Important Update to the November Newsletter – Concerning Marketplace and Healthcare Subsidy – May Impact Your Client

Please review the first page of the November Newsletter to get the background on this issue – here is what has happened thus far:

The client’s return has been received but on where’s my refund – it says the return is being processed and a date for the refund will be provided at a later date…

The return was e filed and accepted on 06/25/2020.

The taxpayer received an email from healthcare.gov, that they are in danger of losing their benefits because they have not filed their return and reconciled there 2019 assistance that they received on form 8962.

Per healthcare.gov they are notified by a tape about whether a “customer” that received a subsidy has filed their return for the current year (2019) and reconciled the subsidy on form 8962. They can still apply for insurance they just will not receive the subsidy.

So, the taxpayer has to go in and apply for the insurance and subsidy – Then they will receive a formal letter that states they are at risk of losing their financial assistance starting 2021 since they have not filed. The letter advises the if they have filed to do nothing, or if not, file the original return or amended return with the form 8962. This letter will also advise the taxpayer that after they file (and receive the letter per the assistor) they can go back into the market place and there is a box for them to check attesting that the return has been filed and the reconciliation has been done for any past premium credits. This has to be done before or by the 15th of December.

Once this is done the account will be reviewed – If the return still has not processed, the taxpayer will be notified by the marketplace that the taxpayer is ineligible for financial assistance to help pay for marketplace coverage in 2021. If the taxpayer disagrees with this decision, they can file an appeal. A separate notice will be sent, from the marketplace, on how to file an appeal. The appeal must be filed within 90 days from the date of the letter that tells you that you and your household members have been determined to be ineligible for financial assistance.

The appeal form is on the website at www.healthcare.gov/marketplace-appeals/appeal-forms/

You can ask to keep you’re your eligibility during your appeal, if you previously received the coverage with financial assistance.

Out of the three clients– One of the returns has now processed and I am told that should be updated with marketplace automatically, but I was not able to find out how or often this is updated. Just that they receive updates all the time. I told my client to wait until they receive a refund next week and then apply.

Another return is just not showing up yet – So we are waiting…

The last one is mentioned above.

The Marketplace open season begins November 1, 2020 – December 15, 2020. Since that is a weekend – open season began October 30, 2020.

Congress Update:

Control of the Senate hinges on two January 5, 2021 runoffs in Georgia. The Senate ratio for the next Congress prior to then will be 50 Republicans, 48 Democrats – so we await the results of the election.

Congress will return after the Thanksgiving recess to determine what can be done in the lame-duck session.

Issues are on the table:

- Keeping the government running, as of December 11 funding needs to be extended.

- Secure Act 2.0 has some interesting tax planning opportunities.

- Will we get the #4 Coronavirus Legislation?

These are the three main issues facing Congress as we move into year end. Congress the past few years have passed, and the President has signed into law late tax legislation that we as tax professional scramble to understand and implement. In addition, IRS is in the same position as changes may need to be made to forms and instructions as well as guidance needing to be addressed. The end of 2020 may be a challenge we have to face in 2021 as we prepare for another tax season.

Basics and Beyond will be monitoring Congress and make sure to review the January Newsletter for updates and any last-minute webinars to address any changes that may occur.

Year-End Update: $279

2020 Year-End Seminars

https://www.cpehours.com/income-tax-seminar-information/

Copy and paste the above into your browser to register.

2020 Year-end Income Tax Update (see details below):

- 2020 Tax Legislation–New Developments, Review of Cases, Rulings & IRS Pronouncements

- QBI, CARES and Secure Act Unique Year End Issues

- Meals & Entertainment under the TCJA

- IRC 121 and the Primary Residence

- Ethics – The Creative Tax Professional

- S-Corporation Basis Issues

- Centralized Partnership Audit Regime

- Preparing for the 2021 Tax Season and the Coronavirus Impact

We are also here to assist with other CPE you may need to completed your annual requirements.

December Webinars

| Date | Topic | CPE Hours | Time | Instructor |

| Tuesday December 15, 2020

|

Schedule K-1 Reporting – Notice 2019-66 (Fall/Winter)

|

1 Credit Hour

|

2:00-3:00

Eastern Time |

Michael Miranda

|

| Wednesday December 16, 2020

|

Penalty Abatement & Reasonable Cause

|

1 Credit Hour

|

2:00-3:00

Eastern Time |

AJ Reynolds |

| Thursday December 17, 2020

Date |

“Do the Right Thing” Part 4: Hot Button Issues of the OPR

|

1 Credit Hour | 2:00-3:00

Eastern Time |

Kristy Maitre |

| Friday December 18, 2020

|

“Do the Right Thing” Part 3: Frivolous Returns

|

1 Credit Hour

|

2:00-3:00

Eastern Time |

Kristy Maitre |

Late Breaking PPP Loan Guidance

Revenue Procedure 2020-51: This revenue procedure provides a safe harbor for certain Paycheck Protection Program loan participants, whose loan forgiveness has been partially or fully denied, or who decide to forego requesting loan forgiveness, to claim a deduction for certain otherwise deductible eligible payments on (1) the taxpayer’s timely filed, including extensions, original income tax return or information return, as applicable, for the 2020 taxable year, or (2) an amended return or an administrative adjustment request (AAR) under section 6227 of the Internal Revenue Code (Code) for the 2020 taxable year, as applicable. For taxpayers that decide to forego requesting loan forgiveness, the safe also allows these taxpayer to claim a deduction for the otherwise deductible eligible payments on an original income tax return or information return, as applicable, for the taxable year in which the taxpayer decides to forego requesting forgiveness.

Revenue Ruling 2020-27: This revenue ruling provides guidance on whether a Paycheck Protection Program (PPP) loan participant that paid or incurred certain otherwise deductible expenses can deduct those expenses in the taxable year in which the expenses were paid or incurred if, at the end of such taxable year, the taxpayer reasonably expects to receive forgiveness of the covered loan. The revenue ruling also provides guidance if, as of the end of the 2020 taxable year, the PPP loan participant has not applied for forgiveness, but intends to apply in the next taxable year.

Rev. Proc. 20-51 and Rev. Rul. 20-27 will be in IRB 2020-50, dated Dec. 7.

