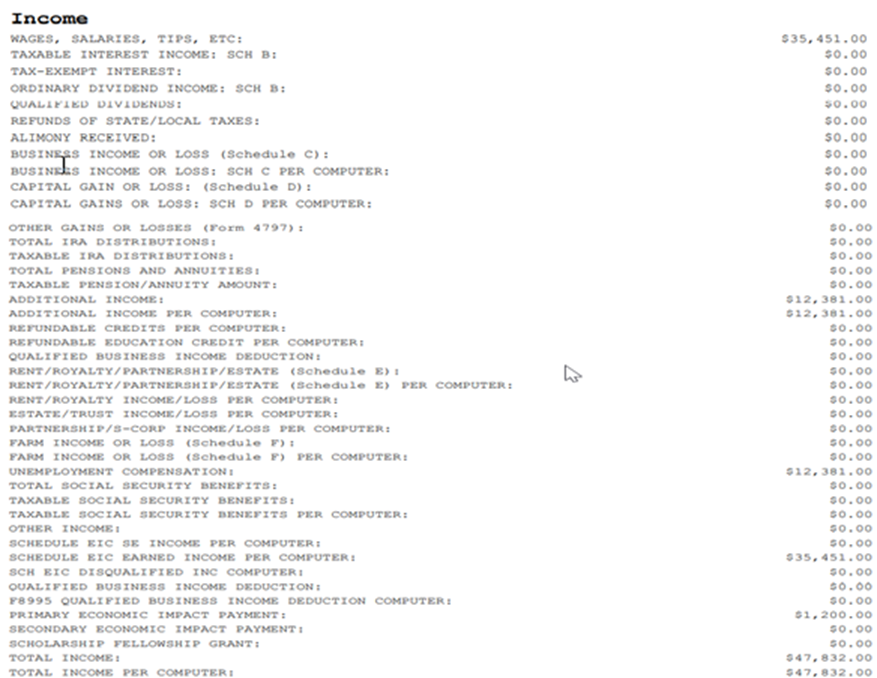

A Closer Look at the IRS Record of Account Transcript

As shown in the fictitious example below, the Record of Account Transcript will summarize any balance due or overpayment on a client’s account for the specified year at the top of the form. If the account reflects a balance due, the transcript provides the date to which any accrued penalty and interest were calculated.

Next, the transcript will show specific information from the client’s return – or the corrected amounts resulting from any changes to the return caused by either a request from the client or an IRS determination. This is noteworthy should a taxpayer find it necessary to file an amended return. The correct figures must be used as the starting point on Form 1040X, Amended US Individual Income Tax Return, when requesting any subsequent account adjustments – otherwise, processing problems may occur.

Figure 1

![]()

The Tax Account Portion of the Record of Accounts

This section of the Record of Accounts Transcript provides details regarding the taxpayer’s account activity, as shown in Figure 2.

Figure 2

![]()

Some of the common TCs on the tax account portion of a transcript are:

- TC 150 – Date of filing and the amount of tax shown on the taxpayer’s return when filed – or as corrected by the IRS when processed.

- TC 196 – Interest Assessed.

- TC 276 – Failure to Pay Tax Penalty.

- TC 291 – Abatement Prior Tax Assessment.

- TC 300 – Additional Tax or Deficiency Assessment by Examination Division or Collection Division.

- TC 420 – Examination Indicator reflects that a return is under examination consideration though the return may or may not ultimately be audited.

- TC 428 – Examination or Appeals Case Transfer.

- TC 460 – Extension of Time for Filing.

- TC 480 – Offer in Compromise Pending.

- TC 494 – Notice of Deficiency.

- TC 520 – IRS Litigation Instituted.

- TC 530 – Indicates that an account is currently not collectible.

- TC 582 – Lien Indicator.

- TC 768 – Earned Income Credit.

- TC 806 – Reflects any credit the taxpayer is given for tax withheld, as shown on the tax return and the taxpayer’s information statements such as Forms W-2 and 1099 attached to the taxpayer’s tax return; and

- TC 846 – Represents the issuance of a taxpayer’s refund if the credits and withholding exceed the amount of tax due, and there are no issues with the return, the system will automatically generate a refund.

In the above example, tax credits, withholding credits, credits for interest the IRS owes to a taxpayer, and tax adjustments that reduce the amount of tax owed, are shown as negative amounts on the tax account transcript. In other words, negative amounts on an IRS transcript can be considered amounts “in the taxpayer’s favor.”

Because TCs on a client’s account are essentially instructions to the IRS system, it is important to note that some TCs are input for informational reasons not directly associated with an accounting-related dollar amount.

The Tax Return Portion of the Record of Accounts

The tax return portion of the Record of Accounts depicts most of the line entries on the taxpayer’s tax return when it was filed. Figure 3 provides only the income section of our fictitious example; however, the actual Record of Accounts will depict all the sections of a client’s filed tax return and can be useful when the client has not maintained a copy of his or her return and needs to know what was reported to the IRS on his or her return.

