Tax Newsletter: The Fall Virtual Tax Seminars were a success! We summarized all of your Q&A from the 6 sessions below.

We have 5 open sessions left for the Year-End, don’t wait to claim your spot.

Virtual Tax Seminar Information is available here: Year-End Tax Seminars

In This Issue:

Issue 1: Starting October 28, 2021, a New User Fee Applies to Estate Tax Closing Letters

Issue 2: IRS Proposes to Raise Fee for Taking Enrolled Agent’s Exam

Issue 3: IRS Sending Incorrect and Incomplete Recovery Rebate Credit Notices

Issue 4: IRS Releases Draft Form 8379, Injured Spouse Allocation, and Instructions

Issue 5: S Corporation Compensation Issues Raised by TIGTA

Issue 6: IRS Reminds Business Owners to Correctly Identify Workers as Employees or Independent Contractors

Issue 7: Draft 2021 General Business Credit Form Released

Issue 8: Bills from the Hill

Issue 9: Expanded Tax Benefits Help Individuals, Business Give Charity During 2021, Deductions up to $600 Available for Cash Donations by Non-itemizers

Issue 10: IRS Bifurcates Treatment of Instrument as Stock for Certain § 382 Purposes

Issue 11: IRS Publishes Updated 2021 Filing Season Statistics

Issue 12: Fact Sheet Using E-Signatures on Paper IRS Forms

Issue 13: IRS Updates ITIN Application Procedures with FAQ’s

Issue 14: Draft 2022 Form 1099-NEC Issued

Issue 15: PMTA Discusses Penalty for Failure to Deposit Taxes Deferred Under CARES Act

Issue 16: IRS Awards Three New Collection Contracts – IR 2021-191

Issue 17: IRS Issues Correction Notice for 2021 Schedules K-2 and K-3 (Form 1065)

Issue 18: CCA: IRS Can Use Either of Two Forms to Levy Rental Payments

Issue 19: IRS: Drought-stricken Farmers, Ranchers Have More Time to Replace Livestock

Issue 20: Applicable Federal Rates for October 2021, Rev. Rul. 2021-21

Questions and Answers from the Fall 2021 Virtual Seminars

| Do the proposals before Congress any of the provisions have retroactive effective dates? | Currently the proposed legislation is under discussion. It will take some time to go thru all provisions. We have to remember that a mark -up is subject to amendments so until the bill comes to the floor of the house or senate it can be subject to many changes. |

| Would you recommend clients setup IRS accounts so that they can get the EIP and child tax payments? | Yes, an IRS account would be beneficial to all clients.

Taxpayers can securely access and view their IRS tax information anytime through their individual online account. They can see important information when preparing to file their tax return or following up on balances or notices. This includes: Adjusted gross income. This can be useful if the taxpayer is using different tax software or a different tax preparer this year. They may need their AGI so they or their preparer can validate their identity. Additionally, taxpayers can view: · The amount owed for any past years, updated for the current calendar day · Payment history and any scheduled or pending payments · Payment plan details · Digital copies of select notices from the IRS · Tax records using Get Transcript Later in 2021, taxpayers will be able to digitally sign certain authorization forms, such as a power of attorney, initiated by their tax professional. |

| If the EIP payments for a child was sent to one parent and then on the 2020 return the other parent claimed the child would they be eligible to get the EIP for that child | Only one EIP per child is allowed, based on the current information. |

| As tax preparers do, we need to have a§ 7216 for each client so that we can prepare the tax returns? | No, a § 7216 disclosure is not required to prepare a tax return. |

| ENQ is probably why no one else can ever get through to the IRS anymore because it’s always busy now. | IRS staff that answers the phone is extremely “few”. Until IRS funds more customer services dollars to customer service the phone system will not get better. Customer service doesn’t bring in “dollars”, so it is low on the IRS funding pyramid. |

| I am not clear on the difference between a Non-Designated Beneficiary & an Eligible Designated Beneficiary | Under the new Secure Act, a new designation was forms. An eligible designated beneficiary (EDB) is always an individual. In other words, an EDB cannot be a nonperson entity—such as a trust, an estate, or a charity; these are considered not designated beneficiaries.

There are five categories of individuals included in the EDB classification: The owner’s surviving spouse. The owner’s child who is less than 18 years of age. A disabled individual. A chronically ill individual. Any other individual who is not more than 10 years younger than the deceased IRA owner. A nonperson entity is classified as a “not designated beneficiary.” |

| Meals: purchasing snack items for the employee lounge is only deductible at 50%? | Correct. |

| I prepared a 941X for the ERC on 1/29/21 followed up with IRS in June and they stated it is being processed. Is this how long everyone’s has been taking.? | Most general processing was taking 6-8 months, but as of August many 4th quarter Form 941 for 2019 were not yet processed. I currently do not have a handle on processing of amended Form 941, but I do know they will not be processes until the original return has been processes. IRS priority in January 2021 was 1040’s and they were not back to full processing staff. We will continue to have many processing delays in the future. |

| How does IRS calculate how much each taxpayer reports as stimulus received when they go from MFJ to MFS and there are dependents involved and they didn’t get the whole amount because the income level was over the $150,000? | IRS has not provided any guidance on this particular issue – which I think is more prevalent that many believe. If they were over the income level, they should not have received anything. |

| Setting up an IRS account: Is that only to receive information from the IRS or can you also send the IRS info or ask the IRS questions through this online portal? | This IRS account is only for individual clients to receive their tax information. |

| Do both taxpayer and spouse need to sign the consent to disclose information? | Yes, both must sign. |

| An employee died in June of 2021. This employee did not have a spouse, but had a domestic partner. There was no designation of beneficiary form completed. Are the children of the deceased eligible DB’s (10 yrs.) or non-designated(5yrs)? beneficiaries? | First, without a designated beneficiary the surviving spouse or children must follow state law.

Under the new Secure Act – if determined by state law they would be the beneficiary the 10-year rule would apply. |

| Since clients constantly request, usually verbally, to give or send tax returns to banks for loan, PPP purposes, or other reasons, are we to insist and/or require that they actually personally pick these tax returns up and sign for them? | Yes, or have them come into the office and sign a § 7216 Disclosure Form. |

| If the PPP loan was for $250,000 for example of which only 60% was needed for forgiveness, does the remaining 40% of the $250,000 loan that was forgiven count as payroll expenses against the ERC calculation even though only 60% was needed. | Yes, if the full amount of the loan was used for payroll. |

| If we put the clients returns in our portal for them when it is complete – can they just use the pdf without sending us a letter? | Many have a secure portal for clients who cannot personally sign and identity verification for e-signing is part of the portal. No § 7216 disclosure document is needed. |

| In regard to the child tax credit what is the difference between the $150,000 phase out and the $120,000 safe harbor phase out? | First there are two phase-outs that impact the amount of Child Tax Credit a client can receive.

The original phase-outs of $200,000 for all clients unless married filing jointly then the amount of $400,000. This phase-out was law as it related to the $2,000 Child Tax Credit. In 2021 an additional phase-out applies based on the new amounts of Child Tax Credit available. The Child Tax Credit begins to be reduced to $2,000 per child if your modified AGI in 2021 exceeds: $150,000 if married and filing a joint return or if filing as a qualifying widow or widower; $112,500 if filing as head of household; or $75,000 if you are a single filer or are married and filing a separate return. The first phaseout reduces the Child Tax Credit by $50 for each $1,000 (or fraction thereof) by which your modified AGI exceeds the income threshold described above that is applicable to you. Pay Back Provision The new law implemented a “pay back” provision for the 2021. The client will not qualify for any repayment protection if the modified AGI is at or above the amounts listed below based on the filing status on the 2021 tax return. $120,000 if you are married and filing a joint return or if filing as a qualifying widow or widower; $100,000 if you are filing as head of household; and $80,000 if you are a single filer or are married and filing a separate return. The client will qualify for full repayment protection and will not need to repay any excess amount if the main home was in the United States for more than half of 2021 and their modified adjusted gross income (AGI) for 2021 is at or below the following amount based on the filing status on your 2021 tax return: $60,000 if you are married and filing a joint return or if filing as a qualifying widow or widower; $50,000 if you are filing as head of household; and $40,000 if you are a single filer or are married and filing a separate return. The repayment protection may be limited if the modified AGI exceeds these amounts, or the main home was not in the United States for more than half of 2021.

|

| Can you back up on that 6% penalty? I am thinking about rolling my Simple to my IRA. I will be 72 next year | Any amount contributed to a SIMPLE IRA above the maximum limit is considered an “excess contribution.” An excess contribution is subject to an excise tax of 6% for each year it remains in the SIMPLE IRA. An excess contribution may be corrected without paying a 6% penalty.