In This Issue

Issue 1: IRS Warms of New COVID Related Scam

Issue 2: Renew Your PTIN by December 31, 2020

Issue 3: 2020 Instructions for Form 8995 Qualified Business Income Deduction Simplified Computation – What’s New with the Form

Issue 4: FAQ’s on Electronic Filing of Form 1040X

Issue 5: New Schedule LEP – Form 1040

Issue 6: Virtual Currency

Issue 7: 2020 Form 990-T Exempt Organization Business Income Tax Return Changes

Issue 8: IRS Payment Arrangements Easier to Set Up – IR 2020-248

Issue 9: Deferral of Employment Tax Deposits and Payments Through December 31, 2020 – Self-Employed

Issue 10: Employment Coverage Thresholds Changes for 2021 – Social Security Administration

Issue 11: Form 8283 Changes – Noncash Charitable Contributions

Issue 12: Tax Court Suspends In-Person Acceptance of Hand-Delivered Documents

Issue 13: Tax Court Updates Attorney Admission to Practice Application

Issue 14: Draft Instructions for Forms 1094-B and 1095-B – Changes

Issue 15: IRS Updates Operations During COVID – October 30, 2020

Issue 16: Draft of New Form 8915-E for Qualified 2020 Disaster Retirement Plan Distributions and Repayments (Use for Coronavirus-Related Distributions

Issue 17: New Filing Addresses for Form 8857 Request for Innocent Spouse Relief

Issue 18: IRS Will Issue Proposed Deduction Regulations for Passthrough Entities

Issue 19: Guidance Issued When Applying for PPP Loan Forgiveness

Issue 20: IRS Has Release Publication 1494, Tables for Figuring Amount Exempt from Levy on Wages, Salary, and Other Income (Forms 668-W(ACS) and 668-W(ICS)) for 2021

Issue 21: Applicable Federal Rates (AFR) for December 2020 – Rev. Rul. 2020-26

NEWS

Issue 1: IRS Warms of New COVID Related Scam

The Internal Revenue Service, state tax agencies and the tax industry today warned of a new text scam created by thieves that trick people into disclosing bank account information under the guise of receiving the $1,200 Economic Impact Payment.

The IRS, states and industry, working together as the Security Summit, remind taxpayers that neither the IRS nor state agencies will ever text taxpayers asking for bank account information so that an EIP deposit may be made.

The scam text message states: “You have received a direct deposit of $1,200 from COVID-19 TREAS FUND. Further action is required to accept this payment into your account. Continue here to accept this payment …” The text includes a link to a fake phishing web address.

This fake phishing URL, which appears to come from a state agency or relief organization, takes recipients to a fraudulent website that impersonates the IRS.gov Get My Payment website. Individuals who visit the fraudulent website and then enter their personal and financial account information will have their information collected by these scammers.

People who receive this text scam should take a screen shot of the text message that they received and then include the screenshot in an email to [email protected] with the following information:

- Date/Time/Time zone that they received the text message

- The number that appeared on their Caller ID

- The number that received the text message

The IRS does not send unsolicited texts or emails. The IRS does not call people with threats of jail or lawsuits, nor does it demand tax payments on gift cards.

People who believe they are eligible for the Economic Impact Payment should go directly to IRS.gov.

Issue 2: Renew Your PTIN by December 31, 2020

Preparer Tax Identification Number (PTIN) renewal for 2021 is underway, as is participation in the Annual Filing Season Program for 2021. The IRS Return Preparer’s Office (RPO) will be sending letters reminding tax professionals to renew the PTIN and the AFSP participants to take annual test. More than 780,000 active tax return preparers are starting to prepare for the upcoming 2021 filing season by renewing their Preparer Tax Identification Numbers (PTINs) now. All current PTINs will expire December 31, 2020.

Anyone who prepares or assists in preparing federal tax returns for compensation must have a valid 2021 PTIN before preparing returns. All enrolled agents must also have a valid PTIN.

Tax preparers must pay a fee of $35.95 to renew or obtain a PTIN for 2021. The PTIN fee is non-refundable.

Issue 3: 2020 Instructions for Form 8995 Qualified Business Income Deduction Simplified Computation – What’s New with the Form

Tracking Losses

A worksheet is added to provide a reasonable method to track and compute the previously disallowed losses or deductions to be included in the qualified business income deduction calculation for the year allowed. Software should also track.

Charitable Contributions

A change to the instructions concerning whether charitable contributions must be deducted in computing qualified business income (QBI) for purposes of computing the QBI deduction.

The 2019 Form 8995 instructions provide:

Your QBI includes items of income, gain, deduction, and loss from your trades or businesses that are effectively connected with the conduct of a trade or business in the United States. This includes income from partnerships (other than PTPs), S corporations, sole proprietorships, certain estates and trusts that are included or allowed in figuring your taxable income for the year. To figure the total amount of QBI, you must consider all items that are related to the trade or business. This includes, but isn’t limited to, charitable contributions, unreimbursed partnership expenses, business interest expense, deductible part of self-employment tax, self-employment health insurance deduction, and contributions to qualified retirement plans.

In the 2020 draft PDF of the instructions, the last sentence of the above paragraph is:

This includes, but isn’t limited to, unreimbursed partnership expenses, business interest expense, deductible part of self-employment tax, self-employment health insurance deduction, and contributions to qualified retirement plans.

Note: Nothing has been released that states that charitable contributions no longer are part of the QBI deductions. This is after all a draft and may have been missed. We are monitoring.

![]()

Issue 4: FAQ’s on Electronic Filing of Form 1040X

Can I file my Amended Return electronically?

If a client needs to amend the 2019 Forms 1040 or 1040-SR you can now file the Form 1040- X, Amended U.S. Individual Income Tax Return electronically using available tax software products.

What are some reasons that an Amended Return cannot be filed electronically?

Amended Returns must be filed by Paper for the following reasons:

- Only Tax Year 2019 1040 and 1040-SR returns can be amended electronically at this time. Amended Returns for any other tax years or tax types must be filed by paper.

- There must be a record of an “original” electronically filed return for Tax Year 2019. If the original Tax Year 2019 return was filed by paper, it must be amended by paper.

- If the Primary Social Security Number is different from the one provided on the Original Return, then the Amended Return must be filed by paper.

- If the Spouse’s Social Security Number (if applicable) is different from the one provided on the Original Return, then the Amended Return must be filed by paper.

- If the Filing Status differs from the Filing Status on the Original Return, then the Amended Return must be filed by paper.

How do I file my Amended Return electronically?

Contact your preferred tax software provider to verify their participation and for specific instructions needed to submit amended return and to answer any questions.

How many Amended Returns can be filed electronically?

Filers will be allowed to electronically file up to three “accepted” Amended Returns. After the third accepted Amended Return, all subsequent attempts will reject.

Can I file my Amended return electronically for previous tax years?

You can only amend tax year 2019 Forms 1040 and 1040-SR returns electronically at this time.

Will filing my Amended Return be processed faster when filed electronically?

Currently, the normal processing time of up to 16 weeks also applies to electronically filed Amended Returns.

What forms are required with an electronically filed Amended Return?