Figure 3

New Tax Transcript Format and Utilizing a Customer File Number

In July 2021, IRS updated a webpage on IRS.gov to educate taxpayers regarding the new transcript format and use of the “customer file number,” which was designed to better protect the client’s data. This new format partially masks personally identifiable information. However, financial data will remain visible to allow for tax return preparation, tax representation, or income verification. These changes apply to transcripts for both individual and business taxpayers.

Here’s what is visible on the new tax transcript format:

- Last four digits of any Social Security number on the transcript: XXX-XX-1234.

- Last four digits of any Employer Identification Number on the transcript: XX-XXX1234.

- Last four digits of any account or telephone number.

- First four characters of first name and first four characters of the last name for any individual (first three characters if the name has only four letters).

- First four characters of any name on the business name line (first three characters if the name has only four letters).

- First six characters of the street address, including spaces; and

- All money amounts, including wage and income, balance due, interest, and penalties.

For security reasons, the IRS no longer offers fax service for most transcript types to both taxpayers and third parties and has stopped its third-party mailing service via Forms 4506, 4506-T, and 4506T-EZ.

Only individual taxpayers may use Get Transcript Online or Get Transcript by Mail. Because the full Taxpayer Identification Number is no longer visible, the IRS created an entry for a Customer File Number.

The Customer File Number is a ten-digit number assigned by the third-party, for example, a loan number that can be manually entered when the taxpayer completes his or her Get Transcript Online or Get Transcript by Mail request. This Customer File Number will then display on the transcript when it is downloaded or mailed to the client. The transcript’s Customer File Number serves as a tracking number that enables a lender or other third party to match the transcript to the taxpayer making the transcript request.

Tax Planning Tips

Issue 4: Flexible Spending Arrangements

The carryover period for unused amounts in a health flexible spending arrangement (health FSA) is expanded as follows:

For plan years ending in 2021, FSAs may allow participants to carry over any unused benefits or contributions to 2022, the plan is not required to offer this option.

Plans may extend the grace period for a plan year ending in 2021 to 12 months after the end of the plan year, with respect to unused benefits or contributions remaining in a health FSA or dependent care FSA.

FSAs may allow an employee who ceases participation in the plan during calendar year 2021 to continue to receive reimbursements from unused benefits or contributions through the end of the plan year in which the participation ceased.

There is a special carry forward rule for dependent care FSAs.

Issue 5: What Do We Need to Be Concerned About Related to Capital Gains?

Under proposed legislation, top capital gains tax rates would increase from 20% to 25%. The rate increase would apply for purposes of both the regular tax and the AMT. The effective date would be gains realized after September 13, 2021. The top rate would be 28.8% when combined with a 3.8% surtax on net investment income. Take care to monitor this situation carefully when planning with clients.

Issue 6: Non-itemized Deduction: Charitable Contributions

For 2021, an individual who does not itemize deductions for the tax year is entitled to deduct eligible charitable contributions up to $300 ($600 for a joint return). Eligible contributions must be in cash, and be made to a public charity, and not be made to a § 509(a) (3) supporting organization or to establish or maintain a donor advised fund.

In 2020 the above-the-line deduction was limited to a total of $300 regardless of filing status.

Issue 7: 2021 Education Changes

- For tax years 2021-2025, discharges of many public and private student loans are excluded from gross income.

- The above-the-line deduction for qualified tuition and related expenses was repealed.

- Qualified emergency financial aid grants under the CARES Act are excluded from the gross income of college and university students.

- The different phaseout rules for the American Opportunity Tax Credit (AOTC) and the Lifetime Learning Credit are replaced with a single phaseout.

Issue 8: Earned Income Tax Credit Changes

- In determining EITC for 2021, clients may elect to substitute their earned income for 2019 if that 2019 amount is greater than the earned income for the client’s earned income for 2021.

- The EITC rules under which certain separated married people do not need to file jointly have been relaxed.

- An individual will not be treated as married if the following apply:

- The individual is married (as defined in § 7703(a)).

- The individual does not file a joint return for the tax year.

- The individual lives with their qualifying child for more than half of the tax year; and

- Either (1) during the last six months of the year, the individual does not have the same principal place of abode as their spouse, or

- (2) The individual has a written separation agreement or a decree requiring one spouse to make payments for the support or maintenance of the other spouse.

- An individual will not be treated as married if the following apply:

NOTE: This is not a new filing status and only applies the EITC as described above.

- The maximum age for the EITC is eliminated for 2021 (only).

- The disqualified income threshold is raised from $3,650 to $10,000.

- The EITC is expanded for clients with no qualifying children, for 2021, for clients with no qualifying children:

- The 7.65% credit percentage and phaseout percentage is increased to 15.3%.

