In This Issue

- IRS Taxpayer Assistance Centers Open on Special Saturdays for Face-to-Face Assistance IR 2022-26

- Offer in Compromise – What Are Our Options When the Client Owes Tax

- IRS Announces Transition Away from Third Party Verification When It Involves Facial Recognition

- Math Error Notices Galore Due to the Recovery Rebate Credit and IRS Suspends Certain Notices

- Status of the IRS Addressed by the National Taxpayer Advocate

- Bills from the Hill

- IRS plans Tax Pro Account Updates and Potential Revision of Circular 230 Release Late in 2022

- IRS Provides Further Details on Additional Relief for Certain Partnerships and S Corporations When Preparing Schedules K-2 and K-3 for 2021

- IRS Issues Interim Guidance for Examining Tax Returns Reporting a Net Operating Loss

- Fact Sheet Addresses the ARPA Tax Benefits for 2021 Filers – IR 2022-29; Fact Sheet 2022-10 (02/08/2022)

- IRS Reminds Taxpayers to Remove Excess Salary Deferrals by April 15

- New Compliance Campaign Announced “Basis Issues” Directed at Partnerships Losses That Exceed Basis

- Interest Rates Increase for the Second Quarter of 2022

- Your Chance to Help Improve the IRS – Apply to Join the IRS Taxpayer Advocacy Panel by April 8

- Applicable Federal Rates for March 2022, Rev. Rul. 2022-3

Issue 1: IRS Taxpayer Assistance Centers Open on Special Saturdays for Face-to-Face Assistance IR 2022-26

As part of a larger effort to help people during this year’s filing season, the IRS announced special Saturday hours at many Taxpayer Assistance Centers (TACs) across the country.

TACs provide taxpayers with in-person help. Select TACs are open from 9 a.m. to 4 p.m., March 12, April 9, and May 14. Normally, these centers are not open on Saturdays. No appointments are required.

People can receive walk-in help on select services, however, the TACs will not accept cash payments on these Saturdays.

To arrive prepared, individuals should bring the following information:

- Current government-issued photo identification.

- Social Security cards for members of their household, including spouse and dependents (if applicable) and

- Any IRS letters or notices received and related documents.

During the visit, IRS staff may also request the following information:

- A current mailing address.

- An email address and

- Bank account information, to receive payments or refunds by direct deposit.

Issue 2: Offer in Compromise – What Are Our Options When the Client Owes Tax

Delinquent clients have several options for working with the IRS to settle their debts, but each individual situation dictates what type of offer in compromise (OIC) should be presented.

An OIC is an agreement between the client and the IRS to resolve a tax debt in a way that’s equitable for both parties. The process begins with the client submitting a proposed arrangement based on what the IRS deems to be the taxpayer’s “true ability to pay,” or the reasonable collection potential (RCP). RCP is the sum of net realizable value (NRV) of real and personal assets plus future net income (FNI).

If the client does not currently have a steady, predictable source of income, their income may be averaged over the previous three years to forecast FNI. Alternatively, the client and the IRS can enter into a future income collateral agreement, which may be appropriate in cases in which the taxpayer’s future income is uncertain but is expected to substantially increase.

To qualify, liability must have already been assessed or will be assessed against the client before the OIC is accepted.

Economic Hardship

Economic hardship means the taxpayer is unable to pay monthly expenses. Economic hardship factors include, but are not limited to:

- long-term illness, medical condition, or disability.

- the number of dependents or if someone else can claim the taxpayer as a dependent.

- the taxpayer’s age, employment status, or employment history.

- cost of living in the taxpayer’s geographic area.

- court-ordered payments (alimony, child support, etc.).

Effective Tax Administration

An Effective Tax Administration (ETA) OIC can be accepted on the grounds of public policy or equity factors if the taxpayer’s liability is the direct result of:

- an IRS processing error.

- erroneous advice or instruction from the IRS.

- third-party criminal or fraudulent activity.

To apply for an ETA OIC, a taxpayer should complete both Forms 656 and 433, draft an eligibility statement, submit supporting documentation, and pay the application fee (if the income waiver does not apply).

Doubt as to Collectability

A doubt as to collectability with special circumstances (DATCSC) OIC may be best for taxpayers who can prove that the tax due cannot fully be paid, and that special circumstances qualify the taxpayer for acceptance for less the amount of RCP calculated by the IRS. Allowable special circumstances are the same as those under economic hardship or public policy or equity grounds.