Both the electronic Form 1040 and 1040-SR Amended Returns (with attached Form 1040-X) will require submission of ALL necessary forms and schedules as if it were the Original 1040 or 1040-SR submission, even though some forms may have no adjustments.

When electronically filing Form 1040-X, is a new Form 8879 required?

A new Form 8879 is required each time an Amended Form 1040 or Form 1040-SR is electronically filed.

Are two Form 8879s required when filing an electronic Amended Return (one for the 1040-X, one for the Amended 1040)?

Only one Form 8879 is required.

When electronically filing Amended Returns, if a field on Form 1040 Amended Return is blank, should the corresponding field on the Form 1040-X Amended Return also be blank or should a zero be entered?

For electronically filed Amended Returns: If an amount in a field on the Form 1040 or 1040-SR is blank, then the corresponding field on the Form 1040-X must also be left blank. If there is a zero in a field on the Form 1040 or 1040-SR, then the corresponding field on the Form 1040-X must also contain a zero.

Is direct deposit available for Tax Year 2019 for electronically filed Form 1040-X?

Direct deposits are available for Tax Year 2019 electronically filed Forms 1040 or 1040-SR Amended Returns.

Can a Form 8888 Allocation of Refund (Including Savings Bond Purchases) be filed with an Amended Return?

Page 2 of the Form 8888 Instructions states “Don’t attach Form 8888 to Form 1040-X. A refund on an amended return can’t be directly deposited to an account or used to buy savings bonds.”

Where do I mail a paper check for an electronic Amended Return and should I use a Form 1040-V Payment Voucher?

A Form 1040-V Payment Voucher should be used when mailing a paper check for payment made on an electronically filed Amended Return. Please use Form 1040-V instructions which provides the mailing address for sending paper checks.

How can I check on the status of my electronic filed Amended Return?

If you file your amended return electronically, you can use the “Where’s My Amended Return?” online tool to check the status of your amended return.

How soon will the Where’s My Amended Return application be updated for checking the status of an electronically filed Amended Return?

Filers can check the status of a paper or electronically filed Form 1040-X Amended Return using the Where’s My Amended Return (WMAR) online tool or the toll-free telephone number 866-464-2050 three weeks after filing the return. Both tools are available in English and Spanish.

Can I get the status of an amended return for multiple tax years?

Where’s My Amended Return? can get you the status of the amended returns for the current tax year and up to three prior tax years.

What is happening when my amended return’s status shows as adjusted?

IRS has made an adjustment to your account. The adjustment will result in a refund, balance due, or in no tax change.

How often does the tool update?

Where’s My Amended Return? updates once a day, usually at night. You can check it daily.

It’s been longer than 16 weeks since you received my amended return, and it hasn’t been processed yet. Why?

Some amended returns take longer than 16 weeks for several reasons. Delays may occur when the return needs further review because it: Has errors Is incomplete Isn’t signed Is returned to you requesting more information Includes a Form 8379, Injured Spouse Allocation Is affected by identity theft or fraud Delays in processing also can happen when an amended return needs: Routing to a specialized area Clearance by the bankruptcy area within the IRS Review and approval by a revenue office Review of an appeal or a requested reconsideration of an IRS decision IRS will contact the client whenever they need more information to process the amended return.

What types of amended returns can I find out about using the tool?

You can find out about amended returns mailed to the IRS processing operations. Form 1040X, Amended U.S. Individual Income Tax Return tells you where you need to mail your return. Where’s My Amended Return? cannot give you the status of the following returns or claims: Carryback applications and claims Injured spouse claims A Form 1040, U.S. Individual Income Tax Return marked as an amended or corrected return (not a Form 1040X, Amended U.S. Individual Income Tax Return) An amended return with a foreign address A business tax amended return An amended return processed by a specialized unit—such as our Examination Department or our Bankruptcy Department.

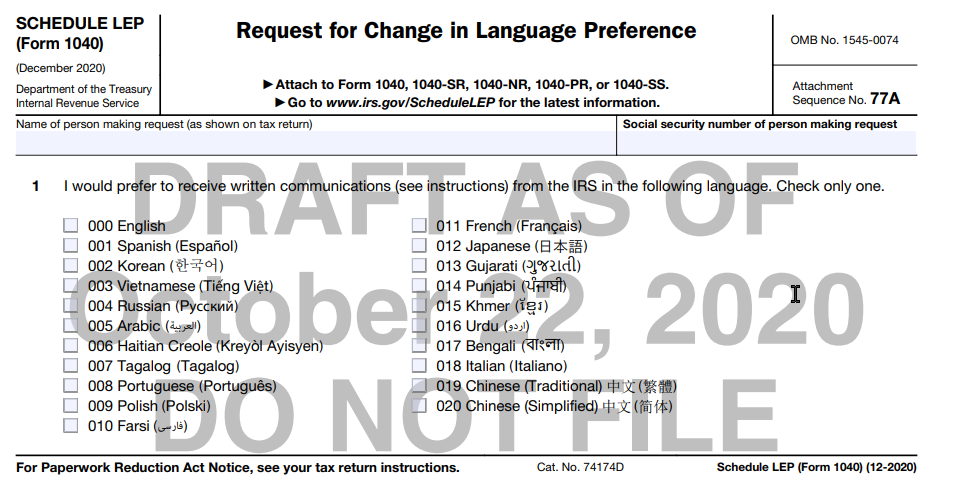

Issue 5: New Schedule LEP – Form 1040

Schedule LEP is a new form that allows taxpayers to state a preference to receive written communications from the IRS in a language other than English.

Issue 6: Virtual Currency

If in 2020, the client engaged in a transaction involving virtual currency, we will need to address this question as posed on page 1 of the Form 1040.

- A transaction involving virtual currency includes:

- The receipt or transfer of virtual currency for free (without providing any consideration), including from an airdrop or hard fork.

- An exchange of virtual currency for goods or services.

- A sale of virtual currency; and

- An exchange of virtual currency for other property, including for another virtual currency.

A transaction involving virtual currency does not include the holding of virtual currency in a wallet or an account or the transfer of virtual currency from one wallet or an account owned or controlled to another that is owned and controlled by the individual. If the client disposes of any virtual currency that was held as a capital asset through a sale, exchange, or transfer, use Form 8949 to figure the capital gain or loss and report it on Schedule D Form 1040.

If the client receives virtual currency as compensation for services or disposed of any virtual currency that they held for sale to customers in a trade or business report the income as of the same type. For example, W-2 Wages or inventory or services on a Schedule C.