- The $4,220 earned income amount is increased to $9,820.

- The $5,280 phaseout amount is increased to $11,610. (The $5,000 increase for married taxpayers filing a joint return stays the same, so the phaseout amount this year for joint filers is $16,610.

Issue 9: Retirement Plan Proposals

Under pending legislation that would be effective for tax years beginning after 2022, high-income taxpayers and others with very large retirement plan and/or IRA accounts would be subject to new contribution limits, distribution requirements, and penalties. Aggregate plan accumulations could not exceed $10-million, annual additions would be limited, increased minimum distributions would be required, and new excise taxes could be imposed on violations. New restrictions would also apply to conversions from IRAs and employer plans to Roth IRAs. Monitor this issue as we move close to year end. Planning may be required in 2022 to avoid potential changes under the proposed legislation, if it were to become law.

Issue 10: Gift Tax Changes

Besides the typical year-end estate planning considerations, substantial proposed estate tax legislative changes could come into effect in 2022, requiring reevaluation of many estate plans.

The annual gift tax exclusion for 2021 is $15,000, for 2022 it has increased to $16,000. For calendar year 2022, the first $164,000 of gifts to a spouse who is not a citizen of the United States (other than gifts of future interests in property) are not included in the total amount of taxable gifts under §§ 2503 and 2523(i)(2) made during that year.

A gift that qualifies for the exclusion is not subject to gift tax or Generation-Skipping Transfer Tax. Unused annual exclusions cannot be carried over and are forever lost.

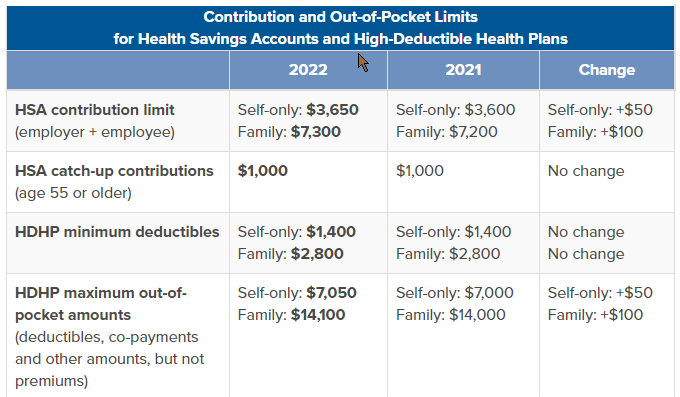

Issue 11: Health Savings Account – 2022 Changes – Rev. Proc. 2021-25

The revenue procedure provides the 2022 inflation adjusted amounts for Health Savings Accounts (HSAs) as determined under § 223 of the Internal Revenue Code and the maximum amount that may be made newly available for excepted benefit health reimbursement arrangements (HRAs) provided under § 54.9831-1(c)(3)(viii) of the Pension Excise Tax Regulations.

Annual contribution limitation.

Issue 12: Extenders and Expiring Provisions 2021

Note: The ever-changing provisions of the Build Back Better Act could change any one of the provisions listed below.

Provisions Expiring in 2021

- Three-Year Depreciation for Racehorses Two Years or Younger.

- Accelerated Depreciation for Business Property on an Indian Reservation.

- American Samoa Economic Development Credit.

- Indian Employment Tax Credit.

- Mine Rescue Team Training Credit.

- The Rum Cover Over Other Temporary Provisions.

- Computation of Adjusted Taxable Income Without Regard to Any Deduction Allowable for Depreciation, Amortization, or Depletion.

- 5% Increase in Annual LIHTC Authority.

- Temporary Business Provision Enacted in the Families First Coronavirus Response Act, 2020, and Subsequently Extended.

- Payroll Tax Credits for COVID-19 Sick and Family Leave.

- Employee Retention and Rehiring Credit – Ends September 30,2021.

- Prevention of Partial Plan Termination Provisions.

Expiring in 2022

- 50% Rate for Railroad Track Maintenance Other Temporary Provision.

- Full Deduction for Business Meals Provisions.

Expiring in 2025

- Special Expensing Rules for Certain Film, Television, and Live Theatrical Productions.

- Seven-Year Recovery Period for Motorsports Entertainment Complexes.

- Empowerment Zone Tax Incentives.

- New Markets Tax Credit.

- Employer Tax Credit for Paid Family and Medical Leave

- Work Opportunity Tax Credit.

- Transfers of Excess Pension Assets to Retiree Health and Life Insurance Plans.

- Look-Through Treatment of Payments Between Related Controlled Foreign Corporations Other Temporary Provisions.

- Deductibility of Employer De Minimis Meals and Related Eating Facility, and Meals for the Convenience of the Employer.

- Higher Exclusion Rates for GILTI and FDII.

- Lower Tax Rates and Credits for BEAT.

- 20% Deduction for Pass-Through Businesses Provisions.