Doubt as to Liability

The third OIC, doubt as to liability (DATL), differs compared to ETA or DATCSC OICs. Essentially, a DATCSC is a mechanism for correcting an IRS assessment if the taxpayer failed to timely file a petition with the Tax Court. Therefore, DATLs do not apply to liabilities established by a final court decision or judgment. Unlike an ETA or DATCSC, the taxpayer’s ability to pay is not at issue, and Form 433 and the related filing fee is not required.

Issue 3: IRS Announces Transition Away from Third Party Verification When It Involves Facial Recognition

The IRS announced it will transition away from using a third-party service for facial recognition to help authenticate people creating new online accounts. The transition will occur over the coming weeks. Congress has been voicing displeasure with the current identity verification process.

Update: February 21, 2022

The IRS announced a new option in the agency’s authentication system is now available for taxpayers to sign up for IRS online accounts without the use of any biometric data, including facial recognition. This is consistent with the IRS’s commitment earlier this month to transition away from the requirement for taxpayers creating an IRS online account to provide a selfie to a third-party service to help authenticate their identity.

Taxpayers will have the option of verifying their identity during a live, virtual interview with agents; no biometric data – including facial recognition – will be required if taxpayers choose to authenticate their identity through a virtual interview.

Taxpayers will still have the option to verify their identity automatically through the use of biometric verification through ID.me’s self-assistance tool if they choose. For taxpayers who select this option, new requirements are in place to ensure images provided by taxpayers are deleted for the account being created. Any existing biometric data from taxpayers who previously created an IRS Online Account that has already been collected will also be permanently deleted over the course of the next few weeks.

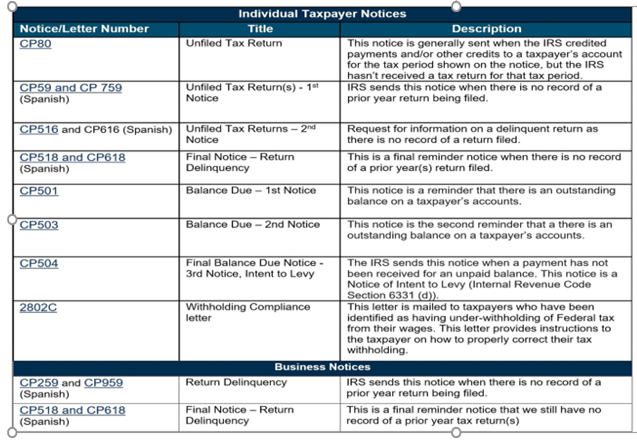

Issue 4: Math Error Notices Galore Due to the Recovery Rebate Credit and IRS Suspends Certain Notices

The number of math error notices sent to taxpayers increased exponentially in calendar year 2021, largely because of adjustments relating to the recovery rebate credit (RRC) and other refundable tax breaks for low- and moderate-income taxpayers.

A math error is a return adjustment which results in the IRS either increasing the amount due, reducing a refund—or, in rarer cases—increasing a refund. Math error additions or subtractions can reflect clerical mistakes, missing identifying information, or miscalculations, as described under §6213(b).

These notices and ultimate responses in addition to IRS’s “turn on a dime” response to the Advanced Child Tax credit and continued backlog of unprocessed returns dating back the pandemic has place the IRS in a critical customer service situation.

Suspension of Notices

Thus, IRS has taken additional steps with changes to specific notices with a suspension policy. This includes the mailing of automated collection notices normally issued when a taxpayer owes additional tax, and the IRS has no record of a taxpayer filing a tax return. In addition, the mailings include balance due notices and unfiled tax return notices.

The IRS does not have the authority to stop all notices as many are legally required to be issued within a certain timeframe.

The suspended notices include:

Issue 5: Status of the IRS, Addressed by the National Taxpayer Advocate

The National Taxpayer Advocate offered suggestions to Congress to assist IRS from digging out from under the burden – basically initiated by Congress and its lack of foresight and pandemic legislation that has tested IRS resources to the breaking point.

What are the issues:

- The year 2021 was the “most challenging year ever for taxpayers,” whose phone calls to IRS support lines were answered only about 11% of the time.