Rolling the Simple IRA into a traditional IRA will not trigger the 6% penalty. |

| Can you elaborate on the § 7216 requirements if we are using a Foreign 3rd party vendor to assist with preparation? | Furnishing tax return information to tax return preparers located outside the United States. If a client initially furnishes tax return information to a tax professional located outside of the United States or any territory or possession of the United States, an officer, employee, or member of a tax professional may use tax return information, or disclose any tax return information to another officer, employee, or member of the same tax professional, for the purpose of performing services that assist in the preparation of, or assist in providing auxiliary services in connection with the preparation of, the tax return of a client by or for whom the information was furnished without the client’s consent under §301.7216-3.

BUT: Tax professionals located within the same firm in the United States. If a client furnishes tax return information to a tax professional located within the United States, including any territory or possession of the United States, an officer, employee, or member of the tax professional firm may use the tax return information, or disclose the tax return information to another officer, employee, or member of the same tax professional firm, for the purpose of performing services that assist in the preparation of, or assist in providing auxiliary services in connection with the preparation of, the client’s tax return. If an officer, employee, or member to whom the tax return information is to be disclosed is located outside of the United States or any territory or possession of the United States, the client’s ‘s consent under §301.7216-3 prior to any disclosure is required. |

| If a client is in your office and requests you to email them a PDF copy of the return, do you still need to have written consent? | I would never e-mail a tax return. Unsafe. But no disclosure is needed as no third-party is involved. |

| If a client brings a flash drive, could we upload electronic copies instead of or in addition to providing hardcopies without additional disclosure forms. | I see no disclosure issue with this, but a jump drive is not a secure method, and may become corrupted in the future. |

| The institution is still required to tell each person what the RMD will be, correct? | Yes, but in my experience many people do not read the information or always understand the requirements. This is a good conversation to have with your clients once they reach a certain age. |

| Is a scam deductible as a personal bad debt? | Under old law that would be a casualty/theft loss, but now the loss has to be in a federally declared disaster area and I assume that they are not in an area. It would never be a bad debt. The way the law is currently, there is no provision to allow a deduction of theft. |

| You mentioned PPP interest. Did you say it was deductible when the loan is forgiven? | If the loan is forgiven so, is the interest. If for some reason they have to pay back all or part, then it would be business interest.

We stated in the webinar that interest was still deducible as a business expense, But IRS has not provided guidance on the issue AND they are mixed opinions on this issue currently. I would proceed with caution until IRS addresses the issue fully. |

| If tuition is paid to a private college by the grandparents, can they get charitable contribution deduction? | The charitable contribution needs to be used without condition, so paying for tuition thru a charitable contribution will not qualify. |

| Question on Not More than 10 years younger as it applies to the new rules under the Secure Act, this can be a non-related person, such as a partner, boyfriend, girlfriend, etc. | Yes |

| Are wages paid to an owner of an LLC taxed as an S- Corporation or S-Corporation eligible for the ERC? | IRS issued Notice 2021-49 on August 4, 2021 which states that the Employee Retention Credit (ERC), made available for businesses suffering from the COVID-19 crisis, will not be available with respect to wages paid to a majority owner, or such owner’s spouse, if the majority owner has a brother or sister (whether by whole or half-blood), ancestor, or lineal descendant.

In the event that the majority owner of a corporation has no brother or sister (whether by whole or half-blood), ancestor, or lineal descendant, then wages paid to a majority owner and such owner’s spouse will qualify for the Employee Retention Credit. |

| To qualify for the first quarter of 2021, you can compare 4th quarter 2020 vs. 2019. Are we looking for a drop of only 20% when comparing the 4th quarter of 2020 vs. 2019? | For 2021

Fully or partially suspends operations due to a governmental order limiting commerce, travel, or group meetings due to COVID-19 (employer is eligible to claim ERC for the suspension period), or Has gross receipts for any quarter or for the immediately preceding quarter that are less than 80% of its gross receipts for the same quarter in 2019. |

| For ERC Income … income is considered all receipts, correct? | Revenue Procedure 2021-33 provides a safe harbor permitting employers to exclude certain amounts from gross receipts solely for determining eligibility for the ERC. These amounts are:

The amount of the forgiveness of a Paycheck Protection Program (PPP) Loan; Shuttered Venue Operators Grants under the Economic Aid to Hard-Hit Small Businesses, Non-Profits, and Venues Act; and Restaurant Revitalization Grants under the American Rescue Plan Act of 2021. An employer elects to apply the safe harbor by excluding these amounts solely for determining whether it is an eligible employer for a calendar quarter for purposes of claiming the ERC on its employment tax return. Revenue Procedure 2021-33 requires employers to apply the safe harbor consistently for determining eligibility for the ERC. The employer must exclude the amounts from their gross receipts for each calendar quarter in which gross receipts are relevant to determining eligibility to claim the ERC. The employer claiming the credit must also apply the safe harbor to all employers treated as a single employer under the aggregation rules. An employer is not required to apply this safe harbor, and the safe harbor does not permit the exclusion of these amounts from gross receipts for any other federal tax purpose. |

| So, if Q1-2019 revenues were $100 and in Q1 -2021 revenue was $78 the taxpayer would qualify for ERC….correct? | Trade or business experiencing:

● A full or partial shutdown; or ● Significant decline in gross receipts, which means a 50% decline in gross receipts from same calendar quarter in 2019 and continues through end of first quarter for which business’s gross receipts are greater than 80% of comparable 2019 calendar quarter. In your example there is not a 50% reduction in gross receipts. This rule applies to the 2020 tax year. |

| A question about aggregate. If 3 companies qualify for ERC as a group with Company A revenues falling, and Company B and C revenues not falling, do all 3 companies receive ERC? | the aggregation rules are very complex, I did find this though. The amount of the Employee Retention Credit must be apportioned among members of the aggregated group on the basis of each member’s proportionate share of the qualified wages giving rise to the credit. This would imply that not all three would get the credit. https://www.twrblog.com/2020/04/irs-faqs-on-retention-credit-highlight-aggregation-concerns-and-narrow-potential-eligibility/ |

| If you use the alternative method for qualifying in 2021 for ERC, is there somewhere on the 941X where you mark that you are using an alternative method? | None that I know of – if audited just substantiate how you came up with the figures. |

| So, what are the final rules on Excess Business Loss for 2021? | It goes back the TCJA and fully applicable in 2021. |

| Annual Dollar Limit on Loss Deductions Married taxpayers filing jointly may deduct no more than $500,000 per year in total business losses. Individual taxpayers may deduct no more than $250,000. Unused losses may be deducted in any number of future years as part of the taxpayer’s net operating loss carryforward. |

The rules were suspended in 2018-2020 but for 2021 they are active. |

| If the Eligible Designated Beneficiary is the surviving spouse, under the new rules, the spouse has only 10 years to distribute her inherited IRA? | No, the spouse is exempt from the 10-year rule, they are allowed to use the life expectancy tables. |

| If an employer provides lunch to their employees at the employer’s facility by ordering in from a restaurant, is it 100% or 50% deductible? | Watch out for the “fringe benefit” rules. An occasional “lunch” would be 100% since it was from a restaurant. If this is a regular event the deductibility may come into question. |

| § 1398(d)(2) bankruptcy short year election. Do you have example of election that has to be attached or does writing “Section 1398 Election” at top of 1040 suffice? | To avoid delays in processing the short year return, write “Section 1398 Election” at the top of the return. The statement must say that you chose under IRC section 1398(d)(2) to close the debtor’s tax year on the day before the filing of the bankruptcy case. You may also make the election by attaching a statement to IRS Form 4868 – Application for Automatic Extension of Time to File. File Form 4868 by the due date of the return for the first short tax year. |

| If you have a pizza delivered from Casey’s, is it 50% or 100%? | Casey’s is not a restaurant – therefore 50% deductible. |

| If you are already a Register Tax Return Preparer, would you need to take the test every year under the proposed law to regulate tax preparers? | We will have to await any new guidance if they pass new regulations requiring a license. |

| Where should we report the 1099-K if not Self-employment or if under $600? show as other income? | We are awaiting guidance on this. However, there was an old rule that you reported as a Short-Term Capital Transaction with no Loss Allowed |

| Can I show 1099-K income as Misc. income? | All depends on the reason why you received. What was the source of income from 1099-K? |