Issue 7: 2020 Form 990-T Exempt Organization Business Income Tax Return Changes

The Form 990-T is being revised for tax year 2020 to allow for e-filing in calendar year 2021 (reporting on tax year 2020), as required by the Taxpayer First Act. Revisions are also being made to improve its utility for reporting unrelated business taxable income consistent with the ‘siloing’ rules of §512(a)(6) as put in place by the Tax Cuts and Jobs Act.

The 2020 Form 990-T separates the tax computation (which will be on Form 990-T) from reporting of separate unrelated trades or businesses, which will be on as many Schedules A (Form 990-T) as the organization needs.

Issue 8: IRS Payment Arrangements Easier to Set Up – IR 2020-248

The IRS assessed its collection activities to see how it could apply relief for taxpayers who owe but are struggling financially because of the pandemic, expanding taxpayer options for making payments and alternatives to resolve balances owed.

Taxpayers who owe always had options to seek help through payment plans and other tools from the IRS, but the new IRS Taxpayer Relief Initiative is expanding on those existing tools even more.

The revised COVID-related collection procedures will be helpful to taxpayers, especially those who have a record of filing their returns and paying their taxes on time. Among the highlights of the Taxpayer Relief Initiative:

- Taxpayers who qualify for a short-term payment plan option may now have up to 180 days to resolve their tax liabilities instead of 120 days.

- The IRS is offering flexibility for some taxpayers who are temporarily unable to meet the payment terms of an accepted Offer in Compromise.

- The IRS will automatically add certain new tax balances to existing Installment Agreements, for individual and out of business taxpayers. This taxpayer-friendly approach will occur instead of defaulting the agreement, which can complicate matters for those trying to pay their taxes.

- To reduce burden, certain qualified individual taxpayers who owe less than $250,000 may set up Installment Agreements without providing a financial statement or substantiation if their monthly payment proposal is sufficient.

- Some individual taxpayers who only owe for the 2019 tax year and who owe less than $250,000 may qualify to set up an Installment Agreement without a notice of federal tax lien filed by the IRS.

- Additionally, qualified taxpayers with existing Direct Debit Installment Agreements may now be able to use the Online Payment Agreement system to propose lower monthly payment amounts and change their payment due dates.

The IRS offers options for short-term and long-term payment plans, including Installment Agreements via the Online Payment Agreement (OPA) system. In general, this service is available to individuals who owe $50,000 or less in combined income tax, penalties and interest or businesses that owe $25,000 or less combined that have filed all tax returns. The short-term payment plans are now able to be extended from 120 to 180 days for certain taxpayers.

Installment Agreement options are available for taxpayers who cannot full pay their balance but can pay their balance over time. The IRS expanded Installment Agreement options to remove the requirement for financial statements and substantiation in more circumstances for balances owed up to $250,000 if the monthly payment proposal is sufficient. The IRS also modified Installment Agreement procedures to further limit requirements for Federal Tax Lien determinations for some taxpayers who only owe for tax year 2019.

In addition to payment plans and Installment Agreements, the IRS offers additional tools to assist taxpayers who owe taxes:

Temporarily Delaying Collection — Taxpayers can contact the IRS to request a temporary delay of the collection process. If the IRS determines a taxpayer is unable to pay, it may delay collection until the taxpayer’s financial condition improves.

Relief from Penalties — The IRS is highlighting reasonable cause assistance available for taxpayers with failure to file, pay and deposit penalties. First-time penalty abatement relief is also available for the first time a taxpayer is subject to one or more of these tax penalties.

Other requests, including this new relief, can be made by contacting the number on the taxpayer’s notice or responding in writing. However, to request relief, the IRS reminds taxpayers they must be responsive when they receive a balance due notice.

Issue 9: Form W-2 Reporting of Employee Social Security Tax Deferred Under Notice 2020-65

On August 8, 2020, a Presidential Memorandum was issued, directing the Secretary of the Treasury to use his authority pursuant to § 7508A to defer the withholding, deposit, and payment of certain payroll tax obligations.

In response to the Presidential Memorandum, Treasury and the IRS issued Notice 2020-65 on August 28, 2020. The Notice allows employers the option to defer the employee portion of Social Security tax from September 1, 2020 through December 31, 2020, for eligible employees who earn less than $4,000 per bi-weekly pay period (or the equivalent threshold amount with respect to other pay periods) on a pay period-by-pay period basis.

To pay the deferred amount of the employee portion of Social Security tax, the employer will ratably withhold the amount of Social Security tax deferred from the employees’ paychecks from January 1, 2021 through April 30, 2021.

If you deferred the employee portion of Social Security tax under Notice 2020-65, when reporting total Social Security wages paid to an employee on Form W-2, Wage and Tax Statement, include any wages for which you deferred withholding and payment of employee Social Security tax in box 3 (Social security wages) and/or box 7 (Social security tips).

However, do not include in box 4 (Social security tax withheld) any amount of deferred employee Social Security tax that has not been withheld. Employee Social Security tax deferred in 2020 under Notice 2020-65 that is withheld in 2021 and not reported on the 2020 Form W-2 should be reported in box 4 (Social security tax withheld) on Form W-2c, Corrected Wage and Tax Statement.

On Form W-2c, employers should enter tax year 2020 in box c and adjust the amount previously reported in box 4 (Social security tax withheld) of the Form W-2 to include the deferred amounts that were withheld in 2021.

All Forms W-2c should be filed with SSA, along with Form W-3c, Transmittal of Corrected Wage and Tax Statements, as soon as possible after you have finished withholding the deferred amounts. Review the 2021 General Instructions for Forms W-2 and W-3 (to be published in January 2021) for more information about completing and filing Forms W-2c and Forms W-3c. Forms W-2c should also be furnished to employees, and you may direct your employees to (or otherwise provide to them) the Instructions for Employees, below, for instructions specific to this correction.

Similarly, when reporting total Railroad Retirement Tax Act (RRTA) compensation include any compensation for which you deferred withholding and payment of the employee Social Security tax equivalent of Tier 1 RRTA tax under Notice 2020-65 in box 14 of the 2020 Form W-2, Wage and Tax Statement.

However, do not include in box 14 any amount of deferred employee Tier 1 RRTA tax that has not been withheld. Employee RRTA tax deferred in 2020 under Notice 2020-65 that is withheld in 2021 and not reported on the 2020 Form W-2 should be reported in box 14 on Form W-2c for 2020.

On Form W-2c, employers should adjust the amount previously reported as Tier 1 tax in box 14 of the Form W-2 to include the deferred amounts that were withheld in 2021. Review the 2021 General Instructions for Forms W-2 and W-3 (to be published in January 2021) for more information about completing and filing Forms W-2c and Form W-3c, Transmittal of Corrected Wage and Tax Statements. Employee copies of Forms W-2c should be furnished to employees, and you may direct your employees to (or otherwise provide to them) the Instructions for Employees, below, for instructions specific to this correction.