- The IRS’s Where’s My Refund tool—accessed 632 million times last year—lacks information on unprocessed returns and provides no context on status delays.

- The IRS’s shrunken workforce lacked the resources, manpower, and time to meet demand, leading to millions of refunds that have yet to reach taxpayers.

- Taxpayer assistance is sadly lacking.

To address its backlog of unprocessed previous-year tax returns and weak customer support, the IRS should offer higher pay to attract new employees and rely on short-term help from outside consultants. It has been challenging for IRS in recent years to boost staffing due in part to lack of a consistent budget and low pay.

The IRS has filled only 179 of the 5,000 positions opened to add to the roster of return processers. The submission-processing employees are typically hired at or around the federal government’s GS-3 level, at which the base salary is $24,749. Even if new hires were offered better pay and incentives, it is feared the IRS will not be able to hire enough people to get them out of the hole, Congress and IRS has dug jointly.

Note: In 1986 the based salary for customer services “telephone” assistors was under $14,000. Considering inflation, that salary has not progress much as we enter 2022.

The Advocate as well as Congress have suggested increasing automation of IRS processes as another way to reduce the backlog and improve taxpayer service, but the IRS would need “sustained, multiyear” funding to modernize its systems. IRS operates on 1980’s technology.

IRS and the Paper Processing Problem

For the 2022 filing season, the IRS needs to process millions of remaining 2020 paper returns alongside incoming returns for 2021. IRS has dispatched 1,200 workers to sort through amended paper returns from the previous year and is setting up another specialized team to tackle the same task for this year’s returns.

There is no doubt that paper processing remains the agency’s biggest challenge, and that will continue throughout 2022. As of late December 2021, the IRS still had backlogs of 6 million unprocessed original individual returns (Form 1040 series) and 2.3 million unprocessed amended individual returns (Forms 1040-X). For original returns that were e-filed, the IRS has mostly worked through the backlog.

But the story is very different for paper returns, taxpayers have been experiencing significant delays in receiving their tax refunds because of unprecedented IRS backlogs in the processing of original and amended tax returns.

As of February 14, the IRS website reported that “all paper and electronic individual refund returns received prior to April 2021 have been processed if the return had no errors and did not require further review.” The comment suggests that returns filed as far back as April 2021 are still awaiting processing.

Part of the backlog problem stems from the IRS suspending about 35 million returns due to errors—an increase of nearly 86% from previous years, mostly due the Recovery Rebate Credit – Economic Stimulus Payment matching.

The following recommendations have been made to ease many of the customer service problems in the short term:

- Prioritize the processing of original and amended paper tax returns through an “all hands-on-deck” strategy.

- Explore options to increase compensation for processing employees, minimize hiring lags, and use outside consultants to assist if necessary.

- Provide penalty relief for 2020 and 2021 tax returns.

- Suspend all automated collection notices until the IRS gets current in processing original and amended tax returns and taxpayer correspondence – IRS has acted on this issue.

- Add a dedicated team to accelerate the processing of claims for tentative refunds and employers’ quarterly federal tax returns.

- Create and update a weekly “dashboard” on IRS.gov to provide the public with current and specific information about delays – the new Special Tax Season Alerts was created, see below.

The taxpayer advocate also testified about the need for sufficient multiyear funding of the IRS to modernize its information technology systems and outlined her recommendations to improve tax administration.

IRS Announces They Will Not Close the Austin Campus Processing Center

After receiving a letter from several members of Congress, including U.S. Reps. Bill Pascrell, Jr. (D-NJ) and Lloyd Doggett (D-TX), and U.S. Sen. Bob Menendez (D-NJ), questioning its plans to close another return processing center, the IRS announced on February 17 that it will not be closing its Austin, TX, return processing center after all.

In 2016, the IRS announced its plans to close all but two of its return processing centers. The remaining processing centers would be Kansas City, MO, and Ogden, Utah. Under that plan, by the end of 2021 the IRS had closed all but three of its return processing centers: Austin, TX, Kansas City, MO, and Ogden, Utah. The IRS planned to close the Austin processing center by September 2024.