| What about the employee expenses? We now have more individuals working at home. Is there anything in the bill Congress is considering? f | Nothing specific that I have read. Remember 2026 gets us the employee business expenses back but nothing new. And working from home needs to be for the convenience of the employer. In most cases the employer convenience issue would not apply, due to COVID. |

| Does basis in a nondeductible IRA transfer to beneficiary? | Yes, the nondeductible basis transfers to Beneficiary. |

| Is that basis kept separate from beneficiary’s own basis in nondeductible? | Since the IRA will be listed as rollover, must be separate. |

| How is per diem affected by the 100% meal rules for 2021 and 2022? | Using per diem would be 50% as it would not qualify under the definition of a “restaurant”. |

| How do you get a CAF number? You need one to set up a Tax Pro account. | File your first POA the old fashion way and one will be assigned. |

| Can you send a pdf file to the client if you have a secured email? | If the email system is a secured file share system. I use Verifyle.com |

| Does a new business that is formed after 2/15/20 that buys a business that was operating before 2/15/20 and none of the owners of the business acquired have ownership or even work with the newly formed business qualify for the employee retention credit? | If you purchased an existing business that was open on or before 2/15/2020 your business is NOT a startup business and would qualify under the other ERC rules. As a Recovery Startup Business, here is what you need to qualify for the ERC:You must have 1 or more employees.You must be a startup company and started operations on or after 2/15/2020.Note: If you purchased an existing business that was open on or before 2/15/2020 your business is NOT a startup business and would qualify under the other ERC rules.You must have gross receipts under $1 million dollars for 2020 and 2021 eachIf you own multiple companies or have common ownership, you will need to speak to an accountant as the requirements differ and are beyond the scope of this blog. (In short: certain businesses with common ownership are grouped together through what the IRS calls “attribution rules.”)You must not be eligible for ERC under the other requirements, i.e., a significant decline in gross receipts or subject to governmental imposed orders/restrictions.You will be paying employees during Q3 and Q4 of 2021. There are essentially zero stipulations to qualify for the ERC under these new rules for new businesses, as long as you opened doors on or after 02/15/2020 and make less than $1M in revenue. Please review the October Newsletter located at the CPEhours.com website under Blog. https://www.cpehours.com/tax-newsletter-october-2021/ The question has been more fully addressed. |

| Is that full time or using the “Full Time Equivalents” calculation? | For the purposes of the employee retention credit, a full-time employee is defined as one that in any calendar month in 2019 worked at least 30 hours per week or 130 hours in a month (this is the monthly equivalent of 30 hours per week), and the definition based on the employer shared responsibility provision in the ACA.

Employers who were in business the entire calendar year in 2019 or 2020 would take the sum of the number of full-time employees in each calendar month and divide by 12. An employer who started a business during 2019 or 2020 determines the number of full-time employees by taking the sum of the number of full-time employees in each full calendar month in 2019 or 2020 in which the business operated and divide by that number of months. An employer who started a business in 2021 determines the number of full-time employees by taking the sum of the number of full-time employees in each full calendar month in 2021 that the business operated and divides by that number of months. |

| Will this have any effect on “Field” meals done by farmer’s especially during planting and harvest? | Meals would be 50% deductible. |

| Have we heard if the Treasury Dept is going to either set up an IRS Look-up page for the advances? | Client should receive letter. However, as of now, no IRS Look up page. It will be on transcripts; however, you would need POA or Form 8821 approval to look at transcripts |

| Are restaurant revitalization grants taxable? | Grants will not be included as federal taxable gross income by the IRS.

Will entities be able to deduct federal tax expenses paid with RRFG funds? Yes, the law states that “no deduction shall be denied, no tax attribute shall be reduced, and no basis increase shall be denied, by reason of the exclusion from gross income.” See § 9673 of ARP Act of 2021. Grant money MUST be used for eligible expenses incurred between 02/15/2020 and 03/11/2023. If entity cannot use all grant funds or permanently ceases operations on or before 03/11/2023, the entity must return the unused funds to the Department of Treasury |

| Can you give the website for the EnQue service? | www.calleng.com |

| Is Form 7203 part of form 1040 then? | It is an attachment to the Form 1040. |

| What if they were laid off for 3 weeks, but withdrew $90,000. Didn’t seem like they needed this much for a 3-week shut down | The law made no stipulation concerning the amounts to be withdrawn based on need. Only the maximum amount could not exceed $100,000. |

| Truckers who take per diem for meals – is that 100% and does that need to be divided between 100% and 80%? | Truckers that are employees is N/A. However, Truckers that are self-employed will maintain their deduction at 80% NOT 100%. |

| I tell my clients I am not an expert in retirement plans and they should consult with the administrator of the plan when it comes to these questions. I have a general understanding but the administrator should know the specifics of their plan. | That is the best way approach. BUT I would annually remind them of their required minimum distribution if they are of the age. |

| Secure Act: How old can an eligible beneficiary child be? I thought I read they can be in their 20’s if still in college? | Legal age of majority, which is 18 or 21 depending on State law. We should have regulations by the end of the year on this definition of eligible beneficiary child. It should be defined based on what state law provides for age majority of a child. |

| In an analysis of the Secure Act by the National Law Institute written by Harvard Lawyer, Steven Siegel; after he states a minor child of the plan participant based on the definition of minor in the persons state of domicile, as Michael stated…Siegal goes on to state: “A student who has not completed a specified course of education and is under the age 26 is considered a minor child”. I can’t find that anywhere else and that is relevant in my practice for many of my clients. | I have not seen this any analysis that I have researched. Interesting point. I will look to see if I can find anything |

| I just researched the “minor” eligible designated beneficiary again while on break.

I just found: an article which references in Treasury Regulation § 1.401(a)(9)-6,Q&A-15, which supports a minor age 26 who has not completed a specified course of education and is under the age of 26. Although the Treasury Regulation stated immediately above applies to minors under a defined benefit or annuity contract; the article goes on to state that this Treasury Regulation appears to now apply to inherited IRAs and other defined contribution plans, regardless of the state age of majority. The detailed article can be found at: Kites.com/blog/secure-act-it’s-401k-elimination-eligible-designated-beneficiary-retirement-accounts-taxes/ |

It will be interesting to see what the regulations say on this matter. I can tell you that I doubt that the Treasury is going to permit a child at age 10 be allowed to made RMD until age 26 when it can set the 10-year period to start when the individual reaches age 18 or 21. With the pressure to raise taxes, I can’t see it; but I’ve been wrong before. |

| Kristy, can you tell me what form a client would need to send to get the refund for their deceased parent. I did the return and that evening the person passed away. Even though the persons account has remained open the IRS has not sent the refund that was due. | Form 1310 |

| Can truckers use per diem or is that solely for employers. | Truckers can use per diem and would use the 80% limitation. |

| Is that only college tuition or does private grade or high school qualify? | Under 529 Plan arrangement K-12 expense will qualify and part of the $15K per year including the 5 year per-fund limit of $75K (i.e., put 5 years’ worth of gifting in one year).

Follow up point Stacy – the annual $10K expense limit is available to “private” K through 12 grades under the TCJA |

| At some point can you address how a self-employed taxpayer that deferred 1/2 of their self-employment tax in 2019 pays that back (half by December 31, 2021). Is there a tax form that goes with this payment? Where does the check get sent? | How individuals can repay the deferred taxes

Individuals can pay the deferred amount any time on or before the due date. They: Can make payments through the Electronic Federal Tax Payment System or by credit or debit card, money order or with a check. Should be separate payments from other tax payments to ensure they are applied to the deferred tax balance on the tax year 2020 Form 1040 since IRS systems won’t recognize the payment for deferred tax if it is with other tax payments or paid with the current Form 1040. Should designate the payment as “deferred Social Security tax.” Individuals making deferred Social Security tax payments in EFTPS should select 1040 US Individual Income Tax Returns and deferred Social Security tax for the type of payment. They must apply the payment to the 2020 tax year where they deferred the payment. Taxpayers can visit EFTPS.gov for details. Those using Direct Pay should select the reason for payment “balance due.” If they are using the Card Program to pay with a debit or credit card, they should select “installment agreement.” They should apply the payment to the 2020 tax year where the payment was deferred. |

| Should we presume, that Congress will continue to enact tax legislation during tax season, retroactive to the previous year (and thus affecting returns already completed or in process)? | According to the House Ways & Means Mark Up on 09/13/2021, the capital gain tax rate takes effect on September 13, 2021. Other provisions have effective dates on the date of enactment and other provisions are effective 1/1/2022 (i.e., income tax rate of 39.6%). We’ll just have to wait and see what happens. |

| If PPP forgiveness application included more wages than the amount of the loan can the excess over the forgiveness amount be used for ERC since there was no benefit from the excess wages? | Yes, the excess wages must be used for ERC.