Instructions for Employees

If you had only one employer during 2020 and your Form W-2c, Corrected Wages and Tax Statement, for 2020 only shows a correction to box 4 (or to box 14 for employees who pay RRTA tax) to account for employee Social Security (or Tier 1 RRTA tax) that was deferred in 2020 and withheld in 2021 pursuant to Notice 2020-65, no further steps are required.

However, if you had two or more employers in 2020 and your Form W-2c for 2020 shows a correction to box 4 (or to box 14 for employees who pay RRTA tax) to account for employee Social Security (or Tier 1 RRTA tax) that was deferred in 2020 and withheld in 2021, you should use the amount of Social Security tax (or Tier 1 RRTA tax) withheld reported on the Form W-2c to determine whether you had excess Social Security tax (or Tier 1 RRTA tax) on wages (or compensation) paid in 2020.

If the corrected amount in box 4 of the Form W-2c for 2020 causes the total amount of employee Social Security tax (or equivalent portion of the Tier 1 RRTA tax) withheld by all of your employers to exceed the maximum amount ($8,537.40) of tax that you owe, or increases an already existing excess amount of employee Social Security tax (or Tier 1 RRTA tax withheld), then you should file Form 1040-X, Amended U.S. Individual Income Tax Return, to claim a credit for the excess Social Security tax (or Tier 1 RRTA tax) withheld. See the instructions to line 10 of Schedule 3 in the 2020 Instructions for Form 1040 and Form 1040-SR for more information.

Issue 10: Employment Coverage Thresholds Changes for 2021 – Social Security Administration

A coverage threshold is an amount of earnings that triggers coverage under the Social Security program. Earnings below the threshold are not taxable under Social Security nor do such earnings count toward future benefits.

For most wage earners, there is no coverage threshold; that is, every dollar of wages is covered and taxable. Federal law requires specific coverage thresholds for self-employed workers, farm workers, domestic employees, and election workers.

The thresholds for self-employed workers and farm workers are fixed amounts, but the thresholds for domestic employees and election workers change with changes in the national average wage index.

For 2021, the domestic employee coverage threshold amount is $2,300, and the coverage threshold amount for election officials and election workers is $2,000.

Issue 11: Form 8283 Changes – Noncash Charitable Contributions

Section B

- Under Section B, Part I, Information for Donated Property, there is a new checkbox for clothing and household items.

- Partial Interests and Restricted Property has been moved from Section A, Part II to Section B, Part II.

- Under Section B, Part IV, Declaration of Appraiser, there is a new line requiring the appraiser’s name, signature, title, and date.

Issue 12: Tax Court Suspends In-Person Acceptance of Hand-Delivered Documents

Effective Friday, October 30, 2020, and until further notice, the United States Tax Court will be suspending its in-person acceptance of hand-delivered documents. The Court will continue to receive mail and other deliveries, and taxpayers may comply with statutory deadlines for filing petitions or notices of appeal by timely mailing a petition or notice of appeal to the Court. The eAccess and eFiling systems remain operational.

If you have any questions, please contact the Public Affairs Office at (202) 521-3355.

Issue 13: Tax Court Updates Attorney Admission to Practice Application

Attorney applicants must, as a condition of being admitted to practice before the Court, complete an Application for Admission to Practice (available at www.ustaxcourt.gov). Review Rule 200, Tax Court Rules of Practice and Procedure.

A current (within 90 calendar days of the application filing date) certificate from the Clerk of the appropriate court, showing that the applicant has been admitted to practice before and is in good standing of the Bar of the Supreme Court of the United States, or the highest or appropriate court of any State or of the District of Columbia, or any commonwealth, territory, or possession of the United States must be submitted along with the application for admission. The

If an applicant fails to satisfy the requirements of Rule 200, Tax Court Rules of Practice and Procedure, the United States Tax Court may deny such applicant admission to practice before the United States Tax Court. The Tax Court Rules of Practice and Procedure are available at no cost in electronic format at www.ustaxcourt.gov.

To obtain a printed copy of the Tax Court Rules of Practice and Procedure, please submit an order and payment either by (1) using www.Pay.gov, through which payment can be made using specified credit cards, specified debit cards, or via electronic debit from a checking or savings account, or (2) mailing a check or money order for $20.00, payable to the Clerk, United States Tax Court and addressed to: Office of the Clerk, United States Tax Court, 400 Second Street, N.W., Room 111, Washington, D.C. 20217.

Submission of Application for Admission by Email An application for admission, along with an electronic version of a current original certificate of good standing, submitted by email must be sent for consideration to [email protected]. Electronically submitted documents containing original signatures, certifications, or seals must be maintained by applicants during the tenure of their Bar membership. Upon request by the Court, the filer must provide the original documents for review.

Prior to submitting the application, an applicant should pay the $50.00 admission fee through www.Pay.gov and attach to the emailed application a copy of the payment confirmation.

Submission of Application for Admission by Mail An application for admission, along with a current original certificate of good standing, submitted by mail must be accompanied by a check or money order for $50.00, payable to the Clerk, United States Tax Court, or proof of payment through www.Pay.gov, and sent for consideration to: United States Tax Court, Admissions Section, 400 Second Street, N.W., Washington, D.C. 20217.

Upon examination of your application papers and approval by the United States Tax Court, your name will be entered on the Roll of Practitioners of the Court, and your certificate will be inscribed and forwarded to you. You may also purchase a wall certificate, suitable for framing, for an additional payment of $15.00.

Issue 14: Draft Instructions for Forms 1094-B and 1095-B – Changes

Individual coverage health reimbursement arrangement (HRA).

For plan years beginning on or after January 1, 2020, employers may offer HRAs integrated with individual health insurance coverage or Medicare, subject to certain conditions (individual coverage HRAs). Generally, an HRA, including an individual coverage HRA, is a self-insured group health plan and, therefore, is an eligible employer-sponsored plan.

New type of coverage code.

A new code G must be entered on Form 1095-B, line 8 to identify an individual coverage HRA.

Extension of due date for furnishing statements.

The due date for furnishing Form 1095-B to individuals is extended from January 31, 2021, to March 2, 2021. See Notice 2020-76 and Extension of Time to Furnish Statement to Recipients, later.

Relief for failure to furnish statements.

The IRS will not impose a penalty for failure to furnish Form 1095-B to individuals if certain conditions are met. Review Notice 2020-76 and Information Reporting Penalties.

Extension of good faith relief for reporting and furnishing.

The IRS will not impose a penalty for reporting incorrect or incomplete information on the Forms 1095-B if you make a good faith effort to comply with the information reporting requirements. Review Notice 2020-76 and Information Reporting Penalties.