Expiring in 2026 or 2027

Other Temporary Provisions Expiring in 2026

- Limit on Excess Business Losses of Noncorporate Taxpayers.

- First Year Depreciation.

- Additional Depreciation for Trees Producing Fruits and Nuts.

- Election to Invest Capital Gains in an Opportunity Zone.

Other Temporary Provision Expiring in 2027

- Citrus Plants Lost by Casualty.

Business Tax Extender Provisions Made Permanent

- Credit for Certain Expenditures for Maintaining Railroad Tracks.

- Provisions Modifying the Excise Taxes on Wine, Beer, and Distilled Spirits.

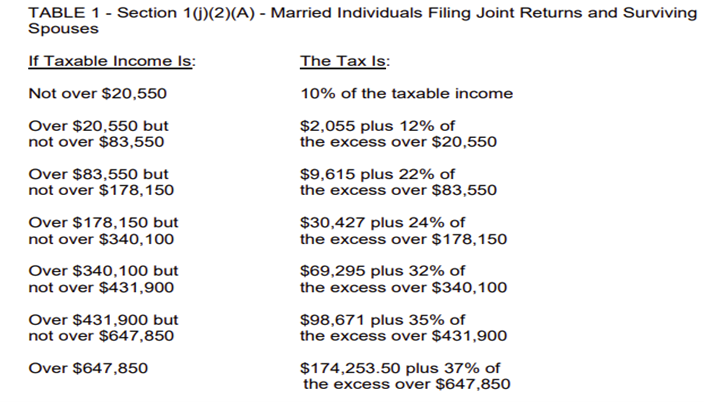

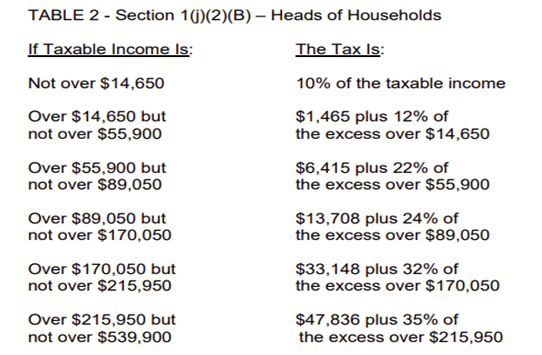

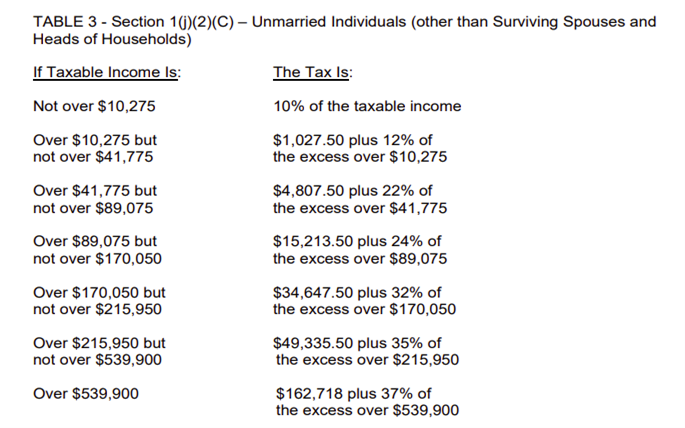

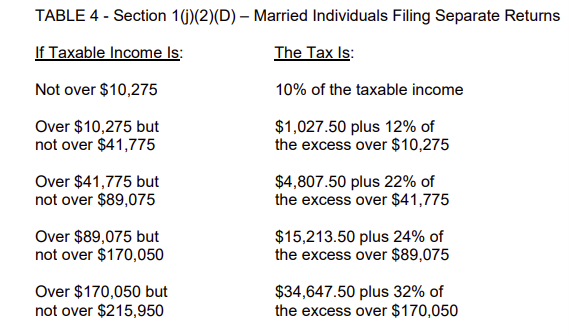

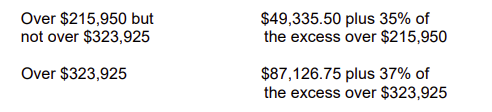

Issue 13: Rev. Proc. 2021-45 Inflationary Adjustments to Key IRS Provisions for 2022

2022 Tax Rate Tables

Unearned Income of Minor Children (the “Kiddie Tax”)

For taxable years beginning in 2022, the amount in § 1(g)(4)(A)(ii)(I), which is used to reduce the net unearned income reported on the child’s return that is subject to the “kiddie tax,” is $1,150.

This $1,150 amount is the same as the amount provided in § 63(c)(5)(A), as adjusted for inflation. The same $1,150 amount is used for purposes of § 1(g)(7) (that is, to determine whether a parent may elect to include a child’s gross income in the parent’s gross income and to calculate the “kiddie tax”).