Notice 2021-20. Q: If I reported more wages on my PPP forgiveness application than was necessary to reach 100% forgiveness of the loan, can I use those excess wages to claim the Employee Retention Credit? A: Yes. The IRS allows excess wages reported on a PPP loan forgiveness application to qualify for the ERC. In general, wages that make up the PPP’s 60% payroll requirement aren’t eligible for the ERC. Wages that exceed the 60% payroll requirement may be eligible for the ERC, but some analysis is required. Wages that aren’t included in your PPP loan amount are eligible for this credit if they meet the definition of qualified wages. For example, compensation paid to employees that exceeds $100,000 annually isn’t an eligible PPP payroll cost. But it could qualify for the ERC. |

| The material says the ERC is not available to those receiving the WOTC. Does this apply in the reverse? Due to increased hiring of unemployed individuals, we were evaluating sending out WOTC information to our clients. Any thoughts? | ERC is not available if the WOTC is claimed. |

| Does the text offer any definition of Emergency Rental Assistance, and what qualifies and how do you get it? | The text information is based on a new release. More information can be found at: https://home.treasury.gov/policy-issues/coronavirus/assistance-for-state-local-and-tribal-governments/emergency-rental-assistance-program |

| This question is probably not relevant to the entire group, but in the long list of clients still waiting on their refund, I have one that recently called me to say that he received his refund, but it came in two installments about a month apart. The two deposits he received added up to about what the refund should be plus a little interest. Is this possible? | It is possible? It so hard these days, because adequate documentation of the refund computation and circumstances no longer exists when the refunds are issued.

Part may have been income tax withheld and the other a credit applies for that needed to be verified by income. |

| If income is out of the phase out, will you have to pay back any of the 3rd stimulus payment? | No |

| I have a client that was talked into a C Corporation 3 years ago, they took out distributions and didn’t pay a wage…so they have like $90,000 income at the C rate and $90,000 of dividends.

Can I reclassify those as wages and file 941 returns??? |

You can always reclassify, but be aware of penalties and interest that may be incurred. |

| If 2021 income is too high for EIC, can an individual look back to 2019 for lower income? | For Tax Year 2020, if the client earned less in 2020 than in 2019, they can “lookback” to use the 2019 income or use the 2020 income when claiming the EITC or ACTC on their taxes. |

| How does the death payment from Government of Covid funeral affect the 1040 and 1041’s. | We do not have any guidance on this issue that I can find.

If it follows other FEMA guidelines in a qualified disaster where funeral payments are provided, they are considered non-taxable. Guidance would be nice to have on this issue. |

| Is the IRS way behind on processing 1139 Forms? | As of May 25, 2021 according to the IRS – Status of filed Forms 1139 and Forms 1045.

The IRS cannot currently provide a timeframe for processing Forms 1139, Corporation Application for Tentative Refund, and Forms 1045, Application for Tentative Refund (used by individuals, estates, and trusts). Submissions are processed in the order in which they are received. The IRS merely suggests that you consider the possibility of significant additional approval time and plan for it. Do not submit duplicate claims as that will only cause more delays. |

| With no RMD in 2020, how does this affect RMD calculation in future years? | The same calculation will be done as in prior years. |

| What is the phone number of the Taxpayer Advocate? | Try this link https://www.taxpayeradvocate.irs.gov/ Contact information is part of this website. |

| Will IRS send a 1099 for the advance payments? | No |

| When determining eligibility for ERC (i.e., % decline in gross receipts). Do you have to use the same method of accounting as you use for income tax (i.e., cash vs. accrual) or can you use whichever method works to show you had the greater decline? | Given the fact that this is tax provision I believe you would have to use the method of accounting that you use for income tax purposes to determine ERC qualification.

Follow up response from the SBA: For PPP, the SBA states that the gross receipts are determined in accordance with the entity’s accounting method. ERC uses the employer’s method of accounting, following the § 448 rules for other than tax-exempt organizations and § 6033 rules for tax-exempt organizations. |

| What if you have a client who claimed one child in 2020, only by the gift of the ex-wife, and then died before he received his refund from the federal government. The IRS sent a letter to his parents saying that he was deceased so no refund would be coming. Can the ex-wife then amend her return to claim all three children rather than the two she originally claimed? | Yes. Especially if she was custodial parent. |

| The deferral is due 12/31/2021 and 12/31/2022, are you saying that for Sch C deferrals, we can wait until we prepare the 2021 return after 12/31/2021? | No, deferral payments are due on 12/21/21 and 12/31`/22. |

| Assume estate exemption goes to 6M. If husband dies in 2021 with 3M estate, files 706 for portability the wife will get 9M to add to her 6M when she dies? | That would be true as long as the law changes to accommodate those figures and portability rules do not change. |

| Did AJ say the Deferred payroll tax could repaid with 1040 for 2021? | AJ and I want to clarify the Social Security tax (self-employed) that the first installment is due 12/31/2021 and the second installment is due 12/31/2022. |

| Will the IRS provide an App to determine how much advanced child tax credit was received by clients? | The taxpayers should receive letter similar to EIP Payments. |

| Did you say wages paid to spouse are eligible for PPP computation in a sole proprietorship?

Page 28, paragraph (4) seems to refer to stockholders. There is no stock involved and this is for PPP not ERC. |

Review Notice 2021-49, page 27, paragraph (h) concerning spouses’ wages.

We believe these deals with married individuals that are not filing MFJ. But note on page 28 the discussion on item (4) as to what is a family. The spouse is treated as a family member. That is true. However, under the attribution rules, the spouse will be deemed to own the husband stock and therefore be precluded from having her wages eligible for the ERC, because she is deemed to be a majority owner. The rules still apply to Schedule C or Schedule F. |

| Is the Paid Sick Leave paid by 09/30 or hours worked by 09/30 but paid after 10/01/21? | It appears according to IRS FAQ #32 on the Paid Sick Leave Required is says “… the ARP “reset” the maximum amount of paid sick leave for which an Eligible Employer could claim tax credits for qualified leave wages paid with respect to leave taken by employees beginning on April 1, 2021, through September 30, 2021” Therefore, it appears that is applied to wages payments made for qualified leave during the 4/1/2021 through 9/30/2021, regardless of when paid. |

| Is RTRP coming back for those of us who have kept up on own CE’s? | It appears that with the IRS 80B funding that Congress has allocated in the 9/13/2021 HW&M tax bill, there may be provisions that further the rules and regulations for RTRP. |

| If you are using ERC for wages, then what are you using the PPP loan for? | I believe you need to determine certain portion of your wages that need to apply to the PPP loan and then use the rest of your PPP loan for overhead rent, mortgage, etc. You need this in order to have your PPP loan forgiven. Then any wages that did not use toward the PPP loan forgiveness can to applied to the ERC. |

| Did the partial above the line charitable contributions change in 2021? | The charitable deduction for 2021 is an above the line deduction taken into account. For 2021 it is $300.00 for all except for a MFJ status where it is $600.00/ $300.00 for each couple. |

| Do you expect changes to the defined benefit plans for retirement, currently set at 25% of gross income? | We expect significant changes. At this point unsure what the changes will be. |

| How can we file electronically when the client has children without a Social Security Number? | You are not able to file electronically if the client does not have social security numbers. |

| If a client emails you to request you send the documents to a third party (as in a house refinance), can you use the email as the official/formal written approval from the client? | I would never use email as information is not safe. |

Issue 1: Starting October 28, 2021, a New User Fee Applies to Estate Tax Closing Letters

Starting Oct. 28, 2021, a new $67 user fee will apply to any estate that requests a closing letter for its federal estate tax return. The IRS also continues to remind executors about the availability of the free transcript option. The new user fee was authorized under final regulations, TD 9957. Closing letter requests must be made using Pay.gov. The IRS will provide further procedural details before the user fee goes into effect.

Issue 2: IRS Proposes to Raise Fee for Taking Enrolled Agent’s Exam

The IRS has released proposed regs that would increase the current $81 per part fee for taking the enrolled agent’s exam to $99 per part. The fee paid to the testing service (Prometric) would remain $104 per part until May 2023.

The proposed regulation would apply to registrations for the enrolled agent special enrollment examination that occur on or after 30 days after publication of the final rule in the Federal Register.