Similar Instructions for Forms 1094-C and 1095-C include the above information plus additional information you may want to review.

Issue 15: IRS Updates Operations During COVID – October 30, 2020

Processing Delays for Paper Tax Returns:

Taxpayers should file electronically through their tax preparer, tax software provider. IRS is experiencing delays in processing paper tax returns due to limited staffing. If you already filed a paper return, IRS will process it in the order received. Do not file a second tax return or contact the IRS about the status of the return.

Telephone Options:

Automated phone lines which handle most taxpayer calls – also remain available. All IRS toll-free phone lines supported by customer service representatives for both taxpayers and tax professionals are also available. However, callers should continue to expect long waits due to limited staffing. For Economic Impact Payment questions, call 800-919-9835.

Taxpayer Assistance Centers:

On Monday, June 29, 2020, the IRS began opening its Taxpayer Assistance Centers (TACs) to the public in phases. To ensure the safety of the public and employees, people seeking in-person assistance at a TAC will need to call 844-545-5640 to make an appointment. Appointments will be available if people need assistance for authentication of identity and document validation related to tax return filing or application for an Individual Taxpayer Identification Number; Sailing Clearances required for foreign travel by resident and non-resident aliens leaving the United States; assistance with Economic Impact Payment Issues; and cash payments.

For an up-to-date listing of TAC locations as they are opened, go to Contact Your Local IRS Office.

IRS Tax Forms:

The IRS’s National Distribution Center has reopened as of July 13, 2020 with reduced staffing. All previously submitted forms/publications requests are being processed as quickly as possible and as products become available. Please do not submit duplicate requests as this may cause further delays. New orders may be placed online at Order Forms & Publications. Taxpayers without access to the internet can call 800-829-3676 to request forms by mail.

IRS Working to Reduce CAF Backlog; Make Future Digital Improvements:

IRS is working hard to reduce the backlog of third-party authorizations. However, due to site closures relating to COVID-19 concerns, we currently are exceeding our five-business day target for approval. Our current time frame for authorization approval is approximately 15 business days. Please consider the additional approval time and plan accordingly. We request you do not submit duplicate authorizations as duplicate filings will only cause further delays. We expect to have full staffing in place soon and reduce the wait time.

Also, the IRS acknowledges the burden on taxpayers and the tax professional community to apply physical signatures to forms, especially during these unprecedented times. The IRS is working on a solution to provide for the acceptance of Forms 8821 and 2848 with electronic signature images by early 2021.

The IRS will continue to work on accepting digital transmissions of these forms in support of the Taxpayer First Act. IRS approves temporary use of e-signatures for certain forms: To protect the health of taxpayers and tax professionals, the IRS will temporarily allow the use of digital signatures on certain forms that cannot be filed electronically. The forms can be submitted with digital signatures if mailed by or on December 31, 2020.

The change will help to reduce in-person contact and lessen the risk to taxpayers and tax professionals during the COVID-19 pandemic, allowing both groups to work remotely to timely file forms. The IRS continues to review long-term actions involving digital signatures.

Taxpayer Correspondence:

Taxpayers who mail tax returns and other correspondence to the IRS during this period should expect to wait longer than usual for a response. While the IRS is receiving mail, our mail processing functions remain scaled back to comply with social distancing recommendations. The IRS’s ability to correspond with taxpayers about a variety of issues including requests for information needed to process a tax return remains limited.

As the phased-in resumption of operations have resumed, IRS is now working through its correspondence backlog.

Pending Check Payments and Payment Notices:

If a taxpayer mailed a check (either with or without a tax return), it may still be unopened in the backlog of mail the IRS is processing due to COVID-19. Any payments will be posted as the date we received them rather than the date the agency processed them. To avoid penalties and interest, taxpayers should not cancel their checks and should ensure funds continue to be available so the IRS can process them.

To provide fair and equitable treatment, the IRS is providing relief from bad check penalties for dishonored checks due to delayed processing. This relief is applicable for payments the agency received starting March 1 and may extend as late as December 31, 2020. However, interest and penalties may still apply. Due to high call volumes, the IRS suggests waiting to contact the agency about any unprocessed paper payments still pending.

Notice Mailings – Some Due Dates Extended to Help Taxpayers:

The IRS began mailing backlogged letters and notices to taxpayers in the agency’s steps to return to normal operations. Because of the COVID-19 shutdown, many of the notices were mailed with past due payment or response dates. To save time and costs, the IRS in most cases will not generate a new notice. Instead, the IRS will include Notice 1052, Important! You Have More Time to Make Your Payment, as an insert that will provide a new, updated pay or response date. Please read the insert carefully. It explains why the notice was delayed and, more importantly, provides a new date in which to pay or respond.

Below are key points recipients should note when the notice is received.

They should:

- Review the last page of the insert to determine if there is a new due date. Disregard the notices if steps have already been taken to resolve the issue.

- Contact the IRS using the number on the notice if they have additional questions. Keep in mind that phone lines remain extremely busy as the IRS resumes operations.

IRS to restart sending 500 series balance due notices:

The IRS began issuing the 500 series balance due notices to taxpayers in October. These notices were paused on May 9 due to COVID-19. Although the IRS continued to issue most agency notices, the 500 series were suspended temporarily because of a backlog of mail at the IRS due to COVID-19. The mail backlog is now caught up enough to account for the timely mailed payments. Some taxpayers will begin seeing in late October or early November, the updated 500 series notices with current issuance and payment dates. The 500 series includes three different types of notices that alert taxpayers about varying stages of nonpayment — the CP501, the CP503 and the CP504.

The CP501 notice alerts individual taxpayers that they still have a balance due and what their options are, while the CP503 alerts them that the IRS hasn’t heard from them and they may be subject to a lien if they don’t pay. The CP504 alerts taxpayers that they must pay their balances immediately or possibly face a levy of their state income tax refunds. These series of notices are generally sent to taxpayers if they don’t respond to or pay their initial notice and demand CP14. Taxpayers who are unable to pay are encouraged to consider available payment options as penalties and interest continue to accrue. Taxpayers who were impacted by the pandemic or other circumstances may qualify for relief from penalties due to reasonable cause if they made an effort to comply with the requirements of the law, but were unable to meet their tax obligations, due to facts and circumstances beyond their control. Taxpayers should call the toll-free number on their notice to request penalty relief due to reasonable cause if they feel they qualify and have the necessary supporting documentation.

Failure to deposit penalties on some employers claiming new tax credits:

The IRS is aware that a small population of employers that reduced their tax deposits in anticipation of claiming the sick and family leave credits, or employee retention credit, may have received a notice stating there was a failure to deposit penalty applicable to the Form 941 on which the credits were claimed.