However, certain members of Congress concerned about how closing the Austin processing center would affect return processing and other issues, on February 17 sent a letter to IRS Commissioner Charles Rettig. The letter noted that while electronic filing was increasing, the effort to close the Austin processing center “no longer made any sense—especially given the extensive paper backlog and hiring challenges that have plagued the IRS for the last two filing seasons.” The letter asked the IRS to reconsider closing the Austin processing center until the current processing issues were addressed. In addition, an earlier TIGTA audit had found that the processing times for ITIN applications, which are processed only at the Austin center, have doubled over the past two years due to COVID-19 closures. This has led to increased wait times for applicants applying for an ITIN to pay their taxes or receive the Child Tax Credit (CTC) or advanced CTC.

The letter expressed concern that “closing the Austin Tax Processing Center will further delay the processing of applications for ITINs, as this facility is the only facility that processes ITIN applications. On the same day it received the letter, the IRS announced it was no longer planning on closing the Austin, TX processing center.

New IRS Web Page – Filing Season Updates – IR 2022-32, 2/14/2022

The IRS has added a page to its website for updates on the 2022 tax filing season as well as efforts by the agency to clear a backlog of unprocessed returns from past years. Special Tax Season Alerts

Issue 6: Bills from the Hill

Below is a list of new tax bills introduced in Congress, for which bill text is now available. The text of each bill can be accessed by clicking on the bill number.

H.R.6428 – Brick and Mortar Small Business Tax Credit Act of 2022. To establish a State and local general sales tax credit for small businesses.

H.R.6590, the Senior Citizens Tax Elimination Act. This bill would repeal the inclusion in gross income of Social Security benefits.

S.3505 – Nurse Corps Tax Parity Act of 2022. To exclude certain Nurse Corps payments from gross income.

Issue 7: IRS plans Tax Pro Account Updates and Potential Revision of Circular 230 Release Late in 2022

This summer and during the third quarter of fiscal 2023, IRS will issue new elements of its dedicated accounts for tax professionals, initiated last year.

The forthcoming updates will include enabling account users to view and print power-of-attorney documents and tax information authorizations once they are approved, along with searchability tools.

This summer’s update is likely to include notifications by email and within mobile apps that tell tax professionals when their clients signed the submitted authorizations, as well as when authorization signatures are required.

The first batch of updates should also establish an expiration system that will “sweep” authorizations pending for up to 120 days out of a taxpayer’s and tax professional’s accounts.

The Tax Pro Account updates planned for the third quarter of fiscal 2023—April through June of the next calendar year—are intended to help tax advisers and preparers collect all central authorization files (CAFs) produced before the online account system was set up. Many such documents are only on paper, and current Tax Pro Accounts include only CAF documents that are electronic.

In addition, and update on the revision of Circular 230 was announced. The Treasury Department has completed its review of proposed revisions to IRS Circular 230, the body of regulations governing tax professionals who practice before the agency. The changes to Circular 230 are meant to address those parts of the rules requiring additional clarity and to eliminate provisions that the IRS has deemed inconsistent or unenforceable. Treasury officials have consolidated and evaluated public comments on the various Circular 230 revisions to determine their feasibility, hopefully, maybe this year, a proposed draft will be out.

Issue 8: IRS Provides Further Details on Additional Relief for Certain Partnerships and S Corporations When Preparing Schedules K-2 and K-3 for 2021

The IRS provided further details on additional transition relief for certain domestic partnerships and S corporations preparing the new schedules K-2 and K-3 to further ease the change to these new schedules. Those eligible for the relief will not have to file the new schedules for tax year 2021.

The new schedules K-2 and K-3 improve reporting by standardizing international tax information to partners and flow-through investors, making it easier for them to report these items on their tax returns. In addition, the changes ease flow-through return preparation compliance by clarifying obligations and standardizing the format for reporting.

Notice 2021-39 provides penalty relief for good-faith efforts to adopt the new schedules. The relief’s transition relief, appears in new frequently asked questions (FAQs) on Schedules K-2 and K-3, and allows an additional exception for tax year 2021 filing requirements by certain domestic partnerships and S corporations.

To qualify for this exception, the following must be met:

- In tax year 2021, the direct partners in the domestic partnership are not foreign partnerships, foreign corporations, foreign individuals, foreign estates or foreign trusts.

- In tax year 2021, the domestic partnership or S corporation has no foreign activity, including foreign taxes paid or accrued or ownership of assets that generate, have generated or may reasonably expected to generate foreign source income (see 1.861-9(g)(3)).