Issue 3: IRS Sending Incorrect and Incomplete Recovery Rebate Credit Notices

The IRS is sending taxpayers Letter 6470 notifying them of “errors” in the Recovery Rebate Credit claimed on their 2020 income tax return. The letters are vague and confusing for a few reasons:

- Letter 6470 is supposed to be a follow-up to Notice CP11, CP12, or CP13, but many taxpayers never received the first notice.

- The letters do not state the actual dollar amount changed on the return, nor the reason for the change.

- Many taxpayers already received their full refunds, as reported on their income tax returns, including the claimed Recovery Rebate Credit and

- Many of the letters appear to be incorrect.

Officially, Letter 6470 is a math error notice, which means that a taxpayer has 60 days to notify the IRS that they disagree with the letter. Help your clients who received these notices set up an online account at www.irs.gov to verify the Economic Impact payments they received, and compare to the amounts reported on the taxpayers’ returns. If the Letter 6470 was issued incorrectly, contact the IRS at the number on the notice or respond by mail within 60 days.

To help taxpayers access or set up their online account, go to: www.irs.gov/payments/view-your-tax-account

Issue 4: IRS Releases Draft Form 8379, Injured Spouse Allocation, and Instructions

The IRS has released a draft Form 8379, Injured Spouse Allocation, and draft instructions.

An injured spouse is a married individual who filed a joint return and all or part of their portion of a tax overpayment was (or is expected to be) applied (offset) to their spouse’s legally enforceable past-due federal tax, state income tax, state unemployment compensation debt, child support, or a federal nontax debt, such as a student loan.

Injured spouse relief allows an injured spouse to get their share of a joint refund that would otherwise be used to pay a legally enforceable past-due debt of their spouse. To claim injured spouse relief, the injured spouse:

- Files Form 8379 with their jointly filed tax return when that return has a joint overpayment which will (or is expected to be) used to offset a past-due debt of their spouse.

A new draft of Form 8379 has two lines for taxpayers to separate their nonrefundable and refundable credits. The ability to report the credits separately was created by repurposing Lines 16 and 17. Draft line 16 is repurposed for reporting nonrefundable credits. Draft line 17 will now be used for reporting refundable credits, instead of all credits.

Issue 5: S Corporation Compensation Issues Raised by TIGTA

On August 11, 2021, Treasury Inspector General for Tax Administration (TIGTA) issued a report on the compliance of S corporation shareholders paying themselves an equitable wage.

The issue of S corporations not paying salaries to officers and avoiding employment taxes has been reported for many years. IRS revenue agents have the opportunity to assess the issue when examining Forms 1120-S, U.S. Income Tax Return for an S corporation, in the field; addressing the issue more directly by examining it in the IRS’s Employment Tax function; or through Compliance Initiative Projects. The IRS is selecting less than 1 % of all S corporations for examination.

When the IRS does examine S corporations, nearly half of the revenue agents do not evaluate officer’s compensation during the examination even when single-shareholder owners may not have reported officer’s compensation and may have taken tax-free distributions in lieu of compensation.

TIGTA’s analysis of all S corporation returns received between Processing Years 2016 through 2018 identified 266,095 returns with profits greater than $100,000, a single shareholder, and no officer’s compensation claimed that were not selected for a field examination. The analysis found that the single-shareholder owners had profits of $108 billion and took $69 billion in the form of a distribution, without reporting they received officer’s compensation for which they would have to pay Social Security and Medicare tax. TIGTA estimated 266,095 returns may not have reported nearly $25 billion in compensation and may have avoided paying approximately $3.3 billion in Federal Insurance Contributions Act tax.

Finally, TIGTA identified 151 S corporations with nonresident alien shareholders. S corporations are not permitted to have nonresident aliens as shareholders. If the IRS had identified these 151 S corporations and their 424 returns, it may have converted them to C corporations and assessed $5 million in corporate income taxes.

Issue 6: IRS Reminds Business Owners to Correctly Identify Workers as Employees or Independent Contractors

An employee is generally considered to be anyone who performs services, if the business can control what will be done and how it will be done. What matters is that the business has the right to control the details of how the worker’s services are performed. Independent contractors are normally people in an independent trade, business or profession in which they offer their services to the public. Doctors, dentists, veterinarians, lawyers, accountants, contractors, subcontractors, public stenographers or auctioneers are generally independent contractors.

Whether a worker is an independent contractor or an employee depends on the relationship between the worker and the business. Generally, there are three categories to examine:

- Behavioral Control − does the company control or have the right to control what the worker does and how the worker does the job?

- Financial Control − does the business direct or control the financial and business aspects of the worker’s job. Are the business aspects of the worker’s job controlled by the payer? (Things like how the worker is paid, are expenses reimbursed, who provides tools/supplies, etc.)

- Relationship of the Parties − are there written contracts or employee type benefits (i.e., pension plan, insurance, vacation pay, etc.)? Will the relationship continue and is the work performed a key aspect of the business?

Misclassified worker

Misclassifying workers as independent contractors adversely affects employees because the employer’s share of taxes is not paid, and the employee’s share is not withheld. If a business misclassified an employee without a reasonable basis, it could be held liable for employment taxes for that worker. Generally, an employer must withhold and pay income taxes, Social Security and Medicare taxes, as well as unemployment taxes. Workers who believe they have been improperly classified as independent contractors can use IRS Form 8919, Uncollected Social Security and Medicare Tax on Wages to figure and report their share of uncollected Social Security and Medicare taxes due on their compensation.

Voluntary Classification Settlement Program

The Voluntary Classification Settlement Program (VCSP) is an optional program that provides taxpayers with an opportunity to reclassify their workers as employees for future tax periods for employment tax purposes with partial relief from federal employment taxes for eligible taxpayers that agree to prospectively treat their workers (or a class or group of workers) as employees. Taxpayers must meet certain eligibility requirements, apply by filing Form 8952, Application for Voluntary Classification Settlement Program, and enter into a closing agreement with the IRS.

Who is self-employed?

Generally, someone is self-employed if any of the following apply to them:

- They carry on a trade or business as a sole proprietor or an independent contractor.

- They are a member of a partnership that carries on a trade or business.

- They are otherwise in business for themselves (including a part-time business).

Self-employed individuals generally are required to file an annual tax return and pay estimated tax quarterly. They generally must pay self-employment tax (Social Security and Medicare tax) as well as income tax. Self-employed taxpayers may be able to claim the home office deduction if they use part of a home for business.

Issue 7: Draft 2021 General Business Credit Form Released

The IRS has issued a draft of Form 3800, General Business Credit, for use for tax year 2021.

The draft has three changes from the 2020 form.

The draft of line 7 of Part II (Allowable Credit), with regards to estates and trusts, now reads, “Enter the sum of the amounts from Form 1041, Schedule G, lines 1a and 1b, plus any Form 8978 amount included on line 1d; or the amount from the applicable line of your return.”

In 2020, that read, “Enter the sum of the amounts from Form 1041, Schedule G, lines 1a and 1b; or the amount from the applicable line of your return.”

The draft of line 1d of Part III (General Business Credits or Eligible Small Business Credits) now reads, “Low-income housing (carryforward only) (see instructions).” In 2020, that read, “Low-income housing (Form 8586, Part I only).”

And the draft of line 1t of Part III now reads, “Enhanced oil recovery credit.” In 2020, that read, “Enhanced oil recovery credit (carryforward only).”

Issue 8: Bills from the Hill

H.R.4759 – Revitalizing Downtowns Act. To provide an investment credit for the conversion of office buildings into other uses.

H.R.5155 – Taxpayer Penalty Protection Act of 2021. To provide for a temporary safe harbor for certain failures by individuals to pay estimated income tax.

S.2529 – IGNITE American Innovation Act. To provide for advance refunds of certain net operating losses and research expenditures relating to COVID-19, and for other purposes.

S.2581 – Automatic Relief for Taxpayers Affected by Major Disasters and Critical Events Act. To provide relief for taxpayers affected by disasters or other critical events.

S.2583 – To provide for rules for the use of retirement funds in connection with federally declared disasters.

H.R.4817 — Affordable EVs for Working Families Act. To provide a credit for previously owned qualified plug-in electric drive motor vehicles.

H.R.4831 — Charitable Equity for Veterans Act of 2021. To provide for the deductibility of charitable contributions to certain organizations for members of the Armed Forces.

H.R.4852 — Residential Solar Opportunity Act of 2021. To make the credit for a residential energy efficient property permanent.

H.R.4889 — Don’t Weaponize the IRS Act. To codify the Trump administration rule on reporting requirements of exempt organizations, and for other purposes.

H.R.4922 — RAISE the Roof Act. To expand the residential energy efficient property credit and energy credit, and for other purposes.