Maximum Capital Gains Rate

For taxable years beginning in 2022, the Maximum Zero Rate Amount under § 1(h)(1)(B)(i) is:

| $83,350 | Joint return or surviving spouse |

| $41,675 | Married individual filing a separate return |

| $55,800 | Individual who is a Head of Household (§ 2(b)) |

| $41,675 | Any other individual (other than an estate or trust) |

| $2,800 | In the case of an estate or trust |

The Maximum 15% Rate Amount under § 1(h)(1)(C)(ii)(l) is:

| $517,200 | Joint return or surviving spouse |

| $258,600 | Married individual filing a separate return |

| $488,500 | Individual who is the Head of a Household (§ 2(b)), |

| $459,750 | Any other individual (other than an estate or trust) |

| $13,700 | An estate or trust

|

Adoption Credit

For taxable years beginning in 2022, under § 23(a)(3) the credit allowed for an adoption of a child with special needs is $14,890. For taxable years beginning in 2022, under § 23(b)(1) the maximum credit allowed for other adoptions is the amount of qualified adoption expenses up to $14,890.

The available adoption credit begins to phase out under § 23(b)(2)(A) for taxpayers with modified adjusted gross income in excess of $223,410 and is completely phased out for taxpayers with modified adjusted gross income of $263,410 or more.

Child Tax Credit

For taxable years beginning in 2022, the amount used in § 24(d)(1)(A) to determine the amount of credit under § 24 that may be refundable is $1,500.

Earned Income Credit

For taxable years beginning in 2022, the following amounts are used to determine the earned income credit under § 32(b). The “earned income amount” is the amount of earned income at or above which the maximum amount of the earned income credit is allowed.

The “threshold phaseout amount” is the amount of adjusted gross income (or, if greater, earned income) above which the maximum amount of the credit begins to phase out.

The “completed phaseout amount” is the amount of adjusted gross income (or, if greater, earned income) at or above which no credit is allowed.

The threshold phaseout amounts and the completed phaseout amounts shown in the table below for married taxpayers filing a joint return include the increase provided in § 32(b)(2)(B), as adjusted for inflation for taxable years beginning in 2022. The threshold phaseout amounts and the completed phaseout amounts shown in the table below for single, surviving spouse, or head of household taxpayers also apply to married taxpayers who are not filing a joint return and satisfy the special rules for separated spouses in § 32(d).

| Number of Qualifying Children | ||||

| Item | One | Two | Three or More | None |

| Earned Income Amount | $10,980 | $15,410 | $15,410 | $7,320 |

| Maximum Amount of Credit | $3,733 | $6,164 | $6,935 | $560 |

| Threshold Phaseout $20,130 $20,130 $20,130 $9,160 Amount (Single, Surviving Spouse, or Head of Household) | $20,130 | $20,130 | $20,130 | $9,180 |

| Completed Phaseout $43,492 $49,399 $53,057 $16,480 Amount (Single, Surviving Spouse, or Head of Household) | $43,492 | $49,399 | $53,057 | $16,480 |

| Threshold Phaseout $26,260 $26,260 $26,260 $15,290 Amount (Married Filing Jointly) | $20,130 | $20,130 | $20,130 | $15,290 |

| Complete Phaseout Amount (Married Filing Jointly

|

$49,622 | $55,529 | $59,187 | $22,610 |

Excessive Investment Income

For taxable years beginning in 2022, the earned income tax credit is not allowed under § 32(i) if the aggregate amount of certain investment income exceeds $10,300.

Employee Health Insurance Expense of Small Employers

For taxable years beginning in 2022, the dollar amount in effect under § 45R(d)(3)(B) is $28,700. This amount is used under § 45R(c) for limiting the small employer health insurance credit and under § 45R(d)(1)(B) for determining who is an eligible small employer for purposes of the credit.

Exemption Amounts for Alternative Minimum Tax

For taxable years beginning in 2022, the exemption amounts under § 55(d)(1) are:

| Joint Returns or Surviving Spouses | $118,100 |

| Unmarried Individuals (other than Surviving Spouses) | $75,900 |

| Married Individuals Filing Separate Returns | $59,050 |

| Estates and Trusts | $26,500 |

For taxable years beginning in 2022, under § 55(b)(1), the excess taxable income above which the 28% tax rate applies is:

| Married Individuals Filing Separate Returns | $103,050 |

| Joint Returns, Unmarried Individuals (other than surviving spouses), and Estates and Trusts | $206,100 |

For taxable years beginning in 2022, the amounts used under § 55(d)(2) to determine the phaseout of the exemption amounts are:

| Threshold Phaseout Amount | Complete Phaseout Amount | |

| Joint Returns or Surviving Spouses | $1,079,800 | $1,552,200 |

| Unmarried Individuals (other than Surviving Spouses) | $539,900 | $843,500 |

| Married Individuals Filing Separate Returns | $539,900 | $776,100 |

| Estates and Trusts | $88,300 | $194,300 |

Alternative Minimum Tax Exemption for a Child Subject to the “Kiddie Tax”

For taxable years beginning in 2022, for a child to whom the § 1(g) “kiddie tax” applies, the exemption amount under §§ 55(d) and 59(j) for purposes of the alternative minimum tax under § 55 may not exceed the sum of:

(1) the child’s earned income for the taxable year, plus

(2) $8,200.