- In tax year 2020, the domestic partnership or S corporation did not provide to its partners or shareholders nor did the partners or shareholders request the information regarding (on the form or attachments thereto):

- Line 16, Form 1065, Schedules K and K-1 (line 14 for Form 1120-S), and

- Line 20c, Form 1065, Schedules K and K-1 (Controlled Foreign Corporations, Passive Foreign Investment Companies, 1120-F, section 250, section 864(c)(8), § 721(c) partnerships, and § 7874) (line 17d for Form 1120-S).

- The domestic partnership or S corporation has no knowledge that the partners or shareholders are requesting such information for tax year 2021.

If a partnership or S corporation qualifies for this exception, the domestic partnership or S corporation does not need to file Schedules K-2 and K-3 with the IRS or with its partners or shareholders. However, if the partnership or S corporation is subsequently notified by a partner or shareholder that all or part of the information contained on Schedule K-3 is needed to complete their tax return, then the partnership or S corporation must provide the information to the partner or shareholder.

If a partner or shareholder notifies the partnership or S corporation before the partnership or S corporation files its return, the conditions for the exception are not met and the partnership or S corporation must provide the Schedule K-3 to the partner or shareholder and file the Schedules K-2 and K-3 with the IRS.

Issue 9: IRS Issues Interim Guidance for Examining Tax Returns Reporting a Net Operating Loss – https://www.irs.gov/pub/foia/ig/sbse/sbse-04-0222-0002.pdf

The IRS’s Small Business and Self-Employed (SB/SE) and Large Business and International (LB&I) divisions have issued guidance to their examiners on scrutinizing tax returns that report net operating losses (NOLs). The guidance focuses on issues related to NOL carrybacks.

Carrying back net operating losses. Generally, eligible taxpayers that want to carry back an NOL to claim a refund may:

- File an application for a tentative refund within 12 months of the end of the loss year, or

- Amend the carryback year return within the normal limitations period for filing refund claims.

Note: The time frames for requesting refunds based on NOL carrybacks are frequently subject to modification. For example, in Notice 2020-26, 2020-18 IRB 744, the IRS provided a temporary extension of time to file a tentative carryback for NOLs arising a tax year that began during calendar year 2018 and ended on or before June 30, 2019.

However, beginning in tax year 2021, NOL carrybacks are limited to farming and insurance company (other than life insurance company) losses.

Examination Guidance

The new guidance provides SB/SE and LB&I Examination employees with step by step instructions for examining tax returns reporting an NOL carryback.

Issue 10: Fact Sheet Addresses the ARPA Tax Benefits for 2021 Filers – IR 2022-29; Fact Sheet 2022-10 (02/08/2022)

The IRS released Fact Sheet 2022-10, which discusses various tax benefits enacted in the American Rescue Plan Act.

American Rescue Plan Act. Among other things, the American Rescue Plan Act (ARP Act, ARPA; PL 117-2), expanded tax credits for families (such as the child tax credit and the child and dependent care credit), expanded the earned income tax credit (EITC) for childless workers, and provided a deduction for non-itemizers who give to charity and a higher limit for itemizers who give to charity.

Fact sheet discusses ARPA tax benefits. The IRS’s newly released fact sheet discusses ARP Act tax benefits taxpayers may be eligible for, including the following:

- Child Tax Credit: Families can claim this credit, even if they received monthly advance payments during the last half of 2021.

- Child and Dependent Care Credit: Families who pay for daycare so they can work or look for work can get a tax credit worth up to $4,000 for one qualifying person and $8,000 for two or more qualifying persons.

- Earned Income Tax Credit: The American Rescue Plan boosted the EITC for childless workers. There are also changes that can help low- and moderate-income families with children.

- Recovery Rebate Credit: Those who missed out on last year’s third round of Economic Impact Payments (EIP3), also known as stimulus payments, may be eligible to claim the RRC. This credit can also help eligible people whose EIP3 was less than the full amount, including those who welcomed a child in 2021.

- Deductions for gifts to charity: Taxpayers who take the standard deduction can deduct eligible cash contributions they made during 2021. Married couples filing jointly can deduct up to $600 in cash donations and individual taxpayers can deduct up to $300 in donations. In addition, itemizers who make large cash donations often qualify to deduct the full amount in 2021.