H.R.4962 — Shareholder Allocation for Rewards to Employees Plan Act (or the “SHARE” Plan). To provide that the stock of certain corporations is eligible for capital gains rates only if such corporation maintains a plan for distributing equity to employees, and for other purposes.

H.R.5078 — First Time Homeowner Savings Plan Act. To increase the amount that can be withdrawn without penalty from individual retirement plans as first-time homebuyer distributions.

H.R.5082 — Cryptocurrency Tax Clarity Act. To clarify the definition of a broker, and for other purposes.

H.R.5083 — Cryptocurrency Tax Reform Act. To clarify the definition of a broker, and for other purposes.

H.R.5097 — V.E.T. Student Loan Act. To retroactively and perpetually apply the exclusion of discharged student loan debt for veterans killed or totally and permanently disabled in connection with their service to the United

S.2583 — To provide for rules for the use of retirement funds in connection with federally declared disasters.

H.R.5214 – To permit expenditures from health savings accounts, flexible spending arrangements, and health reimbursement arrangements for dietary supplements.

H.R.5231 – Relief for Working Families Act. To modify the employer credit for paid family and medical leave, and for other purposes.

H.R.5233 – To make certain adjustments with respect to the nonbusiness energy property tax credit, and for other purposes.

H.R.5254 – SEED Act. To allow early childhood educators to take the educator expense deduction, and for other purposes.

Issue 9: Expanded Tax Benefits Help Individuals, Business Give Charity During 2021, Deductions up to $600 Available for Cash Donations by Non-itemizers

The Taxpayer Certainty and Disaster Tax Relief Act of 2020, enacted last December, provides several provisions to help individuals and businesses who give to charity. The new law generally extends through the end of 2021 four temporary tax changes originally enacted by the Coronavirus Aid, Relief, and Economic Security (CARES) Act. Here is a rundown of these changes.

Ordinarily, individuals who elect to take the standard deduction cannot claim a deduction for their charitable contributions. The law now permits these individuals to claim a limited deduction on their 2021 federal income tax returns for cash contributions made to certain qualifying charitable organizations. Nearly nine in 10 taxpayers now take the standard deduction and could potentially qualify to claim a limited deduction for cash contributions.

These individuals, including married individuals filing separate returns, can claim a deduction of up to $300 for cash contributions made to qualifying charities during 2021. The maximum deduction is increased to $600 for married individuals filing joint returns.

Cash contributions to most charitable organizations qualify. However, cash contributions made either to supporting organizations or to establish or maintain a donor advised fund do not qualify.

Cash contributions carried forward from prior years do not qualify, nor do cash contributions to most private foundations and most cash contributions to charitable remainder trusts.

In general, a donor-advised fund is a fund or account maintained by a charity in which a donor can, because of being a donor, advise the fund on how to distribute or invest amounts contributed by the donor and held in the fund. A supporting organization is a charity that carries out its exempt purposes by supporting other exempt organizations, usually other public charities.

Cash contributions include those made by check, credit card or debit card as well as amounts incurred by an individual for unreimbursed out-of-pocket expenses in connection with the individual’s volunteer services to a qualifying charitable organization. Cash contributions don’t include the value of volunteer services, securities, household items or other property.

100% limit on eligible cash contributions made by itemizers in 2021

Subject to certain limits, individuals who itemize may generally claim a deduction for charitable contributions made to qualifying charitable organizations. These limits typically range from 20% to 60% of adjusted gross income (AGI) and vary by the type of contribution and type of charitable organization. For example, a cash contribution made by an individual to a qualifying public charity is generally limited to 60% of the individual’s AGI. Excess contributions may be carried forward for up to five tax years.

The law now permits electing individuals to apply an increased limit (“Increased Individual Limit”), up to 100% of their AGI, for qualified contributions made during calendar-year 2021. Qualified contributions are contributions made in cash to qualifying charitable organizations.

As with the new limited deduction for nonitemizers, cash contributions to most charitable organizations qualify, but cash contributions made either to supporting organizations or to establish or maintain a donor advised fund, do not. Nor do cash contributions to private foundations and most cash contributions to charitable remainder trusts

Unless an individual makes the election for any given qualified cash contribution, the usual percentage limit applies. Keep in mind that an individual’s other allowed charitable contribution deductions reduce the maximum amount allowed under this election. Eligible individuals must make their elections with their 2021 Form 1040 or Form 1040-SR.

Corporate limit increased to 25% of taxable income

The law now permits C corporations to apply an increased limit (Increased Corporate Limit) of 25% of taxable income for charitable contributions of cash they make to eligible charities during calendar-year 2021. Normally, the maximum allowable deduction is limited to 10% of a corporation’s taxable income.

Again, the Increased Corporate Limit does not automatically apply. C corporations must elect the Increased Corporate Limit on a contribution-by-contribution basis.

Increased limits on amounts deductible by businesses for certain donated food inventory

Businesses donating food inventory that are eligible for the existing enhanced deduction (for contributions for the care of the ill, needy and infants) may qualify for increased deduction limits. For contributions made in 2021, the limit for these contribution deductions is increased from 15% to 25%. For C corporations, the 25% limit is based on their taxable income. For other businesses, including sole proprietorships, partnerships, and S corporations, the limit is based on their aggregate net income for the year from all trades or businesses from which the contributions are made. A special method for computing the enhanced deduction continues to apply, as do food quality standards and other requirements.

Keep good records

The IRS reminds individuals and businesses that special recordkeeping rules apply to any taxpayer claiming a charitable contribution deduction. Usually, this includes obtaining an acknowledgment letter from the charity before filing a return and retaining a cancelled check or credit card receipt for contributions of cash. For donations of property, additional recordkeeping rules apply, and may include filing a Form 8283 and obtaining a qualified appraisal in some instances.

Issue 10: IRS Bifurcates Treatment of Instrument as Stock for Certain § 382 Purposes

“Plain vanilla preferred” stock is not treated as stock for certain § 382 ownership change purposes, including a determination of whether there has been an “owner shift” involving 5 % shareholders of a corporation. But the regulations also contemplate other instances in which a potential for corporate growth may result in an instrument being treated as “stock” for this purpose, although PLR 202131005 illustrates that the analysis is not always binary. The ruling involved a publicly traded corporation which had issued “Instrument I” and “Instrument II” to acquire the stock of a target corporation pursuant to a transaction resulting in an allocation of consideration between the two instruments, with a corresponding issue price assigned to Instrument I.

The treatment of Instrument II was not addressed; as for Instrument I, although terms are redacted, it appears to have been denominated as preferred stock with cumulative dividends but no voting rights. But the issuer also had the right to pay certain dividends in common stock, even though this was not expected to occur on the issue date. And there was potential for a redemption premium in certain unspecified situations, although interestingly, the taxpayer represented that no consideration was given to §382 when the terms of the Instrument were established. In this case, IRS ruled that a specified portion of the Instrument would be treated as stock for § 382 purposes with the remaining portion of the Instrument treated as not stock.

Issue 11: IRS Publishes Updated 2021 Filing Season Statistics

IRS Statistic of Income (SOI) has made available on its website updated 2021 filing season statistics related to individual income tax returns for Tax Year 2020.

The statistics are presented in the form of a table providing data collected from the U. S. Individual Income Tax Returns (Forms 1040) filed and processed through July 1, 2021, for Tax Year 2020.

Through July 1, there were a total of 134,878,000 individual returns received by IRS. Of these, 131,549,000 were e-filed. There were 27,955,000 Forms 1040 filed with no Schedules 1-6 or Schedule A attached.

The link to the table is available here.

The filing season statistics present data from all Forms 1040 processed by the IRS at three critical points during the year: late May, mid-July, and mid-November.

These filing season statistics are presented in two sections.

- First section: Expanded tables present data for selected sources of income, deductions, credits, and taxes for returns filed for the prior tax year.

- Second section: Includes distributional data for AGI, income tax after credits, and the share of income from the sale of capital assets for returns filed for the prior tax year and some late-filed returns for earlier tax years.

Issue 12: Fact Sheet Using E-Signatures on Paper IRS Forms

The IRS allows taxpayers to use electronic or digital signatures (e-signatures) on certain paper forms that can’t be filed electronically. E-signatures are only allowed on certain IRS forms due to security, identity theft, and fraud issues.

Acceptable e-signatures. In the Fact Sheet, the IRS notes that it accepts a variety of e-signatures, including:

- A name typed on a signature block.