Certain Expenses of Elementary and Secondary School Teachers

For taxable years beginning in 2022, under § 62(a)(2)(D) the amount of the deduction allowed under § 162 that consists of expenses paid or incurred by an eligible educator in connection with books, supplies (other than nonathletic supplies for courses of instruction in health or physical education), computer equipment (including related software and services) and other equipment, and supplementary materials used by the eligible educator in the classroom is $300.

Standard Deduction

For taxable years beginning in 2022, the standard deduction amounts under § 63(c)(2) are as follows:

| Filing Status | Standard Deduction |

| Married Individuals Filing Joint Returns and Surviving Spouses (§ 1(j)(2)(A)) | $25,900 |

| Heads of Households (§ 1(j)(2)(B)) | $19,400 |

| Unmarried Individuals (other than Surviving Spouses and Heads of Households) (§ 1(j)(2)(C)) | $12,950 |

| Married Individuals Filing Separate Returns (§ 1(j)(2)(D)) | $12,950 |

Dependent

For taxable years beginning in 2022, the standard deduction amount under § 63(c)(5) for an individual who may be claimed as a dependent by another taxpayer cannot exceed the greater of:

Aged or blind

For taxable years beginning in 2022, the additional standard deduction amount under § 63(f) for the aged or the blind is $1,400.

The additional standard deduction amount is increased to $1,750 if the individual is also unmarried and not a surviving spouse.

Cafeteria Plans

For taxable years beginning in 2022, the dollar limitation under § 125(i) on voluntary employee salary reductions for contributions to health flexible spending arrangements is $2,850. If the cafeteria plan permits the carryover of unused amounts, the maximum carryover amount is $570.

Qualified Transportation Fringe Benefit

For taxable years beginning in 2022, the monthly limitation under § 132(f)(2)(A) regarding the aggregate fringe benefit exclusion amount for transportation in a commuter highway vehicle and any transit pass is $280. The monthly limitation under § 132(f)(2)(B) regarding the fringe benefit exclusion amount for qualified parking is $280.

Income from United States Savings Bonds for Taxpayers Who Pay Qualified Higher Education Expenses

For taxable years beginning in 2022, the exclusion under § 135, regarding income from United States savings bonds for taxpayers who pay qualified higher education expenses, begins to phase out for modified adjusted gross income above $128,650 for joint returns and $85,800 for all other returns.

The exclusion is completely phased out for modified adjusted gross income of $158,650 or more for joint returns and $100,800 or more for all other returns.

Adoption Assistance Programs

For taxable years beginning in 2022, under § 137(a)(2), the amount that can be excluded from an employee’s gross income for the adoption of a child with special needs is $14,890. For taxable years beginning in 2022, under § 137(b)(1) the maximum amount that can be excluded from an employee’s gross income for the amounts paid or expenses incurred by an employer for qualified adoption expenses furnished pursuant to an adoption assistance program for adoptions by the employee is $14,890. The amount excludable from an employee’s gross income begins to phase out under § 137(b)(2)(A) for taxpayers with modified adjusted gross income in excess of $223,410 and is completely phased out for taxpayers with modified adjusted gross income of $263,410 or more.

Gross Income Limitation for a Qualifying Relative

For taxable years beginning in 2022, the exemption amount referenced in § 152(d)(1)(B) is $4,400.

Election to Expense Certain Depreciable Assets

For taxable years beginning in 2022, under § 179(b)(1), the aggregate cost of any § 179 property that a taxpayer elects to treat as an expense cannot exceed $1,080,000 and under § 179(b)(5)(A), the cost of any sport utility vehicle that may be taken into account under § 179 cannot exceed $27,000. Under § 179(b)(2), the $1,080,000 limitation under section 179(b)(1) is reduced (but not below zero) by the amount by which the cost of § 179 property placed in service during the 2022 taxable year exceeds $2,700,000.

Qualified Business Income

For taxable years beginning in 2022, the threshold amounts under § 199A(e)(2) and phase-in range amounts under § 199A(b)(3)(B) and § 199A(d)(3)(A) are:

| Filing Status | Threshold Amount | Phase-In Range Amount |

| Married Individuals Filing Joint Returns | $340,100 | $440,100 |

| Married Individuals Filing Separate Returns | $170,050 | $220,050 |

| All Other Returns | $170,050 | $220,050 |

Eligible Long-Term Care Premiums

For taxable years beginning in 2022, the limitations under § 213(d)(10), regarding eligible long-term care premiums includible in the term “medical care,” are as follows:

| Attained Age Before the Close of the Taxable Year | Limitation on Premiums |

| 40 or less | $450 |

| More than 40 but not more than 50 | $850 |

| More than 50 but not more than 60 | $1,690 |

| More than 60 but not more than 70 | $4,510 |

| More than 70 | $5,640 |

Medical Savings Accounts.