Under Notice 2020-22, employers claiming the new tax credits may reduce their deposits throughout the tax period up to the amount of the credit. However, in reporting the schedule of liabilities on Form 941, the reported liabilities did not match the reduction in deposits for every pay date.

In these situations, they incurred a failure to deposit penalty on the difference in the reported liabilities and the reduced deposits (in situations where deposits were reduced by the amount of the anticipated credit(s) in excess of liability for the employer portion of social security for a given pay date).

Extended Due Dates:

The expired payment due dates printed on the notices were extended, as described in the insert. The new payment due date was either July 10, 2020, or July 15, 2020, depending upon the type of tax return and original due date. More than 20 million notices were mailed since early June with either the appropriate insert or with current dates.

Due to an error, affecting a fraction of these notices, about 11,000 notices were sent without the insert. Upon discovery, we immediately began reaching out to these taxpayers providing them with the appropriate information regarding the corrected due dates for a response to the notice and have updated our systems accordingly. All notices that were previously held as a result of the temporary closure of our facilities, have been mailed. As such, this should not be a reoccurring issue.

U.S. Residency Certification:

Normal operations are resuming. However, there is a backlog, and IRS is working hard to reduce the inventory.

Taxpayer Protection Program:

If you received correspondence (Letters 5071C, 5447C or 5747C) from the IRS asking if you filed a suspicious tax return, you may use the online Identity Verification Service to validate your identity. If you received a Letter 4883C, follow its instructions. Please note phone assistance is limited and wait times are lengthy.

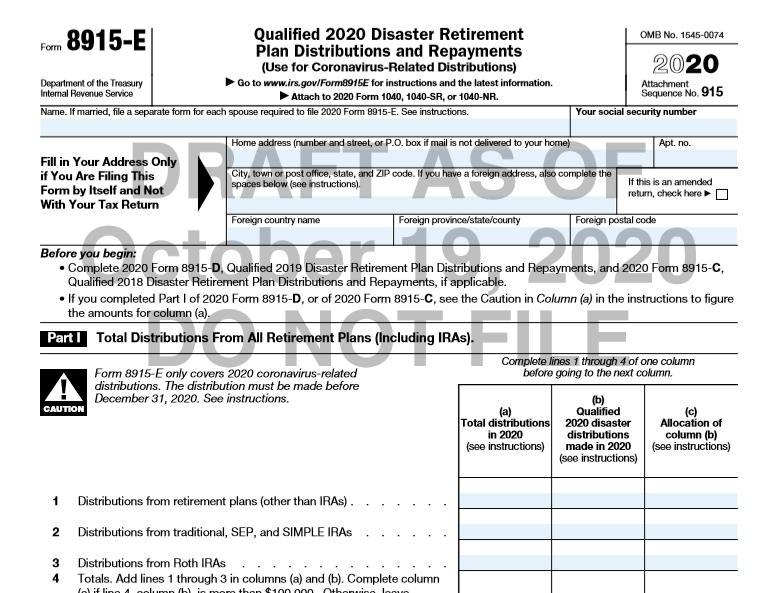

Issue 16: Draft of New Form 8915-E for Qualified 2020 Disaster Retirement Plan Distributions and Repayments (Use for Coronavirus-Related Distributions

Coronavirus-related distributions. The coronavirus is the only qualified 2020 disaster reportable on Form 8915-E. If you, your spouse, your dependent, or a member of your household was impacted by the coronavirus and you made withdrawals from your retirement plan in 2020 before December 31, you may have coronavirus-related distributions eligible for special tax benefits on Form 8915-E.

File 2020 Form 8915-E with the 2020 Form 1040, 1040-SR, or 1040-NR. If the client is not required to file an income tax return but are required to file Form 8915-E, fill in the address information on page 1 of Form 8915-E, sign the Form 8915-E, and send it to the Internal Revenue Service at the same time and place they would otherwise file Form 1040, 1040-SR, or 1040-NR.

The timing of the distributions and repayments will determine whether the client needs to file an amended return to claim them.

The form comes with separate instructions that should be reviewed carefully.

Issue 17: New Filing Addresses for Form 8857 Request for Innocent Spouse Relief

The filing addresses for Form 8857, Request for Innocent Spouse Relief (Rev. January 2014), have changed.

The new addresses are as follows.

If using the U.S. Postal Service:

Internal Revenue Service Center

7940 Kentucky Drive, Stop 840F

Florence, KY 41042

If using a private delivery service:

Internal Revenue Service Center

7940 Kentucky Drive, Stop 840F

Florence, KY 41042

Issue 18: IRS Will Issue Proposed Deduction Regulations for Passthrough Entities – Notice 2020-75

Treasury (Treasury Department) and the Internal Revenue Service (IRS) intend to issue proposed regulations to clarify that State and local income taxes imposed on and paid by a partnership or an S corporation on its income are allowed as a deduction by the partnership or S corporation in computing its non-separately stated taxable income or loss for the taxable year of payment.

Preview:

Forthcoming regulations. To achieve the purpose described in §3.01 of this notice, the Treasury Department and the IRS expect to propose regulations consistent with the provisions set forth below:

Definition of Specified Income Tax Payment

The term “Specified Income Tax Payment” means any amount paid by a partnership or an S corporation to a State, a political subdivision of a State, or the District of Columbia (Domestic Jurisdiction) to satisfy its liability for income taxes imposed by the Domestic Jurisdiction on the partnership or the S corporation. This definition does not include income taxes imposed by U.S. territories or their political subdivisions. Thus, this definition solely includes income taxes described in§164(b)(2) for which a deduction by a partnership is not disallowed under § 703(a)(2)(B), and such income taxes for which a deduction by an S corporation is not disallowed under §1363(b)(2).

For this purpose, a Specified Income Tax Payment includes any amount paid by a partnership or an S corporation to a Domestic Jurisdiction pursuant to a direct imposition of income tax by the Domestic Jurisdiction on the partnership or S corporation, without regard to whether the imposition of and liability for the income tax is the result of an election by the entity or whether the partners or shareholders receive a partial or full deduction, exclusion, credit, or other tax benefit that is based on their share of the amount paid by the partnership or S corporation to satisfy its income tax liability under the Domestic Jurisdiction’s tax law and which reduces the partners’ or shareholders’ own individual income tax liabilities under the Domestic Jurisdiction’s tax law.

Deductibility of Specified Income Tax Payments

If a partnership or an S corporation makes a Specified Income Tax Payment during a taxable year, the partnership or S corporation is allowed a deduction for the Specified Income Tax Payment in computing its taxable income for the taxable year in which the payment is made.