- A scanned or digitized image of a handwritten signature that’s attached to an electronic record. (The IRS accepts images of signatures (scanned or photographed) on documents saved in common file types such as tiff, jpg, pdf, and zip.

- A handwritten signature input onto an electronic signature pad.

- A handwritten signature, mark, or command input on a display screen with a stylus device.

- A signature created by a third-party software (i.e., DocuSign).

E-signatures allowed on certain paper-filed forms. According to the Fact Sheet, taxpayers may use e-signatures on paper forms they cannot file using IRS e-file, including the following:

- Form 11-C, Occupational Tax and Registration Return for Wagering;

- Form 637, Application for Registration (For Certain Excise Tax Activities);

- Form 706, U.S. Estate (and Generation-Skipping Transfer) Tax Return;

- Form 706-A, U.S. Additional Estate Tax Return;

- Form 706-GS(D), Generation-Skipping Transfer Tax Return for Distributions;

- Form 706-GS(D-1), Notification of Distribution from a Generation-Skipping Trust;

- Form 706-GS(T), Generation-Skipping Transfer Tax Return for Terminations;

- Form 706-QDT, U.S. Estate Tax Return for Qualified Domestic Trusts;

- Form 706 Schedule R-1, Generation Skipping Transfer Tax;

- Form 706-NA, U.S. Estate (and Generation-Skipping Transfer) Tax Return;

- Form 709, U.S. Gift (and Generation-Skipping Transfer) Tax Return;

- Form 730, Monthly Tax Return for Wagers;

- Form 1066, U.S. Income Tax Return for Real Estate Mortgage Investment Conduit;

- Form 1120-C, U.S. Income Tax Return for Cooperative Associations;

- Form 1120-FSC, U.S. Income Tax Return of a Foreign Sales Corporation;

- Form 1120-H, U.S. Income Tax Return for Homeowners Associations;

- Form 1120-IC DISC, Interest Charge Domestic International Sales – Corporation Return;

- Form 1120-L, U.S. Life Insurance Company Income Tax Return;

- Form 1120-ND, Return for Nuclear Decommissioning Funds and Certain Related Persons;

- Form 1120-PC, U.S. Property and Casualty Insurance Company Income Tax Return;

- Form 1120-REIT, U.S. Income Tax Return for Real Estate Investment Trusts;

- Form 1120-RIC, U.S. Income Tax Return for Regulated Investment Companies;

- Form 1120-SF, U.S. Income Tax Return for Settlement Funds (Under Section 468B);

- Form 1127, Application for Extension of Time for Payment of Tax Due to Undue Hardship;

- Form 1128, Application to Adopt, Change or Retain a Tax Year;

- Form 2678, Employer/Payer Appointment of Agent;

- Form 3115, Application for Change in Accounting Method;

- Form 3520, Annual Return to Report Transactions with Foreign Trusts and Receipt of Certain Foreign Gifts;

- Form 3520-A, Annual Information Return of Foreign Trust with a U.S. Owner;

- Form 4421, Declaration – Executor’s Commissions and Attorney’s Fees;

- Form 4768, Application for Extension of Time to File a Return and/or Pay U.S. Estate (and Generation-Skipping Transfer) Taxes;

- Form 8038, Information Return for Tax-Exempt Private Activity Bond Issues;

- Form 8038-G, Information Return for Tax-Exempt Governmental Bonds;

- Form 8038-GC; Information Return for Small Tax-Exempt Governmental Bond Issues, Leases, and Installment Sales;

- Form 8283, Noncash Charitable Contributions;

- Form 8453 series, Form 8878 series, and Form 8453 series, Form 8878 series, and Form 8879 series regarding IRS e-file Signature Authorization Forms;

- Form 8802, Application for U.S. Residency Certification;

- Form 8832, Entity Classification Election;

- Form 8971, Information Regarding Beneficiaries Acquiring Property from a Decedent;

- Form 8973, Certified Professional Employer Organization/Customer Reporting Agreement; and

- Elections made per Internal Revenue Code § 83(b).

Issue 13: IRS Updates ITIN Application Procedures with FAQ’s

The IRS has updated its frequently asked questions (FAQs) on the procedure for obtaining an Individual Tax Identification Number (ITIN).

An Individual Tax Identification Number (ITIN) is a nine-digit number the IRS issues to individuals who have a U.S. tax filing or reporting obligation but are not eligible for a Social Security Number (SSN).

Individuals apply for an ITIN by filing Form W-7, Application for IRS Individual Taxpayer Identification Number, with the IRS. (Instructions for Form W-7)

The IRS has updated the answer to the following FAQ:

Will the IRS return my original documents to me? How long will it take to get them back?

The IRS is processing Forms W-7 in the order received and it is taking about 14 weeks to process them.

The IRS will return original documents submitted with a Form W-7 to the applicant at the mailing address shown on the Form W-7 after their form has been processed.

If an applicant will need their submitted original documents for any purposes during the 14-week processing period, the IRS recommends that the applicant apply for an ITIN in person at an IRS Taxpayer Assistance Center (TAC) or with a certified acceptance agent (CAA).

In the alternative, an applicant may submit certified copies of their documents. Certified copies must be obtained from the agency that issued the documents.

Applicants who need to get their documents back as quickly as possible may include a prepaid Express Mail or courier envelope (UPS, FedEx, DHL etc.) for faster return delivery of their documents. The IRS will then return the documents in the envelope provided by the applicant.

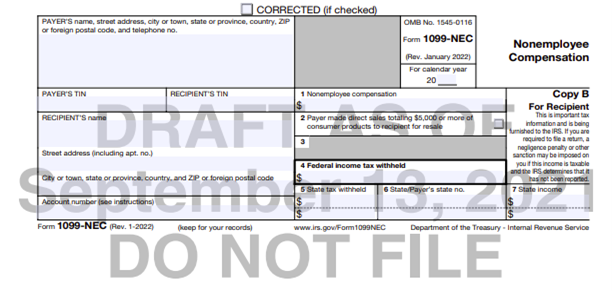

Issue 14: Draft 2022 Form 1099-NEC Issued

Draft 2022 Form 1099-NEC (Nonemployee Compensation) (rev. 9/13/2021)

The IRS has released a draft of the 2022 Form 1099-NEC (Nonemployee Compensation). The draft has no substantive changes from 2021.

Form 1099-NEC rather than Form W-2 (Wage and Tax Statement) is used for payments made in the course of the payor’s trade or business of $600 or more to non-employees.

Issue 15: PMTA Discusses Penalty for Failure to Deposit Taxes Deferred Under CARES Act

Program Manager Technical Advice 2021-007

This memorandum responds toa request for assistance concerning § 2302(a)(2) of the Coronavirus Aid, Relief, and Economic Security Act (CARES Act), Public Law 116-136. This advice may not be used or cited as precedent.

ISSUES: If any portion of an employer’s § 3111(a) (employer portion of social security) taxes or so much of the taxes imposed under § 3221(a) as are attributable to the rate in effect under § 3111(a), the payment and deposit due dates of which are deferred under CARES Act § 2302, is not deposited by the applicable installment due date, is the deferral of the deposit due date invalidated for all of the employer’s deferred §§ 3111(a) or 3221(a) tax, rather than just the remaining delinquent portion? Is the result that the § 6656 penalty for failure to deposit taxes is applicable to the entire deferred amount, assuming that no exception to the penalty applies?

CONCLUSION: Yes, to both questions. CARES Act § 2302(a)(2) conditions the deferral of deposits on the timely deposit of all amounts deferred by the applicable due dates of December 31, 2021 and December 31, 2022.2 For example, if an employer defers the deposit of its portion of the § 3111(a) tax (the employer’s portion of social security tax) in the amount of $50,000, and deposits and pays $25,000 on December 31, 2021 but fails to make any additional deposits or payments by December 31, 2022, the employer is liable for a section 6656 penalty on the entire $50,000 if no exception to the penalty applies.

Issue 16: IRS Awards Three New Collection Contracts – IR 2021-191

The Internal Revenue Service has awarded new contracts to three private-sector collection agencies for collection of overdue tax debts. The new contracts begin Thursday following today’s expiration of the old contracts.

Beginning Thursday, Sept. 23, 2021, taxpayers with unpaid tax bills may be contacted by one of the following three agencies:

CBE Group, Inc.

PO Box 2217

Waterloo, IA 50704

800-910-5837

Coast Professional, Inc.

PO Box 526

Albion, NY 14411

888-928-0510

ConServe

PO Box 307

Fairport, NY 14450

844-853-4875

The IRS will always notify a taxpayer before transferring their account to a private collection agency (PCA).