Issue 11: IRS Reminds Taxpayers to Remove Excess Salary Deferrals by April 15

In an Employee Plans news alert, the IRS has reminded taxpayers that for 2021 the aggregate total of salary deferrals to retirement plans is limited to $19,500 (plus an additional $6,500 if age 50 or over). Taxpayers who have salary deferrals that exceed the limit for 2021, must withdraw the excess amount, plus earnings, by April 15, 2022.

Taxpayers who made salary deferral contributions to two or more retirement plans in 2021 may be most at risk for exceeding the deferral limit. For a taxpayer who withdraws excess salary deferrals, plus earnings, by April 15, 2022:

- Excess deferrals are taxed as 2021 income.

- Earnings on excess deferrals are taxed as income in the year withdrawn (2022).

- Excess deferrals are not subject to the 10% early distribution tax, 20% withholding, or spousal consent requirements.

However, if taxpayers with excess deferrals don’t withdraw those excess deferrals, plus earnings, by April 15, 2022:

- Excess deferrals are taxed as income in 2021 and again when they are withdrawn.

- Earnings on the excess are taxed in the year withdrawn.

- Withdrawals may be subject to the 10% early distribution tax, 20% withholding, and spousal consent requirements.

Issue 12: New Compliance Campaign Announced “Basis Issues” Directed at Partnerships Losses That Exceed Basis

Under the Code, partners that report flow-through losses from partnerships must have adequate outside basis in their partnership interest (as determined pursuant to § 705) to deduct the losses. If the client does not have adequate outside basis, the losses are suspended under § 704(d) to the extent they exceed the partner’s basis in their partnership interest.

Note: The issue here is partners deducting pass-through losses that should be suspended because they exceed the taxpayer’s outside basis in their partnership interest.

Issue 13: Interest Rates Increase for the Second Quarter of 2022

IRS announced that interest rates will increase for the calendar quarter beginning April 1, 2022. The rates will be:

- 4% for overpayments (3% in the case of a corporation);

- 5% for the portion of a corporate overpayment exceeding $10,000;

- 4% for underpayments; and

- 6% for large corporate underpayments.

Under the Internal Revenue Code, the rate of interest is determined on a quarterly basis. For taxpayers other than corporations, the overpayment and underpayment rate is the federal short-term rate plus 3 percentage points.

Generally, in the case of a corporation, the underpayment rate is the federal short-term rate plus 3 percentage points and the overpayment rate is the federal short-term rate plus 2 percentage points. The rate for large corporate underpayments is the federal short-term rate plus 5 percentage points. The rate on the portion of a corporate overpayment of tax exceeding $10,000 for a taxable period is the federal short-term rate plus one-half (0.5) of a percentage point.

The interest rates announced today are computed from the federal short-term rate determined during January 2022 to take effect Feb. 1, 2022, based on daily compounding. You can link to Revenue Ruling 2022-05 announcing the rates of interest.

Issue 14: Your Chance to Help Improve the IRS – Apply to Join the IRS Taxpayer Advocacy Panel by April 8

The IRS is seeking civic-minded volunteers to serve on the Taxpayer Advocacy Panel (TAP). Applications will be accepted through April 8.

What is the Taxpayer Advocacy Panel?

The TAP is a federal advisory committee that serves a vital role in tax administration. TAP members volunteer their time and energy to improve IRS services and taxpayer satisfaction by listening to taxpayers, identifying significant taxpayer concerns and making recommendations to address those concerns. The TAP is a diverse group of ordinary citizens who possess a sense of civic duty, patriotism and belief in an effective and well-regarded tax system The TAP makes a difference and by joining it you can too.

TAP successes in 2021

Each year, the TAP submits dozens of recommendations to the IRS. In 2021 alone, the TAP made 193 recommendations to the IRS, many of which have already been implemented. Because of the TAP’s recommendations in 2021, the IRS has improved many of its tax forms, instructions and publications, and clarified the information in several frequently-used IRS letters.

Who can apply

To the extent possible, the TAP includes members from all 50 states, the District of Columbia and Puerto Rico, as well as one member to represent U.S. citizens living and working abroad. Each member is appointed to represent the interests of taxpayers in their geographic location as well as taxpayers overall.