Specified Income Tax Payments not separately taken into account

Any Specified Income Tax Payment made by a partnership or an S corporation during a taxable year does not constitute an item of deduction that a partner or an S corporation shareholder takes into account separately under §702 or §1366 in determining the partner’s or S corporation shareholder’s own Federal income tax liability for the taxable year. Instead, Specified Income Tax Payments will be reflected in a partner’s or an S corporation shareholder’s distributive or pro-rata share of non-separately stated income or loss reported on a Schedule K-1 (or similar form).

Specified Income Tax Payments not taken into account for SALT deduction limitation

Any Specified Income Tax Payment made by a partnership or an S corporation is not taken into account in applying the SALT deduction limitation to any individual who is a partner in the partnership or a shareholder of the S corporation.

Issue 19: Guidance Issued When Applying for PPP Loan Forgiveness

For Borrowers Paycheck Protection Program (PPP) borrowers may be eligible for loan forgiveness if the funds were used for eligible payroll costs, payments on business mortgage interest payments, rent, or utilities during either the 8- or 24-week period after disbursement. A borrower can apply for forgiveness once it has used all loan proceeds for which the borrower is requesting forgiveness. Borrowers can apply for forgiveness any time up to the maturity date of the loan. If borrowers do not apply for forgiveness within 10 months after the last day of the covered period, then PPP loan payments are no longer deferred, and borrowers will begin making loan payments to their PPP lender.

How to Apply for Loan Forgiveness

- Contact your PPP Lender and complete the correct form

Your Lender can provide you with either the SBA Form 3508, SBA Form 3508EZ, SBA Form 3508S, or a Lender equivalent. The 3508EZ and the 3508S are shortened versions of the application for borrowers who meet specific requirements. Your Lender can provide further guidance on how to submit the application.

2. Compile your documentation Payroll (provide documentation for all payroll periods that overlapped with the Covered Period or the Alternative Payroll Covered Period):

- Bank account statements or third-party payroll service provider reports documenting the amount of cash compensation paid to employees.

- Tax forms (or equivalent third-party payroll service provider reports) for the periods that overlap with the Covered Period or the Alternative Payroll Covered Period:

- Payroll tax filings reported, or that will be reported, to the IRS (typically, Form 941); and

- State quarterly business and individual employee wage reporting and unemployment insurance tax filings reported, or that will be reported, to the relevant state.

- Payment receipts, cancelled checks, or account statements documenting the amount of any employer contributions to employee health insurance and retirement plans that the borrower included in the forgiveness amount.

Non-payroll (for expenses that were incurred or paid during the covered period and showing that obligations or services existed prior to February 15, 2020):

- Business mortgage interest payments: Copy of lender amortization schedule and receipts verifying payments, or lender account statements.

- Business rent or lease payments: Copy of current lease agreement and receipts or cancelled checks verifying eligible payments.

- Business utility payments: Copies of invoices and receipts, cancelled checks or account statements.

This list of documents required to be submitted to the Lender is not all-inclusive. Please refer to www.sba.gov/ppp for a complete list of requirements, instructions and forms.

3. Submit the forgiveness form and documentation to your PPP Lender

Complete your loan forgiveness application and submit it to your Lender with the required supporting documents and follow up with your Lender to submit additional documentation as requested. Consult your Lender for additional guidance and provide requested documentation in a timely manner.

4. Continue to communicate with your Lender throughout the process If SBA undertakes a loan review of your loan, your Lender will notify you of the review and the SBA loan review decision. You have the right to appeal certain SBA loan review decisions.

Your Lender is responsible for notifying you of the forgiveness amount paid by SBA and the date on which your first payment will be due, if applicable.

Please Note: If applicable, SBA will deduct any EIDL advance amount you have received from the forgiveness amount remitted to the Lender, as required by §1110(e)(6) of the CARES Act. Borrowers are required to retain certain documents for six years after the date the loan is forgiven or repaid in full. Questions?

Contact your PPP Lender or find more information at www.sba.gov/ppp

Issue 20: IRS Has Release Publication 1494, Tables for Figuring Amount Exempt from Levy on Wages, Salary, and Other Income (Forms 668-W(ACS) and 668-W(ICS)) for 2021

The tables can be found online at the irs.gov website

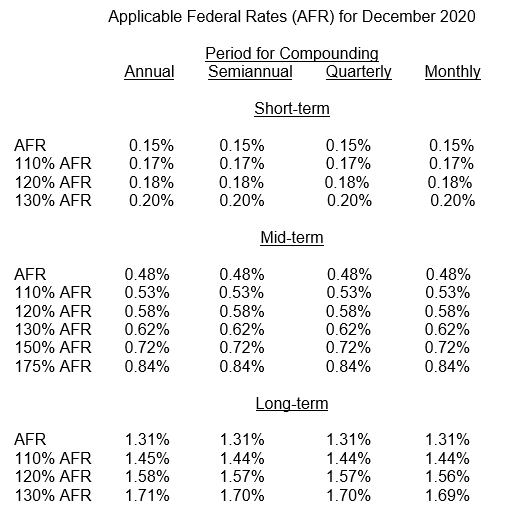

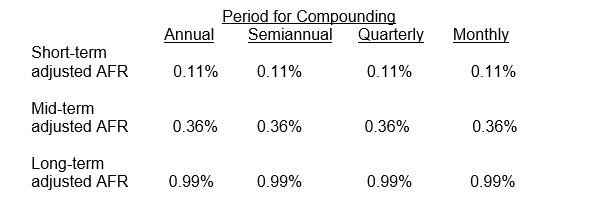

Issue 21: Applicable Federal Rates (AFR) for December 2020 – Rev. Rul. 2020-26

REV. RUL. 2020-26 TABLE 1

REV. RUL. 2020-26 TABLE 2

Adjusted AFR for December 2020

REV. RUL. 2020-26 TABLE 3

Rates Under Section 382 for December 2020

Adjusted federal long-term rate for the current month .99%

Long-term tax-exempt rate for ownership changes during the current month (the highest of the adjusted federal long-term rates for the current month and the prior two months.) .99%

REV. RUL. 2020-26 TABLE 4

Appropriate Percentages Under Section 42(b)(1) for December 2020 Note: Under section 42(b)(2), the applicable percentage for non-federally subsidized new buildings placed in service after July 30, 2008, shall not be less than 9%.

Appropriate percentage for the 70% present value low-income housing credit 7.20%

Appropriate percentage for the 30% present value low-income housing credit 3.09%

REV. RUL. 2020-26 TABLE 5

Rate Under §7520 for December 2020

Applicable federal rate for determining the present value of an annuity, an interest for life or a term of years, or a remainder or reversionary interest .6%