- First, the IRS will send a letter to the client and their tax representative informing them that their account was assigned to a PCA and giving the name and contact information for the PCA. This mailing will include a copy of Publication 4518, What You Can Expect When the IRS Assigns Your Account to a Private Collection Agency.

- Following IRS notification, the PCA will send its own letter to the client and their representative confirming the account transfer. To protect the taxpayer’s privacy and security, both the IRS letter and the PCA’s letter will contain information that will help clients identify the tax amount owed and assure taxpayers that future collection agency calls they may receive are legitimate.

The private collectors will identify themselves as contractors collecting taxes on behalf of the IRS. Employees of these collection agencies must follow the provisions of the Fair Debt Collection Practices Act, and like IRS employees, must be courteous and must respect taxpayer rights.

Private firms are not authorized to take enforcement actions against taxpayers. Only IRS employees can take these actions, such as filing a notice of Federal Tax Lien or issuing a levy.

The private firms are authorized to discuss payment options, including setting up payment agreements with taxpayers. But as with cases assigned to IRS employees, any tax payment must be made directly to the IRS. A payment should never be sent to the private firm or anyone besides the IRS or the U.S. Treasury. Checks should only be made payable to the United States Treasury.

Issue 17: IRS Issues Correction Notice for 2021 Schedules K-2 and K-3 (Form 1065)

Treasury and the IRS released updated early drafts of new Schedules K-2 and K-3 for Forms 1065, 1120-S, and 8865 for tax year 2021 (filing season 2022). The schedules are designed to provide greater clarity for partners and shareholders on how to compute their U.S. income tax liability with respect to items of international tax relevance, including claiming deductions and credits.

The early release drafts of the schedules are intended to give a preview of the changes before final versions are released. The release of an early draft of the instructions for the schedules is planned for this summer.

The redesigned forms and instructions will also give useful guidance to partnerships, S corporations and U.S persons who are required to file Form 8865 with respect to controlled foreign partnerships on how to provide international tax information. The updated forms will apply to any persons required to file Form 1065, 1120-S or 8865, but only if the entity for which the form is being filed has items of international tax relevance (generally foreign activities or foreign partners).

The changes do not affect partnerships and S corporations with no items of international tax relevance.

Issue 18: CCA: IRS Can Use Either of Two Forms to Levy Rental Payments

Chief Counsel Advice 202137010

The IRS can use either Form 668-A, Notice of Levy, or Form 668-W, Notice of Levy on Wages, Salary, and Other Income, to levy current and future rental income received pursuant to a rental contract.

Issues. (1) Whether a Form 668-W can be used for rental income received pursuant to a rental contract (rather than Form 668-A), and (2) if the wrong form was used, whether the results remain the same, meaning that a continuous levy attaches to income proceeds of a rental contract.

Advice. The Chief Counsel (CC) says it has not located any guidance or authority expressly addressing whether a Form 668-A or a Form 668-W should be used in the context of levying current and future rental payments. The Internal Revenue Manual and the instructions to Form 668-W contemplate other income, so it is not necessarily limited to wages

Issue 19: IRS: Drought-stricken Farmers, Ranchers Have More Time to Replace Livestock

Farmers and ranchers who were forced to sell livestock due to drought may have an additional year to replace the livestock and defer tax on any gains from the forced sales.

To qualify for relief, farmers or ranchers must have sold livestock on account of drought conditions in an applicable region. This is a county or other jurisdiction designated as eligible for federal assistance plus counties contiguous to it. Notice 2021-55, lists applicable regions in 36 states and one U.S. territory.

The relief generally applies to capital gains realized by eligible farmers and ranchers on sales of livestock held for draft, dairy or breeding purposes. Sales of other livestock, such as those raised for slaughter or held for sporting purposes, or poultry, are not eligible.

The sales must be solely due to drought, causing an area to be designated as eligible for federal assistance. Livestock generally must be replaced within a four-year period, instead of the usual two-year period. The IRS is authorized to further extend this replacement period if the drought continues.

The one-year extension, announced in the notice, gives eligible farmers and ranchers until the end of their first tax year after the first drought-free year to replace the sold livestock.

The IRS provides this extension to eligible farmers and ranchers who sold livestock on account of drought conditions in an applicable region that qualified for the four-year replacement period, if the applicable region is listed as suffering exceptional, extreme or severe drought conditions during any week between Sept. 1, 2020, and Aug. 31, 2021.

As a result, eligible farmers and ranchers whose drought-sale replacement period was scheduled to expire on Dec. 31, 2021, in most cases now have until the end of their next tax year to replace the sold livestock. Because the normal drought-sale replacement period is four years, this extension impacts drought sales that occurred during 2017. The replacement periods for some drought sales before 2017 are also affected due to previous drought-related extensions affecting some of these localities.

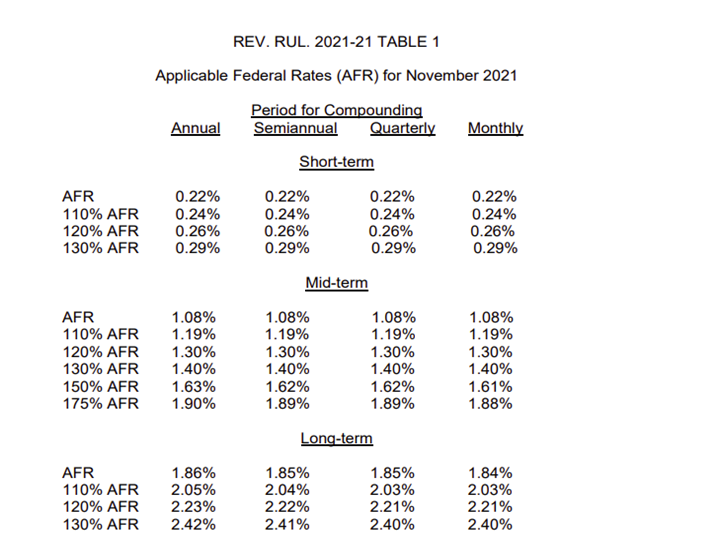

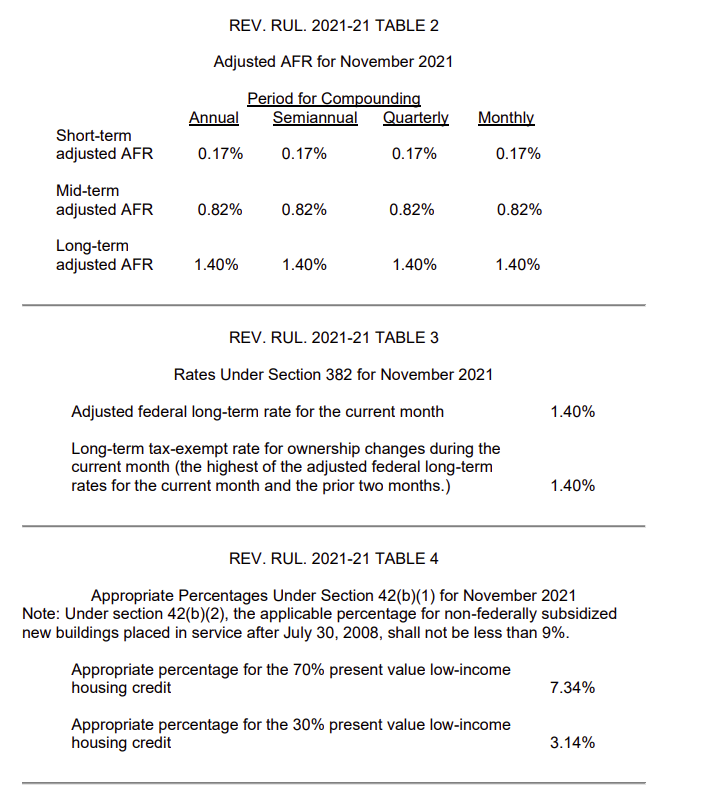

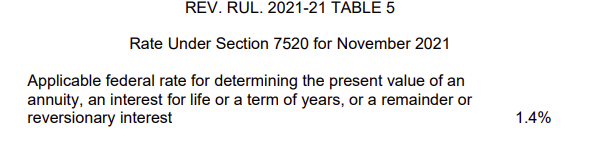

Issue 20: Applicable Federal Rates for November 2021, Rev. Rul. 2021-21

![]() Basics & Beyond Resources

Basics & Beyond Resources

- Blog Page

- Resource List

- Webinar & Seminar Schedules

- Get Registered!

- Note: Paid attendees can request a link to the replay of any previously recorded webinar presentations by emailing us at [email protected]