- Self-only coverage. For taxable years beginning in 2022, the term “high deductible health plan” as defined in § 220(c)(2)(A) means, for self-only coverage, a health plan that has an annual deductible that is not less than $2,450 and not more than $3,700, and under which the annual out-of-pocket expenses required to be paid (other than for premiums) for covered benefits do not exceed $4,950.

- Family coverage. For taxable years beginning in 2022, the term “high deductible health plan” means, for family coverage, a health plan that has an annual deductible that is not less than $4,950 and not more than $7,400, and under which the annual out-of-pocket expenses required to be paid (other than for premiums) for covered benefits do not exceed $9,050.

Interest on Education Loans

For taxable years beginning in 2022, the $2,500 maximum deduction for interest paid on qualified education loans under § 221 begins to phase out under § 221(b)(2)(B) for taxpayers with modified adjusted gross income in excess of $70,000 ($145,000 for joint returns) and is completely phased out for taxpayers with modified adjusted gross income of $85,000 or more ($175,000 or more for joint returns).

Limitation on Use of Cash Method of Accounting

For taxable years beginning in 2022, a corporation or partnership meets the gross receipts test of § 448(c) for any taxable year if the average annual gross receipts of such entity for the 3-taxable-year period ending with the taxable year which precedes such taxable year does not exceed $27,000,000.

Threshold for Excess Business Loss

or taxable years beginning in 2022, in determining a taxpayer’s excess business loss, the amount under § 461(l)(3)(A)(ii)(II) is $270,000 ($540,000 for joint returns).

Tax Responsibilities of Expatriation

For taxable years beginning in 2022, the amount that would be includible in the gross income of a covered expatriate by reason of § 877A(a)(1) is reduced (but not below zero) by $767,000 pursuant to § 877A(a)(3).

Foreign Earned Income Exclusion

For taxable years beginning in 2022, the foreign earned income exclusion amount under § 911(b)(2)(D)(i) is $112,000.

Unified Credit Against Estate Tax

For an estate of any decedent dying in calendar year 2022, the basic exclusion amount is $12,060,000 for determining the amount of the unified credit against estate tax under § 2010.

Valuation of Qualified Real Property in Decedent’s Gross Estate

For an estate of a decedent dying in calendar year 2022, if the executor elects to use the special use valuation method under § 2032A for qualified real property, the aggregate decrease in the value of qualified real property resulting from electing to use § 2032A for purposes of the estate tax cannot exceed $1,230,000.

Annual Exclusion for Gifts

- For calendar year 2022, the first $16,000 of gifts to any person (other than gifts of future interests in property) are not included in the total amount of taxable gifts under § 2503 made during that year.

- For calendar year 2022, the first $164,000 of gifts to a spouse who is not a citizen of the United States (other than gifts of future interests in property) are not included in the total amount of taxable gifts under §§ 2503 and 2523(i)(2) made during that year.

Notice of Large Gifts Received from Foreign Persons

For taxable years beginning in 2022, § 6039F authorizes the Treasury Department and the Internal Revenue Service to require recipients of gifts from certain foreign persons to report these gifts if the aggregate value of gifts received in the taxable year exceeds $17,339.

Exempt Amount of Wages, Salary, or Other Income

For taxable years beginning in 2022, the dollar amount used to calculate the amount determined under § 6334(d)(4)(B) is $4,400.

Failure to File Partnership Return

In the case of any return required to be filed in 2023, the dollar amount used to determine the amount of the penalty under § 6698(b)(1) is $220.

Failure to File S Corporation Return

In the case of any return required to be filed in 2023, the dollar amount used to determine the amount of the penalty under § 6699(b)(1) is $220.

Revocation or Denial of Passport in Case of Certain Tax Delinquencies

For calendar year 2022, the amount of a serious delinquent tax debt under § 7345 is $55,000.

Attorney Fee Awards

For fees incurred in calendar year 2022, the attorney fee award limitation under § 7430(c)(1)(B)(iii) is $220 per hour.

Qualified Small Employer Health Reimbursement Arrangement

For taxable years beginning in 2022, to qualify as a qualified small employer health reimbursement arrangement under § 9831(d), the arrangement must provide that the total amount of payments and reimbursements for any year cannot exceed $5,450 ($11,050 for family coverage).

Issue 14: Tax Professional Can Order More Transcripts from IRS

Tax professionals are able to order up to 30 Transcript Delivery System (TDS) transcripts per client through the Practitioner Priority Service line. This is an increase from the previous 10 transcripts per client limit.