Federal advisory committees are required to have a balanced representation of different viewpoints. Therefore, applicants from under-represented groups, such as Native Americans and non-tax professionals, are particularly encouraged to apply. TAP is currently seeking candidates in the following states: Alabama, Arkansas, Arizona, California, Colorado, Florida, Iowa, Idaho, Illinois, Indiana, Kentucky, Massachusetts, Maine, Missouri, Mississippi, Montana, North Carolina, North Dakota, New Hampshire, New Mexico, Nevada, New York, Ohio, Oklahoma, Oregon, Puerto Rico, Rhode Island, South Carolina, South Dakota, Texas, Vermont, Wisconsin and West Virginia. However, candidates residing in all the listed locations are encouraged to apply, and all timely applications will be considered.

TAP members must be U.S. citizens who are current with their federal tax obligations and able to commit 200 to 300 volunteer hours during the year. TAP members must also pass a Federal Bureau of Investigation criminal background check. Members cannot be federally registered lobbyists. Current Department of the Treasury or IRS employees cannot serve on the panel. Former Department of the Treasury or IRS employees and former TAP members can be considered for appointment three years after their employment or previous TAP membership has ended. Tax practitioner applicants must be in good standing with the IRS (meaning not currently under suspension or disbarment).

New TAP members will serve a three-year term starting in December 2022. Applicants chosen as alternate members will be considered to fill any vacancies in their areas during the next three years.

More information

For additional information about the TAP and to start the application process, visit www.improveirs.org or call toll-free at 888-912-1227 and select prompt number five. Callers outside the U.S. may call 214-413-6523 (not a toll-free number) or email the TAP staff at [email protected]. A video is also available with more information about the TAP and about how to contribute to this dynamic group of volunteers.

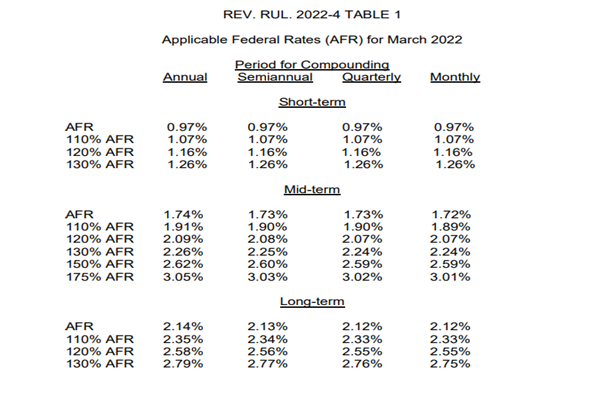

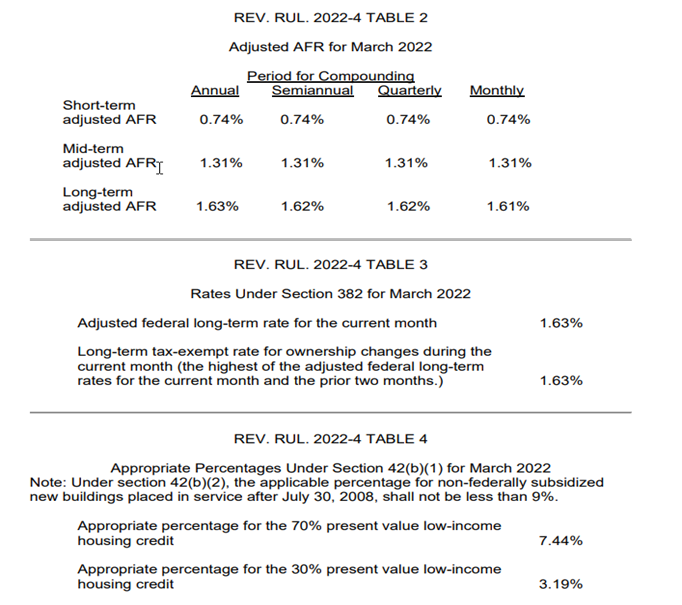

Issue 15: Applicable Federal Rates for March 2022, Rev. Rul. 2022-3

REV. RUL. 2022-4 TABLE 5

Rate Under Section 7520 for March 2022 Applicable federal rate for determining the present value of an annuity, an interest for life or a term of years, or a remainder or reversionary interest 2.0%