Through PPS, tax professionals can order a variety of transcripts. Practitioners can receive transcripts for up to five clients per call. There’s no change to the number of clients.

Transcripts available under this newly expanded limit include the:

- Tax Return Transcript,

- Tax Account Transcript,

- Wage and Income Transcript,

- Record of Account and

- Verification of Non-Filing Letter.

Transcripts not listed above continue to be limited to 10 per client and count toward the total of 30 transcripts per client.

Tax professionals will continue to receive TDS transcripts in their e-Services Secure Object Repository mailboxes. The change also applies to other IRS toll-free lines.

Ordering transcripts online

Tax practitioners can continue to order TDS transcripts using the Transcript Delivery System application on IRS.gov. Individual taxpayers can request their own TDS transcripts using Get Transcript. These tools remain the fastest way to receive transcripts.

Issue 15: The Golden Rules of Quality

Greet the Client

Listening

- Prompt

- Coax

- Mirror

- Agree

- Confirm

- Paraphrase

- Recognize feelings

- Praise and Support

Identifying an Issue

- Listen effectively

- Probe

- Restate problem

- Ask open and closed questions

- Who, what, when where and how never why?

- Sequence of events

Solving the Problem

- Understand the problem

- Assure the client

- Refer when necessary

- Give an overview

- Avoid jargon

- Make sure the client understands

Closing the Conversation

- Pause to see if the client understands

- Ask if the explanation is clear

- Explain further, if necessary

- Thank the client.

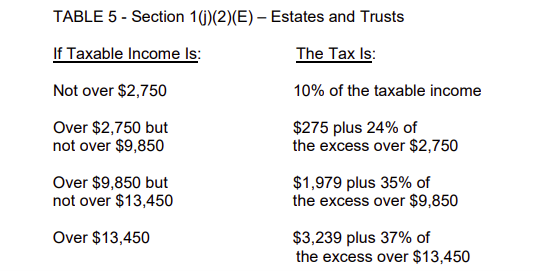

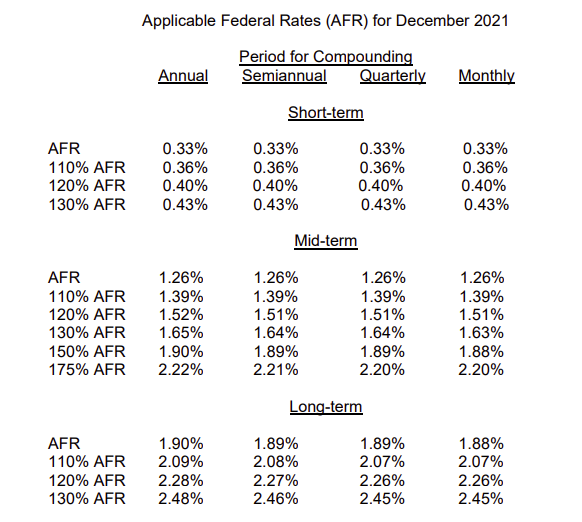

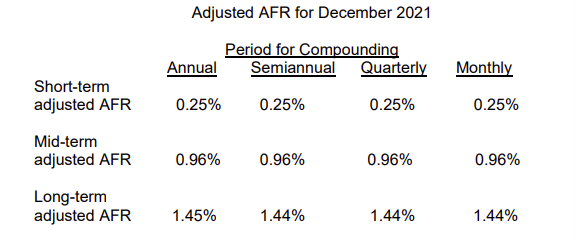

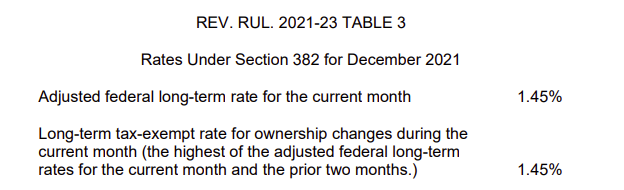

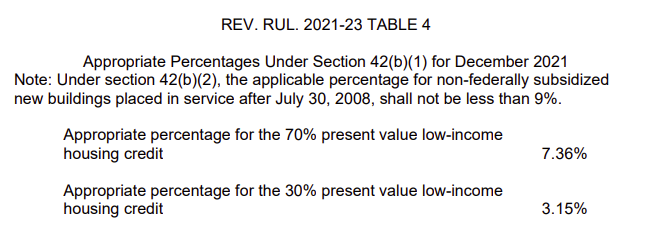

Issue 16: Applicable Federal Rates for December 2021, Rev. Rul. 2021-23

REV. RUL. 2021-23 TABLE 1

REV. RUL. 2021-23 TABLE 2

REV. RUL. 2021-23 TABLE 5

Rate Under Section 7520 for December 2021 4 Applicable federal rate for determining the present value of an annuity, an interest for life or a term of years, or a remainder or reversionary interest 1.6%.